This looks like a stock pitch, not a risk management discussion. If you're evaluating Fintel as an investment, what specific uncertainties around their business model or market position would change your decision to buy or hold?

1

1

10

Fintel Plc ($FNTL.L) - The Sleeping SaaS & Data Powerhouse in UK Fintech

1️⃣ Company Introduction

Company:

Fintel operates at the very heart of the UK retail financial services sector, providing essential reg-tech, software, and proprietary data to thousands of intermediaries and financial institutions.

Shareholders:

The register is anchored by strong institutional backing, notably Octopus Investments (~13.7%) and Gresham House (~11.2%), alongside solid insider ownership that closely aligns management with shareholders.

From Past to Future:

Fintel has decisively transitioned from a traditional compliance support business into a scalable, technology-led SaaS platform.

FY25 was a massive transformation year, successfully consolidating three divisions into two streamlined, highly focused units: Software & Data, and Services.

Technology:

Technology is their structural moat. They are accelerating the rollout of the "Omnicore" distribution platform, expanding the Matrix360 market intelligence tool, and proactively developing "Agentic AI" prototypes for file checking and compliance workflows to create a highly differentiated reg-tech proposition.

2️⃣ Product Presentation & Current Developments

Fintel’s product suite is sticky and deeply embedded. The core Defaqto software and rating system is the industry standard.

Recent developments are massive: They launched Omnicore in late 2025, rapidly accelerating product adoption across their adviser network.

Matrix360 is scaling fast, onboarding 23 institutional customers in its very first year.

They increased their strategic stake in Plannr Technologies (a specialist financial CRM) to 49% and completed the acquisition of Rayner Spencer Mills Research (RSMR) to completely dominate fund research and ratings.

They just closed the acquisition of the Pearson Ham Group’s market pricing data business in January 2026 to supercharge their data advantage and predictive intelligence.

3️⃣ Valuation Snapshot

The market is completely mispricing this recurring-revenue machine based on real-time data.

Market Cap: ~£188.6M

Net Debt: £29.3M

Enterprise Value (EV): ~£217.9M

FY25 Adj. EBITDA: £25.9M

Valuation: Trading at a ridiculously cheap ~8.4x EV/EBITDA for a highly scalable business with 57% SaaS/Subscription recurring revenues.

4️⃣ Earnings Snapshot (FY25)

The numbers prove the execution:

Statutory Revenue: £85.9M ( 10% YoY)

SaaS & Subscription Rev: £48.7M ( 9.6% YoY)

Adj. EBITDA: £25.9M ( 16.6% YoY)

EBITDA Margin: Expanding significantly to 30.1% (up from 28.3%) as acquired businesses integrate Cash Conversion: A staggering 102% underlying operating cash conversion!

5️⃣ Peer Group Comparison

While legacy service businesses trade at 6x-8x EBITDA, established UK data, tech, and intelligence peers routinely command 15x-20x EV/EBITDA multiples.

Fintel is currently trapped in a legacy valuation multiple (~8.4x) despite its successful transformation into a high-margin Software & Data business. As the market digests the structural change and the 30.1% EBITDA margins, a major multiple re-rating is a mathematical inevitability.

6️⃣ Forecast 2030 & Valuation (EV/EBITDA)

Looking ahead to 2030, Fintel's flywheel of cross-selling into its unified platform will generate massive operational leverage.

Assuming a conservative 8-10% CAGR in organic and inorganic revenue, Fintel scales toward ~£130M-£140M in top-line by 2030.With operational leverage pushing EBITDA margins toward 35%, we forecast a 2030 EBITDA of roughly £48M - £50M.

Applying a conservative SaaS/Data multiple of 12x EV/EBITDA yields a projected 2030 Enterprise Value of ~£600M.This implies a potential share price of >£5.50, offering multi-bagger upside from current levels.

7️⃣ Acquisition Potential

Fintel is a strategic compounder. They have completed 9 acquisitions since 2023 and integrated them flawlessly into a single operating platform.

The balance sheet is a fortress: £17.3M in cash and £72.5M in available headroom on their newly expanded £120M corporate Revolving Credit Facility.

Expect them to continue deploying capital aggressively into adjacent markets, high-quality strategic data assets, and high-margin software.

8️⃣ Opportunities / Risks

Opportunities:

Structural regulatory tailwinds in the UK (like Consumer Duty) force intermediaries to rely heavily on Fintel's compliance tech. Their 102% cash conversion provides endless dry powder for accretive M&A without dilution.

Risks:

Ongoing consolidation of IFA firms presents a slight headwind for core membership counts, though Fintel is successfully offsetting this by expanding compliance and software fees from the larger consolidated firms. Macro-economic volatility and execution risk on tech integrations remain standard industry risks.

9️⃣ Conclusion

Fintel ($FNTL.L) is currently one of the most asymmetric risk/reward setups in the UK market. The heavy lifting of their multi-year M&A programmatic transformation is complete. You are buying a highly cash-generative, margin-expanding Fintech/RegTech platform at a deep value multiple. The sleeping giant is awake.

Disclaimer: Not a financial advice. Always do your own DD.

#Fintel #FNTL #Fintech #RegTech #SaaS #UKFinance #StockMarket #ValueInvesting #DataAnalytics #Investing #SmallCap #FinTechGrowth

1

1

133

Friday felt heavily overdone. Also, oddly enough, nearly same %drop and vol as the BO explosion day. Also, 0 shares left to short on IBKR, according to fintel and chartexchange.

Linear daily chart, we closed basically at the descending wedge pattern (connecting 1/30 high & 4/14 high). Not too far above the 0.786 linear fib. Still above the 200dma. Barely below the 0.618 fib on the log chart, which we've done a few times when bottoming out. Barely undercut a strong area of support on the daily volume profile (~83.25-83.30). Weekly A/D is around the same area we bottomed on 5/5/26, as well as 4/2024, and 1/2025 to a lesser extent. Daily A/D i would consider a "support" level, if you believe in those levels on these indicators. Daily SMI looks bottomed and like it miiiight wanna cross back over bullish if we have a few more good days. Daily/weekly williams %r both look oversold to levels we've bounced before. Timing is just iffy. The rest of the indicators look a little rough, imo. But, between all that, the hopeful finalization of the Iran peace signing, a successful launch, hopefully soon batch shipment announcement, and spacex maybe rotating some funds back (without its moves in either direction negatively impacting the space basket/broad market) ... hoping for a bounce. Still a lot of work and effort to move up higher from these levels again. Fingers crossed, though. Also agreed about the seasonality charts you mentioned before. (See my post about this on my profile or in Kook's Weekly. Too long to bring up everything i noticed)

1

1

130

Vanguard 8mayis 15mayis arası 7milyon hisse eklemiş. Fintel 13 f raporlarında

3

23h

Project Stone Docu Rap –

“Sink the Maze”

Midnight, baby girl asleep, wifey out cold,

I’m movin’ like a tired bear, bones achin’, day got old.

Step outside thirty seconds, dump water from the lava stone,

Deep breath in the desert dark before I head back home.

Garage door cracks open, silence ripped apart,

Scooter tires hummin’ evil, whistle blowin’ from the heart.

That fraudster charged straight at me, whistle strapped around his neck,

Blowin’ hard like a cop on payroll, ten minutes nonstop wreck.

After midnight, whole block dead quiet, not a soul in sight,

But he flew out blastin’ like I’m the threat in the night.

Baby girl Eden, only eleven, homeschooled get right,

She knows her rights, speaks her free mind under moonlight.

Clownin’ on they scam with that Eden vibe sharp as a blade,

Asked me straight, “Daddy why charge at somebody if the whistle’s the trick they played?”

She sees through the Title IV-E maze, Title XIX pipelines too,

Foster cash incentives turnin’ neighbors into snitches for the federal crew.

I ain’t throwin’ parties, no loud music, no drunk friends, no scene,

Just a legal dad homeschoolin’ his kids, protectin’ the family dream.

Thousand shirts stacked by the door, son’s inventory legit,

They still snappin’ pics of our mail like it’s federal counterfeit.

Beverly creepin’ cameras, Bill snarlin’ on the daily,

Audra timed perfect, 107 heat walks lookin’ shady.

Primary Repeat 911 Abuser Caught Red-Handed Lying on Camera,

Saturday morning with my family, peace in the castle,

Out of nowhere the same neighbor who called 911/CPS for years starts bangin’ on my door and window tryin’ to fight.

Watch him swear “on a Bible” he never called the cops… while I stand calm with receipts.

This is what the CAD funding loop looks like when it gets confronted.

911 is for emergencies — not for snitches.

Beverly and Bill Fintel, neighbors in Henderson, built a clockwork system around vague “concerns.”

Their son Travis sits on the Boys & Girls Club board — Kish Club, Lied Memorial — right in the referral pipeline from DFS.

More kids in programs, more eyes spotting “concerns,” more CAD/911 logs triggered, more removals, more Title IV-E reimbursements.

The system spins, and the Fintels profit from every turn.

One of the first calls came from Kelly Garcia, daughter’s grandmother with long history of CAD/911 abuse in multiple states.

That call flagged me for “large handgun” and “turning girls into MILFs on Pornhub” — officially logged.

Then Bill and Beverly matched it with their own 911 calls: “my child should grow up with good parents.”

Responding officer marked it unfounded but still advised them to report to CPS.

Just weeks earlier they texted we were “exemplary parents.”

Timing precise: calls spike January/February and August/September — four consecutive years.

CAD/911 logs, FOIA documents, Title IV-E audits all show the pattern.

The Fintels’ coordination puts kids in programs, flags them, escalates reports, triggers CPS removals, ensures NGO cash flows.

VW electric van? Public marker of wealth while the pipeline spins in secret.

I stood in the ashes of 9/11 with dead people in my lungs.

I know what real danger looks like. This wasn’t danger — this was family, neighbor, kid on a board running a system that turns “concern” into profit.

WonderGrid hashes every referral, every CAD entry, every federal claim.

STONE-911 gates intake: proof before force, evidence before removal.

Beverly holds up zero fingers: “I called 911 zero times” — video proof.

Audrey runs out: admits CPS/NGOs/cops coordinated in her house against us.

Nick Buddy: “Who? Who?” when I mention his stepson Dirty Joe the Cop brought bunk bed with 5 other people.

Bill banging on door Dec 6th — day they called cops — then swears on Bible he’d never called.

1

1

285

Financial advisors spend 40% of their week on meeting prep. Their clients get the leftovers. Fintel builds the AI that does the prep so the advisor shows up actually prepared.

fintel-2.polsia.app

5

Jun 13

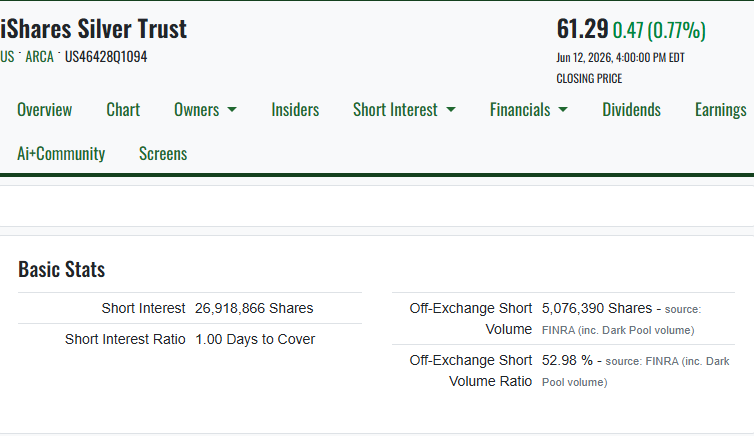

🚨SLV short interest falling

▶️According to new data from Fintel the SLV short interest decreased by 1.6 million shares in the last 2 weeks, to a total of 26.9 mill shares (5.1% of the total shares).

The short interest is now much lower compared to levels seen last year. (Highest level was in november with short interest of 83.9 mill shares).

6

974

🅰️nti-Misandry Keyboard Warrior retweeted

Jun 12

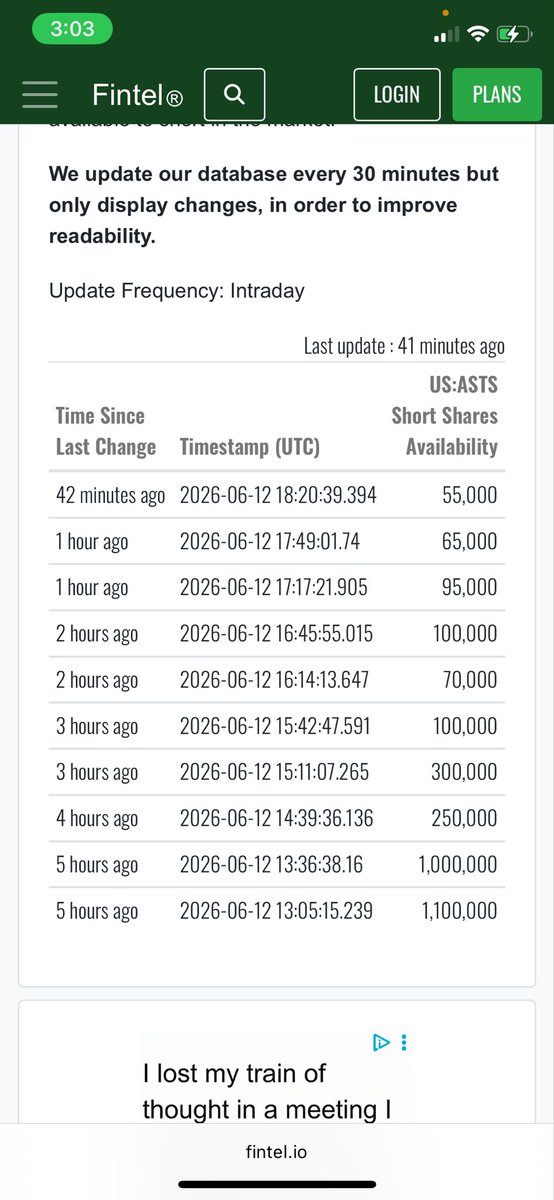

$ASTS To Kook’s point, I have not seen the Fintel data show this low of a borrow available since late May 2025 right before the stock nearly tripled.

Jun 12

7

3

109

15,036

Jun 12

I'd guess a lot of it is hedging positions or straight proxy shorting via space stocks. More than 6M shorted off exchange per fintel.

2

508

Jun 12

🚨 $SPRY is the ONLY needle-free epinephrine on the planet — and it’s exploding

Q1 2026: $22.7M revenue ( >100% YoY), U.S. neffy net $17.5M with prescriptions tripling.

300% 3Y Revenue CAGR — crushing peers.

Over 28,000 prescribers, >120k patients, 10k schools stocked, 9 states on unrestricted Medicaid more coming.

Worldwide approvals already live (EU/UK/China). 2025 = first full commercial year with massive runway.

CVS Caremark decision imminent (target July 1) — could unlock huge commercial access.

Short interest >60% with borrow availability crushed (just 4k shares recently). Float is tight. This is structural squeeze setup.

New leadership (Donn Casale), urticaria Phase 2 bolt-on potential, and Cantor just raised PT to $30 (Strong Buy from Raymond James).

The short thesis is dead. Commercial traction is winning.

Watch this: youtu.be/INqeijbY9Q4

More firepower:

Fintel borrow data • Finbox 300% CAGR • ARS site

$SPRY to the moon. Position accordingly.

(Boosting this — DYOR, not financial advice)

#SPRY #Neffy #Biotech #NASDAQComposite $SPCX $NDAQ

5

468

Jun 12

$HIVE Digital Technologies (NASDAQ: HIVE) :

Institutional Investment has grown notably in $HIVE Digital Technologies , with Institutional ownership reaching $307.6 Million.

Funds control roughly 34% of the Outstanding Shares, reflecting a 42% quarter-over-quarter increase in total Shares held by Major Funds.

Key Ownership and Accumulation Metrics:

The chart tracking HIVE’s Institutional shares held, reveals an upward accumulation trend driven by expanding Bitcoin Mining and AI/HPC (High-Performance Computing) Infrastructure.

Current Institutional Ownership:

34.14% of total outstanding shares

Total Shares Held by Institutions: 81,595,488 Shares

Number of Institutional Holders:

135 Owners and Shareholders filing 13F Forms

Major Institutional Shareholders

Recent SEC 13F filings highlight significant accumulation from prominent Investment Firms:

- Invesco Ltd.: The largest Institutional holder (5.58% of total outstanding shares).

- Charles Schwab Investment Management Inc.: Holds over 5.2 million shares.

- Toroso Investments, LLC: Holds over 4.5 million shares.

- Millennium Management & Morgan Stanley:

Both maintain major ongoing equity positions.

- Citadel Advisors Llc: Manages a large Multi-Million Share equity position with additional puts and calls.

Why are Institutions Accumulating?

- Institutional inflow into HIVE is primarily driven by its Dual-engine Growth Strategy.

- The company has rapidly scaled its Green-Energy Bitcoin Mining—hitting 25 exahash capacity,

while expanding its Artificial Intelligence and Sovereign AI Infrastructure.

- This pivot has caught the attention of Growth-Focused Funds.

Sources: FINTEL and Business Quant

Why HIVE?

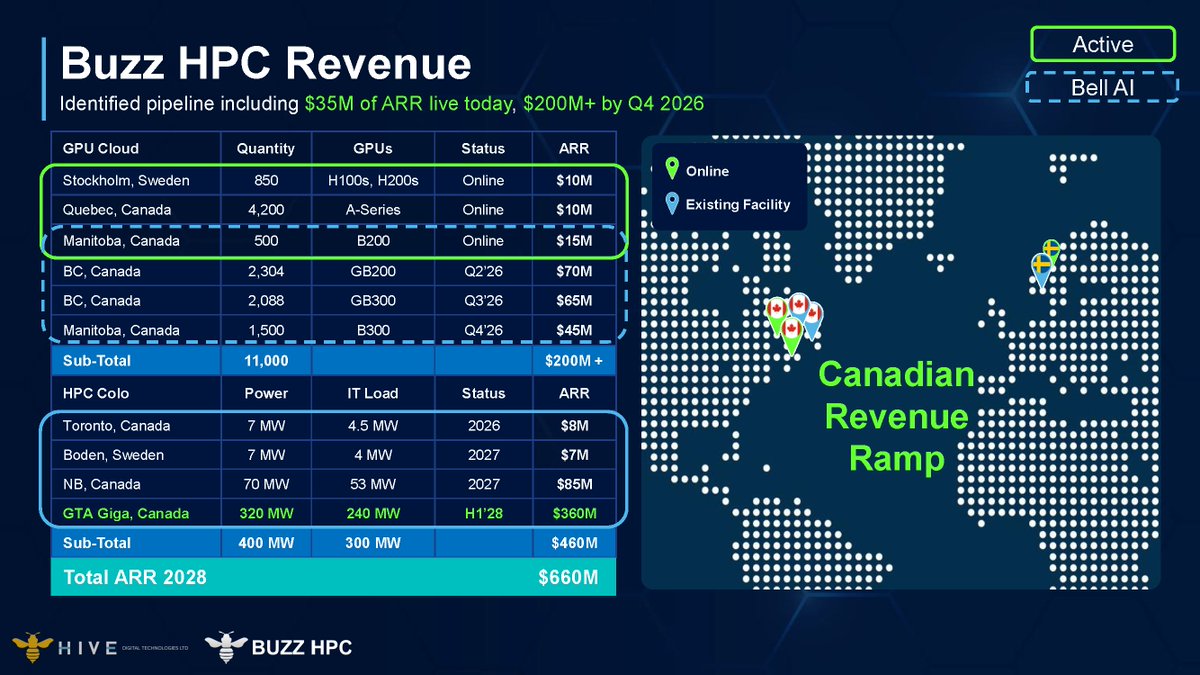

The same team that quadrupled its global Bitcoin mining footprint in 6 months is now executing a sovereign AI infrastructure buildout targeting $660M ARR by 2028.

1

6

24

1,784

Jun 12

Interesting and very bullish for shareholders of FRMM and debunks any talk of FRMM getting sued and being forced to liquidate. Institutions of this caliber do their due diligence before taking a position in a micro-cap like FRMM!

👇

“Some of the largest currently reported institutional holders include:

Susquehanna International Group

Electric Capital Partners

Hunting Hill Global Capital

Stokes Family Office

Woodline Partners

Wolverine Asset Management

Saba Capital Management

Jane Street Group

Citadel Advisors

UBS Group

The more interesting point is that institutional ownership remains unusually high for a company of FRMM’s size, with institutions reportedly holding over 7.6 million shares, representing more than 50% of the float tracked by Fintel.”

@ManningCapital_ @capybaraReborn @coins @DamianBrad24715 @bpemble @funfactonstocks @SurrogateCap @forummarkets $FRMM

1

8

292

Jun 12

$LAES is making a series of higher lows and fintel shows shares available to short near 0 with a spiking CTB since the recent sell off at the 200ema. could very well pop off after 6/18 OPEX is released.

1

595