Not aibased basic crypto scam lol 😂 😂 they show u every time cos panicked screeeeee just let him like Harry hay Lee tough ain't he pre op give him some coins

1

1

58

Jun 10

corporations already get most of their funds from the public sector, this just means more of it goes directly to aibased startups

41

May 25

🔥 全网首发!From Zero to GenLayer:解锁区块链的“终极AI大脑” 🧠✨

如果你以为Web3还只是“发币、质押、搬砖”那套老剧本,那你就快奥特了!

2026年加密圈最狂野的赛道是什么?毫无疑问是 AI Web3。而在这个赛道的绝对风口上,坐着一个被称为“智能合约终结者”的革命性项目—— @GenLayer !

💡 什么是 GenLayer?(用大白话讲)

传统的智能合约(比如以太坊)就像是一个“死板的计算器”,只能处理 If-This-Then-That 的确定性逻辑。它看不懂新闻、读不懂推特,更没办法做复杂的逻辑推理。

而 GenLayer 创造了世界上第一个 “智能资产协议(Intelligent Asset Protocol)”!它把大语言模型(LLM)直接缝合进了区块链的共识层。

一句话总结: 以前的合约是“盲目的代码”,GenLayer 的合约是“会独立思考的AI代理(AI Agents)”。

它能做什么?

📰 自动读取推特和新闻,根据现实世界的舆论风向执行DeFi策略。

⚖️ 充当去中心化的“AI法官”,自动仲裁复杂的现实纠纷。

🎮 创造拥有自主意识、会自己升级赚取收益的Web3游戏NPC。

是不是已经燃起来了?别当围观群众了,今天这篇教程手把手带你 From Zero to Hero,光速打入 GenLayer 生态核心!

🚀 搞钱/搞事情第一步:新手速通三部曲

想要成为 GenLayer 的早期骨干,拿到未来不可言说的“超级红利”,立刻死磕以下三步:

第一步:加入“情报大本营” 📡

项目刚红,信息差就是生产力!

立刻关注官方推特:@GenLayer(开启小铃铛,随时蹲测试网和空投线索)。

冲进 Discord 社区,在 #general 频道里发一句:“Just arrived from the future! Ready to build with GenLayer! 🚀” 混个脸熟。

第二步:极客/开发者速通(生态最肥的肉!) 💻

如果你懂一点点代码,或者对AI Agent感兴趣,GenLayer 简直是你的天堂。他们推出了独创的 Simulator(模拟器) 和 BHev 语言。

🛠️ 打开官网开发者专区: 体验他们的“智能合约浏览器”。

🤖 编写你的第一个 AI Contract: 哪怕只是让AI合约每天帮你自动抓取推特上最火的Memecoin,你也是走在时代前沿的开发者!

第三步:成为“布道者/显眼包”(社区贡献者) 🗣️

不懂代码?完全没关系!GenLayer 目前极度渴望社区声量:

在推特/小红书/Mirror 撰写关于 GenLayer 的分析。

制作趣味 Meme 图(比如:传统智能合约 vs GenLayer AI合约)。

积极参与社区的社区会议(Community Calls),拿到专属 Role(身份组)。

🧐 互动时间:测测你的“脑洞指数”

GenLayer 的魅力在于想象力没有边界。如果让你用 GenLayer 的“AI智能合约”来做一件事,你会选哪个?(在评论区留下你的选项,或者写下你的神级脑洞👇)

疯狂指数

A AI 渣男/渣女鉴定合约:自动抓取社交媒体互动,分析对方是不是海王,是就自动扣除质押金。⭐⭐⭐⭐

B 疯狂预测市场:让AI实时阅读全网新闻,自主判断“明天某名人会不会上头条”并自动结算。⭐⭐⭐⭐⭐

C 24小时无休的AI基金经理:完全根据推特情绪和链上数据,自主帮你调仓的小助手。⭐⭐⭐⭐⭐

💥 冲!别等主网爆发了才拍大腿!

Web3 过去十年在做“去中心化计算”,而 @GenLayer 正在开启“去中心化智能”的新纪元。种一棵树最好的时间是十年前,其次是现在。

现在就去关注 @GenLayer,加入这场科技海啸!

#GenLayer #AI #Web3 #IntelligentAssets #Crypto2026 #AIBASED #智能合约 #区块链新物种

1

2

154

May 20

🚀🎨 Welcome to the Future of Digital Creation 🎨🚀

Your imagination deserves more than just a screen — it deserves permanence on the blockchain. 🌐⛓️

Introducing $AIBased — where creativity meets ownership.

A new era where anyone can transform ideas into timeless, AI-powered on-chain art in just seconds. ⚡🖼️

No complicated process.

No waiting.

No limits.

Simply create, mint, and own your masterpiece forever. 🔥

Whether you're an artist, collector, builder, or visionary — this is your moment to step into the future of NFTs and decentralized creativity. 🌍💎

✨ Why $AIBased?

🎨 AI-Powered NFT Creation

⚡ Fast & Seamless Minting

🔒 Secure On-Chain Ownership

🌐 Built For The Next Generation Of Creators

🚀 Community Driven Vision

Every mint becomes a permanent piece of blockchain history.

Every creation becomes uniquely yours. 🧠✨

The digital art revolution has already started…

Now it’s your turn to leave a mark. 🖋️🔥

💠 Mint Today.

💠 Own Forever.

💠 Create Without Limits.

🔥 $AIBased is LIVE NOW 🔥

📜 Contract Address (CA):

0x643428b9A17917148e527Ef8B22c85924e96Eb76

#NFT #AI #Crypto #Web3 #Blockchain #NFTCommunity #DigitalArt #Ethereum #AIBased #OnChain #NFTArtist #DeFi 🚀

36

7

171

21,551

May 20

Turn your ideas into timeless, on-chain art.

Simple. Fast. On-chain.

Mint your NFT today and own your creation instantly.

$AIBased is live.

CA: 0x643428b9A17917148e527Ef8B22c85924e96Eb76

44

56

1,569

May 20

Unlock your creative power with AiBased.

✨ Generate, mint, and showcase your art on-chain with your prompt.

🧠 Turn ideas into art in seconds.

💎 Your art, your journey, your legacy

Let’s build the future of AI art together 🌐✨

25

35

1,227

May 6

Punjab to roll out AI-based ‘smart cleanliness’ drive under Suthra Punjab

nation.com.pk/06-May-2026/pu…

#punjab #PM #AIbased #suthrapunjab

35

Happy weekend to everyone

Key Base Ecosystem Updates (May 2, 2026)

cbMEGA Launch: cbMEGA is now live on Aerodrome, Rainbow Wallet, and CoW Swap to enable smoother access to MegaETH ecosystem on Base

Performance: The Base ecosystem token market cap is roughly $1.25B with 496 listed cryptocurrencies.

Network Status: No outages are reported for the Base mainnet

Ecosystem Growth: Focus is expanding into AI Agents (AI Agent Arena) and Gaming (AIBased)

Top Performers & Activity: While general market sentiment shows some volatility, projects like Brett remain popular as a cultural icon on the chain

@base

@baseposting

3

18

93

Apr 6

ಡ್ರೋನ್ ಲೋಕದಲ್ಲಿ ರಷ್ಯಾ-ಅಮೆರಿಕಾಗೆ ಸಡ್ಡು ಹೊಡೆಯಲು ನಿರ್ಧರಿಸಿರುವ ಭಾರತ, ಇದೀಗ AI ಆಧಾರಿತ, ಕಡಿಮೆ ವೆಚ್ಚದ ಡ್ರೋನ್ ಗಳನ್ನು ಅಭಿವೃದ್ಧಿಪಡಿಸಲು ಮುಂದಾಗಿದೆ.

#armedforces #Divyastradrone #AIbased

kannadaprabha.com/nation/202…

1

1

66

Mar 29

Base = ucuz hızlı eğlenceli kazançlı bir blockchain.

Ethereum’da 10-20 dolar ödeyeceğin şeyi burada 1 kuruşa yapıyorsun.

Yeni başlayanlar için en dost canlısı ağlardan biri.İstersen “Base’te ilk 100 dolarla ne yapayım? diye özel rehber de hazırlayayım.

Veya Hangi uygulamaları önce deneyeyim? diye liste vereyim.Base Ekosistemi:

Kolay Anlatımlı Rehber 2026 Güncel Base, Coinbase’in Ethereum üzerine kurduğu bir Layer 2 (L2) blockchain. Basitçe söyleyeyim:

Ethereum’un çok pahalı ve yavaş hali yerine, süper ucuz (çoğu işlem 1 kuruş bile değil) ve süper hızlı (saniyeler içinde biter) versiyonu.

Düşün ki Ethereum ana yol, Base ise yan yol ama aynı güvenlikte ve herkesin rahat kullandığı bir yol. Coinbase cüzdanıyla direkt bağlanıyor, yeni başlayanlar için en kolay blockchain’lerden biri.Base’te tam olarak neler yapılabilir? (En popüler şeyler)

Kripto Al-Sat (DEX’ler)Aerodrome Finance → Base’in en büyük borsası (Uniswap gibi).

Uniswap, Sushi Swap da Base’te var.

Memecoin’leri (Brett, Toshi gibi) alıp satabiliyorsun.

Çok düşük ücretle saniyede işlem yapıyorsun.

Para Kazan (DeFi – Yield Farming)Likidite sağla → komisyon ödül kazan (Aerodrome’da çok popüler).

Borç ver / borç al → Seamless, Aave gibi platformlarda faiz kazan.

Stablecoin’le (USDC) düşük riskli kazanç elde et.

Birçok kişi Base’te “pasif gelir” yapıyor.

NFT Mint & TradeZora, Magic Eden gibi platformlarda NFT bas (yap) ve sat.

AI ile otomatik NFT üreten uygulamalar var (AIBased gibi).

Sanat, koleksiyon, oyun item’leri… hepsi Base’te.

Sosyal Medya Kazan (SocialFi)

Base App (base.app) → Instagram Twitter Cüzdan bir arada!Post at, like yap, sohbet et, ticaret yap ve ödül kazan.

Farcaster gibi on-chain sosyal uygulamalar.

Oyun Oyna ve Kazan (Gaming)On-chain oyunlarda item alıp sat, oynadıkça kazanç elde et.

Düşük ücret sayesinde micro-ödüller bile mantıklı.

AI Ajanları ile Otomatik İşlemlerAI ajanlar kur → cüzdanını yönetsin, trade yapsın, NFT bassın.

Yeni trend: Kod bilmeden AI ile para kazanmak.

Gerçek Hayatta ÖdemeUSDC ile kahve al, arkadaşına para gönder (saniyede, 1 kuruş ücretle).

Base App ile her şey tek yerde.

Başlamak çok kolay (5 dakikada hazır olursun)

Cüzdan kurCoinbase Wallet (en kolayı) veya MetaMask indir.

Para yatırCoinbase’ten direkt Base’e USDC/ETH gönder (ücretsiz).

Veya Base Bridge’den Ethereum’dan köprüle (resmi köprü).

Base App’i dene (base.app)Giriş yap, cüzdan bağla → hemen post at, trade yap, kazanmaya başla.

#base

2

1

3

15,544

Mar 20

Rafa AI Rafa Finance)A big, wise, and bright mentor bird imparts knowledge to little owlets. This is a perfect metaphor for how this project works from complex financial algorithms to easy-to-understand steps for every user.

To understand how to go from small to big with Rafa AI, let's delve into the essence of the project and development strategy.

What is Rafa AI?

@RAFA_AI is a modern AIbased platform designed for investment and asset management. Its main mission is to democratize complex financial instruments. What was previously only available to Wall Street hedge funds is now available to the average user thanks to smart agents.

How does it work?

The project uses a multi agent system. Imagine that you have a whole team of analysts working for you:

1. Trend analyst: monitors the market.

2. Risk assessor: tells you when it is dangerous.

3. Strategist: chooses the best moment to enter.

Development path: From small to large

To really advance in this ecosystem and learn to earn/grow, you should follow a clear algorithm.

1. The Owlstage: Learning and basics

In the picture we see an owl with notebooks. This is the first step.

• Education: Don’t try to invest large amounts right away. Learn how AI tips work.

• Testing: Use the platform to analyze small portfolios. Understanding why AI gives this or that advice is more important than the advice itself.

2. The Adaptationstage: Using agents

Once you understand the basics, start delegating. Rafa AI allows you to customize agents to your goals.

• Personalization: Choose your style aggressive growth or stable capital preservation.

• Data analysis: AI processes gigabytes of information in seconds. Learn to interpret these reports to make your own decisions.

3. Mastery Stage: Strategy Building

This is the level of a big bird with blueprints in hand.

• Automation: Set up the system to work for you 24/7.

• Diversification: Use Rafa AI to find hidden opportunities in different sectors Cryptocurrencies, stocks, DeFi.

Next will be Rafa Ai…

6

49

345

Session 8: Preventive Measures – Man Overboard at the Fleet Safety Review Seminar 2026, organised by the Directorate General of Shipping, focused on strengthening onboard safety practices to prevent, detect, and effectively respond to man overboard (MOB) incidents.

The session was delivered by Capt. Anish Joseph, Deputy Nautical Advisor–cum–Senior Deputy Director General (Tech./Maritime Security/IT & E-Governance), DGS, who highlighted the rising trend of MOB and missing-person cases, key contributing factors such as fatigue, complacency, poor deck conditions, and environmental influences, as well as data showing increasing incidents over recent years.

Preventive measures shared included vigilant watchkeeping, proper use of safety gear, improved deck lighting and guardrails, and deployment of modern technologies such as AISMOB transmitters, PLBs, RF tracking systems, thermal detection cameras, and AIbased alert systems.

#DGShipping #FleetSafetyReview2026 #MaritimeSafety #SeafarerSafety

5

403

Feb 24

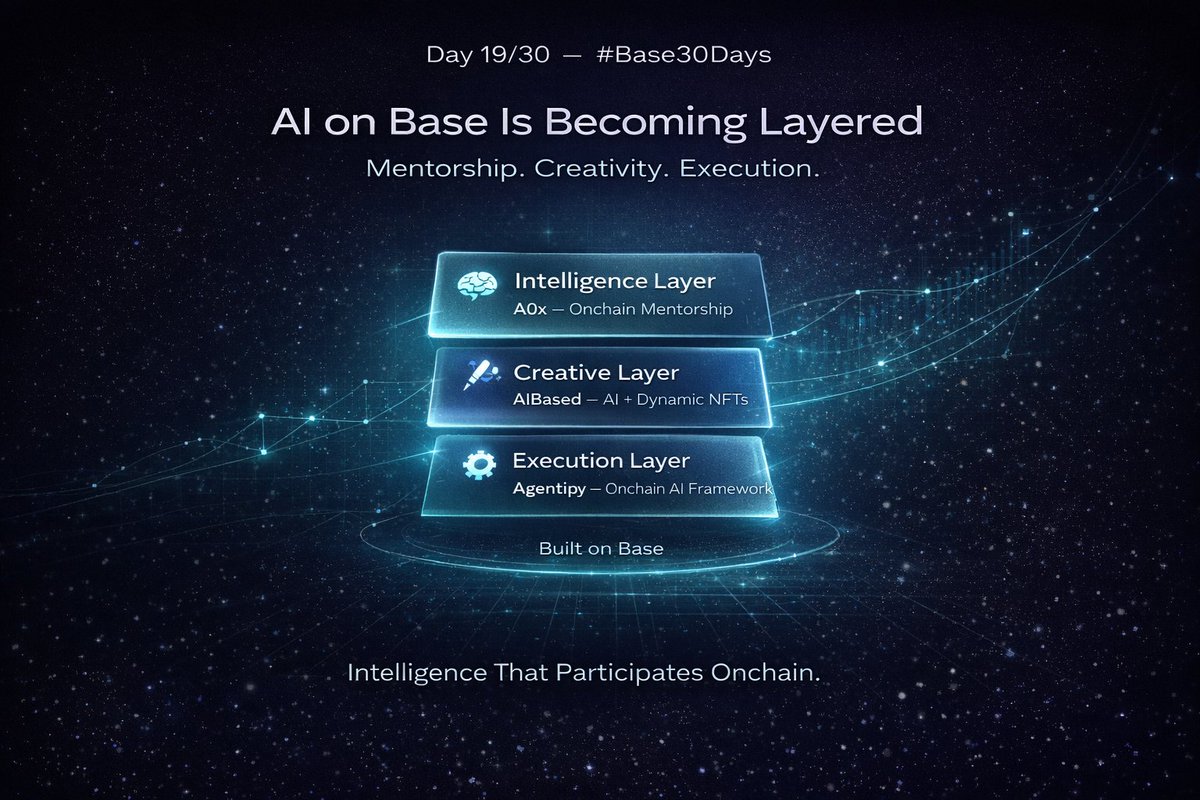

Base quietly stacking the full AI agent flywheel: mentorship (A0x)

creation (AIBased)

execution (Agentipy).

Not just tools, it’s becoming infrastructure for an onchain intelligence economy.

The real flex is how low fees coupled with Coinbase rails make all three actually usable at scale.

Day 19 already feels like a map of tomorrow

1

3

38

Feb 24

The Pattern Emerging

Look at the structure forming:

• A0x → AI mentorship & cognitive leverage

• AIBased → AI-powered creative ownership

• Agentipy → AI execution tooling

Different verticals. Same direction.

AI on Base isn’t just hype cycles and token launches.

It’s quietly forming a layered economy: Intelligence. Ownership. Execution.

And Base with low fees and Coinbase onboarding provides the distribution layer to make this viable at scale.

So here’s the real question:

If AI agents can mentor, create, and transact on-chain…

What role is left for us?

Tomorrow (Day 20): We shift gears social tipping & engagement mechanics inside Base App.

Let’s keep building.

13

42

Feb 24

Two Different Lanes: Creative AI vs Execution AI

Now contrast that with AIBased and Agentipy.

AIBased lives in the creative layer.

Generate AI visuals → Mint dynamic NFTs → Let them evolve onchain.

It merges generative AI with ownership. Not “AI art on a website.” But assets that settle and trade on Base.

Then there’s Agentipy the developer layer.

An open Python framework that allows AI agents to execute onchain actions:

Swaps. Transfers. DeFi strategies. Protocol interactions.

This is where AI stops being conversational and becomes operational.

It’s the difference between: “Here’s what you should do”

and

“I’ve already executed it.”

That’s infrastructure.

1

11

57

Feb 24

Day 19/30: Other AI Agents on Base A0x, AIBased, Agentipy for Onchain AI

We’ve spent the last few days talking about AI agents on Base.

Launchpads. Tokenization. Autonomous revenue.

But here’s the bigger picture:

An ecosystem isn’t defined by one protocol.

It’s defined by layers.

Infrastructure. Creativity.

Mentorship. Execution.

And that’s exactly what’s forming on Base right now.

Today we’re stepping beyond Virtuals to look at three projects building very different but equally important parts of the onchain AI stack:

A0x.

AIBased.

Agentipy.

Three angles.

One emerging reality: AI that doesn’t just assist it participates.

Let’s unpack it.

Feb 23

Day 18/30: Virtuals Protocol AI Agent Launchpad: Create & Monetize Bots on Base Virtuals Protocol @virtuals_io

What if your next startup… wasn’t human?

Not a team. Not a founder. Not a CEO. An AI agent.

On Base, people aren’t just using AI.

They’re launching AI businesses.

Welcome to Virtuals Protocol.

Virtuals is basically a launchpad for AI agents.

But not the “chatbot in your bio” type.

These agents:

• Trade

• Run subscriptions

• Offer services

• Interact onchain

• Generate revenue

And here’s the wild part, They’re tokenized. Meaning people can co-own them.

An AI agent becomes an investable, revenue-generating entity.

21

2

28

557

Feb 24

RNIT AI Solutions Ltd rolls out AI-based FRS for Education Department in Lakshadweep

#RNITAISolutions #AIbased #FacialRecognition #AttendanceManagementSystem #EducationDepartment #Lakshadweep

equitybulls.com/category.php…

4

268

Feb 3

Full Comment:

"Roblox has seen DAU, engagement, and bookings growth accelerate over recent quarters as AI-powered search & discovery improvements have supported a variety of global viral hits such as Dress to Impress, Grow a Garden, and Steal a Brainrot. Additionally, strategic investments aimed at creating a more vibrant economy and improving app performance have led to accelerating user activity and monetization in key international growth markets. However, shares of RBLX have been under pressure since the company’s Q3 earnings report despite this operating momentum, as the company provided cautious FY26 commentary on the call regarding (1) uncertainty for the potential impact on short-term engagement from its implementation of AIbased facial age estimation technology for all users on the platform in order to use chat functionality, and (2) the potential for a y/y decline in margins as the company ramps its infrastructure investments to support heightened engagement levels and ongoing product innovation aimed at genre diversification. We expect Roblox DAU will grow 70% y/y to 145M in Q4, well ahead of consensus but down 6.2M sequentially due to typical seasonality. We forecast 58% y/y Global GBV growth and 50% y/y net revenue growth in Q4, both well ahead of consensus and the upper end of the guidance ranges, as the aging up of the user base and deeper engagement with an increasingly diverse & complex set of experiences fuels robust monetization. Our covenant adj. EBITDA estimate for $597M in Q4 is also well ahead of expectations, with operating leverage from the strong growth offset by greater infrastructure investments. Roblox announced new advertising formats and tools at CES in January as the company looks to continue scaling its advertising platform, including (1) a new premium ad unit embedded on the app homepage that displays video content in an immersive 3D environment, and (2) additional programmatic advertising partnerships, including Amazon DSP, Magnite, and PubMatic."

5

1,040

Jan 30

It was an honor to take part in this campaign and to add Linea as the second official network for AiBased, after Base.

We’ve taken a snapshot of all transactions made by users on the Linea network through AiBased during the Exponent campaign.

A reward will be allocated for eligible users, more details coming soon 👀

Jan 30

Exponent has come to an end.

We’d like to thank every team that built, deployed, and competed.

We're verifying final results and will reach out to winners shortly.

1

2

6

495