Jun 14

DGAF

Feelings aren't a fin. investment 4 an ROI. It thrives onl reciprocity.

ROI's nice, but thing is, it not urs 2control. The ROI is on person & they can choose not 2share "platform".

Reciprocity is where u want it—mutual effort & care.

If not there, u're better off if YDGAF.

8

Jun 14

For the ultra-russophobic warswine criminals nato€Reich ukranistan is the most important territory of the ur-fascist blood cult imperialist €Reich they greedily want 2control.

Russia will nuke the west of it and the €rats may then grab that polish Hungarian Ukro part of it.

113

Maybe u should havepaid 4 a therapist instead 2discuss ur sex addict genital obsessions 2control all in ur deviant sex fantasies -control freak try destroy career as cant control

Another- i fear whoeveru date is also controlled and gaslighted-let me guess u got flying monkeys 2?!

46

When a client constantly dictates to a professional how to do their job, it means a lack of faith in the professional's expertise, leading to micromanagement behavior where the client tries 2control every aspect of the work instead of relying on the professional's judgment. – JPT

17

When a client constantly dictates to a professional how to do their job, it means a lack of faith in the professional's expertise, leading to micromanagement behavior where the client tries 2control every aspect of the work instead of relying on the professional's judgment. – JPT

20

STARMER SHUMER SHEINBAUM MARK CARNEY

MILLIONS MORE

CHEW INSTALLED FRAUDS

IN ALL YTS GOVTS

YT ORGANIZATIONS

YT INSTITUTIONS

2CONTROL YTS PSYOPS TRICK US SCAM YTS MAIM US ROB US DESTABILIZE US

GET US INVADED BY BILLIONS OF BIOWEAPONS

'RRAPED GENOCIIDED POISONED REPLACED

Jun 10

George Floyd protests = GOOD ✅

Vs.

Belfast protests = BAD ❌

Keir Starmer clearly hates white people. 🇬🇧

13

Liar« Hilaria Baldwin »also lied @nypd at my trial 2gain sympathy by playing the victim 2gain fame money.

Nothing stop this narcissist from lying 2control narrative even if her lies on oath are criminal felonies/perjuries (punishable of many years of jail)

She’ll continue 2lie

1

37

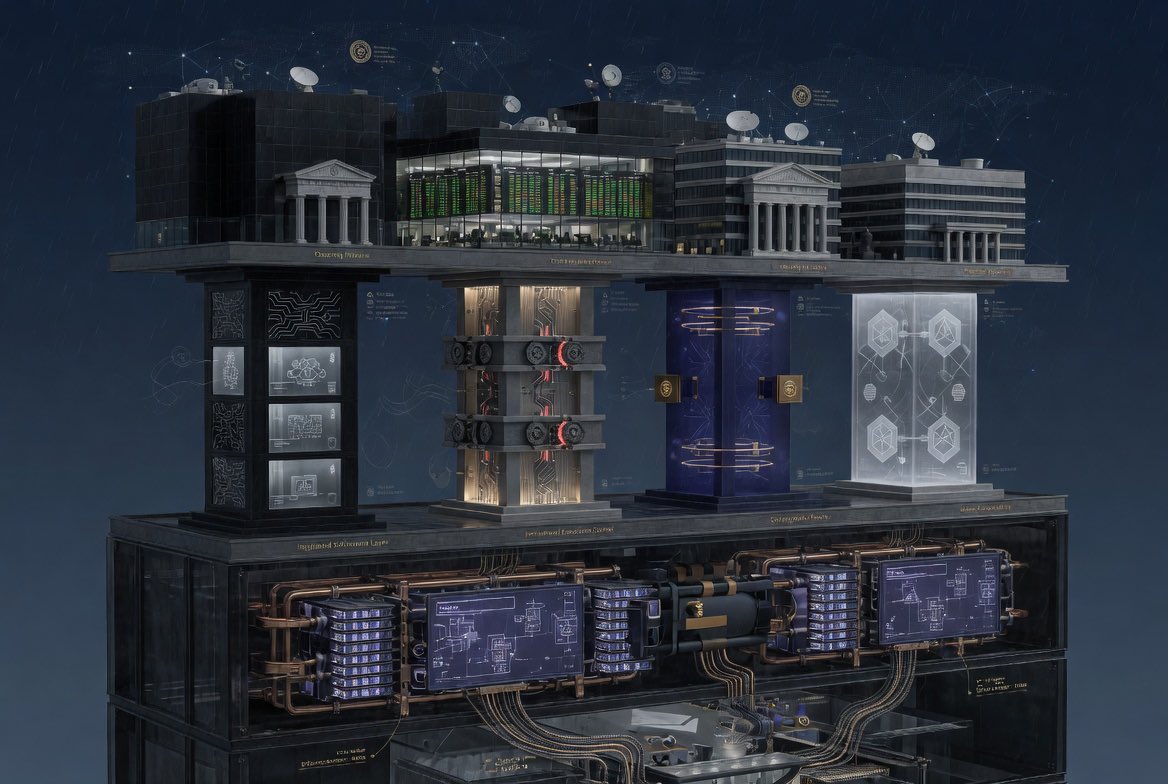

Institutional settlement does not fail because of throughput

It fails because of architecture.

A regulated bank needs four things at the same time:

1Privacy

2Control

3Finality

4Interoperability

Miss one, and the system breaks.

Privacy:

No bank executes on infrastructure where counterparties can observe positions, flows, or strategy.

This is not preference.

It is regulation, fiduciary duty, and basic market structure.

Control:

Institutions need role-based permissions, selective disclosure for auditors, and infrastructure they can operate within governance constraints.

Finality:

Settlement cannot rely on multi-day uncertainty.

Capital markets already run on deterministic settlement assumptions.

Interoperability:

Tokenized deposits, funds, custodians, and payment systems cannot exist in silos.

Institutional finance compounds through connected balance sheets.

This is why @zksync’s current deployments matter.

Not as partnership headlines.

As proof that production architecture is converging.

Deutsche Bank’s DAMA 2.0 platform (Memento) is already deployed in production.

ADI Chain is live with First Abu Dhabi Bank, the Central Bank of the UAE, BlackRock, Mastercard, and Franklin Templeton.

Cari Network is currently onboarding five U.S. regional banks representing $600B in combined deposits, with production rollout planned for later in 2026.

BitGo custody is integrated with Prividium.

Different institutions.

Different jurisdictions.

Different roles in finance.

Converging on the same ZK settlement architecture.

The important question in 2026 is not who has the loudest narrative.

It is who already solved the constraints institutional finance actually cares about.

2026 is not the year banks “try blockchain.”

It is the year they choose rails.

That decision rarely gets revisited.

JPMorgan’s Kinexys has already processed $1.5T on blockchain infrastructure.

DTCC is advancing SEC-cleared tokenized Treasuries.

NYSE, BNY, and Citi are building tokenized securities rails.

This is no longer experimentation.

It’s architecture.

And architecture compounds.

In settlement infrastructure, being first matters differently than in consumer tech.

Why?

Because migration costs are exponential:

• Technical -> years of integration

• Regulatory -> re-audits, re-attestation

• Counterparty -> institutions settle where counterparties already are

Every new participant increases the cost of choosing a competing rail.

SWIFT didn’t win because it was trendy.

It won because once enough institutions connected, not joining became more expensive than joining.

The same logic applies to onchain settlement.

10 institutions create 45 settlement corridors.

100 institutions create ~5,000.

Network density compounds faster than narratives.

93% of tokenized U.S. assets already settle on Ethereum rails. The open question is not whether institutions move onchain.

It’s which infrastructure becomes the institutional standard for privacy, interoperability, and settlement finality.

This is where @zksync matters.

Institutional adoption requires more than throughput:

-> Ethereum security

-> privacy-preserving architecture

-> scalable settlement

-> compatibility with regulated finance

ZKsync already has live and announced institutional deployments.

That lead matters.

Because in financial infrastructure, standards are rarely declared.

They emerge from whoever solves the hard problems first.

82

2

103

1,424

May 20

Pay4play

Is there any other way 4 her 2CONTROL NARRATIVE

& PPLREACTIONS?

1

4

24

This isn’t about Labour this is about a global agenda 2control food production. It’s about time those of us that want 2come out the other end of this start telling it how it really is &stop pushing the illusion that voting makes a difference. None of them are coming to save us!

Keir Starmer has been personally warned – in no uncertain terms – that his brutal inheritance tax raid on British farmers would drive some to suicide. The devastating policy, which hits family farms with eye-watering bills on land and assets passed down through generations, was flagged directly to him as a guaranteed path to despair and death in the countryside.

His response? Cold, calculated, and delivered in that slick lawyerly tone we’ve all come to expect: he simply did not care.

This wasn’t hearsay or exaggeration. It was a direct confrontation with the human cost of his government’s war on rural Britain, and Starmer shrugged it off like it was just another inconvenient statistic. Subhuman indifference from a man who claims to lead the country with “compassion.” Farmers – the backbone of our food security, our landscapes, our self-sufficiency – are being treated as cash cows for the Treasury while their livelihoods are destroyed and their mental health ignored.

And here’s the truth the Westminster bubble hates: the seething contempt ordinary people feel for Starmer isn’t manufactured by the media. It’s not some tabloid conspiracy or far-right narrative. It’s a perfect mirror image of the contempt Starmer himself holds for the British public. He views hardworking farmers, families, and communities as nothing more than revenue sources to fund his failing promises and bloated state machine. No empathy, no understanding, no respect for the people who actually keep the nation fed.

This is the same Starmer who lectures us about fairness while hammering the very people who produce our food. The same leader whose government prioritises net zero targets and migrant hotels over saving family farms from bankruptcy. The mask has slipped completely. Britain’s farmers are in crisis, and the man at the top has made it crystal clear: your suffering doesn’t register.

The public isn’t fooled. This level of cold-hearted arrogance is why trust in Labour is collapsing faster than their economic forecasts. Enough is enough. Farmers deserve better. Britain deserves better than a Prime Minister who looks at potential suicides and says he doesn’t care. 🇬🇧

1

2

18

May 17

This is what you do 2control free speech &stop the spread of important information RIGHT BEFORE MIDTERM ELECTIONS &THE RULING PARTY REPUBLICANS ARE TANKING IN E.THG So @elonmusk the soon 2b trillionaire wants to trample on what MAGA said he was the savior for

34

94

5,471

May 15

Can u please properly label these viruses &start calling them the midterm virus. Anybody who can critically think understands what u guys are trying to do by stoking fear in the public. Folks in fear are easier 2control. It won't work. We don't believe u,u need more people.🤡

1

4

162

May 8

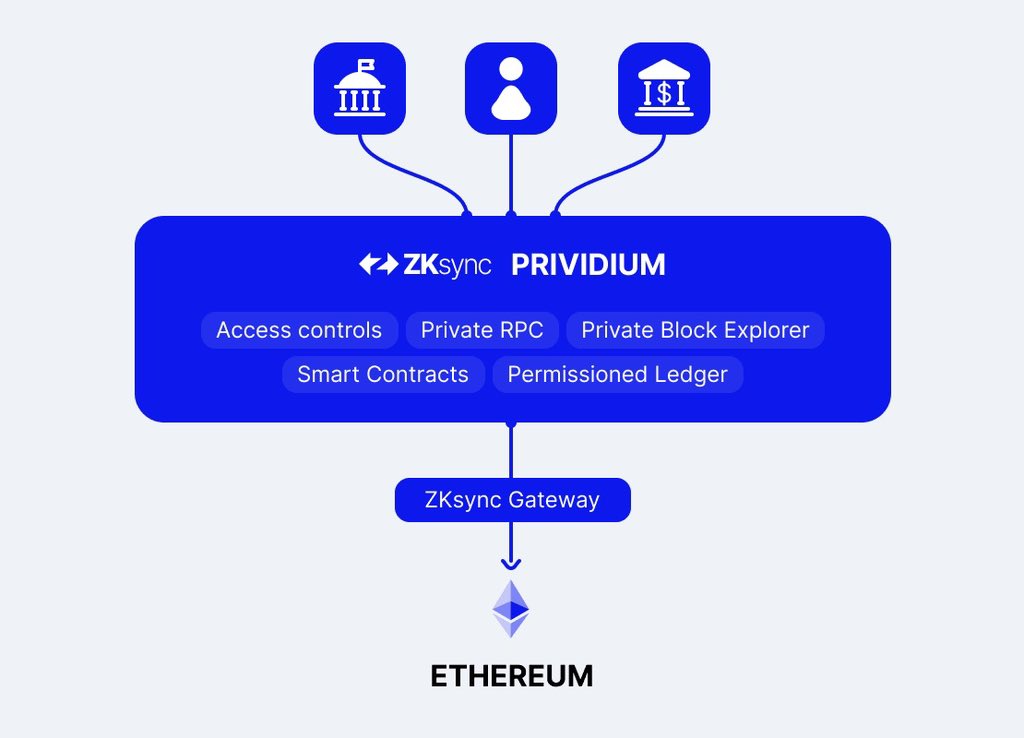

Why Institutions Need Prividium

Global finance still runs on infrastructure designed long before the internet existed. Correspondent banking alone traps nearly $27 trillion in pre-funded capital across the world. Global deposits have crossed $100 trillion, while annual transaction volume now exceeds $3.7 quadrillion. Despite the scale, the system remains fragmented, slow, and incredibly inefficient.

The move toward onchain finance isn’t ideological anymore. It’s practical.

Institutions want faster settlement, better capital efficiency, programmable coordination, and systems that remove unnecessary friction at global scale. That’s the direction the market is moving, and @zksync is building the settlement infrastructure designed to support it.

The problem is that most public blockchains still don’t meet institutional standards.

Banks and regulated entities need four things at the same time:

1Privacy — sensitive transactions can’t live fully exposed on a public ledger.

2Control — institutions need execution environments aligned with internal policies and regulatory requirements.

3Verifiability — every action must be cryptographically provable without relying on trust.

4Connectivity — seamless access to counterparties, liquidity, and the broader Ethereum ecosystem.

Most blockchain architectures can satisfy maybe two or three of these requirements. Very few can deliver all four together.

That’s where Prividium comes in.

Prividium is a permissioned ZK Chain built on the ZK Stack. It operates as a Validium, meaning execution and transaction data stay offchain inside institution-controlled environments, while zero-knowledge proofs and state commitments are published to Ethereum.

That structure gives institutions something they haven’t really had before:

• Private execution environments for regulated financial activity

• Role-based permissions and operational control

• Selective disclosure for auditors and regulators

• Ethereum-level cryptographic verification without sacrificing privacy

• Direct connectivity to Ethereum liquidity and counterparties while inheriting Ethereum’s security and finality

And the network effects here are important.

Every institution added to the network increases the number of potential settlement corridors exponentially — similar to how SWIFT and Visa became more valuable as participation grew. The bigger the network becomes, the more useful and interconnected it gets for everyone inside it.

At the end of the day, institutions aren’t adopting blockchain because of ideology. They’re adopting infrastructure that finally delivers privacy, control, verifiability, and connectivity at the scale global finance actually requires.

Prividium is built for that transition.

What do you think is still the biggest barrier preventing institutions from fully moving to onchain settlement?

12

2

80

7,477

I'm obsessively in love wiz U my Jonty

I insanely love U my Jonty

I'm intensely missing U my Jonty

I dangerously need U my Jonty

It takes all of me 2control my possessive nature over U my love 😅😅😅

2

7

I ♥️my life, my heirs & Divine Sovereignty. Ur obsessed w/me & I do 🙏 this stops.The World has watched this sinister plot putting a stain on our American values & Dreams which make us powerful bc of our Global Culture Art Scene U& the 🌎envy & want 2control & not elevate art.🇺🇸

1

1

6

Apr 20

If u think my 1st movie was about how *amazon* wants 2control ur time, as opposed to how capitalists in general are exploiting us- and how we need to organize on the job, its only cuz the media made u think amazon was the bad capitalism&other capitalists were the benign ones.

10

42

1,689

21,760

Now I have 2hire an attorney 2stop them.

It seems both the power & the cellular companies are implementing a global agenda 2control humanity.

All of these frequencies have real health implications.

Just cause you don’t see it doesn’t mean they’re not harmful.

Fight back!!!

2

2

68

Good morning Mick i saw a while ago the N Trust had got their orders! I wonder why the cult would want 2control them? Land &property maybe? Who’s booking a visit 2a stately home this w/e? No me neither. Quiet day 4me &eve of Friday! Best day of the week🤣 have great day🌞☕️🐾🤗😘

1

3

28

Mar 23

Propoganda in full swing!U know she's Zionist by all D lies comming out of her mouth!Israel never withdrew in 2005!Israel continued 2control D majority of what entered&exited D territory(land,sea,and air),which prompted many international bodies 2still consider it occupied Land!

163

Mar 17

@1cor127

👑🤴🏻

Thank U Sis for letting me use ur 💬 as a platform for conversation or 2 put some scriptures out there 2 🤔 on, so that many can read & know that we are on God's side. Not trying 2control their life. just trying 2❤️our Neighbors as we❤️God. The 2 Greatest Commands

1

1

2

16