Jun 10

In November 2020, Chinese state-sponsored hackers known as the Hafnium group used a zero-day exploit to target flaws in Microsoft's Exchange Server software. This enabled them unauthorized access to infiltrate Covington's network, potentially viewing or exfiltrating the data of up to 298 public company clients.

The SEC demanded the names of all affected clients to investigate potential insider trading and to ensure that the impacted public companies had properly disclosed the security breach to investors but Covington pushed back.

Covington’s legal team at Gibson, Dunn & Crutcher has said the 2020 hack was aimed at a small group of lawyers and advisors to glean information about the incoming Biden administration’s policies on China.

Joe Biden had officially selected Covington & Burling as his presidential campaign counsel in July 2019.

Under Biden, Covington & Burling LLP began advising and publishing legal analysis on UAP in January 2024. Their advisement followed the enactment of the FY 2024 National Defense Authorization Act (NDAA), which was signed into law on December 22, 2023.

Stephanie Barna who Covington hired in fall 2022, wrote a newsletter published on Jan 9, 2024 stating that "given the national security exception built into the law, as well as the long lead-time for disclosure, many contractors may have good arguments to support “postponing” the release of information they believe to be sensitive or protected."

Advanced Technology International (ATI) is a public-service nonprofit that manages research and development (R&D) collaborations for the federal government.

Instead of typical federal procurement, ATI handles billions in flexible, collaborative contracts to fast-track innovation for national security. ATI serves as the single-point prime contractor for large "enterprises" where hundreds of small businesses, academic institutions, and non-traditional defense entities team up, bypassing heavy Federal Acquisition Regulation (FAR) restrictions.

"ATI builds collaborations between industry, academia, and the Department of Defense (DoD) to facilitate rapid contracting (often via Other Transaction Agreements) to help the government acquire novel technologies quickly."

ATI also manage numerous consortia for the DoD, focusing on tech like high-energy lasers, precision navigation, armaments, and directed energy. These include:

• Aviation and Missile Technology Consortium (AMTC): Focused on next-generation flight tech, including the Army's Future Tactical Unmanned Aircraft System.

• Medical CBRN Defense Consortium (MCDC): Developed to counter chemical, biological, radiological, and nuclear threats.

And contracts include:

• Space and Missile Systems ($500 Million): A prototype contract vehicle designed to minimize entry barriers for small vendors deploying space technologies

• Health Innovation (ARPA-H Hub): Selected to run the Customer Experience Hub, driving fast-tracked biomedical science and clinical trial capabilities.

In 2026, the U.S. Army tapped ATI to manage a project called GUARD. This program specifically analyzes "unpredictable" and autonomous aerial behaviors to see if they pose military risks.

Aerospace defense analysts point out that if the government wanted to hide highly sensitive, legacy aerospace programs from broad Congressional view, utilizing a private, non-profit consortium manager like ATI would be the ideal mechanism to distribute pieces of the project across hundreds of private subcontractors.

Also interesting - Guidehouse is an explicit member company of the National Armaments Consortium (NAC), which works directly in tandem with the DoD Ordnance Technology Consortium (DOTC) managed by ATI.

While Guidehouse manages global public health supply chains (such as a 10-year, $2.2 Billion USAID contract), ATI manages the domestic Defense Industrial Base Consortium (DIBC) to secure military supply chains. They routinely coordinate on industrial base data tracking.

Because both firms operate deeply in the Washington D.C. public sector space, corporate talent frequently shifts between them. For instance, senior personnel and management consultants regularly transition from specialized roles at Guidehouse into senior advisory and research analyst positions within ATI.

According to OpenSecrets federal lobbying tracking profiles, both ATI and the Pew Charitable Trusts (my prior employer) sit at the top of the non-profit advocacy bracket influencing government spending.

Both frequently participate as expert submitters to the Bipartisan Commission on Biodefense and the Hoover Institution's Biosecurity Strategy frameworks. Pew advises on the regulatory and public safety aspects of biotechnology, while ATI presents data on the defense industrial base's capacity to scale those exact medical counter-measures.

Specialized defense consultants like Sancorp routinely operate within these ATI-managed consortia networks or partner on adjacent programs funded by the Office of the Under Secretary of Defense for Intelligence and Security (OUSD(I&S)).

Sancorp Consulting, LLC holds a $4.06 million sole-source contract (Award ID: HQ003422C0094) for "AARO Support Services."

Sancorp is primarily a security and intelligence consulting firm specializing in Insider Threat Programs, identity intelligence, and counterintelligence support.

Watchdogs argue embedding a counterintelligence support team inside an office meant to receive public/military tech disclosures creates an inherently intimidating environment for potential whistleblowers.

If Sancorp or any other defense contractor were to actively retaliate against a whistleblower, it would trigger a formal investigation by the Department of Defense Office of the Inspector General (DoD OIG) and constitute a severe breach of federal law.

The All-domain Anomaly Resolution Office (AARO) relies heavily on Associated Universities, Inc. (AUI) to serve as its primary bridge to the civilian scientific community. Rather than operating purely behind closed military doors, AARO leverages AUI’s deep academic network to standardize how anomalous data is tracked, stored, and analyzed.

AARO uses AUI to build a collaborative, professional process that standardizes the study of UAPs across the Department of Defense, "moving the conversation away from conspiracy theories and toward rigorous physical science and peer-reviewed data systems."

Associated Universities, Inc. (AUI) primarily manages world-class radio astronomy observatories and cutting-edge technology development facilities under cooperative agreements with the U.S. National Science Foundation (NSF).

The primary research institutions and facilities managed by AUI include:

1. National Radio Astronomy Observatory (NRAO)

2. Atacama Large Millimeter/submillimeter Array (ALMA)

3. Green Bank Observatory (GBO)

4. Advanced Pharmaceutical & Supply Chain Incubators

AUI has expanded beyond space exploration into national biodefense and logistics. IMCA-CAT (Industrial Macromolecular Crystallography Association): A state-of-the-art research facility located at Argonne National Laboratory that AUI operates to assist pharmaceutical companies with structure-based drug design.

The laboratory is a premier hub for high-performance computing, housing the Argonne Leadership Computing Facility (ALCF). Born out of the University of Chicago's work on the World War II-era Manhattan Project, Argonne today employs thousands of scientists tasked with solving massive national challenges across clean energy, supercomputing, and national security.

Dating back to the dawn of the nuclear age in the late 1940s and 1950s, nuclear and atomic installations—including Hanford, Oak Ridge, Los Alamos, and Argonne—were the primary hotspots for military UFO reports.

When the Pentagon's AARO needs to test alleged physical UAP metal specimens or debris, they do utilize the Department of Energy’s national laboratory infrastructure. However, AARO’s primary materials testing contract was awarded to Argonne's sister site, Oak Ridge National Laboratory (ORNL), to analyze a highly publicized magnesium alloy sample.

Argonne’s Global Security Directorate directly collaborates with defense organizations to develop advanced sensor arrays, risk modeling, and predictive software.

• Argonne frequently leads DARPA-funded initiatives, utilizing its specialized cleanrooms to develop advanced microelectronics for military radar and next-generation communications systems.

• DTRA (Defense Threat Reduction Agency): Argonne engineers model tracking metrics for weapons of mass destruction, chemical dispersals, and atmospheric threats.

• OpenAI, Anthropic, Google, and Microsoft: Argonne collaborates with these frontrunners via specialized partnerships to explore how frontier AI foundation models can be securely deployed to accelerate automated scientific and physical experiments.

• Argonne remains a chief scientific advisor to the agencies that manage and police nuclear technology, such as NNSA (National Nuclear Security Administration). They collaborate closely on nuclear nonproliferation, engineering advanced detection sensors to catch the illegal movement of nuclear materials globally.

The Aurora Supercomputer, located at Argonne National Laboratory, is one of the world's most powerful exascale computing systems. Co-developed by the Department of Energy, Intel, and Hewlett Packard Enterprise (HPE), it represents the pinnacle of modern computing power.

Unlike commercial chatbots, this AI is fed billions of pages of scientific text, chemical structures, and genomic data. Its goal is to act as an autonomous scientific assistant capable of discovering new materials.

The supercomputer also does nuclear fusion modeling, running high-fidelity simulations of plasma physics, helping engineers figure out how to stabilize magnetic fusion reactors to unlock clean, limitless energy.

Because Aurora is a Department of Energy asset, a significant portion of its computing reservation is dedicated to high-level national security tasks for the NNSA. It is utilized to run complex simulations that verify the safety, security, and effectiveness of the nation's nuclear stockpile without the need for live underground nuclear testing.

Private tech and aerospace corporations lease and use computing time on the Aurora supercomputer and other systems at the Argonne Leadership Computing Facility (ALCF).

3

492

$TMC Would be good to see after-market or pre-market news of DIBC funding or other public/private investment. Something is brewing with the sudden 1 million share buys yesterday and today.

2

431

May 28

Yg cewe milih privat yg cowo milih gopub . sabar ya fat , nnti klo kiddo udh ngizinin buat ga privat lg km bsa leluasa up apapun dibc, di mana mana, dtunggu bgt pokoknya🫶🏻kta doain dr sni🤭

3

124

1,990

📢 American Lithium has been accepted into the U.S. Defense Industrial Base Consortium (DIBC) — a Department of Defense initiative focused on strengthening critical mineral supply chains and strategic resource development.

The Company’s inclusion reflects the strategic importance of its critical mineral portfolio, including the TLC Lithium Project in Nevada, as the U.S. continues prioritizing secure domestic supply chains.

🔗 americanlithiumcorp.com/amer…

$AMLI $LI.V $AMLIF #DIBC #Lithium #CriticalMinerals

1

12

366

May 25

We recently sat down with CEO Craig Hallworth of

@copper_gunnison $GCU.TO, a copper developer and producer in Arizona. We focused on the updated PEA that was released earlier this year for their flagship project, the Gunnison copper project, and the PFS work that has started. We discussed how they will secure they money to produce the PFS by Q2 2028 and strategic questions relating to that. We also talked improvements in the PFS and the potential to add resources and grow the production profile, as well as thoughts on valuation and M&A. Tune in!

/ The Team and Financial Position /

0:00 - CEO Craig Hallworth

1:58 - The Team

7:18 - Investors Buying Greenstone's 34% Equity Stake 8:56 - Royalty Buyback Agreement

14:51 - Financial Position

19:04 - Membership in DIBC

/ The Gunnison Project /

24:23 - Updated PEA

39:10 - Exploration Upside

42:22 - Peer Comparison

44:31 - Production Profile

46:37 - Potential To Add a Sulfide Concentrator

48:37 - Confidence in Cost Estimates

49:58 - Initial Capex

51:56 - Construction Period

52:24 - Limestone

56:56 - Recoveries

1:01:22 - Areas of Improvement for PFS

1:04:06 - Amount of Money Required to Raise to Get to a PFS

1:08:16 - Permitting

1:08:55 - Path To Construction

/ Johnson Mine /

1:09:48 - Update on the Johnson Mine

/ Strategy /

1:11:04 - Update on Exploration Alliance

1:12:42 - Type of Companies Interested in Gunnison 1:13:56 - Critical Items For Potential Acquirers

1:14:28 - Gunnison's Ability to Develop and Construct the Gunnison Project

1:16:34 - Catalysts for 2026

1:17:10 - Two-Year Vision For Gunnison Copper

2

3

349

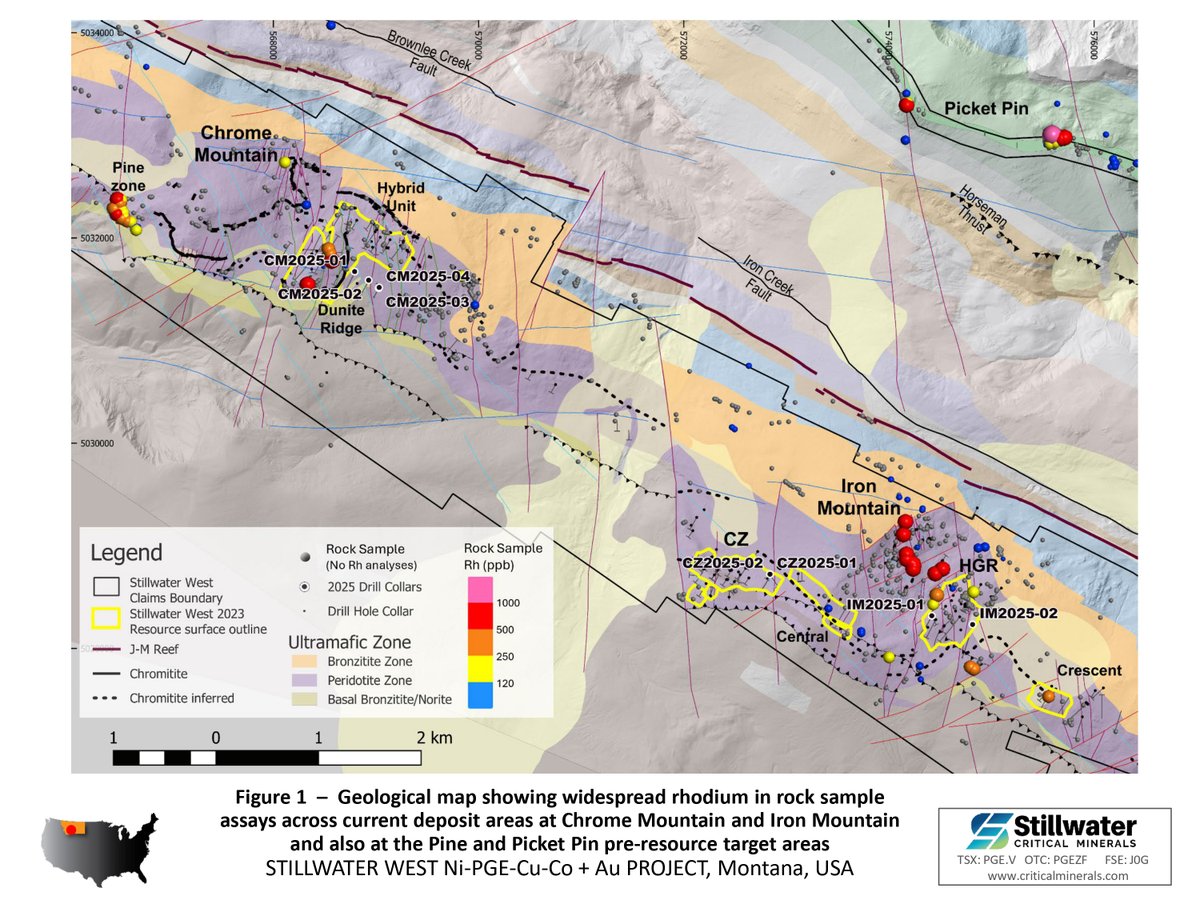

#NewsRelease Stillwater Critical Minerals reports new #rhodium assay results from the 2025 drill campaign at its 100%-owned #StillwaterWest project in #Montana, USA, highlighting the only known rhodium resource in the United States and a defined #chromium resource of 2.3 billion pounds.

New drilling continues to demonstrate widespread rhodium mineralization across the district-scale polymetallic system, with results from both the #ChromeMountain and #IronMountain resource areas supporting rhodium as a potential co-product alongside #nickel, #copper, #cobalt and #platinumgroupmetals. Results will be incorporated into the Company’s updated Mineral Resource Estimate targeted for H1 2026.

Highlights include:

• Up to 0.167 g/t Rh over 1.22m at Chrome Mountain

• 0.148 g/t Rh over 1.22m at Iron Mountain, approximately 7 km away

• Historic samples up to 5.78 g/t Rh at Iron Mountain

• 2.3 billion pounds of contained chromium defined at Stillwater West

Read the full news release: criticalminerals.com/news/20…

#CriticalMinerals #Rhodium #Chromium #Nickel #Copper #Cobalt #PGEs #Mining #MineralExploration #Montana #USA #Defense #DIBC #DOW #DOE $PGE.V $PGEZF

7

24

4,050

#NewsRelease Metallic Minerals is pleased to announce the appointments of Regina Molloy as Vice President, Exploration, Miguel Nassif as Lead Geoscientist, and Allison Coppel as Senior ESG Advisor, strengthening the Company's technical, exploration, and external relations capabilities as it advances its #LaPlata copper-silver-gold-PGE #criticalminerals project in #Colorado and its #KenoSilver project in #Yukon.

The appointments add senior leadership and specialized technical expertise in global mineral exploration, structural geology, project targeting, ESG strategy, and community engagement, with prior experience spanning leading mining companies including BHP, Newmont Corporation, Equinox Gold, and Agnico Eagle Mines, as the Company advances both projects toward key 2026 milestones.

Members of the Metallic Minerals management team, including Ms. Molloy, will be attending the #WesternMiningSummit in Denver, Colorado from May 20-22, 2026, where the Company looks forward to meeting with investors, stakeholders, Colorado state officials, and U.S. congressional representatives.

Learn more about our fantastic new additions here: metallic-minerals.com/news/2…

#MineralExploration #Team #CommunityEngagement #Copper #Silver #Gold #Platinum #Palladium #Hafnium #Zirconium #Scandium #DIBC #DOE $MMG.V $MMNGF

1

10

937

May 18

keren bgt ih aktif bgt dibc pengen si ngerasain kek gini huhu jadi perjuangannya tu kerasa bgt🥹🫰alias beneran aktif dan dari OFC nya juga gerak jadi ga hilang arah mau ngapain alias tearah. love it😗🫰 Lancar lancar ya the nabss rispek☺️🤝

3

189

$GRL has been accepted into the U.S. DIBC, providing engagement with the U.S. DoD via OTA frameworks, R&D programs and funding pathways in #criticalminerals and #rareearths.

Narraburra has produced two MREC samples enriched in heavy #REEs.

➡️godolphinresources.com.au/do…

1

2

175

$GRL has been accepted into the U.S. DIBC, providing engagement with the U.S. DoD via OTA frameworks, R&D programs and funding pathways in #criticalminerals and #rareearths.

Narraburra has produced two MREC samples enriched in heavy #REEs.

➡️godolphinresources.com.au/do…

1

3

162

May 15

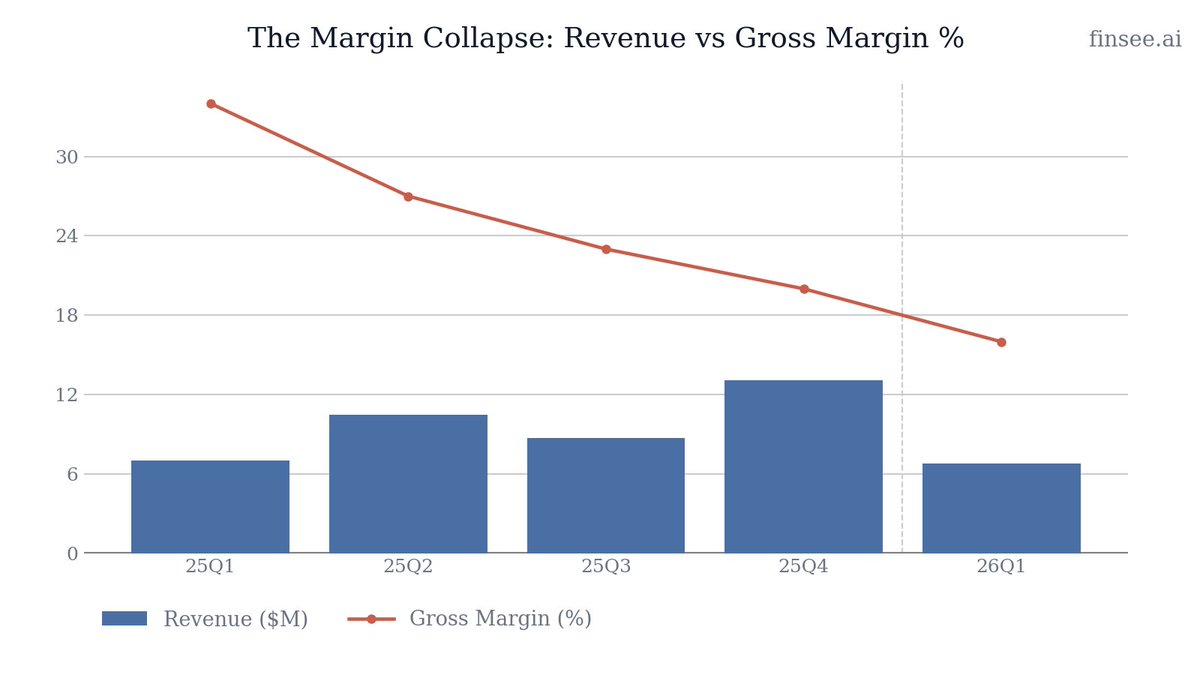

$UAMY Q1 2026 earnings: Antimony Prices Rise 22%. Margins Crash to 16%.

*** Updated after the call:

Q1 was supposed to be the quarter where in-house ore drove margin expansion - that was management's promise on the November call. Instead, gross margin compressed to 16.4% from 33.9% a year ago, the fifth consecutive quarterly decline. Revenue was flat at $6.8M as antimony pounds sold fell 23%, offsetting a 22% rise in selling price per pound. The real problem is on the cost side: cost per pound jumped 69%, more than three times the price gain. Operating expenses quadrupled to $8.6M, including $4.8M of stock-based compensation - 20x last year's level. Net loss reached $11.3M, with $9.3M of that classified as non-cash items. Pro forma liquidity is $108.7M after a $48.6M post-quarter equity raise (4.2M shares at $11.57). Management reiterated $125M FY26 revenue guidance - which requires Q2-Q4 to average $39.4M each, or 5.8x the Q1 run-rate.

Full article with charts - link in bio

🐂 𝗕𝘂𝗹𝗹 𝗖𝗮𝘀𝗲

𝗗𝗟𝗔 𝗖𝗼𝗻𝘁𝗿𝗮𝗰𝘁 𝗙𝗶𝗻𝗮𝗹𝗹𝘆 𝗔𝗰𝘁𝗶𝘃𝗮𝘁𝗶𝗻𝗴: First two delivery notices given under the $245M DLA contract; $12M in sales orders received. Management now expects $75M-$95M of FY26 revenue from federal government antimony ingot shipments alone.

𝗩𝗲𝗿𝘁𝗶𝗰𝗮𝗹 𝗜𝗻𝘁𝗲𝗴𝗿𝗮𝘁𝗶𝗼𝗻 𝗔𝘀𝘀𝗲𝘁𝘀 𝗡𝗼𝘄 𝗜𝗻 𝗣𝗹𝗮𝗰𝗲: Radersburg flotation mill acquired ($4.8M) and operational, with new lab nearly complete. Bolivia hydromet partner producing metallic antimony flake, with first shipment in transit to Thompson Falls. Stibnite Hill mine ready to resume hauling pending Montana DEQ leach-plan approval.

🐻 𝗕𝗲𝗮𝗿 𝗖𝗮𝘀𝗲

𝗠𝗮𝗿𝗴𝗶𝗻 𝗖𝗼𝗺𝗽𝗿𝗲𝘀𝘀𝗶𝗼𝗻 𝗜𝘀 𝗡𝗼𝘄 𝗮 𝗙𝗶𝘃𝗲-𝗤𝘂𝗮𝗿𝘁𝗲𝗿 𝗧𝗿𝗲𝗻𝗱: Gross margin: 34% -> 27% -> 23% -> 20% -> 16%. Management explicitly promised 'significant margin expansion' in Q1 26 driven by in-house ore (on the Q3 25 call). Reality moved in the opposite direction. The thesis that domestic ore unlocks 60% margins remains entirely unproven.

𝗦𝗲𝘃𝗲𝗿𝗲 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗻𝗴 𝗟𝗲𝘃𝗲𝗿𝗮𝗴𝗲 𝗣𝗿𝗼𝗯𝗹𝗲𝗺: Revenue was flat YoY, but operating expenses grew 328% ($2.0M -> $8.6M). Even excluding the $4.8M of SBC, cash operating expenses roughly doubled. The cost base has been built for a much larger company that does not yet exist.

$𝟭𝟮𝟱𝗠 𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲 𝘃𝘀. $𝟲.𝟴𝗠 𝗤𝟭 𝗥𝘂𝗻-𝗥𝗮𝘁𝗲: Hitting $125M requires Q2-Q4 to average $39.4M - 5.8x the Q1 quarterly rate, and higher than the entire FY25 of $39.3M. Thompson Falls won't reach full nameplate (230 tons/month) until late July. CEO Evans openly told investors quarters will be 'bumpy.'

⚖️ 𝗩𝗲𝗿𝗱𝗶𝗰𝘁

🔴 Bearish. The Q1 data flatly contradicts the most important plank of the bull thesis - that vertical integration drives margin expansion. Instead, margins compressed further, the cost base ballooned, and the cash position was rescued by another round of dilution. The $125M guidance is now mathematically dependent on near-perfect H2 execution across Thompson Falls commissioning, Alaska mining, DLA deliveries, and Bolivia ramp - simultaneously.

— • — • —

𝗧𝗵𝗲𝗺𝗲𝘀

New: 🔴🔴 𝗠𝗮𝗿𝗴𝗶𝗻 𝗘𝘅𝗽𝗮𝗻𝘀𝗶𝗼𝗻 𝗣𝗿𝗼𝗺𝗶𝘀𝗲 𝗙𝗮𝗶𝗹𝘀 - 𝗖𝗼𝘀𝘁𝘀 𝗢𝘂𝘁𝗿𝘂𝗻 𝗣𝗿𝗶𝗰𝗲𝘀

The most important data point this quarter: antimony selling price per pound rose 22% to $19.92, while cost per pound rose 69% to $16.28. Gross profit per pound fell from $6.68 to $3.64 - a 46% decline despite record-high antimony prices. This directly contradicts the Q3 25 call commitment that Q1 26 would show 'significant margin expansion' from in-house ore. Management blames 'higher-cost ore moving through cost of sales' - meaning Q1 26 reflects expensive third-party feedstock purchased through 2025, with zero contribution yet from Montana mining or DLA-priced shipments.

New: 🔴 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗻𝗴 𝗘𝘅𝗽𝗲𝗻𝘀𝗲 𝗕𝗮𝘀𝗲 𝗕𝘂𝗶𝗹𝘁 𝗳𝗼𝗿 𝗮 𝗠𝘂𝗰𝗵 𝗟𝗮𝗿𝗴𝗲𝗿 𝗖𝗼𝗺𝗽𝗮𝗻𝘆

Operating expenses quadrupled YoY: salaries and benefits went from $1.0M to $5.9M (with $4.8M of that being stock-based compensation, vs. just $0.25M a year ago), professional fees from $0.4M to $1.3M, G&A from $0.55M to $1.33M. The $4.8M of SBC reflects equity grants tied to leadership hires and share-price appreciation. Even stripped of SBC, cash operating expenses roughly doubled. Management argues this scaffolding is necessary for H2 ramp - but the run-rate now requires significant revenue growth just to break even on cash operating costs.

🔴 𝗟𝗮𝗿𝘃𝗼𝘁𝘁𝗼 𝗣𝗼𝘀𝗶𝘁𝗶𝗼𝗻 𝗥𝗲𝗺𝗮𝗶𝗻𝘀 𝗦𝘁𝗿𝗮𝗻𝗱𝗲𝗱 - 𝗮𝗻𝗱 𝗩𝗼𝗹𝗮𝘁𝗶𝗹𝗲

USAC invested $37.2M for ~10% of Larvotto Resources in late 2025 with intent to take it over; the bid was rejected. Q1 included a $4.1M unrealized mark-to-market loss on the position (carried at $36.4M at quarter-end). The stock has since recovered to $46.6M as of May 13. Management on the call said dialogue with Larvotto's board has gone 'absolutely nowhere' and they are now actively evaluating selling the stake on the open market or to a buyer. CEO Evans cited concern about 10% Chinese ownership and a Chinese marketing agreement. This represents one of the largest capital allocations in company history sitting in suspended animation.

🔴 𝗧𝗵𝗼𝗺𝗽𝘀𝗼𝗻 𝗙𝗮𝗹𝗹𝘀 𝗘𝘅𝗽𝗮𝗻𝘀𝗶𝗼𝗻 - 𝗡𝗼𝘄 𝗣𝗵𝗮𝘀𝗲𝗱 𝗖𝗼𝗺𝗺𝗶𝘀𝘀𝗶𝗼𝗻𝗶𝗻𝗴 𝗧𝗵𝗿𝗼𝘂𝗴𝗵 𝗝𝘂𝗹𝘆

VP Jeffrey Fink walked through a notably more granular timeline: three of nine furnaces can run at 50% capacity now with fabricated parts; OEM heat exchanger parts begin arriving last week of May and continue arriving weekly; all 9 furnaces operational near mid-July. Even at full ramp, management expects only ~80% of nameplate capacity by end of July due to operator learning curve. New plant capacity is 230 tons/month; old plant (which must be shut down for emissions upgrades after new plant stabilizes) is 75 tons/month. The four-to-eight week old-plant shutdown for emissions retrofit will further constrain throughput. The chain of dependencies on third-party equipment makers continues to push timelines: this is now ~6 months behind the original year-end 2025 target.

New: 🟢 𝗗𝗟𝗔 𝗖𝗼𝗻𝘁𝗿𝗮𝗰𝘁 𝗘𝘅𝗲𝗰𝘂𝘁𝗶𝗼𝗻 𝗕𝗲𝗴𝗶𝗻𝘀 - $𝟳𝟱𝗠-$𝟵𝟱𝗠 𝗙𝗬𝟮𝟲 𝗧𝗮𝗿𝗴𝗲𝘁

First two delivery notices have been issued under the $245M sole-source DLA contract. $12M in sales orders received to date. CEO Evans now expects $75M-$95M of FY26 revenue from federal antimony ingot shipments - 60-76% of the $125M full-year target. Government inspection of initial deliveries is underway. The DLA orders carry serial-number stamping requirements and specific packaging, which the company has now built capabilities for. This is the single most important variable in the FY26 outlook.

New: 🟢 𝗜𝗻𝘃𝗲𝗻𝘁𝗼𝗿𝘆 𝗕𝘂𝗶𝗹𝘁 𝗦𝗽𝗲𝗰𝗶𝗳𝗶𝗰𝗮𝗹𝗹𝘆 𝗳𝗼𝗿 𝗛𝟮 𝗥𝗮𝗺𝗽

Antimony inventory grew 503% YoY and 81% sequentially, to $21.7M ($22.0M total inventory). The Madero smelter is receiving ~225 tons/month of high-quality feedstock under consolidated supply contracts. Bolivian partner has commissioned processing circuits and shipped first metallic antimony flake to Thompson Falls. This is the physical raw material needed to deliver against DLA orders and reach the 500 tons/month target. The flip side: $9.7M of operating cash was consumed in this inventory build during Q1 alone.

New: 🟢 𝗭𝗲𝗼𝗹𝗶𝘁𝗲 𝗖𝗮𝘁𝘁𝗹𝗲 𝗡𝘂𝘁𝗿𝗶𝘁𝗶𝗼𝗻 𝗛𝗶𝘁𝘁𝗶𝗻𝗴 𝗜𝗻𝗳𝗹𝗲𝗰𝘁𝗶𝗼𝗻

Bear River Zeolite shipped record monthly tonnage in March (42% above target) and again in April (66% above target). Both months were all-time records. Demand from cattle nutrition customers is now outpacing existing infrastructure, prompting phased capacity and automation upgrades. Two new cattle nutrition customers signed in the two weeks before the call; more in discussion. Management notes beef prices at all-time highs are driving cattlemen toward feed-efficiency additives. Q1 zeolite revenue was still down (~7% YoY) as the segment's record months were March and April - meaning meaningful financial impact won't appear until Q2.

⚪ 𝗚𝗼𝘃𝗲𝗿𝗻𝗺𝗲𝗻𝘁 𝗙𝘂𝗻𝗱𝗶𝗻𝗴 𝗣𝗶𝗽𝗲𝗹𝗶𝗻𝗲 𝗖𝗼𝗻𝘁𝗶𝗻𝘂𝗲𝘀 𝘁𝗼 𝗘𝘅𝗽𝗮𝗻𝗱

Of the $27M Department of War (DoW) award, $12.8M was recognized as a grant receivable in Q1 (received as cash in April). Under newly adopted ASU 2025-10, the $12.8M reduces the carrying value of construction-in-progress for Thompson Falls rather than flowing through revenue or income - lowering future depreciation. Management has $274M in additional federal grant applications filed: $44M Department of Energy for hydromet; $5M DIBC for tungsten exploration; $105M for tungsten/hydromet domestic supply; $119M for a hydromet critical minerals concentrator. First DOE response expected in 45-60 days.

New: ⚪ 𝗧𝘂𝗻𝗴𝘀𝘁𝗲𝗻 𝗥𝗲𝘀𝗼𝘂𝗿𝗰𝗲 𝗥𝗲-𝗩𝗮𝗹𝘂𝗲𝗱 𝗮𝘁 𝗖𝘂𝗿𝗿𝗲𝗻𝘁 𝗣𝗿𝗶𝗰𝗲𝘀

The SK-1300 technical report filed in April disclosed inferred resources of 14.62M metric tons at 0.17% WO3, containing 53.595M lbs of tungsten trioxide. At the TRS assumed prices, the gross resource value is $4.6B; on the call, EVP Bardswich said at today's tungsten price ($3,300/metric ton unit), the gross value would be approximately $9.3B. First Nations blessing ceremony pending to begin operations. Bulk sample of 20,000-50,000 tons targeted for processing at a local Sudbury-area mill, with concentrate shipped to a Pennsylvania ammonium-paratungstate processor. Management was direct that no meaningful tungsten revenue expected in 2026.

— • — • —

𝗢𝘁𝗵𝗲𝗿 𝗞𝗣𝗜𝘀

𝗔𝗻𝘁𝗶𝗺𝗼𝗻𝘆 𝗣𝗼𝘂𝗻𝗱𝘀 𝗦𝗼𝗹𝗱 (𝗤𝟭 𝟮𝟲): 𝟮𝟳𝟴,𝟳𝟵𝟳 𝗹𝗯𝘀 (-𝟮𝟯% 𝗬𝗼𝗬)

Volume decline overwhelmed price gains. Management attributed the drop to 'timing of customer orders and shipments' and stated explicitly that none of the Q1 volume went to the government - i.e., zero DLA deliveries recognized in Q1. The volume number is the most concrete indicator that DLA-driven revenue ramp has not yet begun, with deliveries starting only in Q2.

𝗖𝗮𝘀𝗵, 𝗧𝗿𝗲𝗮𝘀𝘂𝗿𝗶𝗲𝘀 & 𝗘𝗾𝘂𝗶𝘁𝘆 𝗦𝗲𝗰𝘂𝗿𝗶𝘁𝗶𝗲𝘀 (𝗤𝟭 𝟮𝟲): $𝟲𝟬.𝟮𝗠 (𝗤𝟭 𝗺𝗮𝗿𝗸); $𝟭𝟬𝟴.𝟳𝗠 𝗽𝗿𝗼 𝗳𝗼𝗿𝗺𝗮

Breakdown at March 31: $3.2M cash $20.5M HTM Treasuries $36.4M Larvotto equity stake. Pro forma for the $48.6M post-quarter equity raise (4.2M shares at $11.57), liquidity is $108.7M. Larvotto stake further appreciated to $46.6M by May 13. A $19M undrawn margin credit facility provides additional capacity. The optical liquidity is healthy but is entirely a function of capital markets activity, not operations - $24.6M of free cash was burned in Q1 alone.

𝗙𝗿𝗲𝗲 𝗖𝗮𝘀𝗵 𝗙𝗹𝗼𝘄 (𝗤𝟭 𝟮𝟲): -$𝟮𝟰.𝟲𝗠

Operating cash use was $12.1M, driven primarily by a $9.7M inventory build. Capex of $12.6M included $4.8M for the Radersburg flotation mill acquisition, $4.6M for Thompson Falls construction-in-progress, and $3.2M for new mineral rights acquisitions. The DoW grant recognition of $12.8M (received as cash in April) will offset roughly half of the Thompson Falls capex retrospectively but does not change the Q1 cash flow optics. Shareholder dilution remains the primary funding source: 4.2M shares issued post-quarter on top of 24% dilution already absorbed in 2025.

𝗡𝗲𝘁 𝗟𝗼𝘀𝘀 𝗖𝗼𝗺𝗽𝗼𝘀𝗶𝘁𝗶𝗼𝗻 (𝗤𝟭 𝟮𝟲): -$𝟭𝟭.𝟯𝗠 (𝗶𝗻𝗰𝗹. $𝟵.𝟯𝗠 𝗻𝗼𝗻-𝗰𝗮𝘀𝗵)

Of the $11.3M net loss, $4.8M was stock-based compensation, $4.1M was unrealized mark-to-market loss on the Larvotto position, and $0.4M was D&A. The underlying cash operating loss was roughly $2.0M - still well below break-even but smaller than the headline suggests. The SBC line item deserves particular attention: it grew nearly 20x YoY, reflecting equity grants tied to share-price appreciation. As long as the stock appreciates and grants vest, SBC will continue to be a meaningful drag on reported earnings.

— • — • —

𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲

𝗙𝗬𝟮𝟲 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: $𝟭𝟮𝟱𝗠 (𝗿𝗲𝗶𝘁𝗲𝗿𝗮𝘁𝗲𝗱)

Stable vs prior. Implies ~218% growth over FY25's $39.3M. Q1 came in at $6.8M, leaving $118.2M to deliver in Q2-Q4 - a quarterly average of $39.4M, or 5.8x the Q1 run-rate. Management acknowledged the back-half loading explicitly and warned of 'bumpy' quarters. CEO Evans now expects $75M-$95M from federal DLA antimony ingot shipments, which would be 60-76% of the total. The guidance survival depends on: (1) Thompson Falls reaching ~80% nameplate by late July, (2) Bolivia flake flowing to Thompson Falls consistently, (3) DLA acceptance of delivered ingots, and (4) Stibnite Hill resuming operations once Montana DEQ approves the leach-test mitigation plan in the next two weeks.

𝗧𝗵𝗼𝗺𝗽𝘀𝗼𝗻 𝗙𝗮𝗹𝗹𝘀 𝗦𝗺𝗲𝗹𝘁𝗲𝗿 𝗖𝗼𝗺𝗺𝗶𝘀𝘀𝗶𝗼𝗻𝗶𝗻𝗴: 𝗣𝗵𝗮𝘀𝗲𝗱 𝘁𝗵𝗿𝗼𝘂𝗴𝗵 𝗺𝗶𝗱-𝗝𝘂𝗹𝘆 𝟮𝟬𝟮𝟲

Reversing/Decelerating from prior guidance. Original target was year-end 2025; pushed to January 2026; then to May 2026; now phased through mid-July. Three furnaces can operate at 50% capacity now with fabricated parts; remaining six furnaces commissioned weekly through May-July as OEM heat exchanger parts arrive. Even at full ramp, only ~80% of nameplate (230 tons/month new plant capacity) expected by late July. The old plant (75 tons/month) must then be shut down 4-8 weeks for emissions retrofit. This effectively eliminates Q2 as a meaningful ramp quarter.

𝗙𝗲𝗱𝗲𝗿𝗮𝗹 𝗚𝗿𝗮𝗻𝘁 𝗣𝗶𝗽𝗲𝗹𝗶𝗻𝗲: $𝟮𝟳𝟰𝗠 𝗶𝗻 𝗽𝗲𝗻𝗱𝗶𝗻𝗴 𝗮𝗽𝗽𝗹𝗶𝗰𝗮𝘁𝗶𝗼𝗻𝘀

Filed but pending decisions: $44M DOE hydromet (filed January, answer expected 45-60 days); $5M DIBC tungsten exploration; $105M tungsten/hydromet domestic supply; $119M hydromet critical minerals concentrator. The remaining $14.2M of the existing $27M DoW award is gated: $8M expected during 2026 as Thompson Falls commissioning milestones are completed; $7M for Alaska tied to 2027 deployment due to environmental requirements. Grants reduce PP&E carrying value rather than flowing through revenue.

— • — • —

𝗞𝗲𝘆 𝗤𝘂𝗲𝘀𝘁𝗶𝗼𝗻𝘀

𝗤𝘂𝗮𝗿𝘁𝗲𝗿𝗹𝘆 𝗥𝗲𝘃𝗲𝗻𝘂𝗲 𝗧𝗿𝗮𝗷𝗲𝗰𝘁𝗼𝗿𝘆 𝘁𝗼 $𝟭𝟮𝟱𝗠

Given Thompson Falls won't reach 80% of nameplate until late July, and the old plant must then be shut down for 4-8 weeks for emissions retrofit, how does revenue actually phase across Q2, Q3, and Q4? What is the minimum acceptable Q2 number that keeps full-year guidance on the table?

𝗗𝗼𝗺𝗲𝘀𝘁𝗶𝗰 𝗢𝗿𝗲 𝗠𝗮𝗿𝗴𝗶𝗻𝘀 - 𝗛𝗮𝗿𝗱 𝗡𝘂𝗺𝗯𝗲𝗿𝘀 𝗥𝗲𝗾𝘂𝗶𝗿𝗲𝗱

Management has claimed 60% gross margins from in-house ore for over a year, yet not a single ton has flowed through P&L. With Stibnite Hill set to resume hauling in the next two weeks, what is the actual all-in cost per pound of domestic ore vs. the $16.28 third-party Q1 cost? When in 2026 does in-house ore start showing up in cost of sales?

𝗟𝗮𝗿𝘃𝗼𝘁𝘁𝗼 𝗥𝗲𝘀𝗼𝗹𝘂𝘁𝗶𝗼𝗻 𝗮𝗻𝗱 𝗖𝗮𝗽𝗶𝘁𝗮𝗹 𝗥𝗲𝗰𝘆𝗰𝗹𝗶𝗻𝗴

The 10% Larvotto stake is now worth $46.6M (up $10.2M post-quarter). With dialogue described as going 'absolutely nowhere' and a stated openness to selling, what is the timeline? If sold near current value, the $37.2M investment would return roughly $9M after a year of work - what would that capital be redeployed into?

𝗦𝘁𝗼𝗰𝗸-𝗕𝗮𝘀𝗲𝗱 𝗖𝗼𝗺𝗽𝗲𝗻𝘀𝗮𝘁𝗶𝗼𝗻 𝗥𝘂𝗻-𝗥𝗮𝘁𝗲

Q1 SBC was $4.8M, an annualized rate of $19M against $39M of FY25 revenue. Are these grants front-loaded with the leadership build-out, or should investors model this magnitude of SBC continuing through 2026 and 2027? At what stock price do additional grants get triggered?

𝗗𝗟𝗔 𝗖𝗼𝗻𝘁𝗿𝗮𝗰𝘁 𝗣𝗿𝗶𝗰𝗶𝗻𝗴 𝗦𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗲

Under what pricing structure are deliveries made - fixed price, market-indexed, or cost-plus? If antimony prices decline in 2026, does the DLA contract economics shift materially? What is the assumed gross margin on the $75M-$95M of DLA shipments embedded in FY26 guidance?

May 14

$UAMY Q1 2026 earnings: Massive Ambitions Masking Severe Operational Contraction

United States Antimony's Q1 2026 results present a stark disconnect between management's 'warp speed' narrative and operational reality. Despite boasting about government contracts and future riches, actual revenue is Reversing, falling to $6.8M YoY. More alarmingly, the company has suffered a persistent, five-quarter collapse in profitability, with gross margins Decelerating from 34% a year ago to just 16% today due to soaring third-party ore costs. Operating expenses are Accelerating drastically, fueled by an astounding $4.8M in executive share-based compensation on just $6.8M of sales. While the post-quarter $48.6M capital raise and $12.8M Department of War (DoW) grant milestone provide a massive liquidity bridge, management's reiterated $125M full-year revenue guidance requires a near-impossible vertical ramp in the remaining three quarters.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐆𝐨𝐯𝐞𝐫𝐧𝐦𝐞𝐧𝐭 𝐂𝐡𝐞𝐜𝐤𝐛𝐨𝐨𝐤 𝐢𝐬 𝐎𝐩𝐞𝐧 — The company successfully recognized a $12.8M DoW grant milestone and issued its first two delivery notices under the massive $245M Defense Logistics Agency (DLA) contract. National security mandates provide a uniquely captive customer base.

• 𝐏𝐫𝐨 𝐅𝐨𝐫𝐦𝐚 𝐖𝐚𝐫 𝐂𝐡𝐞𝐬𝐭 — Subsequent to the quarter, USAC raised $48.6M at an average of $11.57/share. Combined with cash, Treasuries, and marketable securities, total liquidity sits at a highly defensive $108.7M.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐂𝐨𝐫𝐞 𝐌𝐚𝐫𝐠𝐢𝐧𝐬 𝐄𝐯𝐚𝐩𝐨𝐫𝐚𝐭𝐢𝐧𝐠 — Gross margin has systematically compressed every quarter for the last year. The cost of sold antimony skyrocketed 69% YoY to $16.28/lb, completely wiping out the 22% increase in average realized sales prices.

• 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞 𝐃𝐞𝐟𝐢𝐞𝐬 𝐆𝐫𝐚𝐯𝐢𝐭𝐲 — Maintaining the $125M full-year revenue target requires averaging over $39M per quarter for the rest of the year—nearly six times the $6.8M delivered in Q1. The execution risk here is extreme.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🔴

Bearish. The long-term geopolitical thesis for domestic critical minerals is ironclad, but USAC is currently bleeding cash, paying massive executive stock comp, and struggling to process profitable ore. They are buying time with equity raises.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🔴🔴 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐄𝐱𝐩𝐞𝐧𝐬𝐞𝐬 𝐑𝐮𝐧 𝐀𝐦𝐨𝐤 [NEW]

Operating expenses are Accelerating aggressively, jumping from $2.0M in 25Q1 to $8.6M in 26Q1. The primary culprit is $4.8M in non-cash share-based compensation (compared to $0.25M a year ago). When a company prints $6.8M in revenue but issues $4.8M in equity to its leadership, it flags a concerning misalignment between operational output and executive reward.

🔴 𝐀𝐧𝐭𝐢𝐦𝐨𝐧𝐲 𝐔𝐧𝐢𝐭 𝐄𝐜𝐨𝐧𝐨𝐦𝐢𝐜𝐬 𝐚𝐫𝐞 𝐁𝐫𝐨𝐤𝐞𝐧 [NEW]

The core operational metric is Reversing. Despite the average sales price of antimony rising 22% to $19.92 per pound, the cost per pound spiked a staggering 69% to $16.28. Management blames higher-cost third-party ore moving through cost of sales. Until the company can process its own mined ore from Montana, it is caught in a structurally unprofitable squeeze.

🟢 𝐕𝐞𝐫𝐭𝐢𝐜𝐚𝐥 𝐈𝐧𝐭𝐞𝐠𝐫𝐚𝐭𝐢𝐨𝐧 𝐌𝐢𝐥𝐞𝐬𝐭𝐨𝐧𝐞𝐬

The company's lifeline is its pivot to domestic processing to fix its broken margin profile. The $4.8M acquisition of the Radersburg flotation mill and the near-completion of the Thompson Falls smelter expansion are critical drivers. Management states these facilities will begin processing in-house ore later this year, which is the only visible path to returning to 30% gross margins.

🟢🟢 𝐃𝐞𝐩𝐚𝐫𝐭𝐦𝐞𝐧𝐭 𝐨𝐟 𝐖𝐚𝐫 𝐂𝐚𝐬𝐡 𝐈𝐧𝐣𝐞𝐜𝐭𝐢𝐨𝐧 [NEW]

USAC successfully cleared three project milestones to unlock $12.8M out of its $27M DoW grant. Because of new accounting standards (ASU 2025-10), this doesn't boost revenue; instead, it reduces the cost basis of the Thompson Falls construction. This non-dilutive federal capital acts as a heavy counterbalance to the company's severe operating cash burn (-$12.1M in Q1).

🔴 𝐋𝐚𝐫𝐯𝐨𝐭𝐭𝐨 𝐑𝐞𝐬𝐨𝐮𝐫𝐜𝐞𝐬 𝐈𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭 𝐃𝐫𝐚𝐠𝐬 𝐄𝐚𝐫𝐧𝐢𝐧𝐠𝐬 [NEW]

In addition to operating struggles, below-the-line items crushed Net Income. USAC recorded a $4.1M unrealized loss on its investment in marketable equity securities (Larvotto Resources Limited). While management points to a post-quarter rebound in the stock, playing the public equity markets introduces unwanted volatility to a company already managing extreme execution risk in heavy industry.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐓𝐨𝐭𝐚𝐥 𝐋𝐢𝐪𝐮𝐢𝐝𝐢𝐭𝐲 (𝐏𝐫𝐨 𝐅𝐨𝐫𝐦𝐚): $108.7 million

Accelerating significantly. Base Q1 liquidity was $23.7M (Cash Treasuries). By aggressively tapping the equity market post-quarter, they raised $48.6M at an average of $11.57 per share. Combining cash, U. S. Treasuries, and the Larvotto equity position, management has secured enough runway to complete infrastructure build-outs regardless of near-term operating losses.

𝐀𝐧𝐭𝐢𝐦𝐨𝐧𝐲 𝐈𝐧𝐯𝐞𝐧𝐭𝐨𝐫𝐲 𝐕𝐚𝐥𝐮𝐞: $21.7 million

Accelerating. Up 80.8% sequentially from $12.0M at the end of 2025, and up over 500% YoY. The company is hoarding feedstock (both third-party and owned Stibnite Hill ore) ahead of the Thompson Falls smelter commissioning. Working capital is entirely tied up in this stockpile.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐅𝐘𝟐𝟔 𝐆𝐫𝐨𝐬𝐬 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $125.0 million

Accelerating expectation, but heavily scrutinized. Reiterating this guidance means management is implicitly promising to generate roughly $118.2 million in the remaining three quarters (average ~$39.4M/quarter). Given Q1 generated just $6.8M, this assumes a flawless launch of the expanded Thompson Falls smelter and immediate, massive DLA deliveries.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐓𝐡𝐞 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞 𝐌𝐚𝐭𝐡

Reiterating $125M in revenue after a $6.8M first quarter means you need to average nearly $40M per quarter for the rest of the year. Can you walk us through the exact month-by-month volume ramp and facility commissioning schedule that makes this mathematically possible?

𝐌𝐚𝐫𝐠𝐢𝐧 𝐓𝐫𝐨𝐮𝐠𝐡

Gross margins have compressed from 34% a year ago to 16% today due to third-party ore costs reaching $16.28/lb. When exactly do you expect internally mined ore to cross the threshold where it materially reverses this margin decay?

𝐒𝐭𝐨𝐜𝐤-𝐁𝐚𝐬𝐞𝐝 𝐂𝐨𝐦𝐩𝐞𝐧𝐬𝐚𝐭𝐢𝐨𝐧 𝐑𝐞𝐬𝐭𝐫𝐚𝐢𝐧𝐭

The company issued $4.8M in stock-based compensation to leadership during a quarter where total revenue was only $6.8M and operating losses ballooned. What specific performance metrics govern these equity grants, and why are they accelerating while volume and margins are contracting?

1

1

8

4,288

May 15

🚨 American tool & mold files for chapter 11 protection in florida

AMERICAN TOOL & MOLD, INC.

📊 Assets: $1M-$10M | Liabilities: $1M-$10M | Creditors: 1-49 | Industry: Industrial Mold Manufacturing | District: Middle District of Florida

Chapter 11 – Filing Summary

_____________________________________________

Middle District of Florida • May 15, 2026

American Tool & Mold, Inc., a Clearwater, FL-based industrial mold manufacturer, filed for chapter 11 protection on May 15, 2026 in the Middle District of Florida.

As of May 2026, the company operates as a precision manufacturer specializing in multi-cavity mold manufacturing, liquid silicone rubber, and clean room molding. The firm maintains an active role in the defense industrial base and was recently recognized as a top domestic injection molding company for the 2025 fiscal year.

Key Details

_____________________________________________

– 200 associates employed as of May 2026 [Source: American Tool & Mold Official Website (2026)]

– Ranked as a top 100 injection molding company for the 2025 fiscal year [Source: Kemal Manufacturing Industry Report (2025)]

– Maintained active membership in the Defense Industrial Base Consortium as of April 2026 [Source: DIBC Member List (2026)]

– Specialized in liquid silicone rubber and clean room molding services as of May 2026 [Source: Thomasnet News Release (2026)]

Industrial Mold Manufacturing: NAICS 333511 – Industrial Mold Manufacturing. The company designs and manufactures high-precision multi-cavity injection molds for various industrial sectors.

⚖️ Professionals

_____________________________________________

Debtor's Counsel: Hahn Loeser and Parks LLP

#Bankruptcy #Chapter11 #Manufacturing

*Data from court filings & verified sources. All sources should require independent verification. Not financial advice.

ch11.ai/filing-detail/226_bk…

2

173

May 14

American Tungsten & Antimony Ltd

(ASX: $AT4 | OTCQB: $ATALF)

With a robust cash position confirmed in the latest quarterly and multiple Department of Defense funding applications now under review through DIBC membership, American Tungsten & Antimony Ltd enters the coming months execution-ready.

Key upcoming milestones include targeted exploration drilling, pilot processing advancements, and tungsten mill reactivation across Utah and Nevada assets.

These initiatives are timed against tightening global markets and escalating U.S. demand for antimony and tungsten in defense, electronics, and energy sectors.

AT4’s vertically integrated domestic strategy is poised to deliver meaningful progress through the remainder of 2026 — creating a compelling opportunity for investors as operational and policy catalysts converge.

The window for early positioning is now.

@ATAA_AT4

#OperationalPipeline #TungstenMomentum #DomesticProduction #Ad

1

7

12

14,124

May 13

American Tungsten & Antimony Ltd

(ASX: $AT4 | OTCQB: $ATALF)

American Tungsten & Antimony Ltd has secured a strategic national security milestone by gaining admission to the U.S. Defense Industrial Base Consortium (DIBC), managed on behalf of the Department of Defense.

Membership provides direct pathways to DoD programs, potential non-dilutive funding, and collaboration opportunities with prime contractors focused on strengthening domestic supply chains for critical minerals.

With both antimony and tungsten classified as essential for advanced defense systems, aerospace, and high-performance manufacturing, this move places AT4 at the center of U.S. efforts to onshore production and mitigate geopolitical risks from concentrated foreign supply.

It represents a clear catalyst for project advancement and long-term shareholder value.

@ATAA_AT4

#DefenseSupplyChain #DIBC #CriticalMaterials #Ad

9

9

14

3,523

May 12

✅ Wholly owned subsidiary of @anson_ir $ASN, A1 Lithium, has been admitted as a member of the US Defense Industrial Base Consortium (DIBC).

🔗 Read more here: ap1.hubs.ly/y0Rhr20

#miningnews #exploration #drilling #resources #mining

2

186

Congratulations to @anson_ir and their subsidiary @A1Lithium for being admitted as a member of the US Defence Industrial Base Consortium (DIBC).

What this does is open the door for the company to pursue several federal funding opportunities and help expedite a lot of the stuff that can hold a project back.

One of the reasons I like the GreenRiver project is its the personfication of K.I.S.S they are basing everything on established engineering principles they are not overreaching and trying to be the answer to every new challenge in the lithium industry.

They are developing a DLE project that will do one thing and do it damn well, produce lithium for domestic manufacturers, and we need so many more like them.

2

432

In case you missed it — CEO Michael Rowley presented at the @OTCMarkets Precious Metals & Critical Minerals Virtual Investor Conference, providing an update on the advancement of the Company’s flagship #StillwaterWest project in #Montana.

The presentation covered 2025 drill results, the upcoming updated Mineral Resource Estimate targeted for H1 2026, ongoing U.S. government engagement, and the Company’s position as one of the few large-scale U.S.-based nickel, copper, cobalt, and platinum group element development stories.

Watch the full presentation here: youtube.com/watch?v=q2PpI1c7…

#CriticalMinerals #Mining #Nickel #Copper #Rhodium #DIBC #PlatinumGroupMetals #Montana #OTCMarkets #InvestorConference #USCriticalMinerals $PGE.V $PGEZF

5

24

3,076