Los acuerdos de colaboración con empresas COMPROMETIDAS CON LA EDUCACIÓN, permiten que sus trabajadores alcances sus metas personales, laborales y de su comunidad.

#ICHEAChihuahua #COMMSCOPE

1

1

5

We are proud to announce that CommScope has joined the 9th Annual Airport Modernization Summit as a Silver Sponsor.

📅 13th - 14th July 2026

📍 New Delhi, India

🌐 ams.traiconevents.com/

#traicon #AMSINDIA #CommScope #AirportConnectivity #NetworkInfrastructure #SmartAirports

13

Jun 11

Strong Day 1 at @DCDNEWS Connect APAC 2026 in Bali, connecting on AI-ready data centers.

Excited to showcase CommScope Rapid Fiber Connect for faster, simpler high-density fiber deployments: ow.ly/ET7E50Z9VUH

Looking forward to Day 2.

#DCDConnect #CommScope

1

136

At @MSD_Solutions, we provide end-to-end fiber infrastructure solutions powered by @CommScope , helping service providers, enterprises, data centers, and smart facilities build resilient, high-performance networks that support both current requirements and future growth.

2

I'll only say it once.This might be the fastest way to accumulate $3 million by the end of 2026:

$AAOI (Applied Optoelectronics) → $196 Must buy

$NOK (Nokia) → $13 Must buy

$COMM (CommScope) → $45 Must buy

$VIAV (Viavi Solutions) → $42 Must buy

$LITE (Lumentum Holdings) → $892 Must buy

$CIEN (Ciena) → $452 Must buy

I often get asked why I don't turn this into paid content, but for me, sharing stock information is just a hobby.

I'm not financially struggling, so I choose to share it for free.

NFA

4

1,090

Jun 8

AI reshapes the network edge; fiber infrastructure is key.

Explore evolving FTTH designs for faster, scalable AI networks. ow.ly/vjQ750Z7Fiu

#FTTH #AI #CommScope

ALT Blue-toned digital graphic showing a suburban neighborhood with fiber optic light trails and text promoting a blog on AI and fiber networks by CommScope.

89

Jun 6

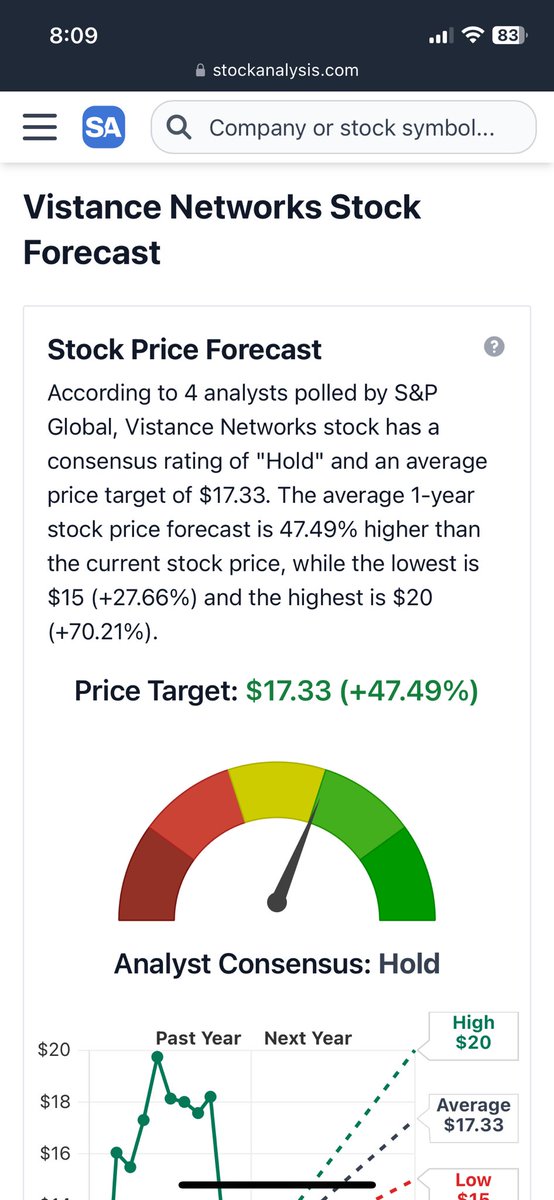

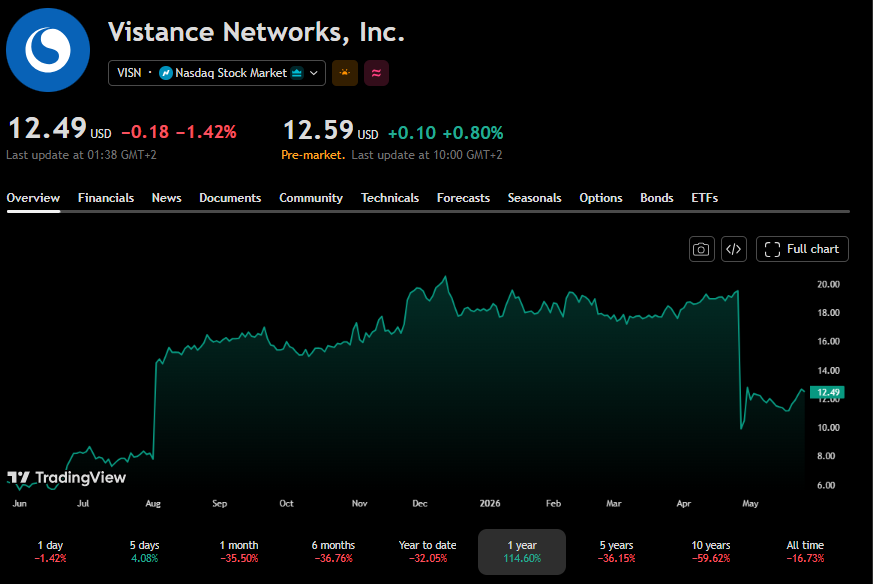

$VISN

Early Saturday morning banger incoming. Get your notes ready. I better see Mark Cuban and BJ Novak GIFs.

This is NOT the next $ANET, $UI, or $CMCSA.

$VISN is something different.

It is becoming one of the market’s few PURE-PLAY broadband access infrastructure companies.

Repost. Bookmark. Subscribe $1.

With a market cap of only ~$2.5B, I think this is one of the more overlooked infrastructure stories in the market today.

The company formerly operated under the CommScope umbrella, but after selling its Connectivity & Cable Solutions business to Amphenol for roughly $10.5B and agreeing to sell the RUCKUS business to Belden for approximately $1.85B, management is transforming the company into a focused Aurora Networks pure-play.

Aurora operates in one of the most important layers of modern digital infrastructure.

While investors focus on data centers, GPUs, and cloud providers, Aurora sits much closer to the customer. The company provides the technologies that help cable operators and telecom providers actually deliver multi-gigabit broadband to homes and businesses.

Its portfolio includes DOCSIS 4.0 infrastructure, Distributed Access Architecture (DAA), Remote PHY solutions, virtualized cable platforms, fiber access technologies, and next-generation PON deployments. These are the tools operators need to modernize networks without completely rebuilding existing infrastructure.

The growth is already showing up in the numbers.

During Q1 2026, Vistance generated $471.8M of revenue, representing 21.6% year-over-year growth. Aurora Networks was the primary growth engine, generating $298.4M of revenue and growing 32.6% year-over-year as demand accelerated for DOCSIS 4.0 amplifiers, FDX nodes, Remote PHY products, DAA deployments, and fiber access solutions.

RUCKUS also contributed positive growth, generating $173.4M of revenue and increasing 6.3% year-over-year, demonstrating strength across both segments before the planned divestiture.

Aurora is benefiting from DOCSIS 4.0 deployments with major North American operators, continued Distributed Access Architecture rollouts, fiber-deep network migrations, virtualized broadband solutions, and large-scale broadband modernization projects in Europe and Latin America.

The company also reported adjusted EBITDA of $87.3M during the quarter, up 38.4% year-over-year, while adjusted EBITDA margins expanded to 18.5%. Aurora alone delivered roughly $50M of adjusted EBITDA, increasing approximately 32% from the prior year period.

Another reason I find the story compelling is the visibility management is beginning to build. Orders increased 49% year-over-year during Q1 and total backlog reached approximately $843M, providing meaningful support for future revenue growth. Aurora’s backlog alone approached $400M.

The customer relationships are also difficult to replicate.

Aurora has longstanding relationships with major broadband operators including Comcast, Vodafone Germany, Liberty Global, and numerous cable and telecommunications providers around the world. Comcast has historically represented roughly 35% of sales, and the company continues to benefit from ongoing DOCSIS 4.0 deployments across that network.

The broader investment thesis is simple.

Management has guided for Aurora standalone adjusted EBITDA of approximately $225M-$250M in 2026, while continuing to invest behind DOCSIS 4.0, PON, DAA, and virtualized broadband platforms.

At roughly $2.5B market cap, around $2B of annual revenue, and approximately 1.3x sales, I believe the market is still valuing VISN primarily as a restructuring story.

I think investors should be paying closer attention to what Aurora could become over the next several years.

$VISN $CSCO $ANET $NBIS $IREN $AAOI $COHR $NOK $HLIT $UI $AVGO $GOOG $MSFT $BB $MU $AMD $DGXX $HYLN

This isn’t an AI hype stock.

It’s a broadband infrastructure enabler sitting directly in the path of increasing global data consumption.

21

7

67

3,314

Jun 4

What market is looking in sterlite Tech

Their current relation with hyperscalers and their reputation.

Which paves ways to future tech and participation.

Remember Corning and Commscope

2

30

2,833

Welcoming @CommScope as In Association With Partner at #BroadbandIndiaSummit2026—powering next-gen connectivity.

1

2

10

May 28

The Anatomy of a Financial Engineering Masterpiece: Why $VISN Plummeted 36% and the Massive Cash Trap Left Behind

Imagine walking up to a luxury penthouse listed for $12 million.

Inside, the owner points to a secure vault packed with $7 million in cash and promises it is entirely yours on closing day.

When you look for the catch, you realize the keys to the vault will take a few months to clear, and the broader market is steering completely clear of the property simply because the building's exterior still bears a tarnished "Foreclosure" sign from the past.

This is precisely the type of spectacular market anomaly occurring right now with Vistance Networks ($VISN).

In my last post, we broke down the fundamental setup over at HILT.

Today, we are diving straight into the deep end of structural corporate arbitrage.

If you take a surface-level look at the raw stock chart of $VISN over the last few months, you see what looks like a textbook disaster - shares collapsed from the $20 range to the current $12.38. Instinct says: run.

Yet, when we peel back the layers of market noise, filter out the automated AI slop, and scrutinize the latest 8-K filings and SEC disclosures from late April and May 2026, a completely different reality emerges.

This isn't an operational failure. It is a highly aggressive, meticulously planned liquidation of an old debt-laden conglomerate designed to unlock massive cash and hand it straight back to shareholders.

Let's dissect exactly what is happening under the hood.

1⃣The Great Reset: Erasing the Ghost of CommScope

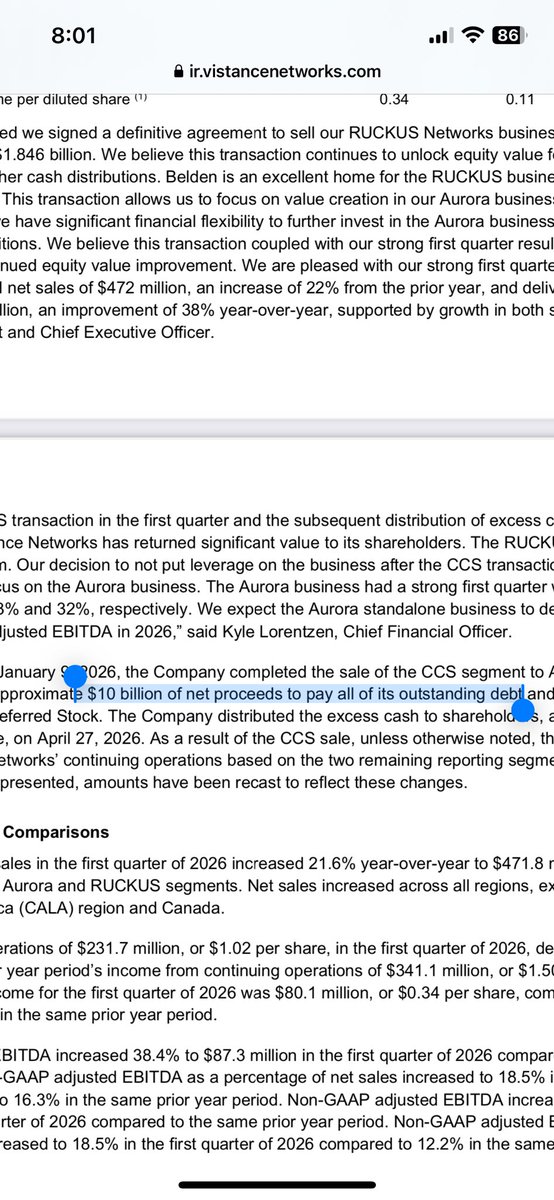

To understand why $VISN is trading at just $12.38 today, we have to look back to January 9, 2026.

On that day, the heavily indebted legacy titan known as CommScope Holding Company finalized the deal of a lifetime: it sold its cornerstone Connectivity and Cable Solutions (CCS) segment to Amphenol Corporation for a staggering $10.5 billion in pure cash.

As part of the transaction, the "CommScope" name and brand transitioned to Amphenol.

The remaining listed entity changed its corporate name to Vistance Networks, Inc. and hit the Nasdaq under a brand-new ticker: $VISN.

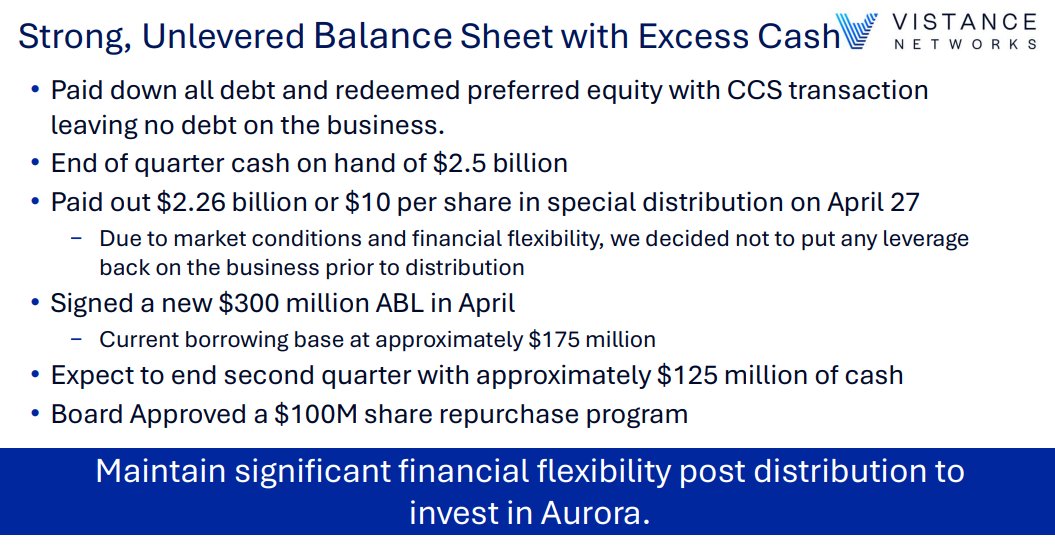

Faced with a literal mountain of money ($10.5 billion), management executed a balance sheet cleanup of a scale rarely seen on Wall Street:

➡️Total Debt Obliteration:

They completely wiped out the company's choking liabilities, fully redeeming outstanding Senior Secured Notes due 2031, terminating credit agreements, and buying out preferred equity held by firms like Carlyle Group.

➡️A Monstruous Dividend Payout:

On April 27, 2026, shareholders were paid a massive $10.00 per share special cash distribution (classified for tax purposes via IRS Form 8937 as a return of capital due to the lack of historical accumulated earnings and profits).

This massive $10.00 distribution is the sole, technical reason the stock chart appeared to "crash" overnight.

The company transformed from a highly leveraged zombie into an agile entity with zero net debt.

2⃣The Second Strike: Selling RUCKUS for $1.84 Billion

Just as mainstream analysts were rewriting their financial models for the "new" $VISN - expecting it to operate as a twin-pillar tech firm running the Aurora broadband segment and the RUCKUS wireless business - management dropped a second bombshell.

On April 30, 2026, Vistance Networks announced a definitive agreement to sell its RUCKUS Networks reporting segment to Belden Inc. (NYSE: BDC) for $1,846 billion in cash.

This divestiture is an absolute masterclass in unlocking value for three primary reasons:

➡️Premium Valuation:

Belden is paying roughly 13x projected 2026 Adjusted EBITDA for RUCKUS. Before this announcement, the market was lazily pricing the entire $VISN complex at a mere 7x to 8x multiple.

Vistance perfectly exploited Belden’s strategic urge to acquire high-density Wi-Fi 7 and enterprise switching tech to bridge their IT/OT architecture.

➡️Clean Dry Powder:

After taxes and deal-related friction, Vistance will net approximately $1.7 billion in cash upon closing, slated for the second half of 2026.

➡️The Dividend Sequel:

Management left no room for speculation, explicitly declaring in the official announcement that they “intend to distribute a significant portion of the excess proceeds to shareholders in the form of a special distribution within 60 days of closing the transaction.”

3⃣The Brutal Math of the Arbitrage Trap

Let’s lay out the basic arithmetic, because the numbers highlight a massive disconnect between the stock price and the underlying corporate actions:

➡️Current Stock Price: $12.38

➡️Vistance ($VISN) Market Cap: ~$2.82 billion

➡️Expected Net Cash from RUCKUS Sale: $1.70 billion

The cash alone flowing into the company in a matter of months accounts for more than 60% of its total market capitalization.

If the board allocates just $1.2 to $1.3 billion of those proceeds toward the next special dividend, investors can expect a massive direct cash return of roughly $4.50 to $5.00 per share.

By buying equity at $12.38 today, you are effectively positioning yourself to recoup nearly half of your principal investment in cash before the year is out.

4⃣What’s Left In the Box? The Hidden Value of Aurora Networks

Once the RUCKUS transaction closes, Vistance completely sheds its legacy conglomerate identity.

It emerges as an ultra-focused, niche "pure-play" infrastructure company operating entirely under the banner of Aurora Networks (formerly the Access Network Solutions arm).

➡️What exactly is this remaining core, and why is the market's blind spot creating a massive opportunity here?

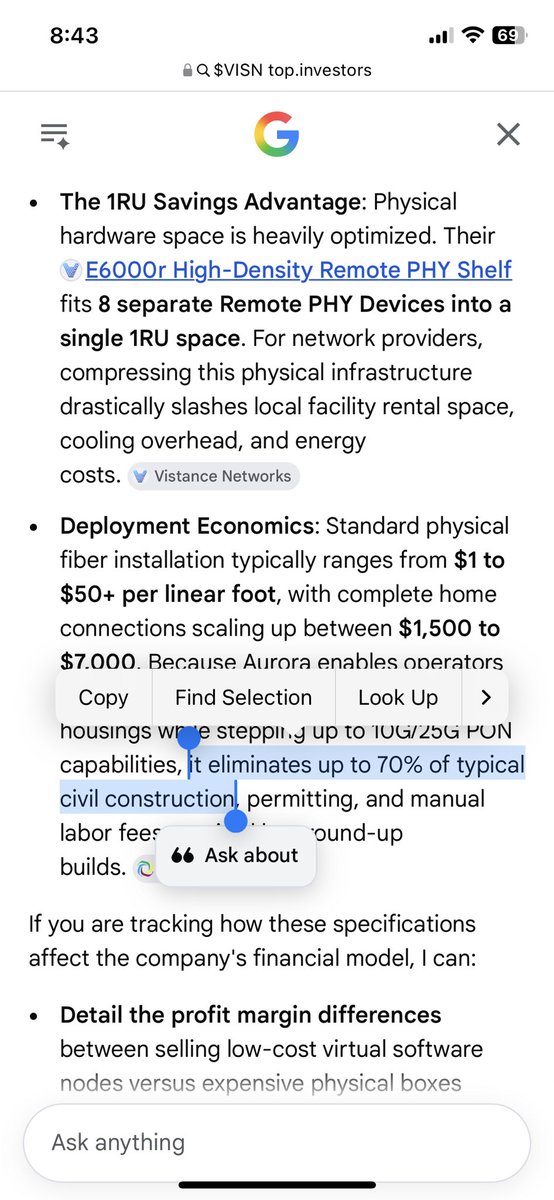

Aurora is the physical and digital architecture powering modern broadband.

The segment provides the high-tech machinery of the "last mile" of data transmission: advanced hybrid fiber-coaxial (HFC) systems, passive optical networks (PON), physical optical nodes, and intelligent line amplifiers.

This isn't low-margin commodity cable manufacturing; it is specialized hardware integrated with proprietary software managing immense data flows.

In the Q1 2026 financial results reported on April 30, this core segment proved its operational health is highly robust:

➡️Quarterly Revenue: $471.8 million (beating consensus estimates by $10 million).

➡️Adjusted Earnings Per Share (EPS): $0.34 (comfortably beating Wall Street projections of $0.22).

5⃣The DOCSIS 4.0 Supercycle: Fuel for the Next 5 Years

The multi-year catalyst anchoring Aurora is the massive, non-negotiable architectural upgrade currently sweeping North American cable infrastructure: the transition to DOCSIS 4.0.

Major multi-system operators (MSOs) like Comcast and Charter Communications face a competitive wall - they desperately need to deliver symmetrical multi-gigabit speeds and ultra-low latency to counter direct fiber-to-the-home (FTTH) buildouts.

Instead of spending hundreds of billions ripping up physical ground infrastructure to lay new fiber everywhere, operators are taking a drastically faster, capital-efficient route: upgrading their existing hybrid fiber-coaxial networks using Aurora's state-of-the-art equipment.

➡️Blue-Chip Backlog:

Aurora is the foundational vendor driving Comcast's massive, multi-city deployment of Full Duplex (FDX) amplifiers.

The order book heading into the back half of 2026 is swelling as the wider industry moves out of testing and into mature, mass-market rolling deployments.

➡️Consolidation Strategy:

The broadband infrastructure sector is highly fragmented.

Following the RUCKUS sale and the subsequent dividend distribution, Vistance is poised to retain several hundred million dollars of unallocated cash.

Management’s stated forward strategy is to use this "dry powder" to aggressively acquire smaller, high-margin niche hardware and software players, positioning Aurora as the undisputed, unified consolidation platform for access network technology.

6⃣Real Structural Risks to Keep in Mind

Investing in special situations and corporate spin-offs demands an objective view of execution risks. For the "new" Aurora, two issues matter most:

➡️Stranded Corporate Costs:

Dismantling a legacy corporate giant means the slimmed-down Aurora initially inherits structural overhead (redundant real estate, large-scale IT enterprise systems, legacy administrative burdens) from old CommScope.

Management must aggressively slash these legacy costs over the next two quarters to protect operating margins.

➡️Product Margin Shifts:

The initial phase of transitioning clients away from legacy tech and onto newly manufactured DOCSIS 4.0 components naturally carries tighter early-stage gross margins before manufacturing hits peak volume efficiencies.

This explains why management's current Q2 2026 guidance projects relatively flat quarter-over-quarter growth.

⬇️The Verdict: A Free Option on Broadband Infrastructure

The broader market has evaluated $VISN using a completely rigid, automated perspective.

Quantitative algorithms see a "steep year-to-date chart decline" combined with "declining aggregate revenue" (ignoring that revenue vanished because the massive CCS unit was intentionally carved out). The result is unthinking selling pressure.

The true picture represents a highly asymmetric risk/reward configuration:

➡️Hard Capital Downside Protection:

The impending $1.7 billion cash injection from Belden creates an absolute structural floor for the asset.

The potential for shares to sustain a fundamental drop below the $11–$12 mark is heavily insulated by the cash value of the deal.

➡️The "Free" Aurora Growth Engine:

When you net out the explicit value of the RUCKUS deal, the market is effectively valuing the remaining, profitable Aurora broadband business at nearly zero.

Investors are being handed the leading player in the domestic DOCSIS 4.0 upgrade cycle virtually for free.

At $12.38, $VISN is a compelling, high-conviction play on pure capital arbitrage and deep asset mispricing.

Wall Street likely won't re-rate the equity to its fair structural value until the second special dividend is cleared by regulators and Aurora displays the full, unencumbered operating leverage of its independent margins late this year.

May 26

$HLIT I’ve been watching this company for two weeks (since their solid earnings report).

It has been getting a lot of attention lately, and while I might not be the most original here, I really like what I see.

But investing isn't about being original; it's about making money.

I haven't bought any shares today, but I am strongly considering it.

First of all, big congratulations to @KawzInvests, @CKCapitalxx , and @michaelsikand for pulling this Cinderella out of the shadows and onto the main stage. Excellent fundamental eye.

Here is a little secret - I currently work in the ICT industry, so I see this market from the inside.

I recently found out that the first smaller tier operator in my country has started deploying Harmonic’s solutions.

The market giants haven't made the move yet - yet, because given current technical realities, they simply have no other choice.

This means one thing: we are still incredibly early.

@KawzInvests has written extensively about the adoption wave in the US, but I am looking at this from Europe.

This is a massive market where infrastructure challenges are often significantly worse due to extreme population density and decades-old urban layouts.

So not only US, but whole world is global TAM.

Here is my view of $HILT story

1⃣The Infrastructure War:

Squeezing HFC and xPONTo understand the investment thesis for $HLIT, you have to look underground at the physical and financial constraints of global broadband delivery:

➡️HFC (Hybrid Coaxial-Fiber):

This is the dominant legacy footprint owned by cable giants.

Historically, it’s an operational nightmare - prone to RF signal attenuation, "ingress noise" (interference leaking into old copper lines), and dependent on a delicate cascade of physical, power-hungry analog amplifiers that fail during seasonal temperature swings.

➡️xPON (Pure Fiber-to-the-Home):

Regarded as the long-term endgame, but operators face immense deployment bottlenecks.

Tearing up dense European cities to lay new fiber to every single doorstep requires unimaginable capital expenditures (CAPEX) and years of bureaucratic permitting.

Furthermore, xPON relies on shared bandwidth architecture; as data traffic explodes, existing optical lines experience severe split-ratio congestion at the central offices.

⬇️Where Harmonic steps in:

Their cOS platform (virtualized CMTS) completely digitizes the hardware architecture, commanding an absolute monopoly in the virtualized core.

The software platform now powers 150 customers globally, serving 45.7 million connected devices.

For HFC cable operators, cOS replaces failure-prone analog headends with centralized software and simple, dumb optical nodes.

By upgrading to the DOCSIS 4.0 standard via software, operators achieve multi-gigabit symmetric speeds over their already deployed and fully depreciated coaxial assets.

But here is the critical expansion: Harmonic is now a fiber play as well.

For xPON networks, Harmonic’s cloud-native virtual OLT solutions allow fiber providers to decentralize and virtualize their optical routing.

Instead of building massive, expensive new hardware aggregation hubs to solve fiber congestion, operators use Harmonic's software to dynamically allocate and optimize bandwidth across existing fiber strands.

Whether it is cable or fiber, Harmonic acts like DSP (Digital Signal Processing) did for telephone wires decades ago - it squeezes unprecedented life and efficiency out of an existing medium.

Paying Harmonic for software is a pure financial play for infrastructure giants to extract maximum ROI from historical CAPEX.

2⃣Business Model and TAM Expansion

Harmonic does not target your local neighborhood ISP.

Their sales model exclusively targets large-scale Tier-1 infrastructure operators managing millions of subscribers.

They monetize this via a highly predictable Hardware-Enabled Software hybrid model:

➡️The Initial Hook:

They sell physical optical nodes and hardened appliances to the operators.

The gross margins on these are lower due to hardware manufacturing and global chip costs.

➡️The High-Margin SaaS Core:

To run those nodes, operators must purchase ongoing subscription licenses for the cOS software core, billed per active connected customer modem.

This drives a highly recurring, high-margin revenue stream.

➡️The Addressable Market:

The market for core virtualized cable infrastructure is scaling toward $1 Billion by 2030.

Concurrently, by utilizing the cOS ecosystem to aggressively break into the pure fiber access market (Remote OLT), Harmonic is tapping into an additional global fiber TAM of over $2.5 Billion.

As an agile new entrant in pure fiber, Harmonic already saw fiber products represent over 14% of its appliance and integration revenue over the past year.

3⃣Dissecting the Financial Reality

The latest financial statements validate the immense operating leverage of this software-centric pivot:

➡️The Strategic Corporate Cleansing:

On March 20, 2026, Harmonic formally executed a definitive Asset Purchase Agreement to sell its legacy, low-margin Video business to MediaKind for $145 million in cash.

The transaction is on track to close during this current quarter (Q2 2026).

The Video segment has already been moved to "discontinued operations," leaving HLIT as a pure-play broadband tech stock.

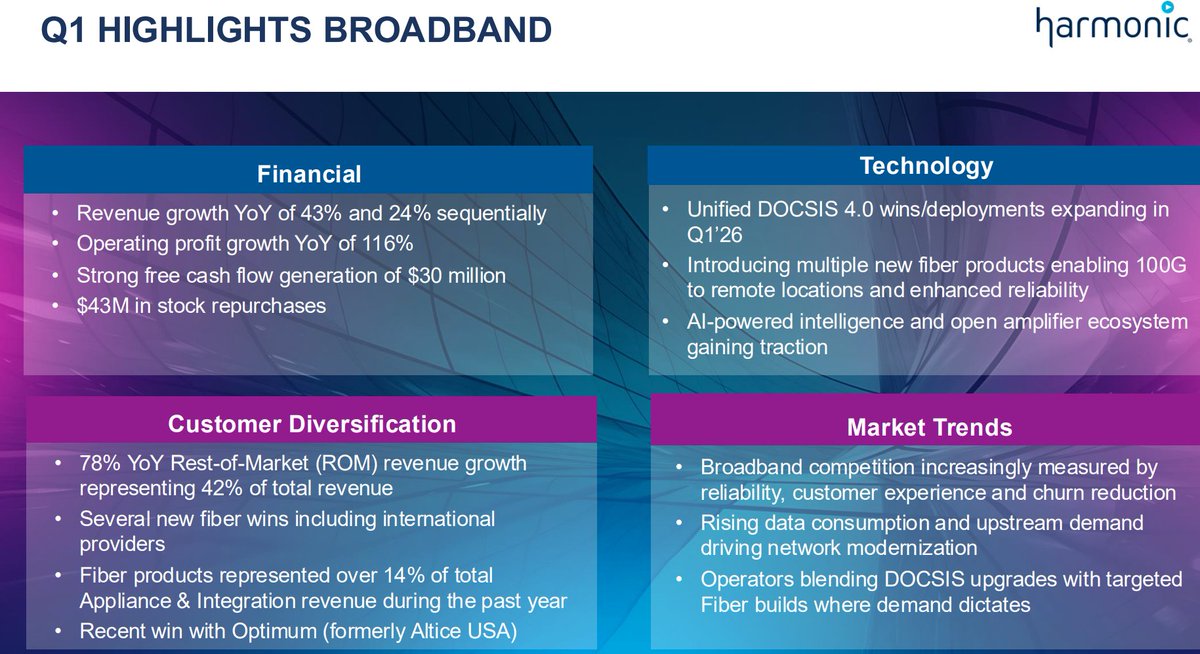

➡️Top-Line Surge:

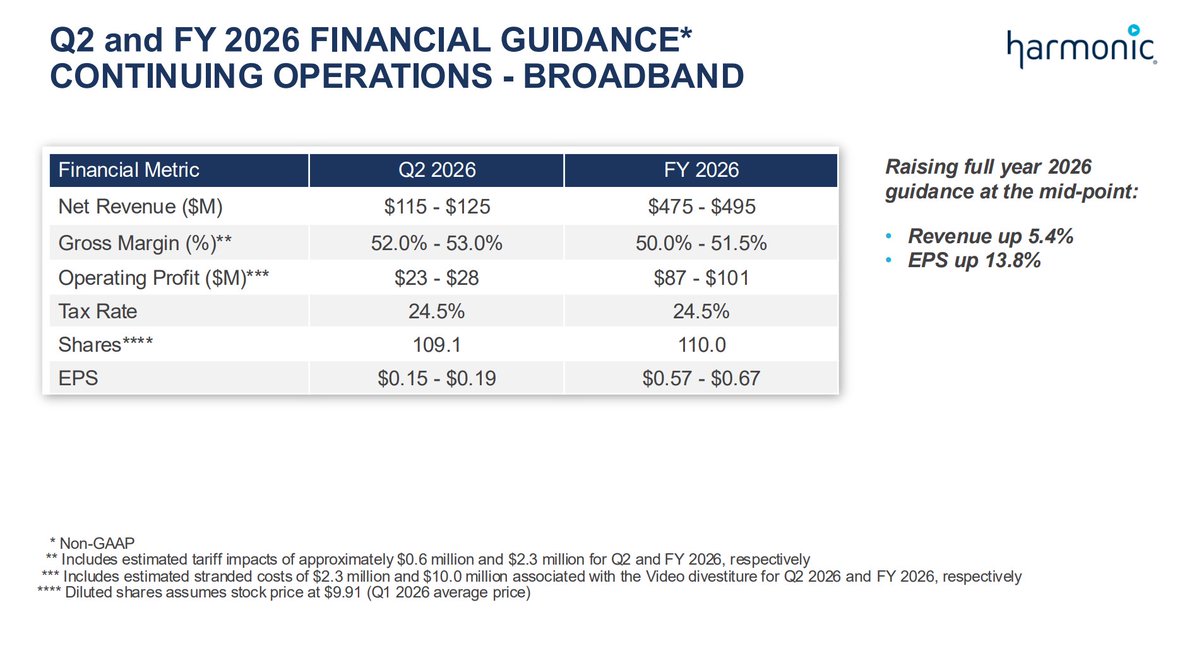

Pure Broadband revenue from continuing operations rose an impressive 43% year-over-year to $121.7 million (beating management’s own guidance range of $100M–$105M).

➡️Guidance Hiked & Backlog Up:

Backed by accelerating commercial traction, management officially raised full-year broadband revenue guidance to $475M–$495M.

Total broadband backlog and deferred revenue grew 87% YoY to a record $582.1 million, with 60% contractually obligated to convert to revenue within the next 12 months.

➡️De-risking Customer Concentration:

Bears always point out HLIT's historical reliance on Comcast.

However, the latest data reveals a massive structural shift: HLIT’s "Rest-of-Market" (non-top 2 clients) segment grew an explosive 78% YoY, now accounting for 42% of total revenue, driven directly by international Tier-1 rollouts - particularly across dense European footprints.

➡️The Margin Counter-Weight:

To remain completely objective, watch the near-term margins.

While Broadband non-GAAP gross margins were strong at 54% in Q1, full-year non-GAAP guidance sits at 50%–51.5% due to a temporary $6 million macro headwind from elevated global memory component costs (RAM/Flash) used in initial product hardware ramps.

The Summary👇

Thanks to my background in the ICT sector, I can see that the modernizing wave hitting Europe is just the tip of the iceberg.

When the Video divestiture closes this quarter, Harmonic will enter H2 as a debt-free, cash-rich pure-play broadband machine with absolute market dominance.

As Wall Street permanently shifts its valuation models from low-multiple telecom hardware to high-multiple enterprise software metrics, a major structural re-rating is highly likely.

I really consider to join to this party tomorrow.

8

4

40

12,970

May 28

FIBER INTERCONNECTION AND OPTICAL TRANSPORT

LONG-HAUL AND MIDDLE-MILE AI FIBER BUILDOUT IS STILL EARLY AND MAY BECOME A 2027-2028 ACCELERATOR (READ-THROUGH 10)

Affected companies: Ciena (CIEN: US), Corning (GLW: US), Coherent (COHR: US), Nokia (NOK: Finland), Lumen Technologies (LUMN: US), and private fiber network owners such as Zayo.

Directional impact and magnitude: positive, medium-to-large for optical transport and fiber suppliers; positive, medium for fiber network owners with relevant long-haul routes. The magnitude is largest for suppliers exposed to high-capacity coherent optical systems, high-count fiber, data-center interconnect, and long-haul network upgrades.

Call support: Management stated that long-haul and middle-mile remain in “early innings,” with calendar 2027 “coming online” and calendar 2028 becoming the “fast and furious” year. Management also said the previously discussed $20 billion long-haul/middle-mile opportunity has “certainly grown.” The most important technical datapoint was management’s reference to customers discussing routes with “up to 7,500 to 10,000 fiber strands per route,” compared with common 864- or 1,728-count deployments today.

Transmission mechanism: 7,500-10,000-strand route discussions indicate an architectural shift rather than incremental maintenance. AI workloads, cloud regions, and data-center clusters require much higher bandwidth between campuses, metros, and long-haul routes. This pulls through high-count fiber, conduit, splicing, route engineering, optical transport, coherent modules, line systems, and network monitoring. For Ciena and Nokia, the read-through is stronger for optical transport and long-haul network equipment. For Corning, it is stronger for fiber cable and connectivity. For Coherent, it supports longer-duration demand for optical components tied to high-capacity networking.

Near-term trading catalyst: limited near-term revenue impact relative to FTTH because management explicitly framed this as a 2027-2028 acceleration. The near-term catalyst is sentiment and backlog commentary, not immediate revenue.

Longer-duration fundamental shift: the call suggests AI infrastructure requires a new middle-mile and long-haul fiber architecture that could last more than a decade. That is a major fundamental read-through because it extends the fiber cycle beyond residential passings and into data-center interconnect, hyperscaler connectivity, and high-capacity backbone modernization.

BEAD AND RURAL BROADBAND

BEAD IS A CALENDAR 2027 FUNDAMENTAL UPSIDE RATHER THAN AN IMMEDIATE 2026 REVENUE CATALYST (READ-THROUGH 11)

Affected companies: Calix (CALX: US), ADTRAN Holdings (ADTN: US), Nokia (NOK: Finland), Corning (GLW: US), CommScope (COMM: US), MasTec (MTZ: US), Primoris Services (PRIM: US), and Dycom Industries (DY: US).

Directional impact and magnitude: near-term neutral-to-negative for companies where investors expect material 2026 BEAD revenue; long-term positive, medium, for broadband equipment, fiber materials, and rural construction beneficiaries.

Call support: Management said, “We still believe that we will see revenue in Q2 of this year,” but clarified that investors should “think about that as a calendar 2027” opportunity when BEAD “really starts to take hold and get moving.” Management also stated that BEAD is “not included in our outlook,” making it “potential uplift” for this year rather than a base-case requirement.

Transmission mechanism: BEAD’s conversion from policy approval to field revenue depends on state processes, subgrantee awards, permitting, engineering, procurement, and mobilization. Dycom’s commentary indicates that some small programs can begin earlier, but the larger revenue wave is likely later. That means equipment suppliers and contractors with BEAD exposure may see order timing shift into calendar 2027 rather than materially boosting 2026 numbers.

Near-term trading catalyst: negative for any company whose near-term estimates require a sharp BEAD ramp in 2026. The call supports patience rather than immediate revenue acceleration.

Longer-duration fundamental shift: positive for the broader rural broadband ecosystem once state and subgrantee pipelines convert into awards and construction. BEAD should extend the fiber cycle into harder-to-reach rural markets, which can increase cost per passing and sustain demand for fiber materials, access equipment, engineering, and construction labor. The timing is later, but the structural demand remains intact.

1

3,035

May 28

$DY KEY READ-THROUGHS FROM DYCOM INDUSTRIES Q1 FY2027 EARNINGS CALL

Dycom’s Q1 FY2027 call was a strong cross-sector signal that U.S. digital infrastructure investment is accelerating simultaneously across fiber-to-the-home, long-haul and middle-mile fiber, data-center electrical construction, and low-voltage structured cabling. The highest-value datapoints were Q1 revenue of $1.965 billion, up 56% year over year; organic growth of 25%; Communications organic revenue growth of 24.7%; fiber-to-the-home work up 33% sequentially; Building Systems revenue of $395.4 million at 17.7% adjusted EBITDA margin; record backlog of $11.9 billion; 2.2x book-to-bill; and management’s statement that “the momentum behind fiber deployments and data center builds is stronger today than we have ever seen.” The broader read-through is clearly positive for power demand, utilities in data-center-heavy geographies, merchant generators, electrical equipment suppliers, specialty contractors, fiber materials vendors, and optical transport suppliers. The offsetting negative implications are concentrated in cable broadband competition, telecom carrier free-cash-flow pressure from sustained capex intensity, hyperscaler and data-center landlord construction-cost inflation, and timing risk for companies expecting BEAD to convert into material 2026 revenue.

POWER, UTILITIES, AND ELECTRIFICATION

DATA-CENTER PHYSICAL BUILD ACTIVITY VALIDATES THE LOAD-GROWTH TRAJECTORY FOR UTILITIES AND MERCHANT POWER (READ-THROUGH 1)

Affected companies: Dominion Energy (D: US), Exelon (EXC: US), American Electric Power (AEP: US), Sempra (SRE: US), CenterPoint Energy (CNP: US), Constellation Energy (CEG: US), Vistra (VST: US), Talen Energy (TLN: US), and NRG Energy (NRG: US).

Directional impact and magnitude: positive, medium-to-large for regulated utilities with data-center load exposure; positive, medium-to-large for merchant generators, nuclear owners, and capacity-constrained power markets. The magnitude is highest where data-center development overlaps with constrained transmission, scarce interconnection capacity, and high-value around-the-clock power demand.

Call support: Dycom stated that Building Systems generated $395.4 million of revenue at 17.7% adjusted EBITDA margin, and management raised the full-year Building Systems outlook to $1.35 billion-$1.45 billion with high-teens adjusted EBITDA margins. Management also said data-center demand “has not abated whatsoever” and is “only increasing.” The pending National Technology Integrators acquisition adds exposure in the DMV, Texas, and the Midwest, which are directly relevant regions for data-center power demand. The most important quote was: “Looking ahead, the momentum behind fiber deployments and data center builds is stronger today than we have ever seen.”

Transmission mechanism: Dycom’s data-center electrical and structured-cabling activity is a physical, construction-stage confirmation that data-center load is moving from announced pipeline to active build. That matters for utilities because energization of these facilities requires new service connections, distribution upgrades, transmission reinforcement, substation work, and, in many regions, incremental generation procurement. For merchant generators and nuclear-heavy portfolios, the same signal supports higher confidence in long-duration power demand, bilateral contracting, capacity value, and structurally tighter reserve margins. The signal is especially relevant in the DMV/Northern Virginia-Maryland corridor, Texas, and the Midwest because NTI’s footprint and customer pull are concentrated there.

Near-term trading catalyst: positive sentiment for utility and power names exposed to data-center load growth should be reinforced by Dycom’s statement that data-center demand is not slowing and that electrical/low-voltage trades are being pulled into more markets. This is a near-term narrative catalyst around earnings calls, load-growth updates, interconnection queues, and utility capex plans.

Longer-duration fundamental shift: the call supports the thesis that AI and cloud data-center demand is evolving into a multi-year electricity demand cycle, not a transient construction bulge. The longer-duration implication is higher utility rate base growth, higher transmission and distribution capex, stronger contracting demand for firm clean power and gas-backed reliability, and greater strategic value for generators with deliverable capacity near data-center load pockets. The main negative offset is regulatory and affordability risk if grid capex accelerates faster than customer bills can absorb.

DATA-CENTER ELECTRICAL EQUIPMENT DEMAND REMAINS POWERFUL AND MARGIN-SUPPORTIVE (READ-THROUGH 2)

Affected companies: Eaton (ETN: US), Vertiv Holdings (VRT: US), Schneider Electric (SU: France), Hubbell (HUBB: US), nVent Electric (NVT: US), Powell Industries (POWL: US), and Legrand (LR: France).

Directional impact and magnitude: positive, medium-to-large. The impact is most significant for companies supplying low-voltage and medium-voltage electrical distribution, switchgear, power management, thermal management, enclosures, busway, power distribution, and related electrical infrastructure used in data centers.

Call support: Management said Power Solutions “eclipsed expectations right out of the gate,” producing $395.4 million of revenue and 17.7% adjusted EBITDA margin. Dycom also stated that Building Systems margins are expected to remain in the high-teens range for FY2027. In the NTI discussion, management said structured cabling and inside-plant electrical work are “highly coordinated and in high demand.”

Transmission mechanism: high-growth, high-margin data-center electrical construction is a demand-pull signal for the electrical equipment ecosystem. Contractors such as Power Solutions and NTI do not scale without corresponding demand for electrical gear, structured cabling, rack-level connectivity, controls, power distribution, and thermal infrastructure. Sustained high-teens contractor margins imply that customers are paying for execution certainty and speed, which typically preserves pricing power upstream for equipment suppliers where supply remains tight. This is not merely a unit-volume signal; it also supports pricing, backlog visibility, and mix improvement toward higher-spec mission-critical equipment.

Near-term trading catalyst: the read-through is positive for near-term order commentary and backlog durability across electrical equipment suppliers. Dycom’s data point is particularly useful because it confirms that project execution is occurring at the construction level, rather than remaining only in hyperscaler capex announcements.

Longer-duration fundamental shift: data-center electrification is becoming an integrated construction and equipment cycle. The relevant constraint is not only chips or power generation; it is the availability of high-quality electrical engineering, switchgear, power distribution, cooling, cabling, and field labor. That favors suppliers with scale, short lead times, technical breadth, and relationships with hyperscalers, contractors, and electrical engineering firms. The negative risk is that extreme demand can create backlog quality issues, schedule slippage, or customer pushback if lead times and pricing become too stretched.

TELECOM, FIBER, AND BROADBAND

FIBER-TO-THE-HOME RAMP IS ACCELERATING AND DIRECTLY SUPPORTIVE OF FIBER MATERIALS AND ACCESS NETWORK SUPPLIERS (READ-THROUGH 3)

Affected companies: Corning (GLW: US), CommScope (COMM: US), Calix (CALX: US), ADTRAN Holdings (ADTN: US), and Nokia (NOK: Finland).

Directional impact and magnitude: positive, medium-to-large for Corning; positive, medium for CommScope, Calix, ADTRAN, and Nokia. The magnitude is highest for companies most directly exposed to fiber cable, passive connectivity, access equipment, and last-mile broadband deployment.

Call support: Communications revenue grew 24.7% organically. Management said fiber-to-the-home was the primary driver of the raised Communications outlook and disclosed that “fiber-to-the-home work grew 33% in 1 quarter’s time.” Management also said “demand for fiber infrastructure remains as strong as ever” and referenced “recent announcements from Corning to scale manufacturing capabilities in response to the demand for fiber in the coming years.”

Transmission mechanism: Dycom is a field-level indicator of carrier deployment velocity. When Dycom’s FTTH work rises 33% sequentially and Communications revenue grows almost 25% organically, the implication is that carriers are moving more aggressively from planning and permitting into actual construction. That pulls through demand for fiber cable, terminals, closures, cabinets, optical line terminals, optical network terminals, and access-network software. The read-through is particularly strong for Corning because the call explicitly referenced Corning’s manufacturing expansion as evidence of fiber demand. For Calix, ADTRAN, and Nokia, the mechanism is more downstream and timing-sensitive because access electronics typically follow network design, awards, and construction schedules.

Near-term trading catalyst: positive for fiber supplier order sentiment and for companies levered to accelerating carrier access-network deployments. The strongest near-term catalyst is the possibility that market expectations for U.S. FTTH deployment pace are too low after Dycom’s sequential FTTH growth disclosure.

Longer-duration fundamental shift: management repeatedly described FTTH as still early in the cycle. That implies a multi-year build trajectory rather than a 1-quarter catch-up. The longer-duration impact is a sustained fiber materials and access equipment cycle, with incremental support as passings expand, cost per passing rises in harder-to-build areas, and BEAD adds a later rural broadband layer.

CABLE BROADBAND COMPETITIVE PRESSURE IS INTENSIFYING AS FIBER BUILDS ACCELERATE (READ-THROUGH 4)

Affected companies: Charter Communications (CHTR: US), Comcast (CMCSA: US), Cable One (CABO: US), and Altice USA (ATUS: US).

Directional impact and magnitude: negative, medium-to-large for Charter, Cable One, and Altice USA; negative, medium for Comcast given its larger diversification. The magnitude is highest for cable operators with greater broadband revenue concentration and weaker mobile or enterprise offsets.

Call support: Management said fiber-to-the-home is “still earlier on in the overall cycle,” that “there’s a lot of growth opportunity left in fiber-to-the-home,” and that “there’s still several years where the passings are going to continue to increase.” In Q&A, management added that “the homes in America are going to get past the 60 million that our customers have talked about” and that multiple customers and markets are ramping.

Transmission mechanism: every incremental FTTH passing increases the probability that cable broadband markets face a faster shift from monopoly or duopoly broadband economics to fiber-led competitive overlap. More fiber passings pressure gross adds, churn, promotional intensity, pricing power, and long-term ARPU. Cable operators can respond with DOCSIS upgrades, mobile bundles, and price segmentation, but Dycom’s call suggests the fiber overbuild cadence is accelerating rather than slowing. This is particularly relevant because Dycom’s work is not merely speculative; it represents field execution and customer awards.

Near-term trading catalyst: negative for cable sentiment around broadband net adds and competitive intensity. The call could reinforce investor concern that cable broadband pressure is not only a macro or housing issue but also a structural fiber-overbuild issue.

Longer-duration fundamental shift: the more important implication is a multi-year erosion of cable’s historical broadband scarcity value in markets receiving fiber overbuild. The effect will likely be gradual, market-specific, and nonlinear, but the call supports the view that the competitive footprint of fiber will continue expanding for several years.

CARRIER FIBER BUILD-OUT IS STRATEGICALLY POSITIVE BUT NEAR-TERM FREE-CASH-FLOW NEGATIVE (READ-THROUGH 5)

Affected companies: AT&T (T: US), Verizon Communications (VZ: US), Lumen Technologies (LUMN: US), and other U.S. fiber-building telecom operators.

Directional impact and magnitude: mixed. Positive, medium for long-term strategic positioning and broadband competitiveness; negative, medium for near-term capex intensity and free cash flow. The net equity impact depends on whether incremental fiber deployment produces sufficient penetration, ARPU, churn improvement, and converged wireless-wireline benefits to offset sustained capital intensity.

Call support: Dycom said customers are extending contract durations “to ensure they have the skilled workforce to meet their goals.” Management also said customers are discussing plans “out through the end of the decade” and that “the skilled workforce is really what’s going to make or break their builds.” For FY2027, Dycom raised Communications revenue guidance to $6.03 billion-$6.20 billion, with the increase “largely fiber-to-home.”

Transmission mechanism: Dycom’s backlog and contract-duration commentary imply that telecom operators are locking in labor capacity for multi-year build programs. That is positive for execution certainty and long-term fiber footprint expansion, but it also signals that carrier capex intensity will remain elevated for longer. Fiber deployment requires upfront cash outlays before penetration, ARPU, and churn benefits are fully realized. The read-through is therefore strategically constructive but near-term cash-flow dilutive.

Near-term trading catalyst: negative for investors focused on near-term free cash flow and dividend coverage if carrier capex expectations move higher or remain elevated longer than modeled. Positive for carriers where investors reward fiber penetration, broadband share gains, and strategic network quality.

Longer-duration fundamental shift: a longer fiber build cycle raises the probability that large U.S. carriers become more structurally competitive in fixed broadband. It also increases the strategic importance of scale, network density, and execution capability. The call supports the view that carriers are not retreating from fiber despite macro and rate pressures.

SPECIALTY CONTRACTORS AND INFRASTRUCTURE SERVICES

SKILLED-LABOR SCARCITY IS SHIFTING VALUE TO SCALED CONTRACTORS WITH MULTI-YEAR CUSTOMER RELATIONSHIPS (READ-THROUGH 6)

Affected companies: Dycom Industries (DY: US), MasTec (MTZ: US), Quanta Services (PWR: US), Primoris Services (PRIM: US), and MYR Group (MYRG: US).

Directional impact and magnitude: positive, large for Dycom; positive, medium for other scaled infrastructure contractors with relevant fiber, power, telecom, utility, and data-center exposure. Negative for smaller, less-capitalized, low-bid contractors that lack labor scale, safety systems, customer relationships, and balance sheet capacity.

Call support: Dycom ended Q1 with record backlog of $11.9 billion, up 25% sequentially, and a 2.2x book-to-bill. Management said customers are extending contract durations to lock skilled workforce, and added: “There are still people out there that are looking for low bid numbers, and that’s just not where we play.” Management also described the skilled workforce as what will “make or break” customer build plans.

Transmission mechanism: when customers commit earlier and for longer durations to secure labor, bargaining power shifts toward contractors that can supply trained crews, safety performance, project management, and national execution. That improves backlog visibility, reduces volume cyclicality, and supports price discipline. The statement that Dycom is passing on low-bid work is important because it indicates demand is strong enough for selectivity, not just volume chasing. The broader implication is that scaled contractors can increasingly monetize labor scarcity through longer awards, better terms, and higher-quality backlog.

Near-term trading catalyst: positive for investor sentiment and estimate revisions across contractors with telecom, power, utility, and data-center exposure. Backlog quality and book-to-bill should receive more attention than reported revenue alone.

Longer-duration fundamental shift: skilled labor is becoming an infrastructure bottleneck and therefore a strategic asset. The companies that have labor density, training infrastructure, fleet, project controls, and customer trust should command better multiples than conventional cyclical contractors. The negative read-through is that companies without scale may be forced into lower-margin subcontracting or excluded from the most attractive multi-year programs.

DATA-CENTER SPECIALTY TRADE PROFIT POOLS ARE EXPANDING INTO HIGH-TEENS MARGINS (READ-THROUGH 7)

Affected companies: EMCOR Group (EME: US), Comfort Systems USA (FIX: US), IES Holdings (IESC: US), MYR Group (MYRG: US), Quanta Services (PWR: US), and Primoris Services (PRIM: US).

Directional impact and magnitude: positive, large for companies with direct data-center electrical, mechanical, and specialty trade exposure; positive, medium for diversified infrastructure contractors with partial exposure. The magnitude is highest for contractors able to deliver mission-critical electrical and mechanical scopes in constrained data-center markets.

Call support: Building Systems generated $395.4 million of revenue and $70.0 million of adjusted EBITDA, or 17.7% margin. Management said Power Solutions is expected to maintain margins in a similar high-teens range for FY2027. Management also said Power Solutions is now expected to more than double its trailing 4- or 5-year revenue CAGR, from approximately 15% to more than 30% growth.

Transmission mechanism: Dycom’s Building Systems results validate the margin pool in data-center electrical construction. High-teens margins at this revenue scale suggest hyperscalers and general contractors are paying for execution capacity, not simply lowest-cost labor. This read-through is directly relevant for EMCOR, Comfort Systems, IES, MYR, and other specialty contractors because their value proposition is similarly tied to complex electrical, mechanical, and mission-critical work. The combination of high growth and high margins suggests demand is exceeding available skilled capacity.

Near-term trading catalyst: positive for the data-center-exposed specialty contractor comp group. Dycom’s results could support higher margin assumptions and stronger backlog conversion expectations for peers with similar exposure.

Longer-duration fundamental shift: the call reinforces that data-center construction is not only an equipment cycle but also a specialty labor and field execution cycle. Contractors with proven execution histories, safety records, and relationships with hyperscalers/general contractors may sustain premium margins longer than a normal construction cycle would suggest. The principal negative risk is execution strain from rapid growth, especially if contractors expand headcount too quickly or accept projects outside core competencies.

DATA CENTER, HYPERSCALERS, AND REAL ESTATE

AI DATA-CENTER CUSTOMERS FACE HIGHER LABOR, SCHEDULE, AND CONSTRUCTION-COST RISK (READ-THROUGH 8)

Affected companies: Meta Platforms (META: US), Microsoft (MSFT: US), Amazon (AMZN: US), Alphabet (GOOGL: US), Oracle (ORCL: US), Digital Realty Trust (DLR: US), and Equinix (EQIX: US).

Directional impact and magnitude: negative, medium near term for hyperscaler free cash flow, capex intensity, and project delivery risk; mixed for data-center REITs, with negative development-cost risk but positive scarcity value for existing capacity and secured powered land. The magnitude is highest for companies with the most aggressive new-build programs and the greatest need for scarce electrical and fiber labor.

Call support: Management said customers are trying to lock in Dycom’s teams “all the way through the end of the decade.” The call also stated that inside-plant electrical and structured cabling trades are “highly coordinated and in high demand.” Management’s comment that the skilled workforce will “make or break” customer builds is the key risk signal.

Transmission mechanism: if hyperscalers and data-center developers must secure labor years in advance, then labor availability is a binding constraint alongside power, land, GPUs, switchgear, and cooling. That can increase construction costs, extend project timelines, force earlier contractual commitments, and reduce customer flexibility. For hyperscalers, this can pressure free cash flow and raise the cost of delivering AI capacity. For data-center REITs, the read-through is nuanced: higher development costs can pressure yields, but scarce powered capacity and proven execution capability can increase the value of existing assets.

Near-term trading catalyst: negative if hyperscaler capex commentary becomes more open-ended or if investors begin to focus more heavily on non-chip bottlenecks. Positive for data-center landlords with existing powered-shell inventory or fully entitled campuses.

Longer-duration fundamental shift: the data-center bottleneck is broadening from semiconductor availability into physical infrastructure delivery. That shift favors companies that already control land, power, interconnection, labor relationships, and construction capacity. It disadvantages marginal developers and late entrants dependent on third-party labor availability in constrained regions.

LOW-VOLTAGE STRUCTURED CABLING IS BECOMING A STRATEGIC SCARCITY ASSET IN DATA CENTERS (READ-THROUGH 9)

Affected companies: Belden (BDC: US), CommScope (COMM: US), Legrand (LR: France), Schneider Electric (SU: France), nVent Electric (NVT: US), and privately held low-voltage engineering contractors.

Directional impact and magnitude: positive, medium for public cabling, connectivity, enclosure, and infrastructure suppliers; positive, large for private low-voltage contractors with data-center exposure; positive for M&A valuation comps in the specialty trade ecosystem.

Call support: Dycom announced an agreement to acquire National Technology Integrators for $275 million. NTI has an initial annual revenue run rate of approximately $175 million, historical adjusted EBITDA margins in the mid-to-high teens, and approximately 2-thirds data-center exposure. Management said NTI specializes in “inside-plant structured cabling, including within data centers, as well as audio visual and security systems.” Management also said the combination allows Dycom to offer infrastructure “starting at the racks and connecting data centers across America.”

Transmission mechanism: the acquisition shows that structured cabling inside data centers is no longer a commoditized afterthought; it is becoming a strategic capability tied to speed, reliability, and complete campus delivery. As data-center density and interconnection complexity rise, demand increases for high-quality structured cabling, fiber management, enclosures, raceway, security systems, and low-voltage engineering. Vendors that supply components into these scopes should benefit from higher project volume, while service providers with trained labor should attract strategic premiums.

Near-term trading catalyst: positive for sentiment around cabling and connectivity names with data-center exposure. The implied NTI valuation also provides a private-market comp that supports the scarcity value of specialized low-voltage capabilities.

Longer-duration fundamental shift: data-center construction is converging across electrical, low-voltage, fiber, and outside-plant infrastructure. The contractors and vendors capable of integrating these layers should gain share, while single-scope or low-bid participants may be structurally disadvantaged. The geographic signal is also important: NTI’s exposure to the DMV, Texas, and the Midwest suggests continued strength in major U.S. data-center corridors.

May 27

$DY (Bloomberg) -- (Updates with stock reaction.)

Dycom Industries shares are up 21% premarket after the firm reported contract revenue for the first quarter that beat the average analyst estimate. Adjusted Ebitda also came in above expectations.

FIRST QUARTER RESULTS

•Contract revenue $1.96 billion, 56% y/y, estimate $1.67 billion (Bloomberg Consensus)

•Adjusted Ebitda $262.5 million, 75% y/y, estimate $209.4 million

•Adjusted EPS $4.42, estimate $2.71

•EPS $3.00 vs. $2.09 y/y

•Adjusted Ebitda margin 13.4% vs. 11.9% y/y, estimate 12.4%

COMMENTARY AND CONTEXT

•Raises FY Fiscal 2027 Outlook

•To Buy National Technology Integrators for $275M

•Sees FY Contract Rev. $7.38B to $7.65B

•Sees 2Q Contract Rev. $1.94B to $2.01B

•Sees 2Q Adj EPS $4.40 to $4.82

•Company entered into a definitive agreement to acquire National Technology Integrators, a tenured and fast-growing low-voltage engineering and construction firm based in Maryland, for total consideration of $275 million

•At closing, the acquired business will be included in the Building Systems segment and is anticipated to have an initial annual revenue run-rate of approximately $175 million

•Outlook exclude results from the pending acquisition of National Technology Integrators

1

10

6,062

May 27

Driving the next wave of India’s digital transformation ☁️⚡

The 10th Smart Datacenters & Cloud Infrastructure Summit 2026 brings together industry leaders, innovators, and policymakers to discuss the future of data centres, AI, cloud, and digital infrastructure-powering growth, resilience, and a stronger digital economy.

📍 Hyderabad

📅 28 May 2026

Register now: assocham.org/event-detail.ph…

For more details, please contact: varun.aggarwal@assocham.com

#SmartDatacentersSummit #CloudInfrastructure #DigitalTransformation #AI

@GoI_MeitY @TelanganaCMO @TGRising2047 @OffDSB @ASSOCHAMSG @TheSridharReddy @sttgdcindia @AdaniOnline @Unomindacom @AxisBank @CommScope @DeltaElectIndia @netwebtech @TyroneSystems @Siemon @sifydotcom @Pi_DATACENTERS @yottainfra @PwC_IN @JSALawIndia @bharath_cloud @PDRVideo @morphingm @uravulabs @VMARCwires @TheOfficialSBI @RESecurity @var_agg24

3

112

May 26

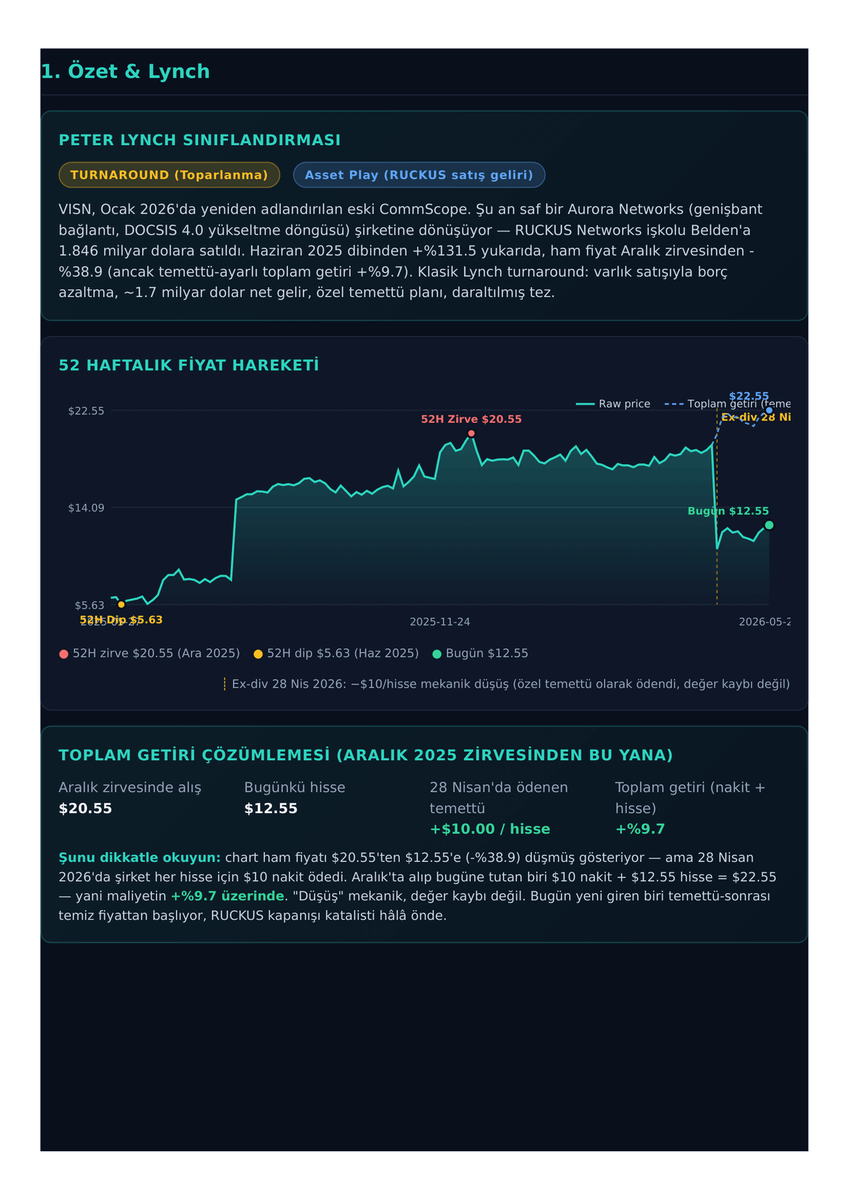

$VISN röntgeni — eski CommScope, yeni adıyla Vistance Networks.

15 Dolar Altında 15 Hisse Serisinin İkinci Hissesi

Fiyat $12.55 · "Zirveden -9 düştü" hikâyesi yanlış. Nisan'da $10/hisse özel temettü ödendi — Şu anki fiyat zirveden sadece %9.7 uzakta.

Analizi oldukça zor bir hisse. Hem olumlu yanları var, hem de riskli.

Lynch: Tam bir TURNAROUND Asset Play.

Youtube'da detaylıca anlattım.

youtu.be/dYKJehAt_AA

$VISN $BDC $CSCO

#fintwit #turnaround #docsis

3

1

15

1,434

May 26

come esempio di questo fenomeno, nel weekend c'era questo (e anche altri) che raccontavano una storia mirabolante su $HLIT Harmonic, l'ho letta e chiesto meglio a Claude che era scettico e non ne ho scritto. Era sui 15 dollari venerdì sera. Ha aperto alle 22 italiane ieri un poco più alto. Stamattina supera 17 dollari nonostante quasi tutte le azioni USA dalle 22 di ieri a stamattina siano più o meno invariate. Ma c'è un gruppo su X come questo sotto che racconta una storia molto convincente e basta quello. Se vedi che pompano un azione piccola funziona

Claude

-----------

Harmonic produce software (la piattaforma cOS) che permette agli operatori via cavo di sostituire le scatole hardware fisiche nelle centrali con software che gira su normali server commerciali. Niente più camion e tecnici per aggiornare migliaia di apparati ogni 3-5 anni: si aggiorna tutto via software.

I numeri reali sono buoni (Q1 2026): ricavi broadband $121,7M ( 43% anno su anno), EPS non-GAAP $0,17 ( 45% sopra le attese), portafoglio ordini $582M ( 87%), margine lordo ~52%, guidance 2026 alzata a $475-495M. Hanno anche venduto la divisione video per $145M e stanno riacquistando azioni proprie ($43M nel solo Q1).

Tutto bello — ma ci sono cinque buchi enormi

Concentrazione clienti drammatica. Comcast da solo è ~39% dei ricavi. Comcast Charter insieme = 67-69%. Non è un "monopolio" alla Microsoft, sono due balene e una lunga coda. Quando Comcast ha rallentato il deployment del DOCSIS 4.0 a inizio 2025, il titolo è crollato del 13% in un giorno. Il post X non nomina mai né Comcast né Charter: è un'omissione gigantesca.

Il grafico a lungo termine è devastante. Massimo storico: $152 nel marzo 2000. Oggi: ~$15. Negli ultimi 5 anni HLIT ha reso 26% totale (~4,75% annuo) contro l'S&P 500 a 84%. Non è un titolo "in attesa di esplodere": è un titolo che ha ripetutamente bruciato gli investitori per oltre due decenni. Ogni qualche anno parte un ciclo di upgrade via cavo, il titolo si gonfia, poi delude quando i deployment slittano. Schema ben noto.

Il "monopolio per costi di switching" è esagerato. Gli operatori via cavo sono compratori sofisticati da miliardi di dollari, che apposta usano più fornitori per evitare il lock-in. Charter, dopo anni di "front-runner", non si è ancora impegnata pienamente su cOS. Esistono concorrenti (Cisco, CommScope/Arris, Casa Systems). Harmonic è abbastanza sola nel virtual CCAP non perché abbia un monopolio, ma perché la nicchia era troppo piccola per attirare i grandi. Sono due cose molto diverse.

Il mercato di riferimento si sta restringendo, non allargando. Negli USA gli abbonati via cavo calano da un decennio (cord-cutting). Gli operatori si spostano sul solo broadband, ma il bacino globale di operatori cavo coassiale non cresce — si consolida. L'idea che "tutti gli ISP del mondo si convertiranno" è una fantasia: gli operatori in fibra pura (FTTH) spesso non hanno proprio bisogno della tecnologia DOCSIS.

Non è ancora davvero un'azienda software. Margine lordo del 52% è discreto, ma molto sotto un vero SaaS (70-80%). L'utile netto è volatile, hanno avuto trimestri in perdita. Fatturato annuo $360M. Si stanno muovendo verso ricavi ricorrenti di tipo software, ma non ci sono ancora.

E poi la valutazione non è più a sconto. Forward P/E ~20x, capitalizzazione $1,4 miliardi su $360M di ricavi. Dopo il 67% in 12 mesi, stai pagando per la crescita futura, non te la portano a casa gratis. Il modello GuruFocus stima il fair value a ~$9,50 (titolo sopravvalutato del ~33%).

Conclusione pratica

Il post X è il classico pitch da Twitter: prendi una storia fondamentalmente solida, la travesti da "monopolio ovvio che nessuno vede", ometti le parti scomode (concentrazione Comcast, 25 anni di delusioni, mercato in contrazione), e chiudi con "DYOR not financial advice". La frase "tra cinque anni guarderemo indietro e ci chiederemo come non sia stato ovvio" è il segnale tipico: è narrativa di vendita, non analisi.

Detto questo, HLIT sta avendo un momento genuinamente positivo. Se Charter alla fine si impegna su cOS, se il "rest-of-market" continua a 70%, e se la cessione della divisione video pulisce il bilancio, può continuare a funzionare ancora un po'.

Come inquadrarlo onestamente: trattalo come una mid-cap ciclica che cavalca l'onda del deployment DOCSIS 4.0, non come un "monopolio software". Se vuoi esposizione, dimensiona la posizione di conseguenza (è volatile e molto sensibile alle trimestrali). I veri catalizzatori da monitorare sono i commenti sul capex di Comcast e Charter, molto più della narrativa cOS. E ricordati che i soldi facili su questa corsa potrebbero già essere stati fatti.

May 22

Opened a long position in $HLIT today. This is the most interesting monopoly setup I have seen in a long time.

Every cable and internet provider in the world has the same problem.

Physical hardware. Cable access boxes sitting in facilities and in homes. Each node costs thousands of dollars to deploy.

Every 3 to 5 years that hardware becomes obsolete and has to be physically replaced. Trucks rolled. Technicians dispatched. Hardware swapped. Over and over forever. The capex never stops.

For a large cable operator running millions of nodes that is a multi billion dollar recurring cost that never goes away.

$HLIT built the solution and it is so obviously better that I genuinely do not see how this does not become the standard for the entire industry.

Their cOS platform virtualizes the entire cable access network in software. The operator buys the platform once and runs it on standard off the shelf cloud hardware. No proprietary boxes. No truck rolls for upgrades. No hardware replacement cycles.

Capacity scales with a software update.

New features deploy remotely overnight. Maintenance becomes a predictable annual subscription instead of a massive unpredictable capital expenditure.

The economics for every operator on earth are impossible to argue with.

Buy expensive hardware every 3 to 5 years forever. Or buy software once and pay a fraction of that in annual maintenance.

The answer is obvious. Every operator that runs the numbers converts. And once they convert they never leave because ripping out the software layer running your entire broadband network is not something any sane operator does.

That is the monopoly. Not a monopoly imposed by regulation. A monopoly created by switching costs so high that once you are in the ecosystem you are in permanently.

And the market they are going after is enormous. Every cable operator. Every internet service provider. Every telecom running broadband infrastructure globally. All of them facing the same hardware problem. All of them needing the same solution.

The numbers are already showing the conversion is happening.

Q1 2026 broadband revenue up 43% year over year. Beat guidance by nearly 20%. Operating profit up 115% year over year. 150 customers already on the platform serving 45.7 million cable modems.

Rest of market bookings up 78% meaning this is expanding well beyond the initial tier one deployments.

Backlog and deferred revenue sitting at $582 million up 87% year over year. Full year 2026 guidance raised to $475 to $495 million. Gross margins at 52% and expanding as the software mix grows.

They just sold the video business for $145 million. Pure play broadband software company. One focus. Clean balance sheet.

Now think about the ceiling.

There are hundreds of cable and broadband operators globally who have not yet converted. Every single one of them is a future customer.

The platform is cheaper. The economics are better. The switching costs lock them in permanently. There is no logical reason for any operator to choose hardware over this.

If $HLIT captures even half the global broadband infrastructure market the revenue numbers look nothing like what they do today.

52% gross margins on a sticky recurring software business with a massive untapped global market and switching costs that make churn nearly impossible.

This is one of those setups that in five years people will look back on and ask why it was not more obvious.

Long $HLIT. Not financial advice. DYOR.

2

3

9

2,168

May 26

$APH is my favorite “Picks & Shovels” compounder in the entire AI data center value chain.

Secular Trend: Main thesis here is AI CAPEX spending on data centers plays out according to Jensen Huang during the recent $NVDA earnings call ($1 trillion by 2027; $3-4 trillion by 2030). This also means the AI infra buildout will last longer than most people expect. And $APH outgrows the industry as it is a moaty compounder that has pricing power.

What they do in 1 sentence:

They sell electronic components that transmit power for data centers under various stressful environments. (Products include interconnect systems, sensors, and specialty cables)

The business is so stable that they were known for being the “consumer staples” within the industry.

A few green flags I like about APH that screams moaty compounder:

- Hyper decentralized structure with over 130 autonomous business units.

- Smart segment/product mix: APH has 3 business segments all with good growth profile and margins.

Think of a split between: AI data centers/military aerospace/automotive, medical, and others - I like diversification here as APH will act less like a monolithic tech manufacturer and more like a compounder.

Product strategy wise, they avoid commoditized consumer products and focus on high mix & low volume. This means they dominate in specialized markets - if you are an AI data center, APH has you covered with the specific type of cable you need. A cable is cheap to a data center but will cause a big damage if it fails - this is APH’s moat because data centers will buy from them and won’t switch.

They have pricing power because of this.

- High switching cost: another main thesis for APH. APH doesn’t just sell parts, they work with customers on the power delivery infrastructure for 2-3 years before product even launches.

- Growth profile: perfect mix of organic growth (a third of historic growth) and M&A growth (two thirds). Their M&A playbook has not only been accretive (ROIC goes up over time), but also helped them scale cost down (they get raw materials such as copper and precious metals for plating cheaper than anyone else).

- Capital light business: CAPEX is 3-4% of sales. This is a business that grows without needing much additional investments.

Fundamentals:

They are a 162 billion market cap company making around 26 billion in topline (TTM) and makes free cashflow of 831 million.

2025 growth was incredible: 51.7% topline growth / 86% operating income growth / 43% FCF growth.

Segment mix was split between Communications / Harsh Environment Solutions / Interconnect & Sensors, with revenue of roughly $12B / $6B / $5B respectively. Communications makes up nearly half of total revenue and grew an impressive 91% in 2025, which basically reflects the AI data center spending boom. Operating margins across the three segments are also strong at around 20–30%.

Recent Q1 2026 results showed even higher growth numbers.

Fundamentals speak for themselves here. And I align my thoughts with Jensen Huang - AI infra build out phase 2 is underway and I will gladly chill on this stock.

Price action and Valuation:

Price has come down quite a bit and the stock is down ~2% YTD but still almost doubled since January 2025.

Recent weakness came from CommScope CCS post acquisition margin pressure. Historically APH recovers margins within 12–18 months post acquisition so this is temporary.

Valuation isn’t cheap - good compounders rarely are and if you don’t buy them at a reasonable price, you never will own them. Forward PE of 26x isn’t cheap, but it’s where I call reasonable. And you factor in forward PEG of 1x, which is reasonable.

Chart reads ok too, bounced off the $120 support area for both daily and weekly time frame. I’m ok adding more here.

1

5

1,509

May 25

$HLIT Şirketinde önemli bir yapısal dönüşüm ve karlılık artışı sebebiyle detaylı bir analiz sunuyorum.

-Önceki İş Kolu : Video (Yayıncılık ve Medya) Televizyon kanalları, yayın platformları ve medya şirketleri için video sıkıştırma , prodüksiyon ve geleneksel yayıncılık donanımları üretiyordu.

-Bu iş kolunu bırakma sebebi : Bu sektörün büyüme hızı yavaştı, kâr marjları düşüktü ve yüksek sermaye yatırımı gerektiriyordu. Şirket bu bölümü 150 milyon dolara MediaKind firmasına satarak tamamen elinden çıkardı.

Geçiş Yaptığı İş Kolu : Geniş Bant (Broadband

Altyapısı)

-Ne Yapıyor : İnternet servis sağlayıcıları ve telekom operatörleri için yüksek hızlı internet altyapı çözümleri sunuyor.

-Öne Çıkan Ürünü : COS adlı bulut tabanlı yazılım platformu. Operatörler, mahallelerdeki internet kutularını devasa donanımlarla yönetmek yerine, Harmonic'in bu bulut yazılımıyla internet hızını ve trafiğini uzaktan dijital olarak yönetiyor.

-Neden Bu Alana Geçti : Dünya genelinde evlere fiber çekilmesi ve internet hızlarının (DOCSIS 4.0 standartlarına) yükseltilmesi nedeniyle bu alanda devasa bir küresel talep patlaması yaşanmaktadır. Brüt kâr marjları çok daha yüksektir.

-Video segmentinin Satışından gelecek 150 milyon dolarlık nakit girdisi, şirketin borçsuz finansal yapısını (Borç/Özkaynak 1.4) daha da güçlendirecektir. Harmonic bu nakit gücünü, 1. çeyrekte başlattığı 43 milyon dolarlık (4.2 milyon adet hisse) geri alım programını agresifleştirmek ve yapay zeka destekli ağ yazılımları geliştirmek amacıyla Ar-Ge yatırımlarında kullanmayı planlamaktadır.

SEKTÖREL ÇARPANLAR VE REKABET ANALİZİ

-HLIT, ağ altyapı sektöründe büyük ölçekli devlerle rekabet ederken, saf bir geniş bant ve yazılım odaklı (Pure-play Broadband/SAAS) yapıya bürünerek çarpan bazında ayrışmaktadır.

-Büyüme Primi: HLIT, geleneksel donanım üreticilerine (CommScope vb.) kıyasla, sanallaştırılmış COS bulut yazılım platformu sayesinde çok daha yüksek çarpanları hak eden bir teknoloji şirketi gibi fiyatlanmaktadır.

-Esneklik Avantajı: Cisco gibi dev pazar oyuncularına karşı en büyük avantajı, sadece operatörlerin yeni nesil altyapı (DOCSIS 4.0 ve Fiber) dönüşümlerine odaklanmış olması ve hantal bir organizasyon yapısının bulunmamasıdır.

DERİNLEMESİNE RİSK ANALİZİ

-Tedarik Zincirindeki "Çip ve Hafıza" Engeli: Küresel çapta CPU, PCB ve üçüncü taraf sunucu (server) tedariğinde sıkışıklık sürmektedir. Yönetim, yılın ikinci yarısında artan bellek (memory) maliyetlerinin net marjlara 6 milyon dolar olumsuz etki yapacağını öngörmüştür. Siparişler teslim edilemediği sürece ciroya dönüşememektedir.

-Gelecek Öngörülerinde Muhafazakarlık (Düz Çeyreklik Görünüm): 2026 ilk çeyreğindeki patlamaya rağmen, tam yıl revize edilen kılavuz (475M - 495M $) incelendiğinde, kalan çeyreklerde ardışık (sequential) bir büyüme beklenmediği görülmektedir. Şirket, her çeyrek için ortalama 122 milyon dolarlık sabit bir seyir öngörmektedir; bu da yönetimin makro belirsizlikler nedeniyle temkinli kalmayı seçtiğini gösterir.

-Müşteri Yoğunlaşmasının Coğrafi Yapısı: Cironun X'ini oluşturan iki dev operatöre (başta Comcast) bağımlılığı kırmak adına Rest-of-Market (Diğer Pazarlar) segmenti x büyümüştür. Ancak Avrupa ve Latin Amerika operasyonlarındaki yeni kazanımlar (DNA Finland, Inter Venezuela vb.) beraberinde döviz kuru riski ve yerel tarife yükleri getirmektedir (Yıllık tarife maliyetinin 2.3 milyon dolar olması beklenmektedir)

SONUÇ VE STRATEJİK YATIRIM GÖRÜNÜMÜ

-Harmonic (HLIT), 15.20 civarındaki mevcut fiyatıyla analistlerin 17-20 $ arasındaki hedef fiyatlarına göre ile 1 arasında bir iskonto (adil değer altında) sunmaktadır. Video biriminin satışından gelecek nakit operasyonları temizleyecek, sipariş birikimi (Backlog) ise sonraki dönemlerin gelir güvenliğini sağlayacaktır. Ancak, yılın ikinci yarısındaki bellek maliyet artışları ve muhafazakar gelecek beklentisi, hissede dönemsel kar satışları veya yatay bant hareketleri yaratabilir.

-Başarılı bilanço ve stratejik dönüşümün hızlı ve emin adımlarla gerçekleşmesi ve talep alanının yoğun ve güçlü olması hisseyi daha agresif fiyatlara taşıyabilir.

TEKNİK GÖRÜNÜM

-Hisse fiyatının bu sonuçlarla boşluk bırakarak bir atak yaptığı görülüyor. Yükselişin devamını bekliyorum. Fakat yatırım yaparken stratejinin uzun vadeli olması ve kademeli alımın yapılması önem taşımaktadır. Yatırıma değer olarak görüyorum.

NOT: Yatırım Tavsiyesi Değildir.

5

1,152