Andre Gironda retweeted

Jun 12

2/21

The kit ships 152 gate modules covering Stripe, Adyen, Braintree, Cybersource, Chase Paymentech, Authorize.net, Worldpay/Vantiv, Recurly, Square, Sagepay, NMI, Checkout.com, Moneris, Payeezy, Payflow, MercadoPago, PayPal, and Zuora. Roughly one third validate cards without charging; the rest run small live transactions to confirm the card is good.

1

1

4

324

Jun 8

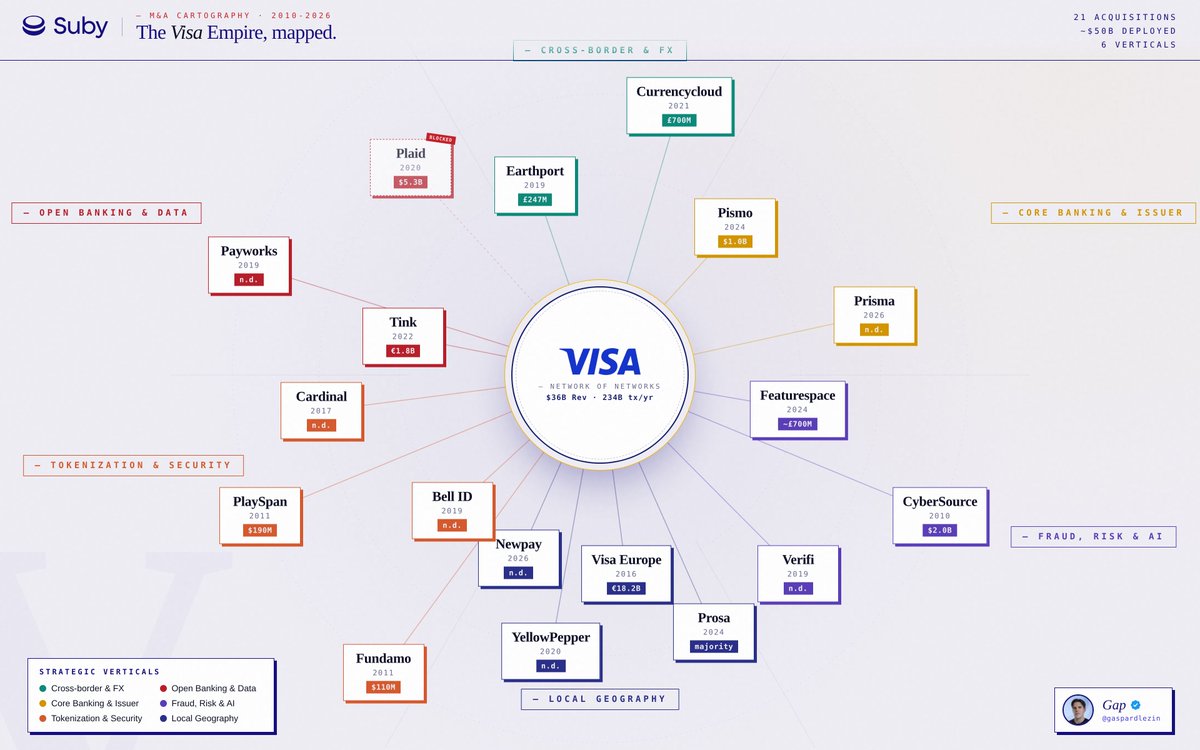

Notable acquisitions such as Cybersource and Plaid have enabled Visa to reinforce its footing in the digital arena.

1

7

Jun 7

Before Stripe was a verb, Cybersource was already routing the internet's money.

Our cover story on @cybersource

yespress.io/cybersource?utm_… via Yespress

15

May 26

Most people think Visa makes money when you tap your card. That's becoming the smaller half of the business.

When people think Visa, they still picture the card network. That's about 30% of what Visa actually does today. The rest is cross-border infrastructure, issuer processing, fraud AI, identity, tokenization, and open banking. Each layer demands a different acquisition playbook, and that's exactly what Visa has built over the last decade.

Card transactions are still massive in volume, but their strategic weight keeps shrinking. In several of Visa's recent deals, the card isn't even the product.

The Visa Europe buyback is the clearest example. Often dismissed as a routine corporate move, it actually rewired the company. $18.2 billion, full control of European payment rails reclaimed from EU banks, and the global network unified under a single P&L.

The same pattern shows up across the portfolio. Earthport and Currencycloud for cross-border. Pismo and Prisma for issuer processing. Featurespace and Verifi for fraud. Tink for open banking. Bell ID and Cardinal for tokenization.

Visa's 21 acquisitions span the full stack of payment infrastructure:

- Cross-border and FX: Earthport (£247M), Currencycloud (£700M)

- Core banking and issuer: Pismo ($1B), Prisma (2026)

- Fraud, risk, AI: Featurespace (~£700M), Verifi Inc., Cybersource ($2B)

- Local geographies: Visa Europe (€18.2B), NewPay, PROSA, yellowpepper

- Tokenization and security: Bell ID, Cardinal, Fundamo pty ($110M), PlaySpan Inc. ($190M)

- Open banking and data: Tink (€1.8B), Plaid ($5.3B blocked), Payworks

Competitive pressure explains the shift. Stripe's full-stack approach, Adyen's unified platform, and the rise of account-to-account payments have made a card-centric strategy obsolete.

By 2026, Visa's strategic exposure breaks down roughly as ~40% card network and cross-border, ~30% issuer processing and core banking, ~30% fraud, identity, tokenization, and open banking.

Real-time payments, embedded finance, and AI-driven risk infrastructure keep pushing that mix further.

Visa isn't a card network anymore. It's becoming the payment infrastructure layer of every digital business.

PS: I write about payments with @subyhq, stablecoins, and what building a payment startup actually looks like, every week.

11

9

59

7,366

May 24

For years, Visa was mostly understood as a card network: authorization, clearing, settlement, acceptance, credentials, and global reach.

That view is now incomplete.

Visa processed 257.5 billion transactions in fiscal year 2025, with total payments and cash volume reaching $16.7 trillion. But the more strategic part of the story is happening outside the traditional transaction processing narrative. Its Value-Added Services business generated nearly $11 billion in revenue in FY2025, growing 24% year over year.

This matters because payments are fragmenting.

A2A payments are growing.

Real-time payment schemes are scaling.

Stablecoins are entering treasury and settlement workflows.

Domestic networks are becoming stronger.

Merchants and fintechs want routing flexibility.

That creates a problem for card networks.

If payment volume moves away from proprietary rails, the old model becomes more exposed. Visa’s answer is not just to defend card volume. It is building software around the transaction.

- Fraud scoring.

- Tokenization.

- Dispute management.

- Open banking.

- Issuer processing.

- Authorization optimization.

- Advisory services.

- AI-enabled risk tools.

These products can be monetized even when the payment does not move over VisaNet.

That is the strategic shift.

Visa is trying to turn payment fragmentation into a software opportunity.

The Featurespace acquisition strengthens fraud and risk capabilities across card and non-card rails. Pismo expands Visa deeper into issuer processing and cloud-native banking infrastructure. Tink gives Visa open banking reach in Europe. Cybersource and Authorize net give it acceptance infrastructure across merchants, PSPs, and acquirers.

This is not a side business anymore.

VAS is becoming Visa’s operating system for the broader payments market.

For fintech founders, the lesson is clear: infrastructure companies win when they move from transaction dependency to workflow dependency.

For product leaders, the key question is whether your product is only attached to a payment method, or whether it solves a recurring operational problem around payments.

For investors, Visa’s VAS growth shows where the defensibility in payments may move next: risk, identity, tokenization, orchestration, compliance, and embedded software.

The card network still matters.

But the higher-margin opportunity is increasingly around the intelligence layer that sits above every rail.

fintechwrapup.com/p/deep-div…

1

8

777

May 6

If you think Visa is just a card network, you're seeing 30% of the empire.

Modern Visa isn't just rails for plastic. It's cross-border infrastructure, issuer processing, fraud AI, identity, tokenization, and open banking, each requiring a different acquisition layer. That's why Visa's M&A strategy has split into a full stack of specialized verticals.

Card transactions are still massive, but their share of Visa's strategic priorities keeps shrinking. In many of Visa's recent deals, cards aren't even the product.

Visa Europe is a good illustration.

Often perceived as a routine corporate buyback, it actually reshaped the company entirely:

- $18.2B deal, the largest M&A in Visa's history

- Reclaimed full ownership of European payment rails from EU banks

- Unified Visa's global network under a single P&L

The same pattern exists across the empire: Earthport and Currencycloud for cross-border, Pismo and Prisma for issuer processing, Featurespace and Verifi for fraud, Tink for open banking, and Bell ID and Cardinal for tokenization.

Visa's 21 acquisitions reflect the diversity of payment infrastructure:

- Cross-border & FX: Earthport (£247M), Currencycloud (£700M)

- Core Banking & Issuer: Pismo ($1B), Prisma (2026)

- Fraud, Risk & AI: Featurespace (~£700M), Verifi, CyberSource ($2B)

- Local Geography: Visa Europe (€18.2B), Newpay, Prosa, YellowPepper

- Tokenization & Security: Bell ID, Cardinal, Fundamo ($110M), PlaySpan ($190M)

- Open Banking & Data: Tink (€1.8B), Plaid ($5.3B blocked), Payworks

Competitive pressure explains this shift. Stripe's full-stack approach, Adyen's unified platform, and the rise of account-to-account payments have made a card-only strategy obsolete.

By 2026, Visa's strategic exposure breaks down roughly as:

~40% card network and cross-border

~30% issuer processing and core banking

~30% fraud, identity, tokenization, and open banking

Real-time payments, embedded finance, and AI-driven risk infrastructure continue to accelerate this trend.

Visa is no longer a card network. It's becoming the payment infrastructure layer of every digital business.

PS: I post about payments with @Subyhq, stablecoins & the reality of building a payment startup, every week. Follow for more!

5

3

41

3,623

Apr 24

Egypt’s MoneyHash, Visa expand partnership with multi-year commitment to expand cybersource enablement disruptafrica.com/2026/04/22…

1

2

231

Apr 23

Egypt’s MoneyHash, Visa expand partnership with multi-year commitment to expand cybersource enablement disruptafrica.com/2026/04/22…

3

5

339

Apr 16

The Ministry of Tourism and Wildlife has launched TouristTap, a digital payment platform that allows tourists to pay for goods and services directly to mobile money platforms without needing a local SIM card. Visitors download the app, register, and complete payments by entering a local till, paybill, or mobile number, then tapping their NFC-enabled phone and entering a secure PIN. Tourism CS Rebecca Miano described the platform as a transformative solution aligned with Kenya's digital transformation agenda. The platform is backed by a partnership with KCB Bank and Visa, powered by CyberSource. Tourism generates approximately Sh500 billion annually and supports nearly three million jobs in Kenya.

3

85

Apr 13

Sii, bastante más. Tiene Tink y Cybersource issuers VAS. Mastercard no tiene nada ahí.

2

3

263

Mar 31

You can receive International card payments using CyberSource payment gateway thats provided by NIC Asia Bank.

1

2

1,099

Já usei muito clearsale e realmente é muito bom. Eu só tenho trauma da cybersource que me fez perder alguns milhares de reais por fraude que eles não pegaram.

2

2

141

Mar 18

Bizwire : Sampath Bank PLC and Apartner (Pvt) Ltd partner to digitise condominium maintenance payments in Sri Lanka, introducing a secure, real-time platform that streamlines collections, reconciliations, and financial visibility for residents and management corporations through Visa’s Cybersource integration.

D: newswire.lk/8mva

9

1,368

Jan 3

My first recommendation is calling your bank or card issuer (if it’s a credit card) and initiating chargebacks for all Etsy charges. Tell them you changed cards because of this issue and it’s persisting. After the chargebacks are made, close the account entirely. What’s likely happened is when you were issued a new card, Visa’s Cybersource Account Updater sent card updates to Etsy when they ran batch updates.

2

3

87