Dave Johnson retweeted

Jun 13

Watch/listen to the episode:

YT: youtu.be/jlYmybNvtq0

M : monumentalsportsnetwork.com/…

Art19: art19.com/shows/off-the-benc…

Apple: monsports.net/off-the-bench-…

Spotify: monsports.net/otb-spotify

1

2

4,723

Jun 11

Watch/listen to the full episode which includes plenty more from John Wall:

YT: youtu.be/jlYmybNvtq0

M : monumentalsportsnetwork.com/……

Art19: art19.com/shows/off-the-…

Apple: monsports.net/off-the-bench-…

Spotify: monsports.net/otb-spotify

1

2

4,237

Jun 11

Háganle clases de educación cívica y financiera a este chuchesumadre porfa. El derecho de educación gratuita es para la ed básica y media (art19 de la constitución)

Aprendan sinvergüenzas culiaos si Ud pide un crédito DEBE PAGAR, si no paga, LO EMBARGAN y a llorar a la iglesia‼️

34

Jun 10

Watch/listen to the full episode:

YT: youtu.be/jlYmybNvtq0

M : monumentalsportsnetwork.com/…

Art19: art19.com/shows/off-the-benc…

Apple: monsports.net/off-the-bench-…

Spotify: monsports.net/otb-spotify

2,138

Jun 10

Niezupełnie....

Każdy Vmax dotyczy warunków optymalnych a więc idealnych.

Jeśli nastąpi ich pogorszenie należy dostosować sposób poruszania do możliwości i umiejętności.

Art19 PoRD

4

59

Jun 9

Find Off the Bench on all podcast platforms as well as YouTube and the Monumental app:

M : monumentalsportsnetwork.com/…

Art19: art19.com/shows/off-the-benc…

Apple: monsports.net/off-the-bench-… Spotify: monsports.net/otb-spotify

YT: youtu.be/nso-ElTkBcU

3

2,178

Jun 8

Watch/listen to the latest episode, which also features great insight from draft analyst Matt Babcock:

M : monumentalsportsnetwork.com/…

Art19: art19.com/shows/off-the-benc…

Apple: monsports.net/off-the-bench-…

Spotify: monsports.net/otb-spotify

YT: youtu.be/nso-ElTkBcU

2

3,569

Wo toh visa lagega unko India me aane ke liye aur protest karenge toh Art19 v nahi milega unko🤣

3

90

May 27

INTERCEPT é uma agência de propaganda e contra inteligência do Soros, Soros é narcotraficante internacional. Ele usa Ong's, think tanks como NETLAB, art19, Data Privacy Brasil, Instituto Igarapé,Sou da Paz e etc para implantação dessa agenda dos infernos.

1

2

234

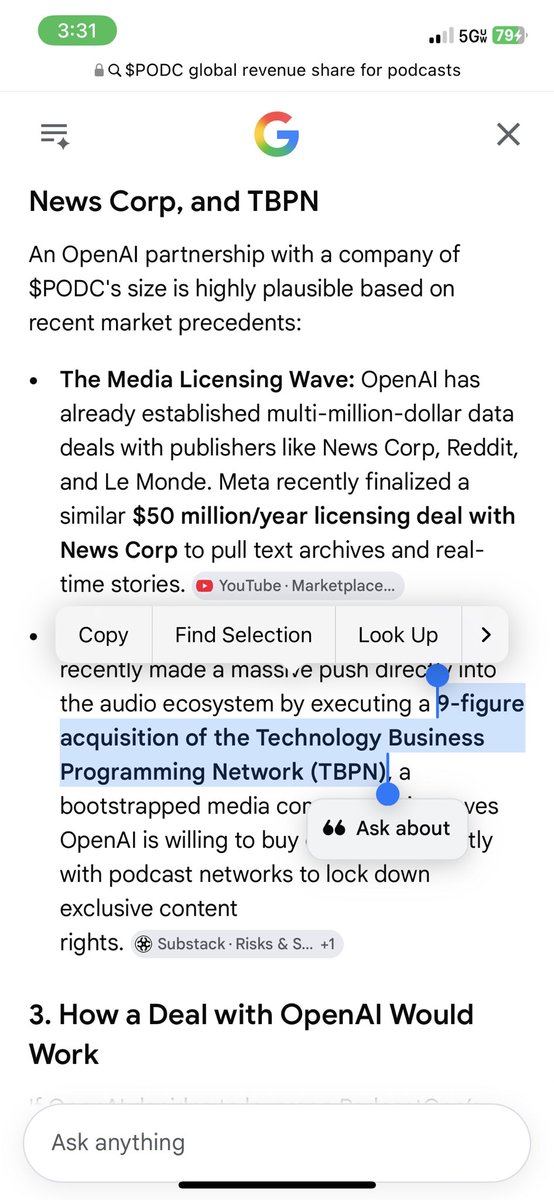

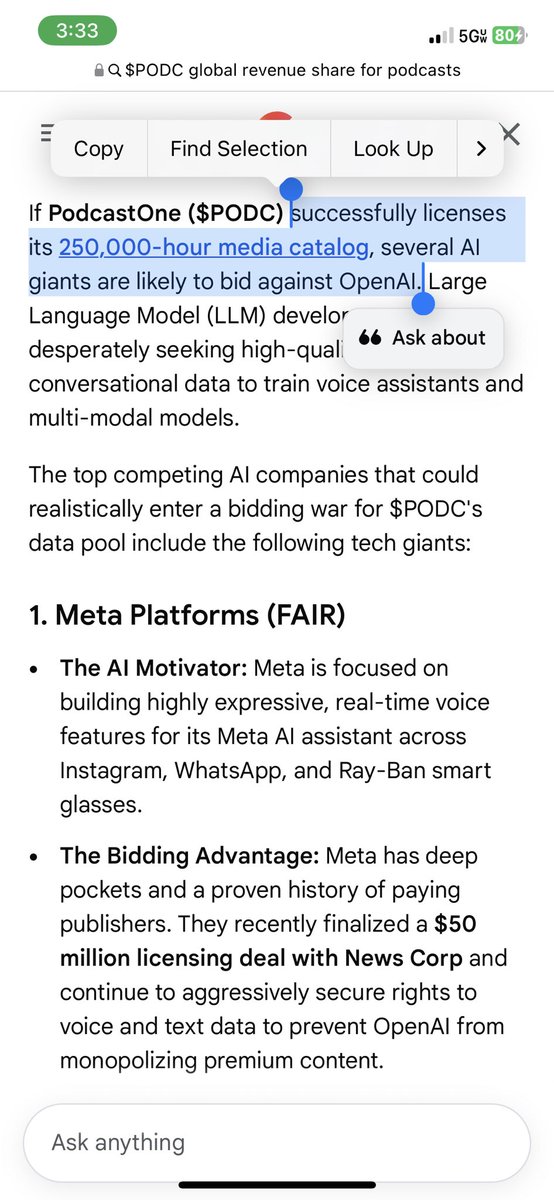

May 27

$PODC

ONLY publicly traded pure-play podcast network in the U.S.

Please repost, bookmark, and subscribe for $1.

One of the most overlooked AI digital media infrastructure stories in small caps.

And the numbers are starting to accelerate rapidly.

Fiscal FY2026 momentum has been massive:

• 9M FY2026 revenue:

$46M ( 21% YoY)

• 9M Adjusted EBITDA:

$4.5M ( 421% YoY)

• Q3 FY2026 revenue:

$15.9M ( 25% YoY)

• Q3 Adjusted EBITDA:

$2.8M ( 516% YoY)

Management has repeatedly raised guidance due to strong execution.

Latest FY2026 outlook:

• Revenue: $68–75M

• Adjusted EBITDA: $7–10M

And unlike many speculative media names, PODC already has major partnerships generating real revenue.

BIGGEST DRIVER:

Amazon ART19 partnership.

PodcastOne moved its entire network onto Amazon’s ART19 hosting monetization platform.

The original deal reportedly carried:

• ~$15–16.5M multi-year minimum guarantee

That later expanded to:

• $20M annual revenue run rate

The ART19 relationship improves:

• dynamic ad insertion

• monetization efficiency

• analytics

• advertiser targeting

• distribution scale

Another major catalyst:

Fortune 250 streaming partner.

That relationship reportedly scaled to:

• $27M annual revenue run rate

Together, those partnerships are powering much of the company’s recent acceleration.

But the real opportunity may be where podcasting, video, and AI all converge.

PODC now operates:

• 200 podcasts

• Top 10 Podtrac network ranking

• 1B monthly impressions

• 4B lifetime downloads

Distribution spans:

• Spotify

• Apple Podcasts

• Amazon

• YouTube

• TikTok

• iHeartRadio

• Samsung TV

• LG

• Pluto TV

• Vizio

• Rumble

• Telly

and more.

This creates a massive monetizable content library.

Video podcast growth is exploding too.

PODC reported:

• 218% YoY increase in video views

across YouTube, Spotify video, TikTok, and other platforms.

That matters because video podcasts unlock:

• higher CPM advertising

• sponsorship expansion

• short-form clip monetization

• broader discovery algorithms

• younger audience penetration

Now add AI.

This is where the story gets interesting.

PodcastOneAI aims to monetize:

• 200,000 hours of premium audio/video content

through:

• AI training data licensing

• LLM monetization

• enterprise data licensing

• media licensing

• government/hyperscaler partnerships

Management specifically highlighted opportunities tied to:

• hyperscalers

• enterprise AI

• media AI

• government AI datasets

Additional AI partnerships include:

• Listener.com

• Gotavi

These partnerships improve:

• AI discovery

• audience targeting

• analytics

• monetization optimization

• cross-platform engagement

• inventory forecasting

$PODC is also expanding through:

• acquisitions

• creator renewals

• TV adaptations

• celebrity partnerships

Examples include:

• Dr. Phil network partnership

• A E renewals

• Varnamtown sold to Paramount

• multiple podcast IP adaptations to TV/streaming

Recent warrant exercises generated:

• ~$5.5M cash inflow at $3/share

Management stated proceeds are targeted toward:

• acquisitions

• AI expansion

• TV/celebrity brand growth

• strategic scaling

Global podcast market projections:

• $80B–$170B long term

• 20–30% CAGR estimates

Key tailwinds:

• podcast ad growth

• video podcast adoption

• creator economy expansion

• AI audio demand

• smart TV distribution

• streaming convergence

• on-demand media consumption

And despite all of this:

PODC remains one of the ONLY direct public market ways to gain pure-play exposure to podcast infrastructure monetization.

Not Spotify.

Not iHeart.

Not diversified media conglomerates.

A direct podcast ecosystem play.

$LVO $SHOP $SPOT $AMZN $RDW $MSFT $GOAI $RDDT $PLTR $NBIS $META $AAPL $NVDA $MU $FUBO $AMC $DIS

#OPENAI $PERPLEXITY #ANTHROPIC

PODC could evolve from a niche podcast network into a broader AI-enabled digital media infrastructure company.

9

6

33

2,773

May 24

En San Luis Potosí hay un Mecanismo Estatal de Protección de personas defensoras de Derechos Humanos y Periodistas. Completamente sometido al @GobEdoSLP inexistente la @CEDHSLP el representante del @CongresoEdoSLP muy contento debe estar @MovCiudadanoMX de que su diputado firme esta complicidad de abuso y represión contra periodistas @AndresCostSLP @MarcoGamaSLP

@Art19 @article19mxca @AlvarezMaynez

@LuisCardenasMx @rivapa @azucenau @J_Fdz_Menendez @CiroGomezL

@GuacamayanLeaks @hdemauleon

9

5

398

May 21

Watch/listen to the full episode, which also includes Drew's thoughts on the draft an interview with Cam Boozer:

M : monumentalsportsnetwork.com/…

Art19: art19.com/shows/off-the-benc…

Apple: monsports.net/off-the-bench-…

Spotify: monsports.net/otb-spotify

YT: youtu.be/A8-hOZDFbvM

1

2

1,274

Amazon Musicもビデオポッドキャスト提供開始👀

Podnewsによると、Amazon Musicが本日、米国のiOSおよびAndroidユーザー向けにビデオポッドキャストの提供を開始したと報道。ビデオはAmazonのART19プラットフォームで開始され、今夏にはさらにパートナーを拡大する予定

#Podcast雑談ニュース

podnews.net/update/amazon-mu…

1

8

632

May 10

Protestant confessions typically distinguish 3 marks of the church (Belgic, 27; cf CofE, Art19; WCF 25):

•preaching the gospel

•administering the sacraments

•church discipline

Open Communion is a failure to exercise discipline and puts people in spiritual danger (1Cor 11:30)

1

3

84

Corrupción En @Audifarma_SA @mutualser_ @casalud_ips En Santa Marta Todos En Concierto Pará Delinquir Evidenciado Con Hechos Hoy 08-05-2026 Niegan Medicamentos Solicitando Autorizaciones Pará Medicamentos Como La Diabetes Solicito Sanción Y Captura Del Regente Alexander. ART19

5

124

118

1,192

Corrupción En @Audifarma_SA @mutualser_ @casalud_ips En Santa Marta Todos En Concierto Pará Delinquir Evidenciado Con Hechos Hoy 08-05-2026 Niegan Medicamentos Solicitando Autorizaciones Pará Medicamentos Como La Diabetes Solicito Sanción Y Captura Del Regente Alexander. ART19

3

4

149

If you own $AMZN, you own:

AbeBooks

Alexa Internet

Amazon Aurora

Amazon Basics (private label)

Amazon Echo

Amazon Elements (private label)

Amazon Essentials (private label)

Amazon Fire TV

Amazon Fresh

Amazon Go

Amazon Kindle

Amazon Marketplace

Amazon Music

Amazon Pay

Amazon Pharmacy

Amazon Publishing

Amazon Robotics (formerly Kiva Systems)

Amazon Studios

Amazon Web Services (AWS)

Annapurna Labs

Art19

Astro (home robot)

Audible

Axio

Beijing Century Joyo Courier Services

Blink Home

Body Labs

Book Depository

BookFinder

Brilliance Audio (Publishing)

ComiXology (Comixology)

Canvas Technology

CloudEndure

Cloostermans

CreateSpace (now part of Kindle Direct Publishing)

Digital Photography Review (DPReview)

Eero

Elastic Beanstalk (AWS product)

Elemental Technologies (AWS Elemental)

Fabric

Fig (AWS)

Freevee (Amazon Freevee)

GlowRoad

Goodreads

Graphiq

Halo (health/wearables brand)

IMDb

IVONA Software

Joyo (Amazon China)

Kindle Direct Publishing

LoveFilm (integrated into Prime Video)

Luna (cloud gaming)

MGM (Metro-Goldwyn-Mayer)

MX Player

Neighbors (community app by Ring)

Nu (investment)

One Medical

PillPack (Amazon Pharmacy)

Pinzon (private label)

Prime Air (drone delivery)

Prime Video

Project Kuiper

Ring

Shopbop

Solimo (private label)

Souq

Thinkbox Software

Treasure Truck

Twitch

Vedaka (private label, India)

Veeqo

Wickedly Prime (private label)

Whole Foods Market

Wondery

Woot!

YES Network (partial stake, ~15%)

Zappos

Zoox (autonomous vehicles)

7

6

90

6,306

Sobre NNyA: Reclutamiento por parte de grupos delictivos.

-Prisión Preventiva Oficiosa #PPO: señala preocupación por la reforma al Art19, que amplió el catálogo de delitos que ameritan esta figura.

-Seguridad: profundización del modelo militarizado de seguridad ciudadana.

1

2

8

335