Apr 16

Greetings from Vienna, Blockchain Day

The crypto and blockchain market kept its steady climb in the past 24 hours. Total value rose nearly 1 percent to hover around 3.10 trillion dollars.

Bitcoin gained about 1 percent and sat comfortably near 105,000 dollars, once again acting as the calm anchor while everything else moves. Ethereum added roughly 0.05 percent while altcoins like Avalanche and Arbitrum enjoyed nice steady gains too.

The biggest spark came from a brand-new decentralized insurance platform that just went live on a leading chain. It lets regular people buy coverage for their crypto wallets, DeFi positions, or even everyday risks like flight delays using smart contracts, with claims paid automatically when conditions are met—no claims adjusters, no waiting, everything transparent and fast. Early users are already locking in protection for their holdings and seeing peace of mind plus small staking rewards on premiums. At the same time, a major traditional insurance giant rolled out hybrid policies that blend crypto payouts with real-world coverage, rewarding users with tokens for safe practices that can be traded or used for discounts.

On the global side, another Asian country just approved crypto for e-commerce settlements and merchant payments, making online shopping and business transactions quicker and cheaper for millions of buyers and sellers. A brief smart contract glitch hit one lending protocol during heavy usage but the team fixed it in minutes with zero losses.

The vibe stays optimistic and secure, finally letting everyday holders protect what they’ve built while mixing real-world safety nets with on-chain efficiency and keeping the big coins rock-solid. This new decentralized insurance platform could shield your portfolio from dips and surprises—what do you think, ready to safeguard your crypto and stop worrying about volatility? Drop your thoughts below! 🛡️ #Crypto #Bitcoin #Ethereum #Blockchain #DeFiInsurance

1

12

1,187

Apr 7

🧠 **Hugo's F1RP prediction poll:**

What will Hugo's Flare Improvement Radical Proposition be?

**I predict: 1:1 FLR lockup = $1 DeFi value** for all interactions!

What do YOU think? 👇

[poll: 1:1 Lockup / Oracles / FTSO / Other]

$FLR #FlareNetwork #XRPFi #FlareNetwork #FLR #XRPFi #BTCFi #Firelight #FlareRWA #FAssets #Songbird #DeFiInsurance #DriftHack #FlareFinance #FTSO #StateConnector #FIP #Flare1 #FlareDrops

6

3

39

2,156

Apr 6

$285M Drift hack in 60 SECONDS 😱

Firelight could've saved them...

Full breakdown 👉 youtu.be/4NNbTqv2lGk

Short 👉 youtu.be/uAQzsMvk-0A

#DriftHack #Firelight #DeFiInsurance #XRPFi

youtu.be/uAQzsMvk-0A

3

159

Building the Future of DeFi Risk Management 🛡️

We have officially partnered with @Spores_Network for the upcoming $TROY IDO!

TroyVest provides a dedicated Layer 3 infrastructure for volatility insurance, securing retail investors against market turbulence. By launching on Spores, we are aligning with a platform that shares our commitment to transparency and high-performance Web3 tech.

📊 Key Details:

▪️ Platform: Spores Launchpad

💎 Secure your spot:

launchpad.spores.app/ido/tro…

#TroyVest #DeFiInsurance #L3 #CryptoSecurity

7

33

54

4,143

Mar 15

😈 Meet SINS — the devilishly clever coin that watches your back when the rug pulls 😱🔥

Stake SINS → Earn premiums → Laugh at traders panicking 📈💀

Telegram bot live: @SolInsuranceBot

#Solana #DeFiInsurance #CryptoMeme #SINS

3

7

97

Mar 14

💥 STOP PANIC-SELLING! 💥

Introducing **SINS Token** — the first memeish Solana insurance for degens 🚀🔥

Stake SINS → Earn premiums → Protect your trades from rug pulls & crashes 💸

HODL your SINS, stay safe, get rewards

#Solana #DeFi #CryptoMeme #SINS #DeFiInsurance

4

59

What are your thoughts?

🇺🇸 DeFi insurance emerges as critical safeguard for onchain finance.

Opinion piece argues that **DeFi insurance** protocols are evolving into essential infrastructure — protecting users from smart contract exploits, hacks, and protocol failures in decentralized lending, trading, and yield farming.

Key points:

DeFi insurance covers on-chain risks traditional insurance can't easily address.

Protocols like Nexus Mutual, InsurAce, and emerging covers offer parametric and claim-based payouts.

Growth driven by rising TVL and institutional entry demanding risk mitigation tools.

Challenges remain: undercapitalization, oracle dependencies, and slow claim processes.

Author sees DeFi insurance maturing into a foundational layer — enabling safer scaling of onchain finance while building trust with TradFi participants.

Full story: cointelegraph.com/opinion/de…

#DeFiInsurance #OnchainFinance #DeFi #CryptoRisk #NexusMutual #BlockchainSecurity

3

22

Jan 7

How does @re handle risk management 🤔🐙

Risk assessment is done by experienced underwriting partners and licensed insurance professionals.

Collateral stays in secure onchain vaults, while every program is designed to reduce concentration and tail risk.

Calm capital. Clear structure. (Re)al risk control.

#ReProtocol #RiskManagement #OnChain #DeFiInsurance #Web3 #RealYield

9

39

273

19 Dec 2025

Why DEIN on Arbitrum Could Change How We Think About Risk in Web3

Every financial system no matter how advanced has one thing in common: RISK.

Something can break, fail, or behave in ways we didn’t expect. In traditional finance, institutions manage this risk for us - often behind closed doors.

#Web3 flips that idea on its head.

Instead of hiding risk, Web3 exposes it on-chain and now, with @DEIN_fi launching on @arbitrum, the ecosystem is getting tools that let users actively participate in how risk is priced and shared.

The Problem With Traditional Insurance And Why Web3 Needs Better

Traditional insurance is centralized by design. Decisions are slow, pricing is opaque, and access is limited by geography, paperwork, and approval processes.

In Web3, this model doesn’t scale.

Protocols move fast. Capital moves faster. But insurance has often lagged behind, leaving users exposed when things go wrong. What Web3 needs is insurance that’s as open and dynamic as the systems it protects.

That’s the gap @DEIN_fi is stepping into.

What Does “Permissionless Insurance” Mean?

Permissionless insurance means anyone can participate, without needing approval from a central authority.

How Permissionless Risk Markets Actually Work

Instead of a company deciding who gets coverage & at what price, DEIN turns insurance into a permissionless market.

Here’s the simple idea:

🔹Users who want protection can buy coverage instantly

🔹Other users provide capital & underwrite that risk

🔹Prices adjust dynamically based on market demand & perceived risk

Everything happens on-chain through smart contracts, removing delays & middlemen.

Risk becomes something the community manages together.

Why Arbitrum Makes This Possible

For #insurance markets to work on-chain, transactions need to be fast, cheap & liquid. High fees kill participation. Slow confirmations kill usability.

That’s why @arbitrum matters.

By leveraging Arbitrum’s low fees, high throughput, & deep liquidity, DEIN can support active insurance markets that feel responsive and accessible not experimental or clunky.

This is insurance built for scale.

What Makes DEIN Different

DEIN isn’t just “insurance on blockchain.” It introduces a different mindset.

✔️ It enables dynamic pricing, meaning risk is priced by the market in real time not by fixed assumptions.

✔️ It’s open by default. Anyone can underwrite risk or buy coverage without permission.

✔️ It’s composable. DEIN can integrate directly into DeFi apps, allowing protection to be built into user flows rather than added as an afterthought.

Together, these features make insurance a native part of the Web3 experience.

Imagine a DeFi protocol on Arbitrum launching a new product.

With DEIN:

🔹Users can immediately buy coverage against potential failures

🔹Liquidity providers underwrite that risk and earn returns

🔹Risk pricing adjusts as confidence in the protocol grows

Instead of fear slowing adoption, insurance becomes an enabler.

The Bigger Vision

The bigger vision behind DEIN is not just protection, it’s collective risk coordination.

As more value moves on-chain, ecosystems will need shared tools to manage uncertainty.

DEIN points toward a future where risk is transparent, tradable, and governed by market participants instead of institutions.

In that world, insurance isn’t a last resort - it’s infrastructure.

My View

To me, #DEIN arriving on Arbitrum signals that Web3 is growing up. We’re moving past just building protocols and starting to build safety nets.

Real adoption won’t come from higher yields alone. It will come when users feel confident enough to stay, build, and participate long-term. Open insurance markets are a big part of that confidence.

If Web3 is serious about replacing legacy finance, it needs systems that don’t just reward upside but also manage downside.

Source: x.com/DEIN_fi/status/2002016…

#Arbitrum #DeFiInsurance #OnchainRisk

DEIN is coming to @arbitrum! 🔵

Leveraging Arbitrum’s speed and deep liquidity, we are bringing permissionless insurance markets with dynamic pricing to the ecosystem.

Arbinauts will have access to risk markets by underwriting policies or purchasing coverage instantly.

5

46

124

12 Dec 2025

Here's a question I've been investigating: Does Lloyd's of London backing actually matter for crypto, or is it just marketing?

Let me show you the data.

DeFi exploits 2023-2024:

- 47 major exploits

- $2.3B total losses

- Community pool insurance payouts: $87M

- Coverage rate: 3.8%

That means 96.2% of exploit losses went uninsured.

Example: Euler Finance, March 2023

- $197M exploited

- Nexus Mutual coverage: $8M

- Actual coverage: 4%

Now compare insurance types:

Community Pools (Nexus Mutual, Unslashed):

- Capital: ~$300M total across all pools

- Coverage: Selective (only certain protocols)

- Payout process: DAO vote (can take weeks)

- Problem: Limited capital, major exploits exceed coverage

Lloyd's of London:

- Operating: 335 years

- Annual premiums: $50B

- Coverage: Institutional-grade contracts

- Payout process: Legal contract (no DAO vote needed)

The difference matters for boards.

When a treasury manager presents: "We'll use Nexus Mutual for insurance"

Board asks: "What happens if exploit exceeds their capital?"

Manager: "Uh... they might not be able to pay out fully?"

Board: "Denied."

When same manager presents: "Lloyd's of London backs this"

Board knows Lloyd's. They know Lloyd's survived:

- 1906 San Francisco earthquake

- 1912 Titanic sinking

- 2001 World Trade Center

- 2005 Hurricane Katrina

Lloyd's has 335-year track record of paying claims. That's institutional trust.

But here's the real question: What's the premium cost?

I tried calculating this based on traditional Lloyd's policies:

Institutional insurance typically costs:

- 0.5-2% of insured amount annually

- Higher for newer/riskier sectors

- Crypto likely 1-3% premium range

If @nilatoken MindWaveDAO insures $96M BTC treasury at 2% premium:

- Annual cost: $1.92M

- Target annual revenue: $11.5M-$17.3M

- Net after insurance: $9.58M-$15.38M

Still massively profitable vs 0% yield from pure HODLing.

The premium is expensive, but board psychology changes completely:

Without Lloyd's:

"We could lose everything with no recourse" → Rejected

With Lloyd's:

"We pay 2% premium for institutional coverage" → Approved

It's not about whether insurance is perfect. It's about whether boards can defend their decision to shareholders.

"We deployed into a strategy backed by Lloyd's of London" is defensible.

"We deployed into a DAO-governed community pool" is not.

Personal research conclusion:

Lloyd's backing isn't just marketing. It's the difference between:

- 5% board approval rate (DeFi without institutional insurance)

- 70% board approval rate (governed framework with Lloyd's)

The TAM increase is 14x even if yields are lower.

That's why institutional treasury infrastructure matters more than high APY protocols.

Watching $NILA for execution. If they actually deliver Lloyd's integration (not just partnership announcement), the thesis validates.

#DeFiInsurance #InstitutionalAdoption #RiskManagement #CryptoSecurity #MindWaveDAO #LloydsOfLondon

118

44

128

2,084

🚀 **Re-thinking insurance in crypto?** Meet **Re Protocol**—the decentralized safety net for DeFi risks! 🌐💡

Imagine a world where reinsurance isn’t locked behind Wall Street doors but lives on-chain, transparent and accessible. That’s **Re Protocol**: a **blockchain-powered reinsurance platform** where risk coverage meets DeFi innovation. 🛡️✨

🔹 **How it works**:

- **Decentralized reinsurance pools** let you underwrite or buy coverage for crypto risks (smart contract hacks, stablecoin depegs, and more).

- **Earn yields** by staking as a capital provider or **get protected** as a policyholder.

- Built for **scalability** and **transparency**—no opaque middlemen, just smart contracts doing the heavy lifting.

🔹 **Why it’s a game-changer**:

✅ **Community-driven**: Governed by $RE token holders.

✅ **Institutional-grade**: Backed by insurers and reinsurers bridging TradFi and DeFi.

✅ **Flexible coverage**: Tailor policies to your risk appetite.

🎯 **Join the movement**:

- Dive into the docs: [re.xyz](re.xyz)

- Chat with the community: [Discord](discord.gg/reprotocol) | [Telegram](t.me/re_protocol/1)

- Follow updates: [@reintern](x.com/REprotocol)

**DeFi needs a safety net. Re Protocol’s weaving it—one smart contract at a time.** ️💰

#ReProtocol #DeFiInsurance #BlockchainReinsurance #CryptoAlpha

2

4

53

🚀 **Re-thinking insurance in crypto?** Meet **Re Protocol**—the decentralized safety net for DeFi risks! 🌐💡

Imagine a world where reinsurance isn’t locked behind Wall Street doors but lives **on-chain**, open to everyone. That’s **Re Protocol**: a **community-driven reinsurance platform** where you can secure coverage, earn yields, and share risk—all powered by blockchain.

🔹 **Why Re?**

- **Decentralized reinsurance**: Tap into global risk pools without middlemen.

- **Coverage for crypto risks**: From smart contract hacks to stablecoin depegs, Re’s got your back.

- **Earn while you protect**: Stake, underwrite, or participate—rewards flow to the community.

- **Built for transparency**: Every claim, payout, and risk is **on-chain, verifiable, and trustless**.

🔹 **How it works**

1️⃣ **Insurers & partners** (like @coverre) bring real-world expertise.

2️⃣ **Risk pools** are funded by stakers and underwriters.

3️⃣ **Claims are assessed** by decentralized governance—no opaque committees.

🌍 **Join the movement**:

- Dive into the docs: [re.xyz/docs](docs.re.xyz)

- Chat with the community: [Discord](discord.gg/reprotocol) | [Telegram](t.me/re_protocol)

- Follow updates: [@reintern](x.com/REprotocol)

The future of insurance isn’t just **decentralized**—it’s **Re-invented**. ️💰

#ReProtocol #DeFiInsurance #BlockchainReinsurance #CryptoCoverage

2

23

28 Nov 2025

RE Project demonstrates strong risk management with a 92% ratio and $168M premiums TVL, signaling real capital backing.

Full on-chain collateral links Web3 to the real economy, boosting trust and sustainable growth.

@re #DeFiInsurance #OnChainCapital

3

10

92

26 Nov 2025

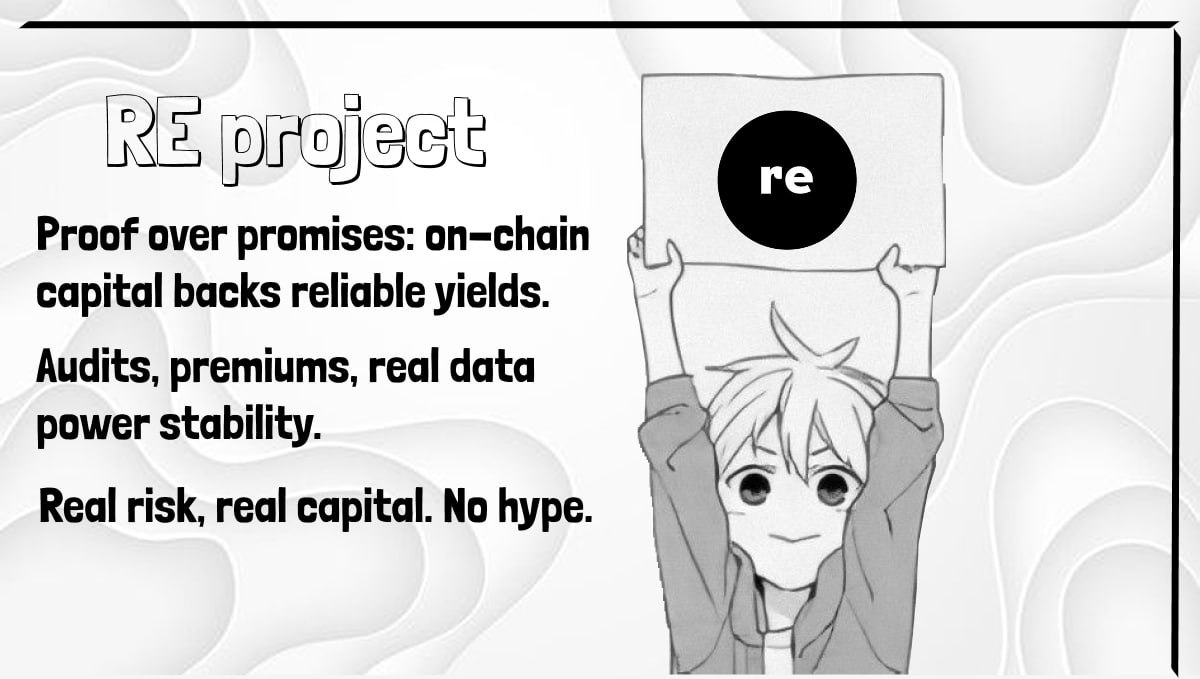

Proof over promises:

on-chain capital backs reliable yields, powered by audits, premiums, and real data.

Real risk, real capital, true stability—no hype.

Join the RE Project and invest with confidence.

@re #DeFiInsurance #OnChainCapital

3

11

51

25 Nov 2025

Diving into the future of insurance — fully on‑chain, programmable, transparent

Excited to build & grow in this re‑insurtech revolution 🚀🔗 #ReProtocol #DeFiInsurance

@ChazEevee

@twinkle2089

New Digital Art 🎭

3

10

71

🚀 **Re-thinking Insurance in Crypto? Meet Re Protocol—The Future of Decentralized Reinsurance!**

Imagine a world where crypto risks don’t keep you up at night. Enter **Re Protocol**—a groundbreaking decentralized reinsurance platform built on blockchain, designed to be your safety net in the wild west of DeFi. 🌐🛡️

**What is Re Protocol?**

Re Protocol isn’t just another insurance project—it’s a *reinvention*. By leveraging blockchain tech, it creates a transparent, community-driven marketplace for reinsurance. Think of it as the “DeFi backstop” that ensures coverage is fair, accessible, and resilient. No more centralized gatekeepers—just pure, decentralized protection.

**Why It’s a Game-Changer:**

🔹 **Decentralized Reinsurance:** Pool risk across a global network of insurers and reinsurers.

🔹 **Transparent Coverage:** Smart contracts automate payouts, so claims are swift and trustless.

🔹 **Earn While You Protect:** Participate as a coverage provider and earn rewards for backing risks.

🔹 **Built for Crypto Natives:** Covers everything from smart contract hacks to stablecoin depegs—because crypto risks need crypto solutions.

**Join the Movement:**

📖 Dive into the docs: [re.xyz](re.xyz)

🐦 Follow updates: [@reintern](x.com/REprotocol)

💬 Chat with the community: [Discord](discord.gg/reprotocol) | [Telegram](t.me/re_protocol/1)

The future of insurance is *decentralized*. The future is **Re Protocol**. Are you in?

#ReProtocol #DeFiInsurance #BlockchainReinsurance #CryptoCoverage

3

24

21 Nov 2025

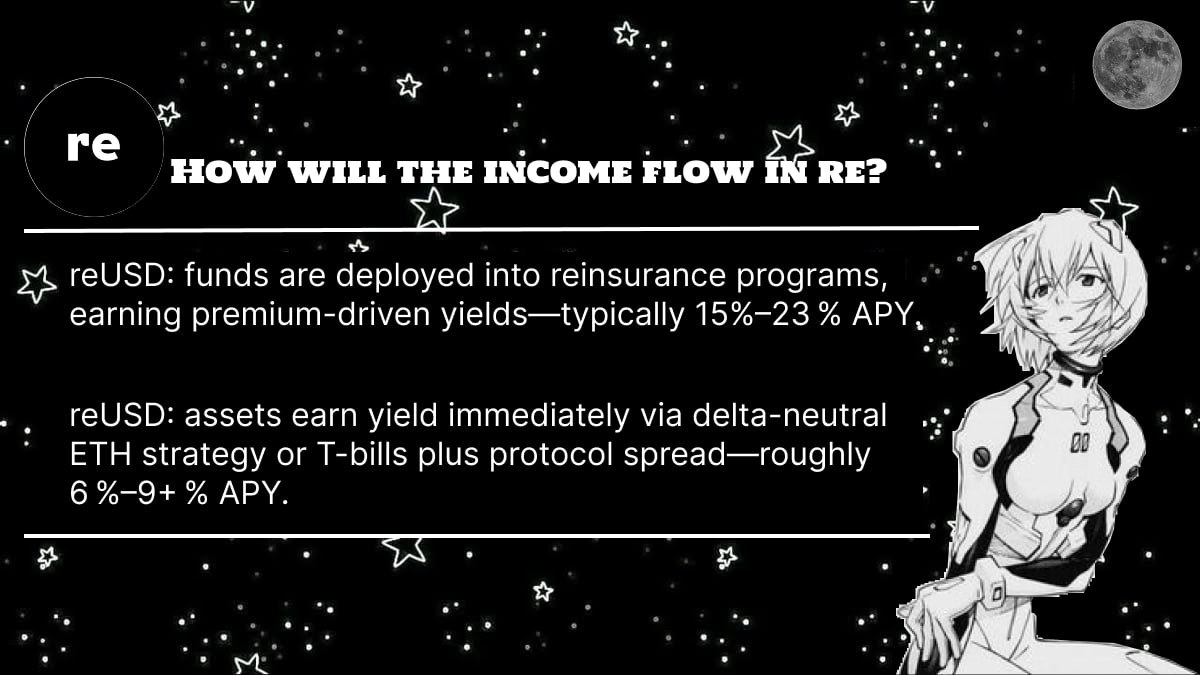

Explore re:💜

A DeFi system pairing reUSDe's reinsurance with delta-neutral ETH and T-bills.

Earn 15–23% APY from reUSDe and 6–9% APY from reUSD, powered by protocol spreads.

Safer, diversified yields in one trusted capital stack. Join us.😋

@re #DeFiInsurance

2

11

45

21 Nov 2025

Revolutionize your DeFi portfolio with @re

the decentralized reinsurance protocol bridging real-world risk to crypto capital! Earn stable yields via Insurance Alpha (up to 16% APY) or Basis-Plus strategies. Fully collateralized, transparent, and built for the future. Secure your spot in the global safety net! #DeFiInsurance #Web3

re.xyz

20 Nov 2025

Imagine a world where your DeFi bags are truly safe ,no matter the hack, rug, or black-swan event.

That world is here.

@re is building the global, decentralized insurance layer Web3 has been begging for.

Stake $RE. Protect the ecosystem. Earn real yield while sleeping peacefully🛡️✨

1

6

307

20 Nov 2025

Meet RE:💜

A safe project bridging traditional insurance markets and DeFi. Transparent risk management, audited safety, and real premiums back steady, predictable yields.

Invest with confidence in a trusted crypto future.💜

@re #DeFiInsurance

2

10

59

18 Nov 2025

Meet re:

A DeFi project blending real risk management with transparent pricing and audited safety.

Built for stability, predictable yields, and community-driven growth. Discover a safer, smarter crypto future with re.

@re #DeFiInsurance #SafeCrypto

9

61