i also created a backtesting engine in python and it's extremly fast, i can test 100 strategies in seconds.

1

Most just plot RR tool and call it backtesting lol. Looks more like an RR study than a backtest in my opinion

3

BUBU retweeted

Backtesting is studying the recipe, the outcome is known already

Forward testing is cooking the meal yourself.

A strategy may look perfect on past charts, but forward testing reveals whether you can execute it when the outcome is still unknown. I really do not backtest.

36

43

345

12,040

Trading with AI is now easier than ever on Fraction AI Index.

Users can quickly choose from ready made strategies like Trend Following, Buy the Dip, and Breakout, then apply them to major markets such as BTC, ETH, and SOL without needing advanced trading knowledge.

A standout feature is "Surprise Me." Just describe what you're looking for and the AI will analyze market data sentiment, on chain activity funding rates and whale movements to find potential opportunities automatically.

Security has also improved with Recovery Email support alongside 2FA, making account protection and recovery much more reliable.

The growing community actively shares strategies backtest results, and trading insights helping everyone discover new ideas and improve their performance.

Each AI strategy comes with a clear explanation of how it works including entry rules exit targets, position sizing and risk controls. Users can also review detailed backtesting results with key performance metrics before going live.

Once a strategy is running the monitoring dashboard provides realtime tracking while onchain transparency keeps every trade publicly verifiable.

Whether you're testing proven strategies creating custom ideas through chat editing or exploring opportunities with AI Index turns complex trading concepts into automated trading systems that anyone can use.

Plus, community participation can earn Fractals and position users for future ecosystem rewards.

@0xshai

@Chaitanya_2709_

@79amadison79

2

18

வெளிநாட்டுக்காரர்கள் என்ன செய்தாலும், அதைப் பற்றி முறையாக ஆய்வு செய்யாமலும்,(backtesting) மதிப்பீடு செய்யாமலும் அதன் விளைவுகளை ஆராயாமலும், நமது சூழலுக்கு அது பொருந்துமா என்று பரிசீலிக்காமலும், அதை அப்படியே தமிழ்நாட்டில் கொண்டு வர வேண்டும் என்ற அடிமை மனப்பான்மை மனநிலை மாற்றப்பட வேண்டும்.

11

I'm not sure trading has ever been as much fun as hypothesizing and building robust portfolio models with AI.

AI feedback isn't 100% reliable but if the right guardrails are put in place, I feel like there can be a lot more confidence in the feedback.

The satisfaction comes from speed of working with AI, yes. But it's also the confidence in knowing when you're actually making progress without spending days backtesting on what might not be reliable data anyway.

And it's not like the AI is doing all the work, limiting sense of purpose for ourselves. We still need to guide the process, we still need to figure out the best team of models on the portfolio from a holistic angle, while the AI works in the trenches.

It's fun being the commander for a change.

19

sniper (Private) retweeted

Jun 9

I made over $150,000 in under a hour last week using my custom breakout strategy.

Months of backtesting.

Hundreds of trades.

Over 97% win rate.

I built it into a TradingView indicator that tells you when to buy/sell. Now it’s yours - free.

Like/RT Comment “Trade” - I’ll DM it to you.

(Must be following to DM)

$SPY $SPX

1,060

101

713

82,074

𝐆𝐌 retweeted

Backtesting is overrated

Not because the data lies

Because you're not testing the version of you that trades at 2am tilted after two losses

2

1

34

671

Profit Factor: sum of wins / |sum of losses|

>1.5 solid · >2.0 strong · <1.0 you're losing money

A strategy with 70% win rate and PF 0.8 loses. Period.

$BTC #DataDriven #Backtesting

1

5

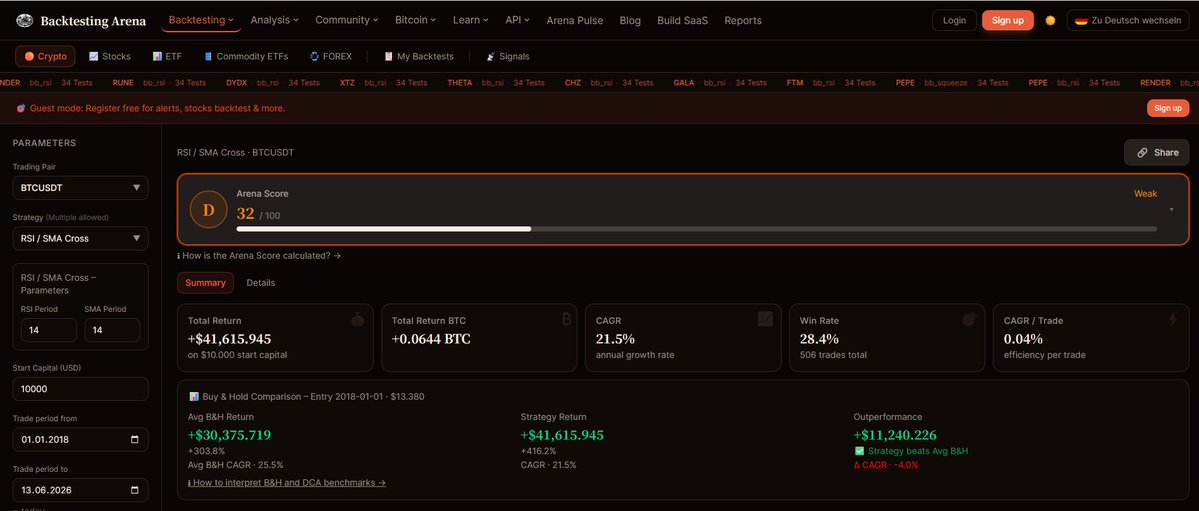

🆕 Backtest result panel upgrade on Backtesting Arena.

Two tabs: Summary (clean, 6 metrics) and Details (deep analysis).

New: SQN · Expectancy · Profit Factor · Monthly breakdown.

$BTC #Backtesting #Trading 🥋

1

5

46m

Backtesting is underrated, its where you can get the basis for any edge, which most seem to overestimate and overlook.

If emotions are a problem, that has nothing to do with backtesting and cant be fixed in backtesting.

20

Engr usman retweeted

Jun 12

Your journaling and backtesting software ✅

• Refine your edge and optimize your trading strategies

• Track your progress month by month with advanced automated analytics

• Seize new opportunities and adjust to market conditions

• Gain valuable insights to improve your trading performance

Start the year with precision and focus.

We are here to support your trading journey!

10

8

15

272

Yeah. I used to force equal R targets both ways because it made backtesting easier.

1

1

2

This matters more for backtesting than live execution, and it's where systematic work quietly breaks. When you stitch ESM26 into ESU26 to build one continuous chart, the two contracts don't trade at the same price, so you get a fake gap at the splice from cost of carry, not from any real move.

Back-adjusting removes the gap but shifts every historical price, so your absolute levels stop matching what actually printed. Ratio-adjusting keeps the shape but distorts the distances. Neither is free. Anything that reads off fixed price levels instead of relative structure is exactly where a backtest diverges from what you'd have actually filled, and the roll is usually the culprit.

Liquidity migration is the other piece. Volume drains out of the front month into the new one across the roll window, so the levels worth watching shift to ESU26 before the calendar says the contract officially changed.

1

1

29

TradingView Developer

🚨 Remote Job Alert

We’re hiring a TradingView Developer.

💰 Salary: $3,000–$10,000/month

🌍 Remote

Requirements:

• Pine Script

• Backtesting

• Trading Experience

No degree required.

❤️ Like

🔁 Repost

💬 Comment “PINE”

We’ll review every profile.

#TradingView #ForexJobs

1

10

Dayyabu Ibrahim retweeted

*Weekend Trap* ⚠️

If you’re “backtesting” but secretly hunting entries…

You’re not preparing. You’re gambling with extra steps.

The market closed to test your discipline, not your WiFi.

Pass the test = Capital stays.

Fail the test = Monday you fund someone else’s win.

*Rule:* Charts off. Journal on. Mindset up.

Want this one on a red/charcoal banner? Red background makes the “trap” warning hit way harder.

2

1

2

20

1h

Exactly 😂. I explained this to my friend, there's no strategy backtested that doesn't give great results. The reason is simple a lot of things are not accounted for during backtesting. I'll always recommend forward testing more with paper trading.

9