L/S investor. Public markets ideas, turnaround disasters & underappreciated optionality. Occasionally sharing thoughts to exchange views. Not financial advice.

Joined August 2018

- Tweets 128

- Following 90

- Followers 77

- Likes 93

10 Photos and videos

May 19

Governance shift matters. CEO Bernard departing. New chairman Rusckowski (ex-Quest, ex-Philips Healthcare) took over Jun 2025. New CEO expected H2 2026. Board more open to strategic alternatives.

75

May 19

$ASE.v announces that its recently appointed COO will step in as Acting CEO.

globenewswire.com/news-relea…

May 5

CEO change is next. David Anthony retires on May 15. A formal CEO search is underway; Baird may effectively drive the reset meanwhile and actually take over both roles near term.

1

3

414

May 19

“early work reinforces that these assets can deliver materially stronger production than what was achieved in Q1 2026. We will update the market on the outcomes of this review, including key expected output and cost parameters, once a revised operating plan has been finalized.”

1

77

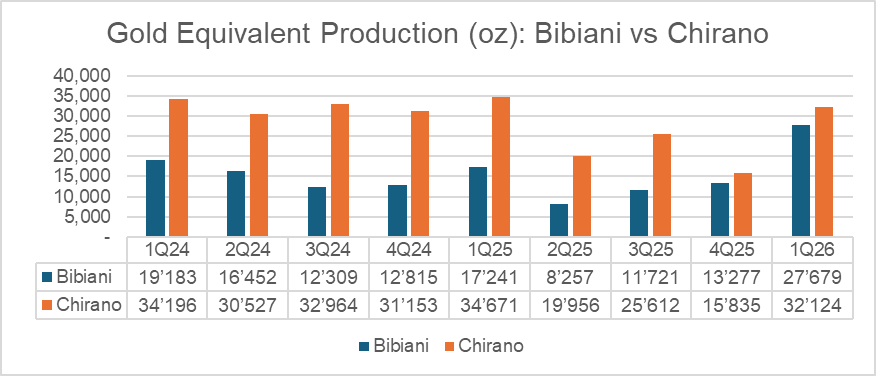

May 16

$ASE.v reported 1Q26 overnight. Bibiani ramp-up supports total production growth (1Q26 run-rate at 240k oz/year), still no guidance, and several arrangements to boost liquidity were discussed. Below a first look at main items.

3

1

5

3,695

May 16

Worth keeping in mind that Bibiani was negatively affected by operational constraints recently (equipment availability, wall slip, slow ramp-up in plant recovery). Forward production might therefore improve quickly vs 1Q26.

1

1

367

May 16

What's missing is the trajectory of production growth at $ASE.v (guidance). Shall we expect a 2Q26 at 60k or more? That will define whether the cash inflows from gold sales will be more than enough to show that additional debt financing can be sustainable.

2

2

523