Intrinsiqq puts free quality scores, DCFs, and financials for 8,000 US stocks right in retail investors’ hands.

2

What the fck is this, you fat fcking POS low-life fcking traitor? You are fcking WORTHLESS. And fck your dcfs and your corrupted court system. Just filed a federal lawsuit against your fcking agencies. Im not quitting until the corruption is exposed. You are a fcking king pig.

6

What the fck is this, you fat fcking POS low-life fcking traitor? You are fcking WORTHLESS. And fck your dcfs and your corrupted court system. Just filed a federal lawsuit against your fcking agencies. Im not quitting until the corruption is exposed. You are a fcking king pig.

6

I didn't vote for this

It's a violation to emoluments

We are forcing fights onto presidential property

With alcohol sponsors

For a guy who claims to love children this is the most fucked up family fun idea I've seen. And I know because I had to put a child to DCFS after the father kept encouraging WWE fighting and imitation of it to be viewed and done in the house respectively.

This resulted in the mother taking a concussion and the child being moved into foster care.

But sure. UFC is totally perfect for all Americans.

Get rid of the ID verification and kids online safety act Donnie.

You don't give a shit when you let grown men covered in sweat dry hump each other in what is legalized soft core porn for people who are hiding their gayness behind it being a sport.

We get it. Y'all wanna suck a rich fighters cock get married to him and live in his mansion as his sex toy. Disgusting perverts b

2

54

Simple Whitney hired a Jew so that a Hispanic could get DCFS to put down a Chinese fuck she picked up out of graciousness

1

32

12h

How Does DCFS Prove a Case Against Parents?

Fedor Kozlov explains the major difference between DCFS investigations and criminal cases. In criminal court, the government must prove charges beyond a reasonable doubt, with strict requirements like expert testimony and chain of custody. But in DCFS cases, the standard is much lower—just “more likely than not.” A simple phone call from a doctor or nurse can be enough to start action, even without revealing the source.

Click the bio link to watch the full episode.

bio.link/fedorkozlov

#FedorKozlov #FamilyLaw #DCFS #ChildProtection #ParentalRights #CustodyCases #FamilyAttorney #LegalInsights #IllinoisLaw #BurdenOfProof #ParentsRights

3

I got into something of a meditation on SpaceX's valuation in another thread

x.com/JimPGillies/status/206…

I decided to cut/paste to my main feed so as to boost visibility.

Also, the Damodaran model discussed below can be found here:

aswathdamodaran.substack.com…

Enjoy...or not...I'm not the boss of you.

---------------------------------------------

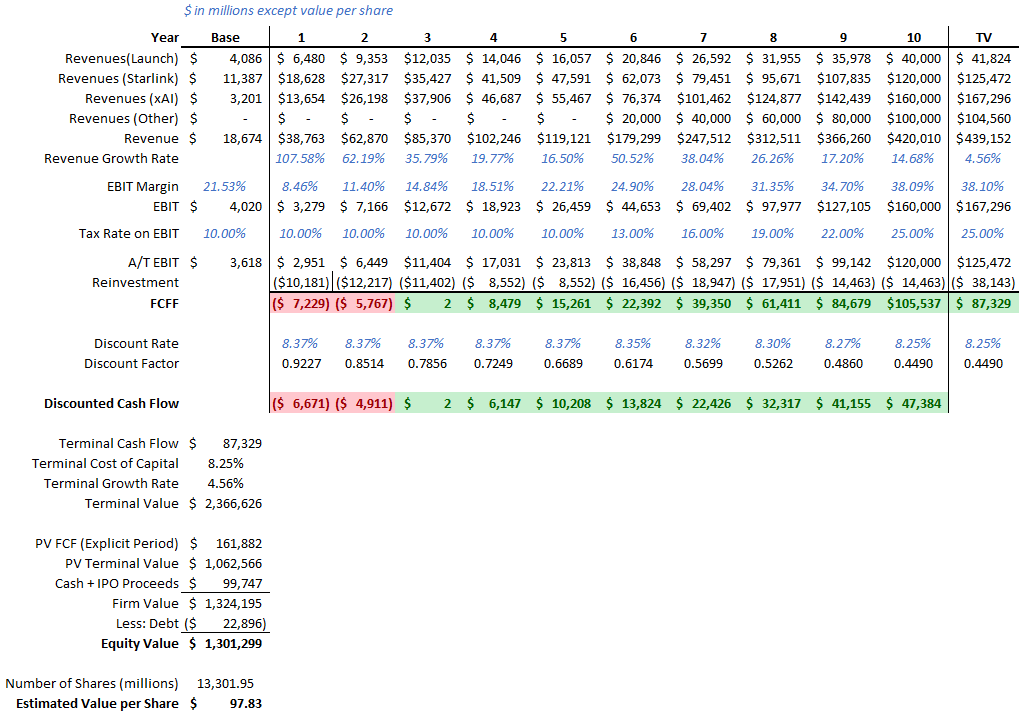

So I recast Damodaran's numbers on my own sheet which you can see below.

Now my contention is that ALL DCFs are wrong ALL of the time. This is not a shot at anyone's work, but rather an acknowledgement that we are dealing with forecasts and reality will absolutely diverge from those forecasts. (I have yet to meet an investor with perfect foresight; it certainly isn't me!)

And the more variables within a forecast, the more places where things can "go wrong" and diverge (to the upside or to the downside).

Take a look at Damodaran's revenue growth here. What if growth falls off faster than anticipated? What if it doesn't? Changes in estimated value, that's what.

Oh, and did you look further at the components of revenue growth here? Did you note how it's just Launch, Starlink, and xAI growing in the first five years of the model, and then "Other Revenues" of $20 billion show up magically in Year 6 of his forecast and increase by another $20 billion in EACH of years 7, 8, 9, and 10 (and then, of course, are PERMANENTLY entrenched in the terminal period/value...which, as you should ALSO observe is the largest component of calculated value).

I mean...what if those "Other Revenues" (what are they again?) don't show up at scale and on-time? Nothing good for the valuation, that's what. Of course, the opposite is ALSO true...if these unspecified billions of "other" revenues DO show up higher than modelled (and/or earlier than forecast) it will boost value per share; given the current enthused share price, I would suggest that investors here should really hope this is what happens.

Take a look at Damodaran's EBIT margin progression. Again, what if it doesn't progress as he forecasts? What if it does better? Again, changes in valuation.

What if his estimated tax rate doesn't stay as low as it does in the early days? What if it stays low longer than he forecasts before the uptick? Again, the estimated value per share changes.

Move down to the lower part of the model. Notice how 80% of the "Firm Value" is in the Terminal Value? That's inherently risky - you're placing ostensibly 80% of the value of today's calculated value per share into the far unknown (i.e. 10 years out).

AND (I would again argue) you're discounting that at far too low of a discount rate (8.25%).

I saw a LOT of very intelligently-constructed and thought-out DCF models for internet companies in 1998-through-early 2000. Reality unfolded...somewhat different than expectations when the calendar turned to mid-2000 and beyond (even for those that survived and thrived - i.e. AMZN).

And there's one rather large omission I'd like to call out about Damodaran's model and that is, it makes no provision for the cost of "equity cookies" given to insiders...something that I think you (and everyone else) will agree will be a "non-zero" cost with a company like SpaceX.

My methodology for dealing with such is to value outstanding options with Black-Scholes (using reasonable assumptions for how many make it to actual vesting) and deduct the calculated value from "Firm Value" as something of a contingent liability akin to debt. I also boost the share count by the number of outstanding, but uninvested RSUs (again, modified by a reasonable forfeiture rate based on historical pattern).

In Damodaran's model, he effectively has this "cost" at zero (I mean, maybe it's buried in his EBIT margin assumption, but that's an accounting construct...I prefer an actual "hard" value I can deduct as that contingent liability.)

But I promise you, the value syphon from firm value into insider pockets will be (significantly) higher than zero; this is an Elon Musk company after all...if you were to compare the man's comp at Tesla to Tesla's lifetime profits, I suspect it might make you ill.

Point is, I think you ALSO need to deduct an amount/increase share count (which would result in a lower "per share" calculated value) for equity cookie "leakage" from this valuation. In other words, I think this is another place where Damodaran's model actually OVERvalues SpaceX.

But leave all that aside.

Damodaran's model calculates an equity value of just over $1.3 trillion, or $97.83 per share.

Meaning that the IPO price of $135 is at a 38% premium to what I consider to be a very generous valuation estimate by Prof. Damodaran, and that the Day 1 Closing price of $160.95 is at a 64.5% premium.

I would not consider investing into that. Feel free to holler back, "Have fun staying poor!" - it doesn't bother me. ;-)

But let's play out a couple of other scenarios.

First, if we used a uniform 11% discount rate (my "opportunity cost" choice remember), and changed nothing else about his forecast and model, equity value falls to about $685.7B with the fair value per share dropping to $51.55.

I remind you again that it closed yesterday at $160.95.

If you wanted to recast the model - again, changing nothing about his forecast or model; no contingent liabilities tied to potential dilutive "equity cookies", no margin compression or removal of the magical "Other Revenues" that show up in Year 6 - to equate the forecasted cash flows/valuatuion to the $135 IPO price, you'd need a 7.35% discount rate.

If you wanted to do so to equate it to yesterday's $160.95 closing price, you'd use a 6.93% discount rate.

And again, when share price equates to calculated value per share, the discount rate can be used as a rough approximation of expected returns going forward.

You think SpaceX investors are excited about prospective 7% returns going forward from here? I mean, I can give you a list of stocks with higher dividend yields that are probably safer...

Look, again, this is no slight on Damodaran - he's simply made an honest effort at valuing the company based on known and inferred inputs plus a healthy dose of Academic Finance methodology.

And folks who want to invest at this level...well, fair play and good luck. I genuinely wish you well.

But as to your last comment that, "anyone who owns index funds will end up owning SPCX sooner or later so they will get some exposure that way, whether they like it or not," I agree with you.

And I think that's actually tragic. I hate that Nasdaq is speed-running SpaceX inclusion. I appreciate that the S&P committee is at least sticking to their guns (for now) and requiring that SpaceX earn their place in the index the old fashioned way.

But there ARE things you can do to mitigate that, "whether they like it or not," statement.

In my family's portfolio we have roughly half our money in index-tracking ETFs and half under active management by yours truly. The index fund allocation used to be about:

* 25% TSX60 (I am Canadian, after all).

* 45% S&P500

* 25% MSCI EAFE Investible Market Index

* 5% QQQ

After word came out that Nasdaq was speed-running SPCX into QQQ I exited all QQQ and redeployed into S&P500 (there was already substantial overlap anyway so not a big deal).

I have also recently swapped about half the S&P500 exposure for an equal-weight S&P500 fund, though this is NOT so much "fear of SpaceX inclusion" and more a risk-mitgation move with the so-called "Magnificent Seven" now making up about 34% of the total weight in the index, and the overall market looking a little "enthused".

When/if SpaceX is added to the S&P500, there are also some options techniques you can use to hedge out exposure if you want to (i.e. basically set up a "synthetic short" in an amount roughly equal to the "look-through long exposure" of SpaceX...or any other company you might not want exposure to for that matter, effectively turning your S&P500 fund into an "S&P499"...just...no bitching if you get it wrong and the stock - again, SpaceX or otherwise - goes up and you're hedged out!)

One final note. I think it's worth noting that inclusion in the index ain't all it's cracked up to be.

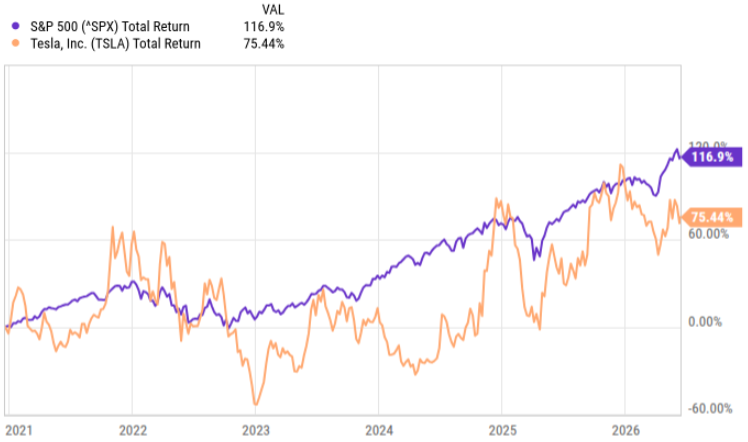

Tesla was added to the S&P500 before market open on 21-Dec-2020. I've included the total return for both Tesla and the index in the chart below. You'll note that Tesla, for all the hype, has UNDERperformed the index since inclusion; not, I think, what Tesla investors were expecting when it was originally announced as being added.

But there's another inference to be made.

If Tesla were never added to the index, the index value would be higher today. (i.e. it has underperformed the index while being a component of said index).

In other words, with Tesla included in the index, passive index investors have been treated to lower overall returns than they would have otherwise received had Tesla never been included.

I expect that the same phenomenon will occur when/if SpaceX is included in the index (and why I'll be looking again into those hedging techniques I mentioned).

Here endth the meditation. Be sure to tip your server.

1) Never said it was “worth nothing.” That’s misrepresentation.

2) I already shared Damodaran’s work a couple weeks back. Note that his valuation pegs it at $1.2T…far below IPO valuation and yesterday’s close.

3) I LOVE Damodaran (used to have his lectures playing while I made dinner at night), but he has constructed a very “Finance Professor” valuation.

Just look at discount rate…he does a 10-yr explicit forecast period with discount rates starting at 8.37% and sliding to 8.25% at entry to terminal period.

That’s a very “Finance Professor” thing to do - CAPM, Beta, equity risk premiums based on current conditions and all that (I used to teach this stuff when I moonlighted as a finance instructor at a local university).

But there are two problems with this…

First, if interest rates ever go up, this valuation (and a bunch of other ones) gets destroyed because you’d now be discounting at 11%, 12% or 13%.

Bluntly, I think it’s madness to discount such an inherently risky company with a rate starting with an 8-handle.

This then leads me to my second “problem”.

As an individual retail investor (who speaks to/tries to help/guide other individual retail investors) I hold that a personal discount rate should NOT be determined by the aforementioned CAPM/Beta/equity risk premium model.

Rather, I’m an “Opportunity Cost” kind of guy. We know that the stock market over the very long term has returned a compounded 10%-12% annually (total return - i.e. with dividends reinvested, depending on your starting date).

Saw that off in the middle and call it 11%.

I “know” I can get 11% annualized over the long term by simply “buying the market.” THAT’S my opportunity cost when considering ANY other stock (SpaceX or otherwise).

A “perfect” DCF valuation in a perfectly efficient market would return a per share valuation that is identical to the share price at the time of the valuation exercise. In other words, if you made a perfect forecast of cash flows and discounted them at an appropriate rate, the share price would equal the calculated valuation per share.

This also means that the employed discount rate forecasts future returns.

For example, if a $100 stock is put through a “perfect” DCF process and found to be worth $100 per share, discounted at 10%, the inference is that you (the shareholder) should expect 10% returns going forward. If the same math happened with a 12% discount rate, you’d expect 12% returns going forward. At 8%, expect 8% returns.

So two exercises for the student (if you care…I suspect many won’t).

1) Recast Damodaran’s valuation using an 11% discount rate rather than his “Finance Prof’s” precisely wrong sliding scale of 8.37%-to-8.25% and tell me what the impact on calculated valuation would be (hint…it won’t be going UP).

2) If Damodaran forecast a $1.2T valuation based on that 8-handle discount rate, then at a $1.2T mkt cap, it would imply roughly 8.25% annualized returns going forward (what every SpaceX investors is, I’m sure, lining up for…measly 8% and change returns from here…wheee!)

But SpaceX doesn’t HAVE a $1.2T valuation today…it closed yesterday at about $2.1T - a 40% premium to “fair value” as per your Damodaran link.

So ask yourself , what discount rate would equate Damodaran’s cash flow forecast to the current $2.1T market value?

Hint…it will be BELOW Damodaran’s 8.25% rate…SIGNIFICANTLY s (probably in the 5.5%-to-6.0% range). And then realize, again, that that’s the de-facto expected annualized returns from here.

Good hunting!

1

1

11

1,669

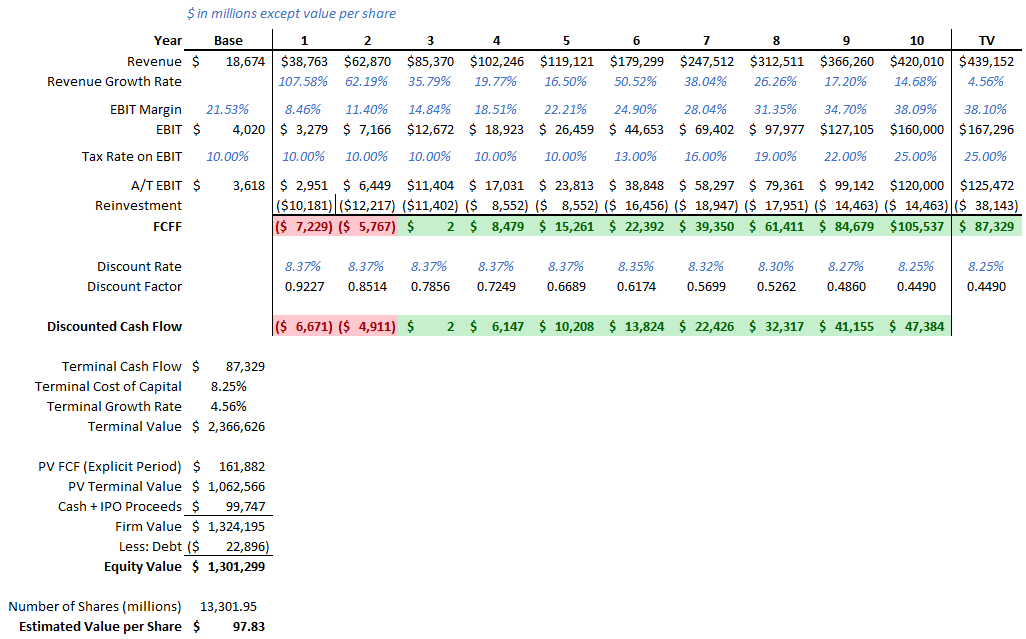

So I recast Damodaran's numbers on my own sheet which you can see below.

Now my contention is that ALL DCFs are wrong ALL of the time. This is not a shot at anyone's work, but rather an acknowledgement that we are dealing with forecasts and reality will absolutely diverge from those forecasts. (I have yet to meet an investor with perfect foresight; it certainly isn't me!)

And the more variables within a forecast, the more places where things can "go wrong" and diverge (to the upside or to the downside).

Take a look at Damodaran's revenue growth here. What if growth falls off faster than anticipated? What if it doesn't? Changes in estimated value, that's what.

Oh, and did you look further at the components of revenue growth here? Did you note how it's just Launch, Starlink, and xAI growing in the first five years of the model, and then "Other Revenues" of $20 billion show up magically in Year 6 of his forecast and increase by another $20 billion in EACH of years 7, 8, 9, and 10 (and then, of course, are PERMANENTLY entrenched in the terminal period/value...which, as you should ALSO observe is the largest component of calculated value).

I mean...what if those "Other Revenues" (what are they again?) don't show up at scale and on-time? Nothing good for the valuation, that's what. Of course, the opposite is ALSO true...if these unspecified billions of "other" revenues DO show up higher than modelled (and/or earlier than forecast) it will boost value per share; given the current enthused share price, I would suggest that investors here should really hope this is what happens.

Take a look at Damodaran's EBIT margin progression. Again, what if it doesn't progress as he forecasts? What if it does better? Again, changes in vaulation.

What if his estimated tax rate doesn't stay as low as it does in the early days? What if it stays low longer than he forecasts before the uptick? Again, the estimated value per share changes.

Move down to the lower part of the model. Notice how 80% of the "Firm Value" is in the Terminal Value? That's inherently risky - you're placing ostensibly 80% of the value of today's calculated value per share into the far unknown (i.e. 10 years out).

AND (I would again argue) you're discounting that at far too low of a discount rate (8.25%).

I saw a LOT of very intelligently-constructed and thought-out DCF models for internet companies in 1998-through-early 2000. Reality unfolded...somewhat different than expectations when the calendar turned to mid-2000 and beyond (even for those that survived and thrived - i.e. AMZN).

And there's one rather large omission I'd like to call out about Damodaran's model and that is, it makes no provision for the cost of "equity cookies" given to insiders...something that I think you'll (and everyone else) should agree with be a "non-zero" cost with a company like SpaceX.

My methodology for dealing with such is to value outstanding options with Black-Scholes (using reasonable assumptions for how many make it to actual vesting) and deduct the calculated value from "Firm Value" as something of a contingent liability akin to debt. I also boost the share count by the number of outstanding, but uninvested RSUs (again, modified by a reasonable forfeiture rate based on historical pattern).

In Damodaran's model, he effectively has this "cost" at zero (I mean, maybe it's buried in his EBIT margin assumption, but that's an accounting construct...I prefer an actual "hard" value I can deduct as that contingent liability.)

But I promise you, the value syphon from firm value into insider pockets will be (significantly) higher than zero; this is an Elon Musk company after all...if you were to compare the man's comp at Tesla to Tesla's lifetime profits, I suspect it might make you ill.

Point is, I think you ALSO need to deduct an amount/increase share count (which would result in a lower "per share" calculated value) for equity cookie "leakage" from this valuation. In other words, I think this is another place where Damodaran's model actually OVERvalues SpaceX.

But leave all that aside.

Damodaran's model calculates an equity value of just over $1.3 trillion, or $97.83 per share.

Meaning that the IPO price of $135 is at a 38% premium to what I consider to be a very generous valuation estimate by Prof. Damodaran, and that the Day 1 Closing price of $160.95 is at a 64.5% premium.

I would not consider investing into that. Feel free to holler back, "Have fun staying poor!" - it doesn't bother me. ;-)

But let's play out a couple of other scenarios.

First, if we used a uniform 11% discount rate (my "opportunity cost" choice remember), and changed nothing else about his forecast and model, equity value falls to about $685.7B with the fair value per share dropping to $51.55.

I remind you again that it closed yesterday at $160.95.

If you wanted to recast the model - again, changing nothing about his forecast or model; no contingent liabilities tied to potential dilutive "equity cookies", no margin compression or removal of the magical "Other Revenues" that show up in Year 6 - to equate the forecasted cash flows/valuatuion to the $135 IPO price, you'd need a 7.35% discount rate.

If you wanted to do so to equate it to yesterday's $160.95 closing price, you'd use a 6.93% discount rate.

And again, when share price equates to calculated value per share, the discount rate can be used as a rough approximation of expected returns going forward.

You think SpaceX investors are excited about prospective 7% returns going forward from here? I mean, I can give you a list of stocks with higher dividend yields that are probably safer...

Look, again, this is no slight on Damodaran - he's simply made an honest effort at valuing the company based on known and inferred inputs plus a healthy dose of Academic Finance methodology.

And folks who want to invest at this level...well, fair play and good luck. I genuinely wish you well.

But as to your last comment that, "anyone who owns index funds will end up owning SPCX sooner or later so they will get some exposure that way, whether they like it or not," I agree with you.

And I think that's actually tragic. I hate that Nasdaq is speed-running SpaceX inclusion. I appreciate that the S&P committee is at least sticking to their guns (for now) and requiring that SpaceX earn their place in the index the old fashioned way.

But there ARE things you can do to mitigate that, "whether they like it or not," statement.

In my family's portfolio we have roughly half our money in index-tracking ETFs and half under active management by yours truly. The index fund allocation used to be about:

* 25% TSX60 (I am Canadian, after all).

* 45% S&P500

* 25% MSCI EAFE Investible Market Index

* 5% QQQ

After word came out that Nasdaq was speed-running SPCX into QQQ I exited all QQQ and redeployed into S&P500 (there was already substantial overlap anyway so not a big deal).

I have also recently swapped about half the S&P500 exposure for an equal-weight S&P500 fund, though this is NOT so much "fear of SpaceX inclusion" and more a risk-mitgation move with the so-called "Magnificent Seven" now making up about 34% of the total weight in the index, and the overall market looking a little "enthused".

When/if SpaceX is added to the S&P500, there are also some options techniques you can use to hedge out exposure if you want to (i.e. basically set up a "synthetic short" in an amount roughly equal to the "look-through long exposure" of SpaceX...or any other company you might not want exposure to for that matter, effectively turning your S&P500 fund into an "S&P499"...just...no bitching if you get it wrong and the stock - again, SpaceX or otherwise - goes up and you're hedged out!)

One final note. I think it's worth noting that inclusion in the index ain't all it's cracked up to be.

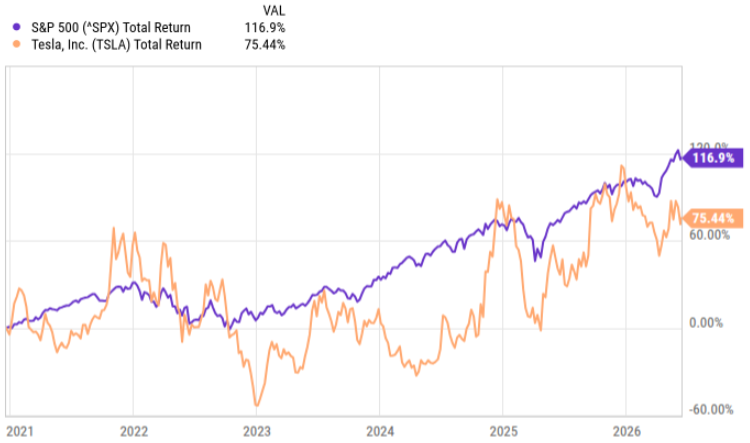

Tesla was added to the S&P500 before market open on 21-Dec-2020. I've included the total return for both Tesla and the index in the chart below. You'll note that Tesla, for all the hype, has UNDERperformed the index since inclusion; not, I think, what Tesla investors were expecting when it was originally announced as being added.

But there's another inference to be made.

If Tesla were never added to the index, the index value would be higher today. (i.e. it has underperformed the index while being a component of said index).

In other words, with Tesla included in the index, passive index investors have been treated to lower overall returns than they would have otherwise received had Tesla never been included.

I expect that the same phenomenon will occur when/if SpaceX is included in the index (and why I'll be looking again into those hedging techniques I mentioned).

Here endth the meditation. Be sure to tip your server.

3

228

A parent can feel absolutely certain. But if they publicly accuse a doctor or vaccine of causing harm without expert support, the state and the medical community can reframe it very fast:

“Or the outcome resulted from delay, noncompliance, home care issues, or neglect.”

That is exactly why expert causation matters. Without it, the accusation is not just weak, it can boomerang.

DCFS knocks and you are locked into the fight of your life over your kids.

Insults have no effect on me, just evidence.

418

Thank you for reading! Check out all of our DCFs and other stock valuations at StockWorthy.co! Sign up for free today and get a 7-day free trial of unlimited valuations!

7

2,938

It's not Trump removing these people from SNAP, it's the SNAP recipients who are too lazy to sign back up on it OR too lazy to go to their nearest DCFS center to help with food and rent.

Remember, the key words are:

Lazy, sign, back, and up

7

If I was a DCFS worker and unless a child was really in danger , I’m definitely telling you who called .

10

i’ve been working in childcare since like late march and i’m convinced that DCFS is giving me a bunch of weird minor immune diseases to test my immune system to see if i am actually able to work in childcare.

i’m holding out strong so far tho NEVER BACK DOWN!!!!!!!!!

15

lealea11 retweeted

Im.smoke joint for the statement stop tell people need treatment for Marijuana dcfs try do that to me assessor say tell them that we don't rehab fir weed ur cured u were here in 2010 I remember u smoke weed ur cured

1

1

13

Jun 13

Because her step mammy oversees cps/dcfs for DC & Bmore, her brother the assistant DA in Bmore ,her daddy (AND Chewnior daddy cuz thts her lil bro) is the top paid lobbyist for Maryland. Thts why

2

387

Jun 12

This month, DCFS celebrates Reunification Month and the children and families who have been safely brought back together. Read more: dcfs.la/rmpr26

34

Jun 12

Act 655 (HB 584) is now law, ensuring foster children in Louisiana can carry their belongings with dignity. Thank you to Rep. Boyd and our legislature for leading the way with generous bag donations. You can help by donating a bag at any DCFS office: dcfs.la.gov/offices

2

29