May 13

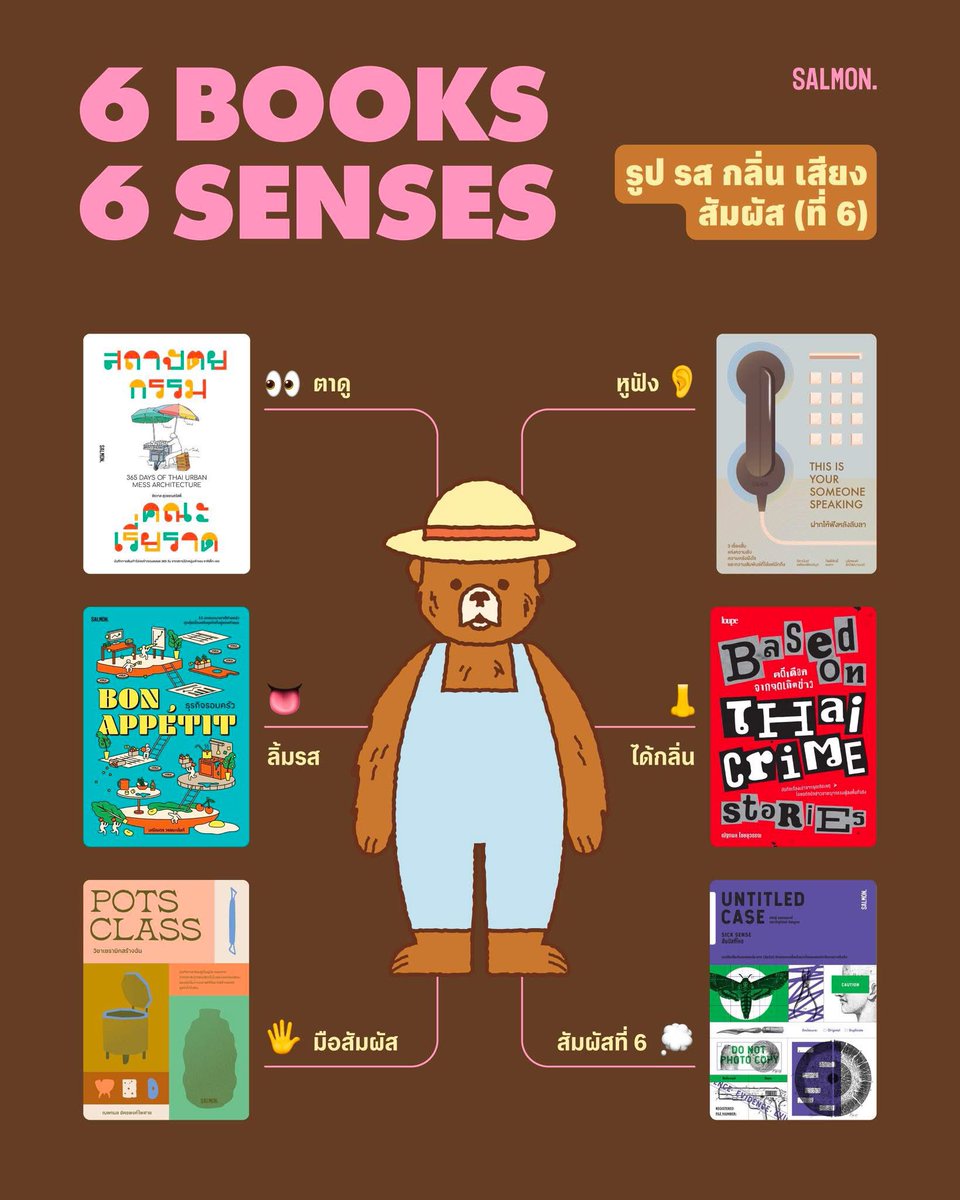

ก๊อกๆๆๆ นักอ่านทุกคน ใครกำลังคิดไม่ตกว่าช่วงนี้อ่านอะไรดี เรามีตัวช่วยยยย 🤩

.

วันนี้เราขอแนะนำหนังสือแบบใหม่แบบสับ แบบครบจบใน 6 ประสาทสัมผัส ใครอยากเลือกหนังสืออ่านตามรูป รส กลิ่น เสียง สัมผัส และสัมผัสที่ 6 อ่านต่อข้างล่างได้เลยนะ

.

👀 ตาดู

เริ่มด้วยการใช้สายตาสังเกตสิ่งละอันพันละน้อยที่เกิดขึ้นเรี่ยราดตามรายทางไปกับ ‘365 DAYS OF THAI URBAN MESS ARCHITECTURE สถาปัตยกรรมคณะเรี่ยราด’ บันทึกภาพสเกตช์และเรื่องราวสั้นๆ ถึงข้าวของที่คนไทยดีไอวายเพื่อแก้ปัญหาที่เกิดขึ้นในชีวิต เช่น การเอาไม้ไผ่ใกล้ตัวมาต่อเป็นราวตากผ้า การใช้ท่อพีวีซีมาอุดรอยรั่วทุกปัญหา และอีกมากมายสารพัดที่อ่านจบแล้วต้องอุทานออกมาว่า ‘นี่แหละ Thailand Only’

salmonbooks.net/product/365-…

👂🏻 หูฟัง

ชวนทุกคนหันมาฟังเสียงในความทรงจำของตัวเอง เพราะอาจมีบางเสียงที่ยังคงคั่งค้างอยู่ในใจ เหมือนกับเสียงในเรื่อง ‘THIS IS YOUR SOMEONE SPEAKING ฝากให้ฟังหลับลับลา’ สามเรื่องสั้นขนาดกะทัดรัด แต่อัดแน่นไปด้วยความรู้สึก ผลงานจาก ‘จิดานันท์ เหลืองเพียรสมุท’ ‘กิตติศักดิ์ คงคา’ และ ‘นริศพงศ์ รักวัฒนานนท์’

salmonbooks.net/product/spea…

👅 ลิ้มรส

เล่มนี้อ่านแล้วหิวแน่! เพราะ ‘BON APPÉTIT ธุรกิจรอบครัว’ จะพาคุณไปลิ้มรสชาติ 15 แบรนด์ธุรกิจอาหารผ่านตัวหนังสือ เจาะลึกตั้งแต่ช่วงเวลาล้มลุกคลุกคลานไปจนถึงวันที่ประสบความสำเร็จ ไม่ว่าจะเป็น ‘Mo-Mo-Paradise’ ชาบูคู่ใจของคนรักเนื้อ, ‘Molto Premium Gelato’ แบรนด์ไอศครีมเจลาโตรสชาติไม่เหมือนใคร และอีกหลากหลายร้านที่คุณอาจเคยได้ยินชื่ออยู่บ่อยๆ

salmonbooks.net/product/bon/

👃🏻 ได้กลิ่น

ได้กลิ่นตุๆ เหมือนมีเงื่อนงำอะไรบางอย่าง! หากอยากรู้ว่าเบื้องลึกเบื้องหลังของคดีอาชญากรรมไทยเป็นอย่างไร ชวนมาหาคำตอบกันใน ‘BASED ON THAI CRIME STORIES คดีเดือดจากจุดเกิดข่าว’ หนังสือแนว True Crime ที่บันทึกเรื่องราวและบรรยากาศรายล้อมที่ไม่อยู่ในข่าว พร้อมกับพาไปดูการทำงานสืบสวนของเจ้าหน้าที่ตำรวจ และการลงพื้นที่หาข้อมูลของนักข่าวอาชญากรรม

salmonbooks.net/product/thai…

🖐🏻 มือสัมผัส

มาต่อกันที่ ‘การสัมผัส’ เพราะ ‘POTS CLASS วิชาเซรามิกสร้างฉัน’ จะพาทุกคนไปรู้จักวิธีการปั้นทั้งเซรามิกและธุรกิจให้เป็นรูปเป็นร่าง! บันทึกเรื่องราวโดย ‘ณพกมล อัครพงศ์ไพศาล’ เปิดเผยตั้งแต่วันแรกที่เธอเริ่มปั้น วันที่เธอได้ก่อตั้ง LMLM. Craftstudio จนถึงช่วงออกไปค้นหาคำตอบของการทำธุรกิจสร้างสรรค์นอกห้องเรียน

salmonbooks.net/product/pots…

🔮 สัมผัสที่ 6

ปิดท้ายสำหรับคนชอบเรื่องลี้ลับด้วยหนังสือที่รวบรวมเรื่องลับลึกที่เชื่อมโยงกับประสาทสัมผัสทั้ง 5 (และสัมผัสที่ 6) ใน ‘UNTITLED CASE: SICK SENSE สัมผัสที่โหด’ ตั้งแต่เรื่องราวของศพหญิงสาวปริศนาที่ผู้เห็นเหตุการณ์ต่างมองภาพเธอแตกต่างกันออกไป ชายผู้ลิ้มรสซากศพและเลือดมนุษย์เป็นอาหารจานโปรด และอีกหลายเรื่องราวกระตุกประสาทสัมผัส ถ่ายทอดโดย ‘ยชญ์ บรรพพงศ์’ และ ‘ธัญวัฒน์ อิพภูดม’ โฮสต์พอดแคสต์รายการ Untitled Case

salmonbooks.net/product/uc3/

#Salmonbooks

3

7

1,080

Apr 17

Every day we're going to tear down a major Indian listed company and map the AI risk/opportunity around it - products, competitive shifts, key concall quotes.

Day 5: LTIMindtree (LTM)

Peak share price: ₹7,332 (Dec 2021)

Current share price: ₹4,742 (-35.3%)

EV today: ₹1,33,726 crore

Revenue(FY25): ₹38,008 crore ( 7.0% YoY)

EBITDA Margin: 16.8%

EV/Sales: 3.52x

Headcount: 87,958 ( 1.3% YoY)

What LTIMindtree does:

LTIMindtree is a global technology consulting and digital solutions company serving 700 clients across BFSI, Manufacturing, and Technology verticals. As an L&T subsidiary, it operates as a strategic transformation partner with deep hyperscaler alliances across AWS, Microsoft, and Google Cloud.

Its core differentiator is the BlueVerse AI orchestration ecosystem and a joint venture with Aramco Digital - NextEra, to localize IT services in Saudi Arabia. Rated IND AAA/Stable and CRISIL AAA/Stable, it is among the most creditworthy mid-to-large IT names on the street.

AI bear case:

The disruption mechanism here is unusually direct - management has explicitly acknowledged that approximately 60% of revenues come from sectors where growth is flat because top clients are recalibrating spend based on AI productivity benefits they have already received. This breaks the headcount-to-revenue link in real time, not as a future risk.

The top 5 client bucket has already tapered as clients enter a post-productivity recalibration era. Net profit margins have declined from 13.3% in FY23 to 12.1% in FY25 - the cost of building AI capabilities and absorbing price pass-backs is showing up in the P&L simultaneously. LTIMindtree is not anticipating this pressure. It is inside it.

AI bull case:

The pivot is toward non-linear, high-complexity mandates that man-hour billing cannot price anyway. The clearest evidence: a ₹3,000 crore, 7-year Insight 2.0 contract from the Central Board of Direct Taxes using AI-powered analytics to modernize national tax infrastructure. This is a revenue surface that has nothing to do with legacy outsourcing.

BlueVerse now carries 1,000 ready-to-deploy AI agents embedded into the delivery framework. A $155 million, five-year strategic partnership with a US insurance firm for AI-led delivery was signed in Q3 FY26. Hyperscaler collaboration agreements across all three majors create a distribution advantage for GenAI solutions in underwriter automation and fraud prevention - specialized enough that pure-play competitors cannot easily replicate the stack.

AI traction:

Over 50% of employees achieved intermediate or advanced AI skills in Q3 FY26. 40-50 accounts adopted AI during the same quarter. BlueVerse CraftStudio launched for AI-driven marketing. Internal deployment at a financial institution delivered 80% reduction in time for writing complex logic.

The CBDT Insight 2.0 contract and the US insurance partnership are the two largest disclosed AI-attributed deal wins. AI traction is real - the question is conversion speed from pilot to production at scale.

Competitive landscape:

TCS, Infosys, and Accenture all operate in the same large-deal consolidation space with significantly larger balance sheets and disclosed AI revenue numbers. TCS is running a $2.3 billion annualized AI revenue base; LTIMindtree has not isolated a comparable figure in filings.

The differentiation play is agility and BlueVerse orchestration depth over scale. Utilization at 86.9% and offshore effort mix at 85.5% are operationally strong but do not insulate against billing rate compression if the recalibration cycle extends beyond two quarters.

Management quotes:

"AI productivity is not a magic wand, right? So we need to redefine the processes. We need to get the right tools in place, right platforms in place, get the team to identify opportunities which can be coded." - Q3 FY26 Concall

"It is a first year of a productivity journey, as I call it. But I am more hopeful of that category of accounts actually with puts and takes to continue to deliver growth, because we have a good pipeline as well." - Q3 FY26 Concall

"Q2 FY26 has been a strong quarter for us, marked by broad-based performance across our business... We are committed to becoming an AI-centric organization, leveraging our BlueVerse ecosystem." - Q2 FY26 Concall

Commentary:

LTIMindtree is in the eye of the productivity storm - AI is a net headwind in the immediate 12-month window as top-tier clients demand price recalibrations that are already compressing the top line. Over a 3-year horizon, the thesis flips: the company is replacing lower-margin legacy work with large, long-duration digital architecture contracts where AI is the delivery mechanism, not the threat.

The CBDT win is the proof point - government-scale mandates at ₹3,000 crore over 7 years do not go to bid on man-hour rates. The unresolved question is whether margin expansion from the New Horizons program can outpace billing rate compression in legacy BFSI and Tech portfolios.

In the next two concalls, watch the top 5 client growth trajectory and conversion rate of AI pilots into Agentic AI production deals, those two signals confirm whether the recalibration phase has bottomed or has another leg down.

Analysis by CompoundingAI

Source : All figures sourced to BSE filings and Q3 FY26 earnings transcripts.

Note : No Buy/Sell Reco.

Apr 16

Every day we're going to tear down a major Indian listed company and map the AI risk/opportunity around it - products, competitive shifts, key concall quotes.

Day 4: Infosys (INFY)

Peak share price: ₹1,999.70 (Dec 2024)

Current share price: ₹1,320.90 (-34.0%)

EV today: ₹4,89,217 crore

Revenue Q3 FY26: ₹45,479 crore ( 9% YoY)

Operating Margin: 21.2% (adjusted for labour code charges)

EV/EBITDA: 11.57x

Headcount: 3,37,000 ( 4.3% YoY)

What Infosys does:

Infosys manages the critical systems and digital transformation of 1,882 active enterprises across 50 countries, with 27% revenue concentration in BFSI and a 96.9% export revenue profile.

Its Global Delivery Model deploys 3,37,000 professionals across application development, cloud migration via Infosys Cobalt, and AI transformation through its Topaz suite. As India's second-largest listed IT company, it is the default navigator for global corporations modernizing legacy stacks at scale - not just advising on transformation but executing it.

AI bear case:

The primary threat is disruption of the "pyramid" labor structure - junior-level coding, testing, and maintenance are high-volume, low-complexity, and directly in the automation crosshairs. GenAI enables clients to automate these workflows or shift them to captive Global Capability Centers in India, compressing volume in the core cost-of-effort segment that drives 55.4% of revenue.

Management has acknowledged that AI productivity gains are frequently shared with clients, creating deflationary contract pricing that requires constant new scope to hold the top line. The labour code charges - ₹1,300 crore impact in Q3 FY26 alone - confirm that the cost of maintaining a specialized human talent pool remains high even as billable hours for entry-level work decline. Attrition at 14.3% adds further cost volatility to an already pressured margin structure.

AI bull case:

Infosys has delivered over 400 GenAI projects and carries 4,600 active AI engagements in pipeline - including 500 purpose-built agents for multi-step business process execution. The Topaz Fabric composable stack includes 50 purpose-built agents for IT operations and 20 managed connector platforms for enterprise data.

Proprietary small language models for banking and cybersecurity reinforce the moat as an enterprise-grade integrator for the 90% of its top 200 clients already engaged in AI work. The $1.6 billion NHS contract is the clearest evidence that Infosys can embed AI into massive, long-term operational modernization programs where hyperscalers cannot simply walk in and displace the incumbent. Distribution advantage is real.

AI traction:

4,600 active AI projects in Q3 FY26, up from 2,500 GenAI and 200 agentic AI projects just one quarter prior - the acceleration is disclosed, not extrapolated. Topaz Fabric launched with Cognition's Devin software agents integrated and deep co-innovation with Intel on Gaudi AI accelerators.

2,70,000 employees now AI-aware; 10% of top technology talent engaged in highly innovative AI solution building. Specific AI-attributed revenue is not yet isolated in filings - the one disclosure gap that matters most for the investment thesis.

Competitive landscape:

TCS has already disclosed annualized AI services revenue exceeding $2.3 billion - a concrete benchmark Infosys has not yet matched with a comparable disclosed number. Accenture and Capgemini are executing the same agentic AI pivot globally with larger consulting revenue bases.

The structural threat from client-owned GCCs in India is accelerating independently of any competitor move - this is demand destruction that no IT major can outrun through better sales execution alone. The race to agentic frameworks is now table stakes across the sector.

Management quotes:

"So, what we have built within Topaz is fabric, Topaz Fabric, as we call it, is a set of purpose-built agents, which work with many different native AI companies interfaces and can support a lot of different functions within clients, horizontal and vertical." - Q3 FY26 Concall

"If you are delivering better productivity, you would be able to keep some of that with you, which will get reflected in better pricing." - Q3 FY26 Concall

"So on the headcount increase, I think it demonstrates that we have confidence in where the market is and what we are seeing in terms of the demand." - Q3 FY26 Concall

Commentary:

The ₹1,300 crore labour code hit distorted Q3 FY26 optics - the underlying story is 9% rupee revenue growth and a 21.2% adjusted margin holding firm. Infosys is defending territory effectively during a period of massive architectural upheaval.

AI is a net tailwind over a 3-year horizon because orchestrating thousands of agents across fragmented legacy enterprise landscapes at the scale of 1,882 active clients is exactly what a large incumbent does and what an AI-native startup cannot.

The unresolved question is whether the "sharing" of productivity gains triggers a race to the bottom in standard digital services contract values - that is the deflationary trap hiding inside every renewal.

In the next two concalls, watch utilization rates and net additions to the "AI masters" talent tier. If the 20,000 fresher hiring target is replacing automated roles rather than generating new revenue, the pyramid model is already hollowing out faster than Topaz Fabric can fill it.

Analysis by CompoundingAI

Source : All figures sourced to BSE filings and Q3 FY26 earnings transcripts

Note : No Buy/Sell Reco. Only for educational purposes.

1

6

1,820

Feb 20

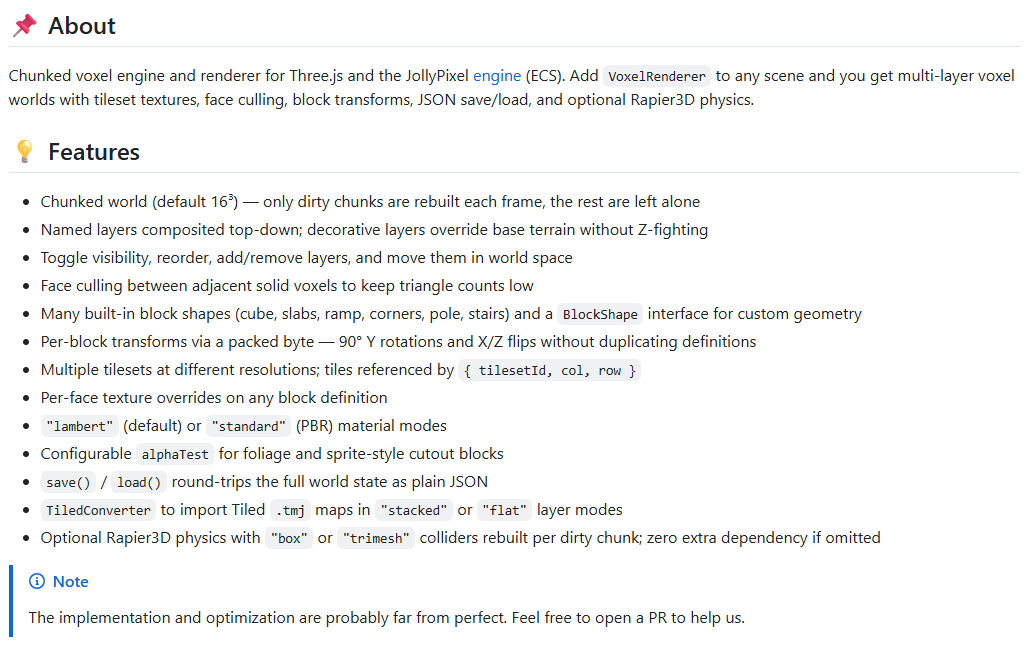

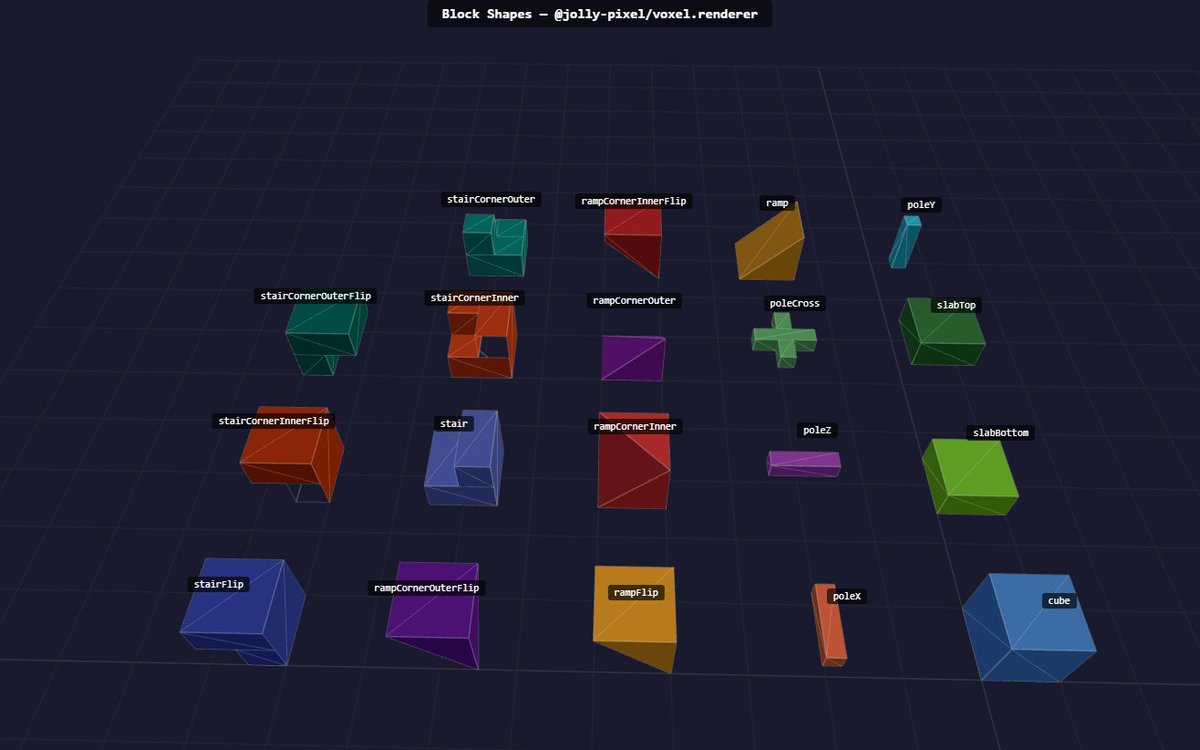

I just released an early V1.x of my VoxelRenderer working with my Three.js engine/ECS (going to be the API behind the graphic voxel level editor I'm working on).

Still a ton of work to do, but it should be cool to build small levels/maps (As in the past on Craftstudio).

1

2

184

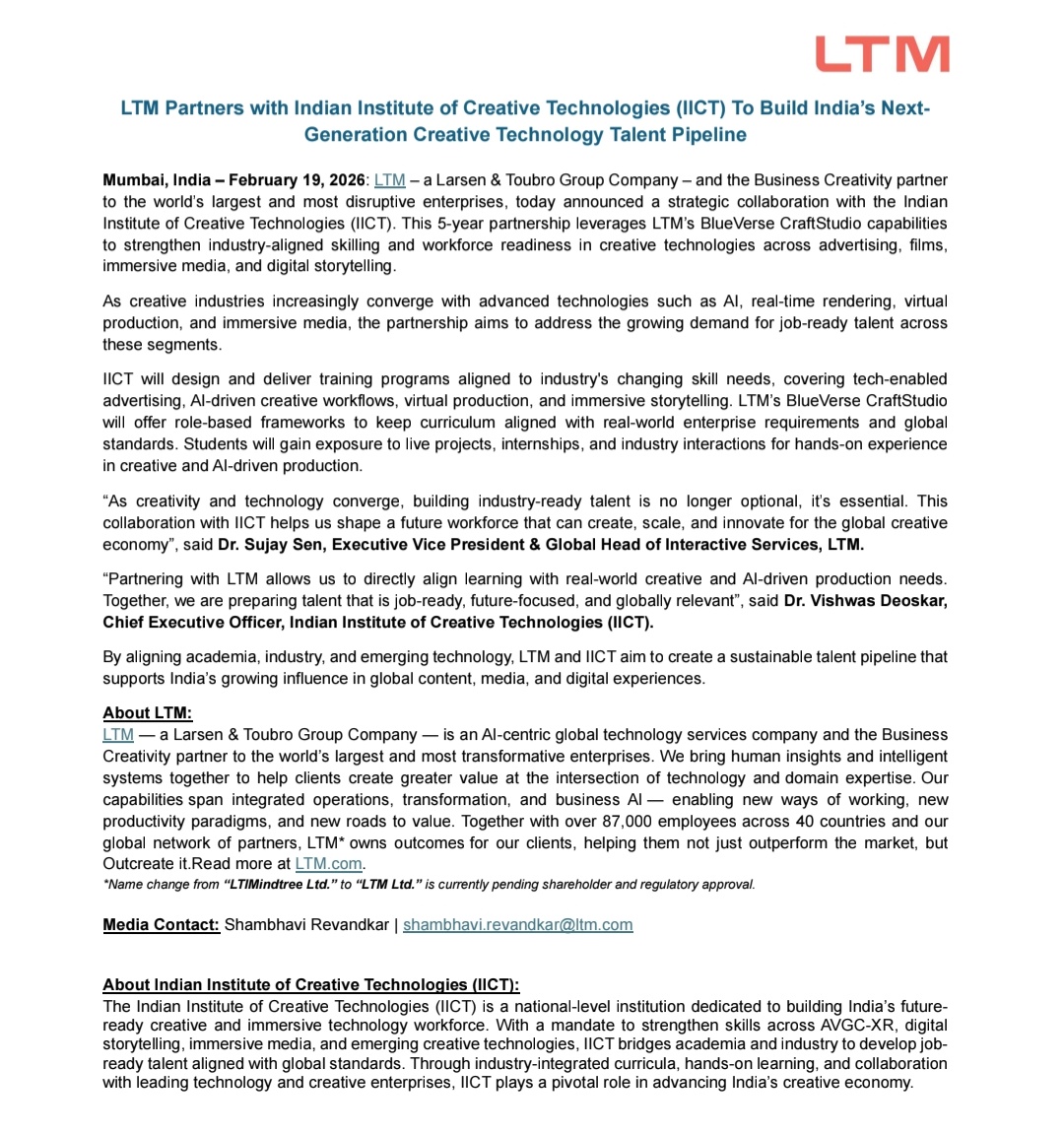

🔹#LTIM:

LTIM અને IICT વચ્ચે ઐતિહાસિક સમજૂતી: ભારતના યુવાનો માટે ક્રિએટિવ ટેકનોલોજીમાં કારકિર્દીની નવી તકો:

મુંબઈ સ્થિત લાર્સન એન્ડ ટુબ્રો (L&T) ગ્રુપની અગ્રણી કંપની LTM અને ઇન્ડિયન ઇન્સ્ટિટ્યૂટ ઓફ ક્રિએટિવ ટેકનોલોજી (IICT) એ આગામી 5 વર્ષ માટે એક મહત્વપૂર્ણ વ્યૂહાત્મક ભાગીદારીની જાહેરાત કરી છે.

આ સહયોગનો મુખ્ય ઉદ્દેશ્ય ભારતના યુવાનોને એડવર્ટાઇઝિંગ, ફિલ્મ નિર્માણ, ડિજિટલ સ્ટોરીટેલિંગ અને ઇમર્સિવ મીડિયા જેવા ક્ષેત્રોમાં લેટેસ્ટ ટેકનોલોજીથી સજ્જ કરવાનો છે,આજની દુનિયામાં જ્યારે આર્ટિફિશિયલ ઇન્ટેલિજન્સ (AI) અને વર્ચ્યુઅલ પ્રોડક્શનનો વ્યાપ વધી રહ્યો છે, ત્યારે આ ભાગીદારી દ્વારા વિદ્યાર્થીઓને સીધો ઉદ્યોગ જગતનો અનુભવ, ઇન્ટર્નશિપ અને લાઈવ પ્રોજેક્ટ્સ પર કામ કરવાની અમૂલ્ય તક મળશે.

આ ભાગીદારી હેઠળ, LTM તેની BlueVerse CraftStudio ક્ષમતાઓનો ઉપયોગ કરીને શિક્ષણના અભ્યાસક્રમને વધુ આધુનિક બનાવશે.

IICT એવા પ્રોગ્રામ્સ તૈયાર કરશે જે ઉદ્યોગોની બદલાતી જરૂરિયાતોને અનુરૂપ હોય, જેથી શીખનાર યુવાનો માત્ર ડિગ્રી જ નહીં પરંતુ વ્યવહારુ કૌશલ્ય પણ મેળવી શકે. LTM ના એક્ઝિક્યુટિવ વાઇસ પ્રેસિડેન્ટ ડો. સુજય સેન અને IICT ના CEO ડો. વિશ્વાસ દેવસ્કરના જણાવ્યા અનુસાર, આ પહેલ ભારતને વૈશ્વિક કક્ષાએ ક્રિએટિવ ઇકોનોમીમાં એક મજબૂત ઓળખ અપાવવામાં અને ભવિષ્ય માટે સક્ષમ વર્કફોર્સ તૈયાર કરવામાં પાયાનો પથ્થર સાબિત થશે.

🔹🔹🔹🔹🔹

#માર્કેટબુલેટિનન્યુઝઅપડેટ

2

287

AI is not just transforming industries. It’s redefining imagination.

In partnership with @nfdcindia and Waves Bazaar, #LTM is proud to bring the AI Cinema Showcase to the India AI Impact Summit 2026. Through LTM BlueVerse CraftStudio, we’re exploring what happens when storytelling meets intelligence — opening new frontiers for creators to shape culture with AI.

Because the future of AI will not be built by technology alone. It will be outcreated through business creativity.

Know more srkl.in/6018BASiUy

#ItsTimeToOutcreate #IndiaAIImpactSummit2026 #ALarsenAndToubroCompany @OfficialINDIAai

1

10

420

2

142

Jan 21

หลังจากบ้านหลังใหม่สร้างเสร็จไปไม่กี่เดือน ในที่สุด ‘ละมุนละไม’ (LMLM. Craftstudio) สตูดิโอเซรามิก Custom-made ก็เปิดบ้านต้อนรับคนรักเซรามิกด้วยเวิร์กช็อปที่ร่วมทำกับสตูดิโอน้องใหม่ ‘เส—รี สตูดิโอ’ ที่ทำงานริโซกราฟ ออกมาเป็นเวิร์กช็อปที่ชวนเรามาจับพู่กัน ปาดสีสูตรพิเศษของละมุนละไมมาเพนต์ลงบนแก้ว พร้อมพิมพ์ที่รองแก้วด้วยเทคนิคริโซกราฟ ออกมาเป็นชุดแก้วและที่รองลายไม่ซ้ำใคร สร้างความสดชื่นรื่นรมย์บนโต๊ะอาหาร

โดยการพิมพ์ริโซกราฟนี้พิมพ์ด้วยหมึกที่เป็นมิตรต่อสิ่งแวดล้อม ซ้อนทับลวดลายและเฉดสีลงไปทีละเลเยอร์ นอกจากให้เท็กซ์เจอร์ที่ไม่เหมือนงานพิมพ์ไหน ๆ การพิมพ์ซ้อนเลเยอร์ยังสร้างเฉดสีใหม่ ๆ อีกด้วย

เวิร์กช็อปนี้เป็นส่วนหนึ่งของงาน Bangkok Design Week 2026 และจัดเพียง 4 รอบเท่านั้น วันเสาร์ที่ 31 มกราคม และ 7 กุมภาพันธ์ พ.ศ. 2569 วันละ 2 รอบ เวลา 11.00 - 13.00 น. และ 15.00 - 17.00 น. สนใจลงทะเบียนได้ที่ forms.gle/K6ss4L1ERgTtWAqf9

#readthecloud #TheCloud #TheCloudRecommends #ละมุนละไม #LAMUNLAMAI #สตูดิโอเซรามิก #เซรามิก #เจริญกรุง #คาเฟ่เจริญกรุง #CasaLMLM #เสรีสตูดิโอ #seristudio

5

4

1,182

Part of the story of Hytale involves @ThomasFrick building a model of the Lich King for fun in my blocky game builder CraftStudio... 13 years ago 🤯. I was so impressed at the time, but I guess it was just a taste of what could be done with blocks!

youtube.com/watch?v=oJ9bryZG…

1

16

1,165

it's a reference to where I started making hytale models, craftstudio :)

2

74

5,284

𝐖𝐡𝐚𝐭 𝐚𝐧 𝐢𝐧𝐬𝐩𝐢𝐫𝐢𝐧𝐠 𝐝𝐚𝐲 𝐚𝐭 𝐖𝐚𝐯𝐞𝐬 𝐅𝐢𝐥𝐦 𝐁𝐚𝐳𝐚𝐚𝐫!

Our Tech Pavilion booth became a creative playground—filmmakers, storytellers, and tech innovators coming together to explore how #LTIMindtreeBlueVerse CraftStudio is opening new possibilities in AI-driven filmmaking.

A standout moment was the conversation between Dr. Sujay Sen and Shekhar Kapur. Their session, 𝐁𝐫𝐢𝐧𝐠𝐢𝐧𝐠 𝐀𝐈 𝐚𝐧𝐝 𝐂𝐫𝐞𝐚𝐭𝐢𝐯𝐢𝐭𝐲 𝐓𝐨𝐠𝐞𝐭𝐡𝐞𝐫 𝐭𝐨 𝐂𝐫𝐚𝐟𝐭 𝐒𝐭𝐨𝐫𝐢𝐞𝐬 𝐭𝐡𝐚𝐭 𝐈𝐧𝐬𝐩𝐢𝐫𝐞, left the room buzzing with fresh ideas.

Key reminders from the day:

✨ AI doesn’t replace creativity—it amplifies it.

✨ Clean, connected data powers intelligent storytelling.

✨ The future of cinema lives where art meets technology.

We’re excited to keep pushing boundaries and co-creating the next era of storytelling! 🎬

#WavesFilmBazaar #AIStorytelling #BlueVerseCraftStudio #GenerativeAI #FutureOfCinema

279

It was a high-energy day at the @IFFIGoa 2025 and Waves Film Bazaar, shining a spotlight on AI-driven storytelling. The excitement around this new wave was truly inspiring, especially seeing the enthusiasm and curiosity of everyone who visited.

#LTIMindtree BlueVerse CraftStudio helped bring the first-ever AI Film Festival to life, demonstrating how intelligent tools can produce faster, bolder, boundary-breaking stories. And this is just the beginning.

Momentum is now building toward the CinemAI Hackathon, which launched yesterday. This 48-hour creative sprint pushes the limits of what AI and imagination can achieve together. Stay tuned for more highlights and gear up for India's first-ever AI Awards, presented by LTIMindtree in association with IFFI and NFDC.

The future of storytelling is unfolding in real time.

#AIStorytelling #IFFI2025 #WavesFilmBazaar #BlueverseCraftStudio #AIFilmFestival #CinemAIHackathon #AIAwards #FutureOfCinema #CreativeTech

1

4

1,123

𝐒𝐭𝐞𝐩 𝐈𝐧𝐭𝐨 𝐭𝐡𝐞 𝐅𝐮𝐭𝐮𝐫𝐞 𝐨𝐟 𝐒𝐭𝐨𝐫𝐲𝐭𝐞𝐥𝐥𝐢𝐧𝐠

At Waves Film Bazaar, the screen doesn’t just light up, it comes alive.

This is where cinema thinks, AI imagines, and creativity breaks its own rules.

We’re exploring how the next wave of filmmaking is crafted bold, intuitive, and limitless with AI. Come Experience the Craft of Possible with LTIMindtree BlueVerse CraftStudio.

We’ll see you at Waves Film Bazaar!

#LTIMindtree #TheCraftHonors #AIStorytelling #FilmFestival #CinemaAI #BlueVerseCraftStudio

1

1

199

6 Oct 2025

Working on a pixel editor/canvas to re-implement tileset texture for an upcoming voxel editor like the one made by @elisee in Craftstudio but for Three.js. Next step: editing and managing UV ^-^.

1

5

288

21 Sep 2025

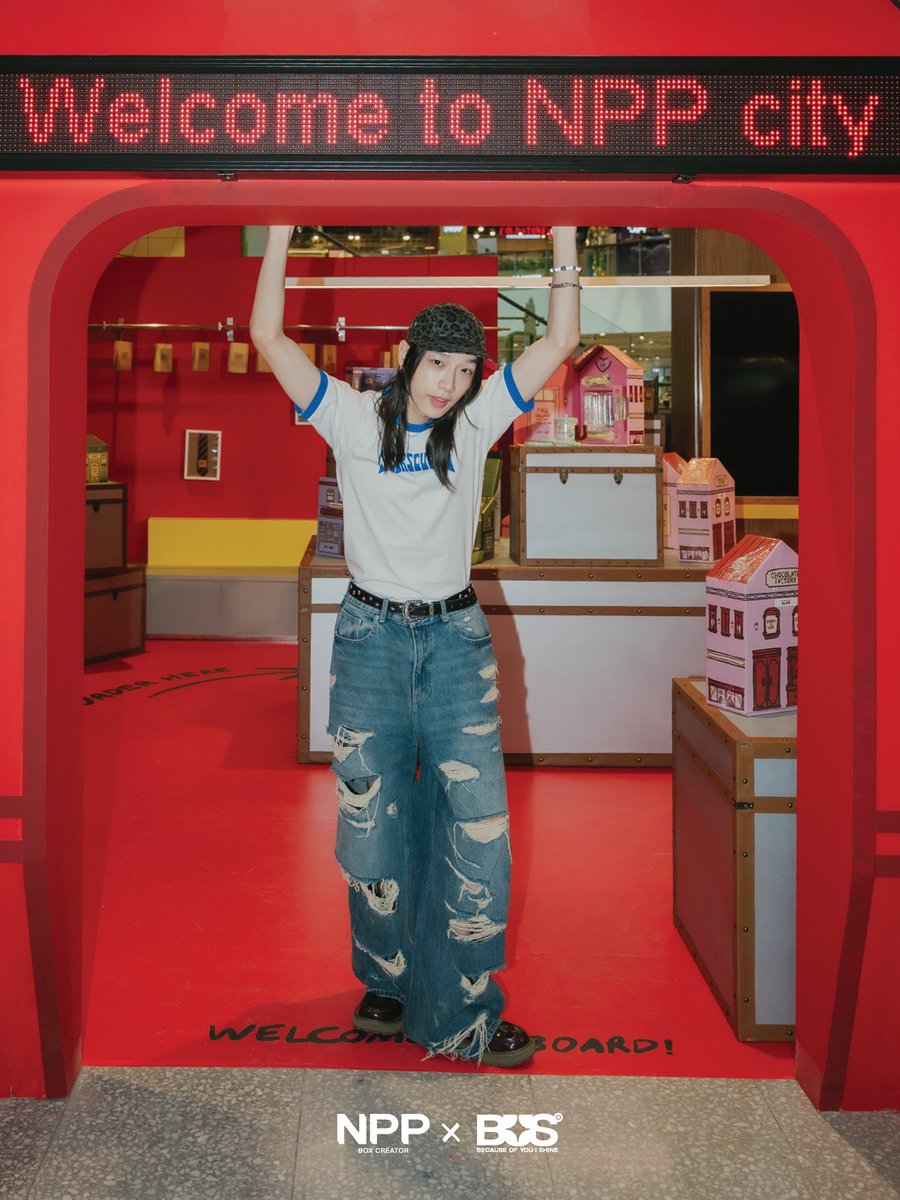

[🏡🌻]

WELCOME TO #NPPxBUS_NPPCITY ✨

ฮ้าทสปุ้ดได้ข่าวมาว่า @NPPBOX กำลังจัด

#NPPxBUS POP-UP STORE

THE JOURNEY TO NPP CITY 🚂🚏🧳

ภายในบูธจะมีทั้งสินค้าตัวอย่างจาก collection ใหม่ล่าสุด รวมถึงมีมุมต่าง ๆ ให้ทุกคนได้มาถ่ายรูปกันแบบสีสันน่ารักสดใส ฮ้าทสปุ้ดเลยขอแอบเก็บภาพบรรยากาศมาฝากทุก ๆ คนกันค่ะ („• ֊ •„)੭

แถมพี่กล่องยังแอบกระซิบมาว่าถ้าซื้อสินค้าภายในงานไม่ว่าจะเป็นพวงกุญแจ แก้วน้ำ หรือกระถางต้นไม้ (จำกัดการซื้อเมมเบอร์ละ 12 ชิ้น) จะได้รับการ์ดที่ระบุเลข serial number สำหรับการใช้เข้าร่วมกิจกรรมที่อาจเกิดขึ้นในอนาคตต่อไปได้ด้วยค่ะ (..◜ᴗ◝..)

อย่าลืมแวะมาหาพี่กล่องที่ชั้น 5 centralwOrld โซน craftstudiO กันนะคะ วันนี้วันสุดท้ายแล้ว พี่กล่องพร้อมต้อนรับทุกคนจนถึง 3 ทุ่มเลยน้าา~

29

22

3,052

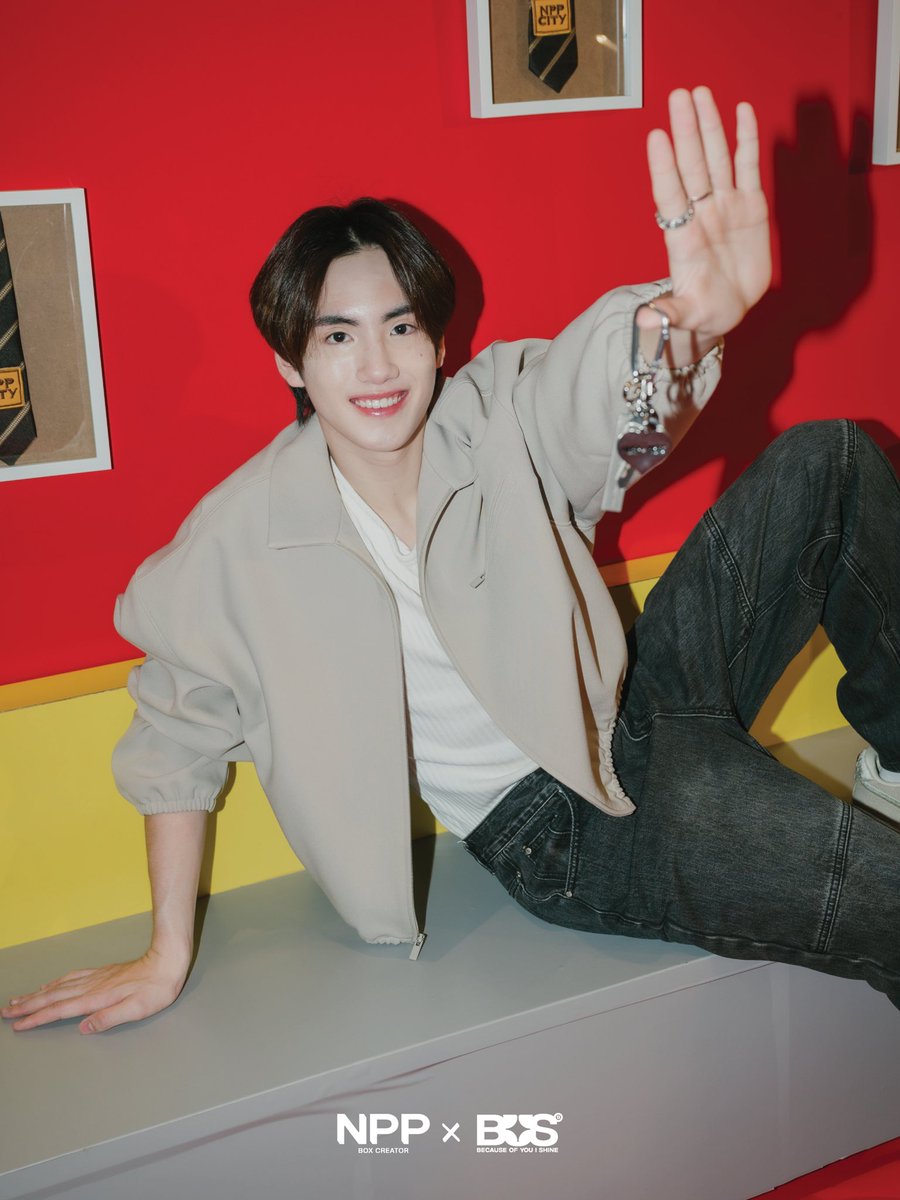

FINAL CALL! 📢

#NPPxBUS_NPPCITY

วันสุดท้ายแล้วน้าบีอัส

มาหากับพี่กล่องกับบัสอ้วรกันนนนน 🫶🏻💗🥺

#NPPxBUS POP-UP STORE

THE JOURNEY TO NPP CITY 🚂🚏🧳

POP-UP ครั้งแรกของพี่กล่อง

ชวนทุกคนมาผจญภัยสู่ #NPPCITY 🏡

ค้นพบลายเส้นจากแรงบันดาลใจของ

“บัสอ้วร” ไปพร้อมกัน

📍craftstudiO ชั้น 5 centralwOrld

🗓️ 18-21.09.25

🕗 10 AM - 9 PM (GMT 7)

▻ ชมและช้อปคอลเลกชัน NPP CITY

ก่อนใคร (จำนวนจำกัด)

▻ สัมผัสและถ่ายรูปบรรยากาศ

ผจญภัยแบบ “บัสอ้วร”

▻ สินค้า Exclusive เฉพาะ

POP-UP STORE เท่านั้น

#NPPBOX #BUSbecauseofyouishine

#COCREATEDWITHNPPBOX

1

714

826

26,922

#NPPxBUS_NPPCITY

IS CALLING!

🍫🌻🗝️🏡

บีอัส! มาผจญภัยสู่ #NPPCITY

กับพี่กล่องกันนน 🗺️🫶🏻

2 วันสุดท้าย ในเส้นทางที่เต็มไปด้วย

ลายเส้น และแรงบันดาลใจของ “บัสอ้วร”

ตามหาร่องรอยสุดคิ้วท์ของ

เจ้าเมืองไปพร้อมกันที่

#NPPxBUS POP-UP STORE

THE JOURNEY TO NPP CITY 🚂🚏🧳

📍craftstudiO ชั้น 5 centralwOrld

🗓️ 18-21.09.25

🕗 10 AM - 9 PM (GMT 7)

▻ ชมและช้อปคอลเลกชัน

NPP CITY ก่อนใคร (จำนวนจำกัด)

▻ สัมผัสและถ่ายรูปบรรยากาศ

ผจญภัยแบบ “บัสอ้วร”

▻ สินค้า Exclusive เฉพาะ

POP-UP STORE เท่านั้น

#THAIchayanon #JINWOOKkim

#NEXnattakit #PHUTATCHAI

#NPPBOX #BUSbecauseofyouishine

#COCREATEDWITHNPPBOX

180

192

12,980

น้อนโต๊ย 🍫 vs พิบ๊อกแบ็ก 🍫

ศึกชนแก้วแห่ง #NPPCITY 🏡

(ตั้งชื่อโดยสุดหล่อท่านหนึ่ง)

ชวนบีอัสมาเล่นชนแก้วกันแบบ

#PHUTATCHAI และ #MARCKRIS

ศึกนี้ไม่มีแพ้ไม่มีชนะ

เพราะน่ารักเสมอคับ 🐶💕

PRE-ORDER #NPPxBUS_NPPCITY 🏡

🔗: tinyurl.com/NPPCITY-BUS

🗓️: 9 ก.ย. 68 - 7 ต.ค. 68

เริ่มจัดส่งสินค้า ตั้งแต่ 15 ต.ค. 68 เป็นต้นไป

หรือ มาช้อปที่ POP-UP STORE

THE JOURNEY TO NPP CITY 🚂🚏(จำนวนจำกัด)

📍craftstudiO ชั้น 5 centralwOrld

🗓️ 18-21.09.25

🕗 10 AM - 9 PM (GMT 7)

*All designs showcased in this collection

are exclusively co-created with

BUS because of you i shine

#NPPBOX

#BUSbecauseofyouishine

#COCREATEDWITHNPPBOX

14

950

1,162

25,916

🗓️ พรุ่งนี้วันสุดท้าย!

แอบเห็นเจ้าเมือง #NPPCITY 🏡

เค้าแอบมาขีดเขียนอะไรกันม่ายรุ

🗺️🧭 แจกลายแทงของเจ้าเมือง

พี่กล่องเจอประมาณนี้

ใครเจอเยอะกว่านี้แท็กมาอวดหน่อยน้า

#NPPxBUS_NPPCITY

บีอัสรีบมาตามหาร่องรอยความน่ารัก

ของ “บัสอ้วร” ได้ที่

#NPPxBUS POP-UP STORE

THE JOURNEY TO NPP CITY 🚂🚏🧳

📍craftstudiO ชั้น 5 centralwOrld

🗓️ 18-21.09.25

🕗 10 AM - 9 PM (GMT 7)

รออยู่น้าาาาา 🫶🏻

#THAIchayanon #JINWOOKkim

#NEXnattakit #PHUTATCHAI

#NPPBOX #BUSbecauseofyouishine

#COCREATEDWITHNPPBOX

2

485

557

20,123

#NEXnattakit & #PHUTATCHAI

are finally in #NPPCITY 🏡

เดินทางเข้าสู่ #NPPxBUS_NPPCITY

แบบเน็กซ์ & ภูธัชชัย

POP-UP ครั้งแรกของพี่กล่อง

ให้บีอัสมาค้นพบลายเส้น “บัสอ้วร”

ไปพร้อมกัน

#NPPxBUS POP-UP STORE

THE JOURNEY TO NPP CITY 🚂🚏🧳

▻ ชมและช้อปคอลเลกชัน

NPP CITY ก่อนใคร (จำนวนจำกัด)

▻ สัมผัสและถ่ายรูปบรรยากาศ

ผจญภัยแบบ “บัสอ้วร”

▻ สินค้า Exclusive เฉพาะ

POP-UP STORE เท่านั้น

📍craftstudiO ชั้น 5 centralwOrld

🗓️ 18-21.09.25

🕗 10 AM - 9 PM (GMT 7)

#NPPBOX

#BUSbecauseofyouishine

#COCREATEDWITHNPPBOX

23

1,068

1,076

32,956