Found something strange.

#ALGOQUANT.

Algoquant Fintech Ltd

CMP : 56.2

🟢 Promoter holding has gone up from 52% to nearly 74% in last 10 years.

🟢 Consistent 3 years of net profit, at-least 25 Cr.

🟢 2 Years of long consolidation.

So what is strange.

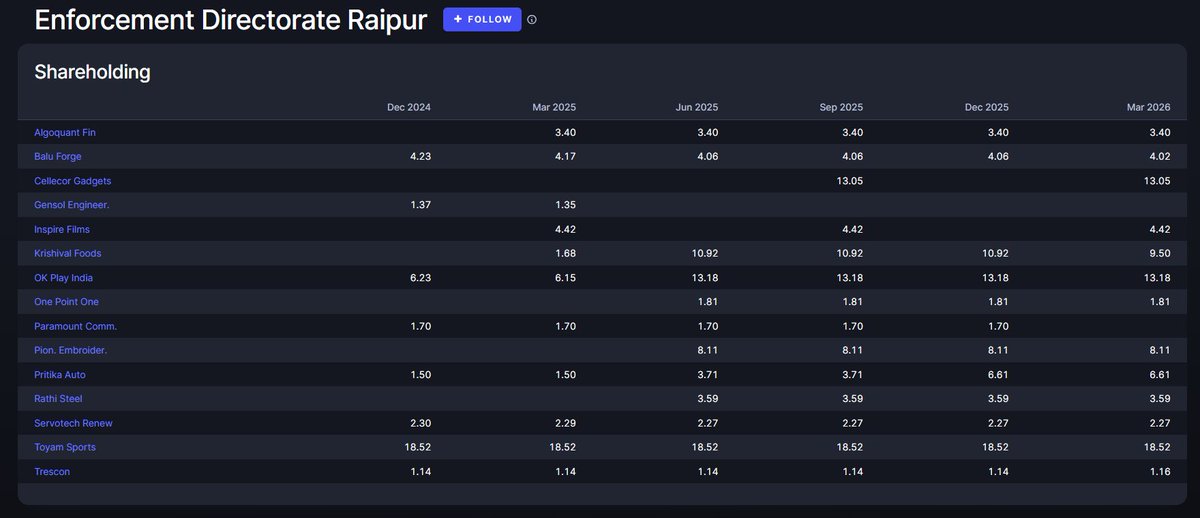

Why there is holding of Government, Enforcement Directorate Raipur. Holding appears to be from March, 2025. Net Profit consistent from Mar2024.

Their holding is as follows.

Even #Gensol was part of their holding till last year March 2025.

57

Algoquant Fintech FY2026

Related-Party Transactions: September 2025 AGM notice flagged approvals for ₹501.25 Cr in RPT limits and ₹1,000 Cr in borrowing/investment caps—sizable headroom. No specific dodgy deal noted yet.

Read full article on Eduinvesting

72

Algoquant Fintech FY2026

The operating CF stayed flat at ₹60 Cr from FY25 to FY26—the machine runs at steady-state. Investing CF stayed negative (capex and loan-outs), while financing CF swung from large debt repayments in FY25 to modest outflows in FY26, signalling the debt cycle has ended.

Read full article on Eduinvesting

120

Algoquant Fintech FY2026: The Algorithm Bets Its House - Eduinvesting eduinvesting.in/algoquant-fi…

87

𝗤𝘂𝗮𝗹𝗶𝘁𝘆 𝗚𝗿𝗼𝘄𝘁𝗵 𝗦𝗰𝗿𝗲𝗲𝗻𝗲𝗿 — 𝗤𝟰𝗙𝗬𝟮𝟲 👀📊

93 stocks with >50% YoY profit growth ROCE >20%

• Atlanta Electricals

• Acutaas Chemical

• Anthem Biosciences

• Diamond Power

• Mobavenue AI Tech

• Quality Power

• Rubicon Research

• Syrma SGS Tech

• Concord Control

• Neuland Labs

• Anondita Medi

• Timex Group

• Multi Comm Exc

• Navin Fluorine

• Olectra Greentech

• Marsons

• Yash Highvoltage

• Hindustan Copper

• Monolithisch India

• Aimtron

• Precision Wires

• Algoquant Fin

• KSH International

• Macfos

• Krishna Defence

• Fredun Pharma

• Lumax Auto Tech

• Vidya Wires

• Tips Music

• CFF Fluid

• Mazagon Dock

• Kirloskar Pneumatic

• Bajaj Consumer

• GNG Electronics

• Indo Thai Securities

• Coforge

• Thangamayil Jewellery

• Ram Ratna Wires

• Kwality Pharma

• KMC Speciality

• V-Marc India

• Fujiyama Power

• Kernex Microsystems

• Redtape

• Premier Energies

• ADF Foods

• Antelopus Selan

• Sky Gold & Diamonds

• Skipper

• Pondy Oxides

• Bharat Dynamics

• Data Patterns

• Zen Technologies

• Astra Microwave

• Paras Defence

• MTAR Technologies

• Solar Industries

• Bharat Electronics

• Cyient DLM

• Kaynes Technology

• Dixon Technologies

• Amber Enterprises

• CG Power

• Apar Industries

• KEI Industries

• Polycab India

• R R Kabel

• Transformers & Rectifiers

• Shilchar Technologies

• TD Power Systems

• Voltamp Transformers

• Elecon Engineering

• Jupiter Wagons

• Titagarh Rail Systems

• Rail Vikas Nigam

• Ircon International

• BEML

• Garden Reach Shipbuilders

• Cochin Shipyard

• Bharat Forge

• AIA Engineering

• Craftsman Automation

• Ratnamani Metals

• JTL Industries

• Hariom Pipe Industries

• Welspun Corp

• Deepak Fertilisers

• Balaji Amines

• Fine Organic Industries

• PI Industries

• SRF

• Clean Science & Technology

• Alkyl Amines Chemicals

• Vinati Organics

• Jubilant Ingrevia

• Suven Pharmaceuticals

• Laurus Labs

• Caplin Point Laboratories

Strong earnings growth healthy capital efficiency is a combination worth tracking 👀

#Q4Results #StockMarketIndia #SmallCaps #Midcaps #EarningsSeason

3

26

1,127

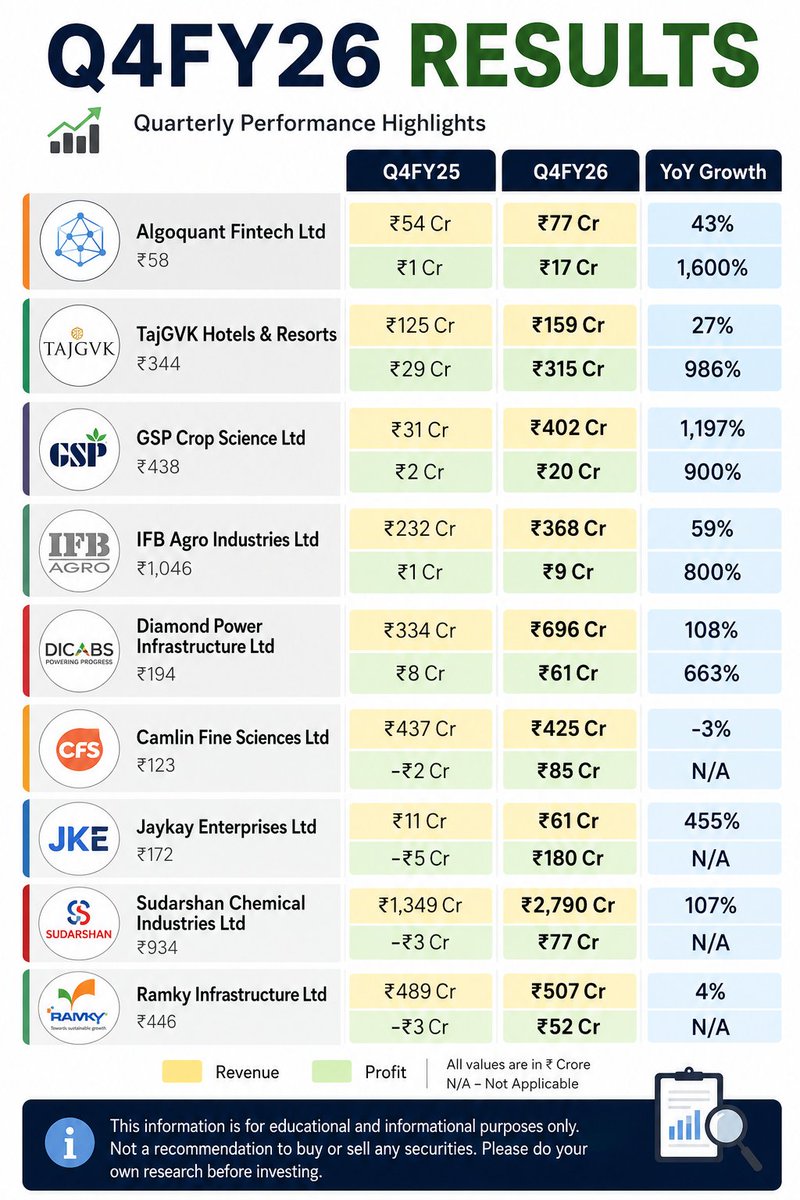

📊 Q4FY26 Earnings Highlights

Strong growth reported by several companies, led by Algoquant Fintech, GSP Crop Science, Diamond Power & more. 🚀

⚠️ Educational purpose only. Not investment advice. DYOR.

#Q4Results #StockMarket #Earnings #Investing

2

118

May 31

𝗤𝘂𝗮𝗹𝗶𝘁𝘆 𝗚𝗿𝗼𝘄𝘁𝗵 𝗦𝗰𝗿𝗲𝗲𝗻𝗲𝗿 — 𝗤𝟰𝗙𝗬𝟮𝟲 👀📊

93 stocks with >50% YoY profit growth ROCE >20%

• Atlanta Electricals

• Acutaas Chemical

• Anthem Biosciences

• Diamond Power

• Mobavenue AI Tech

• Quality Power

• Rubicon Research

• Syrma SGS Tech

• Concord Control

• Neuland Labs

• Anondita Medi

• Timex Group

• Multi Comm Exc

• Navin Fluorine

• Olectra Greentech

• Marsons

• Yash Highvoltage

• Hindustan Copper

• Monolithisch India

• Aimtron

• Precision Wires

• Algoquant Fin

• KSH International

• Macfos

• Krishna Defence

• Fredun Pharma

• Lumax Auto Tech

• Vidya Wires

• Tips Music

• CFF Fluid

• Mazagon Dock

• Kirloskar Pneumatic

• Bajaj Consumer

• GNG Electronics

• Indo Thai Securities

• Coforge

• Thangamayil Jewellery

• Ram Ratna Wires

• Kwality Pharma

• KMC Speciality

• V-Marc India

• Fujiyama Power

• Kernex Microsystems

• Redtape

• Premier Energies

• ADF Foods

• Antelopus Selan

• Sky Gold & Diamonds

• Skipper

• Pondy Oxides

• Bharat Dynamics

• Data Patterns

• Zen Technologies

• Astra Microwave

• Paras Defence

• MTAR Technologies

• Solar Industries

• Bharat Electronics

• Cyient DLM

• Kaynes Technology

• Dixon Technologies

• Amber Enterprises

• CG Power

• Apar Industries

• KEI Industries

• Polycab India

• R R Kabel

• Transformers & Rectifiers

• Shilchar Technologies

• TD Power Systems

• Voltamp Transformers

• Elecon Engineering

• Jupiter Wagons

• Titagarh Rail Systems

• Rail Vikas Nigam

• Ircon International

• BEML

• Garden Reach Shipbuilders

• Cochin Shipyard

• Bharat Forge

• AIA Engineering

• Craftsman Automation

• Ratnamani Metals

• JTL Industries

• Hariom Pipe Industries

• Welspun Corp

• Deepak Fertilisers

• Balaji Amines

• Fine Organic Industries

• PI Industries

• SRF

• Clean Science & Technology

• Alkyl Amines Chemicals

• Vinati Organics

• Jubilant Ingrevia

• Suven Pharmaceuticals

• Laurus Labs

• Caplin Point Laboratories

Strong earnings growth healthy capital efficiency is a combination worth tracking 👀

#Q4Results #StockMarketIndia #SmallCaps #Midcaps #EarningsSeason

3

1

18

1,248

May 29

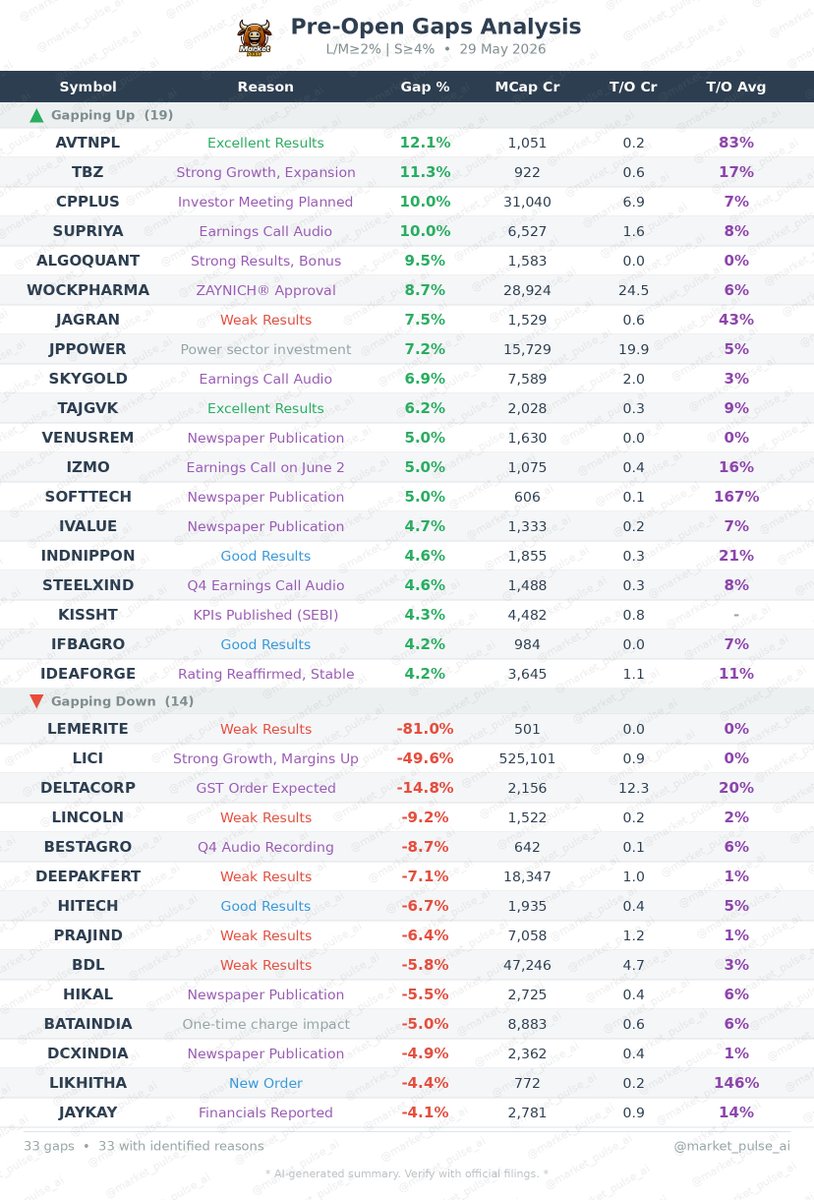

🚀 Pre-Market Gainers — 29 May

Top stocks gapping up at open:

#AVTNPL #TBZ #CPPLUS #SUPRIYA #ALGOQUANT

#PreMarket #Stocks #StockMarket

4

764

May 28

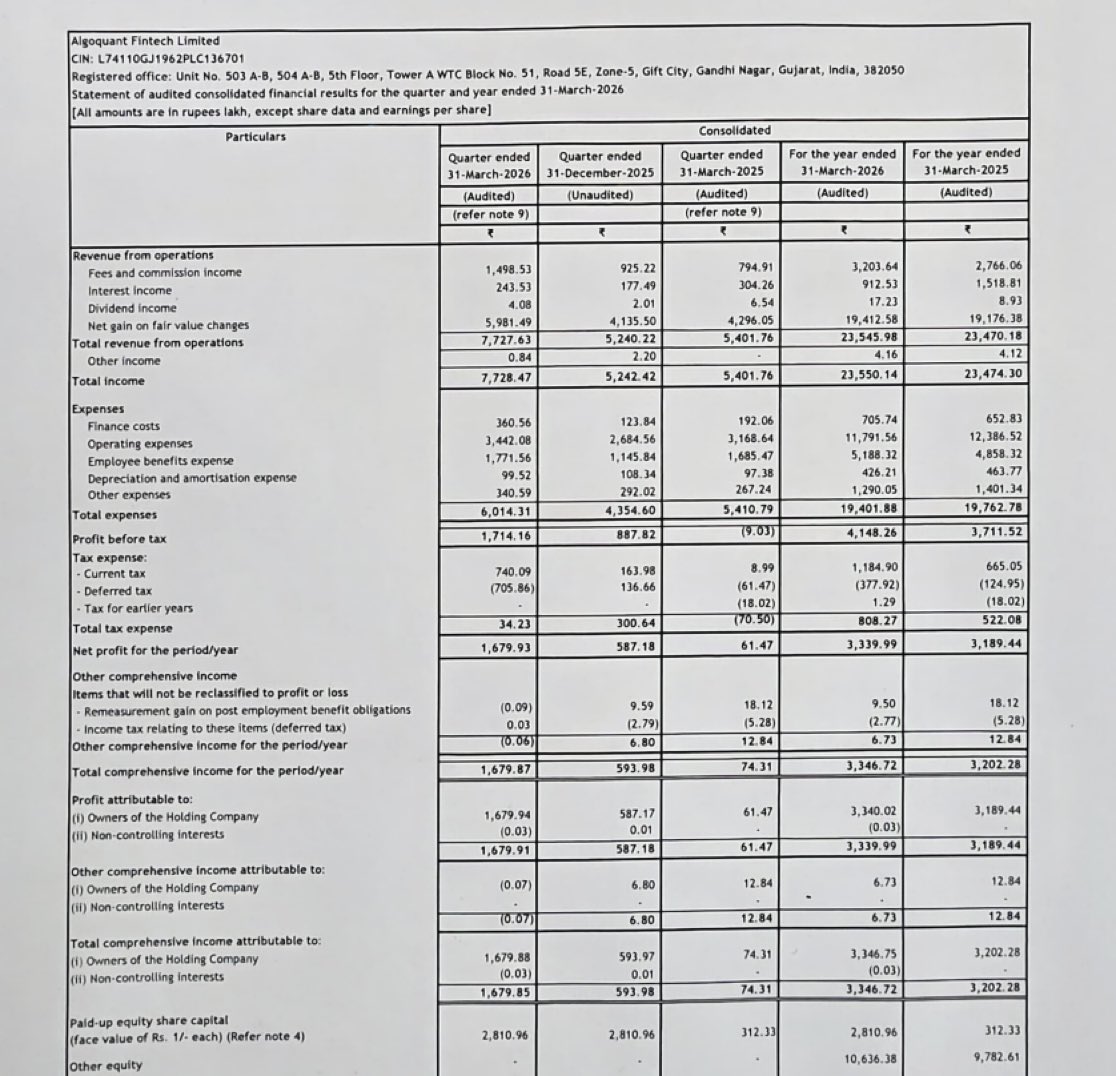

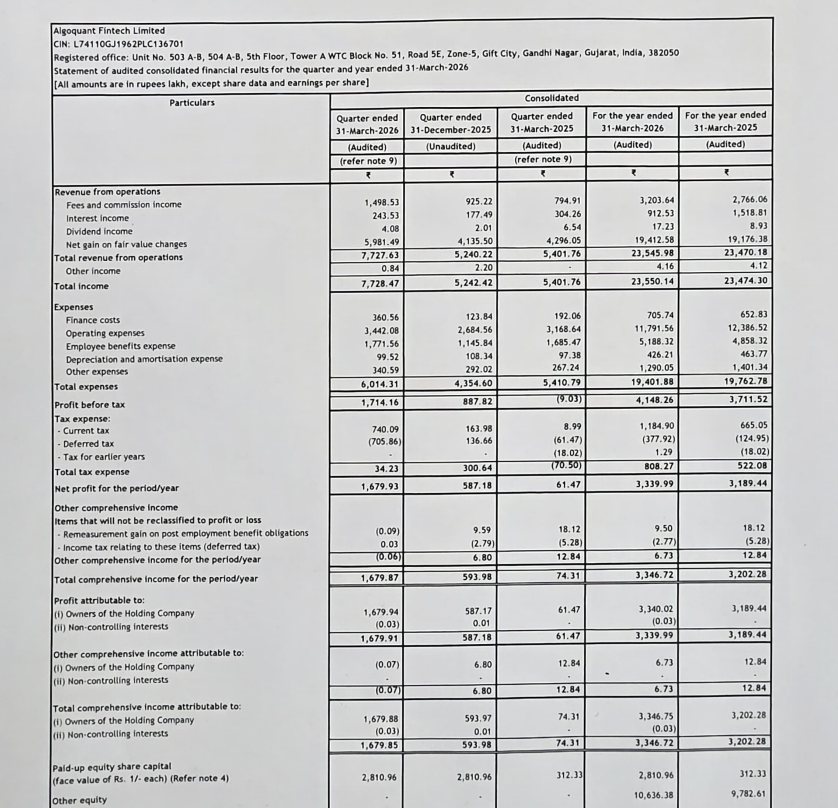

ALGOQUANT FINTECH LTD Q4FY26 RESULTS

#Q4Results #Q4FY26 #StockMarket #Nifty #Algoquant

🟢 Total Revenue: ₹77.28 Cr vs ₹54.02 Cr

( 43.06% YoY┃ 47.47% QoQ)

🟢 EBITDA: ₹21.73 Cr vs ₹2.80 Cr

( 675.08% YoY┃ 94.44% QoQ)

🟢 EBITDA Margin: 28.13% vs 5.19% YoY & 21.33% QoQ

🟢 PBT: ₹17.14 Cr vs -₹0.09 Cr YoY & ₹8.88 Cr QoQ

( 93.08% QoQ)

🟢 PAT: ₹16.80 Cr vs ₹0.61 Cr YoY & ₹5.87 Cr QoQ

( 2632.93% YoY┃ 186.10% QoQ)

🟡 Note: Performance largely supported by net gain on fair value changes

🗣️ Management Update: The company reported a sharp jump in revenue and profitability, with strong sequential and YoY growth across key metrics. However, earnings were significantly influenced by fair value gains, making sustainability of profits an important watchpoint.

Core operating stability vs mark-to-market-driven profits will be key for future trend.

Can Algoquant maintain this earnings momentum without valuation-driven support? 🤔

#FintechStocks #AlgoTrading #IndianStockMarket #StocksToWatch

2

2

76

May 28

ALGOQUANT FINTECH: Q4 NET PROFIT 159M RUPEES VS 11M (YOY) || Q4 REVENUE 773M RUPEES VS 539M (YOY)

4

5

55

15,250

May 28

27th May 2026 Q4FY26 Results Snapshot:-

#Q4Results #Q4FY26 #Nifty

🚩Decent / Good / Blockbuster 👏🔥😀

1) Aditya Infotech (Blockbuster)(FY27 Guidance raised)(FY27 Expected Revenue growth 40-50% EBITDA growth 45-65% PAT growth 50-65% )

2) Sky Gold And Diamonds (Solid)(We now expect to achieve ₹8,100 Cr revenue and 4.5%-4.75% PAT margin, while generating operating cash flows from FY27)

3) Hindusthan Insulators & Industries (Solid)

4) Indian Metals & Ferro Alloys (Solid)(Margin Expansion)

5) IZMO (Margin down)(Revenue up 82.5% EBITDA up 32%)(PAT growth looks higher due to other income)

6) Supriya Lifescience

7) Vadilal Industries (Solid)🍨

8) Advait Energy Transitions (Margin Expansion)

9) Goldiam International (Gold)(Goldiam’s order book position as on March 31, 2026 was at about ₹ 200 Cr)(Doubles ORIGEM stores to 24 operational stores since January 26)

10) Asahi India Glass (Margin Expansion)

11) Ramco Industries (Good)(Margin Expansion)

12) Cummins India (Domestic demand remains steady)(export environment faces some near-term pressures)

13) TVS Srichakra

14) Arman Financial Services (Solid)(MFI player as expected)

15) Sukhjit Starch & Chemicals (Margin Expansion)

16) FDC (Finally good set of numbers after a long time)(Margin Expansion)

17) West Coast Paper Mills (Good numbers after a long time)(Margin Expansion)

18) Medicamen Biotech (Decent)

19) One Point One Solutions (Revenue 43% EBITDA up 77%)(PAT growth lags due to lower other income)

20) Kapston Services (Margin Expansion)

21) Tribhovandas Bhimji Zaveri (Solid)(but these kind of margins are not sustainable)

22) A B Cotspin India (Revenue up 22.5% EBITDA up 21%)

23) Uni Abex Alloy Products (Decent)(Margin Expansion)

24) Adisoft Technologies (SME)(Decent)

25) OnEmi Technology Solutions (Good)

26) Emerald Finance (Good)

27) Shivalik Rasayan (Solid)(EBITDA up 116%)(Lower Other Income dragged PAT growth down)

28) Physicswallah (Margin up YoY)(Matter here is what will AI do going forward here)

29) Dharmaj Crop Guard (Solid Margin Expansion)

30) NINtec Systems (Decent)(Margin Expansion)(PAT growth lags due to other income)

31) Himatsingka Seide

32) DCX Systems (QoQ improvement)

33) Bajel Projects (Solid)(Margin Expansion)

34) Marine Electricals (Margin Expansion)

35) Focus Lighting & Fixtures (Solid)(Revenue up 44% EBITDA up 59%)

36) Apollo Sindoori Hotels (Good)

37) Suratwwala Business Group (Solid)

38) Time Technoplast

39) Sahasra Electronic Solutions (SME)(On FY26 basis Decent)

40) GMR Airports

41) Singer India (Solid)

42) Unifinz Capital India

43) Euro India Fresh Foods (Solid)(Margin Expansion)

44) Algoquant Fintech

🚩Bad / Poor / Weak 😠😡🤬

1) AXISCADES Technologies (Q4 FY26 performance was impacted by deferred revenue recognition of ₹142 Cr)(Impacted by global logistics disruptions, and input material supply constraints)(Aggregate EBITDA impact from deferred revenue exceeded ₹40 Cr)(Delayed Q4 deliverables have rolled over into a hard backlog for Q1–Q2 FY27)

2) Bannari Amman Sugar

3) Bajaj Steel Industries

4) Likhitha Infrastructure

5) GKW

6) RDB Infrastructure And Power

7) Sharat Industries (Margin down)

8) Ganesh Benzoplast (Margin down)

9) Hikal (PPND is back)

10) Thejo Engineering (Margin down)

11) Munjal Auto Industries (Margin down)

12) Best Agrolife

13) Bata India

14) Stanley Lifestyles

15) Delton Cables (Revenue up 58%)(Margin down)(EBITDA Margins suffered due to higher input costs along with supply chain disruptions on account of geo political situation)

16) Tiger Logistics (Margin down)

17) PG Electroplast (Weak)(No guidance given this time)

18) Roto Pumps (Margin down)

19) Ritco Logistics (Margin down)

20) Uniphos Enterprises

21) Orient Ceratech (Margin down)(PAT growth only due to higher other income)

22) Quadrant Future Tek

23) Ramky Infrastructure (Margin down)(During Q4, secured new orders worth ₹4,500 Cr, taking the order book to over ₹13,000 crore as of March 31, 2026)

24) Cello World

25) Om Freight Forwarders (Margin down)

26) Esab India (Margin down)

27) BMW Ventures (Margin down)

28) Goodricke Group

🚩 Mixed / Neutral / Average🙄😑

1) Varroc Engineering (Margin down)

2) HPL Electric & Power (Below Avg to weak)

3) Macpower CNC Machines (Revenue up 25% EBITDA up 13.6%)(Margin down)

4) TCI Express (Margin Expansion)

5) PC Jeweller (EBITDA Margin down)(Reduction in Interest Cost aided PAT growth)

6) Shalby (Margin Expansion)

7) Nimbus Projects

8) Jaykay Enterprises (Margin down)(Revenue up 450% YoY)

9) Oriental Rail Infrastructure (Margin Expansion)

10) Empire Industries (Solid Margin Expansion)

11) Andhra Petrochemicals (Revenue down but Margin Expansion)

12) Anjani Portland Cement (Revenue down but Margin Expansion)

13) Regaal Resources (Revenue down but Margin Expansion)

14) Vinsys IT Services India (SME)

15) Shiv Texchem (SME)(Margin up)

16) Nikhil Adhesives

17) National Fertilizers (Revenue down but Margin Expansion)

18) Marathon Nextgen Realty (Weak Revenue Recognition)

19) MM Forgings

20) KIOCL (Good)(Revenue down but Solid Margin Expansion)

21) Ivalue Infosolutions

22) Isgec Heavy Engineering (Weak side)(Margin down)

23) Kamdhenu (Margin Expansion)(Negative Other Income dragged PAT down)

24) Arkade Developers (Good revenue recognition)(Margin down)(FY26 Pre Sales up 17%)

25) Supreme Power Equipment (SME)(Avg)

26) Nitin Castings (Revenue down but Margin Expansion)

27) Elgi Equipments

28) Foce India (SME)

29) Gillette India (Margin Expansion)

30) Mrs. Bectors Food Specialities

31) Emami Realty

32) Coffee Day Enterprises (Margin Expansion)

33) Ashiana Housing

34) Gulf Oil Lubricants India

35) Gabriel India (Margin down)

36) Swan Defence and Heavy Industries (Track)(SDHI has built a strong order book of ~$500 million through a series of historic, first-of-their kind contracts secured by an Indian shipyard)

37) KELTECH Energies (Below Avg)

38) Prevest Denpro (SME)(Weak)

39) Tejas Cargo India (SME)

40) Varvee Global

41) Kesoram Industries

42) Indostar Capital Finance (No view)

43) STEL Holdings (No view)

44) Dhunseri Investments (No view)

45) Orient Technologies (No view)

46) TechNVision Ventures (No view)

3

7

68

7,396

May 28

Algoquant Fintech Ltd Q4FY26 Results:-

#Q4Results #Q4FY26 #Stockmarket #Nifty #Algoquant

Total Revenue 77.28 Cr vs 54.02 Cr

( 43.06% YoY┃ 47.47% QoQ)

EBITDA 21.73 Cr vs 2.80 Cr

( 675.08% YoY ┃ 94.44% QoQ)

EBITDA Margin 28.13% vs 5.19% YoY & 21.33% QoQ

PBT 17.14 Cr vs -0.09 Cr YoY & 8.88 Cr QoQ

( 93.08% QoQ)

PAT 16.80 Cr vs 0.61 Cr YoY & 5.87 Cr QoQ

( 2632.93% YoY┃ 186.10% QoQ)

Mainly driven by Net gain on fair value changes

1

7

1,403

May 27

#Q4Results TODAY 27 MAY

• Cummins India

• GMR Airports

• PhysicsWallah

• Aditya Infotech

• Gillette India

• KIOCL

• Asahi India Glass

• Elgi Equipments

• Gabriel India

• PG Electroplast

• ESAB India

• Swan Defence & Heavy Industries

• Bata India

• PC Jeweller

• Cello World

• Varroc Engineering

• Time Technoplast

• AXISCADES Technologies

• Indian Metals & Ferro Alloys

• ISGEC Heavy Engineering

• Sky Gold & Diamonds

• FDC

• Supriya Lifescience

• Mrs. Bectors Food Specialities

• Gulf Oil Lubricants India

• Goldiam International

• Bannari Amman Sugars

• OnEMI Technology Solutions

• National Fertilizers

• Ashiana Housing

• IndoStar Capital Finance

• Marathon Nextgen Realty

• West Coast Paper Mills

• Ramky Infrastructure

• Vadilal Industries

• TVS Srichakra

• Hikal

• Ramco Industries

• Jaykay Enterprises

• HPL Electric & Power

• DCX Systems

• Advait Energy Transitions

• Arkade Developers

• MM Forgings

• Bajel Projects

• TCI Express

• Arman Financial Services

• Shalby

• Algoquant Fintech

• iValue Infosolutions

• Orient Technologies

• NINtec Systems

• Quadrant Future Tek

• Roto Pumps

• IZMO

• Himatsingka Seide

• Dharmaj Crop Guard

• Munjal Auto Industries

• Oriental Rail Infrastructure

• Tribhovandas Bhimji Zaveri

4

1,038

🚨UPCOMING QUARTERLY RESULTS Q4FY26:

📅 27 May, 2026 ⏬

21STCENMGM

ABCOTS

ADVAIT

AIROLAM

AKG

ALGOQUANT

ALPHAGEO

APCL

APOLSINHOT

ARKADE

ARMANFIN

ASAHIINDIA

ASHIANA

ASPINWALL

AURIGROW

AXISCADES

BAJEL

BALPHARMA

BANARISUG

BATAINDIA

BEARDSELL

BECTORFOOD

BESTAGRO

BLBLIMITED

BMWVENTLTD

BVCL

CAPTRUST

CELLO

COFFEEDAY

CPPLUS

CUMMINSIND

DANGEE

DCXINDIA

DELTAMAGNT

DHARMAJ

DHUNINV

DPSCLTD

EIFFL

ELGIEQUIP

EMAMIREAL

ESABINDIA

FDC

FOCUS

GABRIEL

GANESHBE

GILLETTE

GKWLIMITED

GLOBALVECT

GMRAIRPORT

GOLDIAM

GULFOILLUB

GULFPETRO

HARDWYN

HAVISHA

HIKAL

HIMATSEIDE

HPL

IL&FSENGG

IMFA

INDOSTAR

ISFT

ISGEC

IVALUE

IZMO

JAYKAY

KAMDHENU

KAPSTON

KAUSHALYA

KCPSUGIND

KESORAMIND

KIOCL

KISSHT

KUNDANMM

LIKHITHA

LOVABLE

LOYALTEX

LYPSAGEMS

MACPOWER

MAGNUM

MARATHON

MARINE

MCL

MEDICAMEQ

MFML

MITCON

MMFL

MUNJALAU

NATCAPSUQ

NDRINVIT

NFL

NIMBSPROJ

NINSYS

NKIND

OMFREIGHT

ONEPOINT

ORCHASP

ORIENTCER

ORIENTTECH

PCJEWELLER

PGEL

PREMIER

PWL

QUADFUTURE

RAMCOIND

RAMKY

REGAAL

RITCO

ROTO

SADBHIN

SBGLP

SHALBY

SHIVALIK

SHIVAMILLS

SHIVATEX

SINGERIND

SKYGOLD

STANLEY

STEL

SUKHJITS

SUPRIYA

SWANDEF

TARAPUR

TBZ

TCIEXP

TECILCHEM

THEJO

TIGERLOGS

TIMETECHNO

TPHQ

TVSSRICHAK

TVVISION

UCAL

UMESLTD

UNIENTER

UNIVASTU

UYFINCORP

VADILALIND

VARROC

VGL

VIPCLOTHNG

WSTCSTPAPR

📅 28 May, 2026 ⏬

ABAN

ABINFRA

AEGISVOPAK

AEPL

AHLEAST

AJOONI

AKSHOPTFBR

ALKEM

AMNPLST

ANTGRAPHIC

ANUP

APARINDS

ARSSINFRA

ASHAPURMIN

ASHOKLEY

ASIANHOTNR

ATCOM

AVANTIFEED

AVTNPL

BALAXI

BANARBEADS

BANCOINDIA

BDL

BEDMUTHA

BFUTILITIE

BIGBLOC

BLKASHYAP

BPL

COMPUSOFT

CORDSCABLE

CURAA

DCM

DEEPAKFERT

DELPHIFX

DEVIT

DHAMPURSUG

DHRUV

DNAMEDIA

ECOSMOBLTY

EFCIL

EIEL

ELGIRUBCO

EMAMIPAP

ENERGYDEV

ESSENTIA

ESSENTIA

FCSSOFT

FINCABLES

GAUDIUMIVF

GKSL

GLOBAL

GOKUL

GPPL

GRAPHITE

HAPPSTMNDS

HECPROJECT

HERANBA

HGINFRA

HITECH

HMVL

HPIL

IFBAGRO

IGCL

INDNIPPON

INDSWFTLAB

INNOVISION

INSECTICID

ISHANCH

ITI

JAGRAN

JAIPURKURT

JMA

JSWHL

KABRAEXTRU

KAKATCEM

KALYANI

KARMAENG

KCP

KOHINOOR

LAL

LEMERITE

LEMONTREE

LFIC

LINCOLN

LORDSCHLO

LUMAXIND

MADHUCON

MALLCOM

MALUPAPER

MANCREDIT

MAXIND

MBECL

MHLXMIRU

MMTC

MONEYBOXX

MOTOGENFIN

MTEDUCARE

NAGREEKCAP

NAHARCAP

NAHARPOLY

NAHARSPING

NDGL

NDL

NIBL

NPST

NSIL

NXT-INFRA

ORIENTLTD

PAVNAIND

PFOCUS

PGHH

PILANIINVS

POKARNA

POWERICA

PRAJIND

PRAKASHSTL

RELAXO

RETAIL

RGL

RHIM

RHL

RMCL

ROLLT

RUBYMILLS

RUCHINFRA

RUCHIRA

SAHLIBHFI

SANCO

SCHNEIDER

SELMC

SHALPAINTS

SHIVAMAUTO

SIMPLEXINF

SPMLINFRA

SUMIT

SUMIT

TAJGVK

TBOTEK

TCPLPACK

TENNIND

TEXMOPIPES

TIIL

TIL

TOLINS

UDS

UNIMECH

UNITECH

URAVIDEF

V2RETAIL

VIRINCHI

VIVIMEDLAB

VRAJ

WEIZMANIND

WEL

ZODIACLOTH

🚀 Stay tuned for updates! 💹

#results #StockMarket #StockMarketUpdate #investing #trading

bullishindia.com/disclaimer

2

917

May 27

4QFY26 - Key Results today

27th May 2026 (Wednesday)

1. Cummins India

2. GMR Airports

3. Physicswallah

4. Aditya Infotech

5. Gillette India

6. KIOCL

7. Asahi India Glass

8. Elgi Equipments

9. Gabriel India

10. PG Electroplast

11. Esab India

12. Swan Defence

13. Bata India

14. PC Jeweller

15. Cello World

16. Time Technoplast

17. Varroc Engineering

18. Axiscades Technologies

19. Indian Metals & Ferro Alloys

20. Isgec Heavy Engineering

21. Sky Gold And Diamonds

22. FDC

23. Supriya Lifescience

24. Mrs. Bectors Food Specialities

25. NDR INVIT Trust

26. Goldiam International

27. Gulf Oil Lubricants India

28. Bannari Amman Sugars

29. OnEMI Technology Solutions

30. National Fertilizers

31. Ashiana Housing

32. Indostar Capital Finance

33. Marine Electricals (India)

34. TechNVision Ventures

35. Marathon Nextgen Realty

36. West Coast Paper Mills

37. Ramky Infrastructure

38. Vadilal Industries

39. TVS Srichakra

40. Hikal

41. Jaykay Enterprises

42. Ramco Industries

43. Mrugesh Trading

44. HPL Electric & Power

45. DCX Systems

46. Arkade Developers

47. Advait Energy Transitions

48. MM Forgings

49. Bajel Projects

50. TCI Express

51. Shalby

52. Arman Financial Services

53. Thejo Engineering

54. One Point One Solutions

55. Algoquant Fintech

56. Ivalue Infosolutions

57. Orient Technologies

58. Hardwyn India

59. NINtec Systems

60. Quadrant Future Tek

61. Macpower CNC Machines

62. Roto Pumps

63. Kapston Services

64. IZMO

65. GKW

66. Himatsingka Seide

Disclaimer : bit.ly/R_disclaimer02

10

922

May 26

🚨 TOMORROW’S EARNINGS | 27 May 2026 📊

⏰ During Market Hours (18 Stocks)

Gillette

Asahi India

Elgi Equip

Varroc

IMFA

Skygold

Bector Food

Goldiam

WSTCSTPAPR

Vadilal

TVS Srichakra

Hikal

Ramco Ind

Arkade

TCI Express

Likhitha

OM Freight

Alphageo

⏰ After Market Hours (59 Stocks)

Cummins India

GMR Airport

PWL

CP Plus

KIOCL

Gabriel

PGEL

ESAB India

SWANDEF

Bata India

Time Techno

Axis Cades

Cello

PC Jeweller

Supriya

FDC

Gulf Oil Lub

Banarisug

Kissht

NFL

Ashiana

Indostar

Marathon

Ramky

Jaykay

HPL

DCX India

Advait

MMFL

Bajel

Shalby

Arman Fin

Algoquant

OnePoint

iValue

Orient Tech

Ninsys

Quad Future

Roto

Izmo

Himatsingka

Regaal

Stanley

Munjal Auto

Dharmaj

TBZ

Stel

Ritco

Ganesh Benzoplast

Kamdhenu

Best Agro

Sukhjit

BMW Ventures

Dhunseri

Coffee Day

Orient Ceratech

ABCOTS

Nimbs Projects

Shivalik

Kesoram

Tiger Logistics

Emami Realty

Medicameq

VGL

KCPSUGIND

Global Vectra

VIP Clothing

Rajputana

BLB Ltd

🎯 Watch: Earnings Surprise | PEAD | Volume Spike | Gap Up/Down 📈

#ResultsSeason #Learning_With_Earning

1

18

1,917

(1/2) DAYS Miami Recap: Panels. Part 8!

→ One of the last discussions was on "Compliance & Regulation for Institutional Onchain Yield," led by Michael Ashby (@lonvangen), CEO & Chief Investment Officer at ALGOQUANT, as a moderator, with Alison Mangiero (@AMangiero), Head of Staking Policy & Industry Affairs at @crypto_council, Moad Fahmi, Chief FinTech Officer at @BermudaMonetary, and Marianela Jaca, VP of TradFi Sales at @P2Pvalidator.

Digital Asset Yield Summit brings the right people in the right room.

1

1

10

362

May 18

🚀 24 Fantastic Growth Smallcaps:

3Year Sales growth >100%,

3Year Profits growth >100%,

(MCap >₹500 Cr & ROCE >15)

📈 Emmvee Photovol.: CMP Rs. 258.0

📈 Waaree Renewab.: CMP Rs. 942.4

📈 Senores Pharma.: CMP Rs. 1050.3

📈 Websol Energy: CMP Rs. 103.4

📈 Kesar India: CMP Rs. 1255.7

📈 Colab Platforms: CMP Rs. 156.7

📈 Indo Thai Sec.: CMP Rs. 269.3

📈 Marsons: CMP Rs. 143.1

📈 Network People: CMP Rs. 1051.2

📈 KP Green Engg.: CMP Rs. 420.4

📈 Solarworld Ene.: CMP Rs. 205.3

📈 Algoquant Fin: CMP Rs. 59.3

📈 Solex Energy: CMP Rs. 1316.5

📈 Kalind: CMP Rs. 87.4

📈 RRP Defense: CMP Rs. 751.1

📈 B-Right Real: CMP Rs. 975.0

📈 Zelio E-Mobility: CMP Rs. 458.6

📈 JOJO: CMP Rs. 256.0

📈 One Global Serv: CMP Rs. 446.4

📈 C2C Advanced: CMP Rs. 443.2

📈 Prizor Viztech: CMP Rs. 683.7

📈 Basilic Fly Stud: CMP Rs. 225.4

📈 Glottis: CMP Rs. 57.9

📈 Nila Spaces: CMP Rs. 13.5

#StocktoWatch

7

63

348

29,944

#ALGOQUANT 🚀📈

#ALGOQUANT, the recently listed Algo & FinTech company, is now coming out of accumulation phase 🔥

After a long consolidation, the stock has given a strong trendline breakout backed by impressive volumes ⚡📊

The stock looks ready for its next big move and has been consistently appearing in my IPO Breakout section of the dashboard 👀

Keep this stock on your watchlist closely 🚨

My AI-driven dashboard helps identify these early breakout opportunities before they become mainstream 💥

To capture these kinds of ideas early, check out my dashboard link in comments 👇

1

3

47

5,704