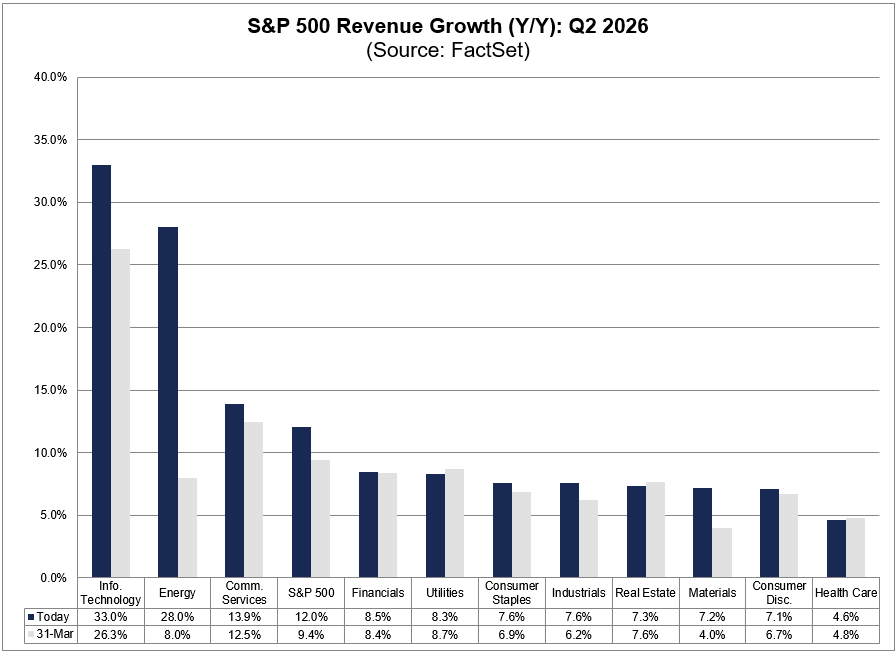

$SPX is expected to report Y/Y revenue growth of 12.0% for Q2 2026, which is above the estimate of 9.4% on March 31. #earnings, #earningsinsight, bit.ly/4w62Civ

3

16

2,979

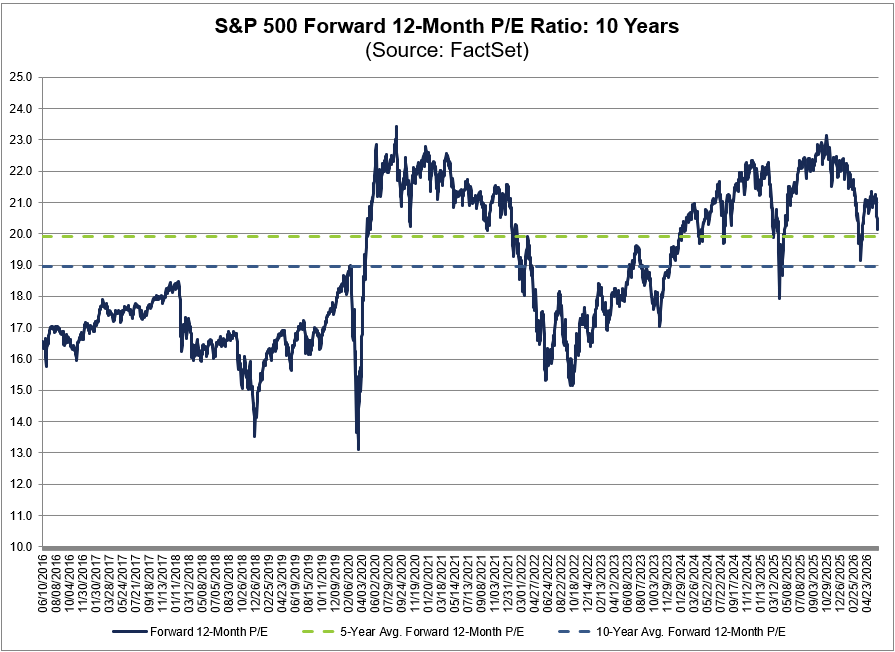

The forward 12-month P/E ratio for $SPX is 20.1, which is above the 5-year average (19.9) and above the 10-year average (19.0). #earnings, #earningsinsight, bit.ly/4w62Civ

6

14

2,546

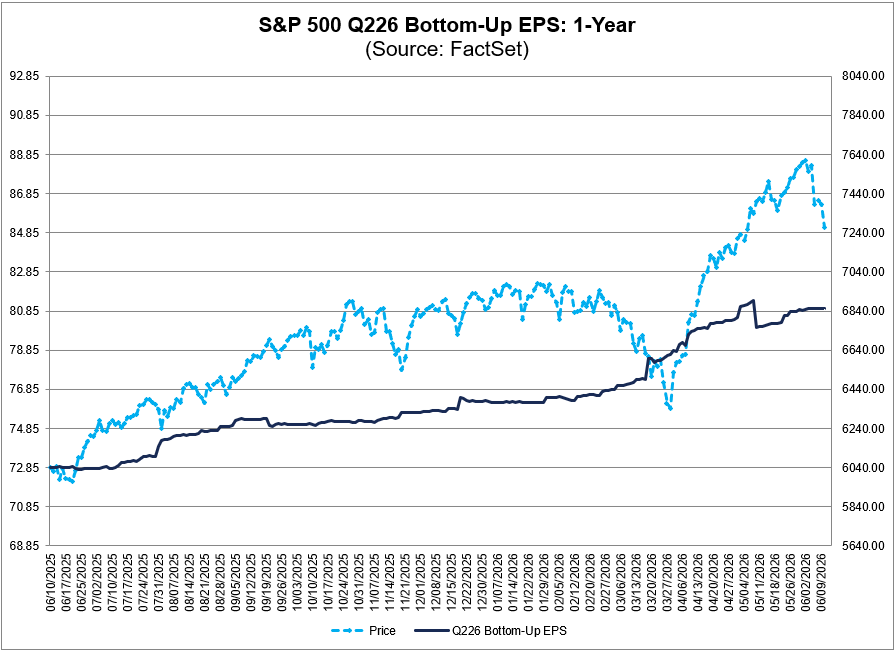

Analysts have increased Q2 EPS estimates for $SPX companies by 2.7% since March 31. #earnings, #earningsinsight, bit.ly/4w62Civ

1

6

22

3,492

O los beneficios son más resistentes de lo que el consenso temía, o el ajuste está pendiente.

Fuente: Goldman Sachs Global Investment Research / FactSet

📩 ¿Inviertes en fondos pero no entiendes del todo lo que tienes?

1

8

I couldn’t agree more with @satyanadella here. This exactly echoes the argument I’ve been making to my hedge fund consulting clients recently.

The architecture I’ve come up with, which is a universal agent-intuitive CLI tool interwoven with a base skill library, combined with a custom skill layer that references the base skills, accomplishes all of these goals very nicely.

The base skill library forms a system: modular, composable skills that have a hierarchy of abstractions. Over time, I expand and refine these skills and push out updates.

The custom skill layer tailors the skills to the specific firm’s particular workflows and knowledge base and represents their wholly owned IP.

The CLI tool is referenced throughout the skill library to give the agent concrete “how-to” knowledge in addition to abstract understanding of workflows.

But because it’s built on top of the base skill library, they’re able to amortize this base R&D across my clients to get something a lot more powerful and expansive than they’d get otherwise.

The client is able to add, expand, and revise their custom skill layer and iterate based on their actual experience and feedback using the system.

And they can do this iteration themselves without needing to ask me or even divulge certain aspects of their approach, methodology, data, etc.

The CLI tool also runs on the client’s machine along with the agent, whether Claude Desktop or the Codex GUI app, and connects directly to data sources like EDGAR, Capital IQ, FactSet, Google Trends, etc., so the client doesn’t need to leak alpha indirectly.

As I add new features, functionality, and data sources to the CLI tool, the clients get those in real-time (if they want), and the skills are updated to reflect the new CLI features.

If I raised VC funding for this business, I’m sure investors would insist that everything run on my servers, that the clients never see the actual base skill library, that the CLI tool just be a dumb client that routes requests to our servers, etc.

That is, all things that lead to vendor lock-in and dependency, but which are clearly NOT in the best interests of the client and the preservation of their IP and alpha.

Ultimately, I believe the client-centric approach will win out. And I can already see how much the messaging resonates with prospective clients.

You can get the benefits of AI agents without giving away the farm (your proprietary IP, workflows, and alpha) to the frontier labs or VC backed startups that will ultimately seek to productize this IP or compete directly with you in the future.

12

9

140

7,765

Laurent BODIN 🇺🇦💛💙🐦🚀 retweeted

Jun 13

🇺🇸📊 According to Factset, nearly two-thirds of the S&P 500 now talks about AI when discussing results, and to me, this is where things get interesting.

➡️ So far, the market has mostly rewarded the first wave of AI and that made sense because this is where the numbers were the most visible with massive CAPEX from hyperscalers, full order books, strong revenue growth and high visibility. However, AI is now moving beyond this first circle and is becoming a transversal framework for the entire equity market. Every company now wants to explain how AI can improve productivity, reduce costs, strengthen its offering or support margins.

⚠️ Still, we should be careful as part of the discourse is clearly corporate narrative. Executives know investors want to hear about an AI strategy, so they talk about it. We have already seen this with cloud, blockchain and even ESG. When a theme becomes dominant, everyone wants to show they are on the train.

📈 In my view, the market is going to become much more selective because when the theme was still young, simply being exposed to AI was sometimes enough to be rewarded, but the more mainstream the topic becomes, the higher expectations get. The higher expectations get, the more companies will need to show concrete evidence.

AI is not a passing trend limited to a handful of technology stocks but we are entering a more demanding phase. Companies will need to show where value is actually being created.

*Link: insight.factset.com/highest-…

3

13

30

6,287

$SPX is expected to report Y/Y earnings growth of 21.9% for Q2 2026, which is above the estimate of 18.7% on March 31. #earnings, #earningsinsight, bit.ly/4w62Civ

1

10

18

3,224

#InteligenciaArtificial | 📊 Codex se conecta directamente a Snowflake, Figma, Salesforce y FactSet 🔌

La nueva actualización introduce seis plugins especializados para analistas, creativos, ventas, diseñadores y banqueros. Sin necesidad de escribir una sola línea de código, Codex puede extraer datos, automatizar reportes y coordinar tareas conectando de manera nativa un total de 62 aplicaciones corporativas.

Revisa la lista completa de las 110 habilidades que incluye esta actualización aquí. 👇🏻

occidente.co/secciones/tecno…

87

Factset finds that "S&P 500 companies that have cited 'AI' on Q1 earnings calls have seen a higher average price increase compared to companies that have not cited 'AI' on Q1 earnings calls since March 31, 2026 (12.7% vs. 2.6%) and since December 31, 2025 (13.1% vs. 7.7%)."

That is also true at the median since March 31st but interestingly is not true for the median company since the start of the year (5.5% vs. 6.2%)."

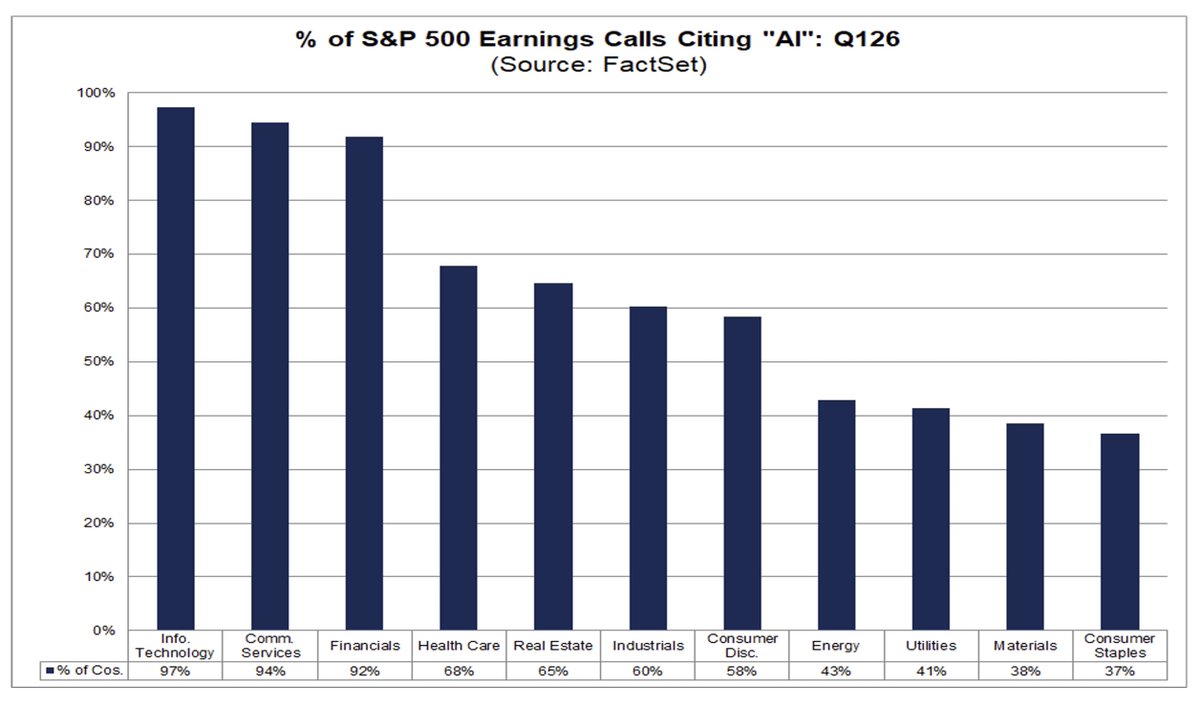

FWIW, 97% of companies in the SPX tech sector, 94% of Comm Services, and 92% of Financials mentioned AI. In contrast less than half of companies in the Energy, Utilities, Materials, and Staples sectors mentioned AI on their earnings calls (a little surprised by that).

Jun 13

🇺🇸📊 According to Factset, nearly two-thirds of the S&P 500 now talks about AI when discussing results, and to me, this is where things get interesting.

➡️ So far, the market has mostly rewarded the first wave of AI and that made sense because this is where the numbers were the most visible with massive CAPEX from hyperscalers, full order books, strong revenue growth and high visibility. However, AI is now moving beyond this first circle and is becoming a transversal framework for the entire equity market. Every company now wants to explain how AI can improve productivity, reduce costs, strengthen its offering or support margins.

⚠️ Still, we should be careful as part of the discourse is clearly corporate narrative. Executives know investors want to hear about an AI strategy, so they talk about it. We have already seen this with cloud, blockchain and even ESG. When a theme becomes dominant, everyone wants to show they are on the train.

📈 In my view, the market is going to become much more selective because when the theme was still young, simply being exposed to AI was sometimes enough to be rewarded, but the more mainstream the topic becomes, the higher expectations get. The higher expectations get, the more companies will need to show concrete evidence.

AI is not a passing trend limited to a handful of technology stocks but we are entering a more demanding phase. Companies will need to show where value is actually being created.

*Link: insight.factset.com/highest-…

3

914

From today will do a 100 days challenge of my day trading learning journal:

Here’s an easy English translation of your daily investment schedule:

7:30 AM

Open TradingView and check my custom news feed: macroeconomic data updates, Federal Reserve official speeches, major tech company news, AI spending trends, supply chain reports, chip spot prices.

8:30 AM

Data maintenance: update NAV (net asset value), review position exposure, adjust portfolio beta. Use FactSet and Bloomberg to track Nasdaq futures, semiconductor index, and US Treasury yield curve. Quickly review major holdings for catalysts and valuation changes.

9:30 AM

Try to learn: “The world is messy.”

12:00 PM

Review morning market performance. Look at sector heatmap and ETF flows to understand where money is going and risk appetite. Even though my portfolio focuses on fundamentals, I do a technical review every day. My team makes independent trading decisions—we handle everything from position adjustments to placing orders ourselves.

1:00 PM

Read research reports: focus on vertical SaaS pricing power, AI spending cycles, HBM (memory chip) adoption rates, liquid cooling equipment orders. Also study chip manufacturing daily—photolithography, etching, deposition, and EDA software.

3:00 PM

Start preparing monthly stock pitches. Primary research takes most effort. I talk with management teams, distributors, equipment makers, customers, and former employees. Often one off-the-record comment changes everything. Since we cover multiple sectors, I also peer-review other teams’ work and track their markets.

5:00 PM

Evening review: portfolio gained today. Performance shows positive stock selection, negative allocation, beta slightly above benchmark. EDA license renewals accelerating; TSMC hiring shows production line expansion; NVIDIA Blackwell shipments may delay (short-term disruption, long-term thesis unchanged).

8:00 PM

Compare ASML and LRCX gross margin analysis, update valuation models, run sensitivity analysis with AlphaSense, regularly check if my investment thesis still holds, eliminate disproven assumptions.

99