#Fintech Geek. Ranting @ fintechbrainfood.com - Views 100% my own

Joined January 2009

- Tweets 58,013

- Following 5,199

- Followers 69,580

- Likes 85,167

1,879 Photos and videos

Jun 13

We need sovereign AI.

Now.

@atitinstitute

Jun 13

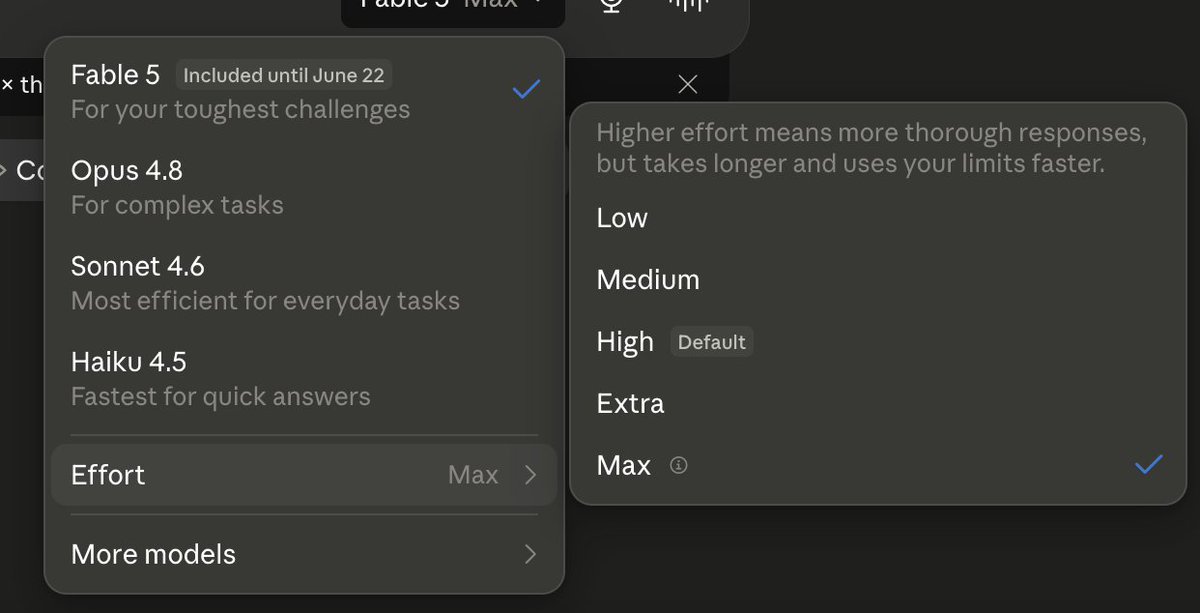

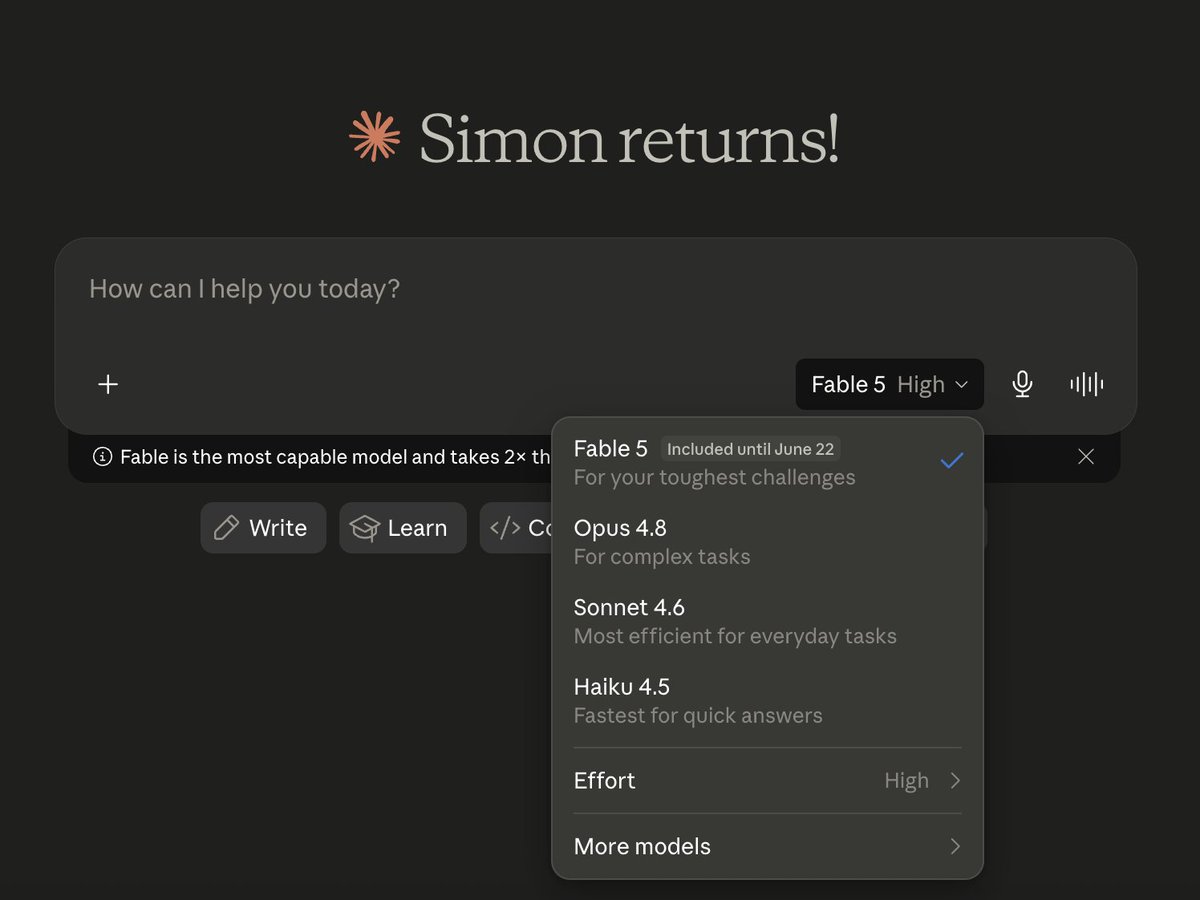

The US government, citing national security authorities, has issued an export control directive to suspend all access to Fable 5 and Mythos 5 by any foreign national, whether inside or outside the United States, including foreign national Anthropic employees.

The net effect of this order is that we must abruptly disable Fable 5 and Mythos 5 for all our customers to ensure compliance.

Access to all other Claude models is not affected.

We apologize for this disruption to our customers. We believe this is a misunderstanding and are working to restore access as soon as possible.

Read our full statement: anthropic.com/news/fable-myt…

5

1

20

2,533

Simon Taylor retweeted

Jun 12

Great discussion with @sytaylor, @nlevine19, and @wbpeck on stablecoins, tokenization, and the launch of @deel’s stablecoin: DLUSD.

Jun 12

Our guest for Monday's Tokenized Podcast

@sytaylor is joined by:

👉 @nlevine19, Partner, @a16z

👉 @thierryEdde44, Head of Crypto, @deel

👉 @wbpeck, Head of Digital Assets, @WisdomTreePrime

Out on Monday at 8am PT / 11am ET / 4pm GMT

Find it on 𝗔𝗽𝗽𝗹𝗲 𝗣𝗼𝗱𝗰𝗮𝘀𝘁𝘀, 𝗦𝗽𝗼𝘁𝗶𝗳𝘆 or 𝗬𝗼𝘂𝗧𝘂𝗯𝗲 by searching "Tokenized Podcast" 📷 💙

4

3

21

6,406

Jun 12

If you want a report that WASN'T hallucinated about real use cases

Start here.

fintechbrainfood.com/p/enter…

Jun 12

FT Exclusive: A KPMG report on how AI is being used by businesses across the world exaggerated adoption of the technology with bogus case studies that appear to have been based on AI hallucinations. ft.trib.al/z44Q3aR

1

1

6

3,735

Jun 12

The SEC moved to kill Rule 611, the 2005 rule that kept tokenized stocks offshore.

This is primarilt market structure story, but tokenization is noteworthy side effect.

Rule 611, the "trade-through" rule, made the national best bid and offer the legal default for US stock trade. (I.e.if there's a best price somewhere, its had to be honored)

It's also why on-chain equities couldn't trade onshore. An on-chain venue can't respect an order price that only lives on registered exchanges in market hours. They're non-compliant by default, or bolted onto the plumbing it was built to escape.

Strip out 611 and best execution falls back to FINRA Rule 5310, a broker-level duty rather than a routing mandate. A broker can meet a duty by routing to an on-chain venue.

Nearly all the tokenized equity trading today sits offshore. xStocks issues out of Jersey and Bermuda. Robinhood launched in the EU.

The on shore incumbents don't want to be caught flat footed. NASDAQ has approval to tokenize, NYSE is building a venue, DTCC starts tokenized trades in July.

611 existed because retail used to get filled at worse prices than were on offer.

With that rule gone, do we get something to replace it or does the consumer lose out?

4

6

18

2,074

Jun 12

🚨 JUST IN: Current just raised $80M at a $1.5B valuation.

In 2021, a16z valued it at $2.2B.

That's technically a down round. But current also the healthiest the business has been.

- 6m members

- 1/3rd of revenue from lending

- already has built a lot internally giving them strong unit economics

- 3x years of 70% growth

- crossing into profitability this year

---

Getting a large round in 2021 was easy for Fintech companies.

Making it to 2026 as a growing company that's on track for an IPO is a much harder slog that we should celebrate.

The new lead is Springcoast Partners, a growth equity firm taking a board seat.

Growth equity prices the cash flows. But this is a growing business...

---

Current is gearing up for more lending.

The company also expanded its financing partnership with Cross River and extended General Catalyst's Customer Value Fund commitment.

That's fuel for more growth.

---

This is the 2021 neobank class finishing its round trip.

Much of that cohort got acquired, wound down, or quietly stopped growing. The ones still standing look like Chime, now public on Nasdaq, and Current, crossing into profit. They took the valuation reset and got the hard stuff right on purpose.

6

2

44

5,557

Simon Taylor retweeted

Jun 11

🚨 Ep. 5 of Stablecoin Stories: KAST: 1M Users on a Stablecoin Neobank

With hosts:

💳 @sytaylor, Head of Market Development, @tempo

🔥 @rangoldi, SVP Payments, @FireblocksHQ

With guest: ⛓️ @raagulanpathy, Founder & CEO, @KASTxyz

In this episode, Sy, Ran and Raagulan discuss:

⛓️ Thesis of building fintech on top of stablecoin rails

❗️ Challenges of scrappy startup fundraising and low salaries

🤝 Early traction through Solana card partnership and trust

🏗️ Building USDK for onchain transparency and trust

🏛️ Plans for licenses acquisitions and raising more capital

🧠 Growth strategy using referrals cashback and better design

📈 Stablecoins will become 30-50% of payments in 20 years

***

Timestamps:

00:00 Introduction

7:35 Thesis of building fintech on top of stablecoin rails

9:53 Challenges of scrappy startup fundraising and low salaries

11:39 Early traction through Solana card partnership and trust

13:09 Building USDK for onchain transparency and trust

18:43 Plans for licenses acquisitions and raising more capital

22:47 Growth strategy using referrals cashback and better design

27:14 Stablecoins will become 30-50% of payments in 20 years

***

👉𝘚𝘦𝘢𝘳𝘤𝘩 '𝘛𝘰𝘬𝘦𝘯𝘪𝘻𝘦𝘥 𝘗𝘰𝘥𝘤𝘢𝘴𝘵' 𝘖𝘯 𝘠𝘰𝘶𝘛𝘶𝘣𝘦. 𝘈𝘱𝘱𝘭𝘦, 𝘚𝘱𝘰𝘵𝘪𝘧𝘺 𝘰𝘳 𝘢𝘯𝘺 𝘗𝘰𝘥𝘤𝘢𝘴𝘵 𝘗𝘭𝘢𝘺𝘦𝘳! 👈

4

8

28

5,790

Jun 11

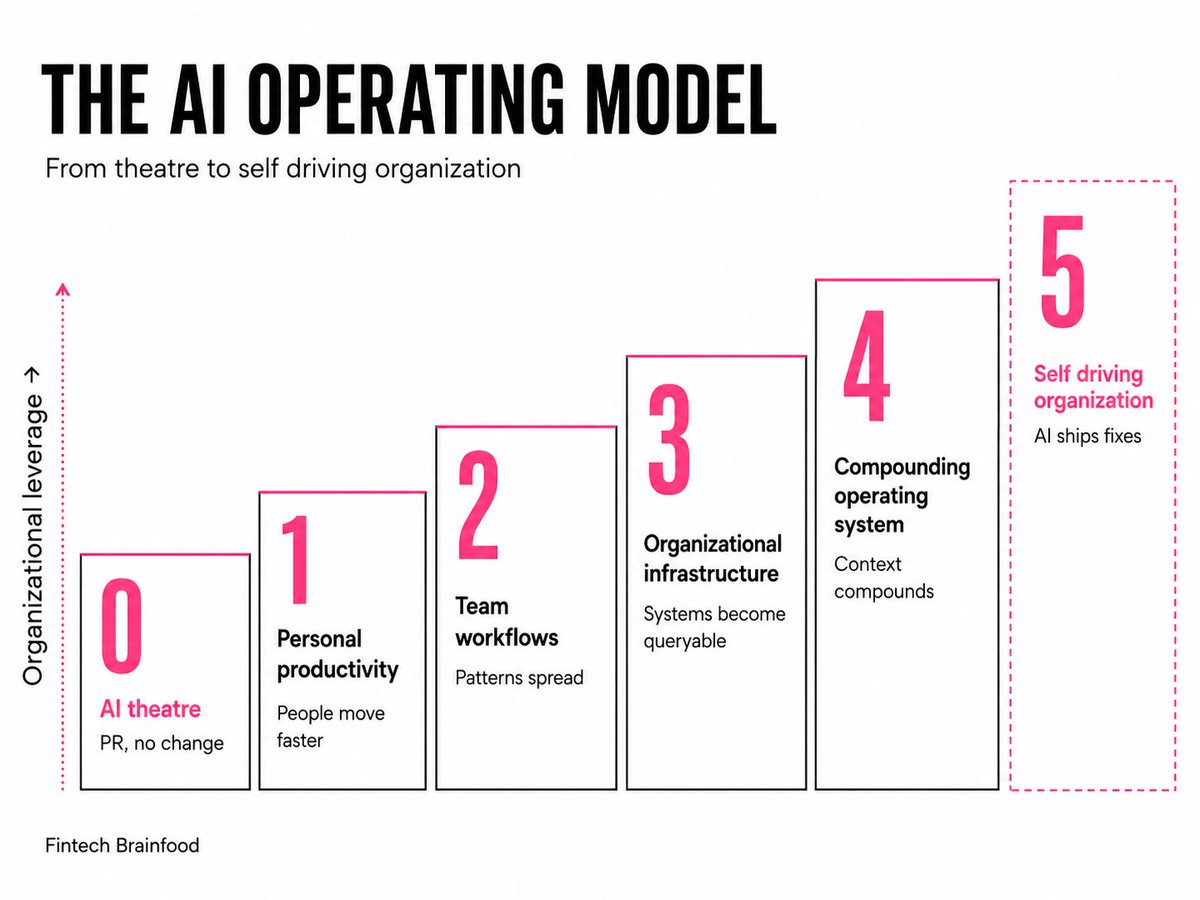

NBER asked nearly 6,000 executives about AI. 70% of firms use it.

Almost 9 in 10 say it's done nothing for productivity in three years.

After studying the companies beating that stat: @AnthropicAI, @tryramp, @AllicaBank and @bbva.

Here's what the exceptions do differently 🧵

2

2

9

3,920

Jun 11

The hardest thing to change is the operating model.

Tools are cheap and instant.

Org charts, incentives and cadence are slow and political.

That's why most companies aren't seeing AI productivity show up.

1

1

382

Jun 11

The full playbook is free for 30 days, then it goes into the archive.

fintechbrainfood.com/enterpr…

1

369

Simon Taylor retweeted

Jun 11

Fintechs are doing an amazing job bringing stablecoins to consumers and small businesses. The next big opportunity is for banks to do the same for their commercial and corporate customers 👇🏻

6

3

37

7,804

Jun 11

Truth

1

1

17

3,143

Simon Taylor retweeted

Jun 10

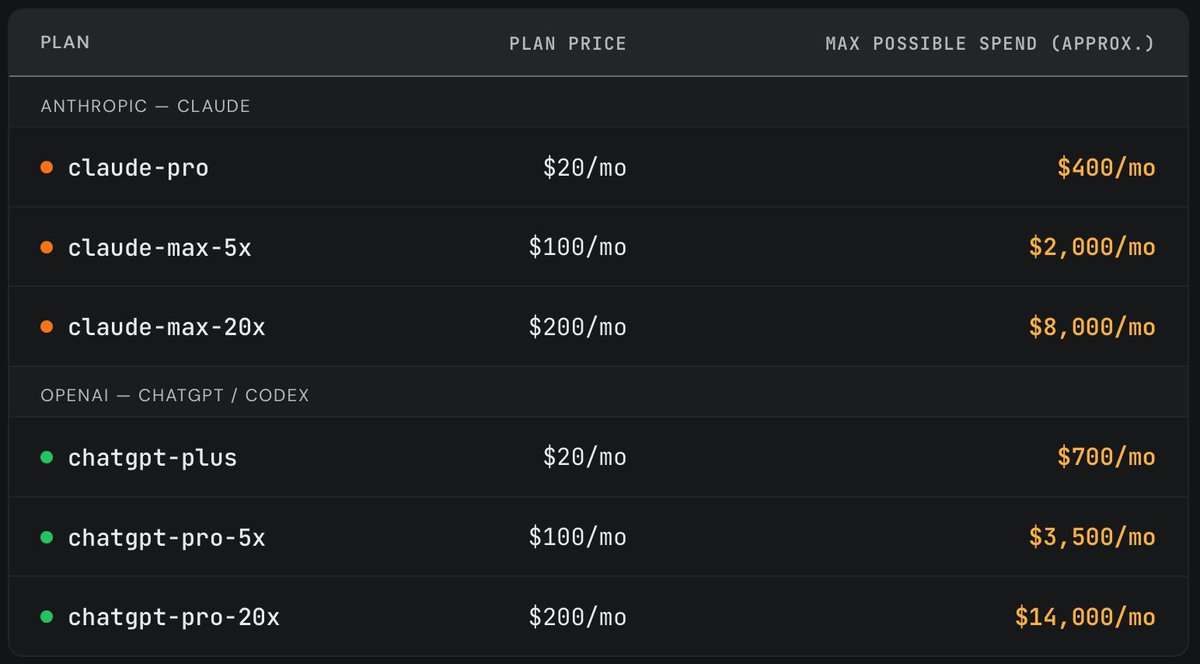

Recently, we purchased one of each Anthropic/OpenAI subscription plan and randomly ran long horizon coding tasks until we exhausted the weekly limit. It's widely believed that a $200/month plan maxes out at ~$2000/month worth of tokens (assuming API pricing). However, we found that the subscriptions are actually far more generous. (2/4)

182

571

6,021

3,444,423

Jun 11

.@Visa just gave AI agents their own card credentials. @OpenAI is partnering.

Agentic commerce has promised a lot, but delivered very little.

Is this finally agentic commerce's mainstream moment?

Announced yesterday at the Visa Payments Forum. The headline reads like "AI can shop for you now." The mechanic underneath is the interesting bit.

Start with tokenization.

It's the technology that takes your 16 digit card number and swaps it for a secure cryptographic token, so your real number never touches the merchant. That's what made Apple Pay work.

Visa Intelligent Commerce extends those tokens to agents.

Once an agent holds a token bound to it specifically, the agent has an identity on the Visa network. The same rails that already clear 300 billion transactions a year.

So when your agent goes to pay:

- Visa knows which agent is transacting

- The merchant knows it's a recognized, trusted agent operating under your rules

- Your bank can authorize in real time, against spending limits and approvals you set

Say your agent buys something and you tell your bank you never authorized it. With agent identity on the network, there's a record that it really was your agent, acting inside the guardrails you gave it. That changes agents from being a hostile "bot" to a trusted customer.

It also rhymes with every agent problem I keep running into. Autonomy only works when the system can prove what the agent did.

24

10

73

5,781