Joined July 2025

- Tweets 126

- Following 109

- Followers 268

- Likes 674

15 Photos and videos

guitar retweeted

$PFP has unified its four FX resolvers into one which supports $PFP / $KTA pair and all Peregrine Falcon Punk NFT.

Add the resolver address below to your Keeta Personal settings:

keeta_aabdoyva5z5wpnx6a7ebgpwzopbipsbzhuyp5opoj2xro2vska6jjxqip5u62wa

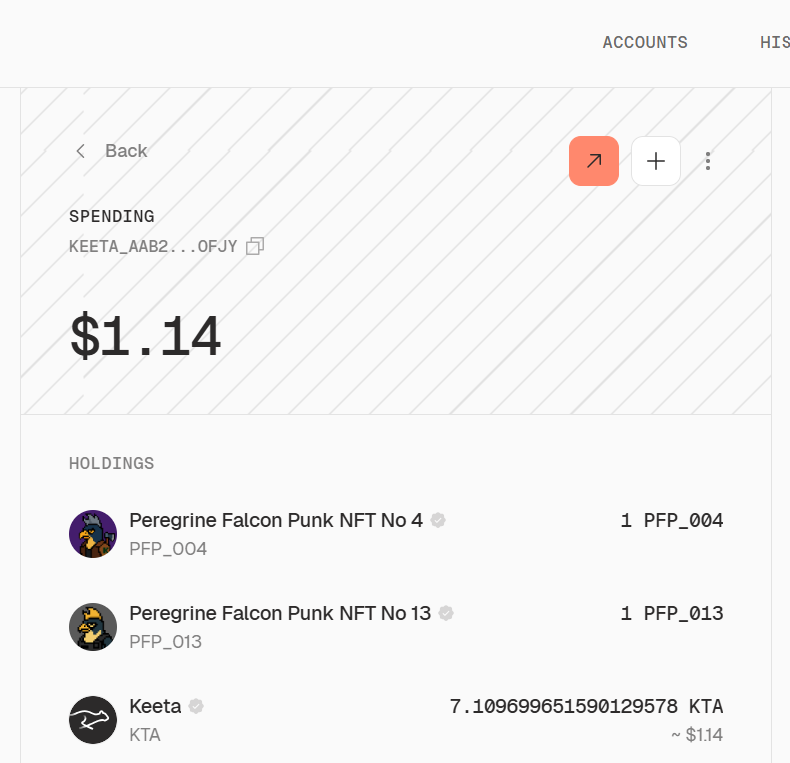

An update on how Keeta Personal looks and works:

PFP NFTs look surprisingly native inside a banking-style account.

$KTA

3

11

374

There’s a sleeping L1 gem everyone is overlooking right now and in the next 5 minutes, I’ll tell you exactly why;

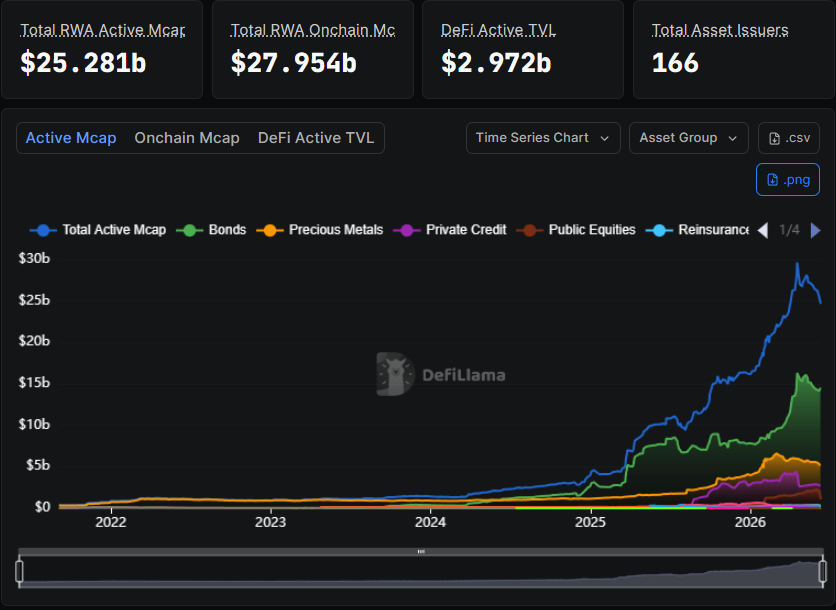

Currently there is only around $27 Billion Dollars of RWAs on-chain across all blockchains.

The Al Nahyan family - the second wealthiest family on Earth with a net worth of around $335 Billion USD - controls approximately 6% of the world's oil reserves through the Abu Dhabi National Oil Company, representing roughly $8.46 Trillion USD in oil wealth alone.

They also produce approximately 4.5 million barrels per day, generating something in the range of $120–130 billion USD in annual gross revenue.

It is this family that Keeta $KTA has entered a joint venture with through ASK Group @askgroupae, founded by H.H. Sheikh Ahmed Bin Sultan Bin Khalifa Bin Zayed Al Nahyan.

In a bear case where Keeta only manages to tokenize just ONE % of Abu Dhabi's reserve value and it eventually finds representation as tokenized assets on Keeta's Network that would roughly $84.6 BILLION Dollars in on chain RWAs.

That's around 3.3x times more than the total market cap of all RWA's today across all chains, and remember that's just in the case that they tokenize JUST 1%.

And this goes far beyond oil. The joint venture includes gold, silver, copper, and a wider basket of Gulf industrial metals. The UAE is already one of the world’s largest commodity trading hubs, with hundreds of billions flowing annually through the Dubai Gold and Commodities Exchange.

It also includes cross-border payments across some of the largest remittance corridors on earth, with the UAE–India corridor alone moving over $20 Billion USD annually. And @askgroupae - linked to the wider royal Al Nahyan family - holds rights to Keeta’s presence across the UAE, the Middle East, India, and Africa.

As of writing this, $KTA sits at just a $100 Million marketcap today - lower than the market caps of some memecoins and dino chains.

Yet the upside scenario people are overlooking is exposure to markets measured in the hundreds of billions and even trillions of dollars.

The deal isn't hypothetical - it's signed, and integration is already underway. Keeta is probably one of, if not the ONLY chain that is able to represent and facilitate this through its tech; Keeta settles transactions faster and at a much larger scale than anyone else, with compliance built into the protocol.

Chains like $XRP have been trying to achieve something similar for the past 14 years, reaching a $200 Billion market cap largely on speculation that they could eventually make it work in some form, somewhere, at some point, somehow. Well, they can’t and their chains will be driven by this same speculation that they could eventually make it work in some form, somewhere, somehow for the next 14 years as well.

Keeta is aiming to accomplish what Ripple couldn’t within a year of its public existence. Now imagine what they will achieve in the next one, two, or five years.

This could end up being one of the biggest opportunities in the market.

Jun 9

(1/9) Keeta and ASK Group @askgroupae, a UAE-based investment group led by His Highness Sheikh Ahmed bin Sultan bin Khalifa bin Zayed Al Nahyan @asknahyan, have created a joint venture aiming to tokenize tens of billions of dollars of commodities and modernize cross-border payments in the Gulf Cooperation Council (GCC) region and beyond, contributing to the UAE's vision and commitment to growth as a global leader in digital finance and real-world asset infrastructure.

29

101

270

24,710

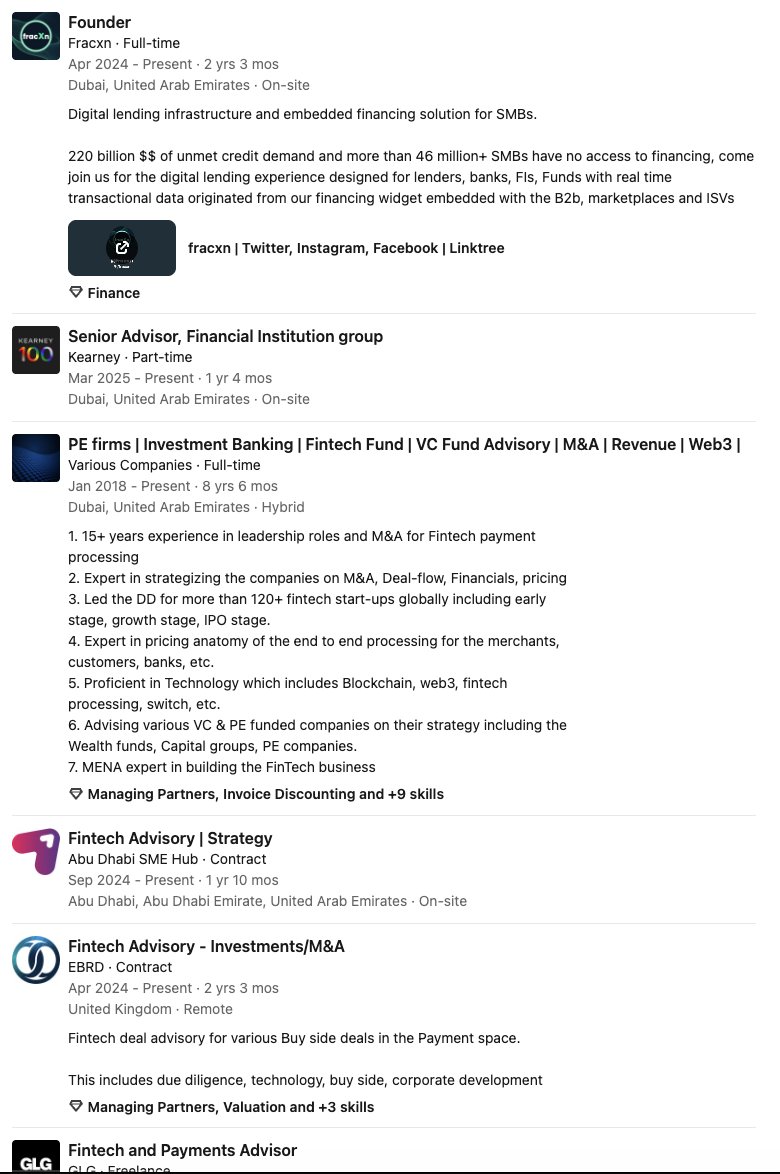

Punit Thakker is the Executive Director of Fintech, Digital Assets, and Blockchain at @askgroupae the group behind $KTA Keeta's joint venture to tokenize Gulf commodities and modernize cross-border payments across the UAE, MEA, and India.

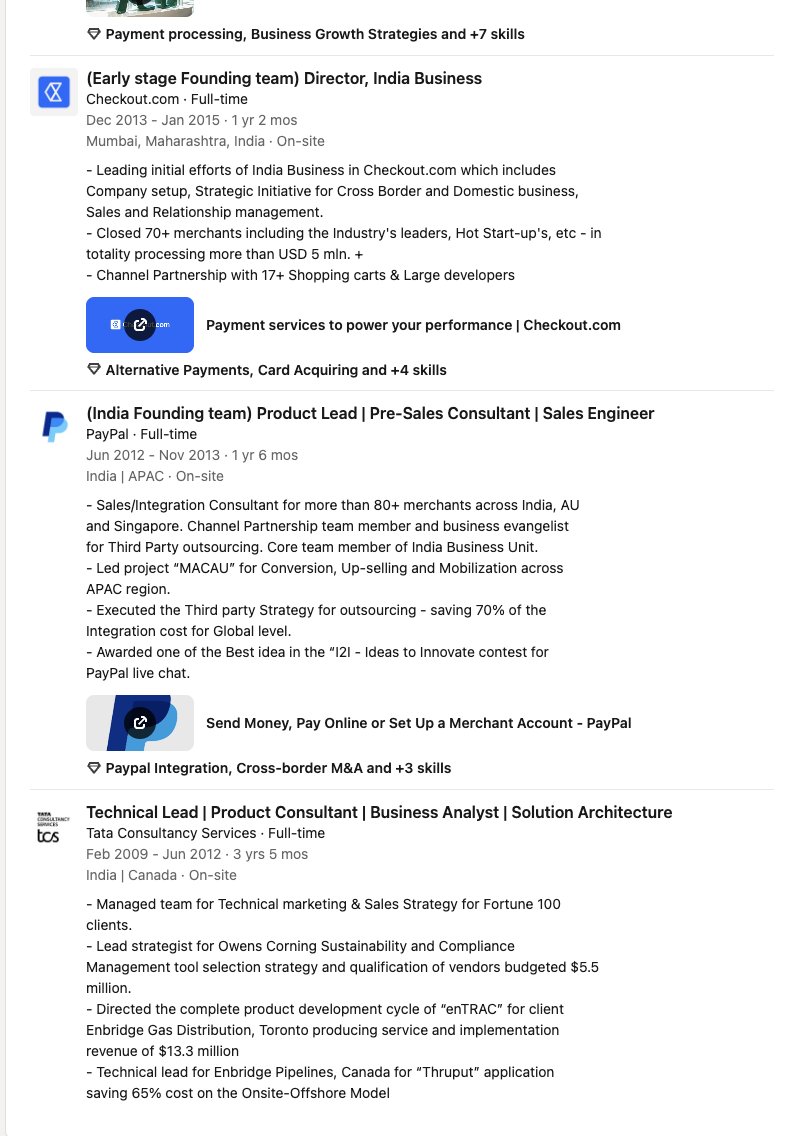

Punit has over 20 years of fintech infrastructure experience across MENA, APAC, and India - with founding team roles at some of the region's most significant payments companies:

- @PayPal India: Part of the team that brought PayPal into one of the world's largest and most complex remittance markets, laying the groundwork for digital payments adoption across the subcontinent.

- @Checkout: One of the most widely used enterprise payment processors globally, built for high-volume, cross-border transactions across financial institutions and merchants at scale who had total of $300 Billion Dollars of total volume of ecommerce payments in 2025 alone.

- @TelrDotCom: A UAE-based payment gateway built specifically for MENA's merchant and e-commerce infrastructure, operating across some of the region's fastest-growing digital economies.

- @PayTabs: A MENA-focused payment solutions provider that became core infrastructure for businesses processing transactions across the Gulf and beyond.

Across all four, Punit was on the ground building culminating in MENA's largest payments switch, processing over $2.6 billion across 28 countries.

Beyond building, Punit advises at the policy level. As Senior Advisor at Kearney FIG, he consults directly with the institutions defining how digital finance moves in the Gulf:

- Central Bank of UAE @centralbankuae

- Dubai International Financial Centre @DIFC

- Abu Dhabi Global Market @ADGlobalMarket

All three on stablecoin regulation and tokenization frameworks.

Now At @askgroupae, he leads the execution of the joint venture with @KeetaNetwork, focused on tokenizing Gulf commodities and modernizing cross-border payment infrastructure across the UAE, MEA, and India, putting Keeta at the center of this institutional push.

Someone with this kind of background isn’t brought in to work on small-scale initiatives, but on market-changing ones. Punit is extremely well connected and has deep knowledge and years of experience in the market, which positions him to help Keeta succeed in its mission both in the region and globally.

Jun 9

(1/9) Keeta and ASK Group @askgroupae, a UAE-based investment group led by His Highness Sheikh Ahmed bin Sultan bin Khalifa bin Zayed Al Nahyan @asknahyan, have created a joint venture aiming to tokenize tens of billions of dollars of commodities and modernize cross-border payments in the Gulf Cooperation Council (GCC) region and beyond, contributing to the UAE's vision and commitment to growth as a global leader in digital finance and real-world asset infrastructure.

20

62

265

15,067

Jun 10

Solana is impressively moving hundreds of millions in 30D RWA flows. @KeetaNetwork partnership with @askgroupae will tokenize billions in RWAs which will allow potentially trillions in monthly asset flow. Keeta's scale is exponentially higher than every network combined.

$KTA

Jun 9

Solana now ranks #1 across all chains at 272.8K holders and #2 chain by RWA Net Flows with $484M in the last 30D

5

17

87

3,265

H.H Ahmed Bin Sultan Bin Khalifa Bin Zayed Al Nahyan On Instagram about the Keeta $KTA joint venture:

''It is a pleasure to begin this journey with Keeta, led by CEO Ty Schenk and supported by former Google CEO Eric Schmidt.

The UAE has always been a place that inspires ambition, innovation, and long-term thinking, and we are proud to play our part in that story. Through this partnership, we look forward to working hand in hand to contribute to the UAE’s vision while helping strengthen cross-border connectivity and unlock the potential of real-world assets through technology.

This is only the beginning, and I am excited for what we can build together for the benefit of our nation and beyond.''

$KTA

11

63

253

9,065

Jun 9

The @KeetaNetwork is on its way to becoming one of the largest global commodities markets in the world by next year. That is a single use case of the network.

Owning $KTA represents a piece of that network.

Jun 9

(1/9) Keeta and ASK Group @askgroupae, a UAE-based investment group led by His Highness Sheikh Ahmed bin Sultan bin Khalifa bin Zayed Al Nahyan @asknahyan, have created a joint venture aiming to tokenize tens of billions of dollars of commodities and modernize cross-border payments in the Gulf Cooperation Council (GCC) region and beyond, contributing to the UAE's vision and commitment to growth as a global leader in digital finance and real-world asset infrastructure.

5

16

101

1,263

guitar retweeted

Jun 9

(1/9) Keeta and ASK Group @askgroupae, a UAE-based investment group led by His Highness Sheikh Ahmed bin Sultan bin Khalifa bin Zayed Al Nahyan @asknahyan, have created a joint venture aiming to tokenize tens of billions of dollars of commodities and modernize cross-border payments in the Gulf Cooperation Council (GCC) region and beyond, contributing to the UAE's vision and commitment to growth as a global leader in digital finance and real-world asset infrastructure.

132

322

921

307,091

Jun 6

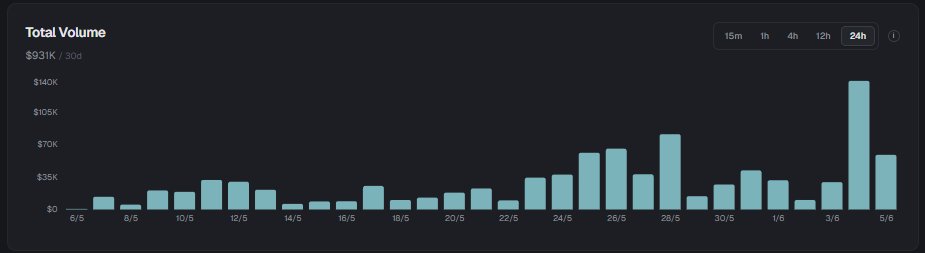

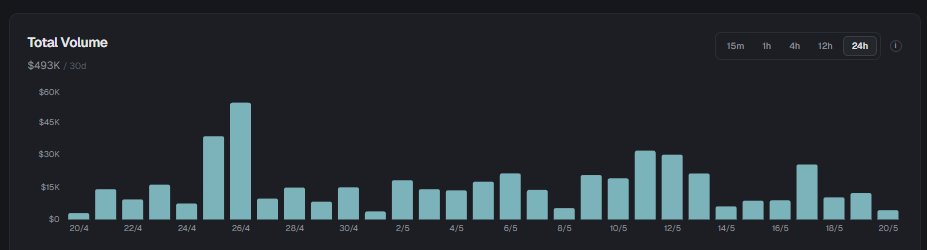

Keeta Personal on @KeetaNetwork $KTA launched ten days ago on May 26, introducing on-chain bank to fiat deposits, withdrawals, and exchanges. Network activity has risen significantly since then and asset flow volume has at least doubled. While there is still tremendous growth potential, the network is now starting to come alive.

Keeta personal launching is one step in a long line of many. I expect to see new anchors, network partners, upgrades, and financial products releasing in the coming months.

Remember: this network has been tested by @googlecloud confirmed to process at least 11m transactions per second. We remain at the beginning stage of an increasingly powerful financial network.

Ten days after KP launch, 30 day asset flow has nearly doubled to $931k, 14 day asset flow has far surpassed my previous May 21 snapshot's 30 day asset flow ($670k current 14 day flow vs $493k 30 day on May 21). These figures show asset flow has more than doubled since KP launch.

Also worth mentioning is that on-chain $KTA is now at an all-time high (7.4m), signaling an increased demand to use the token to interact with the network.

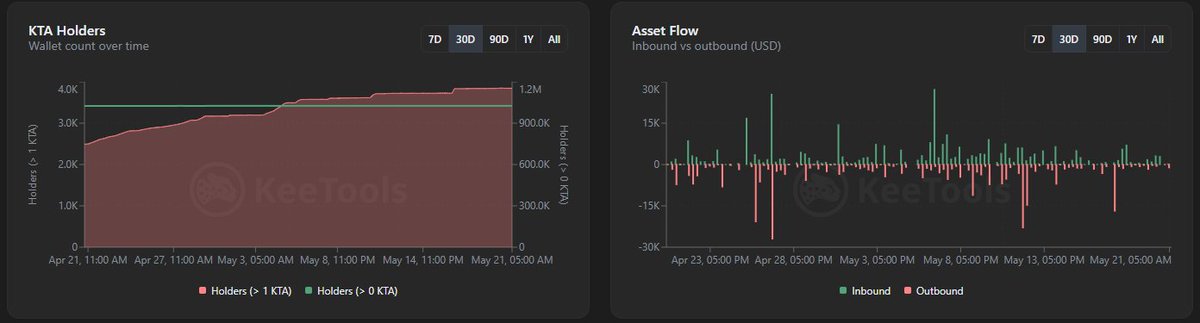

May 21

The metrics I'm focusing on with respect to the Keeta Personal launch are on asset flow and network use. Right now Keeta network is doing about $500k in asset flow per month over roughly 3,850 accounts. Will be interesting to see how these metrics change in the coming months.

8

30

141

6,353

guitar retweeted

Jun 5

Others bolt compliance on. We didn't have to.

RWAs need verified ownership, real currency rails, and liquidity nobody controls. On Keeta, that's on-chain architecture, not an add-on.

The real-world assets that Wall Street ignores are getting a home.

alpacadex.com/rwa/

6

17

54

6,029

guitar retweeted

I think we’re entering a very interesting phase for Keeta.

For the longest time, the conversation was centered around whether the team could actually deliver.

Could they launch the network?

Could they build the products?

Could they connect banking and blockchain in a compliant way?

Could they support digital fiat, cross-border payments, and real financial infrastructure?

Today, those questions are becoming harder and harder to ask.

Keeta Personal is live.

Digital fiat is live.

Multi-currency accounts are live.

ACH is live.

Visa Direct is live.

At some point the conversation shifts from “can they build it?” to “who will use it?”

The iOS app is expected soon and should make onboarding significantly easier, but I think the more important question is what comes after that.

More partners?

More payment corridors?

Institutional adoption?

New financial products?

The foundation is now in place.

The next phase is seeing what gets built on top of it.

If the past year has taught me anything, it’s not to underestimate this team’s ability to execute.

@KeetaNetwork $KTA

6

24

138

2,757

I think you're judging Keeta as if it's already at the end state, when it's still proving out the infrastructure layer.

A few points:

• Keeta Personal isn't the core product. It's the proof that the rails actually work.

• Tokenized KYC by itself isn't revolutionary. Agreed. What's important is that identity, fiat, FX, cards, accounts, permissions and settlement are all being connected on a single network architecture. Most projects talk about this. Keeta is showing it.

• Saying the fiat tokenization is arbitrary ignores what comes next. The value isn't the token itself, it's what tokenized fiat enables: programmable payments, instant settlement, compliance-aware transfers, FX, treasury management, tokenized assets, and cross-border movement without fragmented intermediaries.

• "It's just Bivo and Visa Direct" is like saying Stripe is just a wrapper around banks. The value is the orchestration layer. Infrastructure companies win by connecting systems that don't naturally work together.

• On utilization: every network starts with low usage. Amazon had no merchants. Stripe had no payment volume. The question is whether the rails can support scale once demand arrives. Keeta was literally designed around that problem, with identity, permissions, tokenization, atomic swaps and high-throughput settlement built into the base layer.

• As for token value, that's a fair debate for any infrastructure network. But network utility is not limited to today's fee revenue. The question is whether institutions, applications, assets, payment providers and liquidity providers eventually settle through the network. If they do, token demand looks very different from today.

• The "wrapper" argument also misses the bigger picture. Keeta isn't trying to replace every bank, FX provider or card network. It's creating a common settlement layer that lets them interoperate.

The real question isn't "how much volume does Keeta have today?"

The real question is:

"Has anyone else actually demonstrated identity, tokenized fiat, FX, banking rails, card rails, permissions and compliance infrastructure working together on a purpose-built financial network?"

So far, very few have. That's why people are paying attention.

2

3

13

352

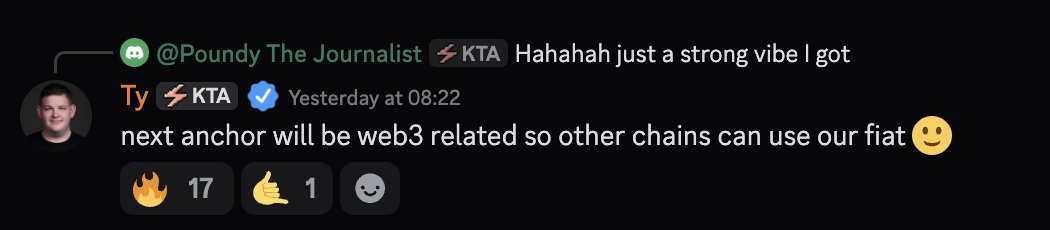

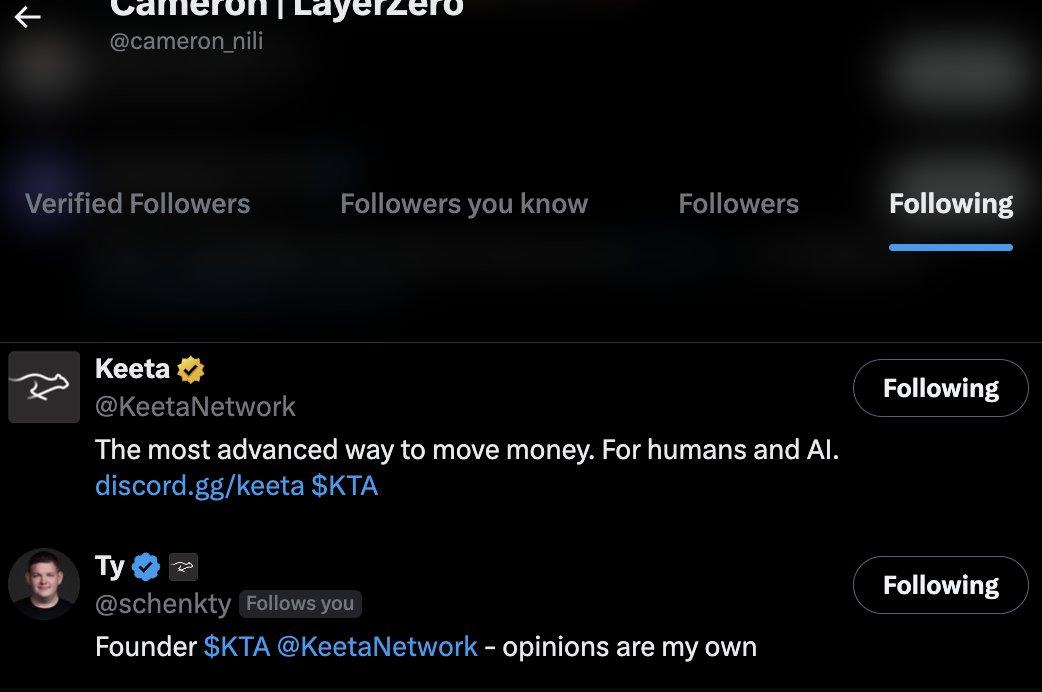

Ty mentioned that the next Keeta $KTA anchor is Web3-oriented, and in a recent Space he noted that a product often compared as a competitor to Keeta is looking to integrate with them.

Cameron Nili, Banking and Capital Markets Lead at LayerZero, also appears notably interested in Keeta following multiple Keeta-related accounts, interacting with them.

Little bit about LayerZero: LayerZero is a cross-chain messaging protocol that lets different blockchains like Ethereum, Base, Solana, and others communicate directly with each other.

Instead of building separate apps for each chain, developers can use LayerZero to create a single "omnichain" app that works across all of them simultaneously, and tokens built on its OFT standard can move natively between chains without the risks of traditional bridges.

LayerZero has processed hundreds of millions of cross-chain messages and is integrated with 70 blockchains, making it one of the most widely deployed interoperability protocols in crypto.

On top of that, there's a little not known piece of alpha: one of Keeta's engineers previously worked at LayerZero (name will be withheld, as it isn't publicly documented).

Just food for thought and nothing concrete but seems interesting.

May 30

Nicely put, loving this framing between push vs pull.

8

33

155

13,000

Keeta put 9 of the most popular fiat currencies on its blockchain

These tokens are like your Revolut or PayPal balances but fully onchain with all the benefits:

Programmable currency swaps, third party wallet apps, cheap off ramps..

And you actually own your own money

$KTA

May 30

Full banking details, fast international transfers, crypto management, and much more.

Have you tried Keeta Personal yet?

8

32

163

6,896

guitar retweeted

May 30

Full banking details, fast international transfers, crypto management, and much more.

Have you tried Keeta Personal yet?

33

103

426

33,230

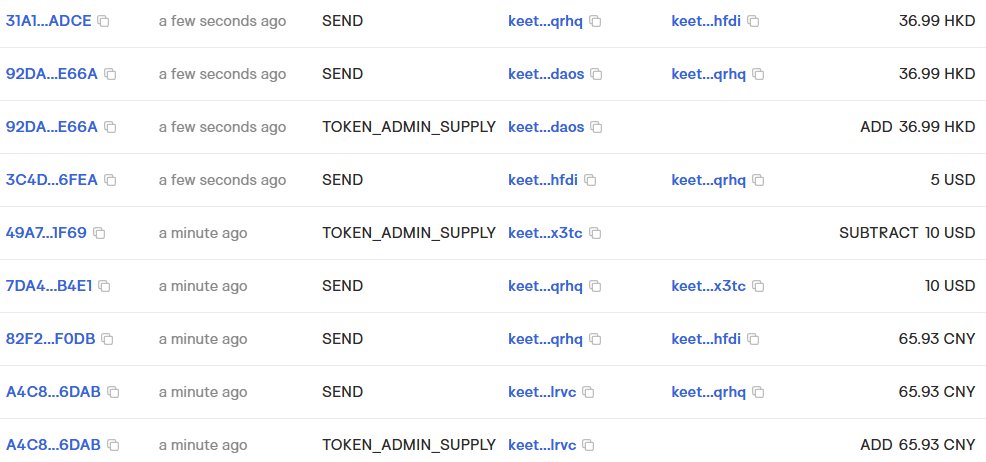

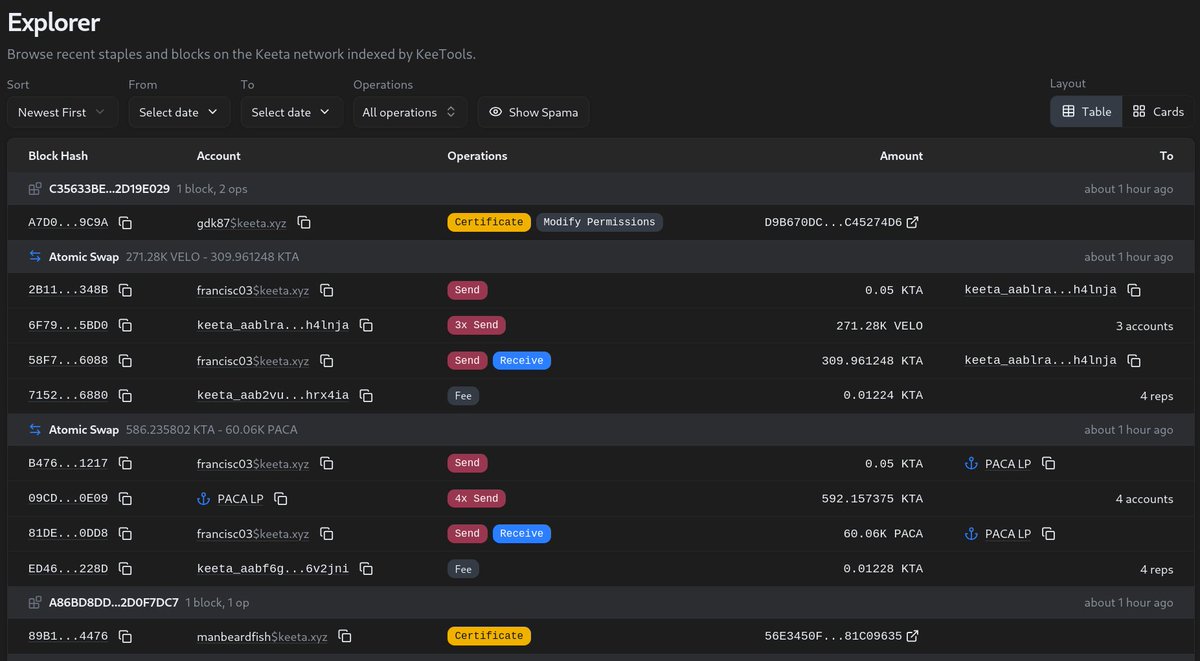

Keeta Personal went live and KeeTools now supports usernames!

Browse all claimed usernames and find accounts by username. Usernames are now also displayed by default instead of addresses. Prefer seeing raw addresses? Just disable username resolution in the settings.

keeta:native

1

12

55

1,688

guitar retweeted

An update on how Keeta Personal looks and works:

PFP NFTs look surprisingly native inside a banking-style account.

$KTA

This is how the $KTA Wallet handles routing.

By default it selects the Best Rate, while still letting you compare all available quotes.

Very curious to see how Keeta Personal evolves this concept.

Could it eventually become the best place to swap fiat currencies?

1

5

79

4,654

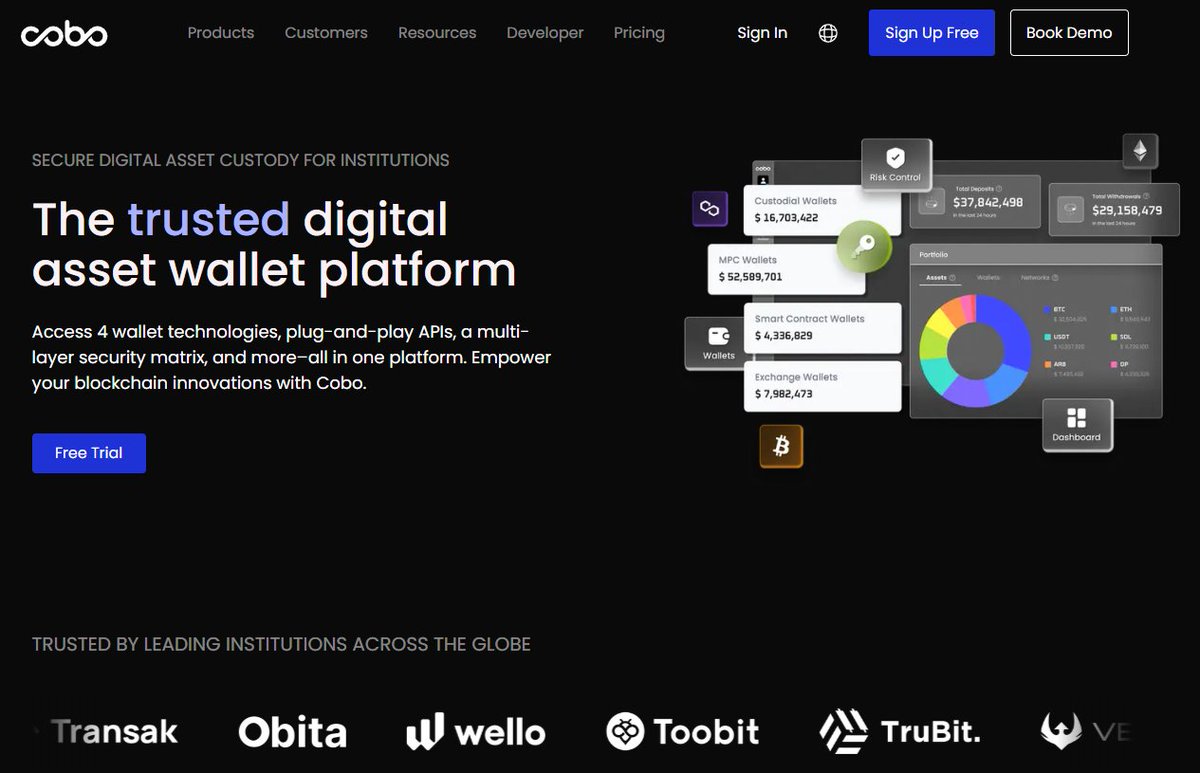

Something I stumbled on completely by accident.

I was doing some AI agentic testing yesterday, running through keeta:native's infrastructure, checking what is live, what connects, what does not. And then I landed on keeta.com/agents.

Right there, sitting in the agent wallet section, was Cobo. Not mentioned in any announcement. Not hyped by the team. Just quietly sitting there, already integrated.

You can verify it yourself right now. Cobo has a dedicated Keeta page live at cobo.com/assets/keeta-agenti… and Keeta is listed there by name. The GitHub repo for the entire infrastructure stack is public at github.com/CoboGlobal/cobo-a…, Python and TypeScript SDK, MCP server, agent framework integrations, all open and available today.

So who exactly is Cobo?

Cobo is not a small side project. They are one of the most serious wallet infrastructure companies in the space, Singapore-based with deep institutional reach across Asia and China. They service exchanges, funds, and financial institutions at scale. Their product is custodial wallets, MPC wallets, smart contract wallets, and exchange wallets all in one platform. Billions in assets under management.

But their newest product is the one that caught my attention. The Cobo Agentic Wallet is built specifically for AI agents, not for humans. Instead of giving an agent unrestricted access to funds, you create what Cobo calls a Pact, a delegation agreement that defines the intent, execution plan, spending policies, and completion conditions. The agent operates autonomously within those boundaries. It can send payments, manage treasury, execute transactions, and it does it all without exposing private keys or requiring manual approval on every move.

Now think about what Ty said recently,

"My AI project has a Keeta wallet and is accessing all the different rails through the SDK. Theoretically you could create an agent that sends an invoice, accepts a payment, and then does something based on that. It is all available today."

That is exactly what Cobo's Pact system is designed for. And it is already inside Keeta's official agent infrastructure.

Ty has been clear that Keeta's real business is not Keeta Personal. The core product is the SDK. The goal is to go two, three vendors deep and replace the infrastructure that the brands you already know are built on, without those brands or their customers even realising it. Cobo already sits inside institutional crypto infrastructure across Asia. If Cobo integrates Keeta rails into their agentic wallet stack, every institution, fund, and fintech that builds on Cobo automatically gets Keeta underneath. That is not one partner. That is an entire ecosystem of downstream customers flowing through a single integration.

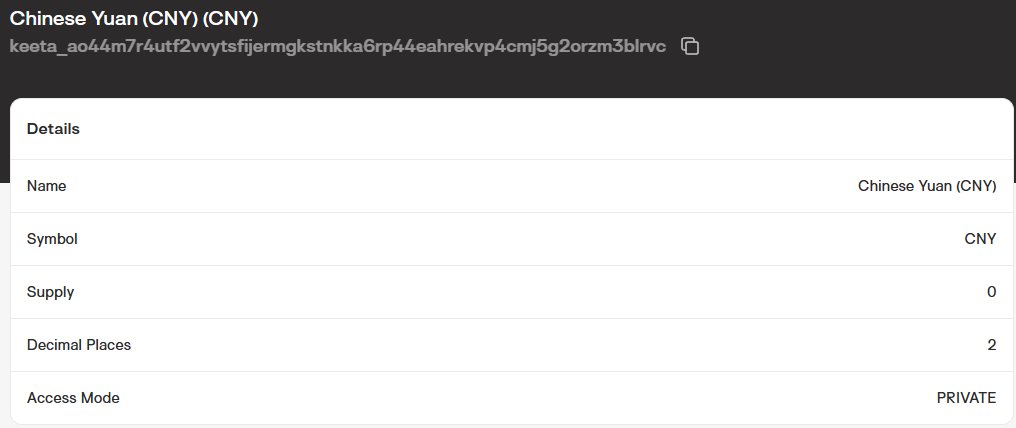

Cobo is headquartered in Singapore with deep institutional roots across Asia and China. The Chinese Yuan is already one of the eight live fiat currencies on Keeta Personal today.

Is this the top secret mission? Probably not. Is this the out of the blue announcement Ty teased? Maybe not that either. But this could be exactly the project Ty has been quietly building on the side, the AI agent with a live Keeta wallet, built on Cobo's infrastructure, already running on mainnet.

Nobody announced this. Nobody made a post about it. I just found it by accident while building. Draw your own conclusions.

cobo.com/assets/keeta-agenti…

github.com/CoboGlobal/cobo-a…

youtu.be/xcwB3ufsGuA

@KeetaNetwork @schenkty @Cobo_Global keeta:native

21

35

132

8,693