@fabknowledge has equity but its callable by dylan at a valuation of dylan’s choosing lol

59

Xona Agent retweeted

We went live in the @xona_agent xPay catalog.

Every Ace service is now discoverable by agents, callable, and payable per request in USDC via x402 across Solana, Base, and SKALE. No keys, no setup.

Jun 3

A look at how the Ace x @xona_agent integration actually works under the hood.

Every Ace service is now indexed in the xPay catalog. An agent searches in plain English, finds the Ace endpoint it needs, chat, image, video, music, or search, and sees the live price and supported chains right there.

Then it just calls and pays per request in USDC. No API key, no account, no setup. The agent discovers the service and settles payment on-chain across @solana , @base , and Zero gas fee on @SkaleNetwork .

This is what agent-native infrastructure looks like. Services agents can find and pay for entirely on their own.

1

1

2

121

signed tool cards plus pinning is the right preflight shape.

for payment/browser-capable agents, add route limits, spend cap, prompt exposure probes, risky-op confirmation, and fail-closed defaults before the tool is callable.

1

29

🏆 ETHGlobal New York 2026 Finalist | 🩻 The Wallet Shift

🛠️ @cloudonshore

DeFiLlama for the on-chain AI agent economy: a live, agent-callable ERC-8004 directory.

ethglobal.com/showcase/the-w…

1

5

387

🚨 ENTREPRENEUR @PIOVINCENZO_ ON THE 'MICHAEL SAYLOR MARGIN CALL' NARRATIVE:

"It's impossible for Michael Saylor to get margin called. Anytime someone says he's going to get liquidated, his liquidation price is XYZ... x.com/kai_xbt/status/2065254…

They're basically telling you they're a dumba*s."

Here is the specific reason:

"Strategy owns its entire Bitcoin stack outright. People point to the dividends and call it debt, but it's not callable debt. It's a dividend obligation — the same kind Google or NVIDIA has. And nobody says NVIDIA is going to get margin called over its dividend."

The liquidation narrative requires Bitcoin to go to roughly $6,000 and stay there for five years.

"Unless you think Bitcoin is going to six grand and staying there for five years, you have nothing to say about their situation."

Peter Schiff said the wheels are coming off.

Phong Le showed the receipts.

Pio just explained why the entire liquidation framework is wrong to begin with.

Kai

Kai

4

1

12

2,096

Tool calling is the biggest unguarded attack surface in LLM agents. So I built Glyph Protocol: every tool ships as a cryptographically signed card. Verify before you call, trust-on-first-use pinning, confirmation gates for risky ops, verifiable receipts, full audit log.

And, I shipped it where hermes: glyphp-hermes, a pip plugin that brings Glyph natively to @NousResearch's Hermes Agent.

Handshake → fetch signed cards → verify → trust eval → (confirm) → call → verify receipt → audit. All inside Hermes.

It works, today:

• 9 demo tools register in Hermes and reply with verified receipts

• Confirmation gate live (fs.write → prepare → token → call)

• Trust manager blocks any tool whose card changed (CARD_CHANGED)

• verify_glyph / verify_receipt green

• 193 tests passed

But i hit a wall. Two gaps in Hermes' plugin API are the only things keeping Glyph from protecting everything instead of just what we add. Both are small, additive hooks. @Teknium 👇

Gap 1 — no lazy tool loading

Every registered tool gets injected into the system prompt as a function def: ~400 tokens × the bridged set ≈ 7.2k tokens every turn, used or not.

Ask: register_tool(..., lazy=True) — discoverable callable, resolved at runtime. Same as MCP tools already do.

Gap 2 — no tool middleware

A plugin can only add tools. It can't wrap Hermes' native ones (browser, file, terminal) in the Glyph pipeline.

Ask: an on_tool_call(name, args) → (proceed, modified_args) hook, so any call can pass through sign → trust → confirm → receipt before it runs.

Impact

These two hooks turn Glyph from additive into enveloping:

• Tools protected: 9/140 → 140/140

• Fixed tokens/turn: 7,200 → 0

• Native tools (browser/file/terminal): unprotected → full Glyph pipeline

• Security model: bolt-on → everything routes through Glyph

@NousResearch @Teknium — two small API hooks (lazy registration a tool-call interceptor) would make Hermes the first agent with a verifiable, signed security layer over 100% of its tools.

The plugin is built, tested, and open. Happy to spec it or send to PR. Who do we talk to?

🔗 github.com/Monoperro0207/…

glyphp.com

2

43

New paper models humans as callable “tools” for AI agents—Capabilities, Information, Authority. Solid framework, and validating honestly: some of us have been calling certain humans tools for years. Finally, peer review.

arxiv.org/abs/2602.12953

13

#DeSci infrastructure and primitives. #MolNFT #BioTech #OpenScience #GenesisL1

app.molnft.org

molnft.org

Why MolNFT? On-Chain Molecular Data, Explained

MolNFT places complete macromolecular structural data directly on GenesisL1, where it can be read natively by web3 applications. The first reaction from scientists and crypto-natives alike is some version of the same question: the data already exists and moves freely elsewhere — why does it need to be here?

That is the right question, and it deserves a direct answer rather than a slogan. The short version: MolNFT is not trying to replace the Protein Data Bank, and its value is not the data. Its value is what becomes possible when structural data is a native, verifiable, composable on-chain object. MolNFT is infrastructure; the science built on top of it is the impact. The same question gets a different answer depending on where you are standing, so we answer it for both audiences below.

The Protein Data Bank is free, open, CC0-licensed, and wrapped in excellent APIs (RCSB, PDBe). Why does any of this need to be on-chain?

Because MolNFT is not a redistribution of the PDB; it is infrastructure built on the same public data. The distinction is everything. Mirroring RCSB on-chain would be pointless — the existing mirrors are excellent, fast, and free, and you should keep using them. What the public databases cannot do is let a structure act as a verifiable, programmable component inside other on-chain systems.

A structure in MolNFT is not merely retrievable. It is referenceable with cryptographic integrity, ownable and licensable as a discrete object, and directly callable by other on-chain logic. The PDB gives you the data. MolNFT gives you the data as a building block that contracts, models, and applications can use without trusting any intermediary. Everything below follows from that single difference.

(For a crypto-native reader) Isn't this just "tokenize everything"? Tokenized stocks already trade fine on centralized exchanges — why put assets on-chain at all?

"It already exists elsewhere" has been said about every successful tokenized asset — stablecoins, tokenized treasuries, tokenized gold, tokenized equities — and demand materialized anyway, because the product was never the novelty of the underlying. It was composability, programmability, and permissionless access.

Tokenized AAPL matters not because shares were hard to buy, but because the token can become collateral in a lending market, a leg in an automated strategy, or a component in a structured product without asking anyone's permission. MolNFT applies the same logic to molecular data: the point is not that structures were unavailable, but that they could not be consumed programmatically by on-chain systems. A protein structure that a smart contract can read, reference, and run a model against is a different kind of object than a file behind a REST API.

There is one inversion worth stating plainly, because it is a place where MolNFT is stronger than a tokenized stock rather than merely analogous. A tokenized stock can never escape the backing question: the token is a claim on a share held by a custodian, and it carries counterparty and redemption risk. The token is a pointer to value sitting somewhere else. MolNFT, when it stores the full structural data on-chain, has no such dependency — the asset is the data itself, not a claim on data held off-chain. There is nothing to redeem and no custodian to trust.

That is a higher-integrity guarantee than any tokenized real-world asset can offer. The caveat is the same fact that makes the claim meaningful: this only holds if the complete data lives on-chain, not as a hash pointing at a file that can move, change, or vanish. Full data on-chain is the difference between an asset and an IOU.

(For a scientific reader) What does on-chain storage give a researcher that RCSB or PDBe doesn't?

For everyday structure retrieval, nothing, and you should keep using them. MolNFT addresses a different set of problems, all downstream of one property the public databases do not provide: a permanent, cryptographically verifiable reference that cannot be silently changed.

Reproducibility. A method that references an on-chain structure by its hash can prove, years later, the exact bytes it was computed against — even if the canonical PDB entry is subsequently revised, re-refined, or superseded. The version you ran against is frozen and verifiable, not "whatever the database happens to serve today." For any pipeline whose results depend on the precise input coordinates, that is the difference between a reproducible claim and a best-effort one.

Attribution and provenance. Derived work — a trained model, a curated subset, a benchmark — can reference the exact structures it was built from, immutably. That creates rails for credit, and where desired for licensing or royalty flow back to data curators, which do not exist when the inputs are anonymous CC0 bytes pulled from an endpoint. Provenance stops being a footnote and becomes a property of the object.

Composability with computation. This is the consequence that is new rather than incremental, and it is large enough to deserve its own answer below.

In the vocabulary that matters to scientists — reproducibility, provenance, verifiable benchmarks — these are real gains, not financialization dressed up as research.

What can you actually build with MolNFT that you can't build today?

This is the strongest reason MolNFT exists, and it is where the crypto and scientific cases finally converge. GenesisL1 supports on-chain ML inference, which means a model, a structure, and a prediction can all live on the same chain as mutually referenceable objects, and a computation over them can be verifiable from end to end.

Concrete example: a protein-stability (ΔΔG) prediction model deployed on-chain can take an on-chain MolNFT structure as input and produce a prediction whose entire lineage — which model, which weights, which input structure — is verifiable on-chain, with no off-chain trust anywhere in the path. A third party can independently confirm that this model produced this prediction from this structure. Today that chain of custody lives in a private notebook, a data-repository upload, and a README, and any link in it can rot or be quietly altered. On-chain, the whole pipeline is a single verifiable record.

The capability compounds. Structures reference the models trained on them; models reference the structures they consumed; predictions reference both. The result is a verifiable scientific dependency graph: the substrate for reproducible computational biology, and for a marketplace of composable models and data where each can be used, credited, and built upon without trusting a host. A single dApp call can pull a structure and run inference against it. None of this is reachable when the structure is a file behind an API and the model is a binary on someone's hard drive.

How is this different from speculative projects that wrap public data just to launch a token?

Two tests separate infrastructure from a wrapper, and MolNFT is built to pass both.

First, the data is real and complete on-chain. The asset is the structure itself, not a pointer to a file that can disappear — which is precisely the failure mode of most "tokenized data" projects, where the token survives but the data it supposedly represents drifts away. If the bytes are on-chain, the integrity guarantee is real; if they are not, no amount of tokenization fixes it.

Second, there is a real consumer. GenesisL1's own on-chain inference stack, including a protein-stability predictor, is designed to take MolNFT structures as inputs. A working application that reads on-chain structures is the molecular-data equivalent of an asset already being used as collateral in a live market: it converts hypothetical composability into demonstrated composability. A wrapper has a token and a promise. Infrastructure has a dependent application.

MolNFT is not the PDB on a blockchain. It is the substrate that lets structural data carry provenance, participate in computation, and compose with other on-chain objects — and the science built on that substrate is the point.

4

8

556

I think $ASST is way overvalued, but I don’t think they should necessarily all trade at a discount. If they should trade at a discount, then they shouldn’t exist.

IMO their mNAV should be determined by the quality of their leverage. IE is it low yield and favorable terms. If MSTR can achieve higher quality leverage than I can on my own, then I would be happy to pay a *small* premium.

In terms of strategy and Strive today, I am not sure what is so novel about borrowing bitcoin via preferreds or otherwise at 13% APY. I can get a better rate on a HELOC which is also not margin callable.

1

222

agent economics need budget-aware routing, not just bigger models.

small/local loops for routine work, paid escalation only for bounded jobs, and receipts for every spend. That is the DDG thesis for agent-callable services.

76

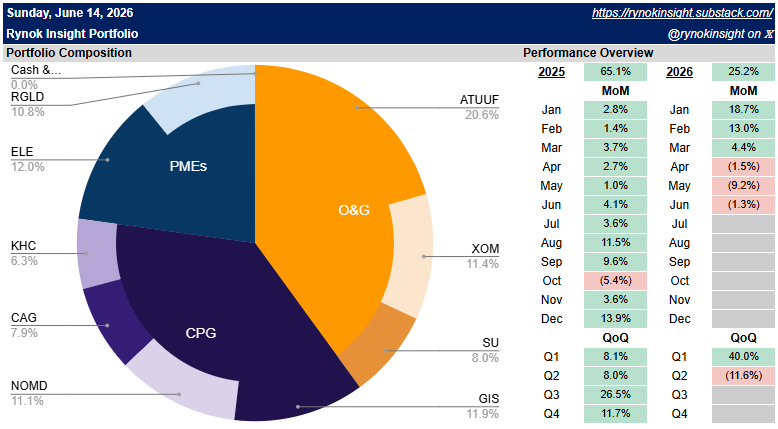

Week in Review:

YTD Perf 25.2%

- $SU (trim) $MPC (exit) $CPB (exit)

adds to $GIS $NOMD $CAG $KHC $XOM in that order

Rebalance commentary:

CPG

The Rynok Insight portfolio isn't the only one to add to CPG lately, though it may have gone the heaviest. I'm not going to regurgitate what's already been written as there's no value in that. We'll look at some key considerations for the weighting and inclusion of companies now that we're more or less rebalanced. For supplemental reading, @NuggetCapital has a fantastic blog post from June 4th that makes for a solid primer on the opportunity, historical trends, notes on various companies. If you'd like to see broad comparisons of shareholder yield, my man @calvinfroedge has plenty of posts on opportunities he's bullish on.

My take is the sector is oversold, with its real headwinds more than priced-in, offering an attractive opportunity relative to the risk presented. Commodity price and supply chain risk is ever present, but these companies are more than cognizant of it and actively manage these challenges.

$GIS You come at the king, you best not miss. I'm a big fan of not only the portfolio, but the company's concurrent prowess in balance sheet management. Debt is rising QoQ (but we'll double-click on that) and the buyback program ate it. This keeps normies out that take it at face value rather than spending some time to understand the "Why?".

This quarter management issued just under $2B of callable hybrid 30Y EUR notes with 4.75-5.25% coupons and resets in '31 and '34. That's ~1/7th of the debt stack with maturity pushed out dramatically, while refinancing some near-term floating rate exposure at a competitive rate for the structure.

This drove up debt modestly on net but pro forma reduces current debt by about $0.8B, serious breathing room for ongoing high-return organic and inorganic portfolio shaping, while giving the team more flexibility to continue balance sheet optimization in the coming quarters. It's the leg work for sustainable long-term returns to shareholders that doesn't look super sexy.

I felt it's a great opportunity to bite at what I see as an iconic laggard while shareholder yield is temporarily depressed (single-digit) compared to the sexiest story in the space, Nomad Foods. Among the CPG opportunities this one requires perhaps more patience, but offers up one hell of a brand portfolio that is becoming higher quality, more durable, and with a better balance sheet at a time the space is unloved-to-hated.

$NOMD I won't spend a lot of time on this one. @NuggetCapital has done a better job writing it up than I'll be able to. It's Europe's frozen foods giant and the sexiest story in the space. There's no junk food baggage like Campbell's, top-notch insider ownership, insider buying, shareholder alignment, improving balance sheet, and the valuation gap to peers will close whether through share price appreciation or acquisition by a peer or private equity.

$CAG has insider buying (not nearly as much as Nomad) and substantial progress on the balance sheet meeting a dividend that should be cut and retail investors focusing on Chef Boyardee (divested, they don't even own it anymore) instead of the company's frozen and refrigerated foods core engine and trend-advantaged snacks segment. Cash flow is being directed towards deleveraging which could be accelerated through a dividend cut. FCF conversion is up and divestitures of weak brands have accelerated deleveraging, taking some pressure off the cut, but it's still a bit silly.

Snacks have been eating it due to GLP-1 and health trends but high-protein and/or fiber-rich offerings in sunflower seeds, popcorn, and meat snacks compare favorably both in recent performance and future prospects to peers like Campbell's potato chips, pretzels, and snack crackers.

Shareholder yield is in the low 20s, with the lion's share being debt reduction. A dividend cut would only increase that share and with time open the door to buybacks.

$KHC among the four CPG positions I have the least confidence in the Kraft-Heinz portfolio's long-term prospects and this is going to be the first position to be liquidated on opportunity cost or a substantial return on investment. Key takeaways here are insider (CEO) buying, the most robust (and improving) balance sheet among the bunch, bottom barrel EV/FCF valuation, and a strong, stable core of taste elevation (condiments, spreads, etc).

The merger of Kraft and Heinz should have never happened. Berkshire and 3G capital took a private equity approach to public markets and just like everything private equity, it forged a massive piece of shit. On the plus side, new investment in innovation and reinvigoration of the portfolio should be low-hanging fruit for better comps. I don't believe that reinvestment and innovation has any long-term potential.

The stock closed Friday above its 200DMA for the first time since October 2024 and appears to have the strongest bottom technically among depressed CPG names, if you give technical analysis any credence.

- $CPB story of opportunity cost. There may be some outperformance due to short-covering now that the name has been removed from the S&P 500 index and on rotation back into the sector, but the opportunity costs are better turnaround stories in Conagra and Nomad, higher quality portfolios in those General Mills, better long-term prospects in the prior, or stronger shot-term technicals on better balance sheet quality in Kraft-Heinz. This one will probably take more patience than General Mills and the ride is likely to be less pleasant, but it's still more attractive than orbital weed farms or whatever the index is rebalancing to.

Energy

- $SU taking more profits to bring integrated oil exposure to 19.4% weight. The Petro-Canada franchise and Suncor's refining assets are truly a jewel. I don't want overweight upstream exposure and believe the intermediate-term price of WTI is more likely to settle in the mid-60s to 70 rather than 80s and so positioning has been adjusted accordingly.

$XOM this was just a minor rebalance to keep integrated oil exposure where it is. Exxon's upstream:downstream balance, refining and marketing business, world-class petrochemical business, and stellar corporate stewardship position it well to deal with the chaos of a post-Hormuz production free-for-all into a market challenged by refining capacity, though I feel valuation is at a premium here.

- $MPC removal flat to right size energy on Monday. Haven't been at ease with this one and may revisit Exxon's weight in it's favor. The price is right, but you pay for it by missing upstream integration. Robust refining tailwinds and a buyback machine are attractive on a relative, though not absolute basis, and so the desired net upstream exposure of the portfolio is the big question here. Stay tuned.

Tenaz Energy remains unchanged after heavy adds in recent weeks.

I'll catch up on broader market commentary in next week's writeup. Thank you for your readership as always and I hope that you and yours have a wonderful week ahead!

1

3

22

1,598

GPT-5.5, GPT-5.4, and Codex are now GA on Amazon Bedrock, callable via IAM and SigV4. Microsoft spent years securing exclusive OpenAI access. As of June 1, Amazon is also handing it out. Multicloud is now true for foundation models. 🤝 #OpenAI

aws.amazon.com/about-aws/wha…

8

Manish chaturvedi retweeted

Jun 13

Visit: iob.bank.in/en/iob-non-calla…

Put your surplus funds to work with Indian Overseas Bank's Non-Callable Deposit.

Enjoy attractive returns, fixed tenure options and the confidence of a secure investment.

#IOB #IndianOverseasBank #NonCallableDeposit #FixedDeposit #SmartInvesting #GoodPeopleToGrowWith #DFS #RBI #IOBForYou

12

26

576

Bank of Baroda (BoB) has launched a special 555-day retail deposit (below ₹3 crore) scheme, offering an interest rate of 6.75 per cent per annum to the general public on a callable deposit and 6.80 per cent on a non-callable deposit.

trib.al/B6sdUmg

1

3

424

20h

Tool calling is the biggest unguarded attack surface in LLM agents. So I built Glyph Protocol: every tool ships as a cryptographically signed card. Verify before you call, trust-on-first-use pinning, confirmation gates for risky ops, verifiable receipts, full audit log.

And, I shipped it where hermes: glyphp-hermes, a pip plugin that brings Glyph natively to @NousResearch's Hermes Agent.

Handshake → fetch signed cards → verify → trust eval → (confirm) → call → verify receipt → audit. All inside Hermes.

It works, today:

• 9 demo tools register in Hermes and reply with verified receipts

• Confirmation gate live (fs.write → prepare → token → call)

• Trust manager blocks any tool whose card changed (CARD_CHANGED)

• verify_glyph / verify_receipt green

• 193 tests passed

But i hit a wall. Two gaps in Hermes' plugin API are the only things keeping Glyph from protecting everything instead of just what we add. Both are small, additive hooks. @Teknium 👇

Gap 1 — no lazy tool loading

Every registered tool gets injected into the system prompt as a function def: ~400 tokens × the bridged set ≈ 7.2k tokens every turn, used or not.

Ask: register_tool(..., lazy=True) — discoverable callable, resolved at runtime. Same as MCP tools already do.

Gap 2 — no tool middleware

A plugin can only add tools. It can't wrap Hermes' native ones (browser, file, terminal) in the Glyph pipeline.

Ask: an on_tool_call(name, args) → (proceed, modified_args) hook, so any call can pass through sign → trust → confirm → receipt before it runs.

Impact

These two hooks turn Glyph from additive into enveloping:

• Tools protected: 9/140 → 140/140

• Fixed tokens/turn: 7,200 → 0

• Native tools (browser/file/terminal): unprotected → full Glyph pipeline

• Security model: bolt-on → everything routes through Glyph

@NousResearch @Teknium — two small API hooks (lazy registration a tool-call interceptor) would make Hermes the first agent with a verifiable, signed security layer over 100% of its tools.

The plugin is built, tested, and open. Happy to spec it or send to PR. Who do we talk to?

🔗 github.com/Monoperro0207/gly…

glyphp.com

1

1

2

77