I write about asymmetric investments that go unnoticed, with a deep focus on emerging markets.

Joined August 2018

- Tweets 12,872

- Following 579

- Followers 22,020

- Likes 13,346

1,506 Photos and videos

Pinned Tweet

Jan 7

It's been almost 16 months since I started publishing my deep dives in public and 6 months since going paid.

I thought it would be a good moment to pause and express my gratitude for the community that has formed around this work.

When I first started writing, there were no expectations beyond wanting to think more clearly by documenting my process, and sharing ideas with like-minded individuals. The response since then has been far more encouraging than I could have imagined.

I also think it’s an appropriate time to take stock of how things have been going and provide some transparency around the performance of these deep dives so far.

I've published 13 deep dives to date, 10 bullish and 3 neutral. I have no interest in being bearish or short. If I don't like a business/stock, I simply don't buy it.

Of the 10 bullish picks, 9 are currently in the green while 1 is in the red. One of the green positions has been closed, while the others continue to be held.

Of the 3 bearish picks, all 3 are in the red as I write.

On average:

- Bullish picks: 38.7%

- Bearish picks: -26.7%

- SPY: 12.2% over the same period

I must also acknowledge that I’ve been fortunate to have started this blog in the middle of a bull market, and the performance to date is by no means a reliable indicator of long-term success.

I’m sector-agnostic, and these names span e-commerce, consumer discretionary, SaaS, infrastructure and more. It's still very early and I've thoroughly enjoyed the process thus far. There will definitely be drawdowns and mistakes ahead. As always, I'll stay transparent and share both the research and the outcomes, good and bad.

Thank you to everyone who has been part of the journey, in particular to paid subs who continue to place their trust in an anonymous person from a tiny country in Southeast Asia. I hope to continue rewarding that faith by producing high-quality research grounded in facts, not hyperbole. ❤️

9

4

114

31,756

5h

As an investor, it always pays to be an optimist.

Pessimism sounds smarter because there is always something to worry about from valuation, competition, dilution to macro, regulation and execution risk.

However, markets don’t reward the person with the longest list of concerns. It rewards the person who can identify when a business is getting structurally better, before everyone else is willing to believe it.

Great companies often look expensive on the way up. The easy thing is to wait for perfect clarity. The problem is, by the time clarity arrives, the opportunity is usually gone.

Of course, optimism doesn’t mean ignoring risk. It means understanding that a few exceptional winners can more than pay for many mistakes.

1

2

22

1,414

10h

$GLXY

Anyone who has studied the business understands this, and the dislocation in valuation is frankly quite shocking.

It has been the case for over a year now and led to severe underperformance compared to peers who have been rewarded extremely well.

The two catalysts remain:

(1) The next 830 MW being rented out to one of the hyperscalers

(2) Delivery of further tranches to $CRWV and recognising of revenues in upcoming earnings reports

Jun 12

Valuation is not what it seems. That's why I said twist on $NBIS.

Type of thing that would be clear if spun off. SImilar to NBIS with the different assets and business lines back then.

Misunderstood imo.

4

2

32

4,585

11h

$GLXY remains one of the most undervalued assets in the market, even after the recent strong performance.

OG Cap details a simple but extremely reasonable napkin math valuation that aligns well with my view on $GLXY

Check it out! 👇

Some napkin math on $GLXY.

It's market cap is around $12B.

$GLXY has three core businesses:

> its crypto balance sheet, currently around $3-4b;

> its crypto Investment Banking type business;

> its data centre business.

Essentially, $GLXY already has 800MW approved and leased to $CRWV and has another 800MW approved (@novogratz said we'll learn of the tenant by July hopefully).

If you apply the same margins as their $CRWV deal, that is 2.4B in revenue and 2.16B in EBITDA (90% EBITDA margins). Say you slap a 15x P/ EBITDA, that's $32B on its data centre business alone. Say 1.6GW comes online 2028? So since market is forward looking, that's a FY 2027 price.

It also seems very likely that $GLXY can have 3.5GW come fully online by 2031/2032. Applying the same metrics, that's $5.25b in revenue and 4.725b in EBITDA in 2031/2032 just from the data centre business alone. At15x P/EBITDA that's $70b ($170 per share) in 7 years.

It's crypto IB business is another beast altogether, but I think it can conservatively be valued at $5B (bull $20B).

Conservatively, $GLXY should at least be $5B (IB Business), $30B (data centre, accounting also for 1.9GW more in study), and $3B crypto balance sheet.

That adds up to $38B. $GLXY is trading at $12B now.

I am long $GLXY.

1

1

31

4,082

14h

Watch what they do, not what they say.

FundSmith has been buying poor businesses, overpaying and trading in and out of positions.

Not surprising they’ve underperformed.

Jun 13

"Buy good companies, don't overpay, do nothing."

— Terry Smith

2

3

37

6,803

Jun 13

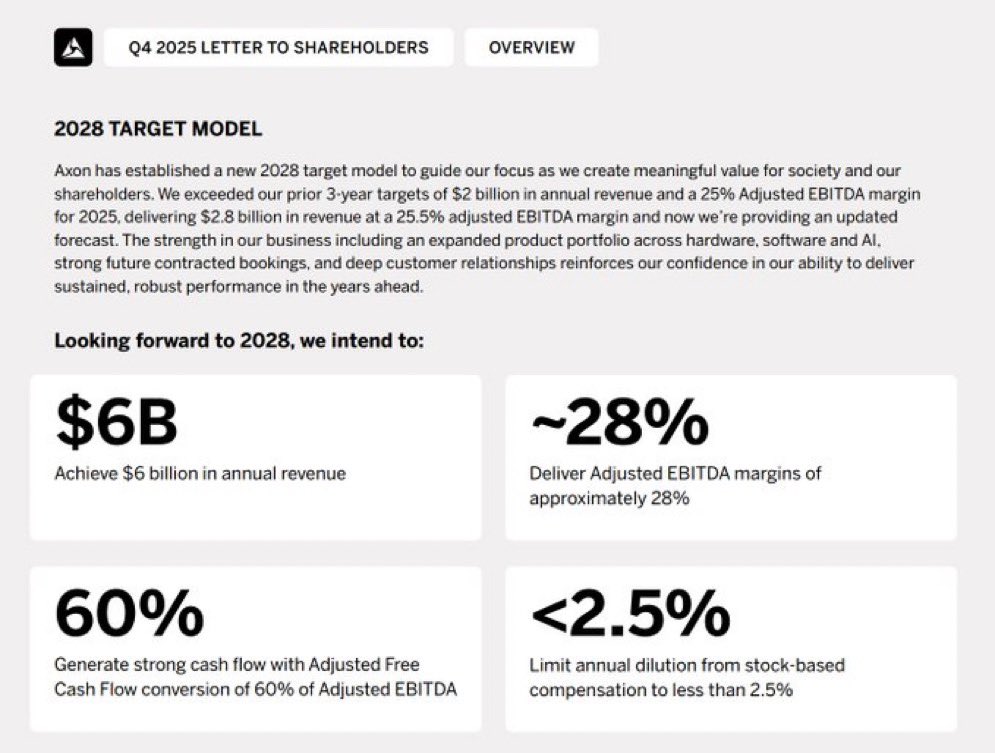

$AXON

In the next 3 years:

- Annual Dilution from SBC will come down from 3% -> 2.5%

- Revenue will more than double from $2.8B -> $6B

Jun 13

$AXON

I know and appreciate the concerns with valuation and SBC.

However, putting that aside, there’s not many better businesses to own in the next decade.

1

12

2,315

Jun 13

The best part about this post is that both people who love/hate Elon will like the post assuming their view point.

Greatest test of intelligence is asking someone what they think of Elon Musk

1

10

1,790

Jun 13

$AXON

I know and appreciate the concerns with valuation and SBC.

However, putting that aside, there’s not many better businesses to own in the next decade.

7

21

6,085

Jun 13

re Valuation:

Great businesses can outgrow their valuation, poor businesses can never grow into theirs.

re SBC:

$AXON SBC has always been extremely high, top percentile, but that hasn’t stopped the stock from being up 25.5x in the past 10 years.

5

1,239

Jun 13

Which are the operating companies and the equipment companies of today?

Will we see a repeat?

Jun 12

Annualized Returns: 1877 - 1926

All Stocks: 8.06%

Railroad Operating Companies*: 7.58%

Railroad Equipment Companies**: 12.89%

*(Survivors subsumed into Big 6 -- UNP, CSX, NSC, CNI, CP, BNSF)

**(Survivors subsumed into, eg, WAB, ALO (Euro),

TRN, business lines of GE, etc.)

6

3,039

Jun 13

When (not) to buy $SPCX: four phases of the IPO playbook:

1 - PUMP

2 - DUMP

3 - DEAD MONEY

4 - REDISCOVERY

2

1

25

4,264

Jun 12

Shared with X subs the 2 stocks I was looking to add this week, turned out pretty well!

$GLXY up about 32% since Monday. $CRWV now added to Nasdaq and up 8% on the day!

I only share high-conviction ideas, come join us if it interests you.

x.com/GabGrowth/creator-subs…

1

18

3,149

Jun 12

$GLXY is one of the most misunderstood assets in the market.

And it’s not even that hard to understand!

Jun 12

3

2

40

5,579

Jun 12

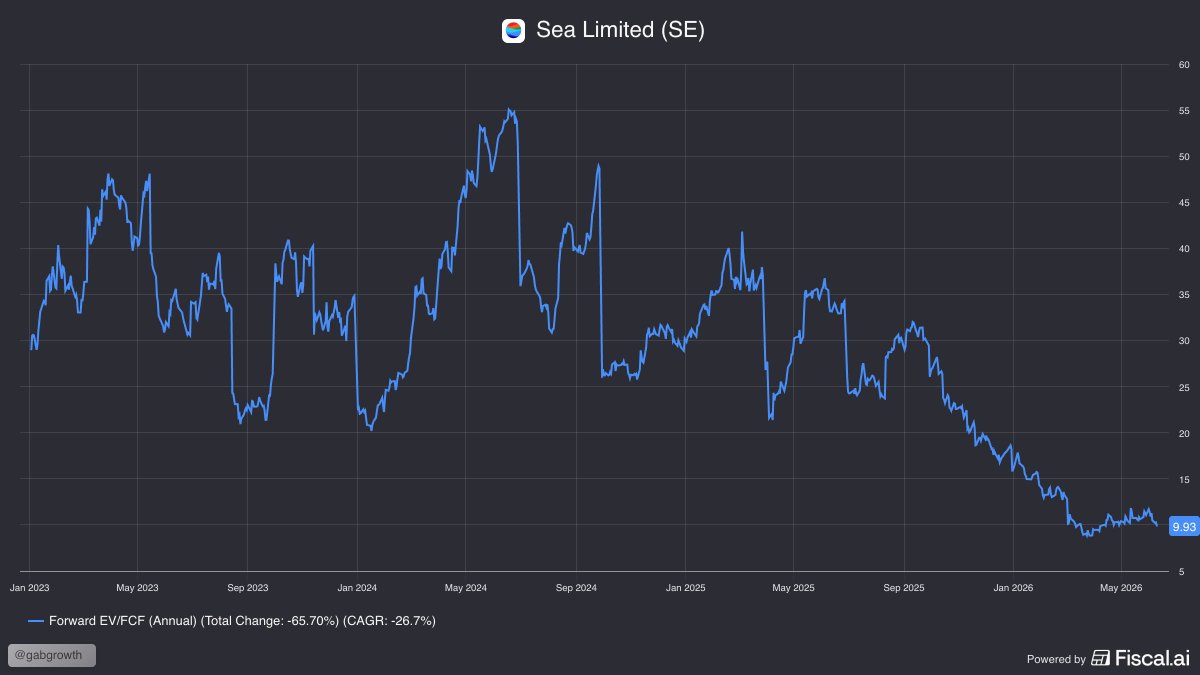

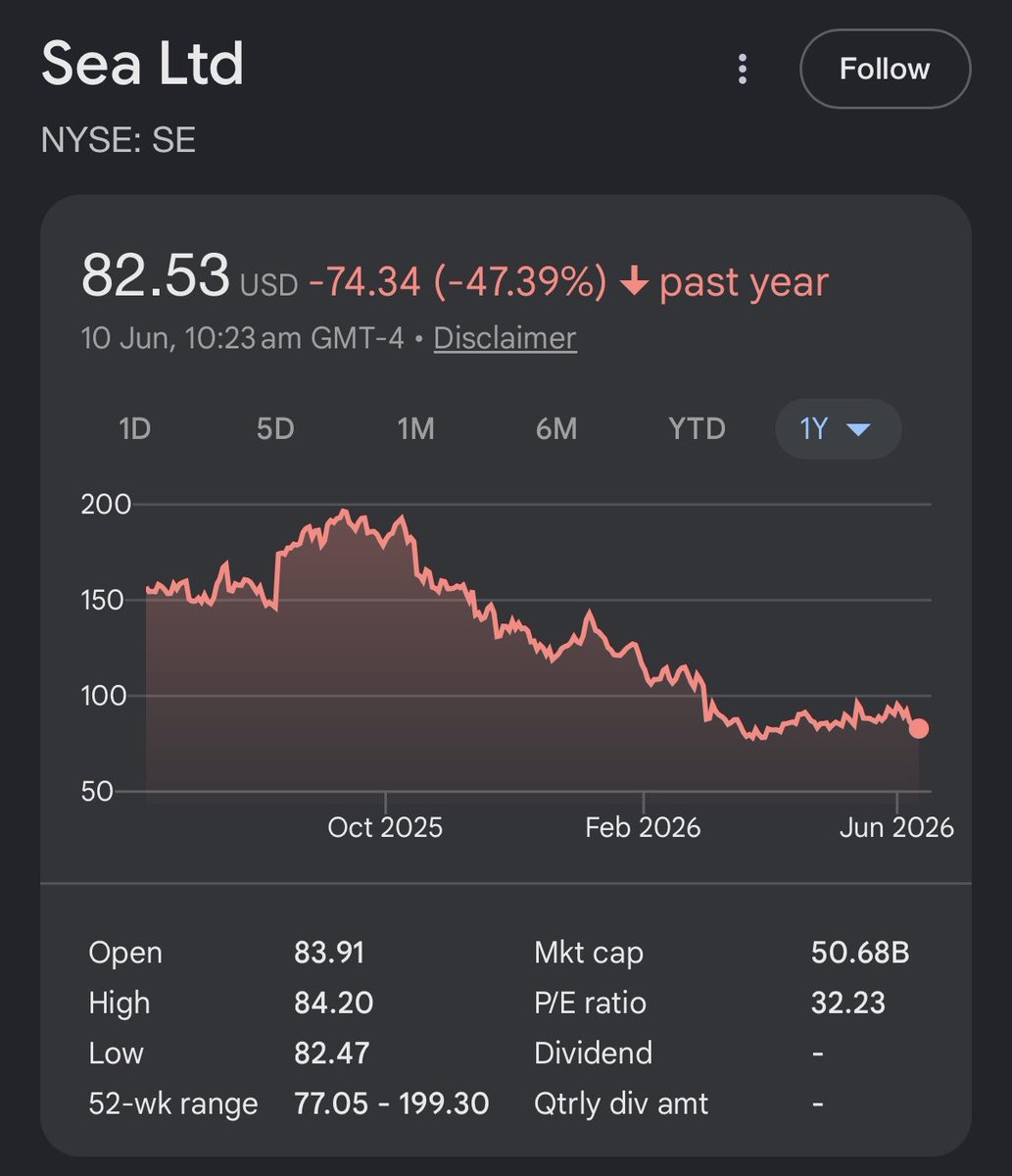

$SE ShopeeFood GMV growth in the past 3 years:

2023: $1.52B ( 66%)

2024: $2.35B ( 54%)

2025: $3.33B ( 42%)

Jun 12

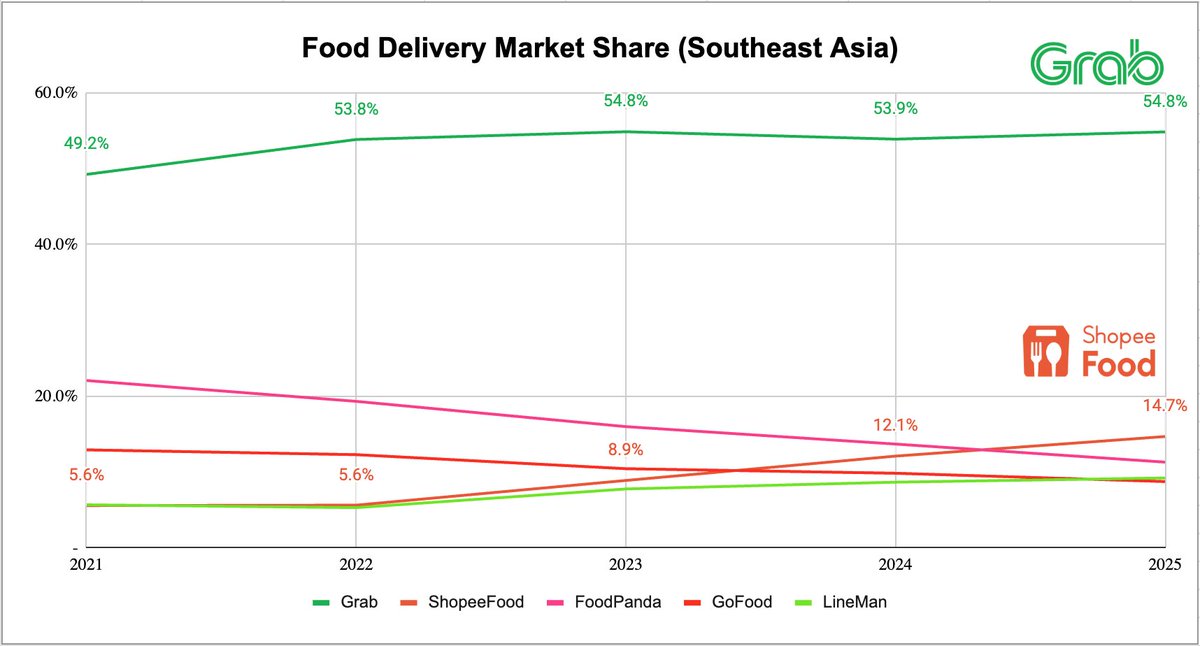

An extremely under-looked area of $SE is food delivery.

ShopeeFood has gone from 5.6% (5th place) -> 14.7% (2nd place) market share in 4 years.

Again, we are seeing a duopoly emerge with $GRAB leading the way.

2

33

3,718

Jun 12

x.com/GabGrowth/creator-subs…

In case you missed it, I’ve launched subs on X. It’s at a 70% discount to the other site (SS) at the moment.

SS remains where I publish all the detailed deep dives, but I publish shorter-form content and ideas on here. Come join us if it interests you!

5

1,173

Gab retweeted

Jun 12

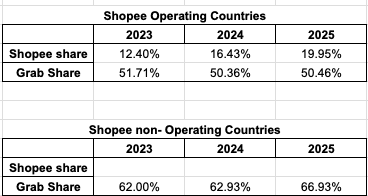

Also $SE Shopee Food only operates in four Southeast Asia countries. So if calculate the weight average market share, Shopee market share is near 20%! versus $GRAB's 50%.

In the places where ShopeeFood are not operating. (aka. Singapore and Philippines.) $GRAB market share is much higher and are continue trending up.

Jun 12

An extremely under-looked area of $SE is food delivery.

ShopeeFood has gone from 5.6% (5th place) -> 14.7% (2nd place) market share in 4 years.

Again, we are seeing a duopoly emerge with $GRAB leading the way.

2

17

3,228