John Schloegel retweeted

The $700 billion AI infrastructure buildout just hit a wall that capital alone cannot fix and Jefferies just laid out exactly why (Save this).

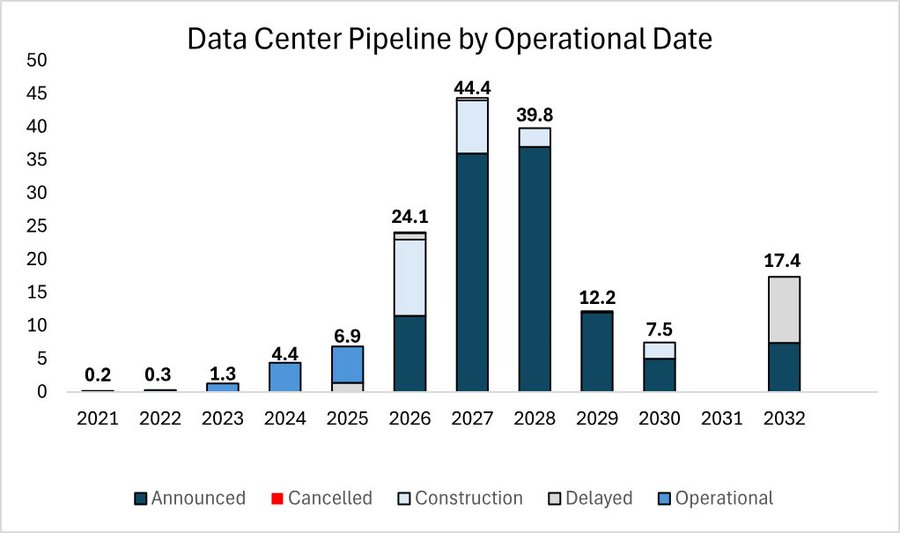

The data center pipeline chart below shows announced capacity surging from 6.9 GW in 2025 to 24.1 GW in 2026, peaking at 44.4 GW in 2027, and sitting at 39.8 GW in 2028, numbers that look like an unstoppable infrastructure buildout on the surface.

But Jefferies issued a stark warning that approximately 50% of 2026 data centers and approximately 80% of 2027 and 2028 data centers do not appear to have started construction as of Q2 2026.

JPMorgan independently confirmed it, finding that over 60% of data center capacity planned for 2027 has not broken ground, with another 7% already flagged as delayed.

Sightline Climate put the raw numbers behind it, of the roughly 12 to 16 GW of US capacity announced for 2026, only about 5 GW is actually under active construction meaning the rest is still paper.

The reason so much of the announced pipeline is stalled is not capital but rather physics.

High-voltage transformer lead times that ran 12 to 18 months in 2022 have extended to 30 to 36 months in 2026, and in some cases up to five years, a catastrophic mismatch for data centers that need to deploy within 18 months to match AI demand timelines.

Grid interconnection queues in high-demand regions like Texas, Virginia, and the Carolinas have grown to 3 to 5 years, meaning projects that broke ground in late 2024 expecting to be online by mid-2026 are finishing construction and finding they cannot physically receive power.

Capacity market clearing prices in these regions reflect exactly that scarcity, hitting $329 per megawatt-day in 2026, up from $28.92 the year before: a 1,037% increase in a single year.

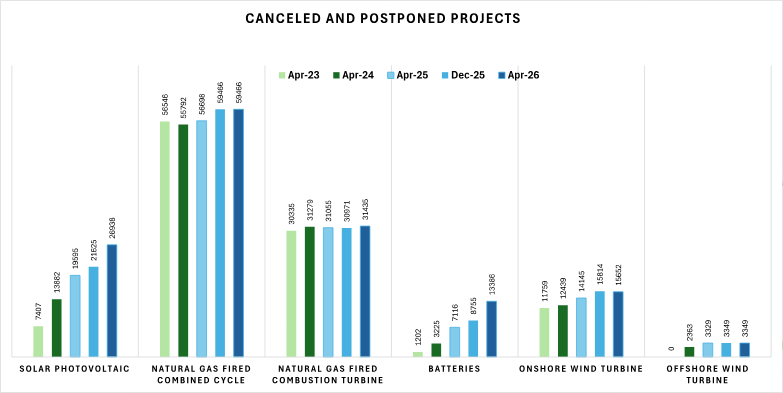

The power generation cancellation data makes it significantly worse.

The second chart shows canceled and postponed power generation projects across every major category, solar, natural gas, batteries, onshore wind, and offshore wind, all trending sharply higher from April 2023 through April 2026.

Battery cancellations in ERCOT which Jefferies specifically flagged as the key forward indicator are accelerating precisely when they should be expanding to support new data center demand.

The conclusion is that headline pipeline figures materially overstate the capacity that will actually come online, solar and battery project attrition is accelerating just as data center demand firms, and the supply environment is getting tighter.

What this means for the AI infrastructure trade is direct and consequential.

When 50% of 2026 capacity and 80% of 2027 capacity is on paper rather than under construction, the AI compute shortage does not ease on the timeline the market is currently pricing but rather extends.

Every gigawatt that slips from 2026 into 2027 or 2028 is a gigawatt of compute that hyperscalers, model labs, and enterprise AI teams cannot access which means they will pay a premium for whatever capacity actually exists, and the companies that already have operational data centers with secured power today are not in a competitive market.

They are in a seller's market with no meaningful competition, for longer than the consensus currently believes.

Long the Neoclouds stock and come koin Milk Road Pro for just a dollar for our full breakdown of the data center delivery gap, its impact on AI cloud pricing, and the infrastructure companies set to benefit.

Link below!

11

30

116

12,746

Canada's pension money is now betting on India's AI infrastructure. CPPIB takes 8.2% of CtrlS, which runs 15 data centers across India. Retirement savings chasing the GPU buildout.

24m

Anyone who knew anything about the power grid knew at a glance that the proposed data center buildout was complete and utter BS.

71

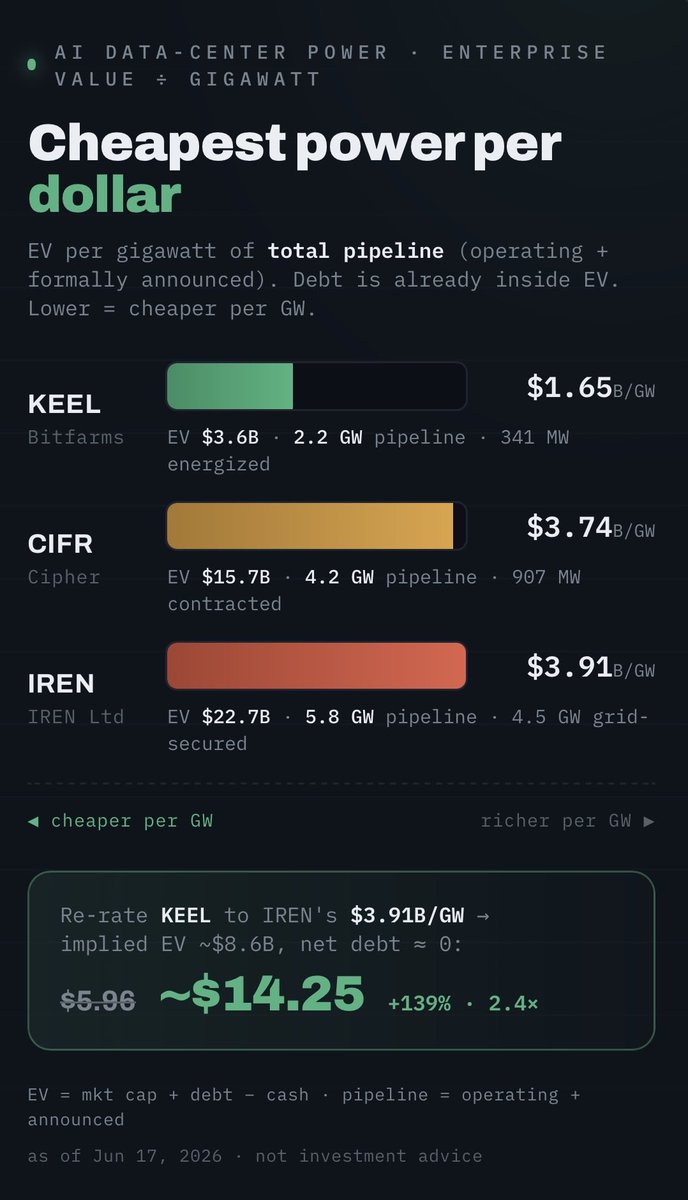

The greatest barrier to the AI buildout remains energy. Bitcoin miners have all pivoted to data centers given they have power locked down. I’ve been bullish $KEEL and $CIFR to name a few names but $KEEL in the early innings of their pivot. I compared $KEEL $CIFR and $IREN enterprise value to gigawatt of power secured and planned. Interesting valuation. This doesn’t make me bearish any of the names but there is a reason $KEEL is my second largest position.

1

3

112

🤣🤣🤣🤣🤣🤣🤣🤣

Only those $IREN idiots can guide down in the AI buildout - basically the 4th Industrial Revolution.

42

People are going to hate me for this:

But now is not the time to buy $NBIS.

I do think it's worth selling here. Let me explain why:

1) $NBIS operates in the AI data center / GPU cloud hosting layer ofc. Basically, selling compute capacity. This segment is becoming increasingly crowded and competitive:

- Hyperscalers ($GOOGL, $AMZN, $MSFT, $META, etc.) are aggressively building their own internal capacity at massive scale.

- Multiple specialized neoclouds and traditional providers are chasing the same constrained resources (power, land, GPUs, and interconnection).

- As capacity comes online across the industry, utilization rates and pricing power can compress for pure hosting plays.

2) $NBIS has outlined multi-GW data center buildout plans. This creates elevated binary risks:

- Power procurement and grid interconnection delays (a major industry bottleneck).

- Construction and permitting timelines.

- Actual customer utilization ramp after facilities come online.

- High ongoing capex intensity to stay competitive.

3) $NBIS has geopolitical risk (origin overhang):

- As a carve out from Yandex, $NBIS carries residual geopolitical perception risk (Russian origins, sanctions history), which can affect trust and long-term contracts with Western hyperscalers: Even as it focuses on US/Europe assets.

4) $NBIS valuation seems pretty high here:

- In Q1 2026 earnings were decent. Revenue $399M (strong beat, massive YoY growth) and narrower EPS loss than expected. But it's still unprofitable.

- They have crazy 2026 guidance ($3B–$3.4B revenue/ARR range discussed) which seems pretty aggressive and requires close to flawless execution on new capacity imo.

- Insane Trailing Multiples: TTM P/S: 80x, EV/Revenue (TTM): 77x, Trailing P/E: 102–108x (on $2.60–2.92 EPS). Even high-growth AI names rarely sustain 50x trailing sales for long without massive profitability or clear path to it.

- Still Losing Money on a Normalized/Operating Basis:

Operating income TTM: –$619M (op margin deeply negative), EBITDA TTM: –$38.6M, normalized net income is negative; the big positive GAAP net income ($817M TTM / $621M in Q1) is also heavily boosted by unusual/one-time items (likely spin-off gains, investments, or fair value adjustments from the Yandex restructuring).

- Forward P/S on Guided Revenue Is Still Premium (22x). At $71B mkt cap and $3.2B midpoint FY2026 guidance -> 22x forward sales. This is pretty crazy.

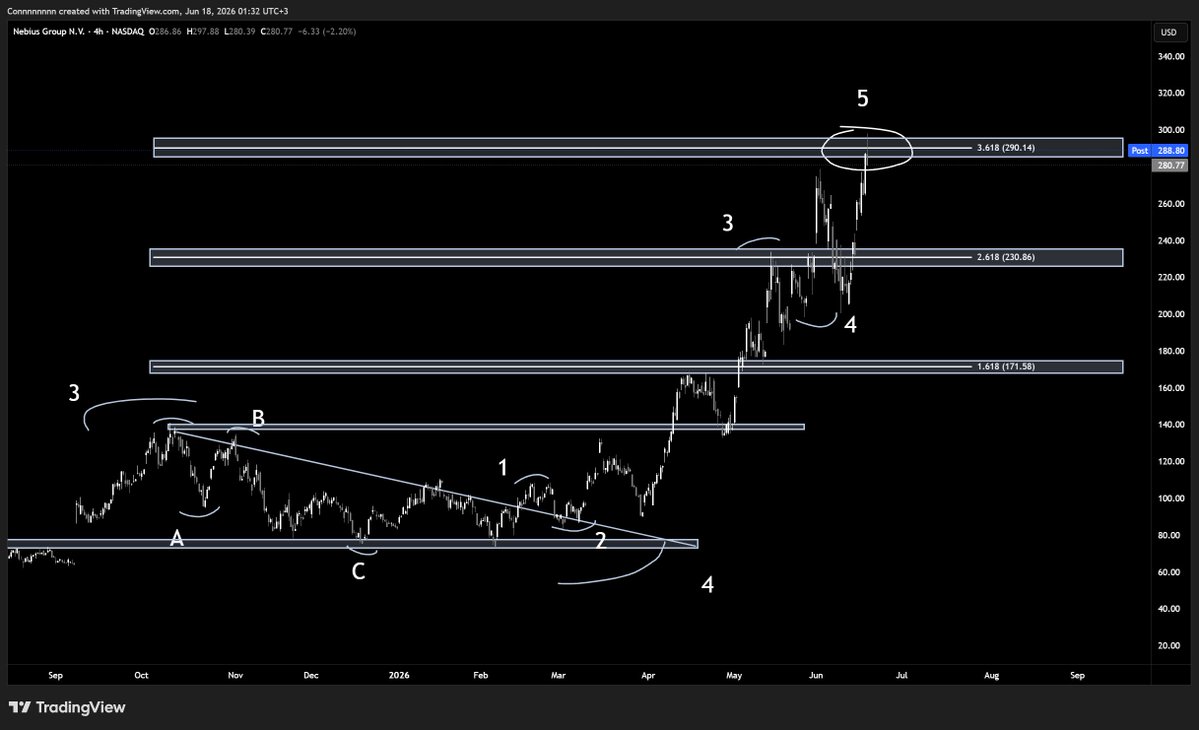

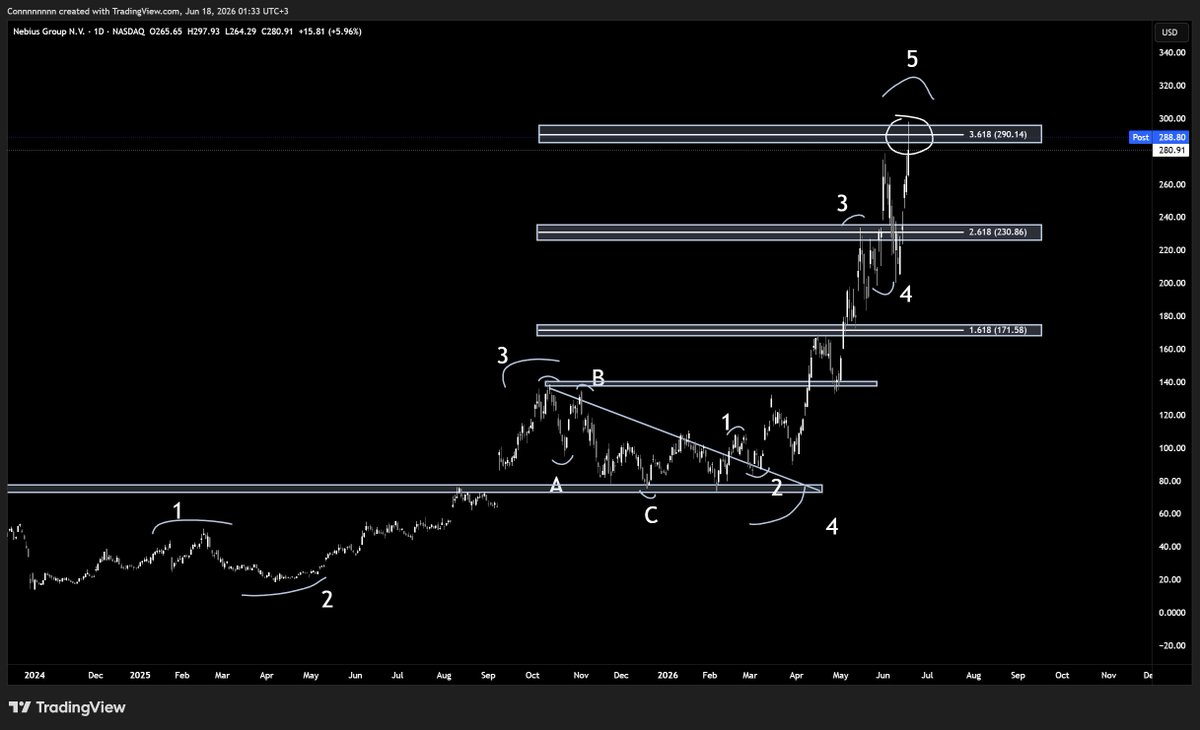

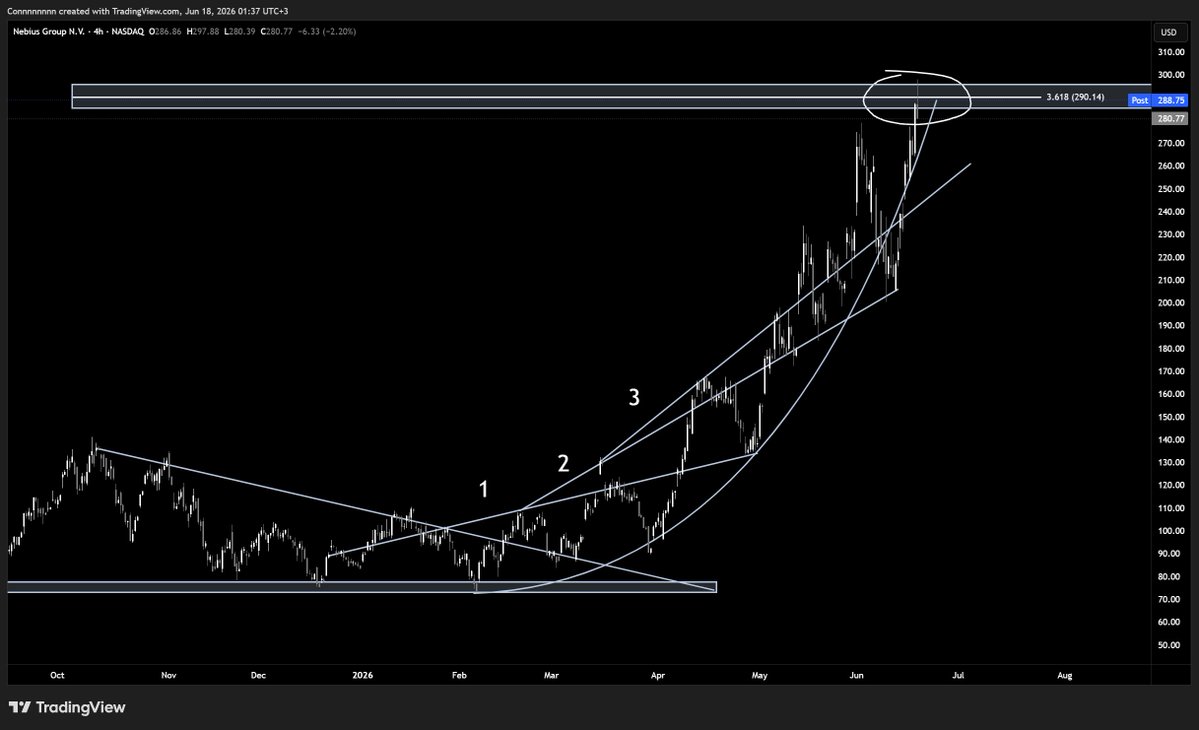

5) $NBIS technical analysis wise looks massively overbought):

- We seem to be hitting the top of the 5 wave (out of the 1-2-3-4-5) on the HTF. On the LTF, we also seem to be hitting the wave 5, adding confluence to this resistance area.

- We ran through the 1.618 level and 2.618 level showing a high sign of aggressive buying. Now we're at the 3.618 level, which means very aggressive buying has just occured.

This is why, overall, I'm bearish $NBIS.

"What are some other names worth buying then, and what should be my game plan?"

I gotchu.

$OPTX, $ASYS, and $SHMD are 3 great stocks.

It's worth buying these right now imo.

It's just not worth the risk holding $NBIS here, compared to them.

Now, I don't fully dislike $NBIS (for a couple reasons), so here's how I'm going to play this out though:

I'm going to sell my shares here (that I bought at 90). If $NBIS goes to 310, then uses the 3.618 level as support, then I will look to get in again, because that means we're going fully parabolic.

It would mean losing a 5% move to the upside, on the potential of a large 20% move downward.

That's why I'm doing this.

Hope this makes sense on what I'm doing, and why.

Of course, there are counter takes to these arguments (I'm not denying that). But, it's all about if those counterarguments make more sense.

Right now, it seems we are very overbought, with a very high valuation.

If we continue to run, and this "bubble" continues to grow, I'd happily join that (after losing out on a 5% run lol).

If you enjoyed, pls lmk your guys' thoughts.

And if you have any other sort of reasoning you guys want to come to me with, feel free to comment it below (I try to read everyone's comments, and respond ofc).

Just my 2c and what I'm doing here.

6

18

1,132

no but govt shud take a stake in anthropic and openai to help with buildout

10

Eezee Pezee retweeted

AMERICA’S A.I. BUILDOUT IS ACCELERATING 🚀

“By the end of next calendar year, we’ll have basically quadrupled the output.” — Coherent CEO Jim Anderson

2

9

493