Helping investors navigate AI, Shifting World Order, and Energy Transition | Daily market wraps & our portfolio positioning at substack.com/@mintfinance

Joined June 2022

- Tweets 3,066

- Following 526

- Followers 232

- Likes 527

922 Photos and videos

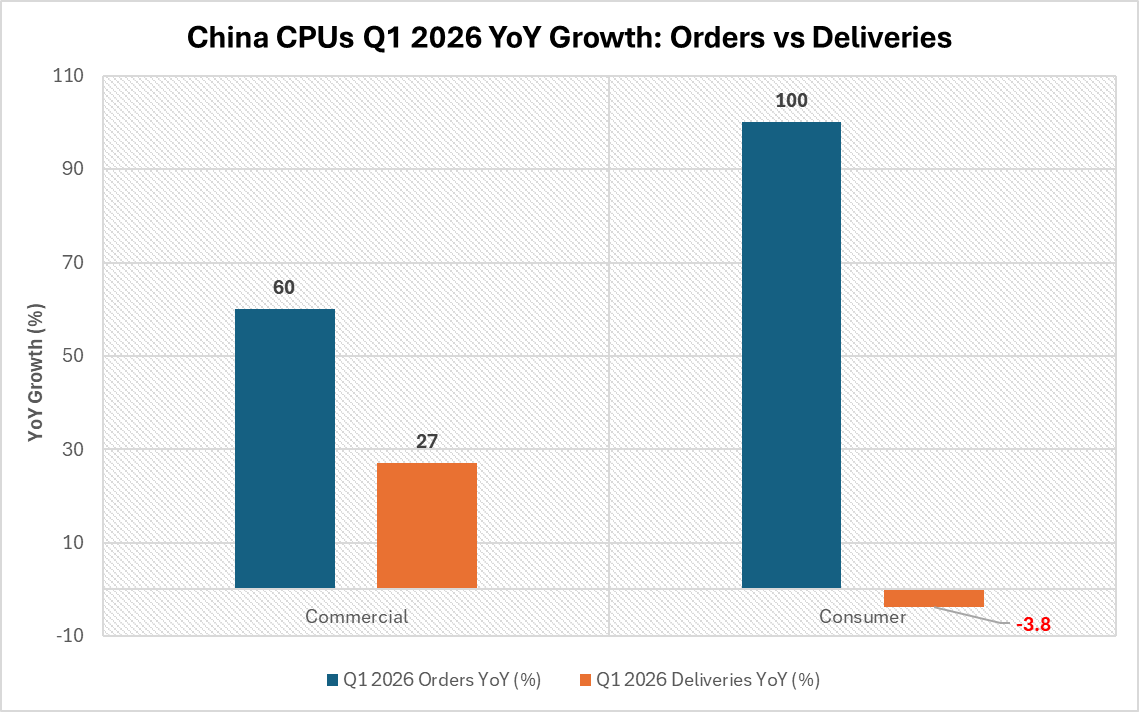

Apr 15

This China Q1 CPU data is wild.

One doesn't print a -4% delivery number on 100% order growth unless the fabs are running flat out.

$INTC and $AMD are actively starving the lower-margin consumer channel to prioritise commercial (and U.S.) volume.

$INTC reports on 23/Apr, and the beats (on margins too) should not come as a shock

1

3

179

Mar 28

You can see that tension starting to show up in the stock, $SOFTBY is still 42% below its Oct/2025 highs.

At the same time, subsidiary $ARM is moving into data-centre CPUs to further expand the former's AI ambitions. But shipments for that begin late this year as well!

Recurring revenue for that sits even further out, notwithstanding the x86 ( $INTC and $AMD) lock-in for enterprise!

Mar 28

$SOFTBY has now arranged a $40bn bridge loan to help fund the $30bn commitment made previously to #OpenAI.

This is meant to carry the group through an interim period where capital commitments are real, but cash flows are at a meaningful distance.

1

122

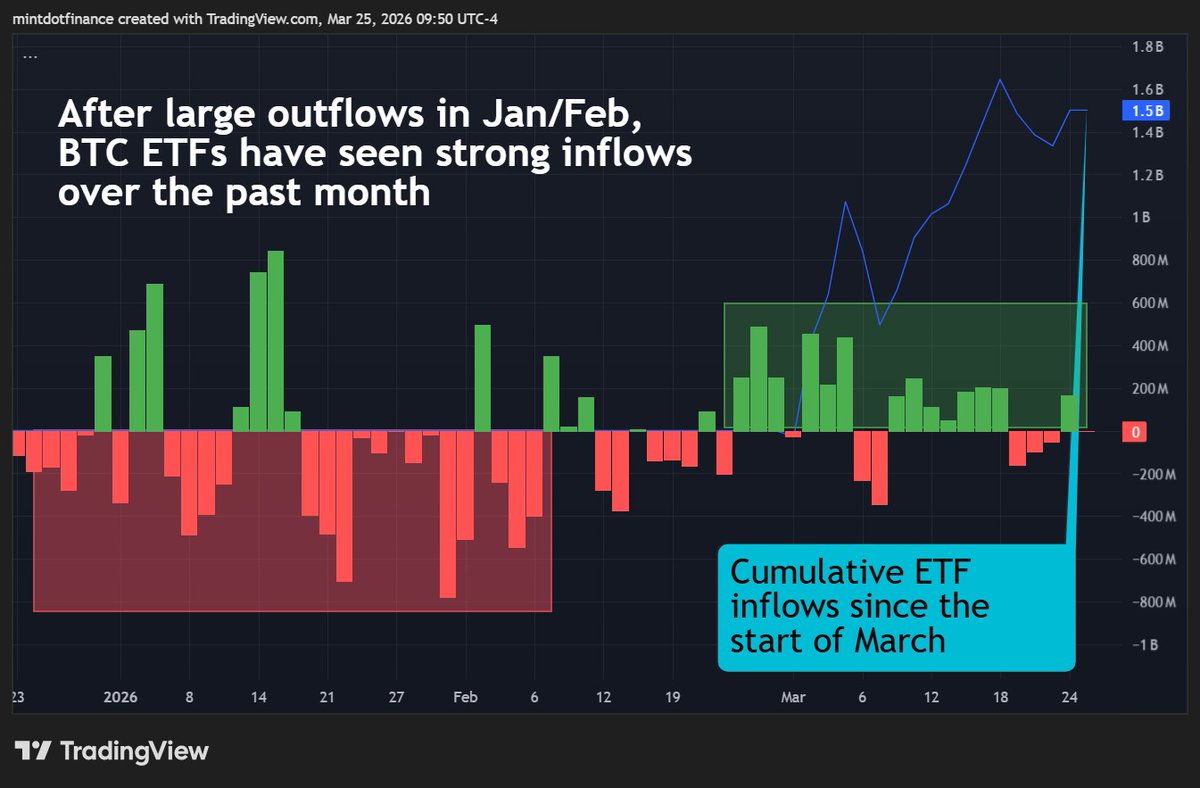

Mar 25

After getting drained through Jan/Feb, $BTC ETFs have flipped hard into inflows, touching $2.5B this month already.

Price hasn’t exploded, though, which is interesting and hints at a base-building phase for the coin.

If that thesis holds, this could start to resemble late-2023 conditions, where similar setups quietly built before price followed.

For a more detailed breakdown, we’ve put together a note, along with a historical trade set-up: tradingview.com/chart/MBT1!/…

4

58

Mar 23

x.com/dnystedt/status/203587…

Who’s willing to out-prioritise $NVDA at $TSM on leading-edge nodes?

An unexpected buyer at 1.6nm would say more about future bottlenecks than the rumour itself…

Also makes you wonder if external demand for $INTC 18A/AP is closer than we think.

Mar 23

Rumor: Nvidia plans to redesign its next-gen Feynman chips because there won’t be enough TSMC A16 capacity (1.6nm) to meet demand, media report, so Nvidia will use A16 only for the most critical dies, and shift others to TSMC’s N3P process instead (3nm). TSMC’s A16 capacity is expected to reach 20,000 wafers per month (wpm) by end-2027, and 40,000wpm in 2028. $TSM $NVDA #semiconductors #semiconductor news.cnyes.com/news/id/63919…

3

198

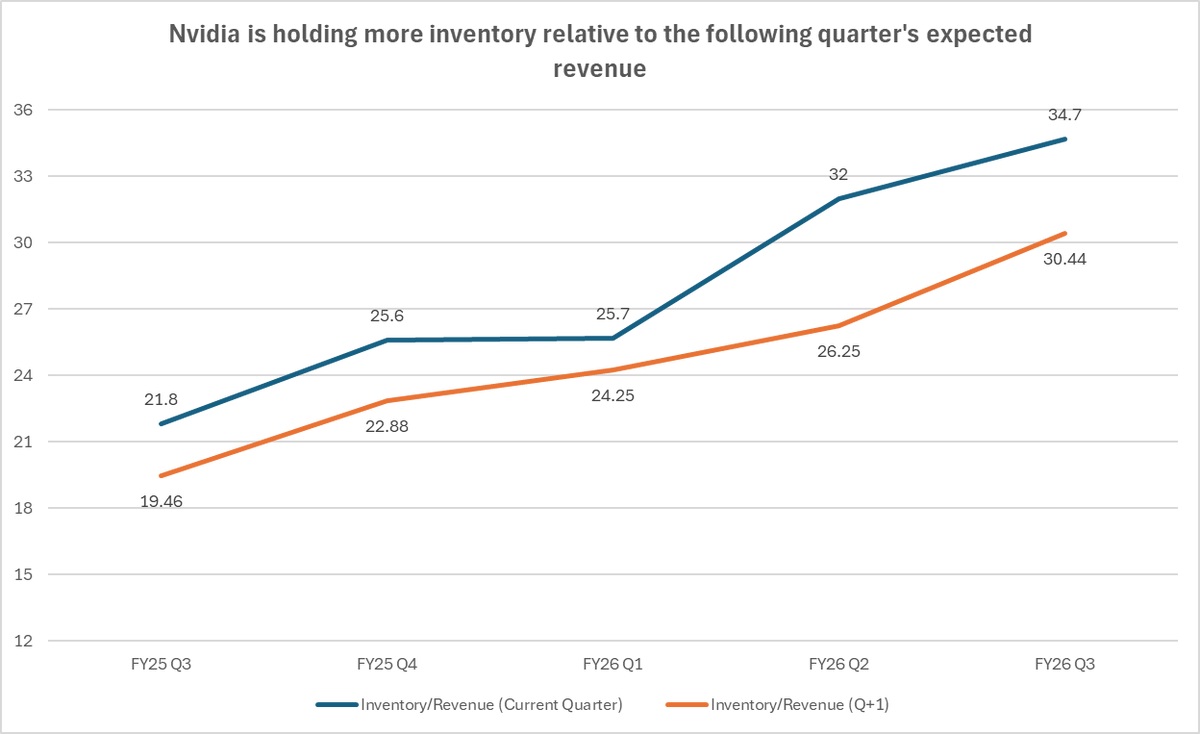

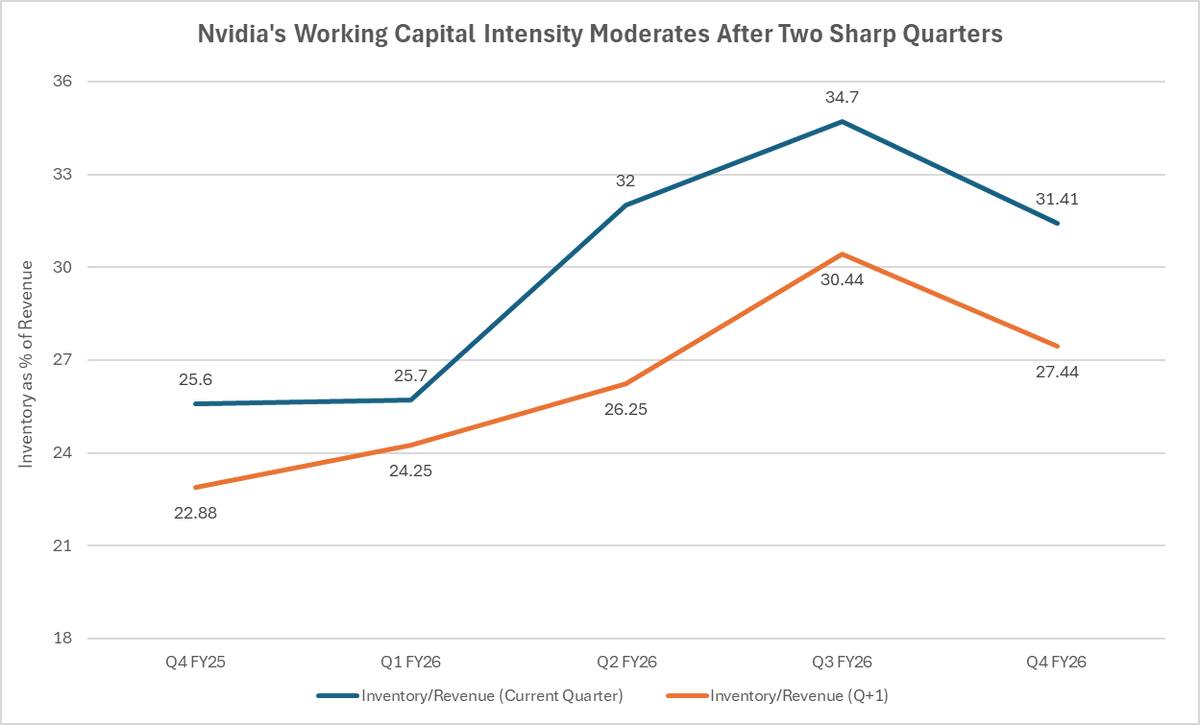

Feb 27

For reference, this is what the trends looked like over the past 5 quarters (excluding the most recent one).

$NVDA

Feb 27

Inventory growth at $NVDA slowed to 8% QoQ in Q4, down from 30% builds in the prior two quarters.

The sharp acceleration we saw through mid-FY26 has clearly cooled.

But if you look at the chart, inventory relative to revenue is still sitting well above FY25 levels after more than doubling through the year.

The slowdown suggests the heavy Blackwell ramp-driven build may be normalising, but the balance sheet is still carrying a much larger footprint than it did a year ago.

Overall, an improving sign still, and not so consistent with yesterday's meltdown!

3

155

Feb 27

Inventory growth at $NVDA slowed to 8% QoQ in Q4, down from 30% builds in the prior two quarters.

The sharp acceleration we saw through mid-FY26 has clearly cooled.

But if you look at the chart, inventory relative to revenue is still sitting well above FY25 levels after more than doubling through the year.

The slowdown suggests the heavy Blackwell ramp-driven build may be normalising, but the balance sheet is still carrying a much larger footprint than it did a year ago.

Overall, an improving sign still, and not so consistent with yesterday's meltdown!

3

265

Feb 25

$NVDA has convincingly outperformed infrastructure owners for the better part of a year.

We know that the economics of the AI buildout is increasingly shifting downstream toward physical capacity, power delivery, and integration.

That the real constraint has not been absolute compute for some time, but rather the path it must take toward deployments.

Having said that, markets are still pricing the value at the point of GPU shipment (also when Nvidia books its revenue).

But infrastructure players only monetise at activation; when the sites are powered, integrated, leased, and actually running.

Until that capacity is occupied and earning, infra remains exposed to financing timelines and execution risk; value to accrue downstream convincingly with clean deployment acceleration.

How do you think the power and cooling players like $VRT and $ETN are to fare along this buildout phase?

3

135

Feb 16

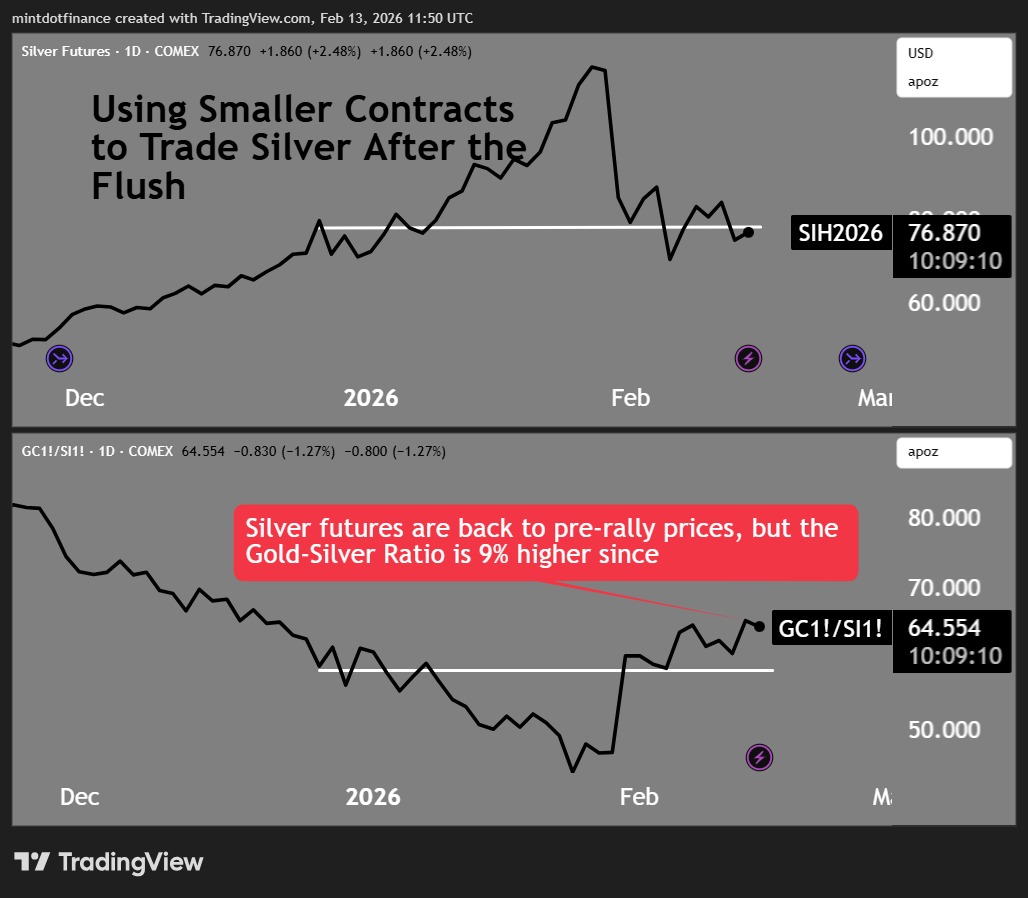

Silver Hasn't Lost its Structural Drivers but One Must Navigate the Reset.

As volatility spiked and margin requirements rose, leveraged positions were forced out. The move reflected capital constraints, while the underlying demand story remained intact. Now, with volatility compressing and positioning resetting, silver is entering a different phase.

📉 CVOL has returned to pre-rally levels

📦 Inventories remain tight across SHFE and COMEX

📊 Positioning has shifted back toward bullish exposure in front-month contracts

What’s different this time is how exposure can be managed.

CME’s new 100-ounce Silver futures contract arrives at a moment when margin sensitivity has become the dominant variable. Smaller contract sizing allows exposure to be rebuilt gradually, hedged more precisely, and adjusted without the capital intensity of standard 5,000-ounce contracts.

📄 Our latest note explores:

* Why the recent decline was driven by positioning, not fundamentals

* How volatility compression is reshaping the post-flush setup

* What inventory and positioning data signal about the next phase

* How smaller contracts can improve risk precision in volatile markets

tradingview.com/chart/SI1!/l…

#Silver #Commodities #Futures #PreciousMetals #CVOL #IV #CMEGroup #Options #GSR #AI

1

96

Feb 11

The Market Has Learned How to Absorb Nvidia

Since 2024, Nvidia’s post-earnings moves have been sharp and asymmetric. Upside has been steady, but when expectations wobble, the drawdowns tend to be fast and deep.

What’s interesting is what happens next.

In several recent quarters, Nvidia pulled back after earnings while the S&P 500 held up or even moved higher. That’s why we look at index-based hedging going into this print.

In this note, we break down:

> How Nvidia earnings have impacted the stock vs the index

> Why recent post-earnings weakness has looked more like rotation than risk-off

> How Micro E-mini S&P 500 futures and options can help absorb volatility around results

Single-stock options price in a lot of fear. Index exposure lets you hedge beta without paying peak IV.

The AI story is intact. The path around earnings is still narrow, and hedging the right risk matters.

tradingview.com/chart/MESH20…

#Nvidia #Earnings #Equities #SPX #CMEGroup #Derivatives #Futures #Options #AI #Markets

73

Feb 4

🚨 The yen is still dancing on a cliff edge. Position accordingly 🚨

At its Jan 23 policy meeting, the Bank of Japan held rates steady and struck a hawkish tone. But instead of strengthening, the yen dropped to a two-week low near 159.

Hours later, it suddenly snapped back to 154. The reason? A Fed spot rate check in New York that spooked FX desks into pricing in a possible coordinated intervention.

That alone pushed the yen to a 90-day high near 152.

📉 But with no follow-through, it’s already weakening again.

💬BoJ hawkishness isn’t changing the trade, and Dollar strength is back.

Our new note breaks down:

* Why dollar strength is the real headwind

* What history tells us about verbal threats vs actual FX intervention

* How traders and investors can protect yen-denominated exposure using CME JPY/USD futures

📊 Includes trade structuring insights via historical payoff examples from the 2024 July intervention window.

📄tradingview.com/chart/6J1!/Q…

#Yen #FX #BoJ #USDJPY #CMEGroup #Futures #Options #Forex #Intervention #Fed

1

68

Jan 28

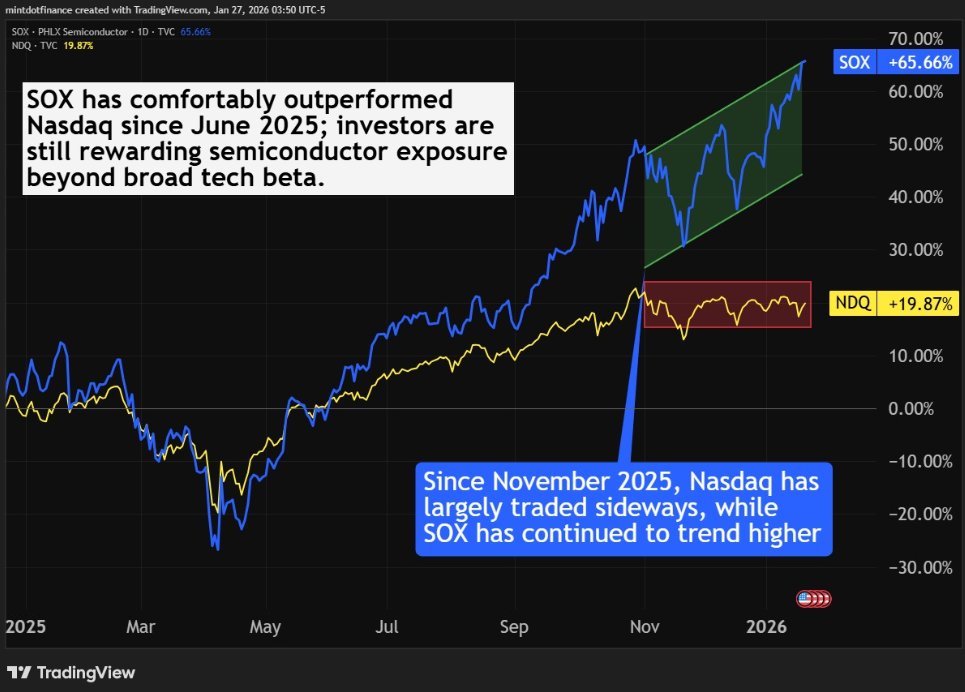

📈 Semiconductors are still running the show.

Since mid-2025, SOX has outpaced Nasdaq by over 45 percentage points.

And it’s not just AI accelerators anymore.

As the market broadens its focus to memory, packaging, and manufacturing leverage, semis remain at the core of the build-out.

Our latest note breaks down:

* Why SOX keeps leading in 2026

* What the market’s telling us about AI ROI vs buildout

* How to express that view using SOX futures

📎 Read the full breakdown on @tradingview

tradingview.com/chart/SOX/eE…

#Semiconductors #SOX #Volatility #Options #Macro #Equities #CMEGroup #CME

1

56

Jan 20

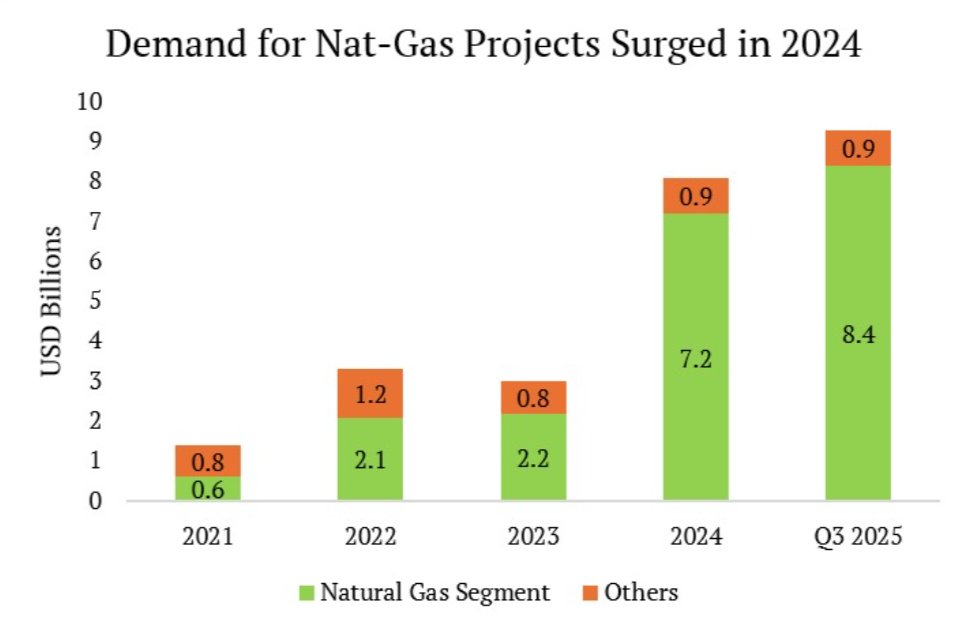

Kinder Morgan is increasingly leveraged to the LNG buildout, with its project backlog surging and now overwhelmingly focused on natural gas infrastructure serving LNG and power demand. This expanding order pipeline provides clear multi-year visibility. Backed by highly contracted cash flows, Kinder Morgan offers a durable way to participate in the next phase of U.S. LNG growth.

Read more @Smartkarma:

smartkarma.com/insights/chev…

To secure a 40% discount when accessing @Smartkarma content as a follower of @MintFinance, please click on this link below smartkarma.com/home/private-… and enter promo code SKAP40 when signing up.

#KinderMorgan #KMI #LNG #NaturalGas #USLNG #EnergyInfrastructure #Midstream #Pipeline #EnergyMarkets #PowerDemand #LNGExport #InfrastructureInvestment #EnergyTransition #CashFlows #Investing

1

75

Jan 16

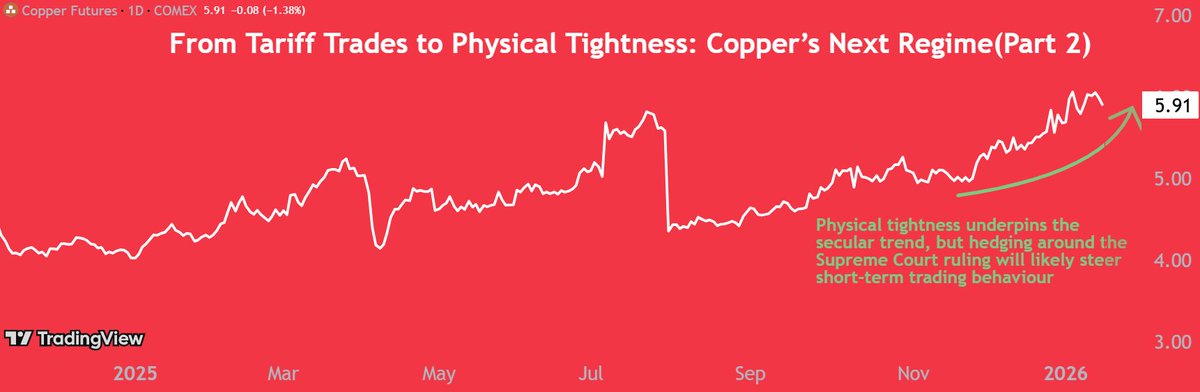

Copper is pricing in more than tariffs.

As we entered a decisive week, the copper market was coiled between two forces: a tight physical setup—and a binary legal risk that could reshape U.S. trade policy in a single ruling.

Volatility is already elevated. Positioning is actively hedged. And the choice of how to express a directional view has never mattered more.

The previous note hinged on the CME-LME spread to back going long Copper futures. In this second note, we break down:

1. What elevated CVOL is telling us about trader expectations

2. How open interest is clustering around key levels

3. Three tactical structures to express a copper view through the ruling window

Read the full piece here on @tradingview :

tradingview.com/chart/HG1!/l…

#Copper #Commodities #CME #Tariffs #Futures #Options #COMEX #Volatility #Metals #QuikStrike

1

51

Jan 15

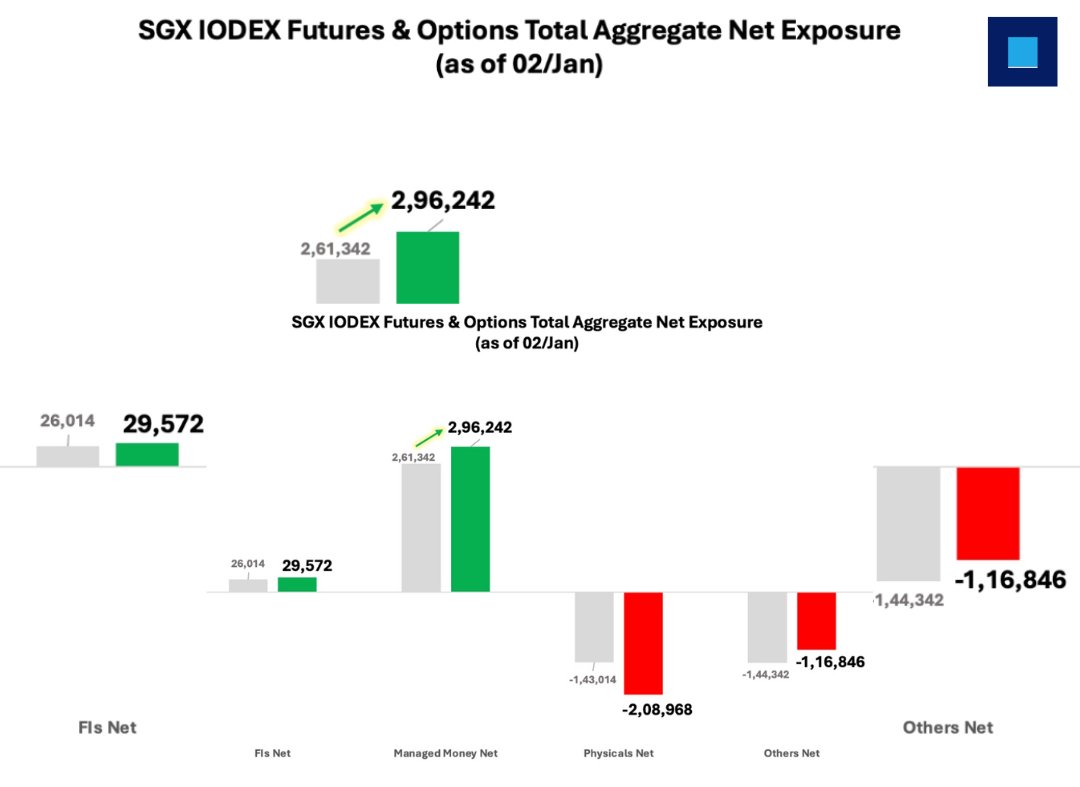

Iron Ore Update: Managed money participants increased their net long exposure during the week ended 02/Jan. Overall open interest dipped by 21.5% WoW.

To read the report in full, please go to @Smartkarma

smartkarma.com/insights/rest…

To secure a 40% discount when accessing @Smartkarma content as a follower of @finance_mint, please click on this link below smartkarma.com/home/private-… and enter promo code SKAP40 when signing up.

#IronOre #SGX #China #ManagedMoney #TacticalPositioning

1

41

Jan 14

Pre-Lunar New Year restocking is lending near-term support to iron ore, but the backdrop remains mixed. Rising arrivals and swollen port inventories keep a lid on sustained upside, keeping the risk-reward finely balanced.

To read the report in full, please go to @smartkarma

smartkarma.com/insights/rest…

To secure a 40% discount when accessing @smartkarma content as a follower of @finance_mint , please click on this link below smartkarma.com/home/private-… and enter promo code SKAP40 when signing up.

#IronOre #SGX #China #LunarNewYear #Restocking #Demand #Shipments #PortsideInventories

2

59

Jan 13

Chevron’s reported joint bid with Quantum for Lukoil’s international assets is less about scale and more about geopolitical positioning, aligning U.S. energy capital with Washington’s push to reassert control over strategic hydrocarbons. With Venezuela optionality and potential Lukoil assets, Chevron is emerging as the best-placed U.S. major to benefit from energy-driven foreign policy, even if the financial payoff is longer-dated.

Read more @Smartkarma:

smartkarma.com/insights/chev…

To secure a 40% discount when accessing @Smartkarma content as a follower of @MintFinance, please click on this link below smartkarma.com/home/private-… and enter promo code SKAP40 when signing up.

#Chevron #EnergyGeopolitics #OilAndGas #GlobalEnergy #USForeignPolicy #StrategicAssets #EnergySecurity #GeopoliticalRisk #EmergingMarkets #EnergyTransition #Upstream #OilMarkets #Hydrocarbons #GlobalPolitics #OOTT $CVX

1

143