The treasury question is: where does the BTC go after the transaction clears? If they're converting to AED on the spot through a payment processor, this is just Bitpay with a different logo. The real signal would be holding crypto on the balance sheet

11

btcpayserver solving the merchant custody gap is underappreciated. accepting bitcoin without routing through coinbase or bitpay is the difference between actual ownership and exposure.

18

Jun 13

Pretty wicked to say but crypto is a pretty hot trend to get into right now

Bitcoin is at a Really good price to jump in before it hits $100K again, and all over the news

Meme coins are launching daily (do your research)

And also,

$BITPAY remains reliable 💎

32

We’ve added ForumPay to our checkout. Enjoy more ways to pay alongside our long-standing BitPay support.

99

BitPay turns 15. Party’s in the app.

✅ No BitPay fees on your first crypto buy via @SimplexCC

✅ Boosted gift card offers (US only)

Your invite: bitpay.onelink.me/Cenw/bitpa…

5

742

Jun 11

Yep welcome to the club x.=.x sure does seem that they're slowly getting everybody in the community. It's been really difficult to commission artists like I used to. Hoping more people switch over to alternatives like cashapp or bitpay!

2

498

BitPay turns 15 this month. Fifteen years of building crypto payments.

From the first Bitcoin transaction in 2011 to a global ecosystem that makes crypto payments work for real people and real businesses.

Here’s to building the next 15. We’re celebrating all month with deals in the app.

3

520

This is a Uri example that can be used by anyone to send to a sponsor, customer, etc, and get paid right away:

bitcoincash:qrtv37u522gz8a5lezfqk5vukly93cu7gc8tn09040?amount=0.00496820&message=Great job with compass-pay

Works in any major BCH wallet also in stack/bitpay😎

Are you are creator? Freelancer? Get yourself a BCH payment link and send to your supporters via chat, WhatsApp, telegram, etc and get paid instantly. No bank, no intermediaries, free to use. Just visit: compasspay.cash

Works on selene, Paytaca, EC, etc

Use BCH tools.

1

1

77

Jun 10

Doesn't hurt to educate!

If you're a merchant and you want to accept and keep Doge, use BitPay. If you're a merchant and want to tap into crypto buyer market, but don't have the flexibility or appetite for price volatility, consider Moonpay.

At the end, you hope that the more Doge being spent will eventually push more adopters on the consumer AND merchant side. Personally, I hope Moonpay adds the ability for merchants to accept payment and keep Doge.

1

3

30

Jun 10

Skip Tria and look into BitPay or Coinbase Card for lower fees and better daily utility.

1

1

20

There's also coinpayments.net, which has been allowing merchants to accept Dogecoin for about a decade.

And they only charge 0.75%

HoD's takes 1%. 😆

Bitpay accepts Dogecoin.

So does Coinbase Commerce.

1

3

6

112

Jun 10

"The next step is to give merchants the option to keep the doge"

This option already exists with Bitpay terminals for example.

3

23

Jun 10

Bitpay card hasn’t been available in the US for quite some time now. Not sure who wrote this article

1

107

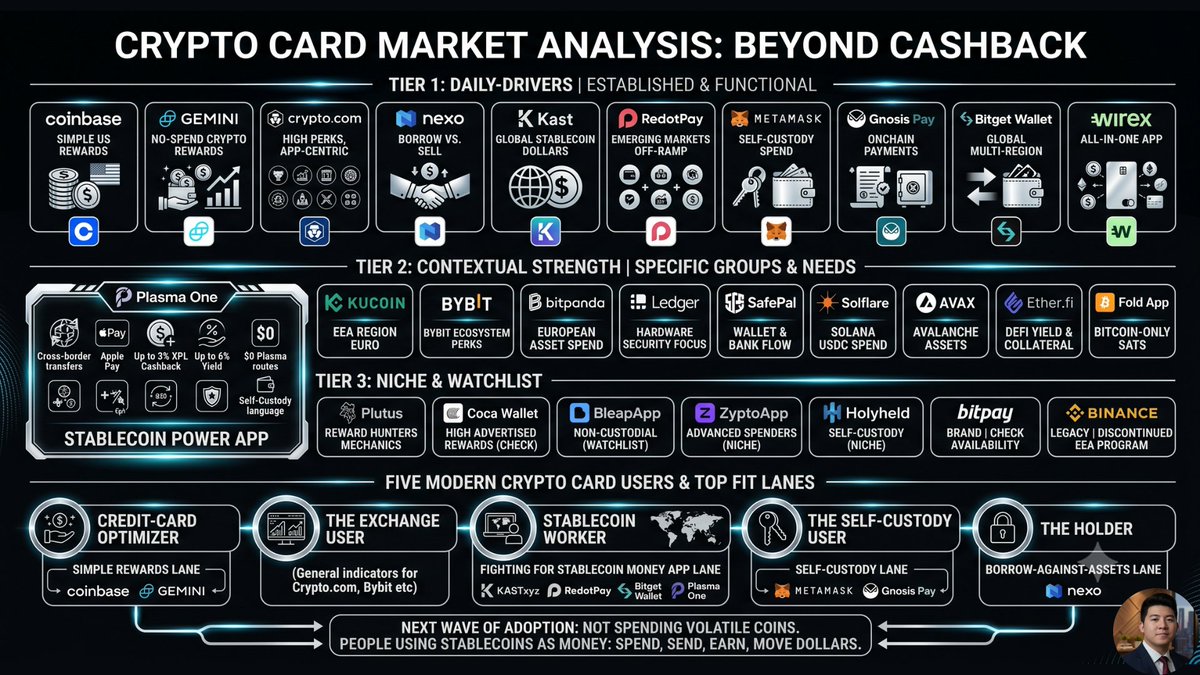

i spent time looking at the crypto card market and the biggest mistake people make is ranking them only by cashback

cashback is the easiest number to market

the real question is:

where does your money already live?

that decides which card actually makes sense

after filtering out legacy, unclear and overly niche cards, i’d split the market into 3 tiers

----------------------------------------------------

tier 1: real daily-driver crypto cards

these are the cards that can realistically become someone’s main card today because they already have a clear user base, clear payment flow, and enough real-world utility.

→ @coinbase

best for u.s. users who want simple crypto rewards from normal spending.

→ @Gemini

best for people who want crypto rewards without spending their actual crypto. strong fit for users who already treat credit cards seriously and pay balances on time.

→ @cryptocom

best for loyal crypto.com users who already live inside that app and can make the perks worth it.

→ @Nexo

best for holders who want to borrow against crypto instead of selling. this fits people who want liquidity while keeping exposure.

→ @KASTxyz

best for global dollar users, freelancers, remote workers, and stablecoin-native spenders who need a practical money app.

→ @RedotPay

best for emerging-market users who care about crypto spending, payouts, local rails, and practical off-ramp access.

→ @MetaMask

best for self-custody users who already use metamask and want to spend from wallet balances.

→ @gnosispay

best for onchain users who care about self-custody, safe accounts, and wallet-native payments.

→ @BitgetWallet

best for users across asia, europe, and latam who already use bitget wallet and want USDT/USDC spending with mobile wallet support.

→ @wirexapp

best for users who want a long-running crypto payment app with card, wallet, exchange, and multi-currency features in one place.

----------------------------------------------------

tier 2: strong cards for the right user

this is where i’d put the products that can become extremely strong, depending on the user’s region, wallet, chain, or spending behavior.

→ @Plasma

i personally use this one, and i’m watching it closely.

for me, the interesting part is the positioning.

Plasma One is clearly going after the stablecoin user.

→ virtual and physical Visa card

→ Apple Pay on iOS

→ stablecoin transfers across borders

→ up to 3% cashback in XPL

→ up to 6% yield on balances, depending on tier and terms

→ $0 transfers on Plasma routes

→ self-custody language where the stablecoin

→ balance backing the card is owned by the user

that combination matters because stablecoin users behave differently from normal exchange users.

if the product keeps tightening the card experience, country coverage, android support, and community referral loop, it can sit in a strong lane:

stablecoins as everyday money.

that is a different fight from “earn points on your credit.”

→ @kucoincom

good for EEA kucoin users who want to spend supported crypto and EUR through a virtual or physical card.

→ @Bybit_Official

strong for bybit users who already keep funds there and want rewards, auto-interest, and subscription perks. region access matters a lot here.

→ @Bitpanda

good for european users who already hold assets on bitpanda and want to spend from the same app.

→ @Ledger

best for people who care about hardware wallet habits and want a card connected to that safer custody mindset.

→ @iSafePal

good for safepal users who want a wallet plus banking-style flow. stronger for people already inside the safepal stack.

→ @solflare

best for solana users who want to spend USDC from a self-custody wallet.

→ @avax

best for avalanche-native users who hold AVAX, USDC, USDT, or other supported avalanche assets.

→ @ether_fi

best for defi users who understand yield, collateral, and smart contract risk. this is more advanced-user territory.

→ @fold_app

best for bitcoin-only users who want to stack sats from normal spending.

----------------------------------------------------

tier 3: niche, watchlist/legacy

these cards may still be useful, but i wouldn’t place them in the core comparison unless the user has a very specific reason.

→ @plutus

more for reward hunters who are comfortable with token mechanics.

→ @coca_wallet

interesting, but high advertised rewards need careful checking.

→ @BleapApp

worth watching, especially for non-custodial stablecoin card users in europe.

→ @ZyptoApp

more niche, especially for high-limit or advanced crypto spenders.

→ @holyheld

interesting for self-custody users, but still more niche.

→ @BitPay

useful brand for crypto payments, but the card side needs clearer active availability before ranking it highly.

→ @binance

legacy reference in many markets because the EEA card program was already discontinued.

----------------------------------------------------

crypto cards are no longer one category.

there are at least five different users now.

→ the credit-card optimizer

→ the exchange user

→ the stablecoin worker

→ the self-custody user

→ the holder who wants liquidity without selling

@coinbase and @Gemini win the simple rewards lane.

@Nexo wins the borrow-against-assets lane.

@MetaMask and @gnosispay win the self-custody lane.

@KASTxyz, @RedotPay, @BitgetWallet, and @Plasma are fighting for the stablecoin money app lane.

that last lane is the one i’m most interested in.

because the next wave of crypto card adoption probably won’t come from people trying to spend volatile coins at coffee shops.

it’ll come from people who already use stablecoins like money and need a better way to spend, send, earn, and move dollars across borders.

47

71

1,551

You fooled me

@grok

No, Walmart does not accept on-chain Bitcoin (or any cryptocurrency) directly for in-store purchases. It also does not support Lightning Network, Bitcoin Cash, or any native crypto payments at checkout. The viral claim in the tweet is exaggerated hype built on OnePay app features, not actual Bitcoin acceptance.

How the OnePay setup actually works

OnePay (a fintech majority-owned by Walmart) added Bitcoin and Ethereum trading/custody to its app around late 2025/early 2026 via a Zerohash partnership. Users can:

• Buy, hold, and sell BTC (and ETH, sometimes mentioned with XRP) directly in the OnePay app.

• When sold, proceeds automatically convert to USD and land in the user’s OnePay cash/checking balance.

• Pay at Walmart checkout using the OnePay Wallet/app (often by scanning a barcode or linked payment). Walmart’s point-of-sale system sees and processes only fiat USD — never crypto.

Key limitations:

• You must sell the Bitcoin first inside the app. There is no direct “spend Bitcoin like cash” or sats sent to Walmart.

• The merchant (Walmart) never receives on-chain Bitcoin, Lightning payments, or any crypto.

• Walmart’s own corporate fraud alerts page states plainly: “Walmart does not accept or send crypto in stores.”

What the tweet gets wrong

• “ANNOUNCED it will NOW accept Bitcoin payments in store” — Misleading. No such direct acceptance exists. Headlines and posts often blur “crypto in the OnePay app” with “Walmart accepts BTC at checkout.”

• “IMMEDIATELY spend Bitcoin like cash” and “1,000,000,000 monthly customers” — Overstated. Walmart cites roughly 150 million weekly U.S. shoppers/visitors in related coverage; the 1B figure is hyperbolic. Conversion to fiat is required first.

• No evidence of Lightning-only, on-chain-only, or Bitcoin Cash involvement. Coverage centers on BTC/ETH trading inside the custodial app.

This is a convenient custodial bridge for people already using OnePay (easy in-app sell → spend USD at Walmart), but it is not Bitcoin adoption in the sense of merchants receiving sats or Lightning payments. Similar hype cycles have appeared before (e.g., the 2021 fake Litecoin partnership Walmart publicly debunked).

For real Bitcoin spending options at retailers, look to Lightning-enabled merchants, BitPay-powered gift cards, or services that actually push sats or Lightning to the seller — none of which apply to standard Walmart checkout today.

The image in the tweet is classic crypto Twitter meme format (Walmart exterior glowing BTC). It drives engagement but does not reflect the actual payment rails. Always verify claims against primary sources like OnePay’s help center, CNBC reporting on the rollout, or Walmart’s corporate statements.

1

1

2

114