A bag that carries your groceries today and nourishes the Earth tomorrow. 🌱♻️

Switch to 100% compostable bags and be part of the solution, not the pollution.

Go Green. Go Biogreen. 💚🌍

#Compostable #Biogreen #EcoFriendly #Sustainability #PlasticFree #GreenFuture

3

Jun 15

💖 El aroma que está conquistando hogares...

🍑 Papaya & Frambuesa ✨ Dulce, frutal y simplemente irresistible.

🌸 Difusor $16.490 🌸 Repuesto $9.990

🏡 Llena tu hogar de bienestar, frescura y energía positiva.

📩 Pídelo hoy en Jakito Biogreen.

6

Jun 14

再入荷成功‼️人気です✨1mlパンパン、お安くて ライブレジン配合のいいフレーバー😽

高体感となっております‼️

Xセール中! 5000円 → 4500円

《H4CBD「UPLIFT 」ライブレジン リキッド》

NO THC / NO CBN

内容量:1.0ml

主成分:H4CBD 70% / CBG 12% / CRDPRO-H (HHCB.H4CBD.CBGDIS)

・新規格対応

(パッケージ表示と成分が異なる場合がありますがこちらが正式な成分となります)

● BioGreen LABから、明るく切れ味のある"アップリフト体感"のリキッド発売

体感の強い H4CBD を70%配合をベースにキレの良いCBG原料、CRD-PRO-H(BGL無結晶化ディストレート)との合成でヘッド・ハイ、アップリフトな心地よく爽快感のある体感を再現しました。

高品質なライブレジン配合し以前にましてスッキリ感が強くなりました!

最新フレーバー「Lemon OG Kush」がございます!

【特徴】

・少量使用することで、十分なリラックス効果を発揮する能力を持っています。

・普段から緊張しやすい方のリラックス目的での使用にも向いております。

・ゆっくりできる場所で一人で、友達とのチルアウトに向いています。

● ライブレジン を使ったカンナビスの自然の香り漂い

フレーバー①:Lemon OG Kush

(Live Resin Terpenes+)

● 成分表記(B.G.L商品製造データシート/COAより引用)

カンナビノイド /各ディストレート

H4CBD 70%

CBG 12%

CRD-PRO-H(HHCB.H4CBD.CBGDIS.CBD)

● カンナビス由来 100%テルペン使用

- Cannabis Terpenes

- Live Resin

(*PG、VG、PEG、MCT、DSMO不使用)

#H4CBD

1

2

11

782

This World Day against Child Labour, Biogreen pledges its voice for every child robbed of their innocence!

Because every child deserves the right to simply be a child!!!

#WorldDayAgainstChildLabour #EndChildLabour #ChildRights #EducationForAll #StopChildLabour #SaveChildhood

4

10

This photo was sent in from Iowa showing a competitor mix (left) vs. Physagro products (right) on corn. 🌽

Mix includes: 16oz #BioGreen, 16oz #MicroBoost, 6oz #AcceleratePro, and some CetaiN.

Nice work!

7

Jun 10

Slow down the wind and weather coming into your #jobsite without decreasing visibility with super duty transparent #tarps from BioGreen: bit.ly/3hmy6eB

6

Jun 9

بيوجرين - البوتاسيوم

Biogreen - Potassium

12-12-35 1.5 MgO 3% Seaweed TE

✔️ تركيبة غنية بالبوتاسيوم معززة بمستخلص الطحالب البحرية.

📦 متوفر: 2 كجم

إيرادكو للأسمدة ... جودة تصنع فرقًا

لمزيد من التفاصيل:

wa.me/966536661645

eradunited.com

12

🌍 Every small choice matters.

Say NO to plastic pollution and YES to compostable solutions with Biogreen. 🌱

Protect our oceans, wildlife, and future—one bag at a time.

🌐 biogreenprojects.com

📞 91 7044308802

#Biogreen #PlasticFree #CompostableBags #SaveOurOceans

3

9

🌱 Trusted by businesses across India for sustainable packaging solutions.

✅ 100% Compostable & Biodegradable

✅ Eco-Friendly & Durable

✅ Reduces Plastic Pollution

Choose sustainability. Choose Biogreen. ♻️

🌐 biogreenprojects.com

📞 91 7044308802

#SustainablePackaging

2

13

Jun 1

BGLの当店定番商品H4CBD70%再入荷成功‼️お値段も安くて体感も強いです🌈よろしくお願いいたします。

⭐️Xセール中! 5000円 → 4500円⭐️

メーカー情報

《H4CBD「UPLIFT 」ライブレジン リキッド》

NO THC / NO CBN

内容量:1.0ml

主成分:H4CBD 70% / CBG 12% / CRDPRO-H (HHCB.H4CBD.CBGDIS)

・新規格対応

(パッケージ表示と成分が異なる場合がありますがこちらが正式な成分となります)

● BioGreen LABから、明るく切れ味のある"アップリフト体感"のリキッド発売

体感の強い H4CBD を70%配合をベースにキレの良いCBG原料、CRD-PRO-H(BGL無結晶化ディストレート)との合成でヘッド・ハイ、アップリフトな心地よく爽快感のある体感を再現しました。

高品質なライブレジン配合し以前にましてスッキリ感が強くなりました!

最新フレーバー「Lemon OG Kush」がございます!

【特徴】

・少量使用することで、十分なリラックス効果を発揮する能力を持っています。

・普段から緊張しやすい方のリラックス目的での使用にも向いております。

・ゆっくりできる場所で一人で、友達とのチルアウトに向いています。

● ライブレジン を使ったカンナビスの自然の香り漂い

フレーバー①:Lemon OG Kush

(Live Resin Terpenes+)

● 成分表記(B.G.L商品製造データシート/COAより引用)

カンナビノイド /各ディストレート

H4CBD 70%

CBG 12%

CRD-PRO-H(HHCB.H4CBD.CBGDIS.CBD)

● カンナビス由来 100%テルペン使用

- Cannabis Terpenes

- Live Resin

(*PG、VG、PEG、MCT、DSMO不使用)

#H4CBD

3

9

766

Let this Eid be remembered not just for the prayers and feasts but for the clean, green, and responsible celebration it is!

Biogreen wishes you a cleaner, greener Eid Mubarak!

#eid #eidmubarak #happyeid

3

24

Small step, big impact 🌍💚

❌ Not plastic

❌ No pollution

✅ 100% Biocompostable

Switch to Biogreen for a cleaner, greener future 🌱

🌐 biogreenprojects.com | 📞 91 7044308802

#Biogreen #PlasticFree #Sustainability #EcoFriendly

4

19

Our oceans deserve better 🌊💚

Say NO to plastic pollution and YES to sustainable, biocompostable solutions with Biogreen 🌱

Protect marine life. Protect the future.

🌐 biogreenprojects.com

📞 91 7044308802

#SaveOurOceans #PlasticFree #Biogreen #Sustainability

3

10

May 9

"Doğanın en güzel mucizesi, karşılıksız sevginin adresi... Tüm annelerimizin #AnnelerGünü kutlu olsun! 🌸🌿 #Biogreen

3

18

Small step, big impact 🌍💚

Say NO to plastic. YES to 100% biocompostable bags 🌱

Switch to Biogreen today.

🌐 biogreenprojects.com | 📞 91 7044308802

#GoGreen #Biogreen #PlasticFree #Sustainability

2

11

May 5

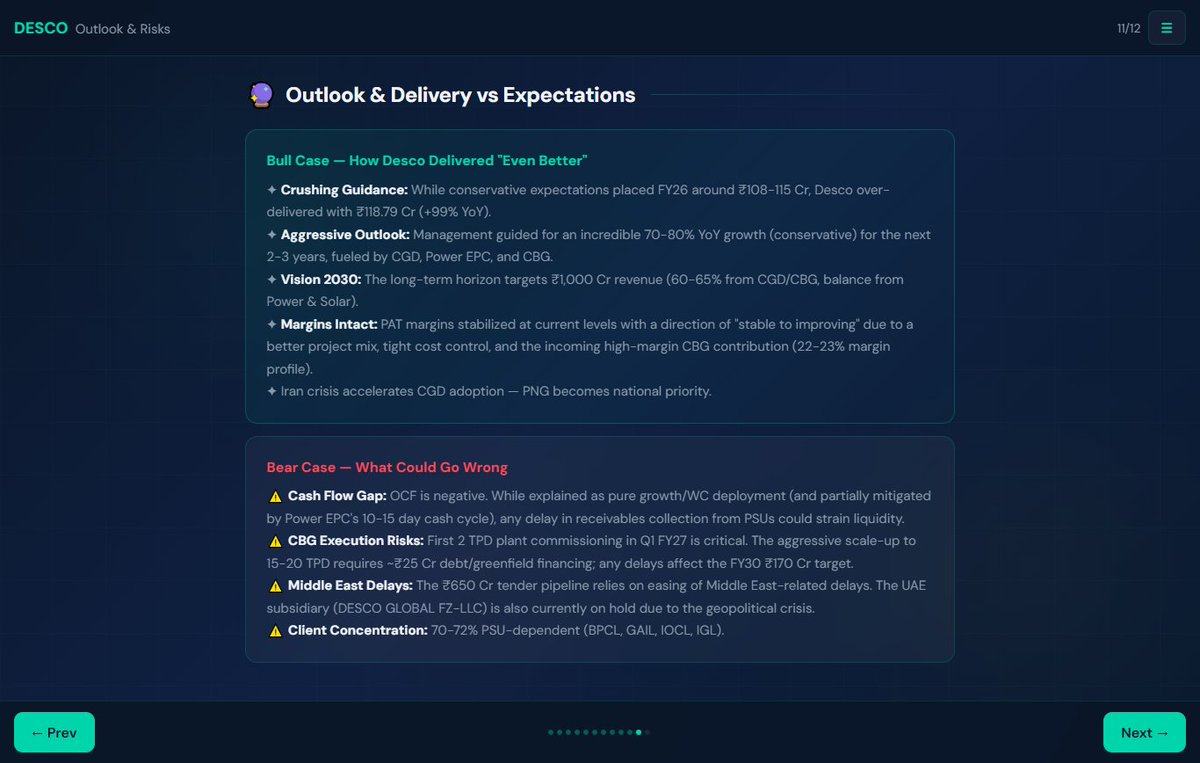

Desco Infratech FY26 Earnings Concall Highlights:

👉 FY27 & Future Outlook:

💠Revenue growth: Management guided 70-80% YoY growth (conservative) for the next 2-3 years on the back of CGD execution, power/solar diversification, and CBG ramp-up.

💠Long-term target: ₹1,000 Cr revenue by FY2030 (5-year horizon). CGD (including CBG) expected to contribute 60-65% of revenue; balance from power distribution & solar EPC.

💠CBG-specific outlook: First 2 TPD plant commissioning in Q1 FY27 (revenue potential ~₹5 Cr p.a. at full utilisation).

💠Additional expansion to 15-20 TPD capacity targeted in next 18 months (Gujarat Madhya Pradesh).

💠CBG revenue expected to reach ~₹170 Cr by FY2030.

👉Margins: CGD PAT margin stable at ~15.4%. Power & Renewable EPC at ~10%. Overall PAT margins sustainable at current levels with direction “stable to improving” due to better project mix, cost control, and higher-margin CBG contribution (PAT margin 22-23%).

💠Break-even on initial CBG plant expected in 18-20 months

💠Cash flow: Operating cash flow to turn positive within 1-2 years (already improving from last year despite 100% revenue growth).

💠Negative cash flow in FY26 was purely growth-driven (working capital deployment), not liquidity stress.

👉 Current Order Book / Projects and Future Pipeline:

💠Order book: ₹345 Cr

💠 CGD: ~₹330-332 Cr (EPC timeline 18-24 months; O&M ~₹35-40 Cr over 24 months).

💠Power distribution: Balance portion (average timeline ~1 year).

💠Tender pipeline: ₹650 Cr (CGD ~₹470-480 Cr solar/power ~₹100 Cr). Expected to convert quickly once Middle East-related delays ease; management sees this as a major order-book booster.

💠Execution focus: CGD pipeline execution continues. Power & solar EPC contributed meaningfully in H2 FY26 due to seasonal execution tailwinds (post-monsoon ROW clearances).

💠CGD remains core (83.24 Cr revenue in FY26).

👉CBG projects:

💠2 TPD commissioning in Q1 FY27 (capex ₹3.5-4 Cr already incurred).

💠SGAEPL (75-76% stake acquired) to add 5 TPD capacity; ready government approvals accelerate rollout.

💠Further 15-20 TPD greenfield via Desco BioGreen Pvt Ltd (total capex ~₹25 Cr planned; funded via bank debt/greenfield financing).

👉 Other Notable Points:

💠FY26 Financials: Revenue ₹118.79 Cr ( 99.28% YoY), EBIT ₹23.43 Cr ( 76.3%), PAT ₹16.38 Cr ( 80.87%), Net Worth ₹70.85 Cr ( 20.3%), Debt/Equity stable at 0.20x, EPS ₹21.34.

💠Segment performance: CGD (70% of revenue) delivered healthy 15.42% PAT margin; new Power & Renewable EPC segment (30%) at 10.01% PAT but offers superior 10-15 day cash conversion cycle vs 30-35 days in CGD — strategic move for working-capital efficiency.

👉Debt & capital allocation: Unsecured NBFC borrowings (short-term, 15-17% cost) taken mainly for solar projects (90-120 days tenure). Plan to restructure post-H1 FY27 to 8.5-9.5% via banks and repay via internal accruals. No aggressive leverage.

👉Strategic initiatives:

💠SGAEPL acquisition → instant regulatory approvals CBG entry.

💠Desco BioGreen Pvt Ltd (WOS) → dedicated green energy platform.

💠DESCO GLOBAL FZ-LLC (UAE) → international EPC push; currently on hold due to Middle East crisis but long-term opportunity in gas infrastructure.

💠Green hydrogen: MOU signed; plans to blend into CGD network once economics improve (solar park required for viability). EPC will be executed in-house.

💠Customer mix (CGD): ~70-72% PSU (BPCL, GAIL, IOCL, IGL etc.), 28-30% private blue-chips (Torrent Gas, Adani Total Gas).

💠Raw material & bidding discipline: Private clients often provide free-issue material; PSUs require full supply by company. Management committed to margin discipline — selective bidding only; rejected low-margin work during recent crisis-driven demand surge

———

🔗 smeresearch.github.io/SMEGem…

———

#SMEGems #SME #DescoInfratech #Desco #SME

Mar 26

👉Mainboard stocks often get all the attention but some of the most compelling businesses are hiding in plain sight — on the SME Platform.

👉Smaller. Less covered, though noisy at times. Yet occasionally, genuinely exceptional.

———

👉Introducing SME Gems — a new independent series on Hidden Champions of the SME Platform :

💠 OBSC Perfection

💠 Aimtron Electronics

💠 Yash Highvoltage

💠 CFF Fluid Control

💠 DSM Fresh Foods

💠 L.T. Elevator

💠 Monolithisch India

💠 GSM Foils

👉Across Different Sectors. One common place.

🔗 smeresearch.github.io/SMEGem…

👉Stay tuned for more insights

———

⚠️ For educational purposes only. Not investment advice. Please DYODD.

#SMEGems #SMEPlatform #HiddenChampions #SME

3

3

39

8,618

Apr 30

Geleceği emekle, dünyayı sevgiyle yeşertiyoruz! 🌍✨

BİOGREEN A.Ş. olarak tüm emekçilerin #1Mayıs Emek ve Dayanışma Günü’nü kutlarız. Yaşasın haklı ve onurlu emek! ✊🌿

#Biogreen #1Mayıs #İşçiBayramı

1

4

15

Every vote matters—and so does every daily choice. 🌍

Vote for clean air, healthy soil, and a plastic-free future.

Choose sustainability. Choose a greener tomorrow.

Go Green. Go Biogreen.

🌐 biogreenprojects.com/

📞 9830022887

#Biogreen #GoGreen #Sustainability #PlasticFree

2

10

Apr 24

Weedyshopより🌿

5月から高品質カンナビノイドリキッド🪄、ハーブの入荷再始動します‼️

全てCBNは不使用のものしか入荷致しません。が、CBNに変わる体感の物質も出てきてるので体感は間違いないと思います🤩🌈

リキッドはBGL(biogreen)さんと打ち合わせ中、また体感の強さで好評のSAWWEED社のリキッド🪄も入荷予定‼️今しばらくお待ちください🫠🫶

#weedyshop

1

2

13

567