May 14

$AUID Q1 2026 earnings: Survival Mode: Massive Disconnect Between Narrative and Financial Reality

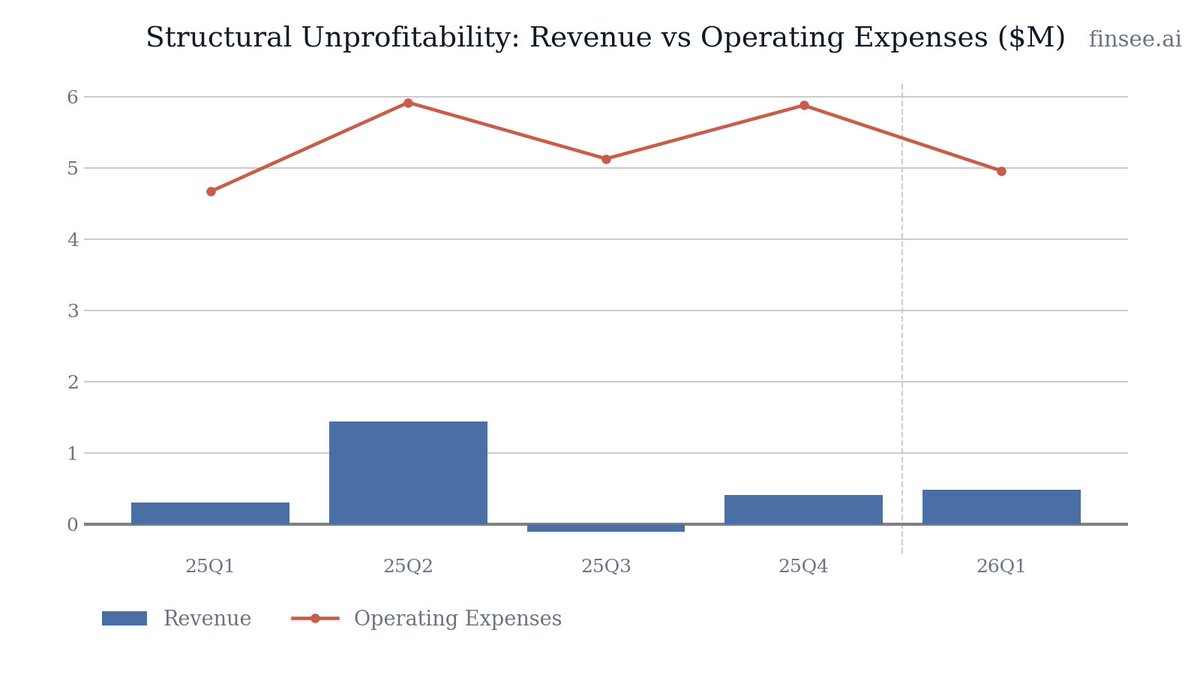

Management called Q1 2026 an 'inflection point', citing structural cost savings and an expanding $40M enterprise pipeline. However, the financials reveal a company in severe distress. While revenue edged up slightly YoY to $0.48M, Gross Booked ARR (bARR) came in at an anemic $80,000, failing to validate the pipeline narrative. More alarmingly, operating cash burn of $3.4M completely overwhelmed the $1.19M in ending cash, forcing the company to secure a $4.2M bridge loan post-quarter just to survive. The continuous erosion of backlog (RPO) points to a business struggling to commercialize its technology.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐌𝐚𝐬𝐬𝐢𝐯𝐞 𝐔𝐧𝐜𝐨𝐧𝐯𝐞𝐫𝐭𝐞𝐝 𝐏𝐢𝐩𝐞𝐥𝐢𝐧𝐞 — The company has built a $40M pipeline across 20 major accounts, with over a dozen active Proof of Concepts (POCs) in sectors like retail, banking, and healthcare. If even a fraction of these convert, revenue could scale rapidly.

• 𝐂𝐨𝐬𝐭 𝐁𝐚𝐬𝐞 𝐑𝐞𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐢𝐧𝐠 — Operating expenses were reduced to $4.96M from higher levels in mid-2025. Coupled with the $4.2M post-quarter bridge loan, the company has bought time to execute its enterprise strategy.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐍𝐞𝐚𝐫-𝐙𝐞𝐫𝐨 𝐒𝐚𝐥𝐞𝐬 𝐄𝐱𝐞𝐜𝐮𝐭𝐢𝐨𝐧 — Despite a supposedly massive pipeline, Q1 Gross Booked ARR was only $80,000. The company is fundamentally failing to close deals and convert its technology into contracted revenue.

• 𝐁𝐚𝐜𝐤𝐥𝐨𝐠 (𝐑𝐏𝐎) 𝐂𝐨𝐥𝐥𝐚𝐩𝐬𝐞 — Remaining Performance Obligation has collapsed from $13.85M a year ago to just $2.0M today. Previous contractual commitments have either been canceled or recognized without being replaced by new business.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🔴🔴

Strongly Bearish. The narrative of an expanding enterprise pipeline is directly contradicted by an $80,000 bookings quarter and a collapsing backlog. The post-quarter $4.2M bridge loan highlights an existential cash crisis, not strategic growth.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🔴🔴 𝐄𝐱𝐢𝐬𝐭𝐞𝐧𝐭𝐢𝐚𝐥 𝐂𝐚𝐬𝐡 𝐂𝐫𝐢𝐬𝐢𝐬 𝐚𝐧𝐝 𝐁𝐫𝐢𝐝𝐠𝐞 𝐋𝐨𝐚𝐧 [NEW]

authID ended Q1 with only $1.19M in cash, while burning $3.42M in operating cash flow during the quarter. This forced the company to secure $4.2M in bridge financing after the quarter closed. This is a severe red flag indicating that the company is operating quarter-to-quarter strictly on external lifelines, vastly increasing dilution and financial risk.

🔴 𝐓𝐡𝐞 𝐑𝐏𝐎 𝐂𝐨𝐥𝐥𝐚𝐩𝐬𝐞 𝐂𝐨𝐧𝐭𝐢𝐧𝐮𝐞𝐬

Remaining Performance Obligation (RPO) is a critical forward-looking indicator for SaaS companies. For authID, this metric has been reversing violently. From a peak of $13.85M in 25Q1, it has bled down sequentially every quarter, landing at just $2.0M in 26Q1. This confirms that the major customer contracts touted in early 2025 either failed to materialize, were canceled, or were heavily negotiated down.

🔴 𝐏𝐢𝐩𝐞𝐥𝐢𝐧𝐞 𝐅𝐚𝐢𝐥𝐬 𝐭𝐨 𝐓𝐫𝐚𝐧𝐬𝐥𝐚𝐭𝐞 𝐢𝐧𝐭𝐨 𝐁𝐨𝐨𝐤𝐢𝐧𝐠𝐬

Management boasts a $40M pipeline and a dozen active POCs with major enterprises. However, Gross Booked ARR (bARR) for the quarter was a microscopic $80,000. There is a glaring, unexplained disconnect between the claimed demand for the product and the company's ability to actually get customers to sign contracts.

🟢 𝐐𝐮𝐚𝐧𝐭𝐮𝐦-𝐑𝐞𝐬𝐢𝐬𝐭𝐚𝐧𝐭 𝐂𝐫𝐲𝐩𝐭𝐨𝐠𝐫𝐚𝐩𝐡𝐲 𝐋𝐚𝐮𝐧𝐜𝐡 [NEW]

authID upgraded its PrivacyKey platform with NIST-standard quantum-resistant encryption algorithms and cryptographic key sharding. This removes single-point-of-failure vulnerabilities. While currently unmonetized in the Q1 numbers, this gives the company a unique technical differentiator for highly regulated industries (government, healthcare, banking) preparing for quantum threats.

⚪ 𝐄𝐱𝐩𝐚𝐧𝐝𝐢𝐧𝐠 𝐭𝐡𝐞 𝐌𝐢𝐜𝐫𝐨𝐬𝐨𝐟𝐭 𝐂𝐡𝐚𝐧𝐧𝐞𝐥 𝐄𝐜𝐨𝐬𝐲𝐬𝐭𝐞𝐦 [NEW]

The company added Formula5, a Microsoft-focused consultancy, as a reseller and implementation partner. Like their existing MajorKey partnership, this embeds authID into the Microsoft Entra and Microsoft Verified ID ecosystems, potentially reducing customer acquisition costs if the channel partners can effectively sell the solution.

⚪ 𝐄𝐧𝐭𝐞𝐫𝐩𝐫𝐢𝐬𝐞 𝐏𝐎𝐂 𝐏𝐫𝐨𝐠𝐫𝐞𝐬𝐬𝐢𝐨𝐧

Management noted that a growing number of the 20 major accounts in their $40M pipeline are coming from their channel partner program. While revenue is lacking today, successfully converting even one or two of these Fortune-level POCs in chip manufacturing or fintech could meaningfully alter the company's trajectory.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀 𝐋𝐨𝐬𝐬: -$3.4 million

Stable compared to the prior year's -$3.9 million, driven by employee and vendor expense reductions, though offset by an increase in stock-based compensation ($1.04M vs $0.45M YoY). The company has marginally optimized its cost structure but remains fundamentally unprofitable.

𝐀𝐧𝐧𝐮𝐚𝐥 𝐑𝐞𝐜𝐮𝐫𝐫𝐢𝐧𝐠 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 (𝐀𝐑𝐑): $1.9 million

Accelerating slightly. While ARR improved from $1.2M in Q1 2025, it is based on annualizing the $0.48M of Q1 2026 revenue. Given the historical volatility of recognized revenue (including a negative quarter in Q3 2025 due to concessions), this annualized metric should be viewed with skepticism until stability is proven.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐒𝐡𝐨𝐫𝐭-𝐓𝐞𝐫𝐦 𝐑𝐏𝐎 𝐑𝐞𝐜𝐨𝐠𝐧𝐢𝐭𝐢𝐨𝐧: ~$1.42 million (Implied)

Decelerating. Management expects to recognize approximately 71% of the current $2.0M Remaining Performance Obligation over the next 12 months (ending March 2027). This implies roughly $1.42M in guaranteed forward revenue, which covers less than half of a single quarter's operating expenses.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐏𝐢𝐩𝐞𝐥𝐢𝐧𝐞 𝐂𝐨𝐧𝐯𝐞𝐫𝐬𝐢𝐨𝐧 𝐁𝐨𝐭𝐭𝐥𝐞𝐧𝐞𝐜𝐤𝐬

You highlight a $40 million pipeline with 20 major accounts in active POCs, yet Q1 booked ARR was only $80,000. What are the specific technical, pricing, or administrative bottlenecks preventing these Fortune-level clients from signing binding contracts?

𝐁𝐫𝐢𝐝𝐠𝐞 𝐋𝐨𝐚𝐧 𝐓𝐞𝐫𝐦𝐬 𝐚𝐧𝐝 𝐃𝐢𝐥𝐮𝐭𝐢𝐨𝐧

Given the critical $4.2 million bridge financing secured after the quarter closed, what are the specific interest rates, warrant coverage, and conversion mechanisms attached to this debt, and how much dilution should current equity holders expect?

𝐑𝐏𝐎 𝐀𝐭𝐭𝐫𝐢𝐭𝐢𝐨𝐧 𝐑𝐞𝐚𝐥𝐢𝐭𝐲

Total RPO has fallen from nearly $14 million a year ago to just $2 million today. Can you explicitly quantify how much of this $12 million drop was recognized as revenue versus how much was written off, canceled, or conceded due to customer failures?

𝐏𝐚𝐭𝐡 𝐭𝐨 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 𝐒𝐮𝐬𝐭𝐚𝐢𝐧𝐚𝐛𝐢𝐥𝐢𝐭𝐲

With operating cash burn running at $3.4 million per quarter, what specific revenue threshold needs to be achieved to reach cash flow breakeven, and by what quarter do you realistically expect to hit that target without requiring further equity or debt injections?

3

574

🛡️ Identity is the new perimeter! $AUID is partnering with Formula5 to bring biometric security to Microsoft-first enterprises.

Key benefits:

✅ Secure remote onboarding for @Microsoft Entra

✅ Passwordless authentication for help desks

✅ Zero Trust architecture for regulated industries

Read more: stocktitan.net/news/AUID/aut…

#authID #AUID #CyberSecurity #MicrosoftEntra #ZeroTrust #Biometrics

@TheBullRunShow

1

4

88

$AUID - authID Announces Strategic Partnership with Formula5 to Deliver Biometric Identity Security for Microsoft-First Enterprises .

548

Kung may MP3 player ka noon, for sure hindi sila nawala sa playlist mo! 🎧✨ Let’s rank #Top5WithFormula5 on #KadaUmaga featuring the True Faith songs na siguradong inulit-ulit din ng ating mga Kada habang nagchi-chill sa radyo o MP3 player nila noon! Agree ka ba sa ranking ng mga kantang ito? 🤔💖 #NET25 #GoodVibes #MorningShow #Top5TrueFaithSongs #TrueFaiht #ThrowbackPlaylist #Formula5

youtube.com/watch?v=-Imx0Pcf…

2

103

20 Nov 2025

La final de la Súper Copa @RoshfransMX se acerca y así luce la tabla general de la categoría GTM Pro 1 con el título en juego🏆

#SuperCopaRoshfrans #AlimentamosTuPasión #GTM #Formula5 #Tractocamiones #MexBike

1

51

17 Nov 2025

NOW: P-Pop boy group #Formula5 serenade the #MutyaNgPilipinas2025 audience before the candidates take the stage. | @diyarista

1

1,806

13 Nov 2025

La 𝐒𝐮́𝐩𝐞𝐫 𝐂𝐨𝐩𝐚 𝐑𝐨𝐬𝐡𝐟𝐫𝐚𝐧𝐬 llega a Monterrey con la Gran Final MRC de la temporada 2025, no te quedes fuera

📆29 de Noviembre

📍Autódromo Monterrey

🔴Boletos en: fanki.com.mx/Super_Copa_Rosh… #SCMonterrey #SúperCopaRoshfransMty #GTM #Formula5 #Tractocamiones #MexBike

2

42

3 Nov 2025

¡Resultados!

#Formula1

👤| Alex Ocenas - P3

👤| Pablo Ortiz - P4

#Formula2

👤| Gergo denes - P2

👤| David campon - P3

#Formula3

👤| Carlos Peyrotón - P6

👤| Alex Martínez - P9

#Formula4

👤| Deckhen - P5

👤| @PasKalGM - P8

#Formula5

👤| Álvaro Marqués - P4

👤| Rubén Aldariz - P8

#LaRevolucion

2

3

6

345

30 Oct 2025

Comenzamos a apuntar hacia el norte➡️➡️🤠

#SuperCopaRoshfrans #SC #AlimentamosTuPasión #GTM #Formula5 #Tractocamiones #MexBike

3

81

13 Oct 2025

La Súper Copa @RoshfransMX se une a la familia Morales, por le sensible fallecimiento del Dr. Jaime Morales, estamos con ustedes 🕊

#SuperCopaRoshfrans #SC #AlimentamosTuPasión #GTM #Formula5 #Tractocamiones #MexBike

3

130

6 Oct 2025

🏆Luego de la emocionante visita de la Súper Copa @RoshfransMX a Puebla, así luce la tabla general de la GTM en sus distintas divisiones.

#SuperCopaRoshfrans #SC #AlimentamosTuPasión #GTM #Formula5 #Tractocamiones #MexBike

2

144

29 Sep 2025

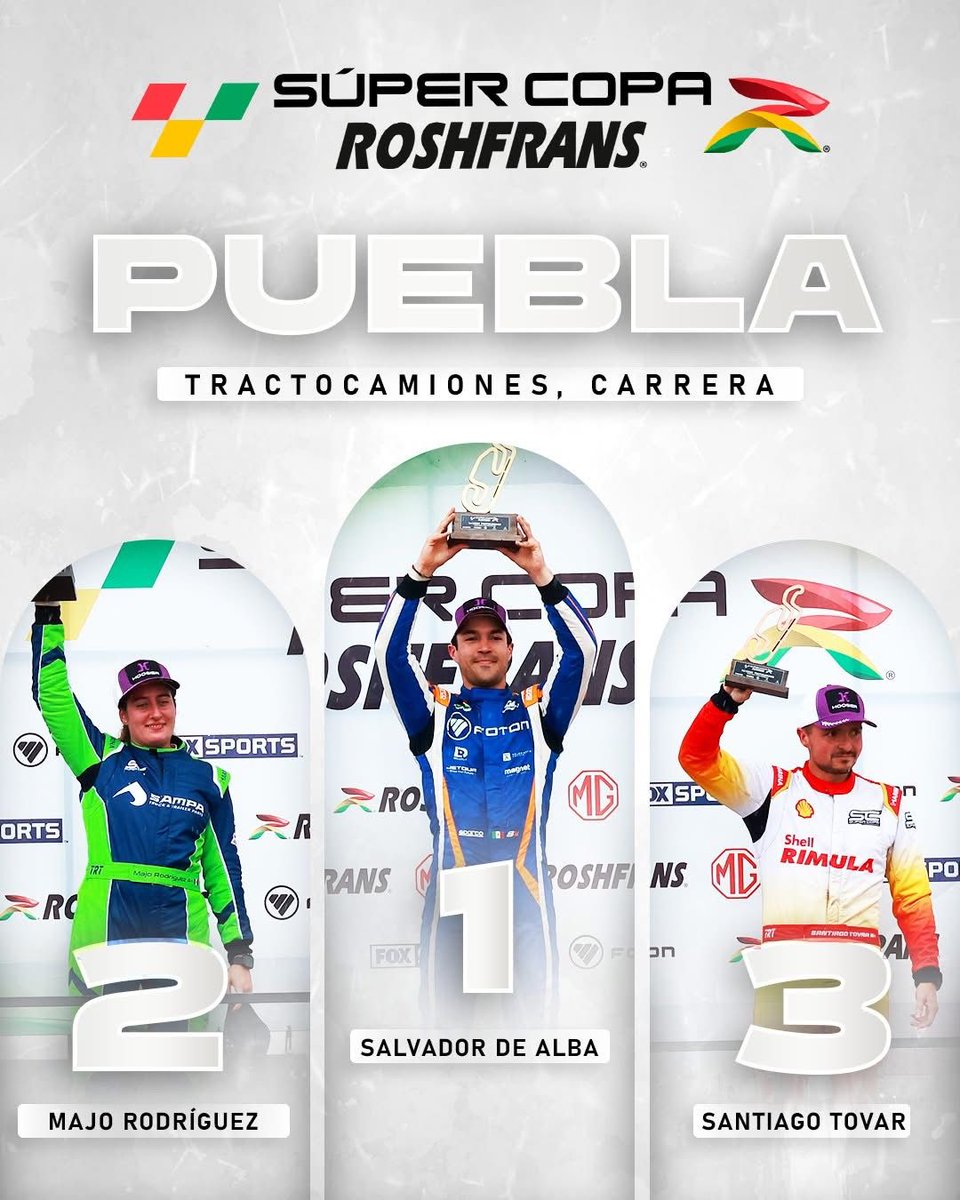

🏁🙋♀️🛻Orgullo poblano en las pistas

Con emoción y mucha entrega, @Majo_rgo brilló en la sección de tractocamiones de la @SuperCopaMex de @RoshfransMX en el Autódromo Miguel E. Abed, llevándose el segundo lugar del podio y el aplauso de la afición poblana. 🎉✨

🏆🏁¡Una vez más confirmamos que somos #TierraDeCampeonasYCampeones! 🏎️🛣️

#PensarEnGrande #PorAmorAPuebl

#SuperCopaRoshfrans #GTM #Formula5 #MexBike #Tractocamiones

#SCPuebla #SúperCopaRoshfransPue #AlimentamosTuPasión

1

6

913

27 Sep 2025

🏁🚀 Velocidad, rugido de motores y se viene la calificación de la GTM en Puebla.

#SuperCopaRoshfrans #SCPuebla #SúperCopaRoshfransPue #AlimentamosTuPasión #GTM #Formula5 #Tractocamiones #MexBike

1

4

98

26 Sep 2025

🔊🎶 La música comienza a sonar en Puebla.

#SuperCopaRoshfrans #SCPuebla #SúperCopaRoshfransPue #AlimentamosTuPasión #GTM #tractocamiones #mexbike #formula5

3

72

24 Sep 2025

Los motores de la Súper Copa @RoshfransMX rugirán en Puebla… ¿qué dicen, @Pericos_Oficial, nos damos una vuelta juntos? ⚡⚾

#SuperCopaRoshfrans #SCPuebla #SúperCopaRoshfransPue #AlimentamosTuPasión #GTM #Formula5 #Tractocamiones #MexBike

1

3

3,362

16 Sep 2025

Un grito también se da en dos ruedas 🇲🇽

#SuperCopaRoshfrans #SC #AlimentamosTuPasión #GTM #Formula5 #Tractocamiones #MexBike

2

89

14 Sep 2025

Gracias a todos los que fueron parte de la Reforestación 2025 de la Súper Copa @RoshfransMX 🌱

Una huella verde ha quedado plasmada en Chihuahua por todos ustedes💚🌿

#SuperCopaRoshfrans #SC #SúperCopaRoshfransCuu #AlimentamosTuPasión #GTM #Formula5 #Tractocamiones #MexBike

1

88

9 Sep 2025

Revive la emoción de la Súper Copa @RoshfransMX en Chihuahua por las pantallas de @FOXSportsMX📺

#SuperCopaRoshfrans #SC #SúperCopaRoshfransCuu #AlimentamosTuPasión #GTM #Formula5 #Tractocamiones #MexBike

1

1

3

153