May 12

I like $PZZA (prob gets bought) and DOM.L (cheap and they're good about share buybacks)

1

2

817

May 12

Perhaps another company for income seekers... Dominos Pizza $DOM.L 🇬🇧

£734 million market cap.

Not so along ago the shares were at 460p, now 191p.

15% operating margins

21% ROCE

6% DY

TTM P/E 10

Still carrying a lot of net debt (and keeps rising) and low growth. More of a cash cow these days, possibly in value destruction mode.

5

532

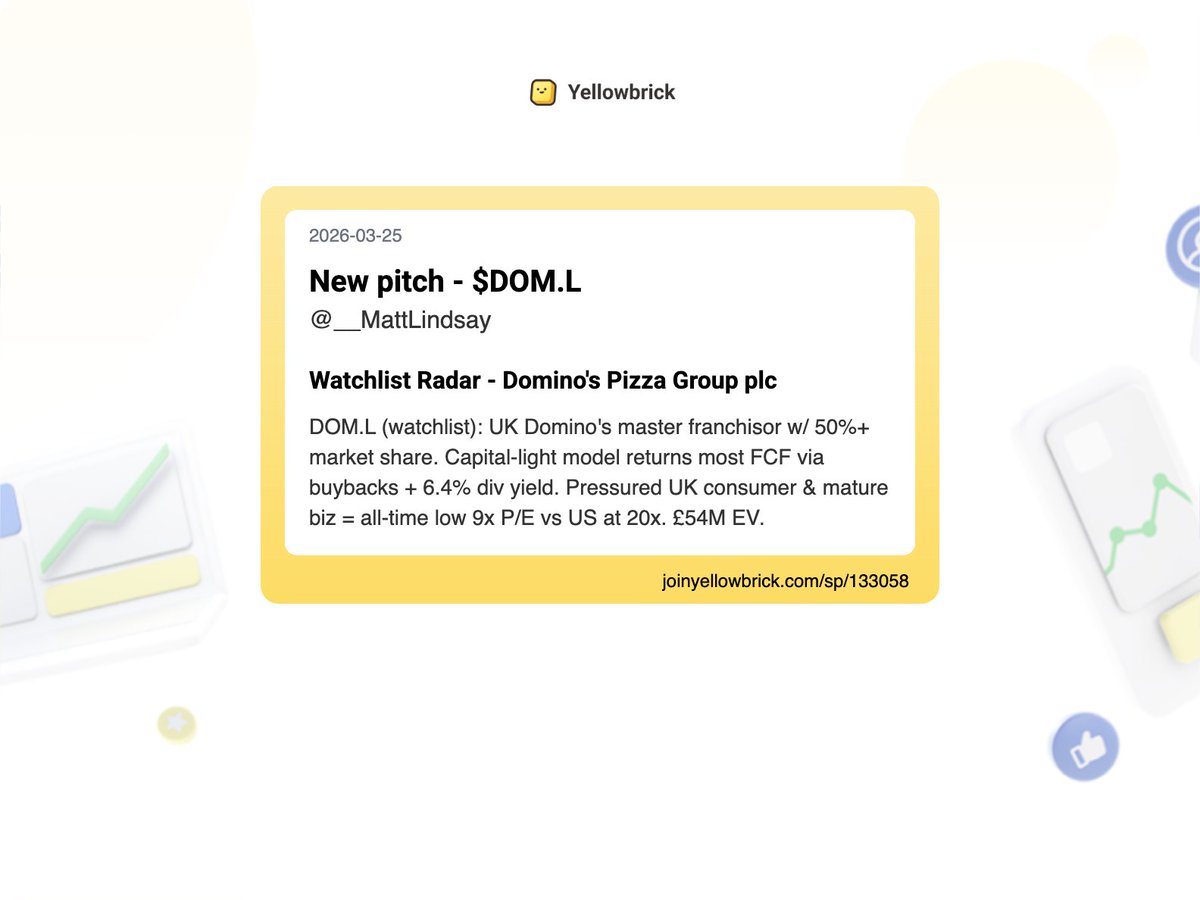

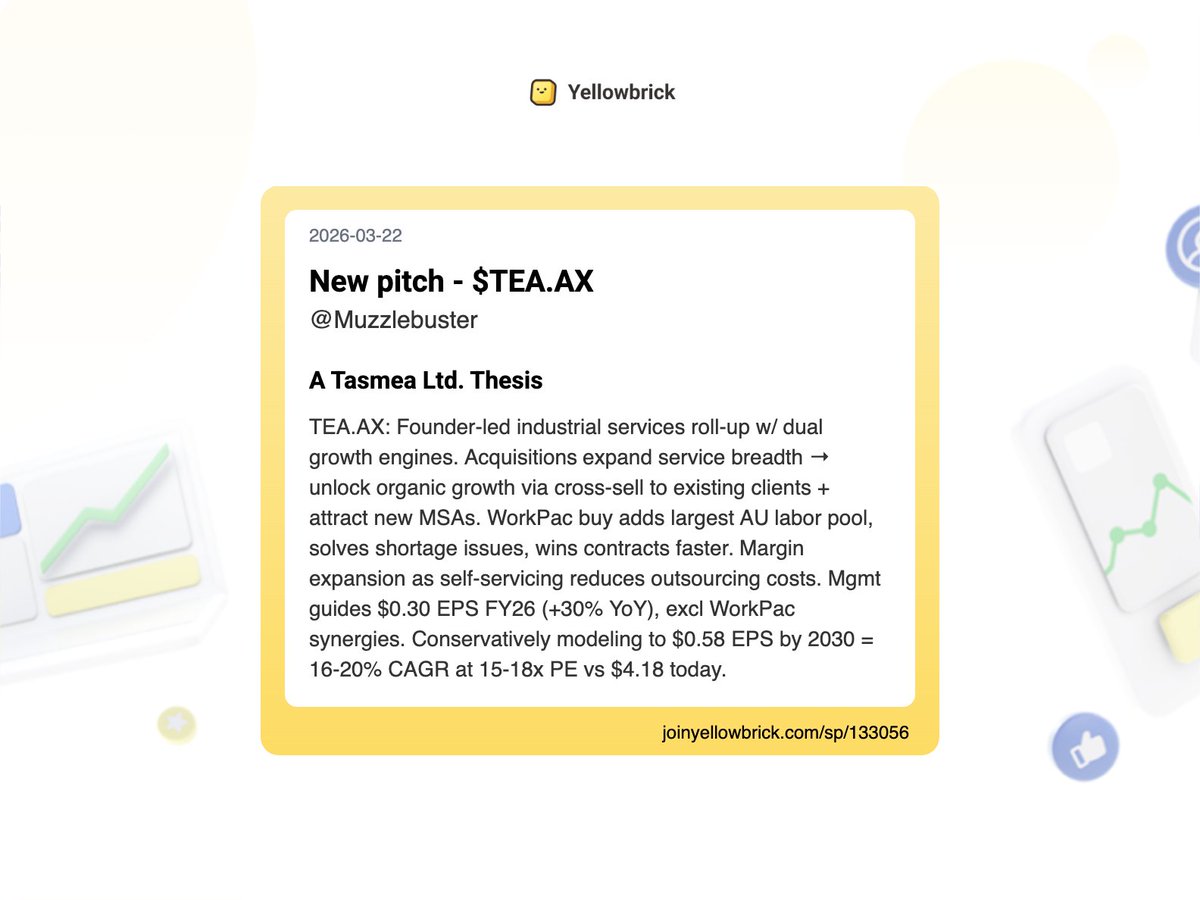

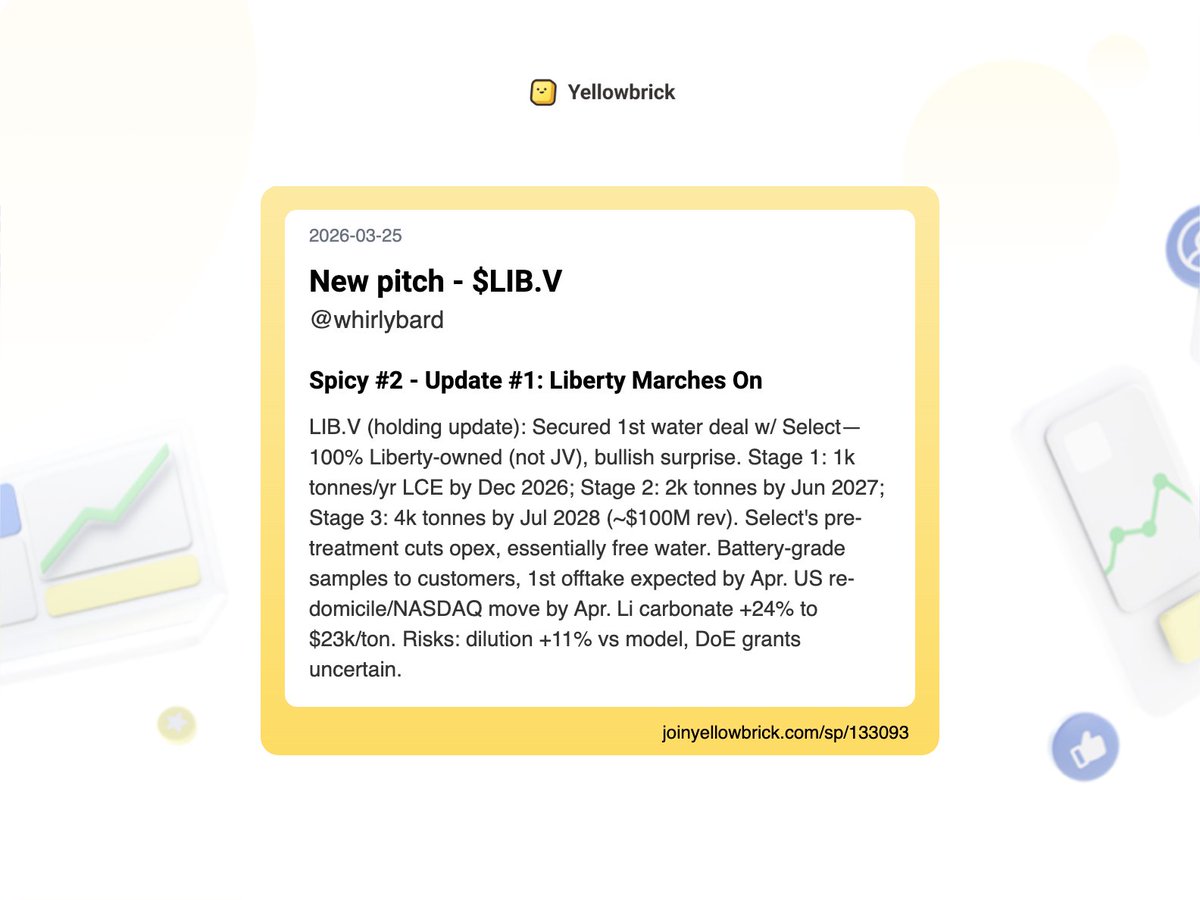

Added 67 new stock write-ups to the site (pt 2):

@__MattLindsay (watchlist) - $DOM.L, $ROCK-B.CO, $SNWV, $FRAS.L

@Muzzlebuster - $TEA.AX, $MELI (overview)

@BlokeOak57182 - $RGL.L (update)

@whirlybard - $LIB.V

@ChrisDeMuthJr - $RGR

@CompoundingUp - $4465.T (overview)

2

2

11

2,654

Mar 5

2

2

6

990

Jan 26

$dom.l it fucking cracks me up that you guys won't own a PIZZA FRANCHISE because it's having some issues. Seriously everyone here deserves exactly what they get. Zero capacity for independent thought.

1

5

1,135

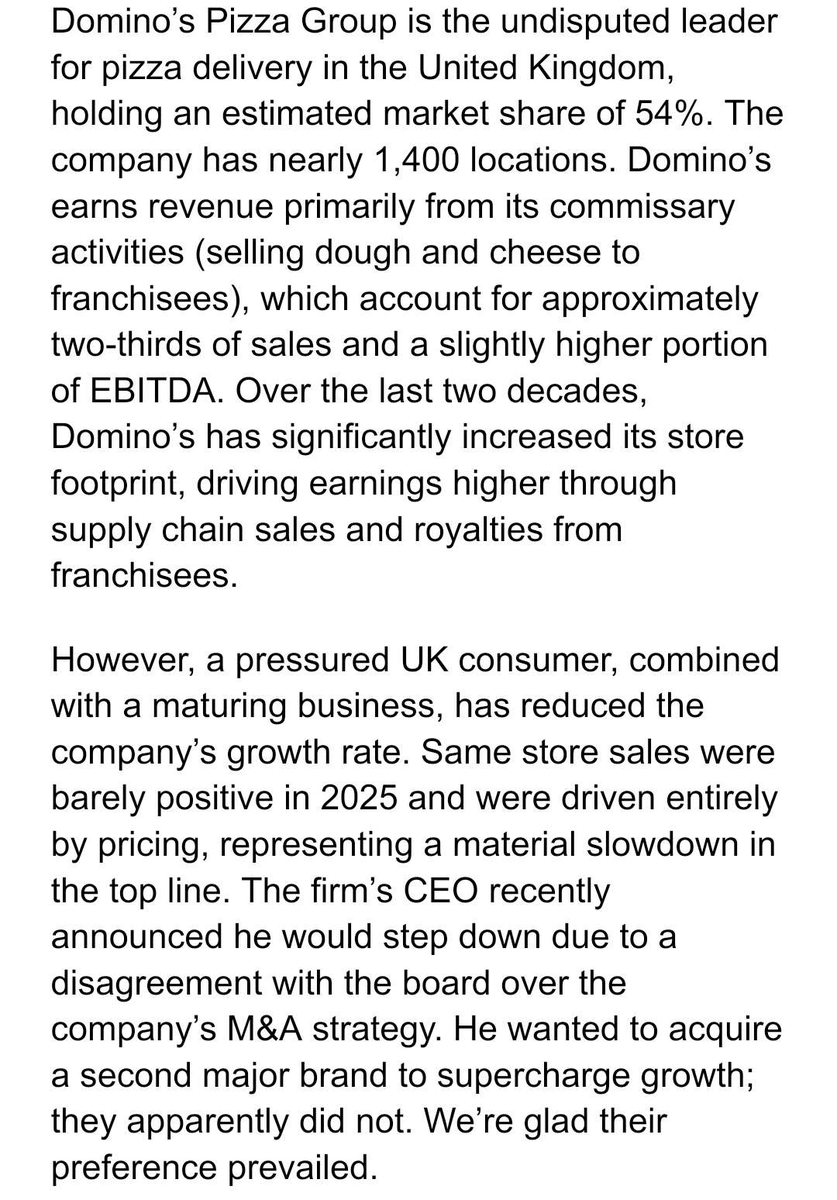

$DOM.L pitch by Palm Valley Capital

- Undisputed leader in UK pizza delivery with 54% mkt share

- Continues to gain mkt share even as industry volumes decline

- Top-line slowdown largely cyclical

- Trades at record low 9x EPS w/ >6% divi yield despite stable fundamentals.

3

7

72

12,510

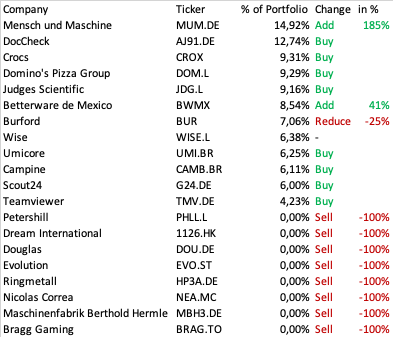

Portfolio going into 2026:

$MUM.DE (14.9%)

$AJ91.DE (12.7%)

$CROX (9.3%)

$DOM.L (9.3%)

$JDG.L (9.2%)

$BWMX (8.5%)

$BUR (7.1%)

$WISE.L (6.4%)

$UMI.BR (6.3%)

$CAMB.BR (6.1%)

$G24.DE (6.0%)

TMV.DE (4.4%)

FY2025 ended with 10.2% (in EUR).

$BUR was my largest position entering the year (18%). The stock is down ~30% in USD and almost 40% in EUR. Given that, I’m fortunate to be up at all. If $BUR had been flat in EUR, I’d be up 27.4%. But that's not how it works.

In hindsight, being that concentrated in a volatile, lumpy business may have been a mistake. That said, I still view BUR as an attractive risk/reward here and expect it to trade much higher over time.

$MUM.DE and $AJ91.DE are my two biggest positions going into 2026.

I’ve discussed DocCheck $AJ91.DE before and have a full post on the stack. It’s a good, growing business with hidden balance sheet assets, trading at <5x operating profit.

Mensch und Maschine $MUM.DE is a German software company selling proprietary (mostly CAM) software (~2/3 of EBIT) and serving as Autodesk’s largest value-added partner in Europe — providing training, consulting, support, and customization for Autodesk’s CAD/BIM products (~1/3 of EBIT).

MUM is a high-quality business: EPS up ~22% CAGR over the last decade, virtually no CapEx or tangible assets (very high earnings quality), and expected to grow EPS ~15% p.a. going forward, driven by continued digitization in construction and machining.

Because I like the business, valuation, and management, I added heavily this year and made it my largest position.

A big reason why I felt confident increasing my holding is the founder and chairman, Adi Drotleff, who owns 47% of the company (management owns another 6%) and comes across as a straight-talking, no-nonsense, level-headed guy.

The company doesn't host public earnings calls, but Mr. Drotleff gives a short, informal 20-minute audio interview after every quarter.

To give you an idea of his understanding of incentives: In the most recent interview, he mentioned how the managers of the ~100 profit centers at MUM (they run a decentralized organization) are compensated solely on profits, and an internal ranking of the highest profit-generating units is published. As you can imagine, nobody wants to be at the bottom third of the list two years in a row. So it's a self-correcting system.

2025 was a transitional year for the company because of Autodesk's commission model change and the unforeseen temporary operational/administrative headwinds that resulted from it. The coming year will therefore have easy comps.

I feel good about my two biggest positions. We will see how it goes.

------------

Biggest winners 2025: $1126.HK, $NEA.MC, $PHLL.L, $AJ91.DE, $BWMX

Biggest losers 2025: $BUR, $BRAG.TO, $TMV.DE, $EVO.ST

Lessons from the winners:

- Cheap growing high earnings quality is the winning formula (duh!)

Lessons from the losers:

- Don't concentrate too heavily in volatile businesses

- Avoid businesses with poor earnings quality

- Extremely high margins have only one direction to go

- Avoid business models that don't pass the smell test (does it make sense that an extremely labour-intensive company can sustain >60% operating profit margins?)

- Don't follow even the best investors into an idea blindly (without having conviction in the thesis myself)

------------

Looking forward to studying businesses, learning, and getting better at this game in 2026.

3

38

6,572

16 Dec 2025

Just put out some work on Domino’s Pizza Group, listed on the LSE. $DOM.L

13.9% FCF Yield, historically low P/E multiple, taking market share from competitors, economy of scale advantages thanks to supply chain centers, and selling pizza, which isn’t going anywhere.

Link 👇

1

3

10

1,203

25 Nov 2025

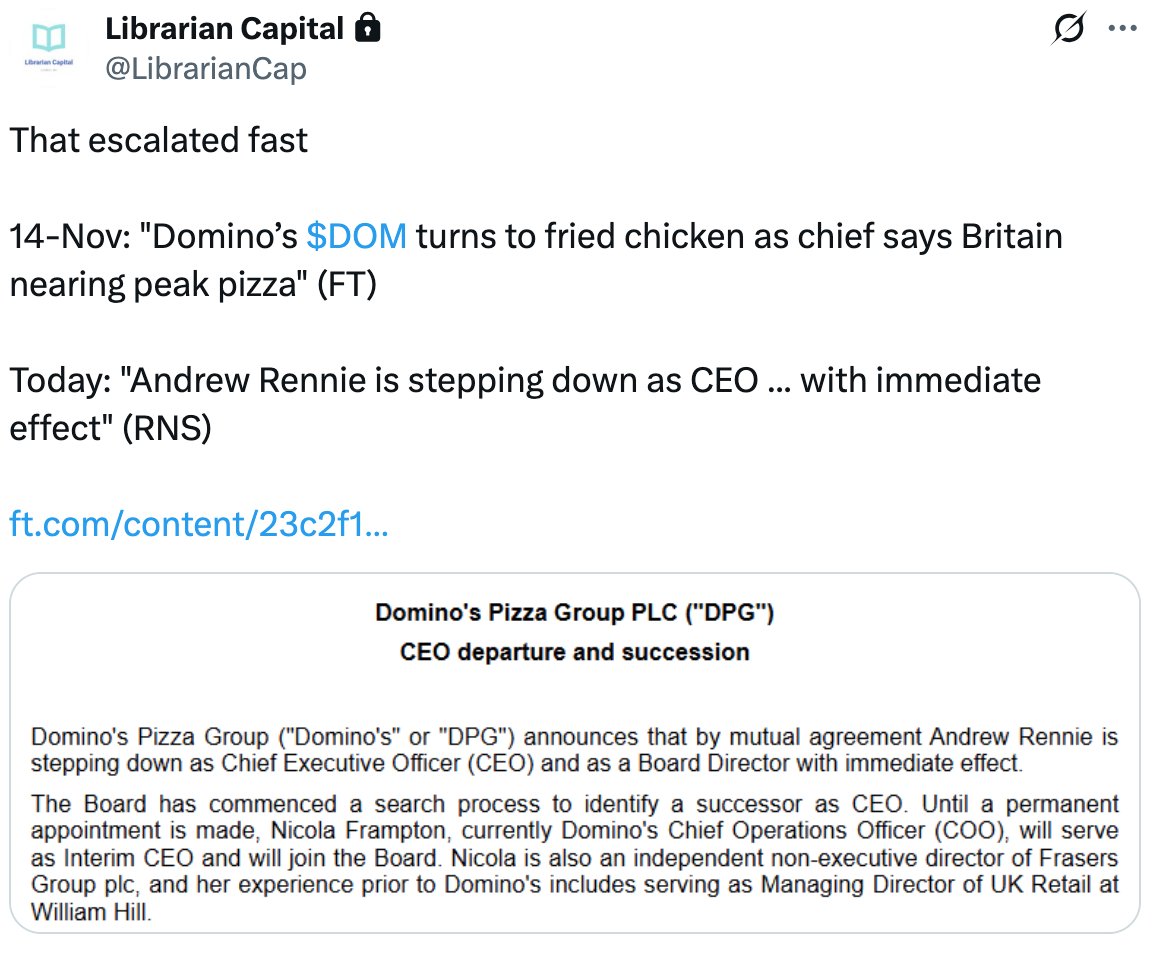

#DOM.L Dominos Pizza (UK) - I assume the departure of Rennie heralds a win for more activist shareholders. If so we could see money injected in share buybacks or even bolder moves. Big franchisees have been sizeable shareholders before (eg Moonpal Singh Grewel). Obviously biz is still challenged and tough environment. But its still the tallest dwarf....(blog link in bio) @librariancap

1

5

878

18 Nov 2025

Will that work?

A good business (high ROE) is not worth that much without Growth

$DOM.L

10 Nov 2025

Domino's Pizza group $DOM.L 🍕

Seems a way above average, good business with (too?) high market share!

Seemingly cheap at 10x and 6% dividend yield plus buybacks.

But growth outlook is unimpressive! SSS flat! (Source checked!)

4

636

10 Nov 2025

You can invest in pizza and robots at the same time

Few understand this

$DOM.L

2

12

2,282