6/6 HCIP Datacom H12-831 784 points Pass

BBSDUMP valid and latest. Contact BBSDUMP to get the latest dump, Whatsapp: 372 54849073

1

I’d very much like to attend myself, but unfortunately I can’t.

I have quite a few questions for management, but if I had to narrow them down to just a few, they would be the following:

1. You confirmed that roughly €20 million of LayTec revenue is “not far from reality” as a medium term perspective. I have three related questions.

First, would you consider introducing separate segment reporting for LayTec once the business reaches sufficient scale?

Second, how much of LayTec’s revenue today is already recurring in nature, such as service, software, and Connected Metrology, versus one time hardware sales? How would you like that mix to evolve over the next few years?

And third, if you break down LayTec’s current order intake by material system, where do you see the strongest momentum today: GaN power electronics or InP/datacom? Are you already seeing orders tied to new epitaxy capacity expansions, or is demand still primarily driven by utilization and optimization of existing production lines?

2. CFO Peters said that he would be surprised if double digit EBIT margins were not achievable by 2027. Could you help us bridge the gap from the 6% to 8% EBIT margin target for 2026 to that level?

Specifically, how much of the improvement is expected to come from volume growth and operating leverage, how much from a more favorable business mix, including higher margin activities such as LayTec, and how much still depends on the remaining benefits from the NyFIT2025 program?

3. You mentioned defense as a growing area of interest. Are we primarily talking about existing spectroscopy and sensing platforms finding their way into defense applications, or are you also pursuing dedicated new product developments for this market?

And beyond LayTec, which business areas are currently benefiting most from increased capital expenditures in the semiconductor industry?

1

5

1,109

6/1 HCIA Datacom V1.0 H12-811 800 points Pass

The coverage rate is approximately 95%.

Notes: The HCIA-Datacom V1.0 exam will be officially discontinued on June 30, 2026.

2

6/4 HCIE Datacom H12-891 700 points Pass

700 points, the dump . Full coverage.

Contact BBSDUMP to get the latest dump, Whatsapp: 372 54849073

4

𝑻𝒉𝒆 𝒄𝒉𝒊𝒑𝒔 𝒘𝒆𝒓𝒆 𝒋𝒖𝒔𝒕 𝒄𝒉𝒂𝒑𝒕𝒆𝒓 𝒐𝒏𝒆.

The real constraints on scaling AI are no longer measured in teraflops alone. They’re measured in megawatts you can actually deliver, photons you can move at rack scale, liquid you can pump without melting the floor, and platforms that turn raw infrastructure into deployed, governed intelligence.

Jensen has been clear for months: the handoff is happening. Copper has limits. Power is the new gate. Cooling density is non-negotiable. The companies securing these layers with long-term contracts and balance-sheet capital are building durable positions.

Here’s how the 2026 AI infrastructure stack breaks down from silicon to intelligence:

LAYER 1: SILICON FOUNDATION

🟠 $TSM — The advanced foundry and packaging backbone (CoWoS and beyond). This is the capacity gate for the highest-performance AI chips. Everything upstream starts here.

LAYER 2: AI COMPUTE

🟠 $NVDA — Still the clear leader in GPUs and full AI systems/racks. The ecosystem investments and rack-level selling show they understand the game has moved beyond individual chips.

LAYER 3: SERVERS & RACK INTEGRATION

🔵 $SMCI — Building dense, liquid-ready AI server and rack systems that hyperscalers deploy at scale. Direct volume beneficiary of the buildout.

LAYER 4: NETWORKING & HIGH-SPEED INTERCONNECT

🔵 $MRVL — Switching silicon, DSPs, and aggressive silicon photonics push via Celestial AI. Essential for scaling clusters beyond single racks.

🔵 $AAOI — Datacom optics leader with explosive data center revenue growth and a major 800G/1.6T order backlog. Scaling domestic capacity while supply chain security matters.

LAYER 5: PHOTONICS & OPTICS TRANSITION

The physics is clear, copper hits the wall on bandwidth density and power. Photonics moves from “nice to have” to required for the next jump in cluster scale.

🔵 $LITE (Lumentum) — Leading provider of high-speed lasers, EMLs, and optical components with a major NVIDIA strategic investment and multi-billion dollar purchase commitments. Scaling US manufacturing for AI data center optics demand.

LAYER 6: POWER: THE BINDING CONSTRAINT

🟠 $VST — Signing multi-decade power purchase agreements directly with hyperscalers. Nuclear uprates and reliable generation capacity are becoming strategic assets.

🔵 $IREN — Renewable-powered data centers executing a clear pivot into AI/HPC cloud. Large-scale sites with secured power and flexible capacity. 5.8 GW-scale pipeline building.

LAYER 7: COOLING & THERMAL MANAGEMENT

🔵 $VRT — Liquid cooling systems are moving from pilot to must-have for high-density AI racks. Record backlog and order growth as power density per rack climbs.

LAYER 8: CLOUD & DATA CENTER PLATFORMS

🔵 $ORCL — Oracle Cloud Infrastructure is seeing massive AI-driven demand. Major capex ramp, OpenAI/Stargate ecosystem work, and enormous remaining performance obligations.

🔵 $NBIS — AI infrastructure specialist rapidly scaling contracted capacity (multi-GW targets). Major hyperscaler deals are driving strong ARR acceleration.

LAYER 9: THE INTELLIGENCE LAYER

🔵 $PLTR — Palantir’s AIP platform turns physical infrastructure plus enterprise data into production-grade, governed AI applications. U.S. commercial momentum is accelerating sharply.

Capital is already voting with real money: direct hyperscaler power deals, NVIDIA’s multi-billion dollar optics investments, pre-payments for capacity years out, and software platforms seeing accelerating commercial traction.

The honest counter-thesis is that real valuations across parts of the stack are elevated, power timelines can slip, cooling and photonics tech is still maturing in some deployments. Software ROI takes time to prove at scale. One digestive quarter can pressure the whole chain. But the structural, multi-year spend from the largest balance sheets in tech is not a narrative. It’s signed contracts and capex plans.

The market has aggressively priced the obvious chip layer. The asymmetry sits in the scarce layers everything else depends on.

Own the full stack. Not just the logo on the GPU.

Bookmark this. Then drop which layer you think moves first or which one I’m underweighting.

Tag the person who’s still only buying NVDA and calling it a diversified AI portfolio.

1

1

4

544

ECE vallu Telecom/Datacom vaipu kuda vellachu..Datacom side chala openings unnayi less competition job kuda easy dorike chance untundhi

Jun 13

Cheppali antey Ece lo jobs and packages >>>> IT as of now....

Chip design and verification courses nerchuko...

Starting kastame job ravadam..intern cheyu or edaina job vastey small job less package ina cheyu....after 2 or 3yrs exp. Shift avvu...manchi packages vasthai MNCs lo..

2

3

1,180

Worth adding $POET 's Blazar to this. Their ELS uses four laser chips instead of eight, two thirds less InP per light source, wafer level packaging that drops cost by 10x vs traditional DFB.

InP wafer supply is already maxed out globally with three producers and AI datacom demand about to consume all of it. Any architecture that solves the InP bottleneck at CPO scale isn't a nice to have, it's the only path that actually scales.

1

256

🛡️ HCIA-Datacom Unlocked: From Zero to Networking Hero – Master Routing, Switching & Cyber Defense Like a Pro Video

undercodetesting.com/hcia-da…

Educational Purposes!

4

Jun 13

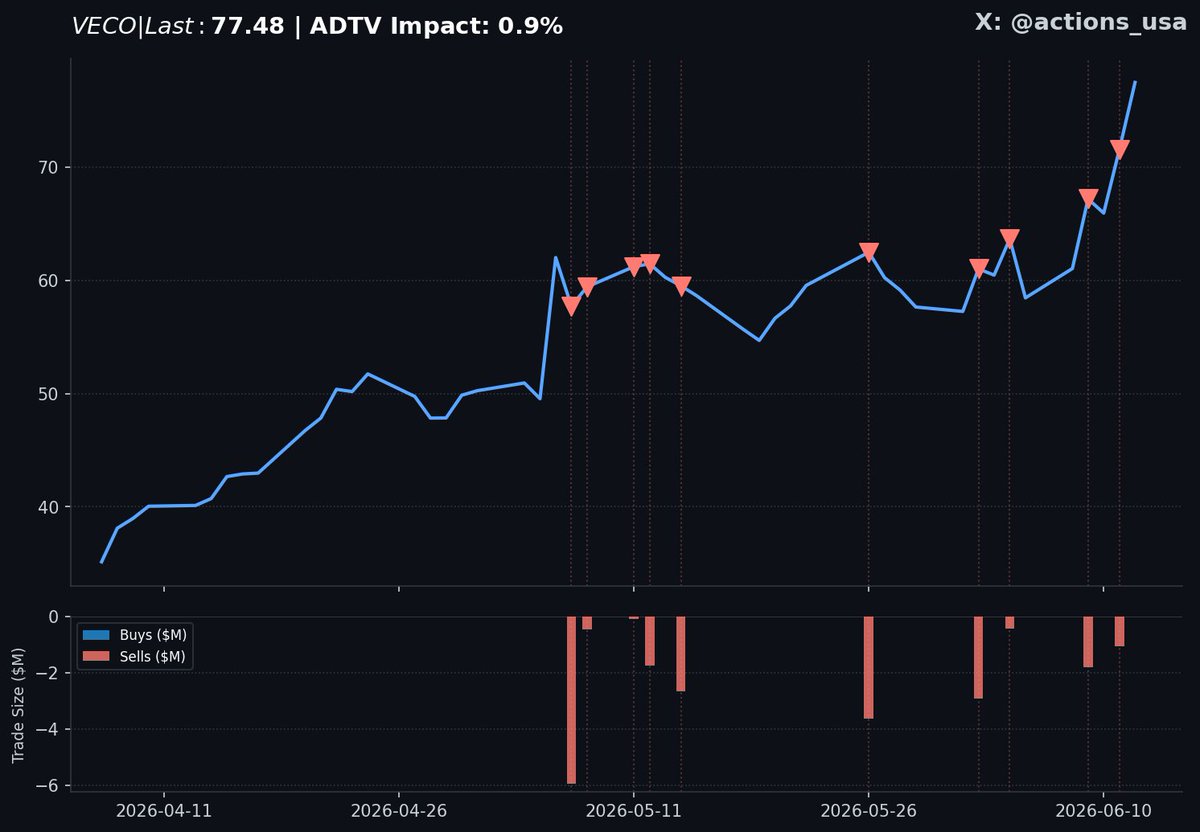

SVP of Global Sales and Service Susan Wilkerson just manually dumped 36 percent of her position for over 1 million dollars in $VECO. This discretionary exit is part of a massive 12.5 million dollar coordinated insider liquidation wave occurring as management cashes out following the 250 million dollar AI datacom order announcement.

144

Jun 13

4/7

The market is already reacting.

$AXTI became one of the most obvious pure-play beneficiaries.

Its InP-related revenue exploded higher in recent quarters, backlog hit record levels, and investors quickly realized that optical supply chains were becoming strategic assets.

But AXTI is also:

• Smaller

• More volatile

• More China-exposed

The larger players are moving aggressively to secure control of the stack.

🔵 $COHR (Coherent)

One of the most strategically positioned names in photonics.

Exposure includes:

• InP substrates

• Epitaxy

• Lasers

• Optical engines

• Datacom components

Coherent is vertically integrated across much of the optical value chain.

As AI networking demand explodes, that integration becomes increasingly valuable.

The company already carries substantial AI-related backlog extending years into the future.

🔵 $LITE (Lumentum)

Another critical optical infrastructure supplier.

Lumentum sits directly in the laser ecosystem powering AI networking.

1

45

Jun 12

I’m pretty good at datacom, but EnodeB fibers hanging out is a a new technology I must’ve missed.

12

Jun 12

pick your poison

( assuming VR's NVL72 numbers for NVL576, just between the racks. We'll see all kinds of telecom stuff entering datacom, including the most mundane but also annoying stuff like their cables. Made by codex. )

Jun 12

• Majority of GPU-GPU links <2m Cu today:

• Scale-up fabric ~9x BW of scale-out network

• ~5:1 copper vs optics

• Cu used for cost and reliability

• Cu limited by reach and density (connectors)

• Majority of GPU-GPU links will remain <50m

• Min 50% of scale-up links must >2m

• Need low-cost, reliable, power-efficient optics

• Must hit targets:

• 30m distance

• Approaching copper-level reliability

• <5pJ/bit (not including PHY)

• 1Tbps/mm

If optics can be applied to 100% scale-up, volume grows >20x over next 5 years

2

6

67

4,270

One contact to Metra Associates connects you to IDEAL Electrical, a trusted name in the electrical industry for decades.

Wire Connectors - Fishing, Bending, and Lubricants - Electrical Tape and Supplies - Power Tool Accessories - Test and Measurement - Datacom

IDEAL Full Line Catalog: idealind.com/content/dam/ele…

Florida Electrical Distributors, reach out for details:

📧 IDEAL@metra-assoc.com

📞 954-428-4803 | Alberto Cervantes

🌐 metra-assoc.com/

#IDEALElectrical #WireConnectors #ElectricalTape #ElectricalDistribution @IDEALElectric_

8

Jun 12

The next growth layer: Optical Transceivers. Same plant. Incremental tooling. Massive TAM!!

🔹India's datacom transceiver demand: growing ~45% YoY driven by AI cluster buildouts.

🔹India market projection: $600 Mn at >30% CAGR.

🔹Global market: $13.5B → $28B by 2030.

👉izmoMicro's roadmap:

🔹400G-DR4 pilot - FY28

🔹800G-DR8 primary - FY28-30

🔹1.6T-DR8 - FY30

👉Why this works: the SiPh packaging line is being built anyway. Transceiver assembly is incremental tooling ON THE SAME PLANT.

@Cryptified_Soul @Pkjat340 @EquityInsightss @mehul_n_trivedi

1

3

248

BizLink agrees $850m acquisition of Blackstone’s Interplex Datacom: BizLink Holding Inc has agreed to acquire Interplex Datacom from Blackstone Inc in an $850m cash tra... dlvr.it/TT0Ywl #AlternativeInvestments

9

Jun 12

$BZAI ✨

reported Q1 2026 revenue of $2.7M, up 170% YoY despite server shipment delays caused by global memory shortages.

Key highlights:

✅ Revenue 170% YoY

✅ Gross margin improved to 58%

✅ Neo Tensor opportunity expanded to $70M

✅ Vinmart partnership expected to generate ~$15M in first-year revenue

✅ Nokia and Datacom partnerships advancing

✅ Blaze AI Services launched

✅ 2026 revenue guidance maintained at $130M

Management expects stronger growth in the second half of 2026 as hybrid server shipments ramp and AI services begin contributing revenue.

The story is evolving from AI hardware to AI infrastructure recurring AI services.

#BZAI #Blaize #AI #EdgeAI #DataCenter #ArtificialIntelligence

3

361

Jun 11

No es novedad, eso hacen también en ENTEL, ATT, AGETIC Y DATACOM. Incluso tienen como gerentes extranjeros de forma ilegal en empresas publicas, me preguntó cómo tienen la libreta militar y el certificado de idioma nativo? Esos son los espías del comunismo venezolano.

1

1

161

Bengt Lord retweeted

Jun 11

Nota bene, i Järfälla så tillverkar Coherent datacom-lasrar (bl.a.) från blanka InGa-substrat 24/7 till just utbyggnaden av datacentren för AI. Vi har 20% andel av världsmarknaden, jämnstora med Lumentum och Sumitomo. De används numera även på mycket korta distanser inom racks.😉

1

1

3

227