NAV erosion on income CEFs persists—premium buyers, you're pricing in someone else's exit.

2

Getting ready to go live. youtube.com/live/HqbTIZ3uqvw… I will recap the top 40 and talk about the issuers. See if you favorite issuer is ranked. Also AMA about any of these 415 ETFs CEFs and BDCs that I cover! See you in 1 minute

1

17

⎐كُـود⎐كوبِون⎐خـِصم⎐

⎐ايهرب⎐ايهيرب اهرب

⊵GCA5893⊴

⎐نون⎐

⊵S3Q⊴

⎐نمشي⎐

⊵AABN⊴

⎐باث▬اند▬بودي⎐

AB6K⊴

⎐ناتشورال ⊴تاتش⎐

⊵C37⊴

⎐فوغا⎐كلوسـيت⎐

⊵V1⊴

⊴ماكـس ⊴

⊵A9B⊴

___

cefS

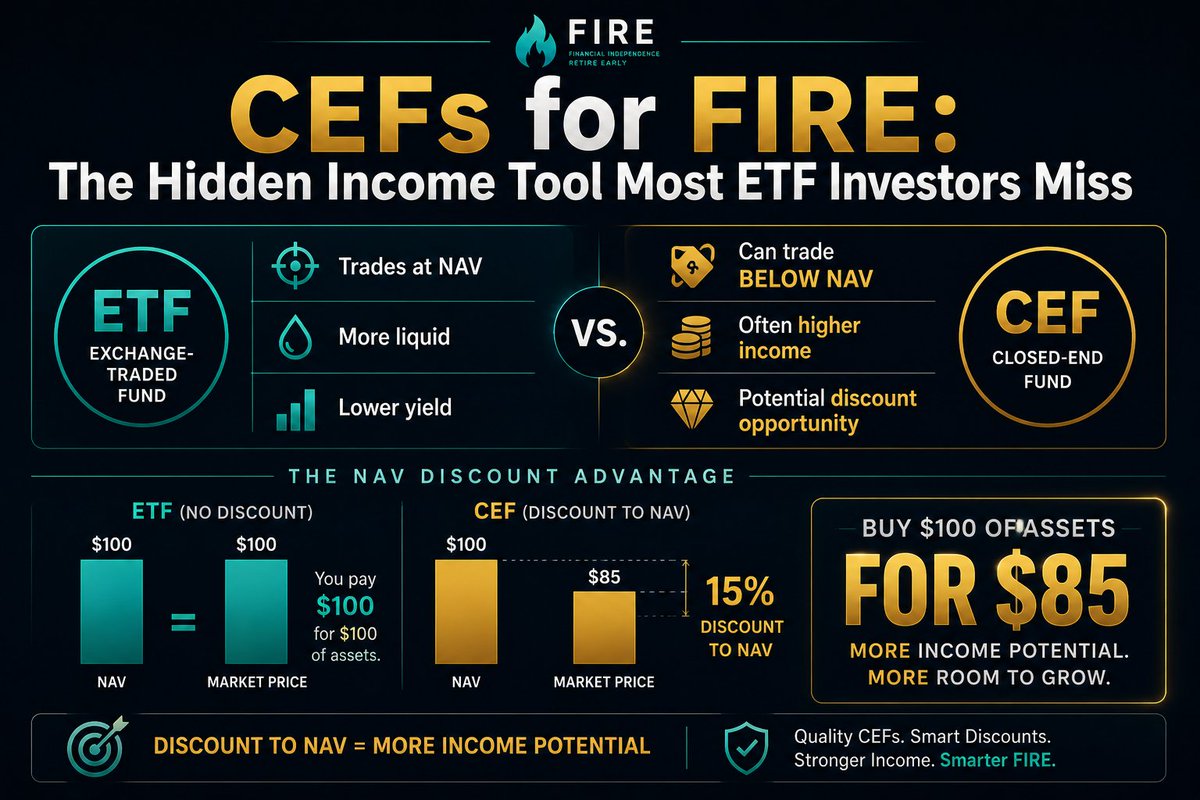

You know ETFs. But do you know CEFs?

Closed-End Funds are the lesser-known income tools of the FIRE community — and they can yield 8–15% . 🧵

📌 What is a Closed-End Fund (CEF)?

A CEF is like a mutual fund that trades on the stock exchange like an ETF.

Key difference: it issues a fixed number of shares at IPO and then trades at either a PREMIUM or DISCOUNT to its Net Asset Value (NAV).

That discount is where the opportunity lives. ✨

🔑 Why FIRE investors pay attention to CEFs:

✅ Often trade at a discount to NAV (buy $1 of assets for $0.88)

✅ High monthly distributions — 8–15% yields are common

✅ Professionally managed income strategies

✅ Can use leverage to boost distributions

✅ Wide variety: bonds, equities, options, real assets

⚠️ The risks to understand:

• Leverage amplifies losses in down markets

• Distributions can be cut without warning

• Less liquid than ETFs — wider bid/ask spreads

• More complex — you need to understand what you're buying

Popular CEF categories for FIRE investors:

📊 Equity income CEFs (options-based strategies)

📊 Bond/credit CEFs (high-yield fixed income)

📊 Multi-asset income CEFs

This week we're exploring CEFs as a companion to your income ETF stack.

Welcome to the next level of FIRE income investing. 🔥

#CEF #ClosedEndFund #FIRE #FIREMovement #IncomeInvesting #PassiveIncome #RetireEarly #HighYield #FinancialFreedom #FinancialIndependence #ETF #DividendInvesting #InvestingEducation

21

Jun 13

Valuation spreads in CEFs have compressed. The 8% yield pool now demands tighter discount triggers for entry. Risk-adjusted returns still there, but patience required. 📉

13

Jun 12

which CEFs do you own? I have a tiny tiny bit of PDI.. have had it for a long time. The premium is shrinking.. if it were at a discount. I'd buy it no sweat. I also have PDO and PDX (bigger positions). PDX is largest. I am a big Ivacsyn fan.

2

1

55

Jun 12

🏡 𝐓𝐑𝐀𝐃𝐈𝐍𝐆 𝐂𝐋𝐎𝐍𝐄𝐃 𝐇𝐎𝐔𝐒𝐄𝐒 🏡

✨ 𝐀𝐋𝐒𝐎 𝐓𝐀𝐊𝐈𝐍𝐆 𝐏𝐄𝐓 𝐂𝐄𝐅𝐒 ✨

✔️ 𝐏𝐄𝐑𝐅𝐄𝐂𝐓 𝐂𝐎𝐍𝐃𝐈𝐓𝐈𝐎𝐍

✔️ 𝐍𝐈𝐂𝐄 𝐓𝐎 𝐋𝐎𝐎𝐊 𝐀𝐓

✔️ 𝐆𝐎𝐎𝐃 𝐎𝐅𝐅𝐄𝐑𝐒 𝐖𝐄𝐋𝐂𝐎𝐌𝐄

📩 𝐃𝐌 𝐌𝐄 𝐓𝐎 𝐓𝐑𝐀𝐃𝐄!

13

1

1,359

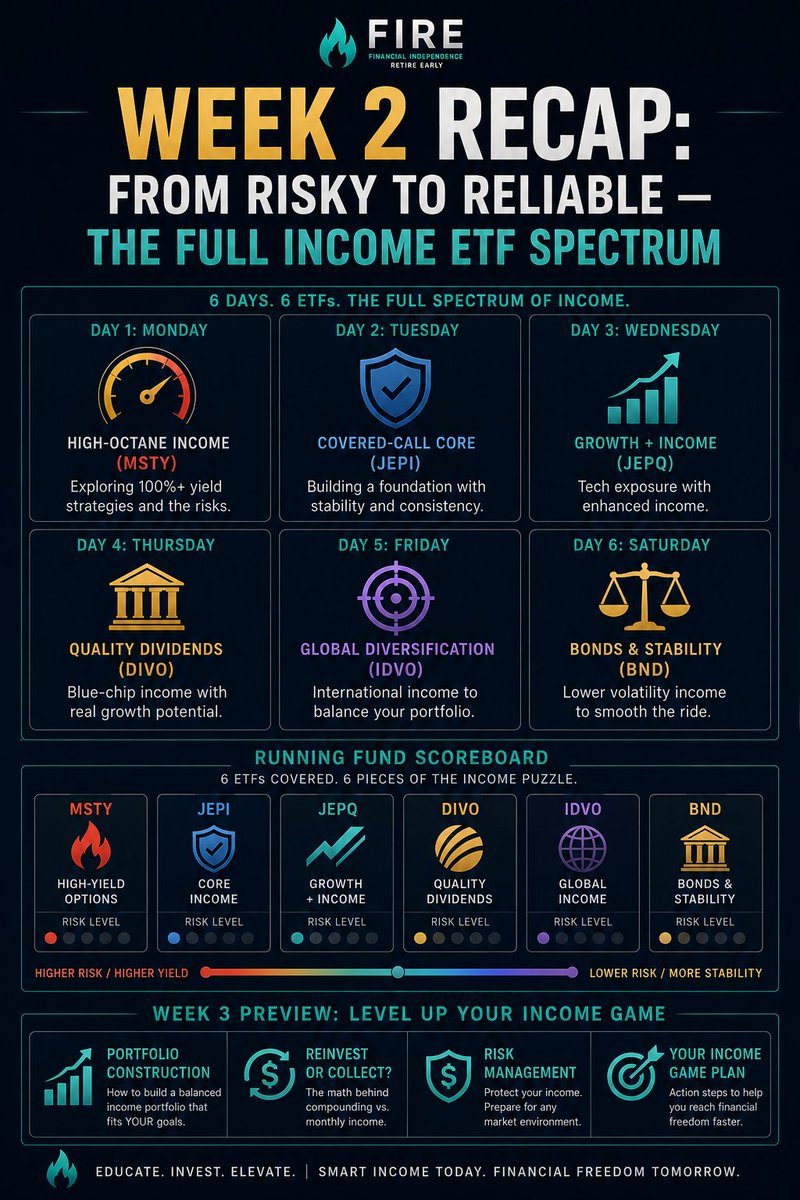

Week 2 done. Here's everything covered for your FIRE income playbook:

📌 Monday — $MSTY Deep Dive

→ 105% yield, extreme risk, Bitcoin exposure — know BEFORE you buy

📌 Tuesday — $JEPI vs $JEPQ

→ JPMorgan's two income funds: same family, different risk profile

📌 Wednesday — Growth vs Income Phase Framework

→ Which funds belong based on your years to FIRE

📌 Thursday — $3,000/Month Portfolio Blueprint

→ Real math building a FIRE paycheck with $QQQI $SPYI

📌 Friday — $DIVO Spotlight

→ The covered-call ETF that grows AND pays monthly

📌 Saturday — 5 Income ETF Myths Busted

→ Common misconceptions costing FIRE investors real money

📊 Running fund scoreboard:

Covered so far: $SPYI • $QQQI • $JEPI • $JEPQ • $MSTY • $DIVO

🔭 Week 3 preview:

→ Introduction to Closed-End Funds (CEFs) for FIRE investors

→ $QYLD — the grandfather of covered-call ETFs

→ The FIRE Income Ladder framework

→ $4,000/month 3-fund portfolio blueprint

Follow so you don't miss it. 🔥

#FIRE #FIREMovement #WeeklyRecap #IncomeETF #PassiveIncome #RetireEarly #MSTY #JEPI #JEPQ #DIVO #FinancialFreedom #FinancialIndependence #CoveredCallETF #ETF

123

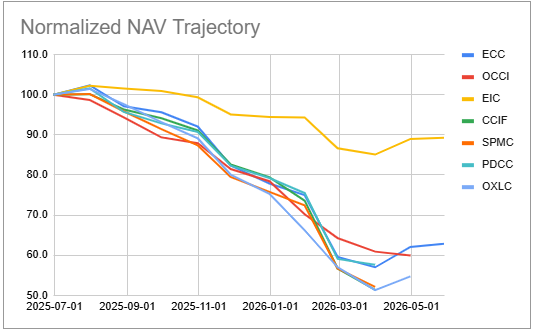

CLO Equity funds have started to report May NAVs and they are marginally higher, at least for $EIC and $ECC. The credit market environment has moved in CLO Equity’s favor. The somewhat nervous credit environment that marginally favors lenders over borrowers means loan refinancings - the killer of CLO Equity over the past year - are much more muted.

At the same time, the two key problems with the sector aren’t going to be resolved. One is the somewhat unpredictable nature of CLO Equity security prices which can move swiftly lower with very little stress in broader markets.

And two, how those downward prices translate into forced deleveraging across the CEFs. Despite some recovery in NAVs over the last two months, most of the sector is still nursing NAV losses of around 40% year-on-year. Even in the best case environment that is not going to be possible to recover from which makes it very hard to have conviction around this asset class. As tactical playthings, however, they are great.

1

3

242

Jun 12

CEF leverage at 8-month highs. Premium erosion in muni CEFs warrants reduced exposure.

12

Jun 12

@AxelMerk Why did you resign today from ASA especially after the SCOTUS ruling today limiting activists in CEFs? The timing makes no sense?

22

Legend FinX retweeted

Check out What's New at DV! dividendvision.com/whats-new

#StockMarketUpdate #FinX #Fintech #SaaS #Stocks #Funds #CEFs

5

8

198

Jun 11

Thanks. That's not one I'm that familiar with, actually. In general I've stuck to OEs and ETFs bc the open-end nature creates its own set of tradeoffs and also CEFs/trust premiums/discounts push some of the fundamentals to the periphery.

1

39