17h

I decided to wait until clearity on the required 100m financing requirement. Plus that they show some clear plan on how to reach lower AISC and reach their production targets. I might miss the bottom but rather see that my position gain back value.

1

96

Thanks, still looks v undervalued for what they have!

Would you avg on $ASE.V now or you waiting for their next step?

1

1

77

Jun 8

$ASE.v crazy selling, I am still holding, will probably buy more at some point. The ones finding the bottom in this stock can make a lot of money in my view. Uncertainity around when AISC drops and how the required 100m$ equity/debt will be raised make buyers hold back for now.

4

1

22

3,667

May 20

Thank you. Yes $ase.v has been a tough one but I expect it to improve a lot once they hit the higher grades. Also a good example why mining investors need to diversify and have lots of patience.

1

1

1

547

May 19

$ASE.v announces that its recently appointed COO will step in as Acting CEO.

globenewswire.com/news-relea…

May 5

CEO change is next. David Anthony retires on May 15. A formal CEO search is underway; Baird may effectively drive the reset meanwhile and actually take over both roles near term.

1

3

412

May 17

$ASE.V — Asante Gold | Q1 2026 Results

Ghana-focused gold producer running the bibiani and chirano mines — riding a record gold price environment

⛏️ Q1 2026 Highlights (USD):

• Revenue: $300.4M ( 112% YoY)

• Gross profit: $60.5M (vs $6.5M)

• Operating profit: $46.9M (vs -$1.4M)

• Net loss: $(8.3M) — derivative & price-protection losses

• EPS: $(0.01)

🪙 Production & Pricing:

• Gold sold: 62,996 oz ( 31% YoY)

• Gold equivalent produced: 59,803 oz ( 15%)

• Avg realized price: $4,769/oz (vs $2,946/oz, 62%)

• AISC: $3,886/oz (vs $2,971/oz)

• Realized-to-AISC spread: $883/oz

💰 Cash Generation & Capital:

• Operating cash flow: $34.1M ( 78% YoY)

• Capex: $77.7M (heavy mine investment)

• FCF: -$43.6M

• Cash: $62.3M (up from $44.0M)

• Total debt: $334.5M

🏦 Capital Markets Activity:

• Private placements: $140.1M raised

• Settled price protection contracts: $59.7M

• Settled gold streaming: $3.2M

• Equity attributable to shareholders: $126M (from $3.2M at YE 2025 — recap completed)

🔄 Fiscal Year Change:

• New FY end: Dec 31 (changed from Jan 31 in Dec 2025)

• This is the first Q1 on the new calendar

Operational story is excellent — production up, prices way up, OCF more than doubled. but ($30M) in mark-to-market losses on derivatives and price-protection contracts kept the bottom line negative even as gross profit nearly 10x'd. the recap has rebuilt the balance sheet; now it's about converting that into clean earnings.

Full analysis:

investorlens.io/stocks/ASE.V

#TSXV #CanadianStocks #Mining #Gold #Ghana #GoldStocks

2

330

May 16

Good write up on $ASE.v , the turning point should soon come although possible some capital raise before getting listed in Australia.

May 16

$ASE.v reported 1Q26 overnight. Bibiani ramp-up supports total production growth (1Q26 run-rate at 240k oz/year), still no guidance, and several arrangements to boost liquidity were discussed. Below a first look at main items.

1

1

16

3,068

May 16

What's missing is the trajectory of production growth at $ASE.v (guidance). Shall we expect a 2Q26 at 60k or more? That will define whether the cash inflows from gold sales will be more than enough to show that additional debt financing can be sustainable.

2

2

521

May 16

"The May 2026 Waiver requires the Company to raise aggregate funding of not less than $100,000[k] on or before August 31, 2026." Debt or equity. Gold forward agreements are excluded. If the ramp-up is real, I believe $ASE.v can make it without equity.

1

2

334

May 16

$ASE.v "to defer $52,568[k] in settlement payments under the price protection agreements that were previously due on May 4, 2026. The deferred instalment payments and interest will be paid in six monthly payments from July 2026 to December 2026."

1

2

339

May 16

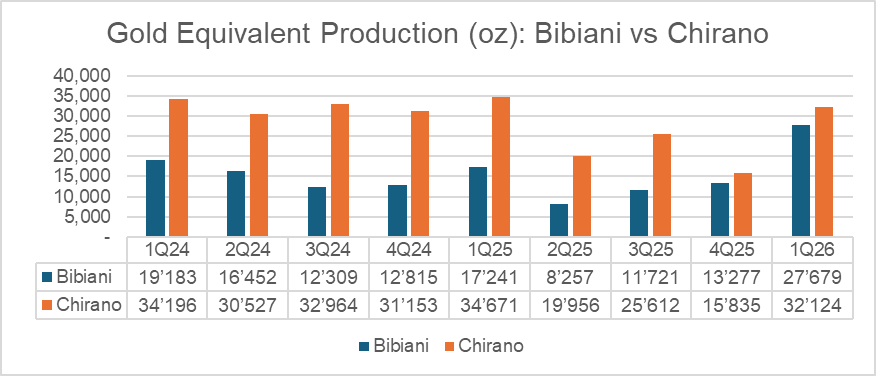

Production of 59.8k Au Eq oz was disclosed thanks to a decent increase at Bibiani. $ASE.v changed end of FY just recently, so past quarters are not directly comparable. AISC are improving as production increase: 1Q26 at US$3,886/oz.

1

2

353

May 16

$ASE.v reported 1Q26 overnight. Bibiani ramp-up supports total production growth (1Q26 run-rate at 240k oz/year), still no guidance, and several arrangements to boost liquidity were discussed. Below a first look at main items.

3

1

5

3,693

May 14

Soma's Q4 report was abysmal. Lots of similarities with Asante ($ASE.v), i.e. overpromising and underdelivering. Like Asante, Soma promised substantial production growth, but failed to deliver. The result: crashing share prices in both cases. I still believe that Asante will ultimately achieve a much higher production level, whether it will be 400 koz per year as guided last year remains to be seen. In the case of Soma, I'm not so sure any more. I think production can increase to a 30 koz annual runrate by the end of this year, but whether the company manages to achieve much higher production numbers as previously guided for 2027 and beyond remains to be seen.

1

3

232