All in on #biotech, #fintech, and #crypto! rss3.bio/0x9de5Fb2e8268…

Joined November 2020

- Tweets 12,685

- Following 1,319

- Followers 1,326

- Likes 14,320

1,204 Photos and videos

🤣 @meremrtl and i don't always agree. in fact, we tend to disagree. perhaps more folks on biox should be open to criticism and learn how to debate the facts, rather than resorting to name calling, making straw man arguments, or parroting talking points from 'popular' x accounts.

Jun 13

@meremrtl is on a mission now. He's getting all his buddies to post on $ABVX. @financebully, @ALLKAResearch just HAPPEN to show up after Stevie makes a fool of himself. He blocks everyone so he doesnt get "cyberbullied" and has his friends, or his burner accounts, start posting

3

7

1,721

Jun 12

context matters.

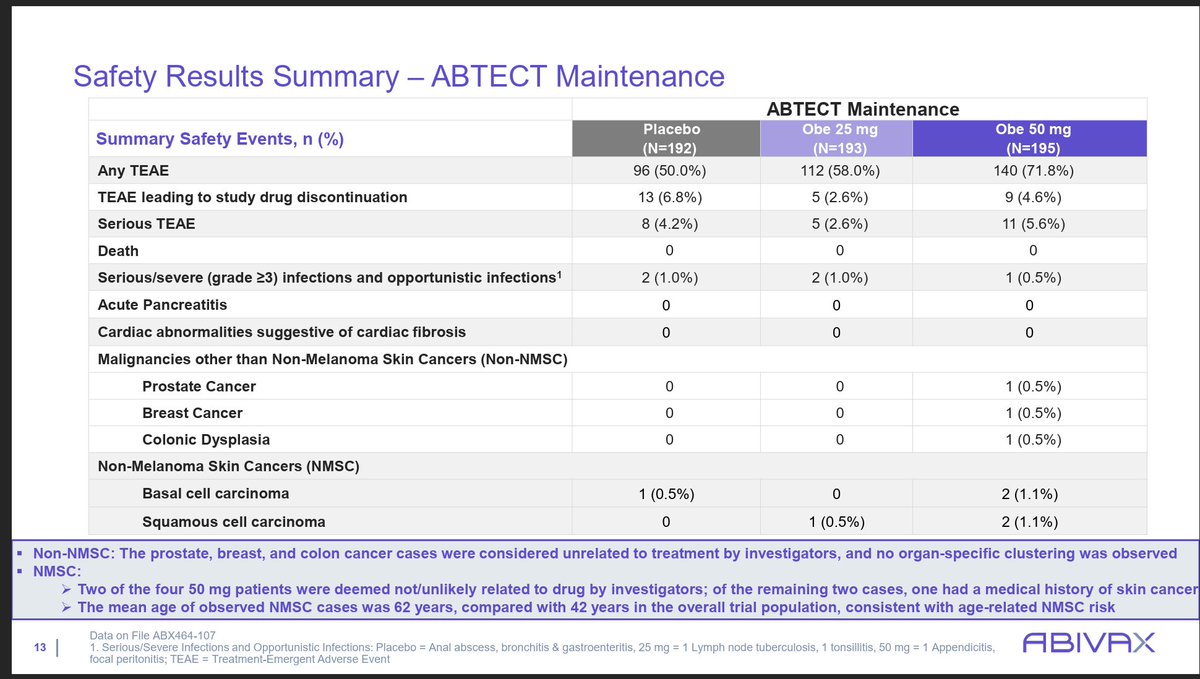

omvoh: 29 cases scattered across 2600 patients tracked over years (0.5% rate).

$abvx: 7 cases clustered in a single randomized treatment group of 195 patients over a 44-week window, while the structurally identical low-dose group had 1 case.

Jun 12

$ABVX

Now that you have details from Abivax for each patient, see how 23 non-NMSC and 6 NMSC cases were reviewed for omvoh resulting in conclusion that not induced by the drug as the rate was still within the background rate for UC patients. Also, FDA review below.

4

13

9,907

Jun 12

$abvx investor, but let’s be objective. company considers high-risk anomalies for the 7 cancers, but baseline traits should be more uniform. why wouldn't cases distribute evenly across arms? m&a strategics will catch the 7:1 ratio & colonic dysplasia hidden in footnotes.

unlike most on biox, i'm not blindly bullish on any stock, even ones i own and assets that i like. while i think $abvx obe efficacy is great, the malignancies will raise eyebrows among potential acquirers, given unknown moa. m&a value will likely dip below original assumption.

12

14

10,172

Jun 11

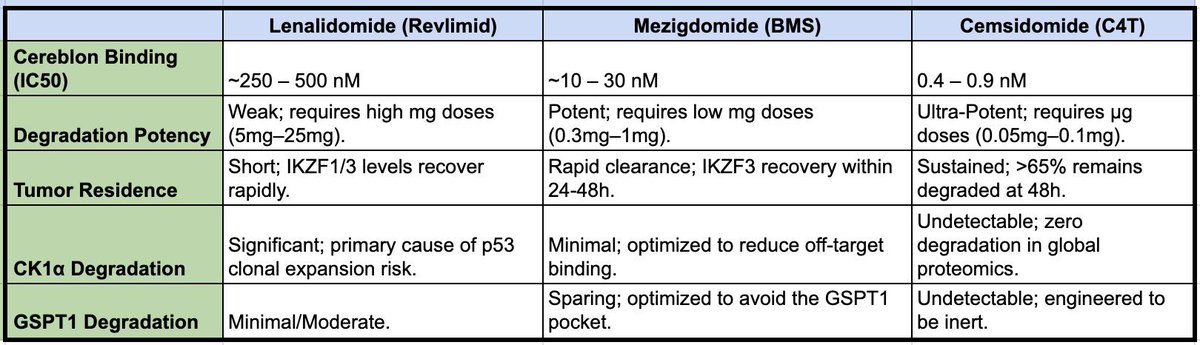

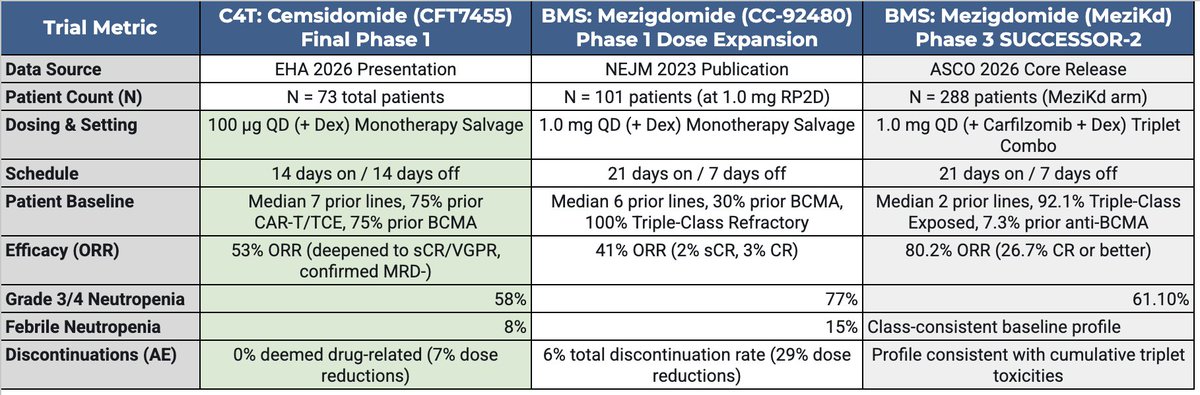

$cccc eha data validates a best-in-class profile for cemsidomide. higher orr than mezigdomide (53% vs 41%) with 0% drug-related discontinuation rate. just like $tern '701 ($mrk), the asset quality makes this an obvious buyout target.

ir.c4therapeutics.com/news-r…

2

21

2,276

Jun 10

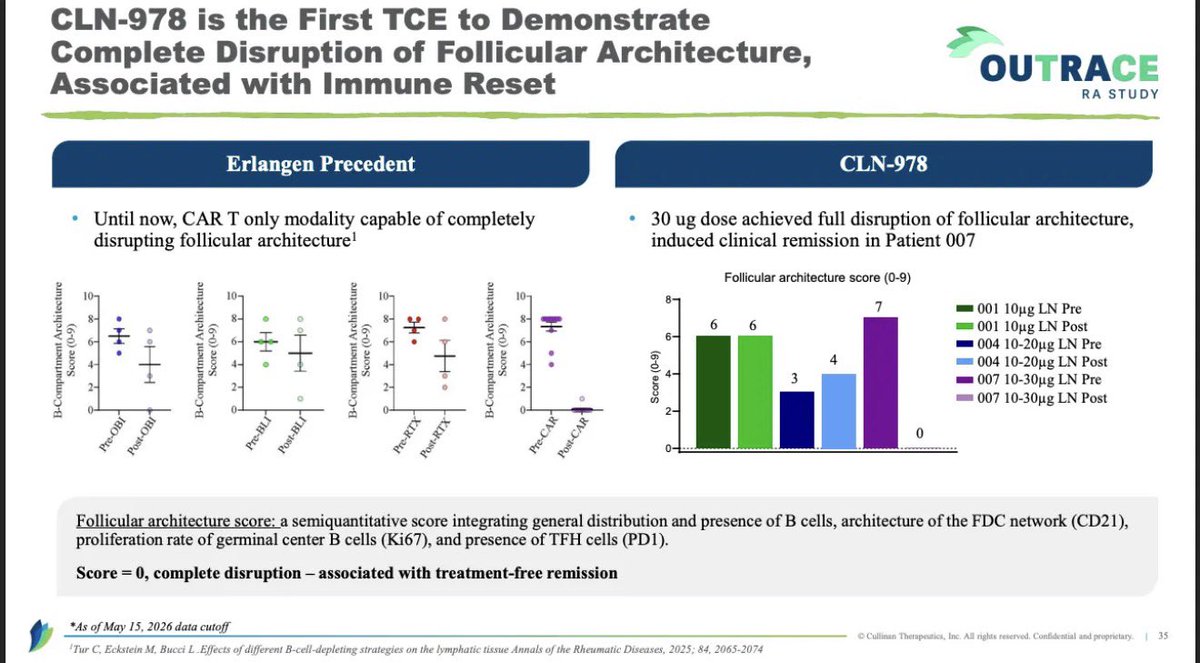

nice $cgem update this morning.

-cln-978 (cd19): multi-dose (no severe crs/icans). poly-refractory ra pt achieved clinical remission.

-velinotamig (bcma): 100% complete renal response (2/2 sle pts) by wk 8 with no crs/icans.

-fdmc: $1b / cash: $375m

investors.cullinantherapeuti…

Mar 24

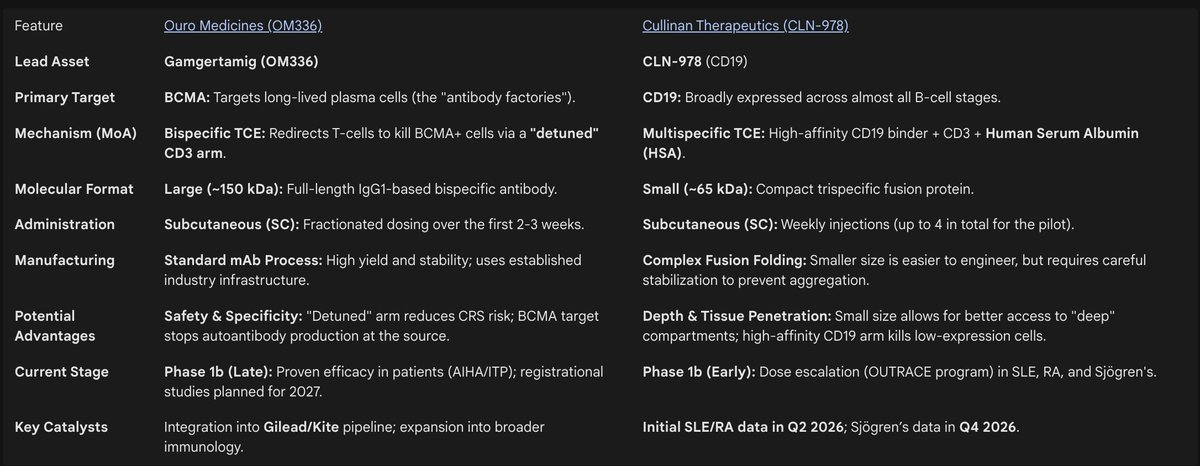

$cgem holds both cd19 and bcma tce assets, whereas ouro was a single-asset play. while ouro's focus made for a "cleaner" m&a target for $gild, it sets a clear $1.68b floor for cgem. at a $950m fdmc with $430m in cash, cgem looks undervalued given bp interest in the tce race. $sny

1

12

2,511

Jun 10

nice. if they can repeat this data in a larger patient pool, i will wonder what the value of non-viral in vivo car-t will be. $CGEM

3

573

smart $celc management move:

-$500m upsized raise on heavy institutional demand

-40% conversion premium locked at $124/sh

-super low 0.25% annual interest rate

wipes out toxic bank debt, fully funds the 1l trial/2l launch, and increases bo leverage.

ir.celcuity.com/news-release…

3

3

25

5,898

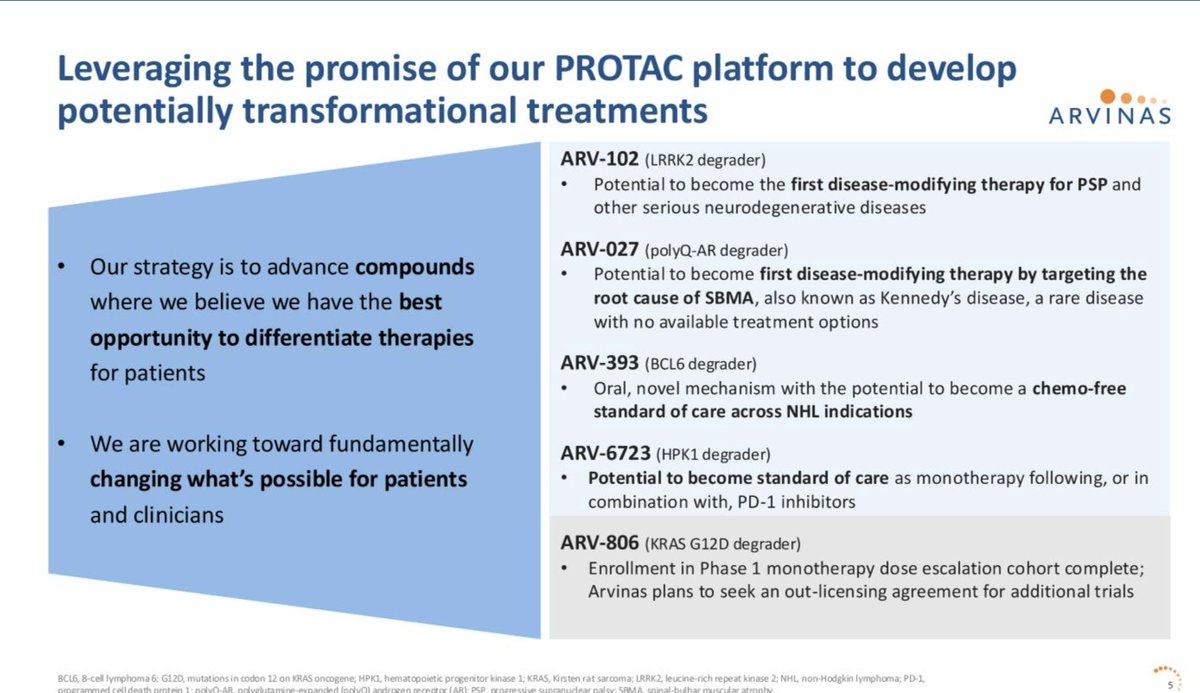

$arvn re(de)prioritizing their g12d kras asset (arv-806). i guess this is probably for the best, given the likelihood for low/no differentiation (or worse) compared to inhibitors. arvinas investors can't catch a break.

ir.arvinas.com/node/12351/ht…

3

760

1

1,487

financebully retweeted

Jun 2

𝐀𝐒𝐂𝐎 𝟐𝟎𝟐𝟔: @celcuity CEO Brian Sullivan discusses the late breaking data for the PAM inhibitor gedatolisib that was just presented at ASCO - doubled the likelihood of survival in HR /HER2- breast. $CELC #ASCO26

Full video: biotechtv.com/post/celcuity-…

1

7

26

10,189

excellent balanced piece by @FierceBiotech on $celc results. i purchased more on this dip ($6b fdmc w/ a $3b initial pys estimate for just the first two indications in 2l).

fiercebiotech.com/biotech/as…

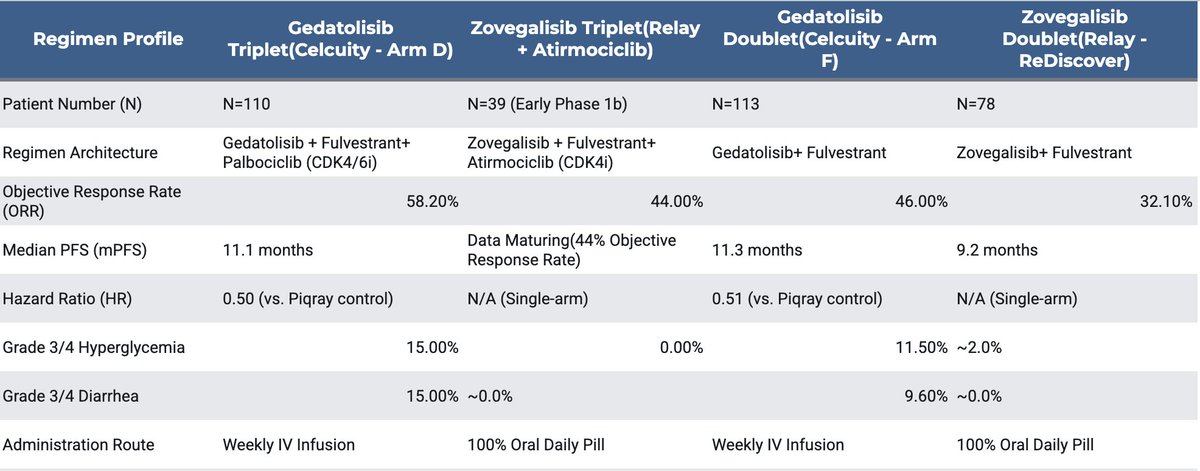

$celc $rlay keep in mind zovega ph3 primary completion isn't until april 2028 (mutants only). meanwhile, geda likely gets approved THIS year for BOTH mutant wt populations—a multi-year first-mover moat. plus, generic palbo economics crush atirmociclib for commercial/payors.

2

2

15

3,415

$celc $rlay keep in mind zovega ph3 primary completion isn't until april 2028 (mutants only). meanwhile, geda likely gets approved THIS year for BOTH mutant wt populations—a multi-year first-mover moat. plus, generic palbo economics crush atirmociclib for commercial/payors.

not seeing anything wrong with the data so far. market wanted mpfs of 14 months, but mpfs 11 mo vs 5.6 mo with hr 0.5 is AMAZING! $celc i'll be buying the dip.

2

3

19

6,385

2

22

12,372