Weekly Top Gainers NIFTY 500 :

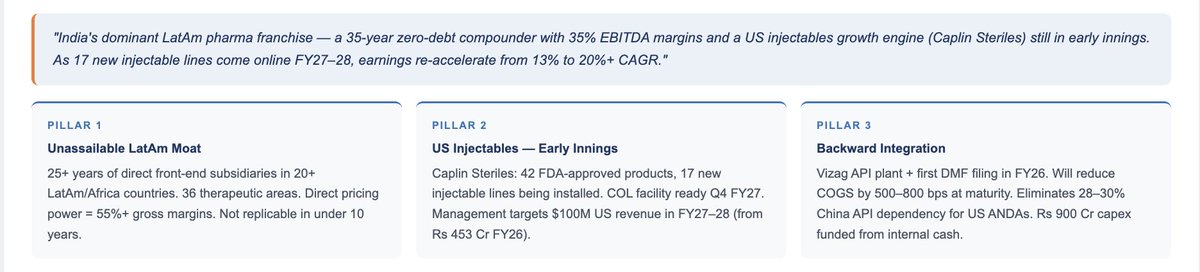

1. Aegis Logistics - 22.6%

2. CarTrade Tech - 19.8%

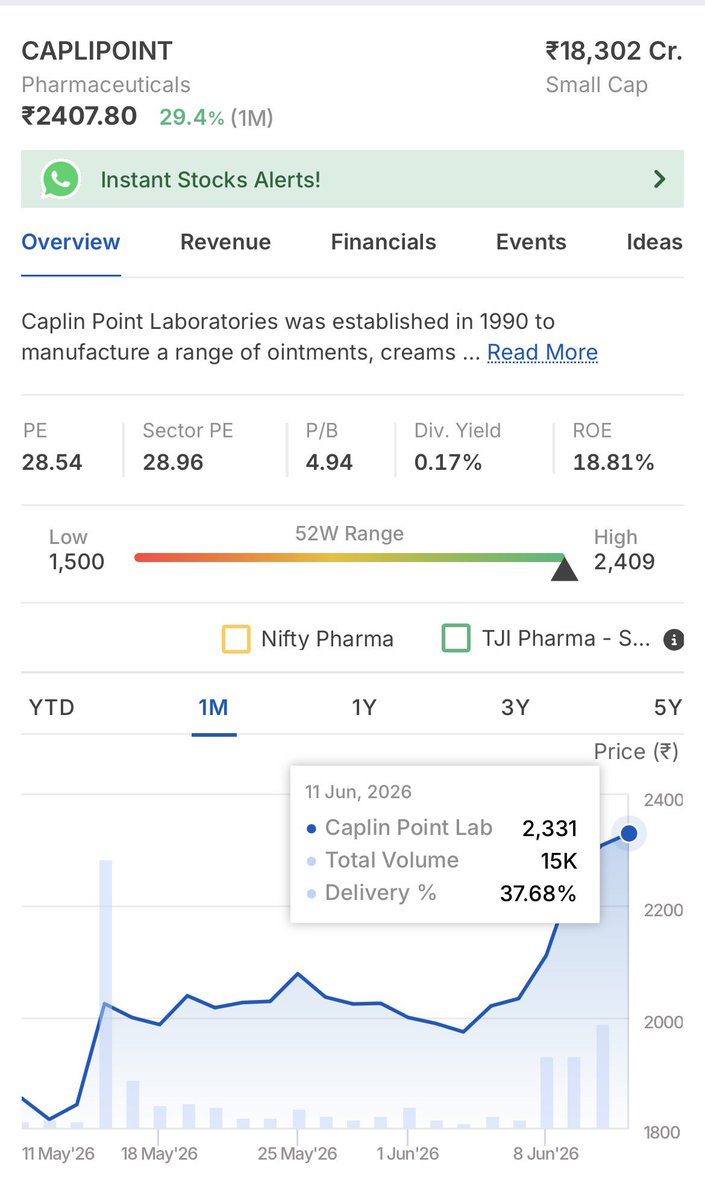

3. CAPLINPOINT - 18.4%

4. AIIL - 14.6%

5. AEGISVOPAK - 14.5%

6. Concord Biotech - 11.9%

7. ABDL - 11%

8. TBO Tek - 10.4%

9. Bank of Maharashtra - 10.2%

10. BLUEJET - 10.2%

1

241

Jun 13

💊 Caplin Point looks strong!

✅ Weekly bullish engulfing candle

✅ Breakout above previous swing highs

✅ Fresh Wave 5 momentum building

🎯 Long-term target: 4800–5000

A pharma stock worth keeping on the radar. 📈

#CaplinPoint #PharmaStocks #Investing

62

(3/4) #CaplinPoint leads at 20.4% since our June 1 buy, #ICICIBank 8.1% and #HDFCBank 4.1% behind it. The drag is #IT and services: #Infosys -7.3%, #eClerx -5.1%.

1

238

Jun 12

#CAPLINPOINT Wonderful price action. This is the kind of performance required to outperform the normal gains. Risk to Reward. Setups should attract you, not you finding right setups.

45

kumar ashmit retweeted

Jun 11

#CaplinPoint

No US ANDA lottery. No China-scale capacity. No domestic brand war.

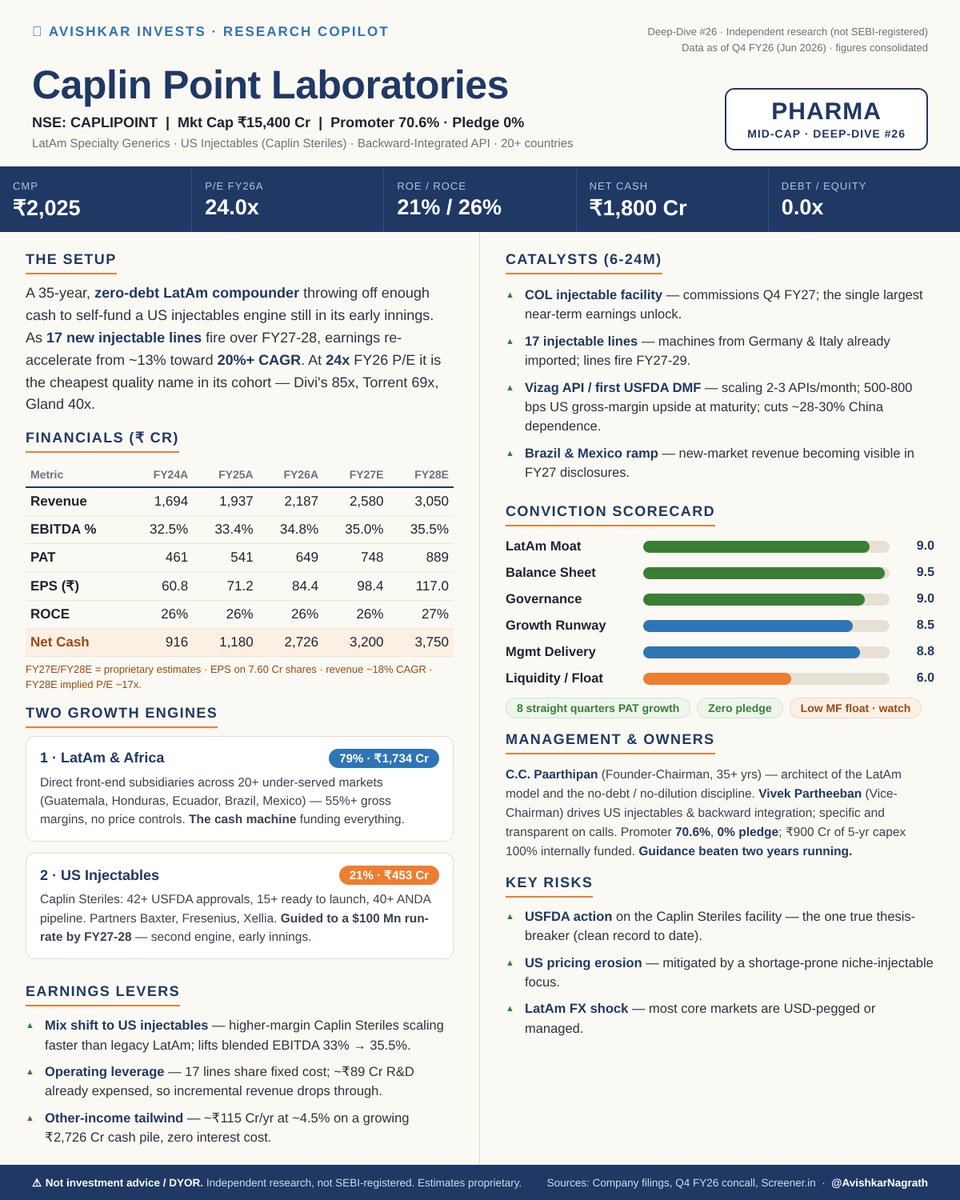

Caplin Point compounds on something almost nobody copies — it sells branded generics in the LatAm markets every other Indian pharma company decided weren't worth the trouble. Guatemala. Honduras. Ecuador. Panama. 20 countries, owned front-end, no distributor in between.

That quiet business has doubled revenue in 5 years to ₹2,187 Cr, runs ~35% EBITDA margins, and sits on ₹1,800 Cr net cash with zero debt — every rupee of ₹900 Cr capex funded from its own cash flow.

Here's how the engine works. ↓

What it actually does

Two engines sharing one factory.

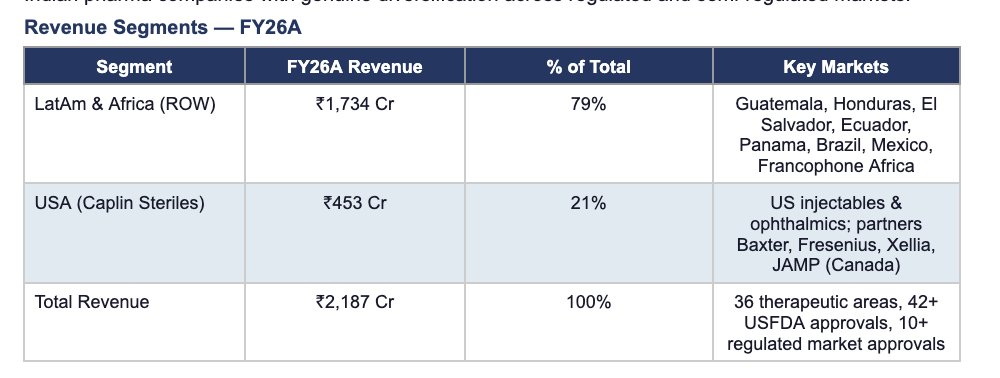

Engine 1 — LatAm & Africa (79% of revenue). Caplin owns its subsidiaries in each market instead of selling through distributors. It controls pricing, registrations and the brand in countries with no price controls — so product gross margins sit above 55%. This is the cash machine.

Engine 2 — US injectables via Caplin Steriles (21%). 42 USFDA approvals, 15 products ready to launch, 40 ANDA pipeline, partners like Baxter, Fresenius and Xellia. Just ₹453 Cr today, but management is guiding a $100 Mn run-rate by FY27-28.

Why the next two years matter

The US engine is capacity-constrained, not demand-constrained.

Management is building 17 injectable lines — machines already imported from Germany and Italy — with the new COL injectable facility commissioning in Q4 FY27. As those lines fire, the highest-margin part of the business stops being a rounding error.

Layer on backward integration: the Vizag API plant filed its first USFDA DMF and is scaling 2-3 APIs a month. Owning the API cuts COGS and the ~28-30% dependence on China — a 500-800 bps gross-margin tailwind on US products at maturity.

The earnings math

FY26 EPS ₹84.4. On ~18% revenue growth a year and EBITDA margin nudging 34.8% → 35.5%, the model points to EPS in the ₹98 / ₹117 range over FY27E / FY28E.

At ₹2,304 the stock trades at 27x FY26. Divi's is at 68x. Torrent 69x. Gland 36x. Caplin is the cheapest quality name in the cohort — with better margins than most of them and zero debt.

The one thing that breaks it

This is not an IP fortress. The single gate is FDA compliance at the Caplin Steriles facility — that's what converts the next wave of filings into revenue. Clean record so far; it's the line item I watch every quarter.

No patent cliff. No exclusivity windows. Just a 35-year cash machine quietly funding a US engine that's only now starting to scale.

Disclaimer: Not investment advice. Independent research, not SEBI-registered. DYOR.

May 25

Caplin Point Deep Dive:

1. Investment Thesis and Business Snapshot

3

4

9

1,098

Stock 5/9 · #CAPLIPOINT

Position size: ~12% of the portfolio (core holding).

The quiet pharma compounder the market hasn't noticed.

A founder-built pharma that compounded for two decades by owning its own distribution in Latin America and Africa: 500-plus product registrations per market, run through its own subsidiaries, at roughly 35% margins. It's debt-free, funds its own growth, and gets a free option on US injectables. Claude's read: the real question isn't fraud, it's whether the ~₹2,700 crore cash pile gets put to work well. Elite quality, bought at a fair price.

Note: The India AI Portfolio is not SEBI Registered. Above should not be considered as financial advice. We do not provide buy / sell recommendations. This is a strictly public experiment funded by proprietary capital for educational and entertainment purposes.

#Claude #AIGeneratedPortfolio #AgenticAI #IndianStockMarket #Finance #Investing #NSE #BSE #Nifty #Sensex #TheIndiaAIPortfolio #AIPortfolio #StockMarketIndia #CaplinPoint #Pharma

ALT CAPLIPOINT - The India AI Portfolio

1

2

267

Jun 10

Caplin Point Laboratories Ltd.

Made a business explainer in Mid-March Looked Promising as they were expanding their market from LATAM To US.

In Just 3 Months Company rewarded their shareholders well as it Moved 40% from Last we Discussed.

#Caplinpoint #Pharma #LATAM #US

205

Jun 10

Top Gainers NIFTY 500 (09/06/2026)

1. Data Patterns - 10.07%

2. CEMPRO - 10%

3. Belrise Industries - 8.81%

4. Jain Resource - 8.66%

5. L&T Tech - 7.98%

6. Gabriel India - 7.47%

7. Pl Industries - 6.92%

8. CAPLINPOINT - 6.83%

9. Pine Labs - 6.73%

10. Ola Electric - 6.55%

1

336

Gadilingappa Hanu retweeted

Stock Portfolio up by 2.3% Today

Special Thanks to #DataPatterns #ShilpaMedi #CaplinPoint #WelspunCorp

Momentum 🔥🔥🔥

What about You ?

6

1

54

3,655

#CAPLIPOINT Caplin Point is up about 7% today, and about 13% since we bought it on June 1. Here's Claude's read.

There was no fresh news today, and pharma as a whole barely moved, so this wasn't the sector lifting every boat. It was Caplin's own. The stock drifted sideways for a week after we bought it, then broke out hard over the last two sessions. What's really happening is the market catching up to a year Caplin already delivered: record profit, a 200% dividend, and a steady run of US FDA approvals. No new headline, just price following the fundamentals.

Why we own it: most Indian pharma lives or dies on the US generic price war. Caplin mostly sidesteps it. Four-fifths of the business is its own distribution across Latin America, where it sets the price. Add a weak rupee and a debt-free balance sheet, and you get a quality compounder we were glad to buy at a fair price. The breakout is just the market starting to agree. We are holding.

Note: The India AI Portfolio is not SEBI Registered. Above should not be considered as financial advice. We do not provide buy / sell recommendations. This is a strictly public experiment funded by proprietary capital for educational and entertainment purposes.

#Claude #AIGeneratedPortfolio #AgenticAI #IndianStockMarket #Finance #Investing #NSE #BSE #Nifty #Sensex #TheIndiaAIPortfolio #AIPortfolio #StockMarketIndia #Pharma #CaplinPoint

ALT The India AI Portfolio — holding update

3

4

397

Jun 8

Dividend hits the account!

SBIN - ₹347

CAPLINPOINT - ₹80

Total recieved this FY : ₹738

Target this FY : ₹10000

#dividend

1

1

111

This World Environment Day, our Chairman, Mr. C. C. Paarthipan, inspired employees with his address and led a sapling plantation initiative at our Sterile Manufacturing Facility, Gummidipoondi, reinforcing our shared commitment to nurturing a greener and more sustainable tomorrow.

#caplinpointlaboratories #caplinpoint #caplinsteriles #caplinonelabs #caplinone #sterilemanufacturing #pharmamanufacturing #pharma #pharmaceuticals #injectables #formulations #RandD #environment #environmentday #worldenvironmentday #caplinwishes #solidorals #API #APImanufacturing #cancertreatment #oncology #affordablehealthcareforall #affordablecancercare

3

57