2,336 Photos and videos

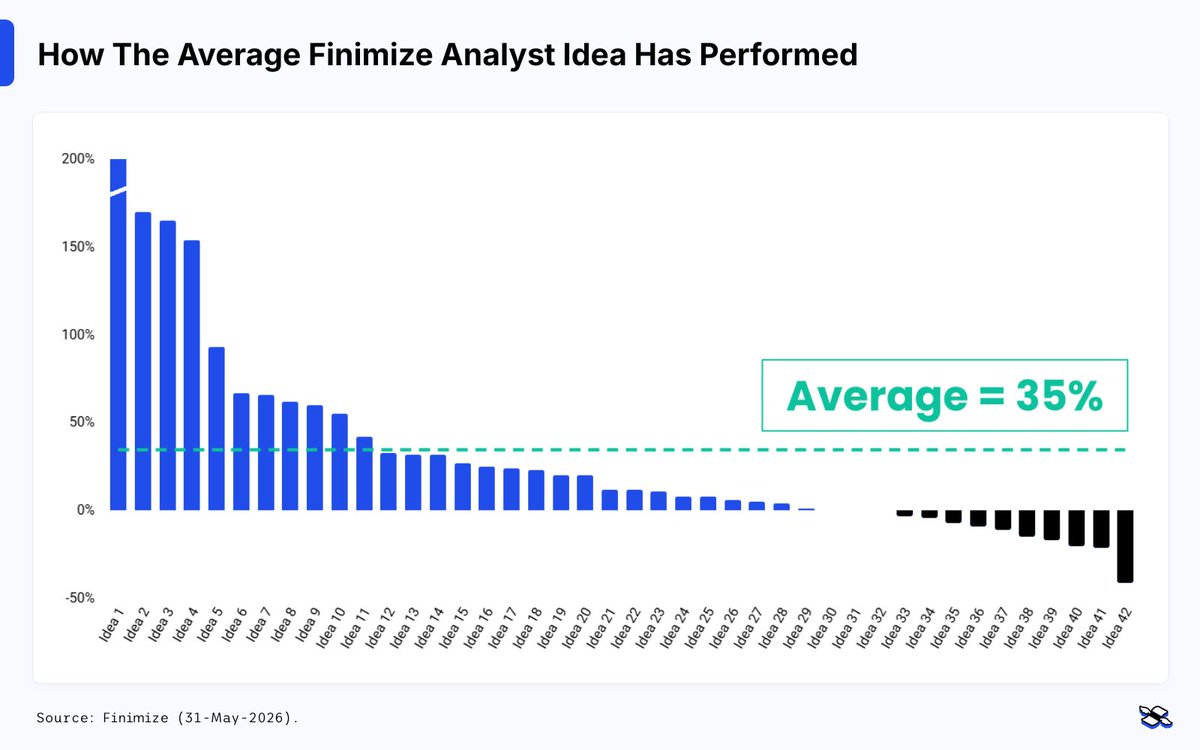

Markets have a very direct way of telling you just how smart your ideas are (or aren’t).

So once a month, we go back through our Research investment ideas and see how they’re actually holding up.

Every trade is tracked, every number reviewed, and every update is there for you to inspect: the hits, the misses, the slow burners, the character-builders.

Since their launch in October 2024, our ideas have delivered an average return of 35%, beaten their benchmarks by 19 percentage points, and posted a 74% “hit rate” – meaning most of our calls made money.

But it’s a new month, so we go analyst by analyst, and get into what worked, what didn’t, and the changes we’re making from here.

Full report here:

finimize.substack.com/p/how-…

2

304

What you need to know about markets today 👇

1️⃣ SpaceX blasted into the public markets with a record-breaking IPO, and a wave of automatic buying from index funds could give the stock another lift in the weeks ahead.

2️⃣ The Nasdaq 100 just added five AI-focused names and kicked out five others, underlining how heavily investors are still betting on the AI boom.

135

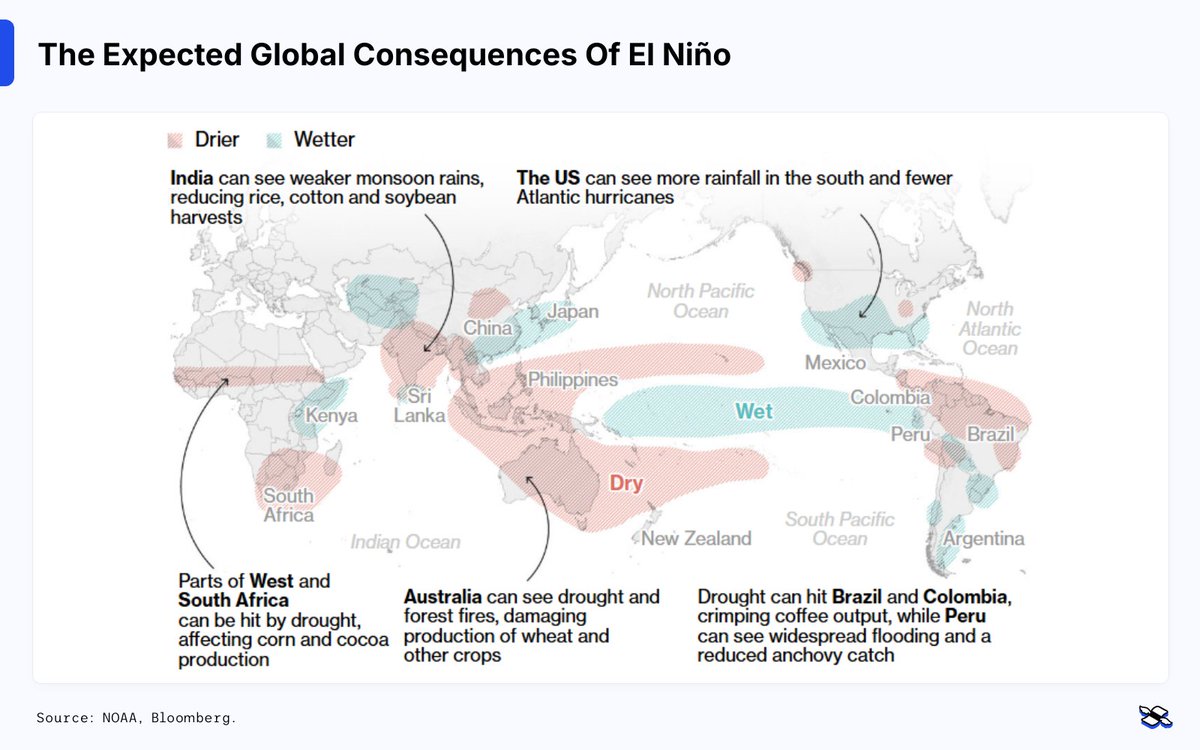

The global economy was already dealing with a lot: an energy crunch, fertilizer shortages, and inflationary pressures, much of that stemming from the war in the Middle East.

And now El Niño is back on the weather map, and this powerful climate disruptor could add another layer of stress to an already fragile backdrop.

It’s a risk too big for investors to ignore. So let’s take a look at how you can protect your portfolio from its potentially catastrophic effects.

That’s today’s Insight: El Niño’s back – don’t let it rain on your parade.

Read or listen to the research here:

finimize.com/content/el-ni%C…

#ElNiño #ClimateChange #Commodities

148

What you need to know about markets today 👇

1️⃣ The World Cup is expected to boost beer sales and betting volumes, but economists reckon the tournament will barely move the needle for the broader US economy.

2️⃣ The ECB raised interest rates for the first time in nearly two years, as policymakers chose to fight inflation even with Europe’s economy already losing momentum.

1

1

175

What you need to know about markets today 👇

1️⃣ A flood of IPOs and share sales could end a two-decade shortage of US stocks, raising concerns that the market’s low supply, big demand tailwind is starting to reverse.

2️⃣ US inflation climbed to its highest level in more than three years, keeping hopes of Fed rate cuts on ice and putting higher borrowing costs back on the table.

192

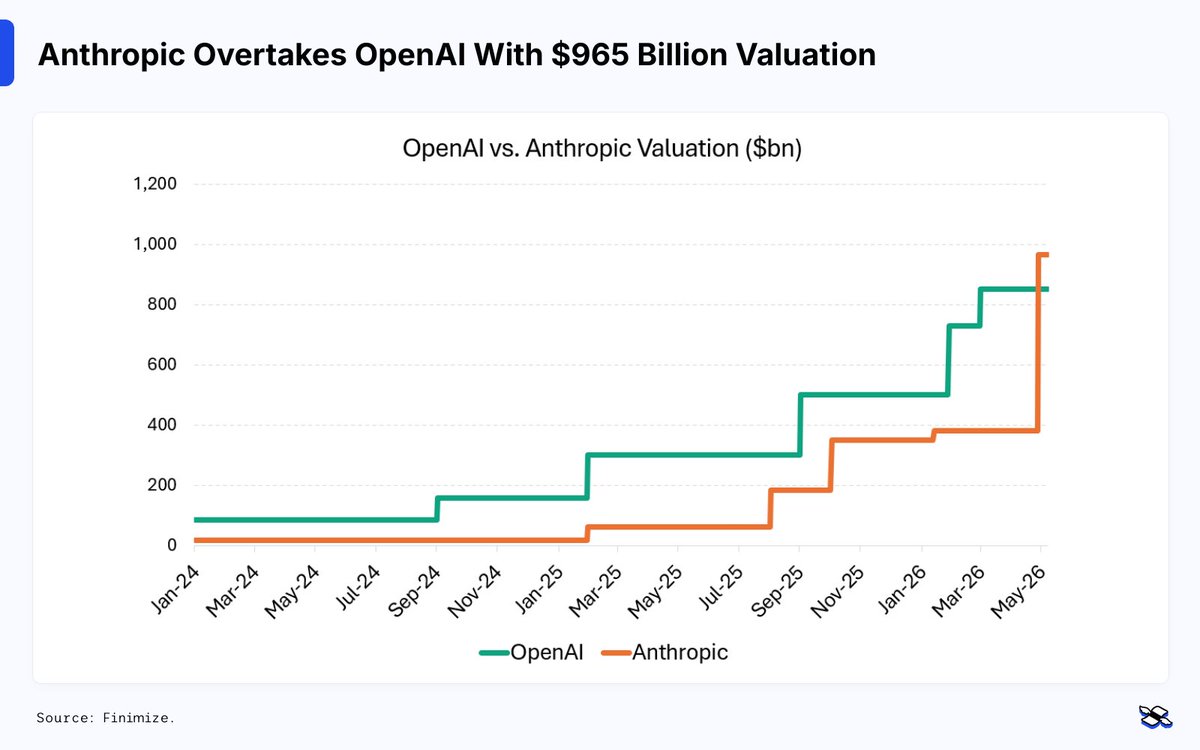

🚨 A Key Trend Supporting Stocks For Over Two Decades Is On The Verge Of Flipping

For over two decades, the total number of shares available on the US stock market has been shrinking.

That's not the same as saying there are fewer listed companies. Rather, the overall pool of publicly traded shares has been getting smaller.

That’s because share buybacks have steadily reduced the number of shares in circulation, while companies going private and delisting have removed even more.

Together, those forces have consistently outweighed the new shares entering the market through IPOs and share issuances by existing public companies.

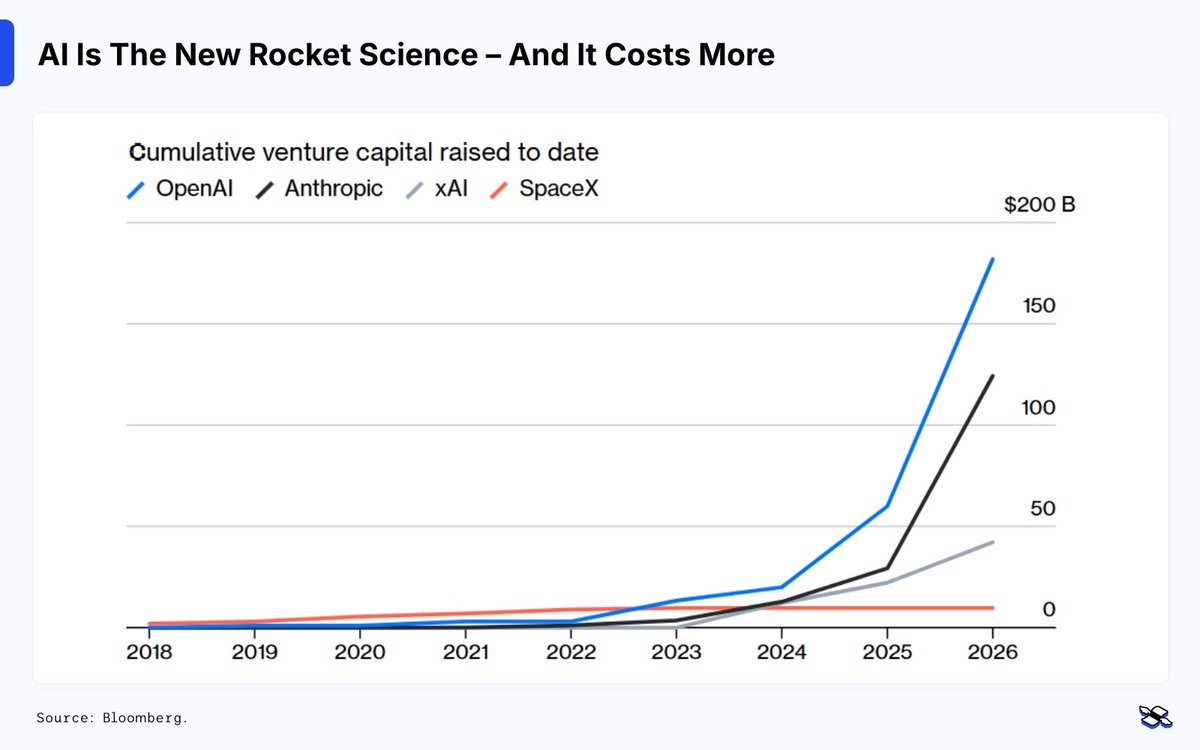

But according to Goldman Sachs, that long-running trend could come to an abrupt end this year, driven by a huge surge of new share issuance.

A string of mega IPOs from the likes of SpaceX, OpenAI, and Anthropic could raise a record $225 billion this year. And share sales by companies already on public markets could represent a bigger shift.

Alphabet, for example, last week raised nearly $85 billion in a record equity raise to fund its huge AI investments. And the fact that investors lapped it up could encourage more Big Tech firms – with equally as expensive AI ambitions – to follow suit, with Meta reportedly already exploring a share sale of its own.

This all matters. See, the stock market's broad rally over the past decade may owe something to this shrinking supply of shares.

After all, when supply falls and investor demand keeps rising, prices tend to go up. There's another effect, too. When companies buy back stock and reduce the number of shares outstanding, their earnings are spread across fewer shares, mechanically boosting earnings per share.

That's why some investors are uneasy about the trend reversing: a growing supply of shares could dilute one of the forces that has supported stock prices for years.

Some fund managers see an even bigger risk. Historically, waves of fundraising have often coincided with market peaks, as company insiders look to cash in on lofty valuations and as a flood of new shares overwhelm investor demand, putting downward pressure on stock prices.

#Stocks #IPOs #OpenAI #SpaceX #Anthropic

1

221

Should You Invest In SpaceX’s IPO – Or Leave It On The Launchpad? (PART TWO)

@SpaceX is about to make history this Friday.

So, building on our deep dive last month, we just published another fresh analysis that breaks down the key takeaways from the prospectus, updates our valuation model, and explains how investors who miss out on an IPO allocation can still gain exposure before trading begins.

Link provided below. In the meantime, here are a few observations that stood out (in no particular order).

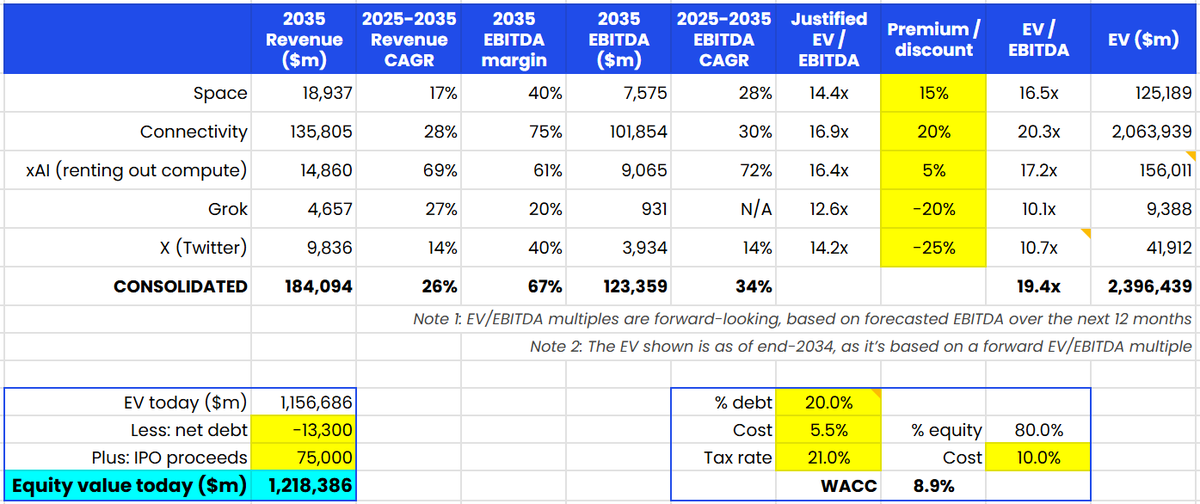

SpaceX is growing fast, but it’s burning cash even faster. Capital spending nearly doubled to $20.7 billion last year, with more than half of that going into building AI data centers.

The launch business is still losing money operationally, driven by heavy R&D spending – especially on Starship.

The two recent deals to lease compute capacity to Anthropic and Google add $26 billion in revenue – more than SpaceX made in all of 2025.

If the rest of the business grows 20% YoY and Cursor (which SpaceX will most likely snap up right after the IPO) hits $5 billion in annualized revenue, then SpaceX could finish 2026 with annualized revenue of around $53.4 billion.

That would drop SpaceX's price-to-sales ratio from over 90x to around 34x. Still very rich (the median Nasdaq 100 stock trades on 6x), but “less rich”.

That said, the Anthropic and Google deals are only through 2029 and can be terminated early. I also don’t expect these economics to last forever.

The rates SpaceX is charging look unusually high, likely because Anthropic and Google are scrambling to keep up with surging demand for their AI models.

Rather than risk capacity constraints that could slow growth and cede market share, both firms appear willing to pay SpaceX a big premium for immediate access to computing power.

Starlink subscribers have roughly doubled every year. But ARPU is falling, reflecting Starlink’s aggressive international expansion and the rollout of cheaper plans designed to grab market share.

SpaceX believes its TAM = $28.5 trillion (almost equivalent to US GDP). But 93% of that figure is tied to AI, with launch and Starlink (the company's actual core businesses before the xAI acquisition) accounting for only 7%. TLDR: SpaceX is pitching itself to IPO investors primarily as an AI play.

Lockups: while most IPOs use 180 days, SpaceX has opted for a structure that’s more staggered. That reduces the risk that the company’s biggest backers all rush for the exits at once, and prevents a flood of shares from hitting the market at a specific date.

Pay: @elonmusk's performance package could eventually be worth hundreds of billions of dollars. But he’ll only get the full amount if he colonizes Mars and relocates a meaningful chunk of the world’s AI infrastructure into the vacuum of space.

Oh, and he’ll also hold 85.1% of the company’s total voting authority.

Risks: too many. The biggest is Starship: it’s essential to nearly every major SpaceX ambition, from Mars colonization to data centers in space.

Full research piece here:

finimize.substack.com/p/the-…

$SPCX #SpaceX #Space #IPOs

1

361

What you need to know about markets today 👇

1️⃣ OpenAI’s confidential IPO filing sets the stage for another blockbuster listing, as the AI boom prepares to unleash a trio of record-breaking debuts.

2️⃣ China’s trade surplus hit a four-month high, with surging exports of AI hardware and green tech helping offset weak consumer demand at home.

189

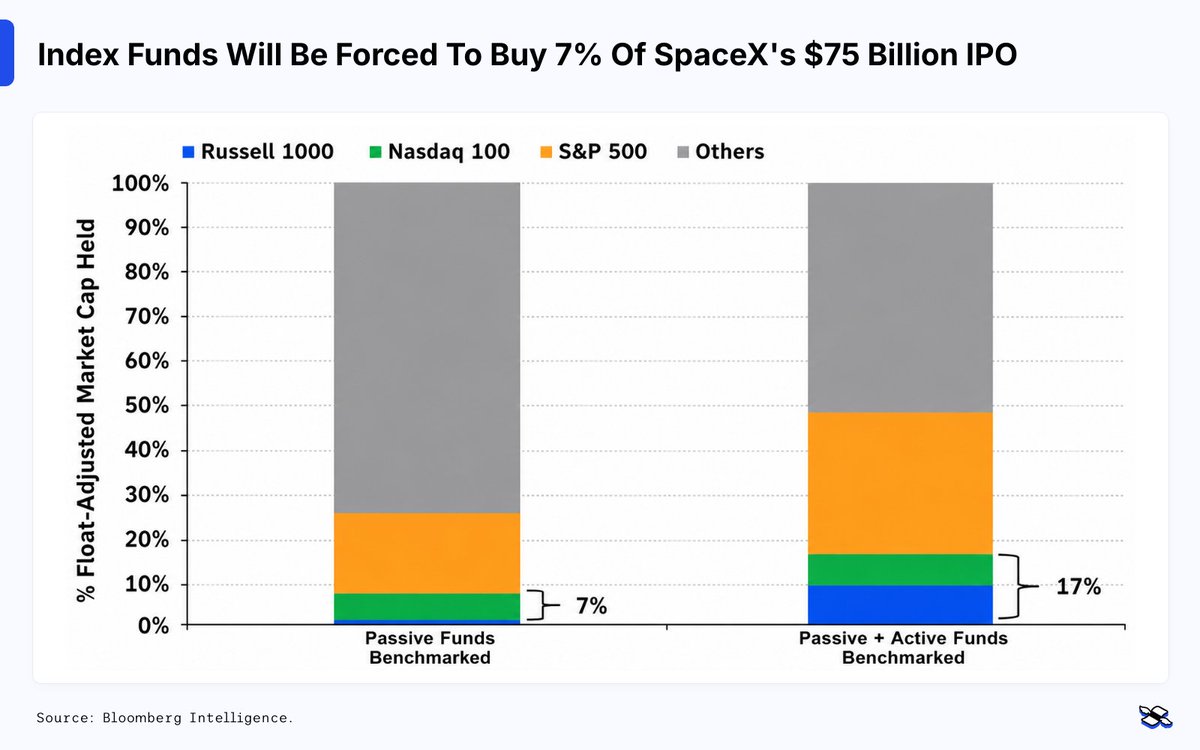

Many traders expect SpaceX’s stock to pop on its debut this Friday.

After all, strong demand will likely be chasing a relatively small free float (i.e. the percentage of a company's stock that’s actually available to trade – excluding insider holdings and other locked-up shares).

Now, some demand will come from Musk's loyal fan base. Some will come from passive index funds that have no choice but to buy what’s added to the lineup.

On that front, the Nasdaq and the FTSE Russell recently changed their rules to allow SpaceX to join their flagship indexes just a few trading days after its IPO.

Bloomberg Intelligence estimates that index funds alone could soak up 7% of the $75 billion IPO. Include actively managed funds aiming to stay market-neutral – by holding SpaceX at the same weight as their benchmarks – and that share jumps to 17%.

S&P Dow Jones Indices, meanwhile, went the other way. They considered proposals to fast-track SpaceX and other blockbuster AI listings into benchmarks like the S&P 500, but then decided to stick with the longstanding existing requirements.

That means the newly public companies would still need to wait 12 months, have at least 10% of their shares freely traded, and post positive earnings for four straight quarters before they can qualify to be included.

That said, if SpaceX eventually clears those hurdles, the prize could be much bigger than what it’ll get with the Nasdaq inclusion: roughly $24 trillion in global investments are tied to the S&P 500, according to Bloomberg Intelligence.

None of this changes SpaceX’s fundamentals. But forced buying among index-tracking funds, combined with a self-reinforcing dynamic as active investors try to front-run that move, could provide a hefty short-term boost for early investors.

$SPCX #SpaceX @SpaceX

1

1

316

Bitcoin is having one of those moments where the story feels more interesting than the price chart.

This should have been its big champagne-popping era, after all. The ETFs arrived. Big, moneyed institutions came in. Regulation grew friendlier. And businesses started treating bitcoin as something you could actually park on a balance sheet without anyone batting an eye.

And yet, bitcoin is down almost 28% this year, while the S&P 500 is up around 8%.

So it’s certainly a compelling time to revisit the crypto’s outlook.

Let’s figure out whether this is a rare opportunity to buy the OG crypto at a discount – or whether bitcoin is likely to flounder until a fresh wave of demand shows up.

Full research piece here:

finimize.com/content/the-cra…

#Bitcoin #BTC

1

154

What you need to know about markets today 👇

1️⃣ The recent wobble in tech stocks is a reminder that ups and downs are part of investing – but a wave of giant share sales and IPOs still could test investors’ appetite in the months ahead.

2️⃣ Germany’s latest factory data suggests Europe’s biggest economy is feeling the squeeze from higher energy prices, raising fears of slower growth and stickier inflation.

213

283

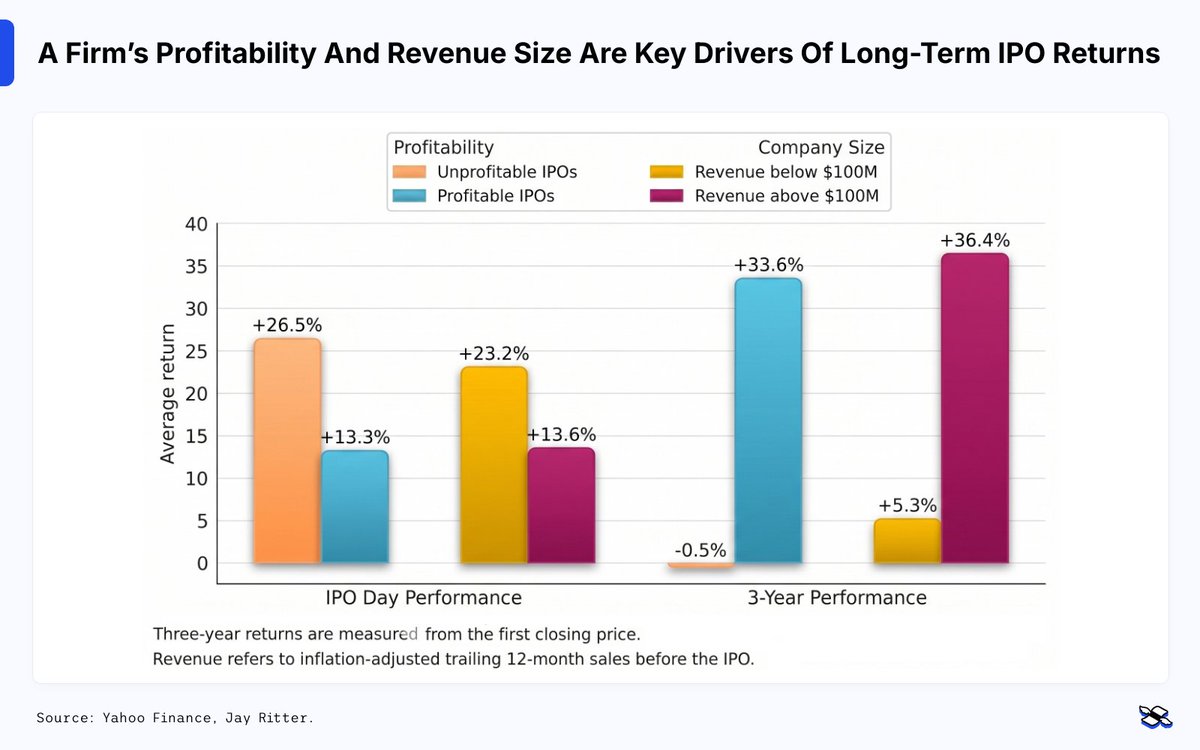

With SpaceX set for a blockbuster market debut on Friday, it’s worth remembering that IPO hype doesn’t always translate into long-term gains.

Research from IPO expert Jay Ritter shows that, between 1975 and 2021, the average newly listed company underperformed over the three and five years after going public.

That said, some IPOs stack the odds in investors’ favor.

Historically, the winners have tended to be companies that were bought at the offer price, backed by venture capital, generating more than $100 million in annual revenue, and – better still – already profitable.

Investors have also generally fared better steering clear of SPACs (so-called “blank-check” companies).

Size matters, too. Larger, more established businesses have typically outperformed their smaller, riskier peers, while tech IPOs have delivered some of the strongest returns after listing.

#SpaceX #IPO

239

Some random thoughts on @SpaceX

First, the valuation multiple is compressing quickly.

$1.8 trillion market cap. $18.7 billion revenue in 2025. Over 90x price-to-sales – enough to freak out even the growthiest of growth investors.

But consider this: a few weeks ago, SpaceX signed a deal to lease compute capacity to Anthropic for $1.25 billion per month = $15 billion per year.

Over the weekend, it signed another deal with Google for $920 per month = $11 billion per year.

Combined, that’s $26 billion in incremental revenue.

If the rest of the business grows 20% year-over-year, then SpaceX could end 2026 with annualized revenue of [18.7 x 1.2] 15 11 = $48.4 billion.

Price-to-sales now drops to 37x. Still very rich (the median Nasdaq 100 stock trades on 6x), but “less rich”.

That said, the Anthropic and Google deals are only through 2029 and can be terminated early.

I also don’t expect these economics to last forever.

The rates SpaceX is charging look unusually high, likely because Anthropic and Google are scrambling to keep up with surging demand for their AI models.

Rather than risk capacity constraints that could slow growth and hand market share to rivals, both firms appear willing to pay SpaceX a big premium for immediate access to computing power.

Second, the big allocation to retail investors could limit the usual first-day IPO pop.

Up to 30% of the offering is being handed to individual investors (versus the typical 5-10%).

Every single bank and broker that I use is spamming me with emails and notifications to participate in the SpaceX IPO.

I suspect many investors will heed the siren call, driven largely by FOMO.

But remember: IPOs often soar on day one because retail investors miss out on the offering and scramble to buy once trading begins.

Considering SpaceX is giving everyday investors meaningful access from the start, that buying frenzy may never materialize – potentially muting the stock's first-day pop.

Third, speaking of bank notifications, my phone lit up over the weekend with an alert from @Revolut inviting me into the SpaceX IPO.

One problem: Revolut is quoting an offer price of $162 a share, despite SpaceX having already set the IPO price at $135. That's a hefty 20% premium.

I've asked why. So far, the explanations haven't really added up. If you're planning to invest through Revolut, it's worth double-checking exactly what you're paying for.

For a deeper dive, check out my full research piece on SpaceX:

finimize.substack.com/p/shou…

#SpaceX #IPO

2

427

What you need to know about markets today 👇

1️⃣ Weight-loss drugs are reshaping more than waistlines, with retailers, food companies, and alcohol makers all feeling the knock-on effects of changing consumer habits.

2️⃣ A stronger-than-expected US jobs report eased fears about the economy, but it also increases the chances that the Fed keeps interest rates higher for longer.

1

182

🤔 Quick question:

What percentage of a typical global stock ETF do you think is invested in the companies that:

⚡ power the grid

⛏️ mine the copper

🛢️ produce the energy

🌾 grow the food

50%?

25%?

15%?

Try 9%.

Here's why that matters more than many investors realize 👇

finimize.com/content/the-9-b…

1

204

What you need to know about markets today 👇

1️⃣ SpaceX is targeting a record-breaking $1.78 trillion IPO valuation, setting up what could be one of the most hyped stock-market debuts ever.

2️⃣ Broadcom’s second-quarter results just beat expectations, but not by enough for investors who’ve grown used to AI-fueled blowouts – a reminder that sky-high expectations can be just as important as strong earnings.

1

186

Finimize Pro users got the #investmentresearch behind the stats in July 2025. But @nebiusai is just one of 32 open and tracked ideas in the full Finimize basket.

Explore Finimize Pro here: finimize.com/join?utm_source…

Russell's OG Nebius research here:

finimize.com/content/the-neb…

154

📈 Every big investment house has a midyear outlook.

Most are full of forecasts that'll be forgotten by Christmas.

Fidelity did something different: it identified 5 forces that could shape markets for the rest of 2026.

🌍 International stocks

💰 US earnings

🌪️ Volatility

🏦 The Fed

🏠 The wealth effect

I unpacked each one and gave my own verdict 👇

finimize.com/content/fidelit…

1

1

167

What you need to know about markets today 👇

1️⃣ Bitcoin slid further after its biggest corporate backer sold a small portion of its holdings, fueling fears that the crypto downturn could have further to run.

2️⃣ The US is proposing a fresh round of tariffs on dozens of trading partners, adding another layer of uncertainty for businesses already grappling with higher energy costs and slowing global growth.

147