Exploring the world of web3 | @SoSoValueCrypto Researcher | signals are NFA | always DYOR

Joined December 2018

- Tweets 738

- Following 347

- Followers 249

- Likes 751

46 Photos and videos

Pinned Tweet

Feb 5

Grateful to be recognized by @SoSoValueCrypto

Wrote deeply on using SoSoValue as a compass to Detect True Projects, truly paid off

m.sosovalue.com/sososcholar/…

This award reinforces and encourages me to do more

Actively contributing more quality research

GSO to all researchers

Feb 5

1/ #SOSOSCHOLAR2025 Results are LIVE! 🏆🌊

Huge congrats to our 39 winners setting a new bar for crypto research. In a world of noise, you are the Lookouts, the first to find signals in the fog and provide the early warnings that guide us all.

📊 4,279 Submissions | 🌍 15 Regions | 💰 $33K Distributed (Upgraded from $30K!)

Quality wins. Check the leaderboard & research: scholar2025.sosovalue.com/

25

9

31

1,945

FadaTech_ retweeted

Jun 13

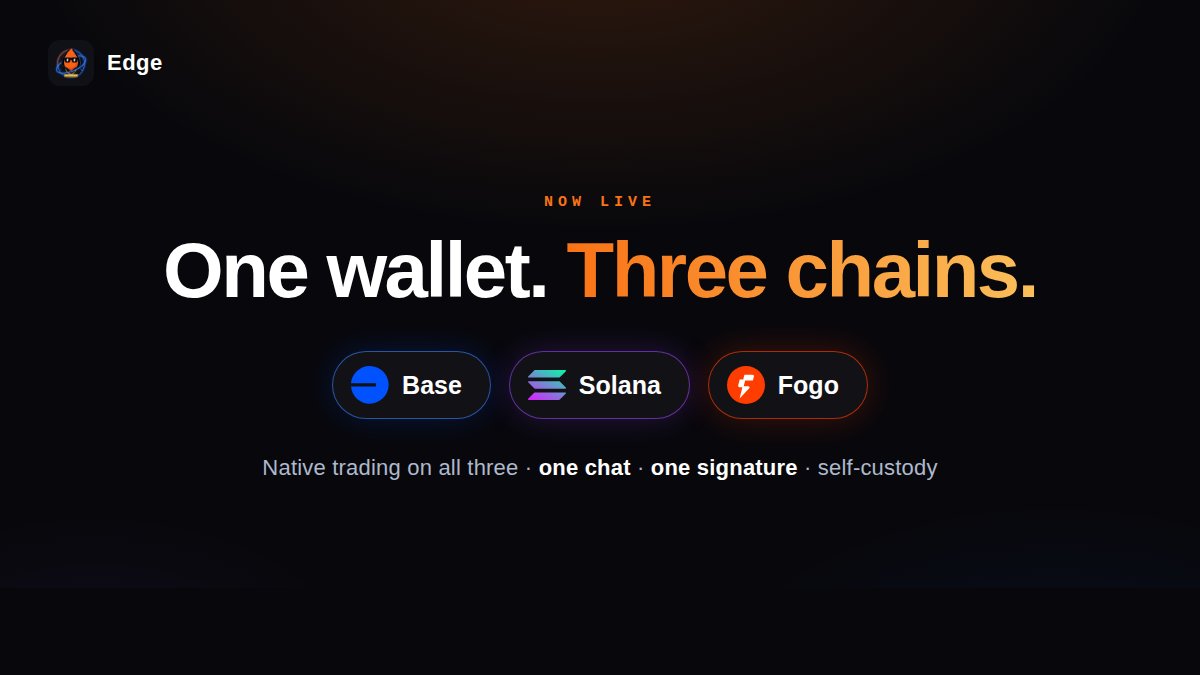

One wallet, Three chains more coming.

Edge now trades natively on Fogo, joining Base and Solana. All from one X login, All from chat.

Fogo is live inside Edge:

- Buy, sell, swap, and send $FOGO, stFOGO, iFOGO, iHUB, and USDC

- Routed through Valiant's concentrated-liquidity pools

- One signature, self-custody, no bridge, no new app, no seed phrase

Here is the part most people miss. Your Edge wallet already works on Fogo. It is the same address as your Solana wallet, so there is zero setup. Open Edge, type /fogo, done.

@Base. @Solana. @Fogo. One chat. Zero custody.

And every fee earned across all three chains flows back into $SMART. We are just getting started.

14

15

22

431

FadaTech_ retweeted

Jun 12

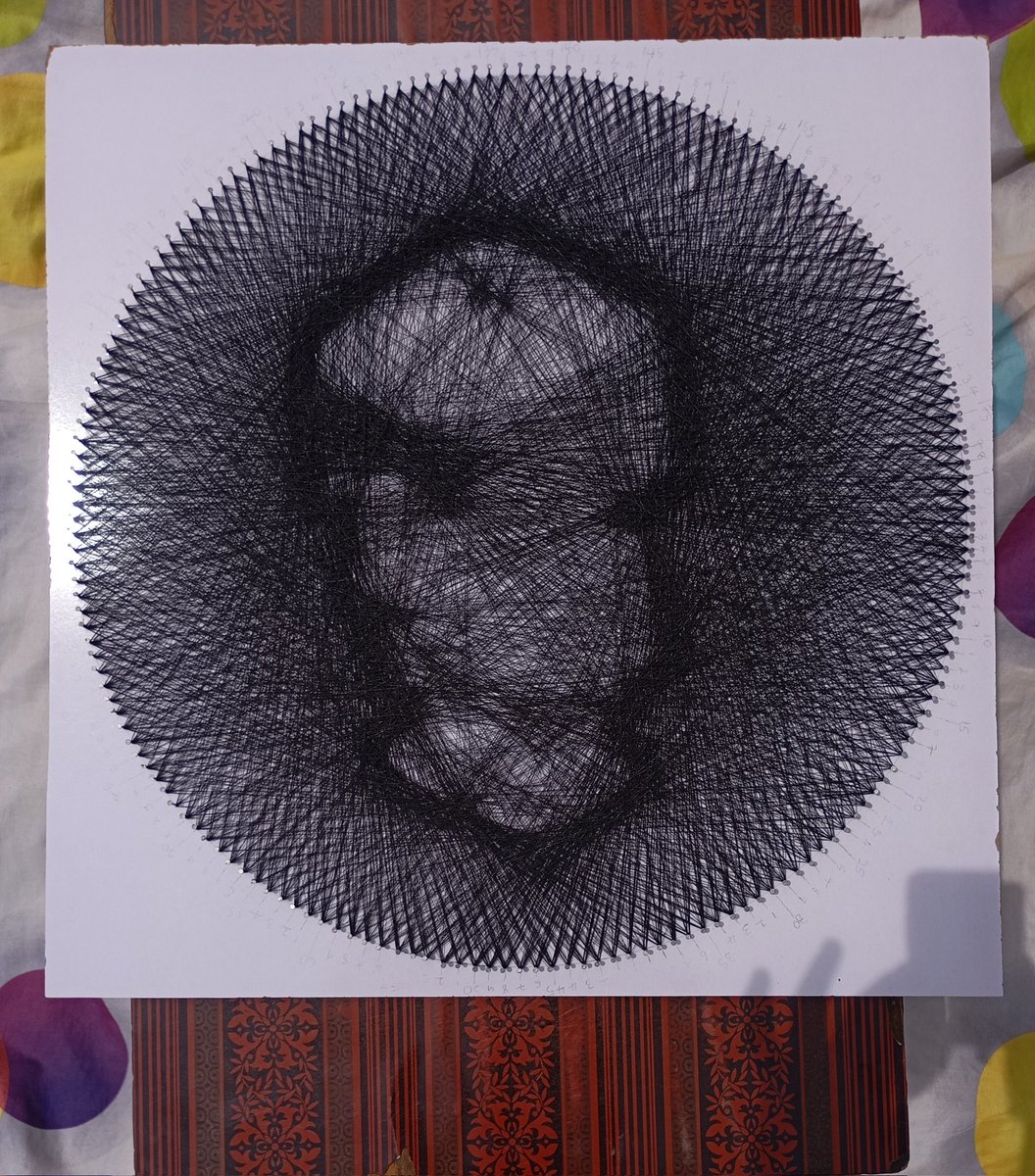

Handcrafted this string art masterpiece of the player avatar in Kintara game for @PlayKintara Meme Contest

Took hours of nails, string & pure dedication, just like the Kintara grind.

Used roughly 10 hours to bring this to life. (It's why I'm submitting late)

Please say something nice about the art, so it can go viral.

I honestly hope I win.🥺

Kintara Username: [Thefemog]

@fibonacki @LexaproTrader

48

15

50

542

Jun 12

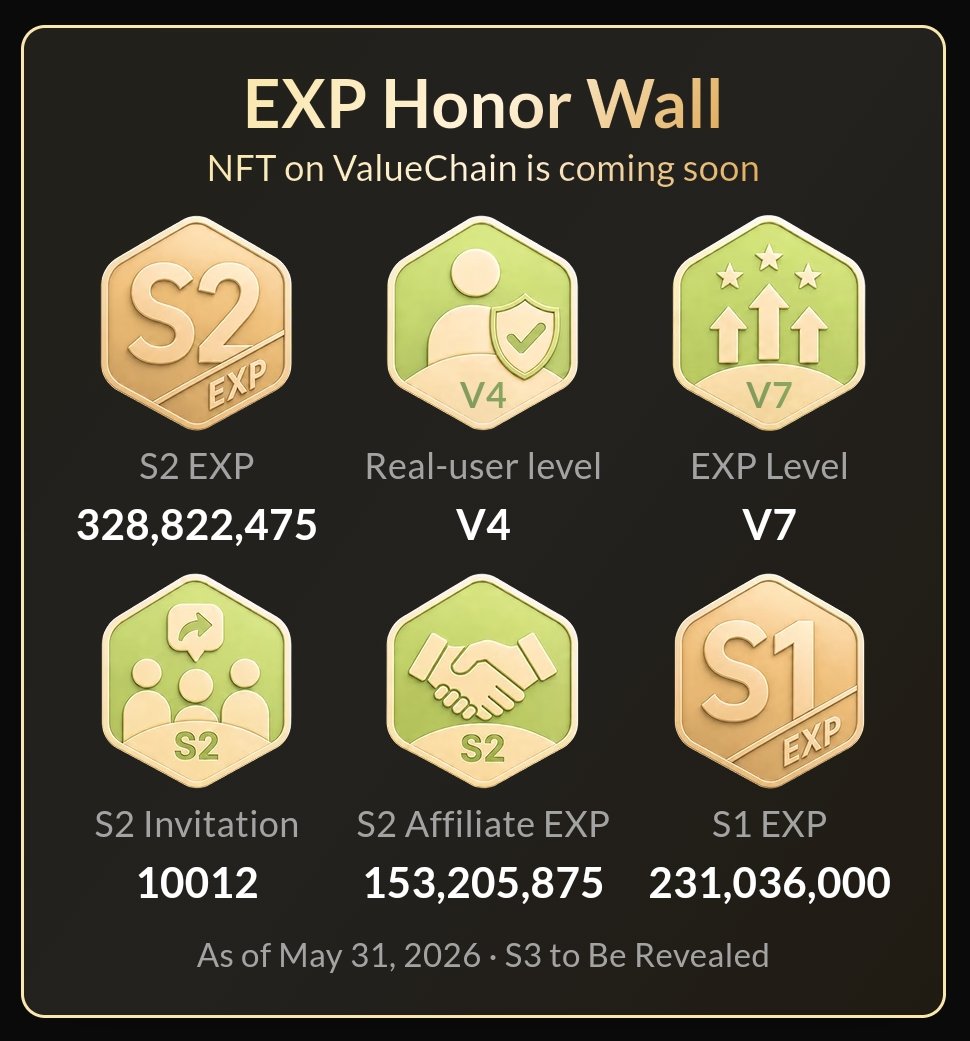

Update on EXP Season 2 Airdrop Checker EXP Season 2 has been an incredible journey!

Participation and data metrics have far blown past Season 1, and our team is currently running final checks on the full dataset.

Because we’re still processing a massive amount of data, the opening of Airdrop Checker (initially set for 12:00 UTC today) will need just a bit more time.

We are grinding hard to push this out and expect the page will go live within the next 8 hours.

Stay tuned @SoSoValueCrypto

1

1

37

Jun 11

WC26 Prediction

South Korea 2-1 Czech Republic

Confidence: 8/10

If I'm right, that's 30 points.

Tracking this prediction with @wc2026token

#WorldCup2026

2

85

Jun 11

This is the kind of lore that gets people invested before a single mint happens 👀

Worldbuilding > hype.

Would love to see more projects take this route, especially on community-first launchpads like GraveMint

Jun 4

Introduction: The Sovereigns

They don't race. They don't compete. They rule.

Long before the circuits were built and long before the first engines ignited, the Sovereigns established the laws that govern every track in the known Grid.

Hidden within forgotten sectors and unreachable networks, they observe every Racer, every victory, and every failure.

Most believe they are a myth.

A story told to new racerz.

1

111

FadaTech_ retweeted

Jun 11

Welcome to Grid Wars 🏁

The battle for grid supremacy starts now. Fill out the form and vote for your favorite community during this 48-hour event.

The Top 5 most active communities will advance to the next stage, where their members will have the opportunity to secure GTD spots for Round 2.

Choose your community. Cast your vote. Claim your place on the grid.

racerz.xyz/

355

895

2,144

84,972

FadaTech_ retweeted

Jun 11

🚨 21 HOURS LEFT — SoSoValue Season 2 Distribution Countdown ⏳🪂

The moment we’ve all been farming for is almost here.

Airdrop distribution allocation checker go live soon 🚀

89

34

307

8,886

FadaTech_ retweeted

Jun 11

Quote this with your favorite $OUTLIER art

outlier is for everyone

4

3

7

118

FadaTech_ retweeted

Jun 10

The market feels slow. The timeline feels quiet. The charts don’t look exciting.

But this is usually where the foundations for the next move are built.

The strongest participants aren’t the ones who show up when everything is green. They’re the ones who keep building, learning, and positioning when attention disappears.

Crypto moves in cycles.

Euphoria creates attention.

Correction creates opportunity.

Right now, liquidity is selective, narratives are rotating faster than ever, and conviction is being tested across the board. Projects without substance will fade. Builders with a long-term vision will keep shipping.

Instead of asking when the next rally starts, ask yourself:

• What am I building?

• What am I learning?

• What position am I creating for myself when sentiment returns?

Markets recover.

Narratives change.

Technology keeps moving forward.

The people who stay active during uncertainty are often the ones best positioned when momentum comes back.

Stay focused. Stay patient. Keep building.

The market may be bleeding today, but innovation never stopped

9

6

27

3,263

Jun 10

World Cup starts tomorrow! 🏆

Jun 10

World Cup starts tomorrow! 🏆

2

21

FadaTech_ retweeted

Jun 10

The 2026 Settlement Standard: Why Institutions Are Choosing Rails Now, and Why the Choice Is Final

In finance, architectural decisions are generational. Right now, a critical mass of banks, central banks, and tokenization platforms are converging on a settlement rail they will use for the next decade. This isn't a lab experiment. It’s an infrastructure lock in moment, and the window is closing in 2026. Here’s why.

*1. The 2026 Deadline Isn't Arbitrary, It’s Driven by Live Pilots Maturing into Mandates

The April 2026 GFMA report didn't just describe a wishlist it catalogued the final open items for institutional adoption: interbank tokenized deposit interoperability, transaction privacy standards, RTGS equivalent settlement, and digital money governance.

These aren't theoretical. JPMorgan’s Kinexys has already processed $1.5T on chain, DTCC is advancing SEC cleared tokenized U.S. Treasuries, and NYSE is building tokenized securities rails with BNY and Citi. The $29B tokenized RWA market is currently fragmented across proprietary platforms. The next 18 months will consolidate these live efforts into a single, regulated, interoperable rail. Institutions aren't planning they're deploying. And the first rail to satisfy all four GFMA requirements becomes the de facto standard.

2. Why First Mover Advantage Here Is Unlike Anything in Tech

In consumer apps, you can switch platforms in minutes. In settlement infrastructure, switching costs are structural:

*Operational, Rebuilding integrations with core banking, risk, and compliance systems takes 2,4 years.

*Regulatory, New rail = re-approval from prudential regulators, re audits, and re-attestation.

*Network dependent, You settle where your counterparties settle.

History shows this lock in is near permanent. SWIFT went from 239 to 11,000 banks because once critical mass was reached, joining was mandatory, leaving impossible. Visa scaled from a regional card network to global infrastructure on the same dynamic. The 2026 decision isn't about technology it's about which rail first achieves that critical mass of Tier 1 banks.

*3 The Network Math That Makes the Lead Uncatchable

With 10 institutions, there are 45 possible settlement corridors. With 100, there are 4,950. Each new participant doesn't just add volume it multiplies connection utility and raises the barrier for the next institution to choose a different rail. This is why winner take most , dynamics apply to settlement rails but not to consumer DeFi apps. In settlement, interoperability is the constraint, in DeFi, it’s optional.

*4. Where ZKsync Fits And Why Timing Matters

ZKsync isn't pitching a vision; it has live institutional deployments with regulated entities today. Its architecture directly addresses the GFMA’s open items: native account abstraction for interoperability, ZK proofs for audit-ready privacy, and instant finality for RTGS equivalent settlement.

But the 93% of tokenized U.S. assets currently on Ethereum raises a valid question: isn't this already decided? because that’s the asset layer. The 2026 decision is about the settlement layer the regulated, institutional rail that banks will use daily. It’s the difference between the internet (Ethereum) and the banking protocols that run on top of it (ZKsync et al.). The rail that wins the institutional settlement layer will absorb the $29B RWA market and the trillions that follow.

*Bottom line, For Heads of Settlement and CIOs, the question is no longer if or when. It’s which rail, and the cost of waiting 18 months isn’t delay it’s permanent lock in to a standard you didn’t choose. The first rail to interoperability at scale becomes the next decade’s plumbing. The rest become legacy before they even launch.

10

75

28

305