Apr 26

You sank my boat, the S.S. Bothunter. No fair bringing a modern destroyer against my WWII diesel sub. 😭Take me to the brig... we can have a lot of fun behind bars. Or against them. To the victor go the spoils.🐱

1

6

101

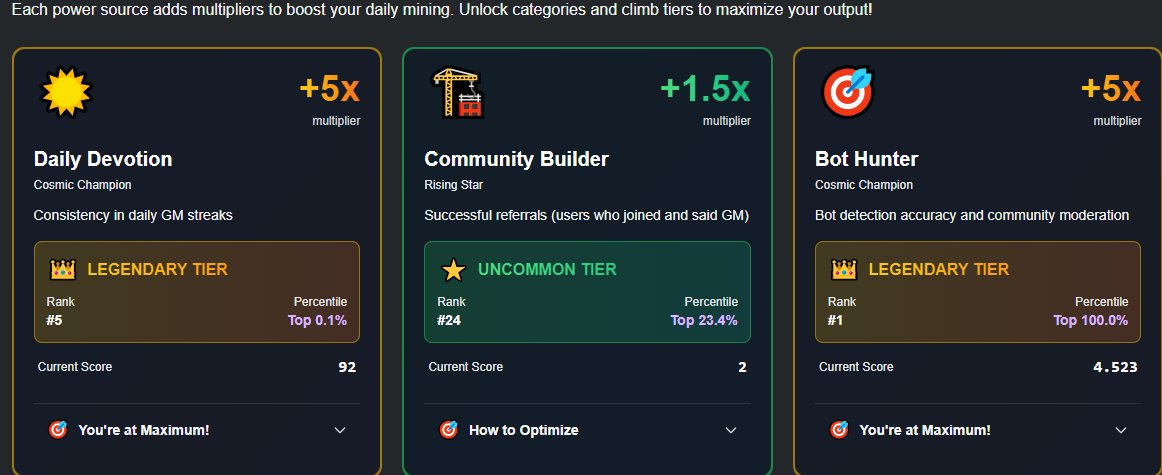

Bot hunter helps improve Discord server security by automatically preventing spam, scams, fake accounts, and raids to maintain member comfort, this is proof of @polana_network 's commitment to building a real community that prioritizes quality over quantity.

#Polana #BotHunter

4

61

The Polana Network family doesn’t move casually.

We operate with discipline, vision, and a professional mindset

to earn high value points that truly matter.

Through new systems and innovative ways to accumulate points,

we’ve opened opportunities that are more rewarding, more engaging, and more meaningful.

And the community has embraced it

with energy, unity, and full support.

This isn’t just about points.

It’s about consistency, contribution, and being part of something built with purpose.

Not joined yet

That means you’re still on the outside

while others are already moving ahead.

Join now and start collecting as many points as possible.

Don’t just watch the journey

be part of it.

Join here

discord.gg/polana

Polana Network

built by those who take action

not by those who wait.

#Polana #Polana_network #gPolana #p2earn #BotHunter #AkashaVoid

4

1

15

239

22 Dec 2025

Bots everywhere ❌

Hunters activated ✅

BOT HUNTER – POLANA NETWORK

Who’s ready? 👀🔥

lets play bot hunter all

#BotHunter #PolanaNetwork

3

39

21 Dec 2025

🚨 Polana Update 🚨

Bot Hunting is now an effective way to earn Polana Points Point Multiplier 🎯

Active contributions = greater boost 🚀

#PolanaNetwork #BotHunter #Web3

3

7

75

20 Dec 2025

Polana Network is in full "human only" mode right now and it's ruthless.

1/ GM streak isn't just a ritual—skip one day and your points multiplier resets. Consistency = rewards. People are hitting hundreds of days just to say "still here" every morning.

2/ BotHunter is on fire. Fake accounts get purged instantly. Want to stay OG? Verify with Humanode in Discord—facial scan, no excuses. Bots get wiped, zero mercy.

3/ The Indo community is going all out: Christmas wish videos to Solana/Polkadot, posts about pSOL bridge, hyping pSOL liquidity injection into Polkadot DeFi.

4/ Dev side is still early—POCs running real Solana contracts on JAM VM, targeting 500K-1M TPS. But right now the vibe is more "prove you're human" than tech specs.

This isn't a chain for spectators. It's for people who grind daily, verify human, and build together. Discord is popping, waitlist/discord link in the official polana.network @polana_network

2

72

20 Dec 2025

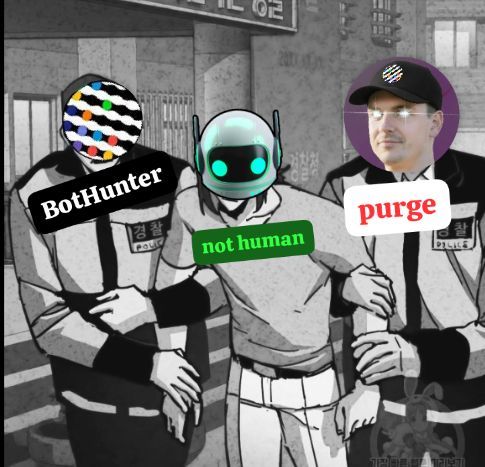

In the world of @polana_network, the line between humans and machines is increasingly blurred.

BotHunter stands on one side, algorithms of judgment on the other.

A single label appears: not human.

No debate. No appeal. Just one decision purge.

This is not about right or wrong.

It’s about who gets to pass when the system holds the control.

Polana is more than just an ecosystem.

It is a test of identity, trust, and the future of digital interaction.

3

1

4

63

16 Dec 2025

new update from @polana_network

bot hunter role now is live, everyone can suggest a bot account for ban and get reward but if they can provide evidence there is a punishment, sounds fair and make it community more organic.

discord.gg/polana

#polana #botHunter #Community

3

35

15 Dec 2025

Powered by design by Old Bob ( @MAlamsyah51745 )

Polana is really cooking this week, with lots of important information on this project. Here's the info:

- Massive Purge

- Content Creator Role

- Akasha Void

- Bot Hunter

#polana #gpolana #polananetwork #bothunter #Web3

1

2

66

BOT HUNTER HAS ARRIVED.

The era of manipulation is coming to an end. All fraudulent activities, fake accounts, and practices that harm genuine community members will be identified and removed.

@polana_network remains committed to its core principle: putting real people and real contributions first.

We do not build on artificial numbers. We build on trust, integrity, and a community that truly participates and grows together.

Quality over quantity. Real community over illusions.

#POLANA_Network #BotHunter #RealCommunity #IntegrityOverNumbers

1

11

161

12 Dec 2025

Incoming BOT HUNTER

Hunt rogue bots. Earn Polana Points.

Get ready for the chase. Coming soon…

#BotHunter #Polana #CryptoGaming #PlayToEarn #NFTGame

1

9

59

10 Dec 2025

Something is coming… 👀

A new role. A new mission. A new hunt.

Bot Hunter arrives soon. 🔍🤖

#PolanaNetwork #polana #bothunter

1

1

5

60

10 Dec 2025

What is a Polanians Bot Hunter? And here's some important information for the future: there will be a new role for the Bot Hunter.

Eradicating users who try to use multiple Discord or X accounts for this project, and cheating, is a crucial role for the @BotHunter role.

#polana

1

1

3

88

26 Sep 2025

“No one cares… UNTIL EVERYONE CARES.”

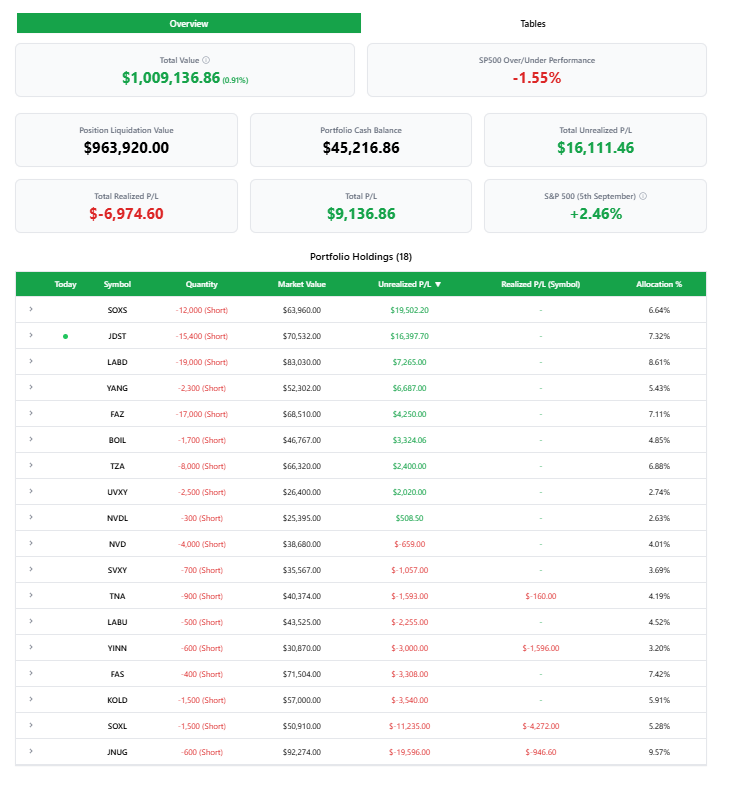

On December 17, 2019, I became an SEC whistleblower and filed my first TCR on LETFs. Since then, I’ve demonstrated—through math—that leveraged ETFs (LETFs/LETNs) and their creation/redemption flows are predatory at best, and likely far worse.

What might interest you: these products can be beaten using gambling math. Like counting cards in blackjack, the edge is rules-driven, it compounds over many hands for those who play the math. I’m collaborating with Brad Hebert @CrossCutProds, Executive Producer of Dirty Money (and others), to document this journey before the everyone-cares phase.

We’re documenting the math, the effort, the gradual realization, and the support many of you have given behind the scenes (you will be known). Documentary-style, public, open-sourced, math-based.

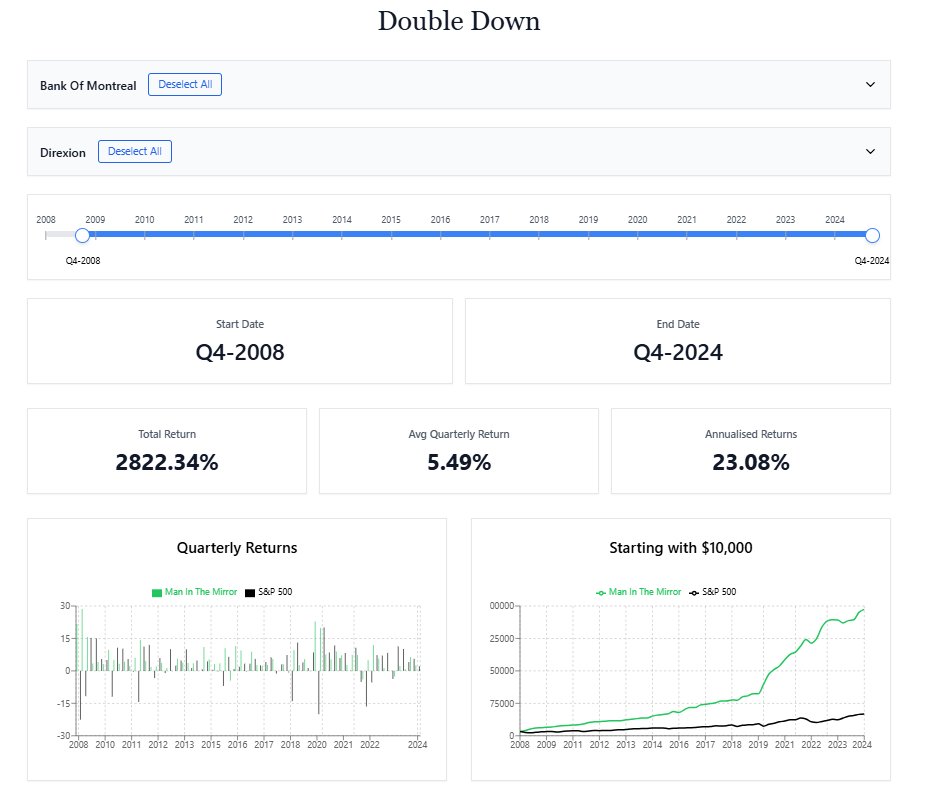

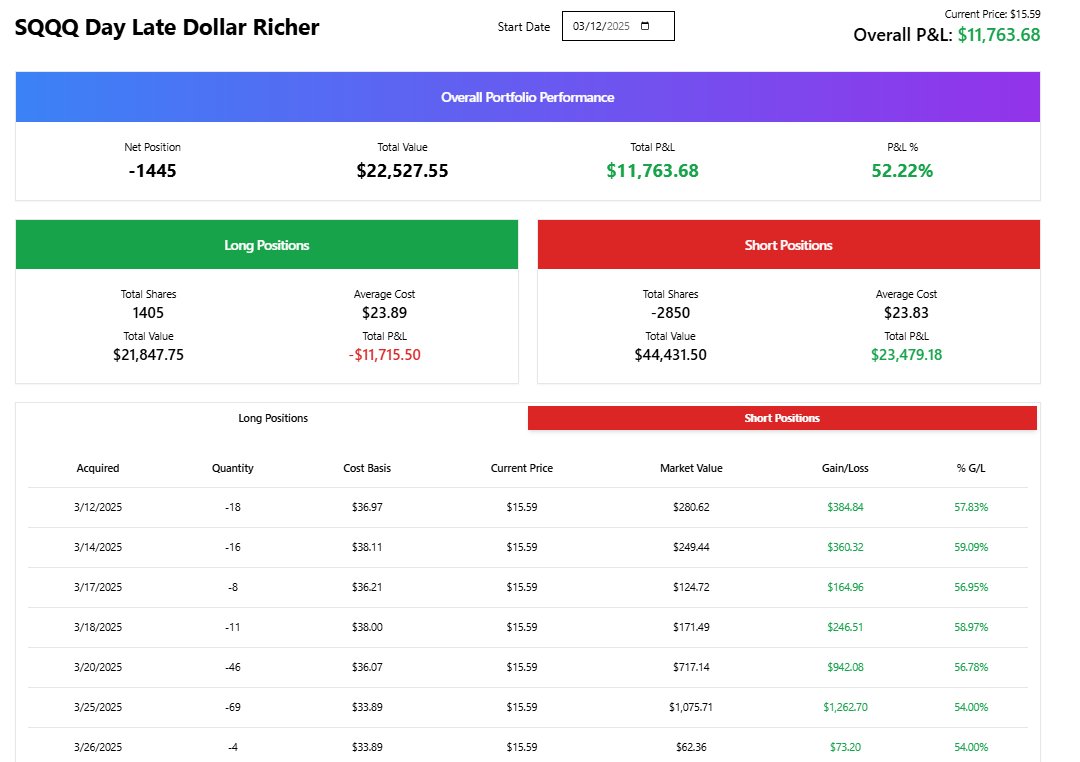

To make it easy,@bothunter and I built backtest tools and launched two live tracking dashboards based on my published, validated models:

• Day Late Dollar Richer: (SQQQ)

• FRAWD Model Portfolio: blending previously published mathematically advantaged models in real time

The math functions as a proof—it’s either true or false. Under unchanged mechanics and specified execution, this is mechanically forced expectancy: you won’t win every hand, but the expected outcome repeats.

I’ll post portfolio values daily versus the S&P 500. The Frawd Model Portfolio has been tracked since Sept 5, and DLDR since Mar 12. Trades and pricing are real; position size is scaled.

Simply put: LETFs are a casino game wrapped in an ETF. Issuers and swap counterparties sit as the house and are financially liable if you win, just like a casino.

If issuers/swap counterparties had average issuance at $100 and average redemptions at $150, they would go out of business. The game had to be built to guarantee investor losses to ensure house profitability (like a casino). Leverage reset, creation/redemption, and swap mechanics make the payout profile incentive-compatible for the house, and I’ve published falsifiable analyses showing how that plays out across time and products.

Papers, models, and more at: frawdresearch dot com

Disclosure: I am a legally represented whistleblower. The math is factual, and when the same mechanics persist, future behavior will rhyme with the past—because these products are structurally engineered that way. Nothing here is investment advice; this work is for investor protection and education.

The Frawd Model Portfolio will take into account corporate actions (dividends) and borrow fees; there is zero need for any vagueness or omissions on my part, the truth is powerful enough.

Lastly, in an effort to walk the fine line of giving the world enough to prove I’m right but not make myself irrelevant or have my work stolen, my published work represents the bottom quartile of my ability; you can safely assume 4× the returns you see (Frawd Model Portfolio) with .75 beta as the upper limit of my non-published, mathematically assured models. As SSRN models are validated and backtested and confirmed by the media, I will release additional enhancements, with average model returns increasing 5% per annum.

If you believe that counting cards is possible, you must by association believe that products that have a defined structure and payout (reset daily, pay 2–3× daily returns) can be gamed for profit, especially when performance tables are disclosed via prospectus and performance too far outside those limits will welcome lawsuits.

Remember: THERE’S NO CRYING WHEN YOU’RE THE CASINO.

Bookmark & follow 🧵 below…

2

10

75

185,900

Back in the Warzone! Battlefield 6...please come back! #Battlefield6beta #twitchclips #dgenxgpa #bothunter

youtube.com/shorts/cQFoNF7gk…

2

29

1 Jul 2025

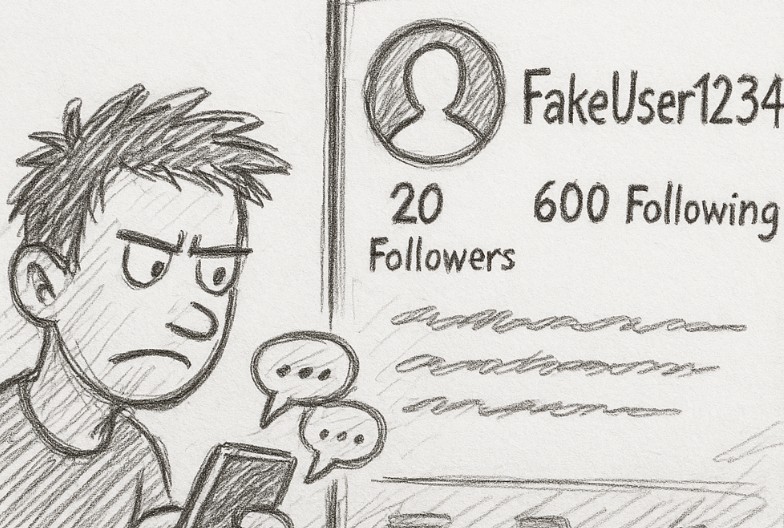

Lo riconosci subito.

Il profilo fake, il bot, il troll da quattro soldi.

Nessuna foto o una presa dal web.

20 follower, 600 following.

Scrive frasi a caso, spesso fuori contesto, piene di errori.

Segnala. Blocca. Ignora.

Perché la manipolazione oggi passa anche da lì.

#StopPropaganda #BotHunter #Disinformazione #SocialCleanUp

1

2

27

1,254

9 Jun 2025

🔍 NEW COSMOCATZ DEPLOYED

Designation: BotZerker

He hunts reply bots.

He detects copypasta in 0.2s.

He doesn’t meow. He flags.

📡 A cyber-feline anomaly built to purge the noise from the Meowverse.

🧬 Wiki: cosmocatz.com/wiki/index.php…

#CosmoCatz #CCTZ #Solana #BotHunter #Meowtonium #Web3Security #LoreDrop

1

1

4

163

22 Apr 2025

How to catch web bots?

Tappy-style: one coin, one hook, zero mercy.

Fake accounts? Reeled in.

Bot armies? Baited.

Greedy clickers? Hooked on $TAP.

Welcome to the Kegfjord Trapline.

Only the real ones survive.

#TappyCoin #BotHunter #giveaway #CryptoMemes #Web3Warriors #Kegfjord

5

10

240