Jun 4

📍เมื่อตัวเลขหนี้ บัญชี BNPL เริ่มขยายวงกว้างมากขึ้น กลุ่มคนเริ่มทำงาน ช่วงอายุ 20-35 ปี ก่อหนี้ประเภทนี้มากที่สุด และในกลุ่มนี้มีหนี้เสียสูงที่สุดด้วย ถึงเวลาต้องมีมาตรการกำกับดูแลที่เข้มงวดมากขึ้น โดยธนาคารแห่งประเทศไทย กำลังเดินหน้าให้เห็นผลภายในปีนี้

.

🔥รู้จัก บัญชี BNPL ที่เล่นกับความอยากได้ก่อน เรื่องจ่ายเงินค่อยว่ากัน

ชื่อเต็มๆ คือ Buy Now Pay Later (BNPL) เป็นบริการสินเชื่อระยะสั้นรูปแบบหนึ่ง ที่อนุญาตให้ผู้บริโภคซื้อสินค้าหรือบริการไปก่อน แล้วค่อยแบ่งชำระเงินคืนเป็นงวดๆ ในภายหลังหรือที่รู้จักกันว่า “ซื้อก่อน จ่ายทีหลัง” ซึ่งโดยส่วนใหญ่มักจะเป็นการผ่อนชำระแบบไม่มีดอกเบี้ย หากชำระคืนครบถ้วนตามเวลาที่กำหนด ทำให้สะดวกสำหรับคนที่ต้องการซื้อสินค้าแต่ยังไม่อยากจ่ายเงินก้อนในครั้งเดียว

.

🔥โดนใจคนรุ่นใหม่ อยากได้ต้องได้ ไม่งั้นตกเทรนด์

และวันนี้คนที่ติดกับดัก บัญชี BNPL คือ กลุ่มคนรุ่นใหม่ ช่วงอายุ 20-35 ปี หรือกลุ่มคนรุ่นใหม่ เจน Z และ ปลายๆ เจน Y และมีหนี้เสียจาก บัญชี BNPL สูงที่สุดถึง 27% จากการเติบโตของบัญชี BNPL ที่เติบโตเฉลี่ยสูงถึง 99.9% ต่อปี ขณะที่สินเชื่อ BNPL ขยายตัว 38% ต่อปี หรือประมาณ 18,000 ล้านบาท

เพราะ BNPL กำลังเปลี่ยนพฤติกรรมการใช้เงิน จาก "เก็บเงินก่อนซื้อ" กลายเป็น "ซื้อก่อน ค่อยจ่าย" ซึ่งคำนี้ ใช้ได้แม้แต่กับ ของกิน ราคาหลักสิบ หลักร้อยบาท เช่น ชานมไข่มุก ข้าวมันไก่ โดยข้อมูลเปิดเผยโดย นายวิทัย รัตนากร ผู้ว่าการธนาคารแห่งประเทศไทย (ธปท.)

.

🔥ได้ง่าย ได้เร็ว มีเงินก้อนเสริ์ฟถึงมือ ผ่านแอปฯ ขายสินค้า

ข้อมูลจาก fintips by ttb มองว่า จุดเริ่มต้นมาจากความสะดวกสบายในการสมัครที่รวดเร็วกว่าบัตรเครดิต มีโปรโมชันผ่อน 0% ระยะเวลาผ่อนชำระจะอยู่ที่ 2- 5 เดือน ที่ดึงดูดใจ และความสามารถในการช่วยบริหารสภาพคล่องทางการเงิน ทำให้สามารถซื้อสินค้าชิ้นใหญ่ได้โดยไม่กระทบเงินสดในมือ ยิ่งทำให้ยังเข้าถึงกลุ่มคนรุ่นใหม่และผู้ที่ไม่มีบัตรเครดิตได้ง่ายกว่าอีกด้วย

แต่ความง่าย ความสะดวก อาจแลกมากับ “การสะสมหนี้” หากผู้ใช้ไม่มีวินัยทางการเงินมากพอ จากหนี้หลักสิบบาทอาจสะสมกลายเป็นดินพอกหางหมู

.

🔥 ซื้อ 1 ชิ้น ต่อ 1 สัญญา จนกลายเป็นราชาเงินผ่อน

คนส่วนใหญ่ไม่ได้มี BNPL แค่รายการเดียว เพราะส่วนใหญ่หนี้ประเภทนี้เกิดขึ้นในแอปฯ ขายสินค้า กดซื้อสินค้า 1 ประเภท ก็ทำสัญญาการซื้อ 1 สัญญา เช่น

- โทรศัพท์ 1 สัญญา

- รองเท้า 1 สัญญา

- เสื้อผ้า 2 สัญญา

- อาหารเดลิเวอรี 1 สัญญา

สุดท้ายกลายเป็นหนี้รายเดือนสูงกว่าที่คิด

ซึ่ง ความง่ายในการใช้ BNPL อาจทำให้เราเพลิดเพลินกับการซื้อของหลายชิ้นจากหลายผู้ให้บริการในเวลาเดียวกัน การมียอดผ่อนชำระเล็กๆ น้อยๆ หลายรายการอาจดูเหมือนไม่เป็นไร แต่เมื่อรวมกันแล้วอาจกลายเป็นภาระหนี้สินก้อนใหญ่ที่จัดการได้ยากและส่งผลกระทบต่อสถานะทางการเงินโดยรวมได้

.

🔥 “จ่ายช้า ผิดนัด” เจอค่าปรับ ดอกเบี้ยบวม

หากชำระล่าช้าหรือผิดนัด ผู้ใช้ BNPL อาจถูกเรียกเก็บค่าปรับ ดอกเบี้ยเพิ่มเติมตามเงื่อนไขของผู้ให้บริการ ซึ่งโดยทั่วไปอัตราดอกเบี้ยอาจอยู่ที่ประมาณ 15% - 25% ต่อปี

นอกจากนี้ อาจมีค่าใช้จ่ายในการติดตามทวงถามหนี้ 50 บาทต่อรอบบิล และหากค้างชำระเกินกว่าหนึ่งรอบบิล อาจถูกเรียกเก็บ ค่าใช้จ่ายในการติดตามทวงถามหนี้เพิ่มเป็น 100 บาท รวมถึงอาจมีการดำเนินการตามกฎหมาย ส่งผลกระทบต่อประวัติการชำระเงินและความสามารถในการขอสินเชื่อในอนาคต

เพราะ BNPL ทำให้การตัดสินใจซื้อง่ายขึ้นและรวดเร็วขึ้น ซึ่งอาจกระตุ้นให้เกิดการใช้จ่ายแบบหุนหันพลันแล่น หรือซื้อสินค้าที่ไม่จำเป็นเพียงเพราะสามารถจ่ายทีหลังได้ พฤติกรรมเช่นนี้อาจนำไปสู่การสร้างวินัยทางการเงินที่ไม่ดีในระยะยาว

นอกจากนี้ การใช้ BNPL บ่อยครั้งยังทำให้ผู้ใช้เกิดความคุ้นชินกับการบริโภคก่อนจ่ายทีหลัง ซึ่งส่งผลต่อการวางแผนงบประมาณ การออมและการจัดการค่าใช้จ่ายในชีวิตประจำวัน ทำให้ยากต่อการควบคุมการเงินในระยะยาวได้

.

🔥 สัญญาณอันตราย แบงด์ชาติออกกฎหมายควบคุมรวดเดียว 4 ฉบับ

BNPL ทำให้เกิดข้อกังวลด้านวินัยทางการเงินและภาระหนี้ของผู้บริโภคในระยะยาว ในมุมมองของธนาคารแห่งประเทศไทย (ธปท.) และสภาพัฒน์มองว่า แม้ BNPL จะช่วยกระตุ้นการใช้จ่ายและเศรษฐกิจดิจิทัล แต่ก็มาพร้อมกับความกังวลต่อแนวโน้มหนี้ครัวเรือนที่สูงขึ้น โดยเฉพาะในกลุ่มผู้มีรายได้น้อย จึงนำมาสู่การกำกับดูแลที่เข้มข้นขึ้นเพื่อสร้างความรับผิดชอบของผู้ให้บริการและป้องกันปัญหาการก่อหนี้เกินตัวของผู้บริโภค

นายวิทัย รัตนากร ผู้ว่าการธนาคารแห่งประเทศไทย (ธปท.) เตรียมออกมาตรการกำกับดูแล Buy Now Pay Later (BNPL) หรือ ซื้อก่อนจ่ายทีหลัง ผ่านการใช้กฎหมายในกำกับของ ธปท. 4 ฉบับภายในสิ้นปีนี้

โดยจะกำหนดกติกาคุ้มครองผู้ใช้บริการ เช่น กำหนดอายุขั้นต่ำของผู้ใช้บริการ กำหนดประเภทสินค้า มูลค่าสินค้าขั้นต่ำ และกำหนดเพดานดอกเบี้ยสูงสุด เป็นต้น เพื่อควบคุมไม่ให้เกิดการบริโภคที่ฟุ่มเฟือย

สำหรับการกำกับดูแล BNPL ธปท. จะเข้าไปควบคุม ทั้งวงเงินที่ปล่อยให้ผู้ใช้บริการและอัตราดอกเบี้ย จากที่ก่อนหน้านี้ ธปท. ไม่เคยเข้าไปกำกับดูแลเลย อย่างไรก็ตามจะกำกับเฉพาะการให้สินเชื่อผ่านแพลตฟอร์มซื้อขายสินค้าออนไลน์เท่านั้น ไม่รวมถึงการผ่อนชำระกับบริษัทผู้ผลิตสินค้าโดยตรง โดยคาดว่าจะเห็นแนวทางที่ชัดเจนภายในเดือนต.ค. - พ.ย. 2569

.

🔥 ถ้าอยากใช้ต้องมีเทคนิค

fintips by ttb แนะเทคนิคว่า ถ้าอยากใช้ประโยชน์จาก BNPL ให้เต็มที่โดยไม่ต้องเจอปัญหาหนี้สะสม ต้องทำสิ่งนี้

- วางแผนงบประมาณชัดเจน กำหนดงบชอปปิ้งในแต่ละเดือนอย่างชัดเจน เช่น ไม่เกิน 20 – 30% ของรายได้ต่อเดือน เพื่อให้การผ่อนชำระไม่กระทบค่าใช้จ่ายจำเป็นและกระแสเงินสดในอนาคต

- ประเมินความจำเป็นของสินค้าและกำลังซื้อ ใช้ BNPL เฉพาะสินค้าที่จำเป็นจริง ๆ และมั่นใจว่าสามารถผ่อนชำระได้ครบทุกงวดโดยไม่สร้างภาระ

- ติดตามรอบบิลและตั้งแจ้งเตือน จดบันทึกวันครบกำหนดชำระและตั้งระบบแจ้งเตือนล่วงหน้า เพื่อลดความเสี่ยงการลืมชำระและค่าปรับที่ไม่จำเป็น

- อ่านเงื่อนไขและข้อตกลงอย่างละเอียด ทำความเข้าใจเรื่องดอกเบี้ย ค่าปรับกรณีชำระล่าช้า และข้อจำกัดของแต่ละแพลตฟอร์มก่อนกดใช้บริการ

- อย่าใช้หลายเจ้าเกินไป การใช้บริการ BNPL จากหลายแพลตฟอร์มพร้อมกันอาจทำให้คุณเสียการควบคุมและเสี่ยงต่อหนี้สะสมได้

.

📍หากมองในมุมบวก BNPL ไม่ใช่ตัวร้ายเสมอไป เพราะด้านหนึ่งก็ช่วยให้เข้าถึงการบริโภคและสภาพคล่องแต่หากขาดการกำกับดูแล "หนี้ก้อนเล็กจำนวนมาก" อาจกลายเป็น "หนี้ครัวเรือนก้อนใหญ่ในอนาคต" เช่นเดียวกับที่บัตรเครดิตและสินเชื่อส่วนบุคคล ที่ตอนนี้ก็ยังเป็นก้อนหนี้มหาศาลกดทับกำลังซื้อและเศรษฐกิจไทยอยู่เช่นกัน

อ่านข่าว : pptv36.news/1WId

#บัญชีBNPL #BNPL #ซื้อก่อนจ่ายทีหลัง #หนี้ #ผ่อนสินค้า #ดอกเบี้ย #เงินกู้ #Wealth #PPTVWealth

1

5

1,780

May 31

Most people use debit cards for:

❌ ATM withdrawals

❌ Cash deposits

❌ Occasional payments

But for the next few weeks, SBI Debit Cards can be surprisingly rewarding.

Do you have an SBI Debit Card?

Reply with your card variant below 👇

And repost this so other SBI users don’t miss out.

#SBI #DebitCard #Banking #MoneyTwitter #FinTips

2

2

948

May 30

📷 ท่ามกลางค่าครองชีพที่ยังไต่ระดับขึ้นต่อเนื่อง ขณะที่รายได้ของมนุษย์เงินเดือนแทบไม่ขยับ “ความอยู่รอดทางการเงิน” จึงไม่ใช่แค่เรื่องการหาเงินเพิ่ม แต่คือการบริหารเงินที่มีอยู่ให้มีประสิทธิภาพที่สุด เพื่อให้ทุกบาทที่หามา “อยู่ได้นานกว่าเดิม”

.

📷 fintips by ttb ชวนปรับมุมมองใหม่ ผ่าน 3 หลักคิดสำคัญ “อยู่ให้เป็น – เย็นให้พอ – รอให้ได้” ซึ่งไม่ใช่สูตรซับซ้อน แต่เป็นวินัยทางการเงินพื้นฐานที่ช่วยเปลี่ยนพฤติกรรมการใช้เงินให้มั่นคงขึ้นในระยะยาว และลดความเสี่ยงเงินชนเดือนแบบไม่รู้ตัว

.

📷 “อยู่ให้เป็น” คือการจัดลำดับเงินอย่างมีระบบ เริ่มจากกันเงินออมก่อนใช้ ไม่ใช่เหลือแล้วค่อยเก็บ แนวคิด 50-30-20 จึงเป็นโครงสร้างง่าย ๆ ที่ช่วยให้เห็นภาพชัดขึ้น ว่าเงินควรไปที่ไหน และอะไรคือ “รายจ่ายที่จำเป็นจริง” ในชีวิตประจำวัน

.

อ่านต่อ : pptv36.news/1WoV

.

#วางแผนการเงิน #มนุษย์เงินเดือน #การเงินส่วนบุคคล #เงินออม #ค่าครองชีพสูง #Wealth #PPTVWealth

1

11

14

1,013

May 1

ในยุคที่ความไม่แน่นอนเกิดขึ้นได้ตลอดเวลา ไม่ว่าจะเป็นเศรษฐกิจผันผวน การมีเงินสำรองไว้ใช้จ่าย ในเหตุการณ์ไม่คาดฝันที่อาจเกิดขึ้นในชีวิตประจำวัน หรือ “เงินสำรองฉุกเฉิน” จึงกลายเป็นพื้นฐานสำคัญที่จะช่วยสร้างความมั่นใจและลดแรงกระแทกเมื่อชีวิตสะดุด

.

PPTV Wealth จึงนำเคล็ดลับจาก fintips by ttb มาชวนทุกคนทำความเข้าใจว่า เงินสำรองฉุกเฉินไม่ใช่แค่เงินออมทั่วไป แต่คือ “เครื่องมือบริหารความเสี่ยง” ที่ช่วยให้ยังใช้ชีวิตต่อได้ แม้ในวันที่รายได้ไม่เป็นไปตามแผน

.

แล้วคำถามคือจะเริ่มสร้างเงินสำรองฉุกเฉินอย่างไร ให้ทำได้จริงและไม่กระทบค่าใช้จ่ายปัจจุบัน โดยเริ่มจาก 4 เคล็ดลับง่าย ๆ ดังนี้

.

1.ตั้งเป้าหมายให้ชัด กำหนดบทบาทของเงินฉุกเฉินโดยเงินสำรองฉุกเฉินควรถูกออกแบบมาเพื่อช่วยให้ชีวิตเดินหน้าต่อได้อย่างน้อย 3-6 เดือน

.

2.เก็บก่อนใช้ เมื่อเงินเดือนเข้า ควรเก็บเงินสำรองฉุกเฉินก่อนเสมอ อย่ารอให้เหลือแล้วค่อยเก็บ พร้อมวางแผนรายจ่ายให้เหมาะกับตัวเอง หรือใช้สูตรแบ่งเงินแบบง่ายๆ อย่างสูตร 50-30–20 หรือ 50% ค่าใช้จ่ายจำเป็น / 30% ไลฟ์สไตล์ / 20% ออมและลงทุน

.

3.แยกบัญชีให้ชัดเจน ซึ่งการแยกบัญชีตามเป้าหมาย จะช่วยลดโอกาสเผลอนำเงินไปใช้ผิดวัตถุประสงค์ เมื่อแต่ละบัญชีมีบทบาทที่ชัดเจน ก็จะช่วยสร้างวินัยทางการเงินได้ง่ายขึ้น โดยเงินสำรองฉุกเฉินควรอยู่ในบัญชีที่สามารถถอนใช้ได้ทันทีเมื่อจำเป็น

.

4.ลดรายจ่ายที่ไม่จำเป็น เปลี่ยนเป็นเงินเก็บสำรองเพราะเมื่อจดรายรับ–รายจ่ายอย่างสม่ำเสมอ จะเริ่มเห็นชัดว่าอะไร “จำเป็น” และอะไร “ตัดได้”

.

อ่านต่อ : pptv36.news/1U0K?FPL

#เงินสำรองฉุกเฉิน #เงินเก็บ #ออมเงิน #fintips by ttb #ttb #เคล็ดลับออมเงิน #Wealth #PPTVWealth

2

4

447

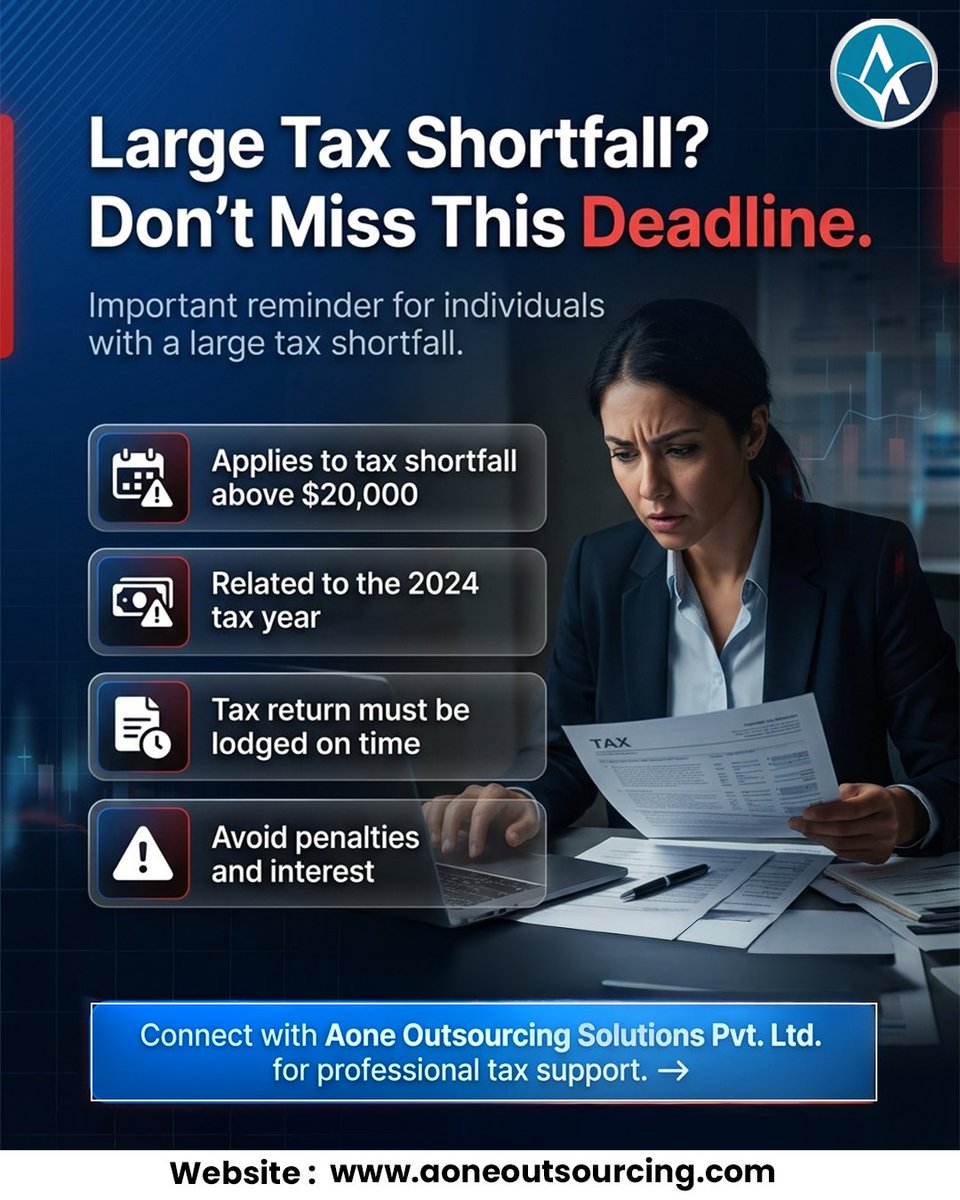

A small tax oversight today can turn into a $20K problem tomorrow.

Stay compliant. Stay ahead. 📊

#TaxTips #BusinessOwners #StartupTips #Finance #Accounting #Entrepreneurs #MoneyMatters #TaxSeason #SmallBusiness #CFO #FinTips

2

11

Mar 17

Which financial goal is YOUR top priority for the next 6 months?

#poll #FinTips #IndiaFinance #MoneyTipsIndia #InvestSmart #SavingsGoals

0%

Build emergency fund

0%

Clear high-interest debt

67%

Save for car/home

33%

Invest for long term 🚀

3 votes • Final results

1

179

Mar 10

💳 SBI PhonePe Black Select Credit Card – My Honest Experience !!!

I’ve been using the SBI PhonePe Black Select Credit Card for my regular spends, and honestly, it has turned out to be one of the best cards in my wallet based on real usage 🔥

With many recent devaluations in other credit cards, a lot of users are now exploring better alternatives — and this card is definitely worth checking out.

✨ Why I Like This Card:

• Strong reward points on everyday spends

• Great value when used through the PhonePe ecosystem

• Simple redemption (1 Reward Point = ₹1 value)

• Works well for vouchers, food orders, and daily spending

If you're planning to move from other cards and explore better rewards, take a look at the detailed post about the SBI PhonePe Black Select Credit Card 💳 😀👇🏼

👉 Interested in applying?

You can also use my referral link to apply and get started.

#CreditCards #SBICard #PhonePe #Cashback #RewardPoints #PersonalFinance #CreditCardIndia #FinTips #ccgeeks #ccgeek

Feb 26

💳 SBI PhonePe Black Select Credit Card – My Honest Experience !!!

I’m using the SBI Card PhonePe Black Select Credit Card and honestly, it’s one of the best cards I hold based on real usage 🔥

Here’s why 👇

✨ Top Benefits I’m Enjoying:

🔟 10% return on Insurance, Bill Payments & Recharges via PhonePe App

🛍️ 5% return on Gift Vouchers via Amazon

🛒 5% return on online spends – Amazon, Swiggy, Myntra, Uber, Zomato & more*

📲 1% return on UPI spends

✈️ 4 Domestic Lounge Access

🌍 Free Priority Pass Membership*

⛽ 1% Fuel Surcharge Waiver

💸 ₹3L annual spend → Fee Waiver

🎁 ₹5L annual spend → ₹5,000 Travel Voucher

📊 Real Example from My Usage:

I pay ₹2,500/month insurance → ₹30,000/year

With 10% return, I get ₹3,000 back annually 💰

👉 That’s 1 month insurance FREE

👉 Plus extra ₹500 benefit effectively

👉 And best part: 1 Reward Point = ₹1 😍

If you’re already paying insurance, bills & doing online shopping regularly, this card literally converts expenses into rewards.

If you’d like to apply for the PhonePe SBI Black Select Credit Card, feel free to use my referral link below 👇

#CreditCards #SBICard #PhonePe #Cashback #PersonalFinance #Rewards #IndiaFintech #ccgeeks #ccgeek

1

2

789

Jan 25

ทุกวันนี้การช้อปปิ้งออนไลน์กลายเป็นส่วนหนึ่งของไลฟ์สไตล์ประจำวันไปโดยไม่รู้ตัว ไม่ว่าจะเลือกซื้อของใช้จำเป็นในบ้าน ไอเทมแฟชัน หรือเครื่องสำอาง ก็สามารถสั่งซื้อได้อย่างสะดวกรวดเร็วผ่านสมาร์ทโฟน และที่สำคัญยังมีโปรโมชันสุดคุ้มมากมายให้เลือกใช้ แต่หลายคนอาจคุ้นเคยกับการเปรียบเทียบราคาหรือการเลือกชมสินค้าจริงก่อนกลับมาสั่งซื้อผ่านช่องทางออนไลน์เพื่อให้ได้ราคาที่ถูกกว่าเดิม

.

แต่เทคนิคการซื้อของออนไลน์ที่นักชอปทั้งหลายใช้ในปัจจุบันก้าวข้ามไปไกลกว่าแค่การมองหา “ของถูก” แต่ยังมองหาความคุ้มค่าด้านอื่น ๆ ผ่านตัวช่วยสำคัญที่หลายคนอาจมองข้ามอย่างบัตรเดบิต วันนี้ fintips by ttb #เรื่องเงินที่รู้จริงแบบเพื่อนที่รู้ใจ ชวนพบกับ 5 เทคนิค ช่วยเปลี่ยนการช้อปปิ้งออนไลน์ให้คุ้มค่ามากกว่าเดิม เปลี่ยนทุกยอดการใช้จ่ายให้กลายเป็นเงินคืนเข้ากระเป๋าได้ง่าย ๆ ดังนี้

.

1. รู้จักเลือกใช้บัตรเดบิตที่มี Cashback หรือโปรโมชัน

ปัจจุบันบัตรเดบิตไม่ได้มีไว้แค่ถอนเงินเท่านั้น แต่ยังมาพร้อมสิทธิพิเศษสำหรับการช้อปออนไลน์มากขึ้น เช่น โปรแกรมได้เงินคืน (Cashback) หรือส่วนลดจากร้านค้าที่ร่วมรายการ ซึ่งข้อดีของการใช้บัตรเดบิตคือ ระบบจะตัดเงินจากบัญชีเงินฝากทันที ช่วยให้ผู้ใช้สามารถควบคุมงบประมาณได้ง่าย ไม่ใช้จ่ายเกินตัว และยังได้รับสิทธิประโยชน์เพิ่มเติมจากการใช้จ่ายอย่างมีวินัย เช่น ได้รับเงินคืน 1-2% จากยอดซื้อ ถึงแม้จะดูเป็นจำนวนไม่มาก แต่หากใช้ต่อเนื่องก็สามารถสะสมไปเรื่อย ๆ ซึ่งได้ประโยชน์ในระยะยาว

.

อ่านต่อ : pptv36.news/1LU5

.

#fintipsbyttb #เงิน #ช้อปออนไลน์ #เทคนิคช้อปคุ้ม #บัตรเดบิต #Cashback #Wealth #PPTVWealth

1

373

29 Dec 2025

Get 5% cashback when you buy an Amazon Pay Gift Card 💳✨

Here’s the hack 👇

➡️ Buy the gift card via Tata Neu App

➡️ Pay using Kotak 811 Super Card

➡️ Earn instant rewards extra NeuCoins 🚀

Perfect for shopping, bill payments & subscriptions on Amazon 🛒⚡

Why pay full price when you can save every time?

@CardNiti @credofly

#CashbackHack #AmazonPay #TataNeu #Kotak811 #SmartSpending #OnlineShopping #FinTips #ccgeek #ccgeeks

4

2

2

1,446

23 Sep 2025

เคยหรือไม่? อยาก “ออมเงิน” แต่คิดว่ารายได้น้อยไม่น่าไหว! ซึ่งนั่นเป็นความเชื่อที่ผิด เพราะจริง ๆ แล้ว ไม่ว่าจะมีรายได้มากหรือน้อยก็สามารถออมเงินได้ และยิ่งเริ่มไวยิ่งดี วันนี้ fintips by ttb #เรื่องเงินที่รู้จริงแบบเพื่อนที่รู้ใจ ชวนทุกคนมาเปลี่ยนมุมมองด้วยเทคนิคออมเงินง่าย ๆ และสนุก ไม่ต้องบีบบังคับตัวเองจนไม่มีความสุข โดยเลือกให้เหมาะสมกับไลฟ์สไตล์ของตัวเอง เพื่อช่วยให้ออมเงินได้จริงอย่างยั่งยืน

.

1. เก็บเงินจากแบงก์ที่ชอบ ช่วยสร้างกำลังใจในการออมเงิน

หนึ่งในเคล็ดลับออมเงินฉบับคนเพิ่งเริ่มทำงานที่นำไปใช้ได้จริง ซึ่งวิธีเก็บเงินรายวันแบบนี้เหมาะกับคนยังไม่มีแผนทางการเงินที่ชัดเจน แต่อยากเก็บเงินอย่างมีความสุขและสนุกกับการได้เห็นเงินเก็บเพิ่มขึ้น เช่น ตั้งกฎการออมเงินด้วยการเก็บแบงก์ 50 บาท ได้มาเมื่อไหร่แยกเก็บไว้ รอครบระยะเวลาที่กำหนดได้เห็นเงินเก็บเพิ่มขึ้นแน่นอน

.

2. เก็บเงินตามวันที่ เคล็ดลับการออมเงินดี ๆ สำหรับคนขี้ลืม

เทคนิคเก็บเงินตามวัน เป็นทางเลือกที่เหมาะกับคนขี้ลืม ช่วยบังคับให้เก็บเงินตามเป้าหมายได้ง่าย แค่ดูปฏิทินว่าวันที่เท่าไหร่และเก็บทุกวันให้ได้ตามวันนั้น ๆ เช่น วันที่ 10 เก็บเงิน 10 บาท ส่วนวันที่ 11 ก็เก็บ 11 บาท หากมีรายได้มากขึ้น และคิดว่าจำนวนเงินที่เก็บน้อยไป อาจคูณจำนวนเท่าเข้าไปตามกำลังทรัพย์ของตัวเอง

.

อ่านต่อ : pptv36.news/1BCB

.

#fintipsbyttb #ทีทีบีฟินทิป #12เทคนิค #วิธีออมเงิน #รายได้ #ออมเงิน #ttb #Wealth #PPTVWealth

2

637

1 Sep 2025

🔥FinTips Futebol (Método Anytime & Assistência) 🔥

Foram 1688 apostas realizadas até agora, todas pré-live, com um ROI de 11,5%.

Resultado disso? ✅ 186,70 unidades de lucro 📈💰

💥 E a meta de 200u, que era nosso objetivo, já foi alcançada logo no primeiro dia de setembro!

Agora é seguir trabalhando para fechar o mês ainda mais positivo.

🚀 Os próximos meses prometem ainda mais. Vamos continuar aplicando o método, buscando evolução constante e resultados ainda maiores.

👉 Longo prazo é a chave. Seguimos!! 🦈🦈

1

1

4

100

18 Aug 2025

🧵 Amazon Gift Cards seem simple, but there are 4 types and countless hacks. Most people leave money on the table!

Here’s your ultimate guide — types, pro strategies, the best places to buy (HDFC SmartBuy & ICICI iShop), and key DOs and DON’Ts 👇

#AmazonGiftCards #FinTips

1

5

21

1,835

4 Aug 2025

Before you buy any stock, ask these 3 questions:

Is revenue growing faster than expenses?

Is debt under control (Debt/Equity < 1)?

Is the promoter holding stable or increasing?

If all 3 = ✅, you are likely looking at a fundamentally strong business.

#Investing #StockMarket #FinTips

4

134

29 Jul 2025

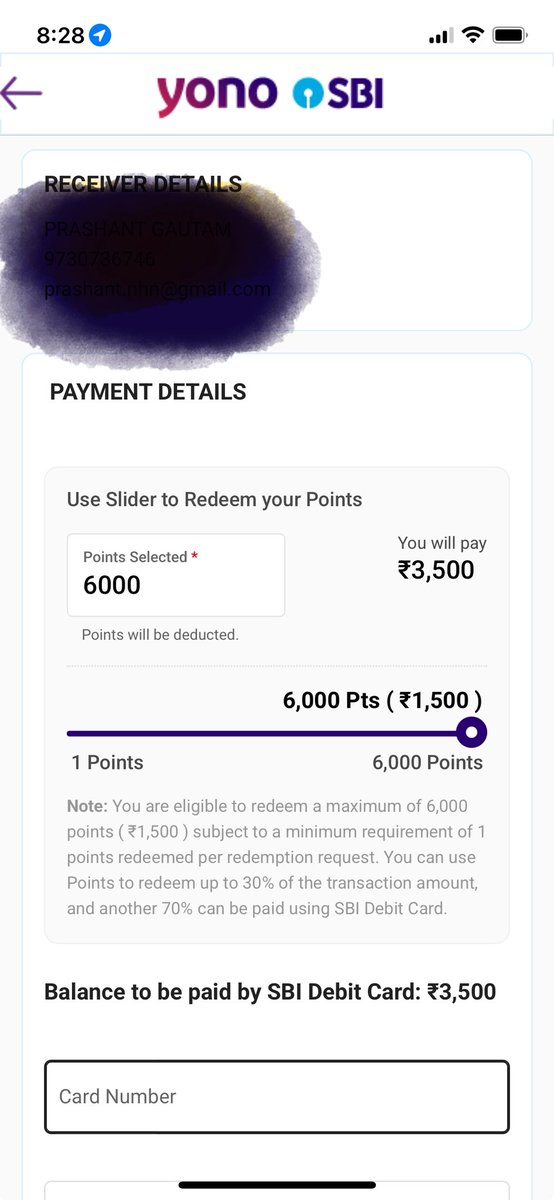

💥 Let me tell you how I Saved ₹4,500 on Amazon Using SBI Virtual Debit Card 💳🛍️

Let me walk you through how a card I’ve been using for months ended up saving me 30% on my Amazon voucher purchase! 👇

For the last 5 months, I’ve been using the SBI Virtual Debit Card (VDC) via the Paytm app to clear my credit card bills.

It’s a RuPay card that works seamlessly on platforms like Paytm, CRED, and Mobikwik.

✨ Bonus? You earn reward points on every transaction! 💰

Earlier, SBI used to offer:

✅ Base rewards (0.25%)

✅ Bonus rewards (another 0.25%)

Which means you could get ~0.50% of the transaction value back just for paying your bills — something you anyway do every month! 😍

I kept using this card diligently — didn’t miss a month. Slowly but steadily, the reward points started adding up in my account.

No extra effort. Just smart use of the SBI VDC on the right platforms at the right time 💡

A few days ago, I thought — “Let me check what I can redeem these points for.”

So I logged into the SBI Rewards portal and went through the redemption catalogue.

And that’s when I stumbled upon this crazy deal 👀👇

🎁 Amazon Pay vouchers : Pay 30% using reward points earned in SBI!

Yup, you heard it right — THIRTY PERCENT! 😳🔥

So here’s what I did:

🛒 Selected a ₹15,000 Amazon Pay voucher

💳 Used my accumulated reward points

💸 Paid just ₹10,500 from my own pocket

📉 Effective saving: ₹4,500

That’s 30% off on real money, not just some coupon cashback! 😎

Most people ignore their debit card reward points, thinking they’re useless or slow.

But with a bit of consistency and the right redemptions, you can unlock serious value 💥

This isn’t a hack. It’s just smart usage. 🔍

💬 Moral of the story?

•Use your SBI VDC (especially for recurring bills)

•Track reward point earnings

•Check the SBI Rewards portal regularly

•Be ready to grab these limited-time deals when they show up

You never know when a ₹4,500 saving is just one click away! 🙌

#SBIRewards #VirtualDebitCard #FinTips #SmartSpends #RewardPoints #AmazonVoucher #PointsGame #TechnoFino #CreditCardIndia #PersonalFinanceIndia #SaveMore #SBIYONO #RupayRewards #DailySavingTips #PassiveIncome #IndiaFinance @ccg33k @AmazingCreditC @milespointspro @SartanparaYash @imYadav31 @greatindianmile

6 Jul 2025

💸 Earn Cashback on Credit Card Payments

Tried 3 options to get cashback or rewards for paying your credit card bills

1) SaveSage Kotak Infinity DC

2) Mobikwik

3) HDFC Platinum DC

Please like and share if you like the content. Kindly add more approaches in the comments.

#ccgeek #PointsPerksPicks

17

4

52

44,358

24 Jul 2025

🟢 Loving the Axis SuperPro RuPay Credit Card — perfect for local QR spends around ₹15K/month!

💸 3% cashback via QR on the SuperMoney app

💳 1% cashback otherwise

⛽ 1% fuel surcharge waiver

✅ Lifetime Free

📥 Cashback credited in the next statement

❌ Cashback capped at ₹500/month

❌ Min ₹100 per txn for cashback

❌ No cashback on utility, rent, wallets

Using it mainly for offline payments & loving the returns so far.

Want to get one? Use this referral to get extra cashback on your first transaction

link.super.money/1ZxyGUg6XUb

#CreditCards #Cashback #FinTips

3

905

15 Jun 2025

Bora com o segundo dia do mundial, vamos com algumas especiais!!

Hoje o mundial promete...

🎯 Apostas - Anytime ou Assistencia

📅 15/06/2025

#SuperBet

🇧🇷 Estevao Goncalves | 1.75u

🇧🇷 ou 🇪🇸 Vitor Roque ou Samu | 1.75u

----------------------------------------

#Betano

🇬🇪 Kvicha Kvaratskhelia | 2.25u

#FinTips

1

4

323

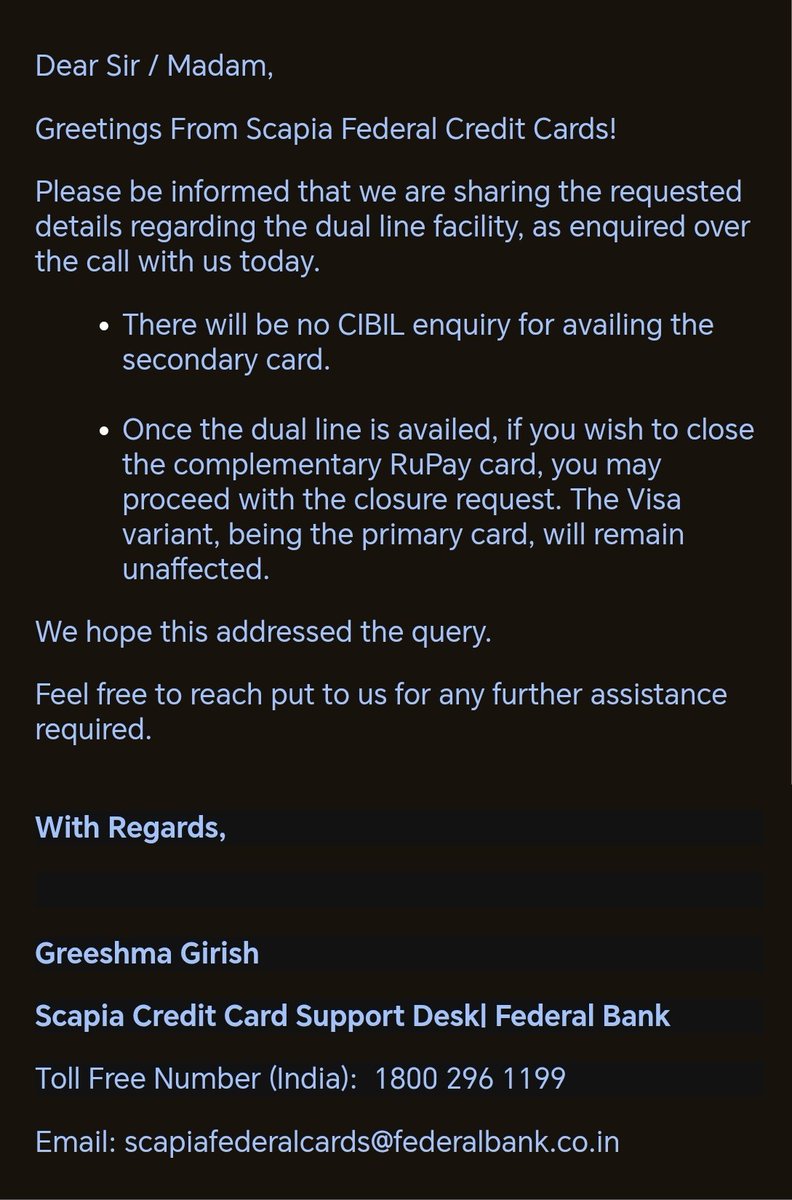

15 Jun 2025

💳 Initially planned to skip the Scapia RuPay variant, but got a confirmation that I can close the RuPay card 🛑 later and still keep the Visa card active 🔥

Plus, just 1 bill & 1 repayment for both cards made the decision easy! ✅

#Scapia

#CreditCard

#Rupay

#FinTips

#ccgeeks

1

2

12

1,640

14 Jun 2025

Bora com duas especiais para esse primeiro dia de Mundial!!

🎯 Apostas - Anytime ou Assistencia

📅 14/06/2025

🇦🇷 Lionel Messi Marcar ou dar Assistencia | 6.75u

(Planilhado 0.70u por conta do limite)

-------------------------------------------------------

🇦🇷 Lionel Messi Marcar | 4.50u

(Planilhado 0.60u por conta do limite)

#Fintips

1

1

4

135

13 Jun 2025

🚨 EVENTO ESPECIAL MUNDIAL DE CLUBES 🚨

Durante o Mundial, vamos mandar apostas exclusivamente aqui no Twitter! 🔥

Serão várias entradas ao longo do evento — Foco total em valor e nada de enrolação.

🔔 Ativa as notificações e acompanha com a gente 🔔

Não vai estar em grupo, mas sera planilhado a parte...

e é só aqui mesmo.

👀 Bora pra cima? #FinTips

6

132

31 May 2025

🚀 The Next Chapter for @defiapp is HUGE! We're not just breaking records in beta ($11B processed, 350K users, 30K DAUs & climbing!), we're building the bridge between traditional finance and DeFi for the next 700 million users. Crypto natives already call Defi App $HOME, and here’s why everyone else will too.

🔥 Recent Milestones Setting the Stage:

The $HOME Token is live, with a massive 45% of supply dedicated to the community! 🤝

By popular demand, Noise.xyz has integrated Defi App.

Our Perps launched just a month ago and have already skyrocketed to ~$2B in processed volume! 🤯

📱 Get Ready: Defi App is Coming to a Play Store Near You!

We're thrilled to announce massive progress on our mobile app – approved for beta launch on the Google Play Store! 🥳 Mobile is set to become a flagship platform, turning Twitter memes and TikTok fintips into seamless onchain buying via Defi App.

Defi App Mobile will offer:

More crypto trading options: The full power of DeFi with a familiar, user-friendly feel like traditional apps.

Enhanced security: True asset ownership for first-time crypto investors.

The simplest path to crypto: Zero KYC friction, no complex wallet management, and goodbye to bridging headaches!

Every chain, every token, every opportunity – in your pocket, one tap away. And that's just the start.

🏡💰 Introducing Home Finance: A World Beyond Trading (Coming Soon!)

You might have seen it perched in our upper navbar

the promise of one-tap yield, zero friction, and real DeFi benefits with clear risk visibility.

ETH holders: Park your ETH in battle-tested protocols with bonus incentives.

Sitting on stables? Put them to work with competitive DeFi yields.

Advanced strategies? Execute them with a single click while you focus.

The vision is simple: The best of DeFi yield, made incredibly easy. No bridging, no endless popups, no headaches.

📈 Why Mobile Home Finance is Our Knockout Combo for Mass Adoption:

With the mobile launch, onchain trading becomes accessible to everyone. But what about those who simply want to earn yield on their savings? This market is MASSIVE.

Home Finance gives them what TradFi often can't:

Higher yields through DeFi's efficiency.

True ownership (your assets, working for YOU).

More flexibility (USDC & ETH strategies first, BTC yield fast-following).

It transforms DeFi yield into a one-tap experience anyone can use, capturing users previously lost to complexity. Mobile first. Home Finance follows fast. That’s when adoption really accelerates.

🌐 Building for Everyone:

@defiapp isn't just for crypto natives. We're for the trader wanting to long SOL with one tap, the professional seeking easy yield, and the newcomer curious about "staking."

With mobile launching, perps live, and Home Finance on the horizon, Defi App is evolving from a cult favorite into crypto’s first true consumer application.

No KYC barriers. No gatekeepers. Just clean, self-custodied access to every token, every trade, and every yield opportunity, across every chain.

This is what crypto’s mass adoption truly looks like. And we’re just getting started.

Get ready to download the app. Get ready for $HOME.

If you’re as excited as we are, share this on X and tag @defiapp !

🔗 Learn more: defi.app

📜 Blog: blog.defi.app

💬 Join the community: discord.gg/defiapp

#DefiApp #HOME #MobileDeFi #DeFiYield #CryptoForAll #MassAdoption #Gasless #SelfCustody #CrossChain #FintechRevolution

7

23

2,075