Aspiring philanthropist. Personal views only. Not investment advice. Posts are not a recommendation to buy or sell any securities.

Joined August 2025

- Tweets 4,090

- Following 1,049

- Followers 2,809

- Likes 13,224

34 Photos and videos

8

1

11

1,998

People are debating whether this is bullish or bearish for AI, but it’s not the right way to think about it.

Being bearish on AI is like being bearish electricity. Or the internet. Except AI is probably even more significant than either of those were.

Technological revolutions don’t get canceled halfway through. We’re not even at the “dial up” phase of AI. We’re crawling right now. Walking, running, and then sprinting comes in the future.

You can be bearish on AI stocks in the short term, you can be bearish on certain companies, you can even think there’s a bubble in segments of the market.

But being “bearish AI” is silly.

Jun 13

The US government, citing national security authorities, has issued an export control directive to suspend all access to Fable 5 and Mythos 5 by any foreign national, whether inside or outside the United States, including foreign national Anthropic employees.

The net effect of this order is that we must abruptly disable Fable 5 and Mythos 5 for all our customers to ensure compliance.

Access to all other Claude models is not affected.

We apologize for this disruption to our customers. We believe this is a misunderstanding and are working to restore access as soon as possible.

Read our full statement: anthropic.com/news/fable-myt…

7

1

22

2,518

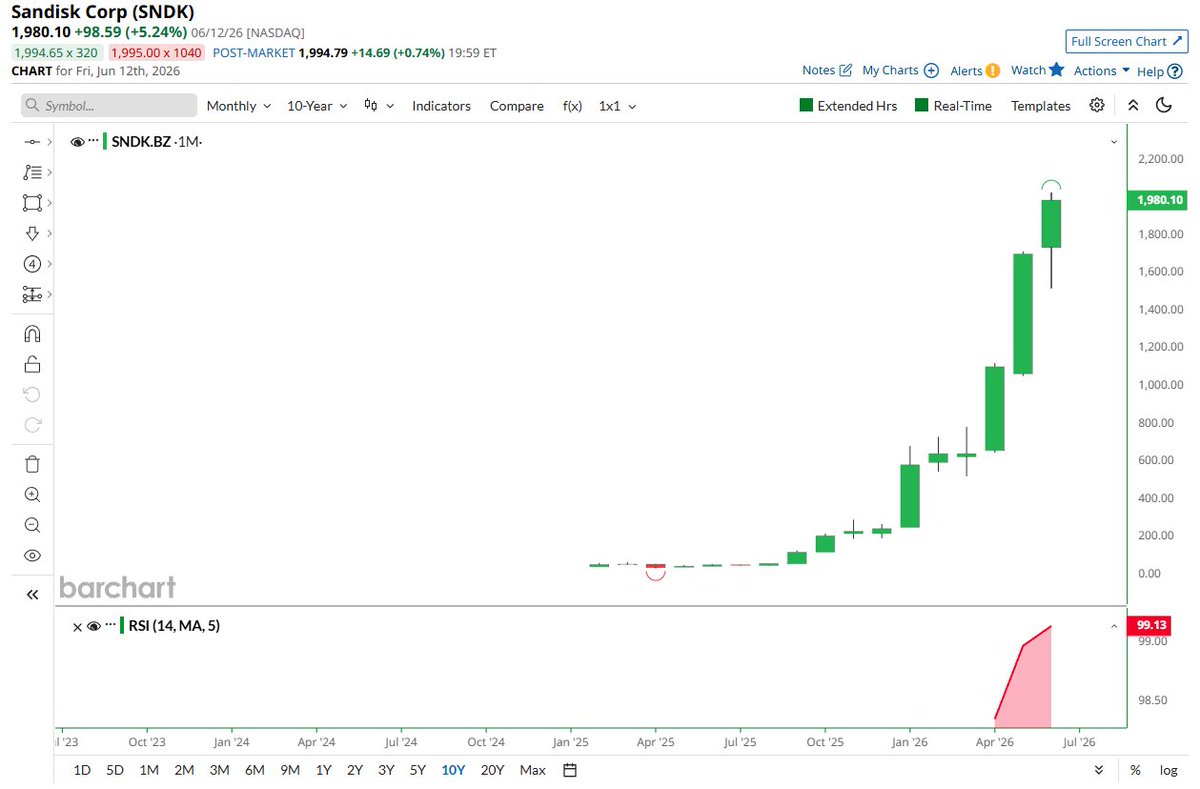

Haters will say it’s unsustainable

Sandisk $SNDK hits a 99.13 on the Monthly RSI, the most overbought level for any stock in history 🚨🚨

4

1

10

3,635

$RDDT is very misunderstood. US DAU growth is slow because the platform has been popular for 20 years now. Yes, it can improve and I think it will but it doesn’t need to.

Increased ad loads is a long term growth engine. They can increase ads at an imperceptibly small level month over month for several years. Improvements to ad targeting and driving better ROAS for advertisers will scale indefinitely.

The way we should look at Reddit is like this: An already hyperscale platform that now needs to be “harvested”. More ads, better targeting, better ROAS, etc. These things can drive huge revenue growth for a very long time.

You also have the data licensing deals. Reddit is by far the largest repository of training data not owned by a frontier lab. The labs need more and more data to feed the models just like they need more and more compute. And they’re doing to continue needing it far into the future.

What are your thoughts on $RDDT?

So much to like about this financial engine. Top-line growth looks amazing. Margin trends look great. Engagement trends are strong. Pretty balance sheet too.

The only thing that doesn’t look absolutely amazing is 7% U.S daily active user (DAU growth. Leadership will explicitly tell you they want to do better here & they’re working hard to improve.

Why does this matter so much with revenue still rapidly compounding regardless?

Ad load can only ramp for so long. As that opportunity matures, revenue & user growth will more closely track each other. So? Faster user growth is vital for making sure they briskly grow revenue for a long time.

And there are great reasons to think they can find that better DAU momentum. Feed personalization, search upgrades, onboarding enhancements & more should all work. They did for $META. They did for other platforms with strong, engaged user bases. They’re already starting to bear fruit for this firm. Every reason to believe these changes will work here like they did for similar models.

And if these changes do work? You’re paying 22x forward profit for a 30% revenue compounder with EPS growing well in excess of that. PEG well under 1.0X for what looks to be a high-quality business.

Interesting. 🤷♂️🙂

3

9

1,141

Jun 13

TRUMP:

- SIGNING DEAL WITH IRAN TOMORROW

- STRAIT OF HORMUZ WILL BE OPEN TO EVERYONE

- LOOKING FORWARD TO WORKING WITH THE ENTIRE MIDDLE EAST

bro saved the deal signing for his birthday 😂

4

14

1,216

x.com/hormuzletter/status/20…

Lol nvm

Jun 13

BREAKING: Iran directly rejects Trump's new claim of a deal being signed tomorrow, saying the insistence on signing the deal on specifically Sunday is engineered around his own birthday, calling it a "propaganda event" that Trump is trying to turn into a unilateral "symbolic occasion" for himself, along with his UFC White House event, per Fars.

The Iranian negotiating team says it "will not permit such a media and ceremonial manoeuvre," explicitly stating that the memorandum of understanding has not been finalized and no signing will happen.

1

7

422

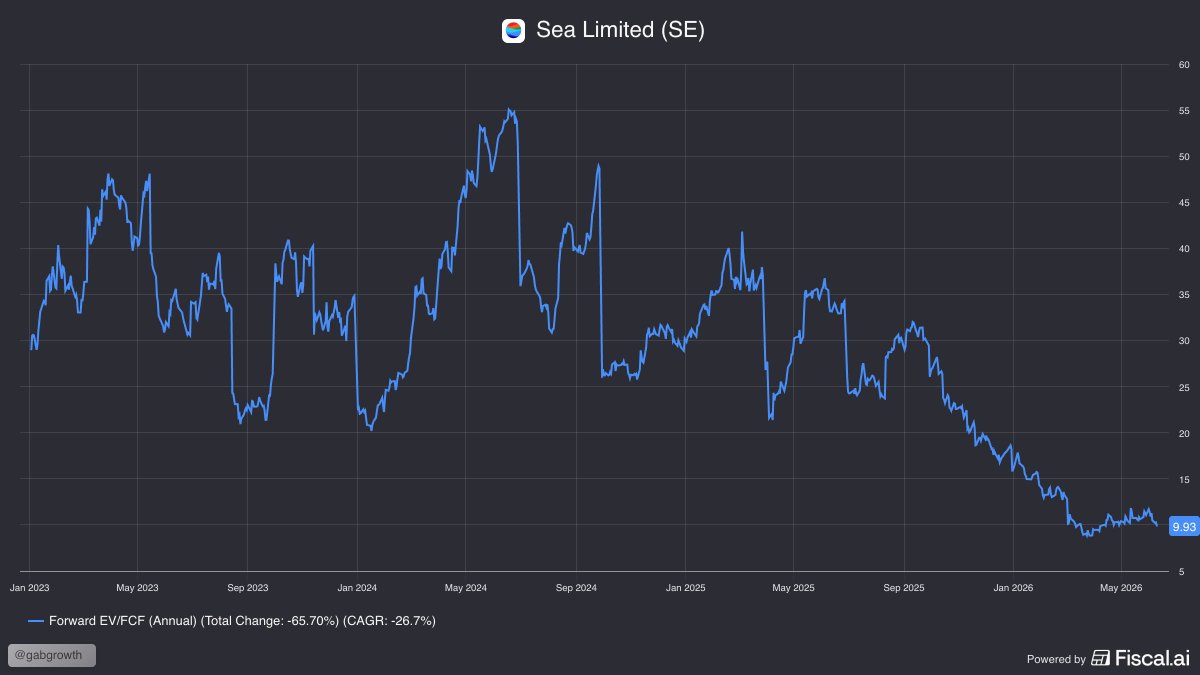

It’s been a tough ~9 months as an $SE shareholder. Especially when it’s a large part of your portfolio (like it is for me).

The business has outperformed my expectations over the past 9 months. All three units have serious momentum. Revenue was up 47% last quarter. I’m more bullish on the company than ever.

The valuation is frankly ridiculous at this point. 2027 consensus EPS estimates are $5.30. That’s 15.6x next year’s EPS. If we strip out the net cash, it’s 13.5x. Revenue will still be growing quickly next year and margins will be expanding. It’s really an amazing opportunity for investors.

Ultimately, I’m grateful that I have the chance to buy such a high quality asset at such a cheap price. And I see this period as a part of the journey.

I look forward to the day we reclaim the all time high, and eventually, when we hit $1T.

9

3

30

4,915

What if $META has the superior capex strategy to the CSPs? Instead of having your cloud business drain your resources, you build a massive compute network for peak needs and then rent out excess capacity. Just like how AWS started.

They’ll always have the compute they need, rent the excess at 35-40%, and they never have to pay someone else’s margin. Just look at the shake down SpaceX is running on Google.

There will be times they have excess capacity. Just route that to a buyer and boom you’re making money. Never an unused GPU, but full capacity whenever you need it.

8

66

6,960

Zuck, I’m begging you to rent just one GPU to someone else. Your stock price will instantly go to $700 and then you can raise equity for more data centers

$META

27

10

433

39,790

It’s so bizarre to me that people are acting as if $SPCX at $2T is normal or okay

Stephanie Link just said it’s a “screaming buy” on CNBC…

It sends a message that being the best charlatan is more valuable than actually making useful products and services for people

14

26

2,218

Jun 12

What stock do you think could double and still not be overvalued?

7

2

31

8,934

What if the $SPCX IPO actually creates more demand for other stocks because a massive pool of formerly private capital is now available to be tapped?

Too cute?

5

9

2,015

$META is now my largest position. I didn’t plan for this but the opportunity here is insane.

The forecast I’m seeing for EPS is $32.21 this year. Over the last twelve quarters, they’ve beat consensus EPS 100% of the time and on average by 12.5%.

That would put us at $36 this year, good for a 2026 P/E ratio of 15.5x! In other words, if the stock is flat over the next six months, the trailing P/E will likely be 15-16x.

Revenue grew 33% last quarter, Plus subscriptions launching, more compute to help the core biz, Meta’s SMB AI suite with over 1M businesses already, a potential cloud unit, 7M pairs of Glasses sold in 2025, significant headcount reduction, and reality labs spending cuts.

When you get a fat pitch, you gotta swing

37

5

276

28,929

$SE is one of the fattest pitches I’ve ever seen.

It’s trading at 15.6x next year’s earnings. They just grew revenue by 47%.

And margins are currently suppressed by high levels of investment, so it’s even cheaper than that. This is CRAZY at this point

Jun 11

$SE at $80 is a fat pitch.

10% forward FCF yield on a business that is growing 47% YoY.

Market is pricing $SE like it's going out of business.

5

2

35

3,808

Some people are asking, what if $NVDA revenue peaks this year or next?

We have enough info to know that Nvidia’s revenue will be significantly higher in ‘27 than ‘26. Guidance from hyperscalers, build out schedules, guidance from Nvidia, etc. Then, there are so many data centers being built that won’t be operational until ‘28-‘30. And the ones coming online in ‘28 to ‘30 are MUCH larger.

Meta’s 5GW Hyperion campus won’t be operational until 2028 and won’t be scaled to 5GW until after 2030. Keep in mind 5GW equates to about 2,500,000 B300s and each B300 costs $50,000. OpenAI is in talks to lease a 10GW DC in Ohio.

These are just two projects. Meta has several other data centers, as do the hyperscalers, model companies, etc. Not to mention, by 2028/2029 you’ll be getting refreshes from 2023/2024 GPU buys. I think it’s totally possible that our 2028 to 2030 revenue forecasts for Nvidia are way below what they’ll actually turn out to be.

If $NVDA revenue PEAKS forever in 2030, falls substantially over the next two years, and then flatlines permanently, it’ll still beat treasury bills according to my model.

Assuming they buy back a lot of stock (2.5-3% per year), and maintain EBIT margins in the high 50s/low 60s

I don’t think that’ll happen, but even if it does you can still get a decent return (7-8% per year).

8

44

10,116

“It’s trading at its lowest historical valuation” is a completely meaningless statement.

If you want to value a company, build a DCF. If you don’t want to build a DCF, compare price ratios to the industry, not the company historically.

Why? Companies change over time. The company you’re looking at could’ve been growing faster, had less competition, better management, stronger balance sheet, all manner of differences that could be lowering the valuation ratios.

2

1

11

732

If $NVDA revenue PEAKS forever in 2030, falls substantially over the next two years, and then flatlines permanently, it’ll still beat treasury bills according to my model.

Assuming they buy back a lot of stock (2.5-3% per year), and maintain EBIT margins in the high 50s/low 60s

I don’t think that’ll happen, but even if it does you can still get a decent return (7-8% per year).

13

2

60

18,852

And same thing if you peak it in ‘29 and it falls off in ‘30 and ‘31. I only have 10% revenue growth in ‘30, so it doesn’t change the outcome that much if it peaks in ‘29

5

760