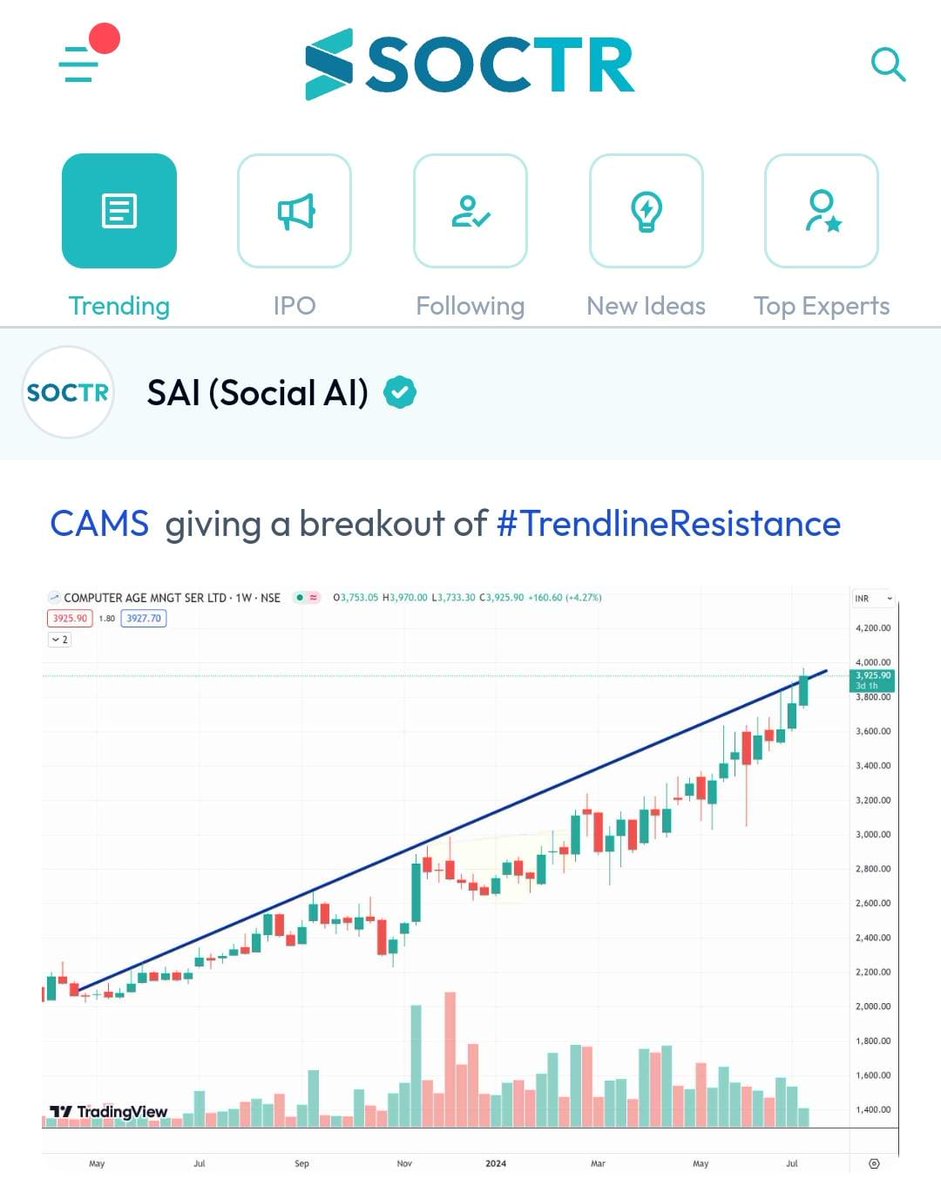

#CAMS #Charts

Check Latest #Chartpatterns on my.soctr.in/x & "follow" @MySoctr

#Nifty #Nifty50 #Investing #Breakoutstocks #StocksInFocus #StocksToWatch #Stocks #StocksToBuy #StocksToTrade #Breakoutstock #Stockmarketindia #StockMarket #Trading #StockMarkets #Breakout #Nse #Stockideas #BO #Sensex #Resistance #Volume #Trendline #Support #TrendlineResistance #TrendlineSupport #HorizontolResistance #chart #HnS #Triangle #CnH #Profit #Gain #return #ComputerAgeManagementServicesLtd #CAMSLtd #CAMSlimited #computeragemanagementserviceslimited #Pennantpattern

1

1

4

479

5 Nov 2024

#CAMS #ComputerAgeManagementServicesLtd #Concall #Insights #Q2FY25 #AISummary

**Growth & Revenue**

- Overall revenue grew 32.7% with MF revenue slightly ahead of non-MF.

- MF revenue grew 32.9% and non-MF revenue grew just short of 32%.

- Fastest quarterly AUM growth with an addition of almost INR 5 lakh crores in a quarter, reaching close to INR 45 lakh crores.

- Active equity asset growth of nearly 59.4%, exceeding the industry growth of 53.5%.

- Achieved 66% of industry net sales, amounting to over INR 1 lakh crore.

**PAT, EBITDA & Margins**

- Absolute EBITDA grew by almost 40%.

- EBITDA margin increased by 240 basis points year-on-year to nearly 47%.

- PAT grew by 44.9% and PAT margin increased by 270 basis points.

- Board approved an interim dividend of INR 25 per share (INR 14.5 as per the 65% payout policy and INR 10.5 as a special interim dividend).

**Alternatives Business**

- 21% year-on-year revenue growth in alternatives business.

- Highest number of quarterly wins with 57 new mandates.

- Opened a second office in GIFT City.

**KRA Business**

- 56% year-on-year revenue growth in KRA business.

- Added 26 new fintechs, platforms, and similar companies to the client roster.

- Launched Nexus, a KRA dashboard, and WhatsApp KYC.

**Insurance Business (Wrap)**

- Added SBI General and ICICI Prudential as integrated insurers on Bima Central.

- Processed 1 lakh service transactions on Bima Central.

- Doubled e-insurance policy conversions to nearly 10 lakhs in Q2 from 5 lakhs per quarter in FY24.

**CAMSPay**

- 69% year-on-year revenue growth in CAMSPay.

- Significant product enhancements and 23 new logos added in Q2.

- LIC empaneled CAMSPay for payment gateway services.

**FinServ**

- Maintained 16.5% market share.

- Achieved around 170% year-on-year revenue growth (on a small base).

- Crossed 1 lakh touch points per month on the Amaze platform.

**Think Business**

- Algo360 secured mandates from LTFS and Stable Money, with go-live expected by December-January.

- Experiencing some cannibalization from account aggregator impacting Algo360 revenue.

- Some US analytics contracts ended, contributing to revenue decline in Think360.

**NPS**

- Crossed 1 lakh CRA accounts, primarily from retail and private sector employers.

- Onboarded Indian Bank as a POP.

- Continue to focus on scaling the NPS business.

**Costs and Margins Outlook**

- Employee costs grew by around 20% year-on-year.

- Expecting operating expenses to be around 8% to 8.5% of overall revenue.

- Other expenses are stabilizing around INR 25 crores to INR 30 crores per quarter.

- Aiming for an EBITDA margin of around 47.5% by the end of the year.

**Key Risks/Challenges**

- Competition in the AIF/PMS segment leading to price pressure.

- Potential impact of RBI's unified lending interface on the account aggregator business.

- Dependence on the capital markets cycle, particularly for MF-related revenue.

- Need to scale insurance business to become a meaningful revenue contributor.

- Cannibalization of Algo360 revenue by account aggregator.

Join the waitlist at compoundingai.in

1

5

457

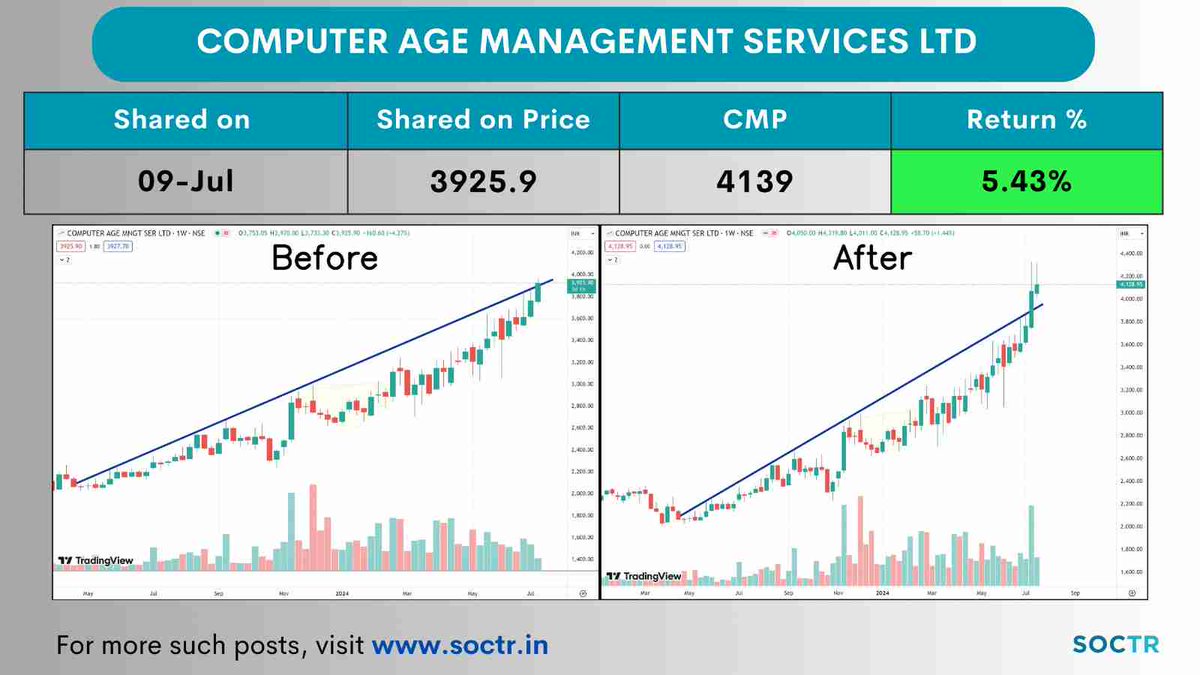

#CAMS 5.43% Return in 10 Days

Check #trending #chartpatterns on my.soctr.in/x & "follow" @MySoctr

#nifty #nifty50 #investing #breakoutstocks #StocksInFocus #StocksToWatch #stocks #StocksToBuy #StocksToTrade #breakoutstock #stockmarketindia #StockMarket #trading #stockmarkets #Breakout #nse #stockideas #BO #sensex #Resistance #Volume #Trendline #Support #TrendlineResistance #TrendlineSupport #HorizontalResistance #HnS #Triangle #CnH #CAMSLtd #chart #Profit #Gain #ComputerAgeManagementServicesLtd #ComputerAge

2

194

#CAMS #Charts

Check Latest #Chartpatterns on my.soctr.in/x & "follow" @MySoctr

#Nifty #Nifty50 #Investing #Breakoutstocks #StocksInFocus #StocksToWatch #Stocks #StocksToBuy #StocksToTrade #Breakoutstock #Stockmarketindia #StockMarket #Trading #StockMarkets #Breakout #Nse #Stockideas #BO #Sensex #Resistance #Volume #Trendline #Support #TrendlineResistance #TrendlineSupport #HorizontolResistance #chart #HnS #Triangle #CnH #Profit #Gain #return #ComputerAgeManagementServicesLtd #CAMSLtd #CAMSlimited #computeragemanagementserviceslimited #Pennantpattern

2

327