Apr 27

DatabricksがNeonを買収し、MetaがManusを買収し、SnowflakeがDatavoloを買収する。

最近のテック業界でM&Aラッシュが起きています。

なぜ今これだけ集中しているのか。

その構造的な背景を整理するのに良い記事があります。

Spotify元ML責任者でModal CEOのErik Bernhardssonの記事です。

1

1

7

686

Apr 10

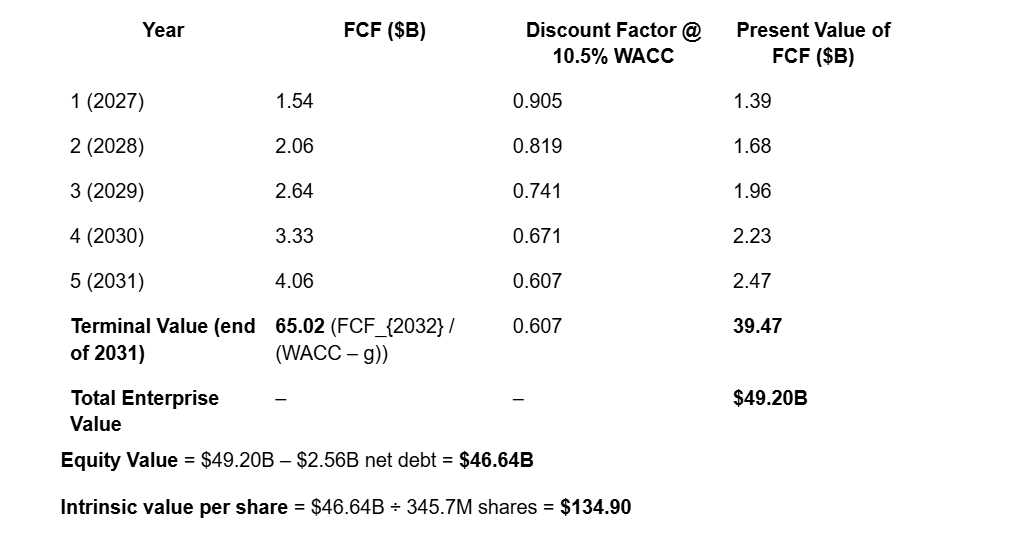

Company Profile: Snowflake Inc. (NYSE: SNOW)

Attribution: I used Notebooklm to build the profile and Grok to build the DCF models using my conservative assumputions.

1. Management Quality and Corporate Culture

Snowflake is led by a management team that has undergone significant strategic transitions recently to align with an AI-first growth strategy. Sridhar Ramaswamy was appointed as Chief Executive Officer in February 2024, succeeding Frank Slootman. The leadership team was further bolstered in fiscal 2026 with the appointment of Brian Robins as Chief Financial Officer and Michael Gannon as Chief Revenue Officer. To strengthen its technical and security posture, the company recruited a Chief Security and Trust Officer in 2026, a veteran with over 20 years of experience at Google.

The company’s culture is anchored by eight core values, including "Put Customers First," "Integrity Always," and "Think Big". As of January 31, 2026, Snowflake employs 9,060 people across 36 countries, maintaining a globally distributed workforce. Management utilizes a total rewards strategy that combines competitive cash compensation with equity alignment to attract high-demand talent, particularly in software engineering and AI.

2. Growth and Potential

Snowflake’s primary growth engine is its AI Data Cloud, a unified platform designed to eliminate data silos and enable organizations to derive value from structured, semi-structured, and unstructured data. The company operates across five key product categories: Data Engineering, Analytics, AI, Applications & Collaboration, and the newly launched Transactions category.

Key Growth Drivers:

Massive Market Opportunity: Snowflake estimates its Total Addressable Market (TAM) will grow to $355 billion by calendar year 2029.

Strategic Acquisitions: The company has aggressively expanded its capabilities through acquisitions, most notably Observe, Inc. (AI-powered observability), Crunchy Data (PostgreSQL technology), and Datavolo (multimodal data pipelines for AI).

Network Effects: The platform benefits from powerful network effects; as more customers join, the volume of data available for exchange through the Snowflake Marketplace increases, enhancing value for all participants.

Enterprise Momentum: As of January 31, 2026, Snowflake serves 790 of the Forbes Global 2000, with these large enterprises contributing approximately 43% of total revenue.

International Expansion: Non-U.S. accounts now represent 25% of total revenue, with ongoing investments in the EMEA, APJ, and Latin America regions.

3. Financial Highlights

Snowflake utilizes a consumption-based business model, meaning revenue is recognized as customers use compute, storage, and data transfer resources rather than ratably over time.

Fiscal Year 2026 Performance (ended Jan 31, 2026):

Total Revenue: $4.7 billion, representing 29% year-over-year growth.

Remaining Performance Obligations (RPO): A significant $9.8 billion, reflecting deep long-term customer commitments.

Net Revenue Retention Rate: A robust 125%, indicating that existing customers continue to expand their usage of the platform significantly.

Profitability Metrics: While reporting a GAAP net loss of $1.3 billion, the company generated $1.1 billion in Non-GAAP Free Cash Flow, representing a 24% margin.

Product Gross Margin: Maintained at a Non-GAAP level of 76%, demonstrating strong operational efficiency despite investments in new AI capabilities.

Customer Scale: The number of customers contributing over $1 million in trailing 12-month product revenue grew 27% YoY to 733.

4. Risk Assessment

Snowflake operates in a rapidly evolving and highly competitive environment, facing several categories of risk:

Intense Competition: The company competes directly with "Big Three" cloud providers—AWS, Azure, and GCP—who are simultaneously Snowflake’s infrastructure partners and primary competitors.

Cybersecurity and Data Privacy: Snowflake has previously been targeted by threat actors who accessed customer accounts through stolen credentials. Any future actual or perceived breaches could result in significant liability, reputational harm, and reduced demand.

AI Execution Risks: The success of the company’s AI strategy depends on maintaining access to high-demand hardware like GPUs, recruiting specialized talent, and navigating a rapidly changing global regulatory landscape for AI.

Historical Losses: Snowflake has a history of operating losses and an accumulated deficit of $9.5 billion; achieving and sustaining future profitability is not guaranteed.

Macroeconomic and Geopolitical Volatility: Performance is subject to fluctuations in global cloud spending, inflation, tariffs, and geopolitical conflicts (such as those in the Middle East and Ukraine), which may cause customers to rationalize budgets.

Intellectual Property Litigation: The company is currently subject to a class action lawsuit alleging copyright infringement related to large language model training.

5. DCF Calculation Table

1

1

10

4,673

Feb 2

$PLTR 은 오늘 4분기 실적을 발표할 예정입니다.

저는 이 회사를 4년 동안 집착적으로 연구해 왔습니다.

몇 가지 생각을 공유하겠습니다:

1. 서사를 형성할 거대한 기회

모든 기업용 SaaS가 "AI"라고 말하지만, Palantir만이 모든 산업에서 대규모로 막대한 성과를 달성하고 있음을 증명하고 있습니다.

Palantir 주가는 SaaS 회사들에 대한 두려움이 커지면서 타격을 받았습니다.

Karp는 Palantir의 실적이 계속해서 다른 회사들과 차별화되는 방식을 보여줌으로써 서사를 통제할 수 있습니다.

다른 회사들은 그들의 길을 계속 가지만, Palantir은 영역을 확장합니다.

2. 애널리스트들은 계속해서 과소평가하고 있습니다

저는 애널리스트들이 다음을 과소평가한다고 봅니다:

• 성장의 강도;

• 성장의 지속성;

• 마진 확장 잠재력.

NTM 기준 116배 EV/FCF 밸류에이션은 높지만, 낮은 추정치에 기반한 것입니다.

즉, 실제로는 저평가될 수 있습니다.

3. 파트너 생태계가 폭발적으로 성장하고 있습니다

파트너 생태계(PLTR을 판매하는 3자 컨설턴트)가 폭발적으로 성장하고 있습니다.

이는 다음을 의미합니다:

• 새로운 고객 = 성장;

• 거의 비용 없이 성장 = 더 높은 마진;

• 브랜드 인지도 = 가격 결정력.

예: 파트너 @NorthslopeAI는 매출이 7배 증가한 후 2,200만 달러를 조달했습니다.

4. 일반 투자자들은 여전히 모르고 있습니다

평균 투자자들의 인식은 다음을 무시합니다:

• Warp Speed;

• AI FDE;

• Hive Mind.

이러한 제품들이 앞으로 몇 년 동안 성장의 핵심 동인이 될 것입니다.

다른 회사들은 따라잡지 못할 것입니다.

5. 탈출 속도가 델타를 넓히게 합니다

AIP 출시 후 약 3년이 지났지만, 빅테크로부터 진정한 경쟁자가 아직 없습니다.

회사들이 FDE 모델을 복제하려 하면서 "X의 Palantir"을 구축하는 추세가 있습니다.

이는 인지도만 높일 뿐, 진정한 경쟁이 되지는 않을 것입니다. Palantir의 제품 품질을 달성하려면 수년간 고통을 감내해야 하며, 가장 중요한 사용 사례에 접근하는 것은 쉽지 않습니다.

경쟁자들은 이제 제품 구축 속도가 10배 빠른 Palantir과 맞서야 합니다.

행운을 빕니다.

6. 다른 회사들은 사들이고, Palantir은 구축합니다

$NOW는 2025년에 100억 달러를 M&A에 썼지만, 혁신적인 결과가 나오지 않고 있습니다.

$SNOW는 2025년에 Crunchy Data, Datavolo, TruEra AI를 인수했습니다. 지금은 Observe를 위해 10억 달러 규모의 인수를 노리고 있습니다.

반면 Palantir은 자체 기술 스택에서 새로운 제품을 구축함으로써 지배하고 있습니다.

누가 보스인가요?

7. 2026년 가이던스가 핵심입니다.

진정한 초점은 26년 가이던스에 있을 것입니다. 시장은 강한 성장을 보고 싶어합니다.

$NOW는 강력한 실적에도 불구하고 10% 하락했는데, 아마도 가이던스가 22% 성장으로 이어지는 데 그치기 때문일 것입니다.

$PLTR 애널리스트들은 2026년에 43% 성장을 예상하고 있으며, 이는 둔화를 암시하지만 저는 그럴 가능성이 낮다고 봅니다.

Palantir의 최선은 아직 오지 않았습니다.

----

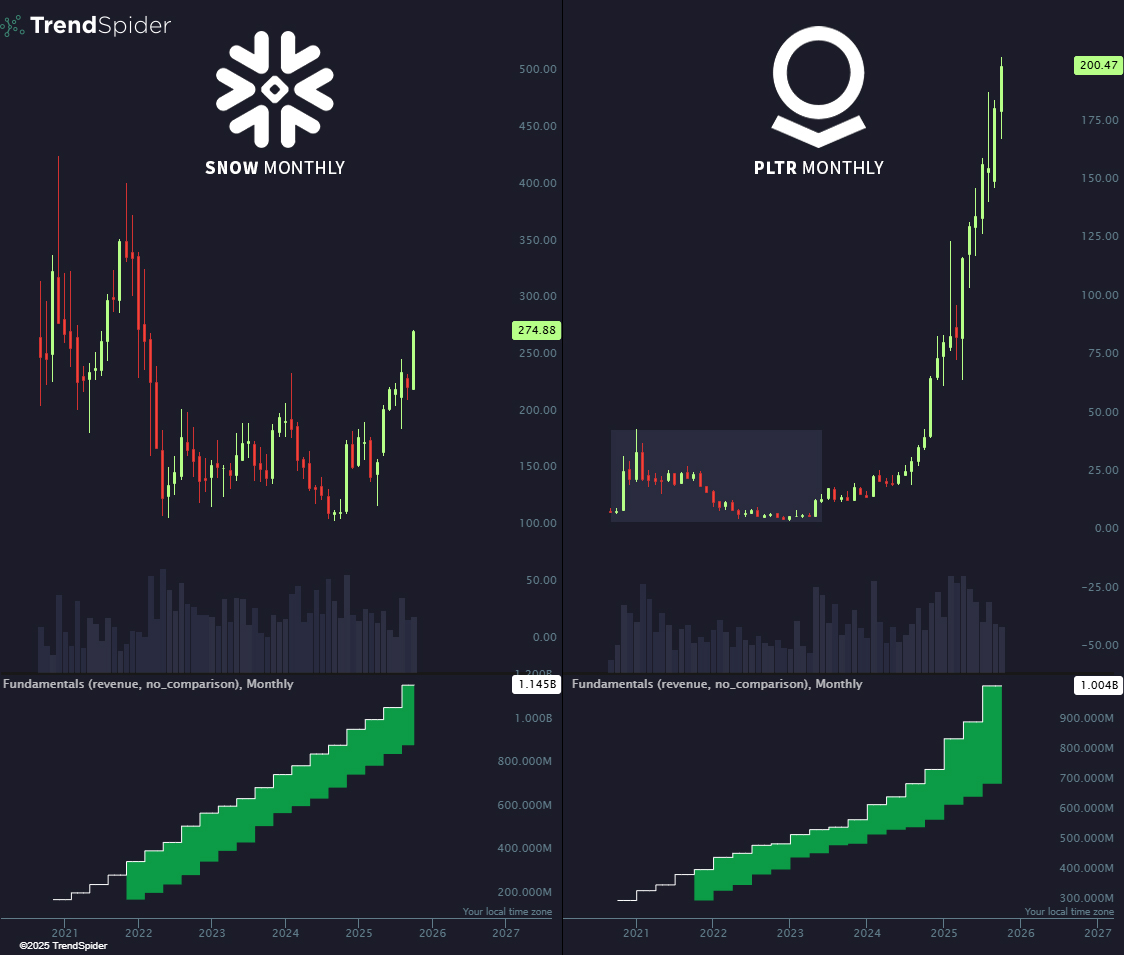

$PLTR 주가는 놀라운 3분기 실적 발표 후 급락했습니다.

이번에는 다를까요?

존경하는,

@arny_trezzi

Feb 2

$PLTR will release its Q4 today.

I've been obsessively studying the company for 4 years.

Here are a few thoughts:

1. Massive opportunity to shape the narrative

While all enterprise SaaS say "AI", only Palantir it is proving it is delivering massive outcomes at scale, in any industry.

Palantir stock has been hit as fear has risen about SaaS companies.

Karp can control the narrative by showing how Palantir's results keep diverging.

Others continue their path. Palantir takes ground.

2. Analysts keep underestimating

I see analysts underestimating:

• the strength of growth;

• the durability of growth;

• margins expansion potential.

The 116x EV/FCF NTM valuation is high, but based on low estimates.

aka it could be actually cheap.

3. The Partner Ecosystem is exploding

The partner ecosystem (3rd party consultants selling pltr) is exploding.

This means:

• new clients = growth;

• growth at almost no cost = higher margins;

• brand awareness = pricing power.

eg. It's partner @NorthslopeAI just raised $22mn after its Revenue 7x.

4. General investors still have no idea

Avg. investor awareness ignores:

• Warp Speed;

• AI FDE;

• Hive Mind.

These products will be the key drivers of growth in the coming years.

Others will fail to catch up.

5. Escape velocity makes the delta widen

After ~3 years since AIP's launch, there is still no real competitor from big tech.

There is a trend of building the "Palantir of X" as companies try to clone the FDE model.

This will only increase awareness, but it will not become real competition. You need to eat pain for many years to deliver the product quality Palantir has, and having access to the most critical use cases is not easy.

Competitors now face a Palantir that is 10x faster at building products.

Good luck.

6. Others buy. Palantir builds

$NOW spent $10bn in M&A in 2025 and nothing revolutionary is coming out of it.

$SNOW bought in 2025 Crunchy Data, Datavolo, and TruEra AI. It is now eyeing a $1bn acquisition for Observe.

Meanwhile, Palantir is dominating by building new products on its tech stack.

Who's the boss?

7. 2026 Guidance is key.

The true focus will be on 26' guidance. Markets want to see strong growth.

$NOW dropped 10% despite strong results, probably because its guidance is just continuing at 22% growth.

$PLTR Analysts see 43% growth for 2026, implying a deceleration, which I don't see as likely.

The best Palantir is yet to come.

----

$PLTR stock dropped sharply after its spectacular Q3 results.

Will this time be different?

Yours,

@arny_trezzi

4

13

112

14,226

Feb 2

$PLTR will release its Q4 today.

I've been obsessively studying the company for 4 years.

Here are a few thoughts:

1. Massive opportunity to shape the narrative

While all enterprise SaaS say "AI", only Palantir it is proving it is delivering massive outcomes at scale, in any industry.

Palantir stock has been hit as fear has risen about SaaS companies.

Karp can control the narrative by showing how Palantir's results keep diverging.

Others continue their path. Palantir takes ground.

2. Analysts keep underestimating

I see analysts underestimating:

• the strength of growth;

• the durability of growth;

• margins expansion potential.

The 116x EV/FCF NTM valuation is high, but based on low estimates.

aka it could be actually cheap.

3. The Partner Ecosystem is exploding

The partner ecosystem (3rd party consultants selling pltr) is exploding.

This means:

• new clients = growth;

• growth at almost no cost = higher margins;

• brand awareness = pricing power.

eg. It's partner @NorthslopeAI just raised $22mn after its Revenue 7x.

4. General investors still have no idea

Avg. investor awareness ignores:

• Warp Speed;

• AI FDE;

• Hive Mind.

These products will be the key drivers of growth in the coming years.

Others will fail to catch up.

5. Escape velocity makes the delta widen

After ~3 years since AIP's launch, there is still no real competitor from big tech.

There is a trend of building the "Palantir of X" as companies try to clone the FDE model.

This will only increase awareness, but it will not become real competition. You need to eat pain for many years to deliver the product quality Palantir has, and having access to the most critical use cases is not easy.

Competitors now face a Palantir that is 10x faster at building products.

Good luck.

6. Others buy. Palantir builds

$NOW spent $10bn in M&A in 2025 and nothing revolutionary is coming out of it.

$SNOW bought in 2025 Crunchy Data, Datavolo, and TruEra AI. It is now eyeing a $1bn acquisition for Observe.

Meanwhile, Palantir is dominating by building new products on its tech stack.

Who's the boss?

7. 2026 Guidance is key.

The true focus will be on 26' guidance. Markets want to see strong growth.

$NOW dropped 10% despite strong results, probably because its guidance is just continuing at 22% growth.

$PLTR Analysts see 43% growth for 2026, implying a deceleration, which I don't see as likely.

The best Palantir is yet to come.

----

$PLTR stock dropped sharply after its spectacular Q3 results.

Will this time be different?

Yours,

@arny_trezzi

59

74

723

65,402

10 Dec 2025

Attacco alla Supply Chain di Asus. Everest sostiene di aver compromesso anche Qualcomm e ArcSoft

📌 Link all'articolo : redhotcyber.com/post/attacco…

#redhotcyber #news #cybersecurity #hacking #malware #ransomware #datavolo #asus #qualcomm #arcsoft

2

177

2 Nov 2025

Imagine a world where your data is not just stored but transformed into actionable insights with just a few words.

Welcome to the future of data management with $SNOW, a company revolutionizing how businesses interact with their information.

Snowflake’s innovative revenue model, which charges based on platform usage, aligns perfectly with its clients’ interests, though it can lead to revenue fluctuations.

In today’s uncertain economic climate, customers are optimizing their usage, leading to shorter contracts. However, Snowflake is turning the tide with its cutting-edge AI solutions.

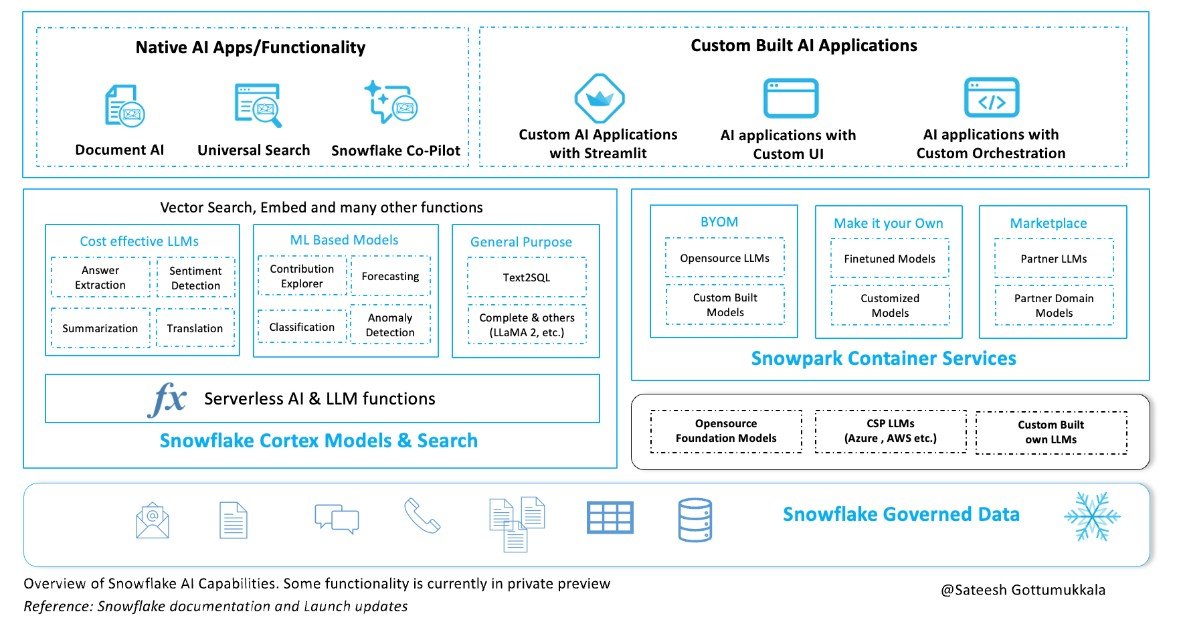

Enter Snowflake Intelligence, a groundbreaking agentic AI platform that lets users engage with their data using natural language, unlocking insights without the hassle of moving data between systems.

Complementing this is Cortex AI SQL, which integrates large language model capabilities directly into SQL databases, further enhancing data analysis.

The acquisition of Crunchy Data has brought Snowflake Postgres into the fold, empowering developers to build AI applications for Online Transaction Processing on the robust Postgres database.

Meanwhile, Snowflake OpenFlow, derived from the Datavolo acquisition, is making waves in the $17 billion data integration market by seamlessly integrating structured and unstructured data, supporting change data capture, and more.

For enterprises looking to migrate Spark workloads, Snowpark Connect for Apache Spark offers a smooth transition to Snowflake’s system.

These AI-driven innovations are not only attracting new customers but also increasing usage among existing ones.

With all these advancements, it’s no wonder that Snowflake is poised for significant growth, and I am increasingly optimistic about its future prospects.

Could Snowflake be the next big success story in the tech world? Only time will tell, but the signs are promising.

8

770

14 Oct 2025

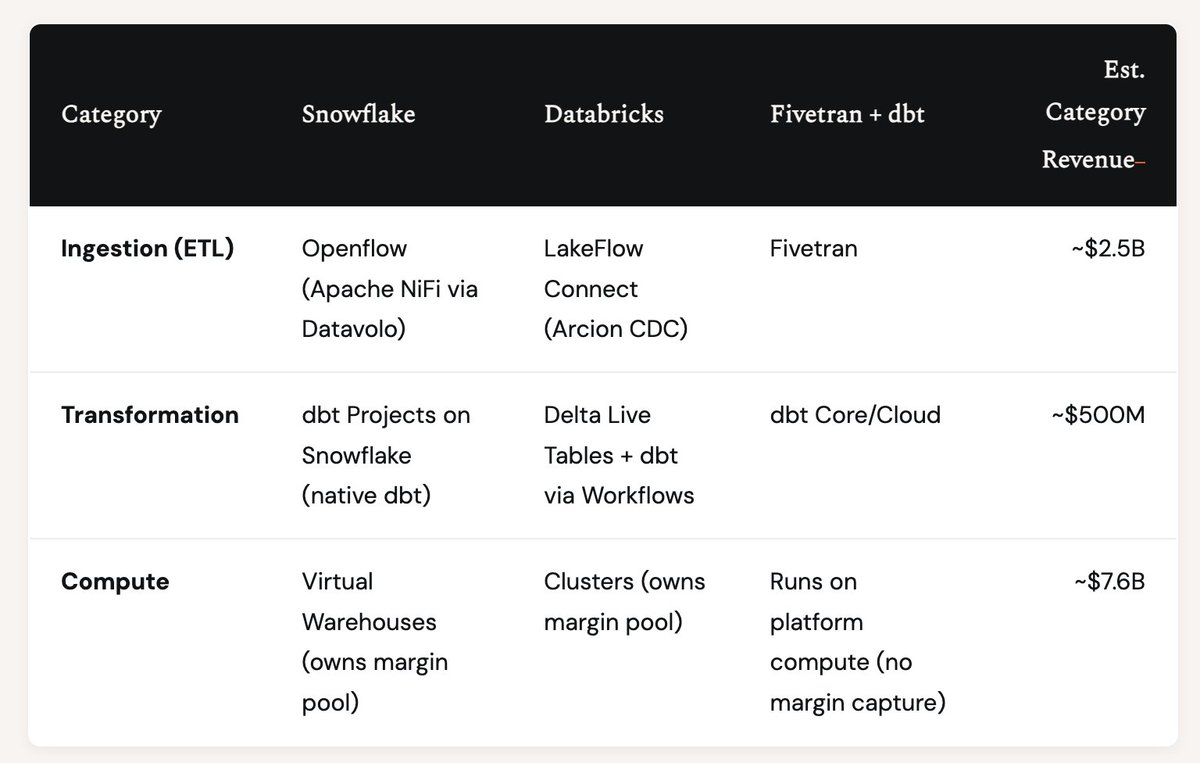

Why was the Fivetran-dbt merger all but inevitable?

Fivetran & dbt Labs announced their merger yesterday. The all-stock deal combines two companies into an entity approaching $600 million in ARR.

The beauty of the modern data stack was the explosion in choice. As the cloud exploded onto the scene, the legacy data warehouse was replaced by a collection of fast-moving platforms. In that era, specialization won. The pendulum is now swinging back towards consolidation.

Why? The answer lies in compute economics & revenue scale asymmetry. The table below shows why.

There are three different categories of software within this subset of the ecosystem:

1. Ingestion takes data from software & moves it into a cloud data warehouse. Snowflake acquired Datavolo, which commercializes the open source product Apache NiFi, calling it Openflow. Databricks acquired Arcion for ingestion through change data capture, calling it LakeFlow Connect. Fivetran focuses exclusively on this layer.

2. Transformation means reformatting the data within the cloud data warehouse. Snowflake launched native dbt Projects on Snowflake. Databricks offers Delta Live Tables, native SQL, & Python, plus supports hosted dbt through Databricks Workflows. dbt Core/Cloud is the leading independent transformation tool.

3. Compute revenue is generated when we ask questions of our data. Snowflake remains one of the leaders in structured data analysis with their cloud data warehouse. Databricks’ compute is their own as well.

Here’s the asymmetry in one number. Compute represents 72% of the overall market ($7.6B of $10.6B). As a result of their massive operations, Snowflake & Databricks exert significant gravity within the ecosystem. They have expanded beyond the compute market to impose their presence & capture marginal revenue within customers, pressuring the competitive ecosystem.

That’s not to say these components are independent. George Fraser analyzed Snowflake workloads in September 2024, finding transformation represents 40-45% of total Snowflake compute, which means even at smaller scales, startups can have significant impact on these behemoth businesses.

The Fivetran-dbt merger is an inevitable evolution of a maturing market. Two unicorns must partner to compete against two decacorns. They solve two of the three customer problems. But not yet compute.

One could surmise this consolidation signals the end of the modern data stack. I view it differently. The MDS has succeeded beyond our expectations. The stakes are higher now. Broad platforms, fast growth, & AI-native architectures define the next phase. Expect more consolidation.

Category revenue estimates based on public disclosures & company filings. Ingestion: Informatica ($1.64B FY2024), Fivetran ($300M est.), Talend ($350M), others ($200M est.). Transformation: dbt Labs ($300M est.), others ($200M est.). Compute: Snowflake ($3.6B FY2025), Databricks ($4.0B ARR Aug 2025).

tomtunguz.com/fivetran-dbt-m…

8

4

55

9,351

30 Aug 2025

$MRVL

公布FY2Q26財報

2Q26營收20.06億美元( 5.85% QoQ, 57.6% YOY),Non-GAAP毛利率59.4%,不如市場預期,係因Data Center業務增長不夠強勁。Non-GAAP營業費用4.93億,低於公司預期,因此Non-GAAP EPS $0.67( 9.0% QoQ, 121.3% YoY),營運槓桿顯著。本季度以25億美元完成汽車乙太網業務的出售。

Data Center營收14.90億( 3.4% QoQ, 69.1% YoY),不如市場預期的15.15億,營收增長仍由AI應用(電光學和Custom ASIC)帶動,約佔3/4以上資料中心營收,800G DSP需求強勁,1.6T DSP向多家客戶出貨,採用度將加速,管理層預期第三季電光學產品季增雙位數,然Custom ASIC業務受到客戶拉貨節奏影響,預期將與第二季持平,第四季才會顯著季增,因此Data Center營收第三季預計季持平。

展望第三季,管理層預期營收20.6億美元,不如市場預期的21.1億,Non-GAAP毛利率預期59.5 – 60%,較上季指引區間高,推測係因低毛利率的Custom業務季持平,Non-GAAP EPS 0.69 – 0.79,中位數符合市場預期。整體來看,第二季法說幾個重點:(1) Custom ASIC指引僅季持平,另投資人擔心公司在Amazon ASIC份額下滑,然管理曾表示第四季將顯著高於第三季,(2) 自6月的Custom AI Event以來,仍有新增數十億美元生命週期的design wins,(3) 電光學業務可見度仍高,且2026年加速器規模帶動的光模組需求預期較原本高,可望成為DSP營收潛在增量。研究處仍維持2027財年(CY 2026)EPS $3.17美元的預估,盤後股價對應Forward P/E約22倍,回到近五年區間下緣,已適度反應潛在風險,基於2027財年Maia ASIC與多個XPU attach專案挹注營收,投資建議買進,目標價 $89(FY2027 EPS x 30倍P/E)。

Snowflake 公布 FY2Q26 財報

Snowflake FY2Q26產品營收 10.9 億美元,高於市場預期的 10.4 億美元,年增率從一季度的 26% 躍升至 31.5%;RPO金額年增 33% 達到 69.32 億美元,大幅優於市場預期的 67.75 億美元,反映未來營收能見度依然穩固;净營收留存率穩定維持在 125%,顯示既有客戶在產品中的消費意願穩定提升。二季度財報展現了強勁的營運表現,多項關鍵指標超出市場預期,成長動能再度加速,帶動股價上漲 20%。獲利方面,Non-GAAP 產品毛利率 76.4%,Non-GAAP 營業利潤率 11%,優於市場預期的 8%,主要受惠於超乎預期的營收表現。管理層上調全年產品營收指引至 43.95 億美元,年增長率 27%,Non-GAAP 產品毛利率 75%,Non-GAAP 營業利潤率 9%,調整後自由現金流利潤率 25%。

本次財報的亮點不只是業績超預期,更在於其背後的成長驅動力,尤其是 AI 策略的成功落地,AI 不再只是願景,而是實質的業務引擎。本季近 50% 的新客戶是受 Snowflake 的 AI 工具 CortexAI 和 Snow Intelligence 所吸引,且平台上已有超過 6,100 個帳戶每週使用其 AI 功能,本季新增 50 家年營收貢獻超過 100 萬美元的客戶,創下公司紀錄,顯示 Snowflake 在大型企業市場的滲透率持續提高。公司加强與微軟 Azure 合作關係,客戶在 Azure 上的使用 Snowflake 產品營收年增 40%,以及透過收購 Crunchy Data 的 PostgreSQL 和 Datavolo 的 Openflow 平台拓展的新產品線,也開始貢獻營收。

研究處持續看好 Snowflake 的轉型策略,從結構型資料倉儲平台轉向非結構型資料湖平台,Cortex AI 在 Gen AI 推動下帶來需求量的提升,維持 RPO 增速在 30% 以上高成長,利潤率在今年逐季好轉看法不變。SNOW 面對的客群從來都不是科技業或 AI 開發者,而是傳統大型企業,這些客戶後端資料庫或 ERP 系統仍是以結構型資料爲主,當導入 Gen AI 之後,結構化和非結構之間的資料處理需求將隨之成長,成爲 SNOW 未來的成長關鍵。目標價 263 美元(18 倍 PSR * FY207 RPS 14.6 美元)。

15

2,276

Preview| $SNOW 2Q25:Snowpark 2.0 on the Horizon

Snowpark Connect, Iceberg, OpenFlow, OpenAI

We conducted channel checks with four SNOW partners and gathered additional insights through cross-referencing.

Our Q2 research revealed that Snowpark just completed a big update. The new Snowpark Connect feature is essentially Snowpark 2.0, but because it changes Snowpark's coding methodology, it may have a negative impact on 2Q25 while driving meaningful upside in 2H25.

We also observed strong Iceberg performance in 2Q25, with increasing customer mentions of OpenFlow from SNOW's 4Q25 Datavolo acquisition.

Detailed Report

open.substack.com/pub/fundam…

1

3

7,582

13 Jul 2025

Here are some promising, lesser-known American AI startups founded in 2023 or 2024 that are building *open* solutions and could soon rival or surpass current leaders like KIMI-2K:

Together AI (founded 2023, San Francisco): Specializes in open-source generative AI infrastructure, making it easier for developers to build and deploy large-scale AI models.

Cognition (founded November 2023): An applied AI lab already valued near $2 billion, working on advanced AI models and tools for developers and enterprises.

Unstructured (founded 2023): Focuses on open-source tools to extract and transform messy, unstructured data for use in large language models and vector databases—already seeing strong adoption among developers.

Datavolo (founded 2023): Builds open-source solutions to help generative AI models access and process unstructured data, making AI more powerful and flexible for businesses.

These startups are attracting major funding and developer interest, and while they may not be as famous as KIMI-2K yet, their open and innovative approaches are putting them on the fast track to becoming industry leaders.

1

27

28 May 2025

$SNOW earnings review (better late than never)

🔼Price: $179 -> $192 pre-earnings to next day open; now at $205

My take

- Strong results ✅ Sales✅ EPS ✅Guide

- Was 12x fwd revenue pre-earnings, now 14x; seems fully valued, but could argue that should trade like other platforms ($NOW at 15x)

- Doubling down on interoperability with Datavolo acquisition and $MSFT Azure partnership - this was a big strategic shift after @RamaswmySridhar took the helm

- $CRM buying Informatica shows that the data platform is THE key piece in the AI stack - very bullish for SNOW's strategic position, though, this means competition is going to intensify

Good

- Product velocity and AI adoption is strong (5,200 accounts using on weekly basis)

- Clear that SNOW benefits both directly from AI workloads and indirectly through the move of data to the cloud as a result of AI

- Datavolo and $MSFT Azure partnerships shows embrace of openness

- Federal government certification unlocks new TAM; great use case fit as government wants to share data across departments

- Data analyst workflow has potential for major productivity boost with agents workflows

Bad

- Nothing bad really, though NRR continues to decline (126->124%); should AI adoption reverse this or does this speak to a natural evolution?

- The future will only be more competitive (CRM, NOW, AWS, Azure, GCP, Databricks, etc.) - everyone wants to own the data platform

4

367

26 May 2025

$SNOW Snowflake Inc. Earnings Call Key Highlights:

📊 Robust Q1 Product Revenue and Accelerated Growth Outlook

Q1 FY26 product revenue reached $997M, up 26% YoY (28% excluding leap year), maintaining consistent growth momentum.

Remaining performance obligations (RPO) totaled $6.7B, reflecting 34% YoY growth.

Net revenue retention remained strong at 124%, demonstrating durable customer expansion.

FY26 revenue guidance raised to $4.325B, reflecting 25% YoY growth, underpinned by stable consumption and strong pipeline visibility.

🚀 Expanding AI Footprint and Rapid Cortex Adoption

Over 5,200 accounts now use Snowflake’s AI/ML capabilities weekly, highlighting rapid adoption of Cortex AI.

Cortex Agents launched to drive enterprise agentic AI workflows; customers include Kraft Heinz, Samsung Ads, and Luminate Data.

Cortex integrates Meta's Llama 4 and supports OpenAI models through Azure, offering customers flexible, best-in-class model access.

AI-powered internal tools like KHAI (Kraft Heinz AI) and sales enablement assistants highlight practical AI deployment at scale.

🔄 Enterprise-Grade Data Lifecycle Expansion

Snowflake Connectors (from Datavolo acquisition) enable seamless data integration from platforms like Google Drive, Workday, Slack, and SharePoint.

Apache Iceberg now supports Snowflake data sharing and security features, enhancing flexibility for open table formats.

Dynamic Tables and Snowpark outperformed expectations; increasingly used for managing complex data pipelines and reducing third-party tool reliance.

Dentsu cut costs by 30% using Snowflake for simplified architecture and secure marketing analytics through Data Clean Rooms.

🏥 Diverse Industry Traction and Mission-Critical Use Cases

Siemens is using Snowflake to unify operational and IT data to improve manufacturing processes.

AstraZeneca analyzes SAP and Workday data via Snowflake for better healthcare decision-making.

Automotive customers like Nissan and CarMax leverage Snowflake for real-time insights and customer personalization.

Expansion into the public sector via Snowflake Public Sector, Inc. and DoD IL authorization broadens addressable market.

📈 Operational Efficiency and Margin Expansion

Q1 non-GAAP product gross margin of 75.7%; operating margin of 9%, up 442 bps YoY.

Adjusted free cash flow margin reached 20%; FY26 target remains at 25%.

Increased focus on productivity and automation across engineering and go-to-market teams.

Robust hiring in Q1 supports strategic growth areas, including AI, public sector, and global enterprise sales.

💻 Platform Cohesion and Developer Productivity Enhancements

Released over 125 product features in Q1, doubling YoY, showcasing rapid innovation cadence.

Cortex Analyst and Notebooks streamline SQL and Python query generation, boosting developer efficiency.

Embedded model development and inference optimization help reduce latency and costs in AI workloads.

Snowflake’s semantic layer integration into Office Copilot allows enterprise data use within productivity tools.

🔐 Strategic Go-to-Market Execution and Record Customer Adds

Added 451 net new customers in Q1, a 19% YoY increase, supported by dedicated acquisition teams and focused segment motions.

Two $100M renewals (in financial services) closed in Q1 after delays in Q4; variability deemed normal within consumption model.

Specialist teams in AI and data engineering enable sales enablement and faster deployment of complex workloads.

Bookings strength attributed to strong customer confidence in Snowflake’s multi-year data and AI strategies.

🧠 AI-Native Data Strategy Becoming Core to Customer Adoption

Customers increasingly view Snowflake as the foundation for AI readiness, integrating structured and unstructured data.

Cortex unlocks new use cases in analytics, document indexing, search, and multi-agent orchestration.

Data strategy is now synonymous with AI strategy among Snowflake customers, embedding AI into the heart of business operations.

Migration tools enhanced with AI for faster legacy system replacement; SnowConvert now available broadly with AI-driven test automation.

🏛️ Competitive Positioning and Partnerships Strengthened

Continued close partnerships with Azure and AWS support hybrid deployments, including OneLake integration and Azure-hosted models.

Snowflake differentiates by offering end-to-end simplicity, performance, and governance, minimizing multi-tool complexity.

Supports both proprietary and open-source ecosystems (e.g., Iceberg), enabling customer flexibility.

Embedding Snowflake across agentic AI and LLM-based data workflows creates high switching costs and platform stickiness.

🏗️ Strategic CapEx and Repurchase Program Update

Q1 CapEx increased due to new office builds (San Mateo, Bellevue); future real estate spending expected to normalize.

Repurchased $491M of shares in Q1 at ~$152.63/share; $1.5B remains under authorization through March 2027.

Cash and equivalents stood at $4.9B at quarter-end, providing ample financial flexibility for long-term investments and M&A.

4

270

【美股 $SNOW 日线看涨220】

Snowflake Inc. (SNOW) 是一家领先的云数据平台提供商,其业务模式基于数据云,专注于帮助客户整合数据、推动业务洞察、构建数据驱动应用以及实现数据共享和人工智能(AI)解决方案。

2025财年第一季度(2024年2月-4月):收入8.29亿美元,同比增长33%。

第二季度(2024年5月-7月):收入8.69亿美元,同比增长29%。

第三季度(2024年8月-10月):收入9.42亿美元,同比增长29%。

第四季度指导(2024年11月-2025年1月):产品收入预计9.10亿美元。

全年预期:2025财年产品收入约33.56亿美元,总收入预计34-35亿美元,同比增长28%-30%。

客户增长:客户总数10,249家( 21%),高价值客户(年收入超100万美元)510家( 28%)。

净收入留存率:127%-128%,客户支出持续增加。

AI 需求:AI 数据云支持生成式 AI 应用,吸引更多企业。

使用量驱动:数据处理和存储需求增长推动收入。

展望

2026财年收入增长预计20%-25%,长期目标2028-2029财年实现100亿美元产品收入。

核心业务

Snowflake 提供云原生数据平台,支持数据仓库、数据湖、数据科学和 AI 工作负载,覆盖多云(AWS、Azure、Google Cloud)。核心优势:

统一平台:整合结构化和非结构化数据。

高性能:计算与存储分离,优化并发处理。

AI 能力:ClearQuery 支持自然语言查询,与 Azure OpenAI 集成。

数据共享:安全高效的数据协作,降低成本。

市场与竞争

定位:服务金融、零售、科技等行业,40%《财富2000强》企业为客户。

竞争对手:Amazon Redshift、Google BigQuery、Databricks、Confluent。

新动态:2024年11月收购 Datavolo,增强多模态数据管道;拟收购 Redpanda,与 Confluent 竞争。

战略

产品创新:推出无服务器产品,65 算法支持,模型准确度达80%。

合作:深化与 Microsoft 合作,优化 AI 功能。

多云战略:灵活支持三大云平台。

风险

竞争:Databricks 在数据湖和 AI 领域威胁加剧。

总结

收入:2025财年收入预计34-35亿美元,AI 和客户增长为主要动力,AI 数据云平台具领先优势,需快速完成收购和合作巩固行业地位。

转载时必须注明原出处:x.com/optiondt及原作者:美股翻倍哥,并不得侵害原作者的其他合法权益,如不得擅自篡改原作者姓名、不得擅自变更文章内容。

--------------

目前群已满,不再增加免费成员,请需要开通会员再进群谢谢!

加入美股翻倍群将: 1.得到准确的高胜率直播开仓信息,避免看反方向,导致不必要的损失!2.每天盘前获取通过当天数据,人工分析的美股纳指标普和7大个股的重要点位,3.免费获取2025翻倍群内部指标

美股翻倍群(discord.gg/meigu)

#美股 #美股期权 #Snowflake $snow

4

3

5

2,216

9 Apr 2025

$SNOW Snowflake announced expanded support for Apache Iceberg, offering customers access to open table formats without sacrificing performance, governance, or security. This integration allows data to be activated with zero movement, helping organizations advance open lakehouse architectures and AI strategies.

Customers can now run Iceberg tables on Snowflake’s compute engine and use features like Search Optimization and Query Acceleration Services. Snowflake also introduced data replication and disaster recovery for Iceberg (currently in private preview), bringing enhanced resilience to open data environments.

Snowflake is enabling secure data sharing across Iceberg tables, aligning with its broader investment in open data ecosystems. Thirty-five percent of Snowflake’s acquisitions over the past four years supported this strategy. Key contributions include Apache Iceberg, Apache Polaris, and integrations with technologies like Modin, Datavolo, Streamlit, and TruEra.

Customer feedback highlights Iceberg’s impact. Illumina improved data agility in manufacturing operations. Komodo Health accelerated insights from healthcare data using Iceberg and Polaris. Medidata cited increased speed and usability for clinical data. WHOOP emphasized interoperability without vendor lock-in.

3

802

27 Feb 2025

$SNOW CEO Sridhar Ramaswamy called Snowflake the “essential enterprise data and AI company on the planet right now” during an interview with CNBC’s Jon Fortt on Wednesday.

Like its peers, Snowflake has pushed to offer new artificial intelligence tools to its customers as the race for advanced large language models and AI capabilities accelerates. It announced an expanded partnership with Microsoft

Azure to offer access to OpenAI models on Wednesday.

Last quarter, the company announced a multiyear partnership with Anthropic and said it had agreed to buy startup Datavolo for an undisclosed sum.

3

1,160

$SNOW スノーフレーク決算メモ✍

✅️新製品の機能拡張により、今期の下期に前年比成長率が加速すると見ています。(約3年半ぶりに成長が加速する見込みです)

【好調な新製品】

1️⃣Snowparkとデータエンジニアリング機能:Snowparkは既にFY '25で全体のプロダクト売上の約3%を占め、データエンジニアリングの新機能(例:Dynamic Tables)とともに採用が進んでいます。

2️⃣AI関連製品

┗Cortex AI:構造化・非構造化データの両方に対応するデータエージェントをシームレスに構築できるプラットフォームとして、先進的な検索機能(Cortex Search)や分析機能(Cortex Analyst)を提供しています。

┗Cortex Agents:最近発表されたエージェントオーケストレーションフレームワークで、複雑なタスクの自動化や計画・実行を容易にし、スケールに合わせた運用を支援しています。

3️⃣新たなコネクタ群とデータ統合機能

Datavoloの技術を活用した新しいSnowflakeコネクタにより、SharePoint、Google Drive、Workday、Slackなど主要プラットフォームとのシームレスな連携が進み、顧客がさまざまなデータソースを効率的に統合できるようになっています。

✅広告分野におけるSnowflakeのAI活用

・Customer Data PlatformをSnowflake上で構築する企業も多いです。実際、Samoohaという企業を買収したのも、データクリーンルーム技術が広告効果測定やプライバシー保護に重要だと考えているからです。

・広告やマーケティング領域では“コンバージョンリフト”や“ROI測定”が鍵になりますが、それをSnowflake上で安全に行うことで大きな価値を提供できます。

・私たちのAI SQLのような拡張機能により、画像や動画などのマルチモーダル分析もSQL感覚で簡単に行えます。たとえば“クリスマスツリーの画像を入れると広告のクリックスルーがどれくらい上がるか”みたいな分析を手軽に実施できるようになる。生成AIの観点では、クリエイティブやコピーを自動生成するユースケースにもSnowflakeが役立つ可能性があると考えています。

スノーフレーク $SNOW Q4 2025決算カンファレンスコール翻訳📅2025-02-26

●会社側参加者

Jimmy Sexton - Head of IR

Sridhar Ramaswamy - CEO

Mike Scarpelli - CFO

Christian Kleinerman - EVP of Product

●アナリスト側参加者

Sanjit Singh - Morgan Stanley

Kirk Materne - Evercore ISI

Raimo Lenschow - Barclays

Brad Zelnick - Deutsche Bank

Brent Bracelin - Piper Sandler

Alex Zukin - Wolfe Research

Sonak Kolar - JPMorgan

Matt Martino - Goldman Sachs

Joel Fishbein - Truist Securities

Operator

「こんにちは。Snowflakeの2025会計年度第4四半期決算カンファレンスコールにご参加いただきありがとうございます。私の名前はマットで、本日のモデレーターを務めさせていただきます。プレゼンテーションの間はすべての回線をミュートとし、終了後にQ&Aの時間を設けます。[オペレーターによる操作説明] それでは、カンファレンスを弊社ホストであるインベスターリレーションズ責任者のジミー・セクストンにおつなぎします。ジミー、お願いいたします。」

Jimmy Sexton

「こんにちは。Snowflakeの2025会計年度第4四半期決算発表コールにご参加いただきありがとうございます。本日は、当社CEOのスリダー・ラマスワミ、CFOのマイク・スカルペリ、そしてQ&Aセッションにはプロダクト担当EVPのクリスチャン・クライナーマンが参加いたします。本日のコールでは、2025会計年度第4四半期の財務実績を振り返り、2026会計年度第1四半期および通年のガイダンスについてお話しします。

本日のコール中には、当社の事業運営や財務実績に関する将来見通しに言及する場合があります。これらの記述にはリスクや不確実性が伴い、実際の結果とは大きく異なる可能性があります。リスクや不確実性に関する情報は、当社の決算プレスリリース、最新のForm 10-KやForm 10-Q、その他のSEC提出書類に記載されています。すべての記述は、本日現在の入手可能な情報に基づいて行われるものであり、法律で義務付けられている場合を除き、それらを更新する義務を負いません。

また、本日のコールでは一部の非GAAPベースの財務指標についても議論します。GAAP指標との調整やビジネスメトリクスの定義は、当社の投資家向け資料をご参照ください。決算プレスリリースおよび投資家向けプレゼンテーションは、当社ウェブサイト(investors.snowflake.com)に掲載しています。なお、本日のコールのリプレイも同ウェブサイトに掲載予定です。

それでは、スリダーにマイクをお渡しします。」

Sridhar Ramaswamy

「ジミー、ありがとう。そして皆さん、こんにちは。本日はご参加いただきありがとうございます。1年で大きく変わるものですね。ちょうど1年前のこのコールで、私はSnowflakeの新CEOとして皆さんに紹介されました。この1年での当社の進歩を振り返ると、本当に驚くべき成果だと思っていますし、これほど誇りに思うことはありません。

当社のコアビジネスは非常に強固で、プロダクトの開発スピードは加速し、営業・マーケティングのエンジンも好調です。イノベーションの勢いはこれまでになく、すべてがうまくかみ合っています。そして、私たちは途方もなく大きな市場機会を目の前にしています。現在、Snowflakeは世界で最も重要なデータおよびAIの企業と言っても過言ではありません。先日の第3四半期のコールでお話ししたように、私たちの目指す先(ノーススター)はAIを活用したエンド・トゥ・エンドの世界最高のデータプラットフォームを提供することです。その実現に向け、日々大きく前進しており、嬉しく思います。

当社が実現している運営体制の厳格さにも強い誇りを感じます。効率性を高めながらも、成長分野への積極投資は変わらず行っています。そしてお客様に対する注力はかつてないほど強く、お客様からはSnowflakeは使いやすく、コストも抑えられ、多くの製品を組み合わせて利用しやすいといった声が寄せられています。当社がもたらす価値は非常に大きく、マルチプロダクトの採用が増加しているのもその証拠です。

私たちはさらにアクセルを踏み込みます。当社の強みを活かし、これからの機会に対して取り組む姿勢には一切の妥協がありません。この1年の好調を来年も継続すべく、迅速かつ的確な行動を取り続けます。

当社の堅実な第4四半期の業績を見ても、こうした進歩を確認いただけるでしょう。そして私たちはこれをまだ始めたばかりです。第4四半期のプロダクト売上は9億4,300万ドル、前年比28%増という力強い伸びでした。残存パフォーマンス債務(RPO)は69億ドルに達し、前年比33%増となりました。ネット・レベニュー・リテンションは非常に健全な126%を記録しています。

今期のNon-GAAPベースでの営業利益率は9%、Non-GAAP調整後のフリーキャッシュフロー比率は43%となりました。ご覧のように、またしても力強い売上成長と全体として非常に健全な数値を示すことができました。

先ほども申し上げたように、私たちは製品の連携(コヒージョン)をとことん追求しています。Snowflakeが市場で勝ち続けるのは、使いやすさ、サイロを取り払いコラボレーションや接続を可能にする点、そしてあらゆる規模・業界の企業から信頼されている点が理由です。だからこそ、ExxonMobil、Honeywell、London Stock Exchange Groupといった象徴的なブランドを含む数千もの企業がSnowflakeを中核としてビジネスを展開しているのです。

例えば、決済およびフィンテックを提供するグローバル企業のFiservは、Snowflakeを通じて自社の顧客企業向けにアナリティクスプラットフォームを提供することで、ビジネス変革を推進しています。Fiservの顧客は自社の取引データを活用し、市場情報を組み合わせ、自社のAIモデルを訓練することが容易になります。その結果、従来なら大企業にしか不可能だった高度な分析に基づいたビジネス上の判断を実現できるようになっています。

先日、私たちは当社最大のビルダー/開発者向けイベントである「Build Summit」を開催し、その後も世界各地で地域別のミートアップやイベントを実施しました。これまでに2万人を超える参加者が集まり、その製品ビジョンに対する非常に大きな期待と盛り上がりが感じられました。

Snowflakeのプラットフォーム上で開発し、構築し、イノベートすることがどれほど簡単か、多くのお客様から絶えず声をいただいています。また、Snowflakeの活用によってまったく新しい収益源、つまりデータを活用したマネタイズを実現している企業も数多く見受けられます。

例えばサプライチェーンのリーダー企業であるBlue Yonderは、Snowflakeのスケーラブルなデータ管理機能を活かし、AI駆動のインサイトを企業に提供することで、サプライチェーン運用を変革しています。Blue Yonderのプラットフォームは小売業者や製造業者、物流企業が在庫管理や配送最適化、混乱への対応をより効率的に行うため、毎日200億件以上のAI予測を処理しています。これは顧客企業が自社独力で構築するのがほぼ不可能な大規模なサプライチェーン・インテリジェンスを実現しています。

競合他社が依然として高コストなエンジニアリングリソースを必要とするのに対し、Snowflakeに切り替えることで、そのコスト削減効果がボトムラインに大きく寄与しているとの声も増えています。事実、Snowflakeに移行した顧客企業の多くが、他社システムの利用時より50%以上のコスト削減を達成しています。さらに先日、Snowflakeのネイティブ・コード変換ツールである「SnowConvert」が、OracleやTeradataなどさまざまなシステムからSnowflakeへの移行を加速するため、無償で利用できるようになりました。

Snowflakeはまた、エンタープライズ界における“循環系”としての役割も果たし始めています。データ共有やコラボレーションが可能であることは、Snowflakeのコアとなる差別化要素の1つです。Stripe、NTT、Brazeといった企業の多くが、すでに160社を超えるパートナーや顧客とデータ共有を積極的に行っています。こうした接続により、安全にデータを交換し、当社エコシステム全体にわたって価値をもたらしています。

開発スピードについても、かつてないほどの速さでイノベーションが進んでいます。昨年1年間で400以上の機能を市場に投入しましたが、これはその前の年の倍以上の数です。特にデータエンジニアリング分野の成長が著しく、Apache Icebergのようなオープンなデータ形式への対応が大きく進展しています。こうした取り組みにより、大規模なデータ管理とクエリがさらに容易になりました。さらに、Snowflake上で開発・連携する企業は急速に増えており、キャパシティ契約を締結しているお客様の3分の1以上が定期的にデータのコラボレーションを行っています。

AIについては、昨年が基盤固めの年となりました。当社は「Cortex AI」を導入し、現在では多くのお客様がこのCortex AIを使って、最先端の検索機能やアナリスト機能(Cortex Search/Analyst)を組み合わせ、構造化データと非構造化データ両方に対してシームレスにデータエージェントを構築しています。AnthropicのClaudeやMetaのLlama、DeepSeekなど市場をリードするモデルをサポートしており、先日発表したMicrosoftとの連携拡大により、OpenAIのモデルもCortexで利用可能となりました。これにより、AnthropicとOpenAI両方の最先端モデルをシームレスにホストできる唯一のデータプラットフォームとして、お客様のデータをSnowflakeのエッジで安全に管理しながらデータエージェントを構築できるようになります。

さらに数週間前には「Cortex Agents」を発表しました。これはAnthropicのClaudeなどの先進的なモデルを活用し、構造化データ/非構造化データを問わず、シームレスな計画策定とタスク実行を可能にする高度なエージェントオーケストレーションフレームワークです。Cortex AnalystやCortex Searchを活用することで、最先端の精度とエンタープライズレベルの信頼性およびガバナンスを両立し、顧客が大規模にエージェントを構築できるようになります。

そして本日、Microsoftとの連携をさらに強化し、Microsoft 365 CopilotおよびMicrosoft TeamsでCortex Agentsを提供すると発表しました。これにより、数百万人のユーザーがMicrosoftプラットフォームからシームレスに情報を入手し、生産性を高めることが可能になります。

私たちのイノベーションは、すべてお客様に真の価値を提供することにフォーカスしています。構造化/非構造化データのチャットボットを簡単につくれるようにし、データ基盤を整備することで、次に来るエージェントの転換点に向けて、お客様がAIの基礎を強化できるようにしています。

現在、毎週4,000社以上の顧客が当社のAIやML機能を利用しています。例えばAstraZenecaは、SnowflakeでAI活用可能な形にデータを統合することで、ヘルスケア分野に変革を起こしています。研究データを統合することで、新薬の発見や臨床開発のスピードを加速させ、2030年までに20の新薬を実用化するという野心的な目標に向けて取り組んでいます。また、世界の金融資産の10%を運用するState Streetは、Snowflake AIや機械学習を活用することで新たな市場インサイトを得て、より優れた投資判断を金融機関に提供しています。

AI製品の拡大が爆発的に進む一方、当社のコアビジネスも引き続き非常に好調です。私たちは、お客様のデータジャーニーにおいてエンドツーエンドの技術プロバイダーになることを目指していると何度もお話ししてきました。すでに複数の新しいSnowflakeコネクタをプライベートプレビューで提供開始しており、Datavolo買収で得た技術を活用し、SharePointやGoogle Drive、Workday、Slackなど主要プラットフォームとのシームレスなデータ連携・統合を実現します。お客様の反応は非常に好評で、非構造化データだけでなく構造化データにも柔軟に対応できる拡張性の高いプラットフォーム基盤を強化できています。

新しいイノベーションを市場に投入し続ける中で、私たちは効率的なスケーラビリティに注力しています。営業・マーケティング活動を強化しつつも、エンジニアリング、製品、マーケティング、セールスの各チーム間の連携を継続的に深めることで、既存顧客により多くの価値をもたらすだけでなく、新規顧客獲得でも成功を収めています。Cortex AI技術を社内でも活用し、営業担当は自然言語で質問をするだけで最適なセールス資料を見つけ出すことができ、当社独自のStreamlitアプリによって消費動向をリアルタイムで把握するなど、大幅に業務効率を高めています。

こうした運営の厳格さを徹底し続けることで、成長への投資と、全社のあらゆる部分における効率性の追求を両立させているのです。これこそが2025会計年度に確立した運営上の姿勢であり、今後も続けていきます。

それでは次に、マイクから財務の詳細をご説明します。」

Mike Scarpelli

「スリダー、ありがとう。さて、2025会計年度(FY ‘25)で当社のプロダクト売上は前年比30%増の35億ドルに達しました。当社のコアビジネスは強固なままです。ネット・レベニュー・リテンションが126%と安定した消費動向がみられるのもその証拠です。また、新製品が成長ドライバーとして重要になりつつあります。SnowparkはFY ‘25のプロダクト売上のうち3%を占めており、データエンジニアリングやAIの新機能も力強く採用が進んでいます。

第4四半期はテクノロジーセクターのお客様が想定を上回る結果を示し、金融サービスは引き続きトップの業種セグメントになっています。EMEA(欧州・中東・アフリカ地域)も好調でした。第4四半期のホリデーシーズンによる影響は我々の想定どおりでした。残存パフォーマンス債務(RPO)は前年比33%増です。

第4四半期中に、大口顧客の中には契約終了より先に容量を使い切り、売上が予約額を上回ったケースがありました。このような場合、通常は契約更新の時期を前倒しするか、従量課金による追加購入を選びます。大口顧客の場合、このような選択はよくあることで、将来の消費動向を示すわけではありません。

マージンに話を移します。FY ‘25のNon-GAAPベースプロダクト粗利益率は76%で、我々の予想どおりに着地しました。FY ‘25のNon-GAAPベース営業利益率は6%です。前四半期にも言及したように、効率化のため、チームの集約化や、若手採用の強化、不要な管理層の削減、継続的なパフォーマンス管理などを行ってきました。第4四半期には、これらの取り組みが実を結び、営業利益率は9%と予想を上回りました。FY ‘25のNon-GAAP調整後フリーキャッシュフロー比率は26%で、こちらは我々の見通しどおりです。

FY ‘25においては、19億ドルを自社株買いに投じ、1株あたり平均130.87ドルで1,480万株を買い戻しました。第4四半期には買い戻しは行っていません。現在、2027年3月まで有効な20億ドルの買い戻し枠が残っています。期末時点での現金及び現金同等物、短期および長期投資は53億ドルです。

次に今後の見通しについて話します。2026会計年度第1四半期(Q1)において、プロダクト売上は9億5,500万ドルから9億6,000万ドルの範囲を見込み、前年比21%から22%の成長となる見通しです。ご承知のとおり、Q1はうるう年の影響があり、前年比では比較が最も厳しい四半期となります。Q1のNon-GAAPベース営業利益率は5%を見込んでいます。このマージン見通しには、例年同様、第1四半期に開催するセールスキックオフイベントの費用(約1,500万ドル)を織り込んでいます。

FY ‘26(2026会計年度)通年では、プロダクト売上を42億8,000万ドル程度と見込み、前年比24%の成長としています。コアビジネスは引き続き安定した成長が見込めると考えています。一方で新製品の機能拡張により、下期に前年比成長率がステップアップすると見ています。いつも申し上げているように、パフォーマンス最適化による逆風はある程度織り込み済みです。前四半期にもお伝えしたように、今後は個別の機能ごとに詳細な予想を細かく切り出すことは行わない方針です。

マージンに移ります。Non-GAAPベースのプロダクト粗利益率は約75%を見込んでいます。長期的にはGPUの調達容易化やAI収益の拡大により、新製品機能に関連するプロダクト粗利益率が改善すると期待しています。Non-GAAPベースの営業利益率は通年で8%に拡大すると見込んでいます。Non-GAAP調整後フリーキャッシュフロー比率は25%を見込みます。

売上の高い成長と、より戦略的な採用計画、そしてAI活用による生産性向上により、株式報酬費用(SBC)の対売上比率にもプラスの影響が出るでしょう。FY ‘26ではSBCの対売上比率が37%程度に低下し(FY ‘25は41%)、今後も年々低下が続くと見ています。

なお、当社はInvestor Dayを6月2日の週にサンフランシスコで開催するSummitに合わせて実施します。参加をご希望の方はir@snowflake.comまでご連絡ください。

最後に、当社の提出書類を通じて私の退任計画についてご覧になったかと思います。後任者が見つかり、スムーズに業務が引き継がれるまで私はフルタイムでこの職にとどまります。FY ‘25に新CEOのスリダーのもとで当社はしっかり成果を上げており、2026年以降も成功に向けて万全だと考えています。今が私の後任に引き継ぐタイミングとして最適だと思っています。会社としては私の後任のCFO探しを開始しますが、適任者が決まり、その方への引き継ぎが完了するまで、私はフルタイムで続投します。」

Sridhar Ramaswamy

「マイク、質疑応答に入る前に少し言わせてください。この1年、あなたは素晴らしいパートナーでした。心から感謝していますし、これからもスムーズな引き継ぎに向けて協力してくれることをありがたく思います。Snowflakeが今日のような象徴的な企業になれたのは、長年にわたるあなたのリーダーシップの賜物です。社員を代表して、あなたのこれからを心から祝福したいと思いますし、今後の数カ月のうちにお祝いをしていきましょう。[音声途切れの可能性] では、質疑応答に入りましょう。」

質疑応答セッション

Operator

「[オペレーターによる操作案内] それでは最初の質問です。Morgan Stanleyのサンジット・シンさん、お願いいたします。」

Sanjit Singh (Morgan Stanley)

「ありがとうございます。こちらサンジット・シンです。スケールあるソフトウェア企業で、現状の環境下でも30%成長を達成するのはすごいですね。そしてマイク、長年にわたる素晴らしいキャリアへのお祝いを申し上げます。

まずはマイクへの質問です。第4四半期で、大口顧客が容量を使い切ったので追加のコミット契約をせず従量課金に移行したという件ですが、これはどの程度通常のことなのか、また近いうちにコミット契約を再度結ぶと考えていいのか教えてください。」

Mike Scarpelli

「ええ、当然、彼らはいずれ新しいコミット契約を結ぶと思います。ご存知のとおり、大口顧客の契約期間は基本的に3年が多いのですが、新規導入の段階では1年契約で開始し、その後3年契約に移行するお客様もいます。契約には、予想消費量に基づいた容量コミットが設定されていますが、そのコミットを契約期間終了前に使い切った場合、お客様には2つの選択肢があります。消費拡大を見越して早期更新をすることでより有利な条件を得るか、そのまま従量課金で契約期間終了まで購入するか、です。ただし、契約期間終了時には、同等以上の容量を再コミットしなければ、同じ価格条件は得られません。

こうしたケースは以前からあり、今回も第4四半期で大口顧客の一部に発生しましたが、いずれも今後1~6カ月の間に正式な新規コミット契約を結ぶと私は確信しています。」

Sridhar Ramaswamy

「付け加えると、こういった大口顧客が予定より早く容量を使い切るのは良いサインです。最初に設定した予想以上の消費をしているわけですから、こうしたアカウントの状況は総じて好調と見ています。契約更新のタイミングが若干前後することはあり得ますが、問題とは捉えていません。」

Sanjit Singh

「非常に納得できます。ありがとうございます。続いてスリダーへの質問です。マイクが新製品は下期に向けた成長ドライバーになるだろうとおっしゃっていました。ここ半年ほど、Snowflakeのプロダクト・イノベーションのペースが大きく加速しているように思います。データエンジニアリングのポートフォリオ、具体的にはSnowparkなどは順調に見えますが、AI/機械学習のアプリケーションプラットフォーム、特にOpenAIやAnthropicとの連携なども含め、そういった新しいワークロードが広く採用され、実際の売上増につながるのは、いつごろからと見ていますか?」

Sridhar Ramaswamy

「いい質問です。データエンジニアリング分野ではご存知のとおり、Snowparkのような機能を強化してきました。こちらについては既に力強い採用が進んでおり、Snowparkが駆動するビジネスが大きく拡張しています。さらに最近ではオープンデータフォーマット、特にIcebergをはじめとする最新の形式を活用することで、大規模アナリティクスをより容易に行えるようにしています。こうした技術的優位性が新しいユースケースをどんどん生み出しています。

AIに関しては、業界全体がまだ黎明期でありながら急速に成長している領域です。当社は「基盤を堅固にする」アプローチを取っており、例えばCortex Searchは世界トップクラスの性能を持つ検索機能を提供しており、当社はそのベンチマーク結果も公表しました。お客様が高い精度の検索機能や、自然言語で質問できるアナリスト機能をSnowflake上で利用できるわけです。

これらは単品で見ても価値がありますが、コネクタによって持ち込むデータ量を増やすほどSnowflakeプラットフォーム全体としての付加価値が増大します。保険の引受や法律文書の分析など、さまざまな業務アプリケーションをSnowflake上で構築し、AI機能と組み合わせる動きが加速しています。

私たちはAI技術を幅広く導入しているお客様の数を追跡していますが、すでに多くの導入が進んでおり、今後四半期を通じてさらなる売上への寄与が見込めると考えています。ただ、何よりも大事なのは、これらすべてがシームレスに繋がることです。コネクタ群を充実させることで、あらゆるデータをSnowflakeに取り込める(あるいはIcebergを通じてSnowflakeからアクセスできる)ようになり、Snowparkがデータエンジニアリングを促進し、その結果としてAIや機械学習向けの最適なデータ環境が整う。この相乗効果がSnowflakeの最大の強みです。確かに下期にはこれらが大きく売上に貢献してくると期待しています。」

Sanjit Singh

「大変参考になりました。ありがとうございます。」

Operator

「ご質問ありがとうございました。次の質問です。Evercore ISIのカーク・マターンさん、お願いします。」

Kirk Materne (Evercore ISI)

「ありがとうございます。素晴らしい決算おめでとうございます。マイクにも、Snowflakeでのこれまでの功績をお祝いしたいです。

スリダー、最近ではデータ企業がエンタープライズソフトウェアベンダーと提携する事例が多いように感じています。ServiceNowやSalesforceとSnowflakeが組んでいるケースもあれば、競合がSAPと組んだという話もあります。こうした発表をどう解釈すべきでしょうか?エンタープライズにおけるデータの“重心”がどこにあるのかをめぐる動きと捉えるべきでしょうか?またご見解があれば伺いたいです。

続いてマイクに簡単に質問ですが、今期に入ってセールスのインセンティブ設計に何か変更があるのか、教えてください。」

Sridhar Ramaswamy

「まず、マイクにインセンティブの話をしてもらいましょう。」

Mike Scarpelli

「そうですね、セールスのコンプモデルについて大きく変えたことはありませんが、やや軸足を戻した部分はあります。基本的には従来どおり変動報酬の中心は消費ベースの売上に連動していますが、契約金額(トータル・コントラクト・ブッキング)にもある程度のウェイトを置くことにしました。ただ、営業担当が最大の報酬を得るメイン指標は引き続き消費ベースの売上です。」

Sridhar Ramaswamy

「ではご質問の本題、データプラットフォームの重心の話に移ります。Snowflakeは“AIデータクラウド”を名乗っていますが、これはお客様にとってアナリティクスや予測といった観点で、私たちが最適解だという自負があるからです。実際、セールスフォースやServiceNow、GitHubなどからデータを取り込むコネクタは既に当社が提供しており、Snowflake上でこれらのデータを一括分析するユースケースは当社内でも日常的に行われています。

企業がこうしたSaaSアプリケーションのデータをSnowflakeに統合することで、BIや機械学習、あるいはAIエージェントを用いた新たなアプリケーション開発まで、多面的に活用できるようになります。これはSnowflakeが提供する価値の大きな部分です。たとえばSalesforceやServiceNow、SAPなどのアプリケーションベンダーが、自社のユースケースに限定した形でエージェントを提供するケースが今後増えるでしょう。ですがSnowflakeの立ち位置は水平的(Horizontal)なプラットフォームであり、お客様のデータがあらゆる形・場所から来ることを前提としています。そういった意味で、Snowflakeはデータの集中管理や一元化を強みに、幅広いパートナーと連携しつつ、最も効率的なデータ活用基盤を提供できるのです。

SAPとのパートナーシップに関しては、クリスチャンが少し補足します。」

Christian Kleinerman

「ええ、スリダーの言う通りです。私たちは常に双方向のデータ共有やデータ移動を行うパートナーシップを数多く結んできました。SAPとはまだ具体的なアナウンスはありませんが、現在協業を進めています。SAPの“Business Data Cloud”の動きにも注目しており、オープンなデータ環境を共に推進するという共通のコミットメントがありますので、近いうちに何か報告できるかもしれません。」

Kirk Materne

「ありがとうございました。」

Operator

「ご質問ありがとうございました。次はBarclaysのライモ・レンショウさんです。」

Raimo Lenschow (Barclays)

「ありがとうございます。素晴らしい決算おめでとうございます。そしてマイクにも、過去2年ほど大変お世話になりました。お疲れさまです。

まずスリダーに質問です。Snowflakeが今後進出し得る隣接領域についてどうお考えでしょうか?たとえば最近では“ストリーミング”にフォーカスしたソリューションに注目が集まっていますが、Snowflakeとしてはストリーミング分野をどう捉え、どう戦略を組むのか教えてください。

続いてマイクへの質問ですが、今年度のガイダンスの保守性についてどうお考えでしょう?昨年は新CEO就任やマクロ環境などで多少慎重だった印象ですが、今年はどう組み込まれていますか?」

Sridhar Ramaswamy

「まず、ストリーミングの領域についてですが、私たちは広範なパートナーと協力しており、データ領域は非常に広いので、自社で大きく投資する領域と、パートナーに任せる領域を明確にしています。一方で、ストリーミングやデータインジェスションはSnowflakeとしても重要な分野だと認識しており、一部は自社でソリューションを提供し、また一部はパートナーと連携して補完し合う形をとっています。

具体的にはストリーミングにもオンプレ型とクラウドネイティブ型などさまざまなアプローチがありますし、コネクタに関しても多面的なニーズがある。私たちはSnowflakeとしてネイティブに提供する部分をしっかり強化しつつ、他の技術ベンダーとの連携も継続します。Snowflake Intelligenceのように従来のBIを超えて新しいアプリケーション体験を提供する取り組みもありますが、これも私たちがエンドツーエンドのデータプラットフォームを目指す上で重要です。ですから、私たちは必要なところでは自社ソリューションを拡充し、それ以外の部分ではパートナーと連携するハイブリッドな戦略を取っています。」

Mike Scarpelli

「ガイダンスについてですが、例年通り“妥当な範囲”を提示しているつもりです。当社ほどの規模になると、3%の上振れがあれば大きな成果とみなされると思いますので、現時点ではこれが最適と感じています。第1四半期と通年のガイダンスも、我々としては信頼できるものだと考えています。繰り返しになりますが、まだ私もしばらくはSnowflakeにおりますので(笑)。」

Raimo Lenschow

「了解です。ありがとうございました。」

3

716

8 Feb 2025

【🇺🇸米国株新着レポート紹介:テクノロジー🚀】

💡弊社HP上で画像付きのレポートが無料でご覧いただけます

✅【テクノロジー:Part 3】スノーフレーク( $SNOW )では何ができるのか?ELTからETLへの流れと高度なRAG(検索拡張生成)との関係性に迫る!

✅【テクノロジー:Part 2】スノーフレーク( $SNOW )の強み:Apache NiFiを活用して高いセキュリティと拡張性を提供!

✅【テクノロジー:Part 1】スノーフレーク( $SNOW )DatavoloとNight Shift Development買収が将来性に与える影響とは?

#インベストリンゴ #米国株 #エヌビディア #高配当

2

3

470

2 Feb 2025

【🇺🇸米国株新着レポート紹介:テクノロジー🚀】

💡弊社HP上で画像付きのレポートが無料でご覧いただけます

✅【テクノロジー:Part 3】スノーフレーク( $SNOW )では何ができるのか?ELTからETLへの流れと高度なRAG(検索拡張生成)との関係性に迫る!

✅【テクノロジー:Part 2】スノーフレーク( $SNOW )の強み:Apache NiFiを活用して高いセキュリティと拡張性を提供!

✅【テクノロジー:Part 1】スノーフレーク( $SNOW )DatavoloとNight Shift Development買収が将来性に与える影響とは?

#インベストリンゴ #米国株 #エヌビディア #高配当

1

4

511

18 Jan 2025

Why is $SNOW My Top AI Play of 2025?

Enterprise Data Dominance

• Snowflake powers data operations for 754 Forbes Global 2000 companies -- showcasing its dominance in the enterprise data segment.

• The platform boasts 542 customers generating over $1M in trailing 12-month product revenue, a 25% YoY increase -- reflecting its scalability in serving high-value enterprise accounts.

• With RPO climbing 55% YoY to $5.7B -- Snowflake’s pay-as-you-go model positions it for sustained revenue growth as customers expand their usage.

AI Integration Driving Growth

• Cortex AI, Snowflake’s flagship AI offering, enables businesses to unlock actionable insights from unstructured data across sectors like finance, healthcare, and logistics.

• A partnership with Anthropic integrates Claude AI, empowering users to build predictive models, automate workflows, and generate real-time visualizations within Snowflake’s ecosystem.

• Strategic acquisitions -- including Datavolo, Neeva, and Applica -- bolster Snowflake’s AI capabilities, streamlining data engineering and accelerating enterprise adoption of AI technologies.

Massive TAM Growth in AI Markets

• Snowflake's TAM is projected to grow from $152B in 2023 to $350B by 2028 -- reflecting ~20% CAGR.

• $NVDA, the undisputed leader in AI hardware, uses Snowflake as its white-label service -- highlighting Snowflake’s reliability and scalability in the AI-driven digital economy.

• AI workloads are poised to drive Snowflake’s growth, with Gartner projecting that 90% of enterprise strategies will depend on AI-driven data platforms by 2026.

30

36

330

51,325