May 28

Blue Water Logistics Ltd Concall Summary for Q4FY26

MANAGEMENT COMMENTARY

• FY26 marked transformational growth phase

• Expanded operations across 28 countries

• Asset-backed logistics platform strengthening

• Focused on end-to-end supply solutions

• Strong confidence post successful listing

OUTLOOK

• Revenue expected doubling over years

• ISO tank share targeting 20%

• Air freight targeting 30% revenue

• Fleet expansion beyond 5,000 tanks

• PAT margins expected improving further

INDUSTRY

• Geopolitical tensions disrupting trade routes

• Logistics demand supported by manufacturing

• Government infrastructure aiding sector growth

• Vietnam and Indonesia seeing opportunities

• Trade shifts creating fresh logistics demand

COMPETITIVE POSITION

• Integrated logistics model provides advantage

• In-house infrastructure improving profitability

• Strong multinational customer relationships maintained

• Diversified customer base reducing risks

• Minimal bad debts across operations

RISKS

• Trade receivables rose sharply Q4

• Hormuz tensions impacting shipping routes

• Expansion dependent on debt funding

• Global security risks remain elevated

• Rapid scaling execution remains critical

GROWTH DRIVERS

• Expansion planned across Southeast Asia

• Turkish Airlines partnership boosting air cargo

• ISO tank fleet expansion accelerating

• Dry container business scaling gradually

• Project cargo vertical under development

PRODUCT MIX

• Ocean freight contributes around 70%

• Air freight reached 13% contribution

• ISO tanks contribute around 8%

• Direct business contributes nearly 85%

• High-margin niche logistics expanding steadily

FINANCIALS

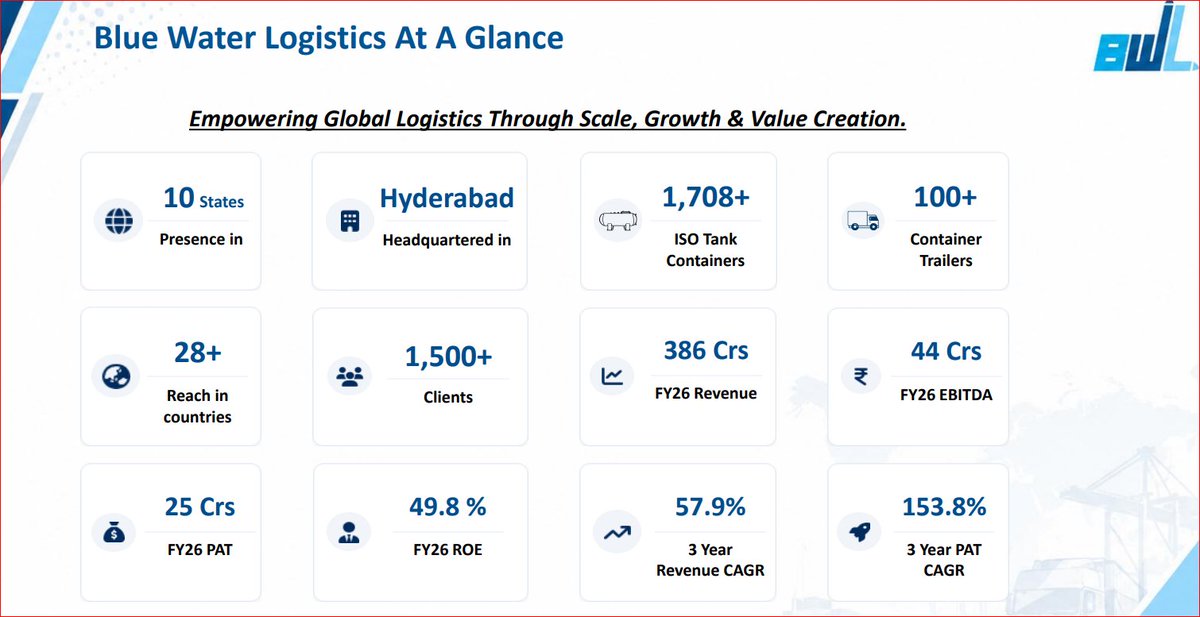

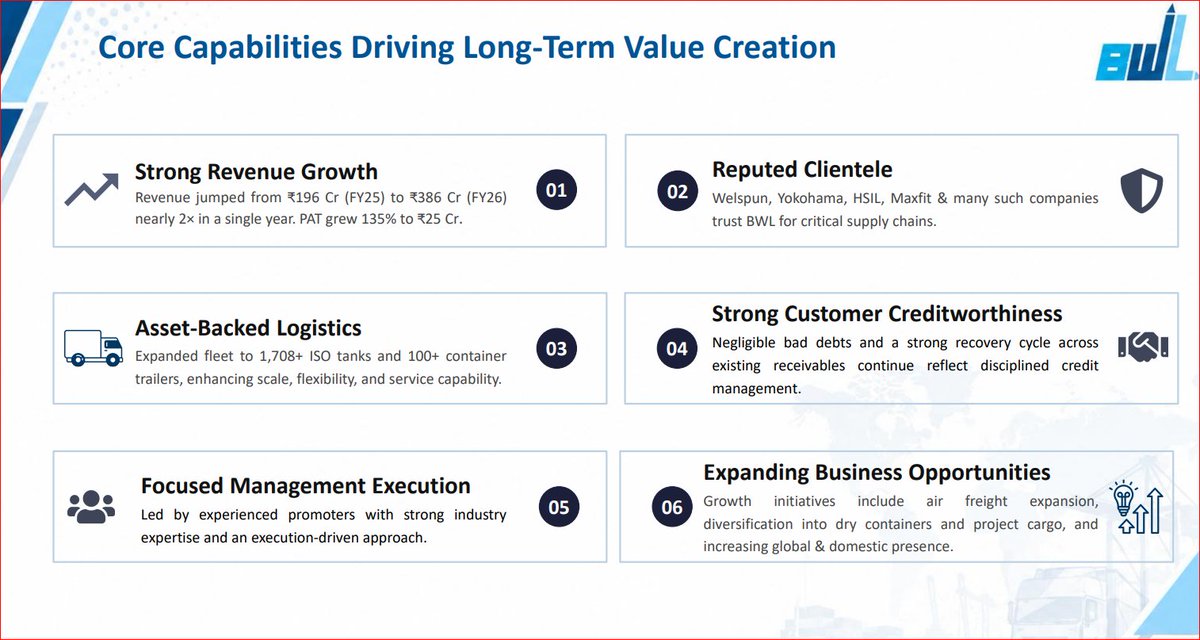

• FY26 revenue reached ₹386 Cr

• EBITDA grew 134% YoY

• EBITDA margin improved to 11.4%

• PAT grew 135.4% YoY

• PAT margin stood at 6.5%

CONCLUSION

• Company entering aggressive expansion phase

• Asset-backed strategy improving operational control

• High-margin segments driving profitability growth

• International expansion strengthening long-term outlook

• Strong execution supporting scalable growth story

#Q4results #sharemarket #stockmarket #BlueWaterLogistics @rajiv_phantom @barathhbm @_Investor_Feed_

1

7

578

May 26

#SME #BlueWater #BlueWaterLogistics

Blue Water Logistics H2FY26 Concall Highlights

👉 FY27 & Future Outlook

▫️ Management is confident of delivering similar growth trajectory as FY26 implying ~2x growth in FY27 with continued momentum into FY28.

💠 Driven by fleet expansion, new service verticals, and geographic diversification.

▫️ NVOCC / Container Logistics (ISO tanks upcoming dry containers) contribution targeted to rise sharply from ~8% of FY26 revenue to ~20% in FY27.

💠 Air freight contribution expected to increase significantly from ~13% to closer to 30%.

▫️ ISO Tank fleet expansion: Current 1,708 tanks; long-term target 5,000 tanks in next 3 years. Additions will be reviewed quarterly based on utilization.

💠 Dry container fleet and project cargo to be added aggressively on EMI/financed basis (no major upfront Capex).

▫️ Resilience to global disruptions: Minimal impact from Red Sea/Hormuz tensions (most ISO tanks in other regions; freight forwarding rerouted safely). Geopolitical volatility viewed as an opportunity rather than challenge.

▫️ Margin trajectory:

💠FY26 PAT margin at 6.5% (up 100 bps YoY)

💠Management expects sustained margins with further improvement in FY27 through higher-margin NVOCC/dry container business, better scale, and operational efficiency.

💠EBITDA margin stable/improving around 11.4%.

💠 Focus on asset-backed model, in-house end-to-end services, and credit management to support margin expansion.

▫️ Strategic growth drivers:

💠Air freight expansion via new airline partnerships (including exclusive tie-up with Turkish Airlines), entry into dry containers & project cargo, fleet additions, deeper customer integration

💠International expansion into Southeast Asia (Thailand, Vietnam, Indonesia in next 2 months; Malaysia & China by year-end) stronger Middle East/Red Sea presence.

👉 Current Order Book / Projects and Future Pipeline

▫️Fleet pipeline includes continued addition of ISO tanks (target 5,000 in 3 years) and new dry container fleet on EMI structure.

💠Trailer fleet already expanded to 100 .

▫️ Geographic & vertical expansion pipeline:

💠 Southeast Asia (Thailand, Vietnam, Indonesia, Malaysia) and China — key manufacturing/trade hubs — to be operationalized in phases over next 6–9 months.

💠 Air cargo: Exclusive partnership with Turkish Airlines already secured for pharma and other high-volume sectors from Hyderabad; new customer onboarding (e.g., pharma majors) expected to contribute from H2 FY27.

💠 Project cargo and dry container diversification already initiated; NVOCC operations scaling up.

💠 Domestic footprint strengthening across 10 states with new branch offices (Mumbai, Chennai, etc.) driving new client additions.

▫️ International network: 28 countries reach; associations with JCtrans, Global Logistics Alliance, FIATA, Neptune NVOCC, etc. Pipeline focused on higher-margin international trade corridors.

👉 Other Notable Points

▫️ FY26 Asset base: 1,708 ISO tanks, 100 container trailers, 6 fumigation units.

▫️ Clientele & Business Quality:

💠1,500 clients including reputed names (Welspun, Yokohama, HSIL, Maxfit, Hetero, Aurobindo, etc.).

💠~85% direct B2B business.

💠Negligible bad debts, disciplined credit cycle.

💠Receivables elevated due to strong Q4 growth and new customer onboarding but improving rapidly (30–35% already collected post-March; average 60–90 days).

▫️ Asset-backed & Integrated Model:

💠End-to-end capabilities (Ocean, Air, Surface/Rail, NVOCC Tank, Customs, Value-added services)

💠Own fleet, warehousing, and in-house customs clearance provide margin advantage and control.

💠ISO 9001:2015 & IATA certified.

▫️ Funding & Liquidity: Growth to be funded primarily through debt/EMI structures (Citibank, Axis, HSBC etc.) and internal accruals. BBB /Stable credit rating. No immediate equity dilution planned.

Mar 26

👉Mainboard stocks often get all the attention but some of the most compelling businesses are hiding in plain sight — on the SME Platform.

👉Smaller. Less covered, though noisy at times. Yet occasionally, genuinely exceptional.

———

👉Introducing SME Gems — a new independent series on Hidden Champions of the SME Platform :

💠 OBSC Perfection

💠 Aimtron Electronics

💠 Yash Highvoltage

💠 CFF Fluid Control

💠 DSM Fresh Foods

💠 L.T. Elevator

💠 Monolithisch India

💠 GSM Foils

👉Across Different Sectors. One common place.

🔗 smeresearch.github.io/SMEGem…

👉Stay tuned for more insights

———

⚠️ For educational purposes only. Not investment advice. Please DYODD.

#SMEGems #SMEPlatform #HiddenChampions #SME

2

2

20

2,968

May 20

📦 BLUE WATER LOGISTICS clocks another quarter of massive growth 🔥🔥

💥 Revenue jumps 158% YoY to ₹135 Cr

💥 EBITDA surges 113% YoY to ₹15.4 Cr

💥 PAT doubles to ₹9.19 Cr

💥 PBT up 116% YoY

QoQ growth also remains strong 👇

📈 Revenue: 20% QoQ

📈 EBITDA: 19% QoQ

📈 PAT: 24% QoQ

FY26 Snapshot 🔥

✅ Revenue: ₹386 Cr

✅ PAT: ₹25.2 Cr

✅ EPS: ₹23.97

Margins slightly softened due to aggressive scale-up, but growth momentum is turning heads

This is the kind of earnings acceleration the market starts rerating fast...

Follow @Rakesh_Invest for more such hidden gems & earnings breakdowns 🚀

#BlueWaterLogistics #Investment #LNPR #Earnings #Multibagger

2

12

1,883

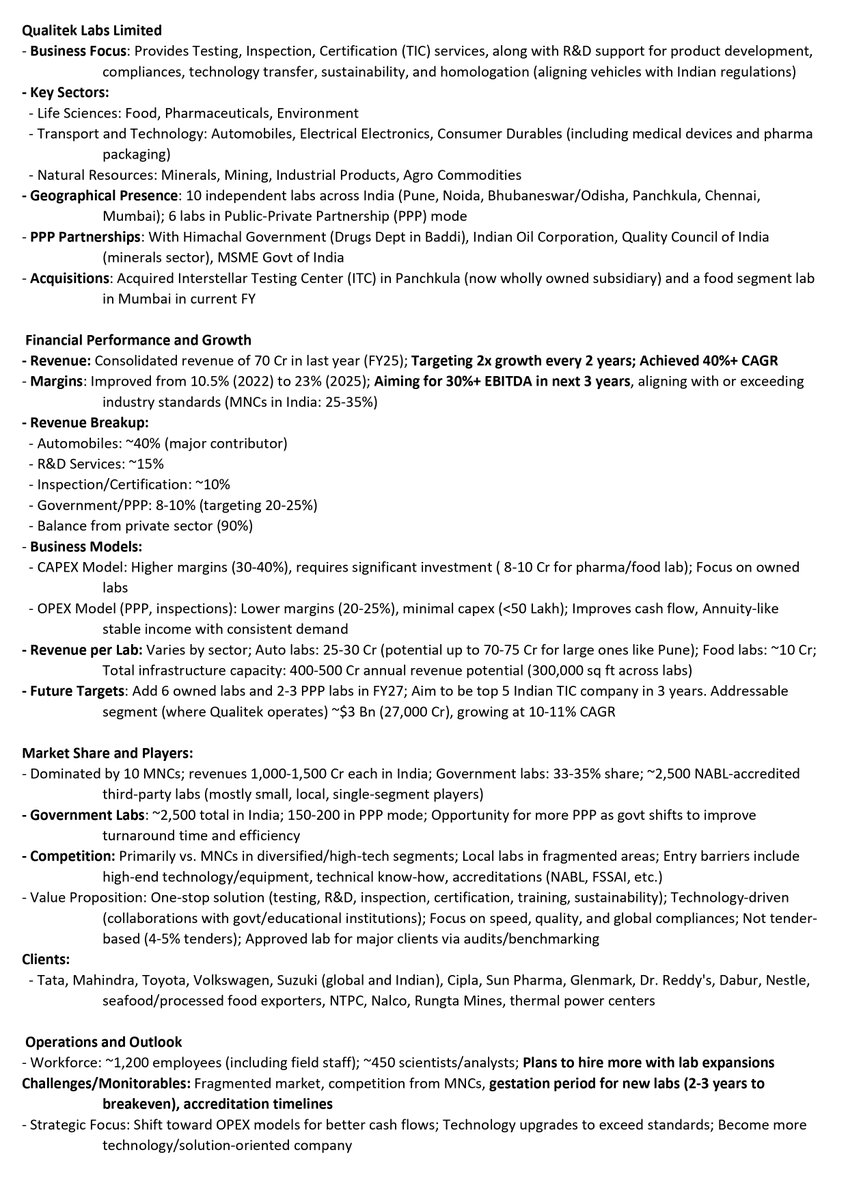

Mar 6

Arihant Bharat Connect Conference March '26:

👉Day 1:

💠Qualitek Labs

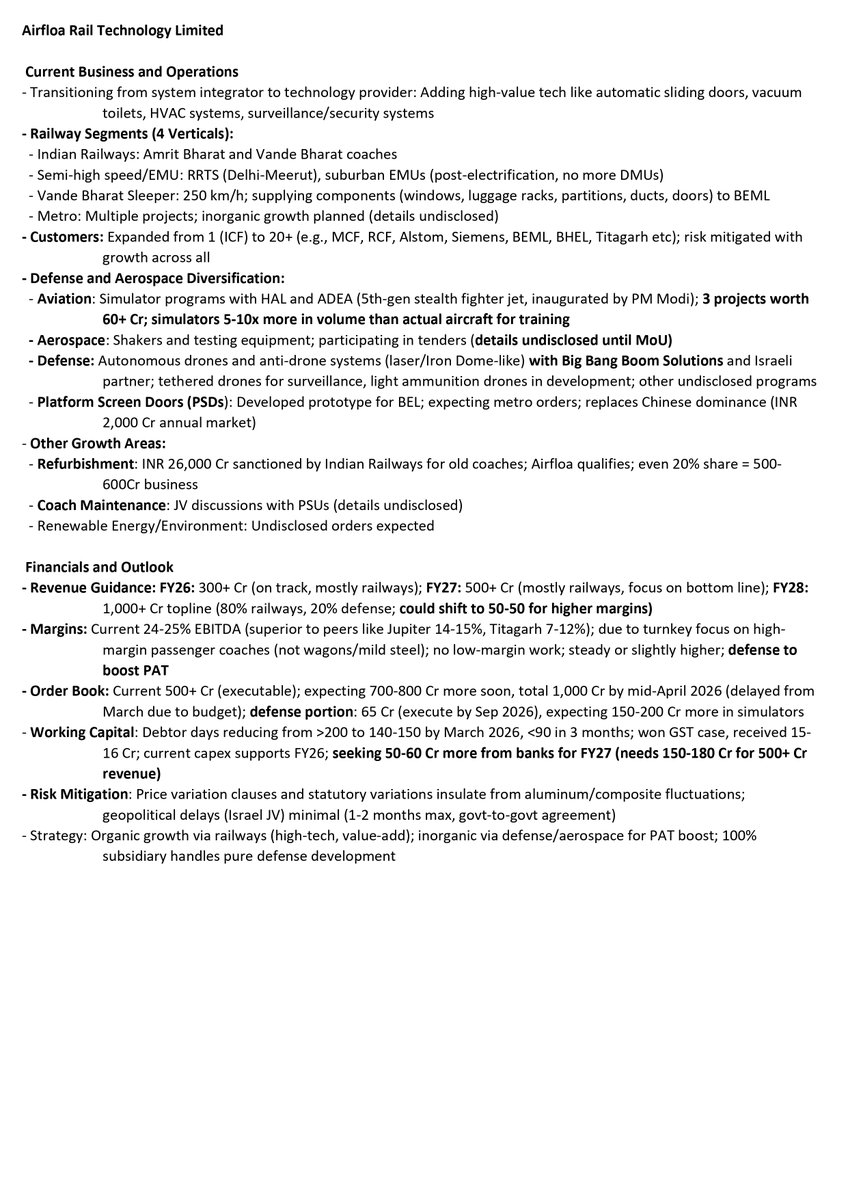

💠Airfloa Rail Technology

💠Blue Water Logistics

💠Sat Kartar Shopping

💠Influx Healthtech

💠Shubhshree Biofuels

💠Virtual Galaxy Infotech

💠WOL 3D India

💠Pro FX Tech

💠New Malayalam Steel

#qll #qualitek #airfloa #bluewater #shubhshree #bluewaterlogistics #bwl #satkartar #influx #vgil #virtualgalaxyinfotech #wol3d #profx #nmsteel #bharatconnectconference #arihantcapital

8

14

107

23,598

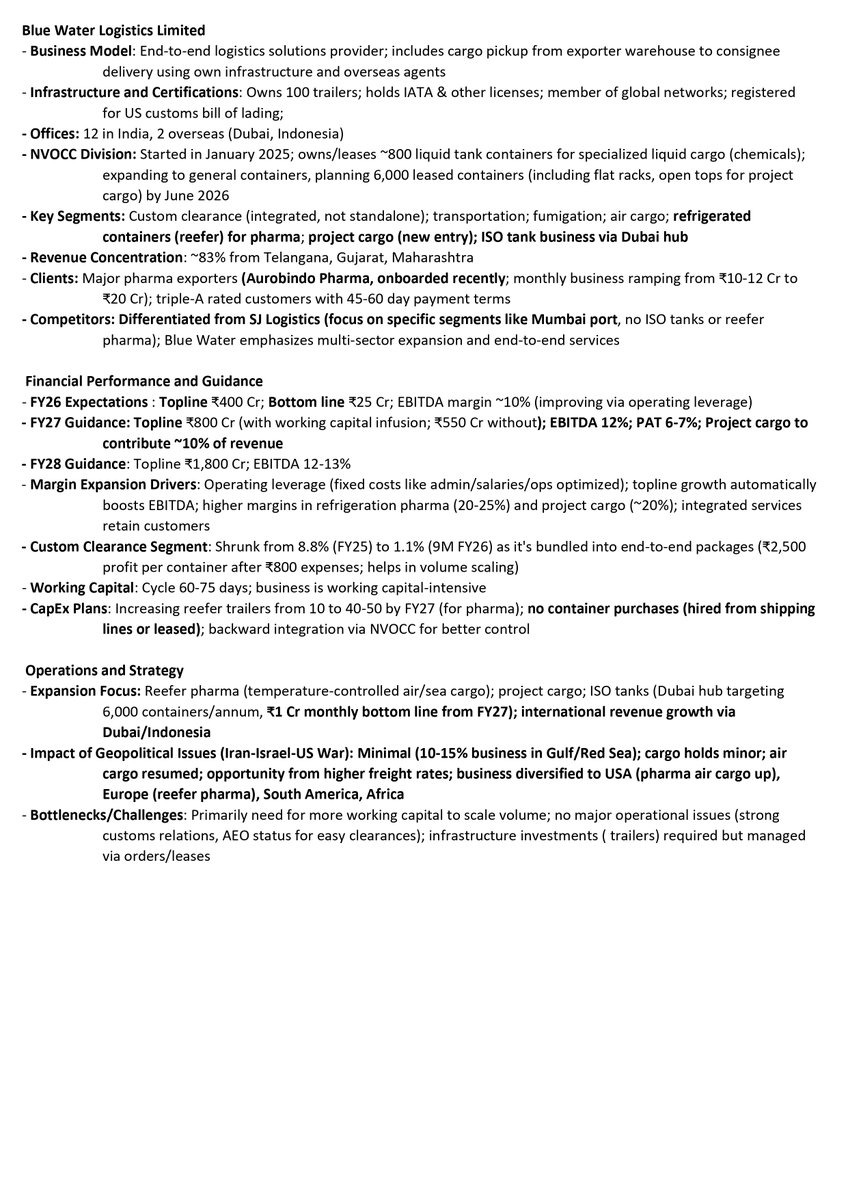

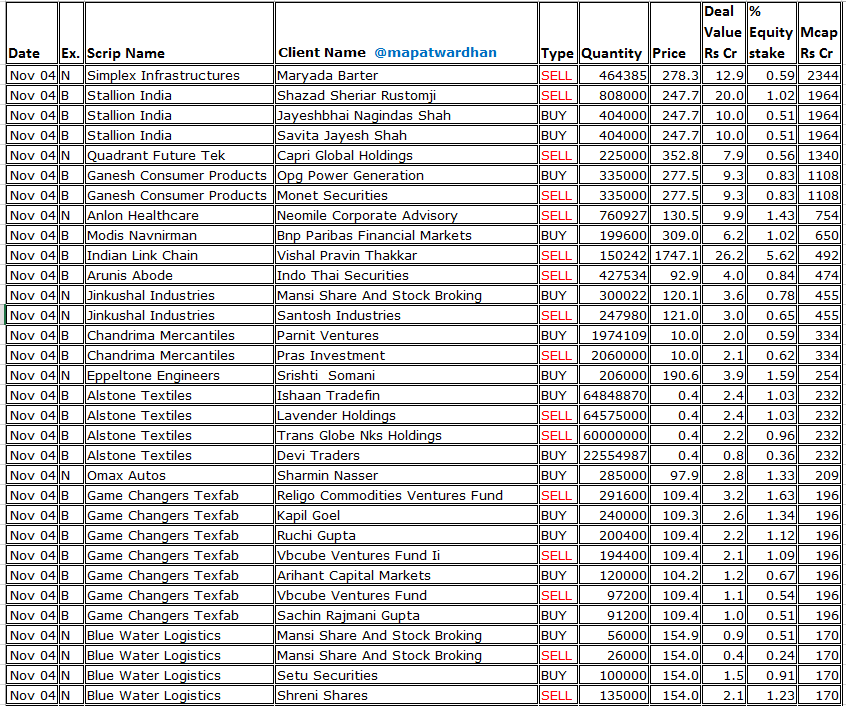

4 Nov 2025

*Today's bulk / block deals*

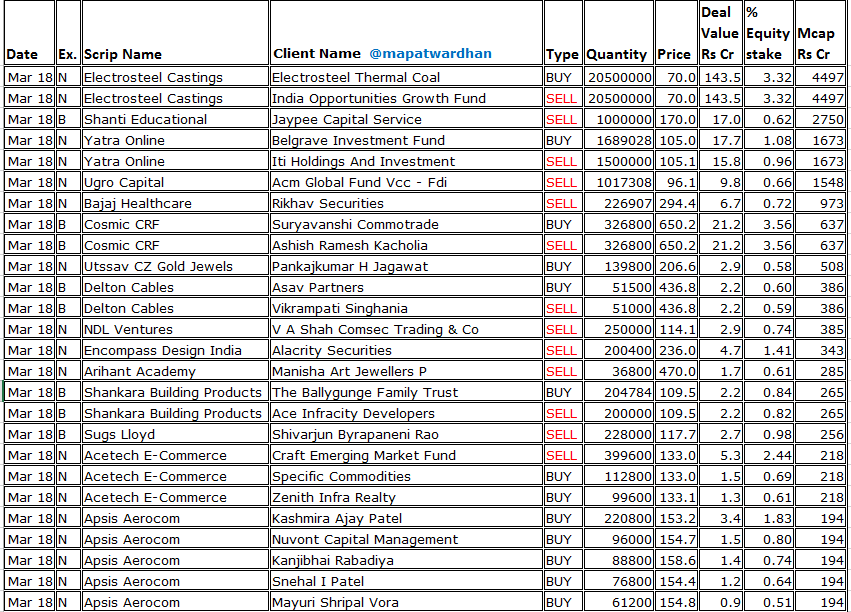

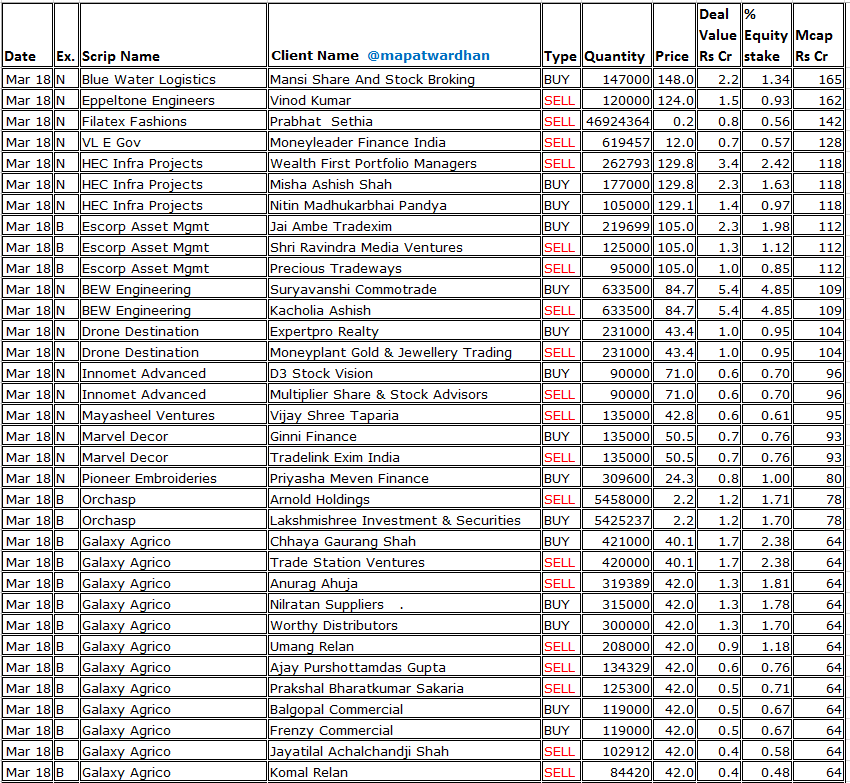

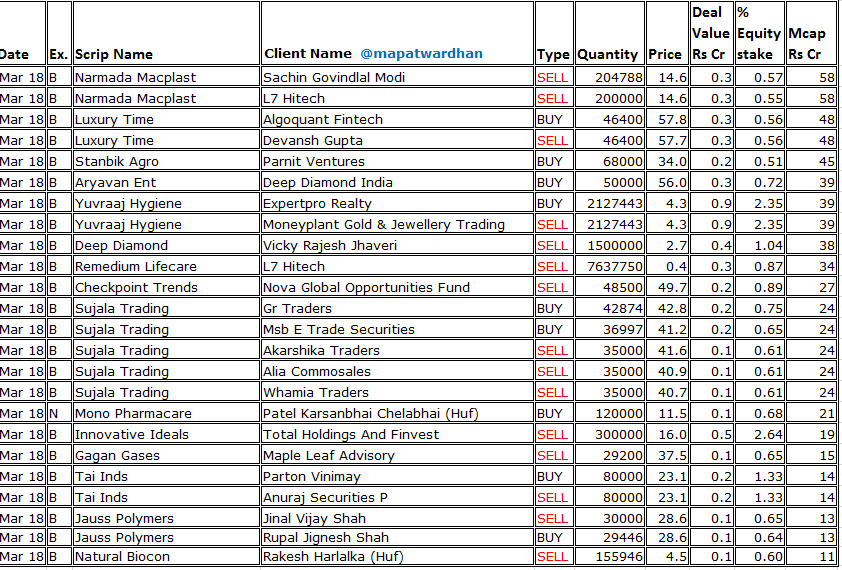

#SimplexInfra #StallionIndia #QuadrantFuture #GaneshConsumer #AnlonHealthcare #ModisNavnirman #IndianLinkChain #ArunisAbode #ChandrimaMercantiles #EppeltoneEngineers #AlstoneTextiles #OmaxAutos #TrueUno #BlueWaterLogistics #IndianEmulsifiers

1

19

1,772

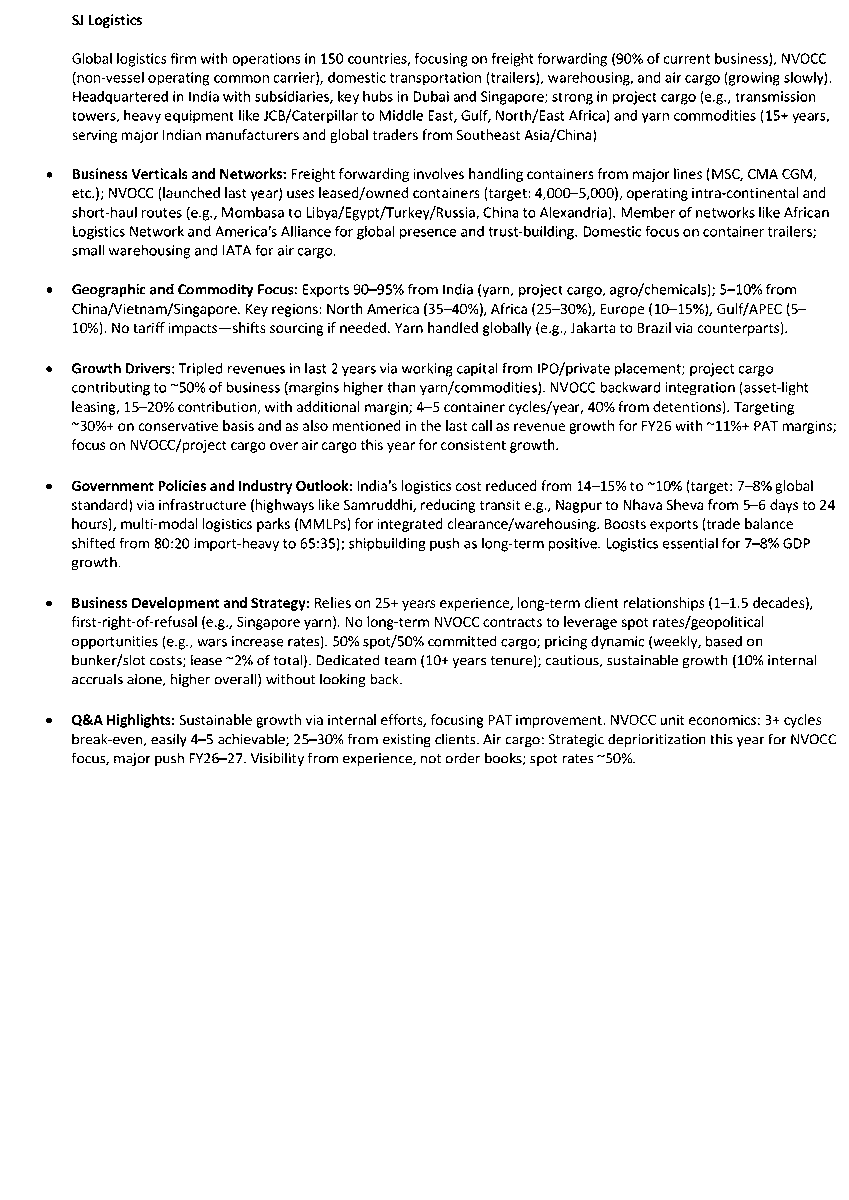

25 Sep 2025

Arihant Bharat Connect Conference :

💠SJ Logistics

💠Blue Water Logistics

💠Shubhshree Biofuels

💠Sahaj Solar

#sjlogistics #bluewaterlogistics #bluewater #shubhshree #shubhshreebiofuels #sahajsolar #sahaj #arihant #bharatconnectconference #arihantcapital

25 Sep 2025

Arihant Bharat Connect Conference :

💠Chemkart India

💠Influx Healthtech

💠Sacheerome

💠Glen Industries

#Chemkart #Glen #Influx #GlenIndustries #InfluxHealthtech #Sacheerome #arihant #bharatconnectconference #arihantcapital

1

1

24

20,132

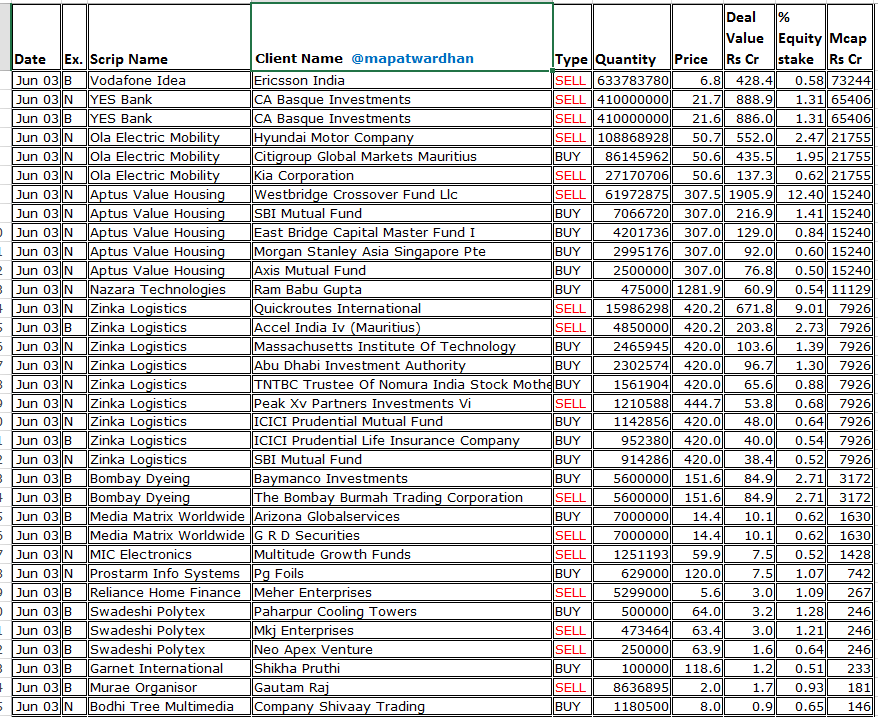

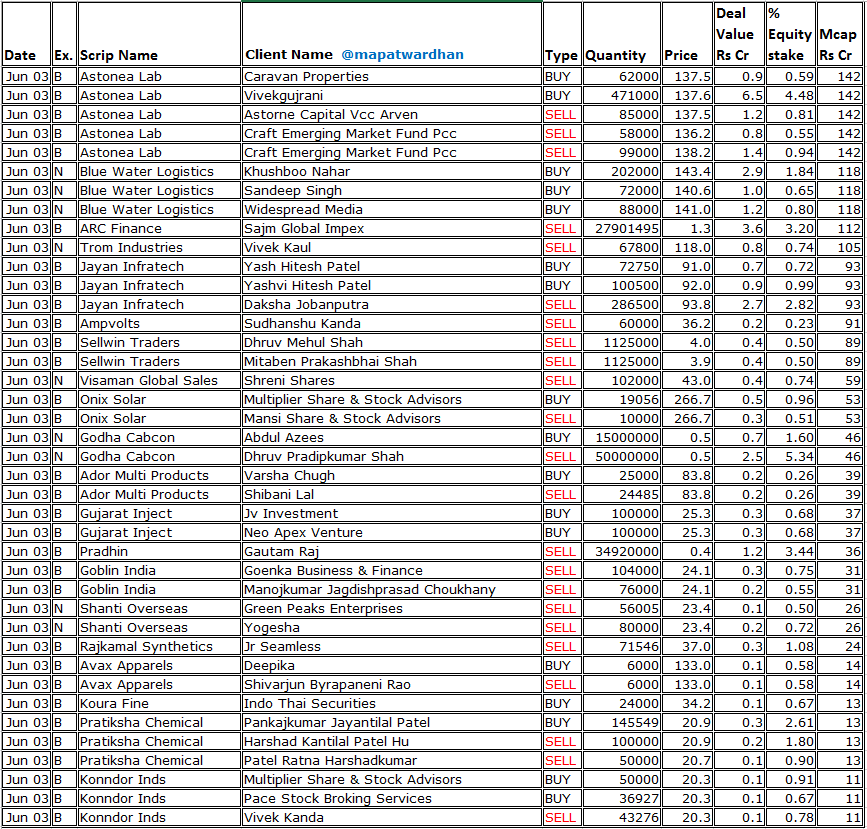

3 Jun 2025

*Today's bulk /block deals*

#VodafoneIdea #YESBank #OlaElectric #AptusValue #NazaraTech #ZinkaLogistics #BombayDyeing #MMWL #MICElectronics #ProstarmInfo #RelianceHome #SwadeshiPolytex #GarnetInternational #MuraeOrganisor #BodhiTree #AstoneaLab #BlueWaterLogistics #ARCFinance

1

20

5,703

3 Jun 2025

Awesome ! Your position makes me believe how to play like an actual ‘Wealthy Retailer’

I sold all Aegis yesterday in minor profit

Holding 50% HNI allotment in Leela still- I am not expecting it to move faster than Aegis because of maximum Retail interest here. On all social media and across my network, I saw people applying to Leela with great eagerness and avoiding Aegis stating it is expensive (and less heard name ofcourse) and market rewarding the retailers as expected with loss to 0 profit for now😅😬

Aegis has more big players hence cleaner and uni directional move ⬆️

Also, you did not update on #BlueWaterLogistics #SME IPO but that also listed decent today- Booked 8% there too on the allotted lots - I was very easy allotment there with guaranteed allotment on a 4/5 lot HNI application 😇

1

6

1,232

3 Jun 2025

#MarketsWithBS | #BlueWaterLogistics makes positive debut; shares list at 4.4% premium.

#Markets #sharemarket #StockMarket #stockmarketsindia

mybs.in/2engqGl

1

1,112

30 May 2025

#BlueWaterLogistics #IPO closes with 8.76 times, #Astonea Labs offer subscribed 2.44 times

Visit: kundkundtc.com

.

.

.

.

#KundkundTC #India #StockMarket #trading #IPOAlert #AstoneaLabs #BlueWaterIPO #AstoneaIPO #labs

9

157

29 May 2025

Thread 🧵: 12 Neutral Observations on #BlueWaterLogistics IPO

(For informational purposes only – not financial advice. Please do your own due diligence before investing.)

1⃣ IPO Details & Listing

– Opens May 27–29, 2025 | Price band ₹132–₹135 | Lot size 1,000 | Fresh issue 30 lakh shares → raise ₹40.50 Cr | Lists June 3 on NSE Emerge

2⃣ Business Profile

– Founded 2010; offers freight forwarding, customs clearance, warehousing & multimodal transport via 5 branches & 25-vehicle fleet

3⃣ Promoter Background

– Promoted by L. N. Mishra, L. Panda, M. Mohanty & S. Mishra; evolved from partnership (2010) → Pvt Ltd (2022) → PLC (2024)

4⃣ Financial Performance

– Revenue: ₹98.1 Cr (FY23) → ₹138.7 Cr (FY24) → ₹196.2 Cr (FY25)

– PAT: ₹1.54 Cr → ₹5.94 Cr → ₹10.67 Cr (FY25)

5⃣ Profitability & Returns

– PAT margins: 1.6% → 4.3% → 5.4%

6⃣ Use of Proceeds

– Working capital (fuel, freight guarantees, receivables)

– Capex (new vehicles & body-building)

7⃣ Current Valuation

– Post-issue shares ~1.10 Cr → Market cap ~₹148.5 Cr at ₹135/share

8⃣ Valuation Multiples

– Trailing P/E: ~25× (₹148.5 Cr/₹5.94 Cr)

– Forward P/E: ~14× (₹148.5 Cr/₹10.67 Cr)

9⃣ Leverage & Liquidity

– Borrowings: ₹36.7 Cr vs. Net Worth: ₹20.2 Cr → Gearing ~1.8×

– Opex cash flow turned negative in FY25 on receivables build-up

🔟 Grey Market Sentiment

– GMP ~₹0 (flat) suggests muted listing-pop expectations despite 2.1× subscription by Day 3

1️⃣1️⃣ Peer Comparison

– S J Logistics: P/E ~14.4×

– Brace Port Logistics: P/E ~22.4×

– Paradeep Parivahan: P/E ~7.8×

1️⃣2️⃣ Final Verdict

Blue Water at a ~14× forward P/E sits below high-multiple Brace Port (22.4×) and SJ Logistics (14.4×), yet above budget‐priced Paradeep Parivahan (7.8×). A balanced entry among peers—muted GMP & small float suggest patience and robust due diligence post-listing.

Since already better players with proven track record are available like #SJlogistics #paradeepparivahan at cheap valuations hence will avoid this

No buy sell reco

This thread reflects public filings and market data. #DYOR #LogisticsIPO #SMEIPO #PeerAnalysis

1

3

858

29 May 2025

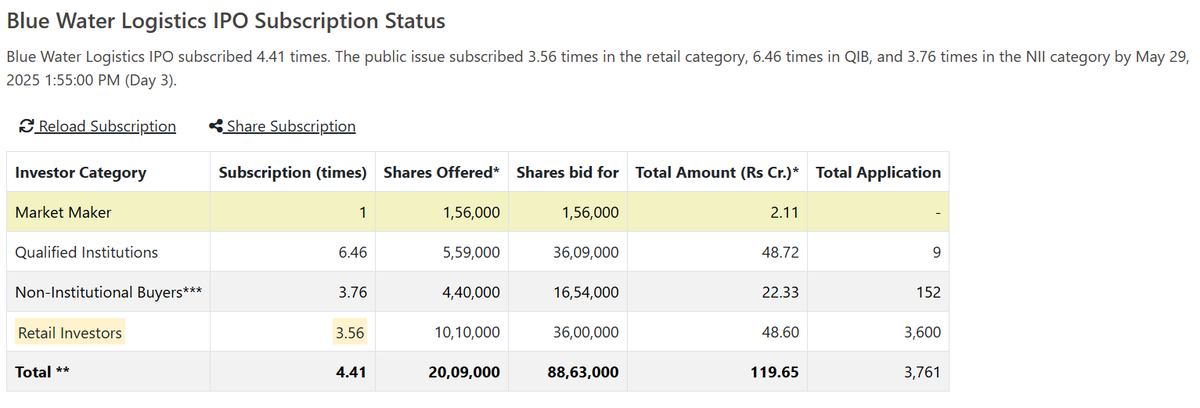

Blue Water Logistics IPO received muted response and subscribed 4.41 times. #Blue #BlueWater #BlueWaterLogistics #IPO #SMEIPO #SME #sebi #sebinis #stock #water #Logistics #transportlogistic2025 #travellove #infrastructure #roadshow #nseindia #NSE #NSEasyConnect #bseindia #BSE

2

663

29 May 2025

#MarketsWithBS | Blue Water Logistics IPO closes today; subscription nears 3x, GMP nil. Check details here

#Stocks #markets #stockmarketindia #stockmarketnews #sharemarket #marketnews #indianstockmarket #BlueWaterLogistics #IPO

mybs.in/2en8aoM

2

1

5

1,388

26 May 2025

इन 9 IPO में पैसे लगाने से पहले सावधान

ET NOW स्वदेश आपको लगातार कर रहा सतर्क

इन IPO's पर जानिए IPO एक्सपर्ट शरण लिलानी की राय 👇

#IPOUpdate #IPOAlert #AegisVopakTerminals #SchlossBangalore #ProstarmInfoSystems #ScodaTubes #BlueWaterLogistics #AstoneLabs #NikitaPapers #NeptunePetrochemical @sharanlillaney @Sharad9Dubey @NewzzPandey @AGaoshinde

2

2

12

2,389

19 May 2025

🚨 Blue Water Logistics Limited SME IPO Alert!

✅ Date: 27-29 May 2025

✅ Price Band: ₹132-135

✅ Market Lot: 1000 Shares

✅ Application Amt: ₹1,35,000

✅ Size: ₹40.50 Cr approx

✅ Retail Portion: 35%

#IPO #SMEIPO #BlueWaterLogistics #StockMarket #Investment #IPOAlert

1

3

227