Graf von Avignon retweeted

Jun 13

Ich würde in meiner Bildungsreform die HTLs entfesseln. Sie werden von allen Sicherheits- und Ethikrichtlinien befreit und die Maschinenbauerbuam dürfen die coolsten Waffensysteme bauen und gemeinsam mit dem Bundesheer testen.

3

1

65

1,716

Jun 12

there may be a few htls with earlier tls but majority no 😔 especially foxaholic now as they even paywall a lot

2

121

Jun 11

@diprjk @AshwaniKumar_92 @ErAaquibSWDeva @kpdcloffice Glad to share that the Augmentation of the 132 kV Alustang–Habak Transmission Line has been undertaken under the CAPEX Budget Scheme by replacing the existing ACSR Panther conductor with HTLS (High Temperature Low Sag) 1/3

1

2

7

447

Jun 11

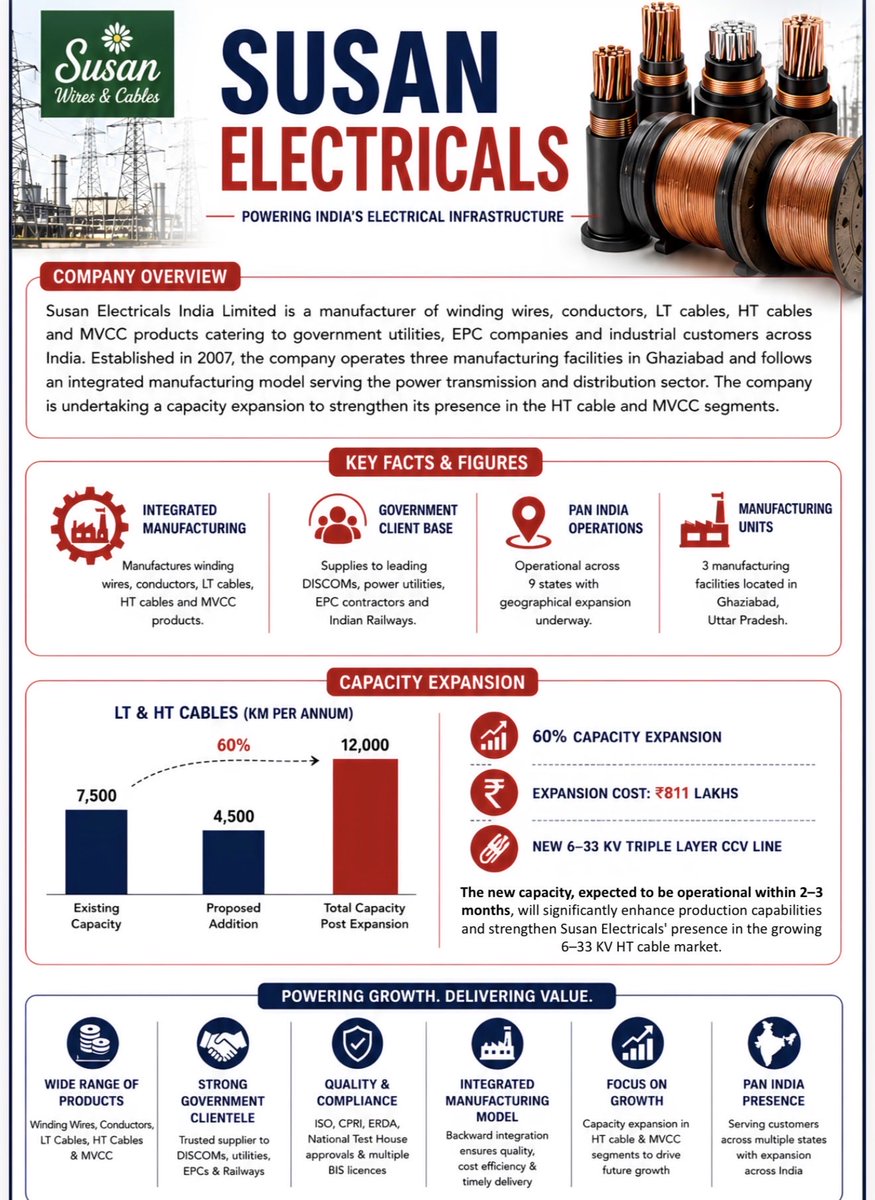

Susan Electricals India Limited SME IPO

Applying 👍

Susan is engaged in the manufacturing of aluminium and copper-based electrical winding wires, conductors, and power cables; Its portfolio of Conductors include AAC, AAAC, ACSR, HTLS, Power Transmission Conductors

The company’s product portfolio includes winding wires and strips used in transformers, motors, alternators, coils, and other electrical equipment, as well as aluminium stranded conductors used in overhead power distribution networks.

Susan's customers primarily Indian Railways, DISCOMs, infrastructure and EPC companies, Etc.

Company Raising 60 Crore in Fresh Issue, Majorly for Working Capital, Capex for expanding its Manufacturing Facility and GCP

60% Capacity Expansion and Ramp-up of Value-Added Products like MVCC to drive further growth

Priced at roughly 14× FY26

As per the working capital data, Priced at ~8× FY27E

Grid modernisation, enhancement and replacement acting as strong tailwinds

Anchor Book includes Motilal Oswal Finvest, SageOne, Shine Star Build-Cap, Arthasanchay, Etc.

7

9

196

16,553

We’re excited to partner with Dynamic Cables in India, which will act as an official stranding partner to manufacture High Temperature Low Sag (HTLS) carbon core conductors using TS technology for this region. wirecable.in/dynamic-cables-…

1

39

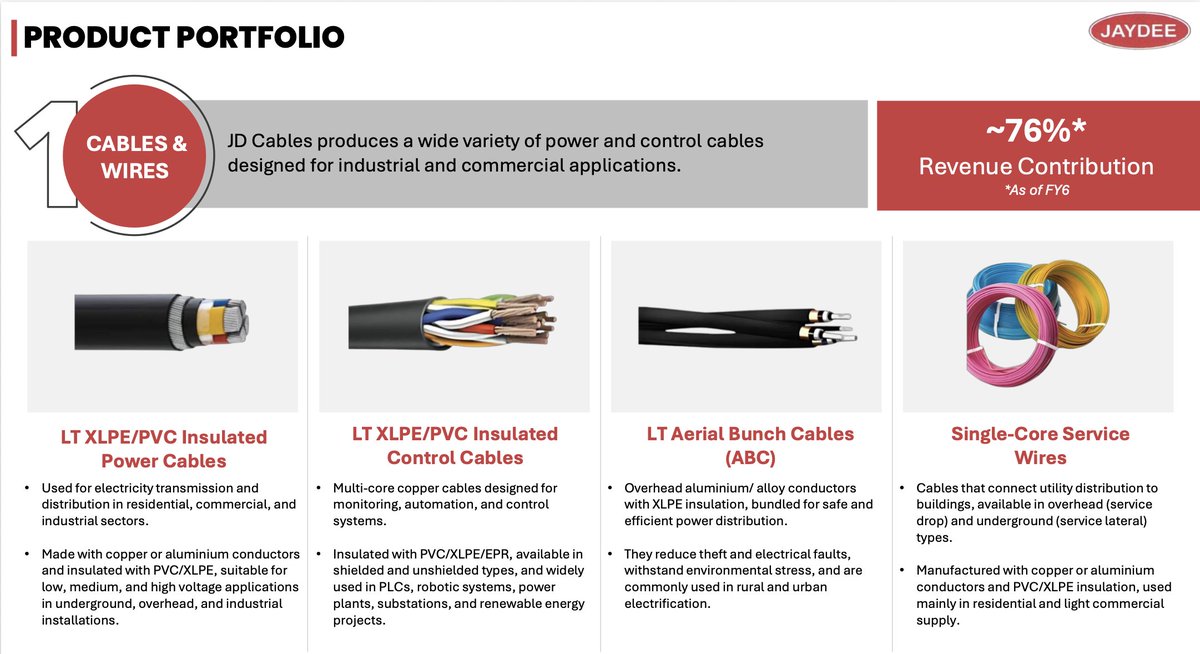

JD Cables Limited is expanding its product portfolio with the introduction of MVCC, AL-59 conductors, HTLS conductors and HT cables as part of its next growth phase.

#JDCables #Conductor #HTCables #PowerTransmission #WireCable #WCI

wirecable.in/jd-cables-expan…

119

🔌 JD Cables targets 50-60% FY27 growth; order book stands at ₹515 Cr

👉🏻 FY26 revenue increased 46% YoY to ₹365 Cr, while PAT grew 44% YoY to ₹31.7 Cr

👉🏻 Order book stood at ~₹515 Cr as of March 31, 2026

👉🏻 Management has guided for 50-60% revenue growth in FY27 and expects similar growth in FY28

👉🏻 Company has bid for over ₹1,000 Cr worth of cable and EPC tenders, with results awaited

👉🏻 New Jamshedpur facility of 1.18 lakh sq ft expected to start operations in phases from FY27 and could double current capacity initially

👉🏻 EPC business revenue expected to rise from ₹30 Cr in FY26 to at least ₹200 Cr in FY27

👉🏻 Management sees potential to expand overall capacity by 3-4x over the next two years depending on order inflows

👉🏻 New products including HTLS conductors, AL-59 conductors, MVCC and HT cables expected to deliver better margins than existing portfolio

#JDCables #Cables #PowerInfrastructure #EPC

1

5

624

THREAD: JD Cables Limited $JDCABLES just dropped H2 FY26 results & they're turning heads!

A small-cap cable manufacturer from West Bengal with a 70% revenue jump in H2 alone?

Let's break it down

H2 FY26 Scorecard (vs H2 FY25)

Revenue ₹243 Cr ▲ 70% YoY

EBITDA ₹28.9 Cr ▲ 52% YoY

PAT ₹19.8 Cr ▲ 69% YoY

EBITDA Margin: 11.84% | PAT Margin: 8.12%

Margins slightly compressed vs H2 FY25 due to scale-up in operations — watch this.

Full Year FY26 — The Big Picture

Total Income ₹365 Cr ▲ 46% YoY

EBITDA ₹48.1 Cr ▲ 98% YoY

PAT ₹31.7 Cr ▲ 44% YoY

From ₹101 Cr in FY24 → ₹251 Cr in FY25 → ₹365 Cr in FY26

3-year revenue CAGR is simply exceptional for a small-cap manufacturer.

Balance Sheet & Key Ratios — This Is The Bull Case

The debt story here is remarkable

D/E Ratio 0.39x ↓ (was 2.27x in FY24)

Current Ratio 2.25x ↑

ROE 21.70%

ROCE 23.11%

EPS ₹14.07

Net Worth ₹146 Cr

Debt-to-Equity collapsed from 2.27x → 0.39x in just 2 years. Company raised equity (IPO/QIP), paid down debt. Balance sheet is now clean

Growth Levers — What's Driving the Next Phase?

📦 Order Book: ₹515 Crore as of March 2026 — 1.4x FY26 revenues. Solid visibility!

🏭 New Capacity: New 1.18 lakh sq.ft. facility at Dankuni (Unit III) — 28,000 km capacity coming online.

🛣️ Infra Play: Entered NH-2 highway project (Bihar-Jharkhand 6-laning) under NHDP Phase V.

🔌 Product Expansion: Adding MVCC, AL-59, HTLS & HT cables — moving up the value chain.

Industry Tailwinds — It's All About India's Infra Push

India Wires & Cables market: $9.32B in 2024 → projected $17.08B by 2032 (CAGR ~8%)

Key demand drivers supporting JD Cables:

Power T&D expansion

Rural electrification

Solar & wind projects

Smart cities

Metro & highways

Data centres

Approved vendor for multiple State Electricity Boards. Presence in 15 states. Repeat government orders = sticky revenue.

tock Data & Valuation Snapshot

Share Price

₹206 as of 05/06/26

Market Cap ₹464 Cr

BSE SME 52W Range

₹130–₹248 currently mid

P/E ≈ 14.6x on FY26 EPS of ₹14.10. For a company growing revenue at 46% with ROE of 36% and clean debt — that's not expensive if growth sustains. Promoters hold 70% — skin in the game. ✅

BSE SME — lower liquidity risk Not SEBI registered advice

My Take — Risks vs Opportunity

Bulls argue: Strong order book, clean balance sheet, margin expansion story, infra supercycle beneficiary.

Bears watch: Raw material price volatility (copper/aluminium), margin compression in H2, order bunching risk, SME illiquidity.

Bottom line: JD Cables is a micro-cap executing well in a macro tailwind sector. Unit III capacity expansion in FY27 will be the key de-risker to watch.

Not financial advice. Do your own research. BSE SME stocks carry higher risk & lower liquidity. | Source: JD Cables H2 FY26 Investor Presentation, BSE Disclosure Jun 04, 2026.

#JDCables #JDCABLES #SmallCap #CableStocks #BSE #InfraIndia

t.me/ HN8MHAdNy7diZjRl

1

1

4

547

Jun 6

JD CABLES – DETAILED CONCALL Q4 FY26 🧾📑

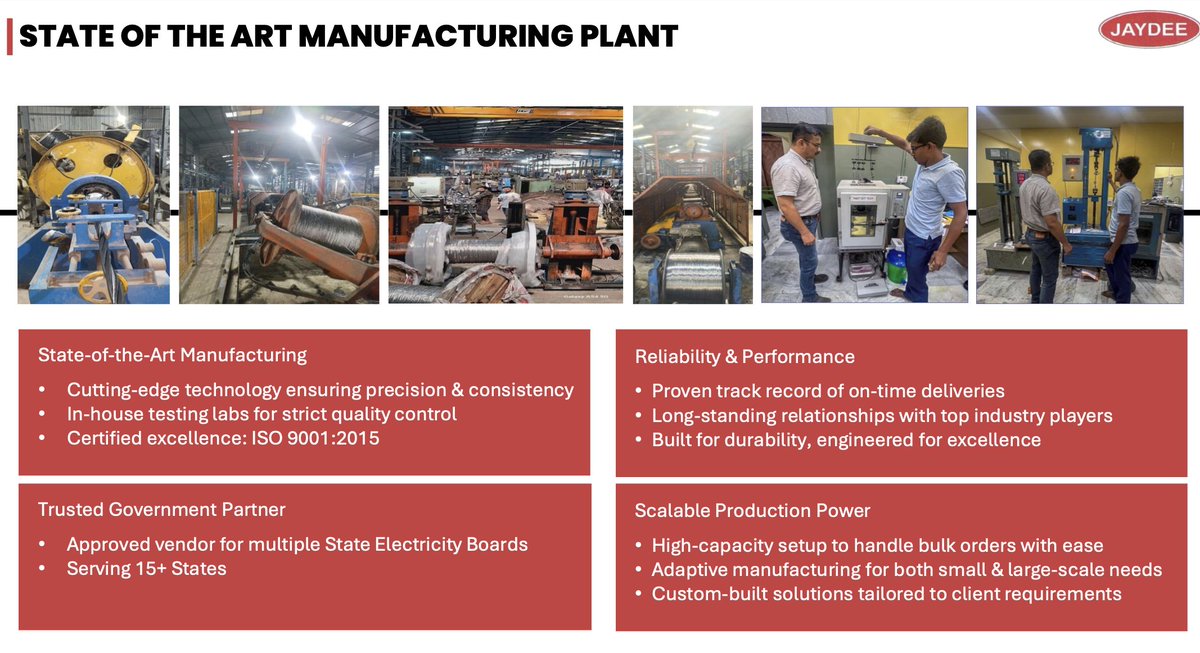

JD Cables continues to strengthen its position in the power transmission and distribution ecosystem through its growing presence in cables, conductors and EPC projects. The company serves utilities, infrastructure projects, industrial customers and various State Electricity Boards across India and has built a strong presence across Northern, Eastern and North-Eastern India.

Its product portfolio currently includes power cables, control cables, instrumentation cables, service cables and conductors such as AAC, AAAC and ACSR. The company believes that rising investments in power infrastructure, transmission networks, electrification programs and industrial development continue to create significant long-term opportunities for growth.

One of the biggest highlights of the concall was the company's manufacturing expansion strategy.

Currently, JD Cables operates two manufacturing facilities with a combined installed capacity of approximately 28,000 kilometres per annum.

▪ Unit I Capacity – 6,000 kilometres

▪ Unit II Capacity – 22,000 kilometres

The existing plants are already operating at strong utilization levels.

▪ Unit I Utilization – 82.4%

▪ Unit II Utilization – 84.6%

This high utilization level is one of the key reasons behind the company's aggressive expansion plans.

🔸 The most important growth driver discussed during the call was the new Dankuni manufacturing facility.

The company has acquired a large industrial facility spread across approximately 1.18 lakh square feet. This facility is expected to become the foundation of JD Cables' next phase of growth.

The conductor division has already been installed and is ready for operations. The only pending requirement is the electricity connection, which the company expects shortly. Once power is received, commercial production can begin immediately.

The cable division is expected to commence operations within the next couple of months.

Management expects the facility to start contributing meaningfully by September 2026 and become a major contributor to growth over the coming years.

A particularly important point highlighted during the discussion was that the company has acquired a facility significantly larger than its current requirements.

The available space allows installation of substantial additional machinery without requiring another major plant acquisition.

In addition, the company has already initiated the process of acquiring adjacent land and has made advance payments towards the same, demonstrating confidence in future expansion requirements.

According to the company, the expansion potential of this facility is significant.

▪ Initial capacity expansion is expected to roughly double existing capacity.

▪ Depending upon demand and order inflows, total capacity can potentially increase 3x–4x over the next two years.

▪ Additional machinery can be installed relatively quickly due to the availability of space and infrastructure.

▪ Future expansion will largely depend upon order book growth and demand visibility.

🔸 Apart from physical capacity expansion, the company is also expanding its product portfolio aggressively.

New products under development and commercialization include:

▪ MVCC

▪ AL-59 Conductors

▪ HTLS Conductors

▪ HT Cables

These products are strategically important because they allow JD Cables to participate in a broader range of transmission and distribution tenders and increase its addressable market.

Several of these products are higher-value products compared to the existing portfolio and are expected to improve the overall product mix.

The company is currently working on BIS approvals, certifications, testing requirements and vendor registrations required for commercial supply. Commercial production and scaling will gradually increase as approvals are received.

Another key takeaway from the call was management's confidence regarding margins in these new products.

While exact profitability cannot yet be quantified, they expect these products to generate better margins than the existing portfolio once commercialized.

The company currently enjoys strong revenue visibility through its order book.

As of 31st March 2026, the order book stood at approximately ₹515 crore.

The broad breakup is:

▪ EPC Projects – ~₹300 crore

▪ Cables & Conductors – ~₹200 crore

The typical execution cycle remains around 1.5 years.

The company also clarified that a significant portion of business comes from repeat customers and shorter-cycle orders, which are not always reflected in the reported order book.

Beyond the existing order book, the company has already participated in tenders worth more than ₹1,000 crore across both EPC and cable businesses.

Many of these tenders are currently awaiting results.

Although the company does not have a long history in some of the newer transmission and distribution categories, it remains optimistic about securing a meaningful share of these opportunities.

Looking ahead, the company is targeting an order book of approximately ₹700–800 crore by March 2027.

If achieved, this would further strengthen revenue visibility for subsequent years.

🔸 One of the most important strategic developments discussed during the concall was the company's expansion into the EPC business.

The company views EPC as a natural forward integration opportunity.

Every transmission and distribution project requires cables and conductors. Since JD Cables already manufactures these products, entering EPC allows the company to move further up the value chain and capture a larger share of project economics. The EPC division is being led by Mr. Rajesh Jhunjhunwala, who brings significant industry experience to the business.

The company has already commenced execution of a National Highway Development Project involving civil and electrical works.

In addition, it has actively started participating in transmission and distribution EPC tenders.

Importantly, management made it clear that EPC is not a temporary diversification effort. The company intends to make EPC a recurring and meaningful business vertical going forward.

Regarding ongoing execution, approximately 10% of the current EPC project has already been completed. A significant portion of the remaining work is expected to be executed during FY27.

The EPC business is expected to become a major growth driver over the next few years.

During FY26, EPC revenue stood at approximately ₹30 crore.

For FY27, the company expects EPC revenue of at least ₹200 crore and potentially higher depending upon project execution and order wins.

The company described this estimate as conservative.

🔸 Growth guidance was another major highlight of the concall.

The company expects revenue growth of approximately 50–60% in FY27.

Interestingly, they also indicated that similar growth momentum could continue into FY28.

This growth is expected to be driven by multiple factors:

▪ Ramp-up of the Dankuni facility.

▪ New product launches.

▪ Existing order book execution.

▪ EPC business expansion.

▪ New tender wins.

▪ Strong demand from transmission and distribution projects.

▪ Increasing participation in state electricity board opportunities.

Within the core manufacturing business itself, cables and conductors are expected to grow approximately 30–40%.

The combination of manufacturing growth and EPC growth is expected to drive the overall 50–60% revenue growth target.

The discussion also covered profitability expectations.

Despite entering EPC and investing heavily in expansion, the company expects overall margins to remain broadly stable.

The management team indicated that EBITDA margins should remain around current levels, broadly in the 12–13% range.

For EPC projects, PAT margins are expected to be around 8%.

The company also expects margin support from the commercialization of higher-value products such as HTLS, AL-59 and HT cables.

🔸 Working capital was extensively discussed during the Q&A session.

The company acknowledged that rapid growth naturally puts pressure on working capital requirements.

In addition, EPC projects require substantial upfront execution before billing milestones are achieved, resulting in temporary pressure on cash flows.

According to the company, the elevated working capital requirement seen recently is largely linked to the ongoing EPC execution phase. Despite this, they remain comfortable with the current financial position and do not foresee any immediate challenges in executing ongoing projects.

For future growth requirements, the preferred funding route remains bank debt rather than equity dilution. The company has already initiated discussions with banks and indicated that funding support is available whenever required.

On the capex front, the company expects additional investments of approximately ₹20–30 crore depending upon future order inflows and capacity expansion requirements.

The flexibility offered by the Dankuni facility means future expansion can be undertaken relatively quickly whenever required.

The management team also sounded optimistic regarding emerging opportunities in West Bengal, where they expect increasing infrastructure spending and project activity over the coming years.

Overall, the key message from the concall was clear

JD Cables is attempting to transform itself from a traditional cable and conductor manufacturer into a larger integrated power infrastructure player.

📌 Key Numbers at a Glance

▪ Installed Capacity – 28,000 km per annum

▪ Unit I Capacity – 6,000 km

▪ Unit II Capacity – 22,000 km

▪ Unit I Utilization – 82.4%

▪ Unit II Utilization – 84.6%

▪ New Facility Size – 1.18 lakh sq. ft.

▪ Current Order Book – ₹515 crore

▪ EPC Order Book – ~₹300 crore

▪ Cable & Conductor Order Book – ~₹200 crore

▪ Tender Participation – ₹1,000 crore

▪ FY27 Order Book Target – ₹700–800 crore

▪ FY26 EPC Revenue – ~₹30 crore

▪ FY27 EPC Revenue Target – ₹200 crore

▪ FY27 Revenue Growth Guidance – 50–60%

▪ Core Cable & Conductor Growth Expectation – 30–40%

▪ Additional Planned Capex – ₹20–30 crore

▪ Potential Capacity Expansion – 3x–4x over next two years

Disclaimer: This summary is based on management commentary during the conference call and is intended solely for educational purposes. Please conduct your own research before making any investment decisions.

May 13

KEI Industries Q4 FY26 Earnings Call - Important Insights On India’s Cable Industry & High Voltage Cable Opportunity ⚡️⚡️

Some very important industry takeaways from KEI Industries management commentary:

▪ Management remains very bullish on India’s power transmission & distribution capex cycle.

▪ Management clearly stated that demand in both domestic and export markets remains very strong.

▪ One important statement from management:

“Whatever capacity we are having, we are able to sell easily.”

▪ Extra High Voltage (EHV) cable business is seeing strong growth:

🔸 FY26 EHV domestic institutional sales: ₹559 Cr

🔸 Growth: 82% YoY

▪ Q4FY26 EHV sales:

🔸 ₹188 Cr vs ₹115 Cr last year

🔸 Growth: 64% YoY

▪ Management expects another ~20% growth in EHV segment going forward.

▪ Company highlighted that India’s transmission infrastructure capex remains a major long-term growth driver for the cable industry.

▪ KEI is aggressively scaling capacity through the Sanand plant expansion.

▪ Management guided:

🔸 17-18% volume growth in FY27

🔸 Similar strong growth expected in FY28 as capacities stabilize further

▪ Sanand expansion is expected to become a major growth contributor for cables and high-voltage products.

▪ Important export commentary:

KEI expects exports to contribute nearly 20% of total sales going forward.

▪ Management highlighted improving global acceptance of Indian cable manufacturers.

▪ One very important trend:

KEI has restarted exports to the United States after tariff-related slowdown earlier.

▪ Data center opportunity was specifically highlighted by management.

▪ KEI expects strong demand for:

🔸 HT cables

🔸 Medium voltage cables

🔸 Copper flexible cables

from data center infrastructure projects.

▪ Management indicated that data centers can become a major long-term demand driver for the cable industry.

▪ Solar and renewable energy opportunity also continues to scale.

▪ KEI has started manufacturing:

🔸 Solar wires using electron beam technology

🔸 Advanced cable products from Sanand facility

▪ Management clearly stated:

“Quarter after quarter, solar cable/wire business will keep growing.”

▪ Industry localization theme also visible:

KEI is exploring backward integration into:

🔸 Medium voltage compounds

🔸 Cable armor wire manufacturing

▪ One important management commentary:

The company is continuously adding products where opportunities are emerging inside the electrical and cable ecosystem.

▪ Current order book visibility remains strong:

🔸 EHV cable order book: ₹625 Cr

🔸 Additional L1 EHV orders: ₹233 Cr

🔸 Domestic cable institutional order book: ₹2,154 Cr

🔸 Export cable order book: ₹497 Cr

▪ Management commentary strongly suggests that:

India’s cable industry is entering a multi-year growth cycle driven by:

🔸 Power infrastructure expansion

🔸 Renewable energy growth

🔸 Transmission capex

🔸 Data center expansion

🔸 Industrial capex

🔸 Real estate demand

🔸 Export opportunities

🔸 High-voltage cable demand growth

Overall, management commentary indicates that the Indian cable industry is no longer dependent only on traditional construction demand, but is increasingly becoming linked with power infrastructure, renewable energy, grid modernization, data centers and global export opportunities.

Disclaimer:

This is only for educational and informational purposes and should not be considered as investment advice. Please do your own research before investing.

4

12

57

15,648

📈 JD Cables Ltd: Strong Growth & Expansion Plans – Order Book at INR515 Crores, Targets INR700-800 Crores by 2027 | MCap 412.69 Cr

- Order book (Mar 2026): INR515 crores, expected to reach INR700-800 crores by Mar 2027.

- FY26 total income: INR365 crores (45.67% YoY growth).

- EBITDA FY26: INR48.11 crores (40% growth); PAT: INR31.72 crores (44% growth).

- Half-yearly highlights: Revenue INR243 crores (70% growth), EBITDA INR28 crores (52% growth), PAT INR19 crores (69% growth).

- Capacity: 28,000 km/year, utilization at 82.4% (Unit I) & 84.6% (Unit II).

- New facility: 1.18 lakh sq. ft in Jamshedpur for expansion.

- FY27 targets: 50%-60% revenue growth, steady margins (12%-13% EBITDA).

- Capex planned: INR20-30 crores for FY27.

- EPC business: Contributed INR30 crores in FY26, expected INR200 crores in FY27 (8% PAT margin).

- New product lines: MVCC, AL59 conductors, HTLS conductors, HE cables.

Disc: Information provided in this tweet can be inaccurate, verify through the source in reply before making any investment decision.

Preview 👇 (First 4 out of 15 pages)

2

10

881

Jun 4

☎️ JD Cables - H2FY26/FY26 Concall Highlights

📊 Financial Performance (FY26)

▪️ Total Income: Stood at ₹365 crores, registering a strong growth of 45.67% YoY.

▪️ EBITDA Growth: Increased to ₹48.11 crores, reflecting a 40% YoY growth.

▪️ Profit After Tax (PAT): Grew to ₹31.72 crores, a robust increase of 44% YoY.

▪️ H2FY26 Performance: Total income for the second half was ₹243 crores (70% YoY growth), with PAT at ₹19 crores (69% YoY growth).

▪️ Margin Fluctuation: EBITDA margin declined from 16% in H1 to ~12% in H2, attributed to volume discounts and higher raw material prices.

📈 Operational Highlights

▪️ Strong Order Book: Maintained a robust order book of approximately ₹515 crores as of March 31, 2026.

▪️ Order Book Mix: The current order book comprises ~₹300 crores from the EPC segment and ~₹200 crores from cables and conductors.

▪️ Capacity Utilization: Achieved healthy utilization levels of 82.4% at Unit 1 and 84.6% at Unit 2.

▪️ Market Reach: Established a strong presence across northern, eastern, and northeastern India, serving multiple state electricity boards.

🏭 Capacity Expansion & New Products

▪️ New Facility Acquired: A new industrial facility spanning 1.18 lakh square feet was acquired to support future growth.

▪️ Expansion Timeline: The new conductor division is set to begin operations within the month, with the cable division starting in the next two months.

▪️ Future Capacity: Plans to initially double capacity, with the potential to expand it 3x to 4x within the next two years.

▪️ New Product Portfolio: Expanding into higher-margin products including MVCC, AL59 conductors, HTLS conductors, and HT cables.

▪️ Land Procurement: Actively procuring additional land adjacent to the new factory for further expansion.

🏗️ EPC Business Segment

▪️ Strategic Diversification: Entered the infrastructure EPC segment, currently executing a national highway development project.

▪️ FY26 EPC Revenue: The company booked ₹30 crores from the EPC business in FY26.

▪️ FY27 EPC Target: Aims to book a minimum of ₹200 crores in revenue from the EPC segment in FY27.

▪️ EPC Margins: The company is operating at an estimated 8% PAT margin (or ~12-13% EBITDA margin) in the EPC business.

▪️ Working Capital Impact: The EPC projects have led to an increase in the working capital cycle due to funds being tied up in project execution.

🎯 Guidance & Future Outlook

▪️ Revenue Guidance: The management is targeting a significant revenue growth of 50-60% for FY27.

▪️ Margin Outlook: Expects to maintain similar EBITDA margins of around 12-13% going forward.

▪️ Capex Plan: A capex of ₹20-30 crores is planned for FY27.

▪️ Order Book Target: Aims to increase the order book to at least ₹700-800 crores by the end of FY27.

▪️ Tender Pipeline: The company has participated in tenders worth over ₹1,000 crores across both cable and EPC segments.

▪️ Regional Opportunities: A change in the state government of West Bengal is expected to unlock significant investment and infrastructure projects.

🚫 No Recommendation

Source: Concallin

May 21

📊 23 Quality SME Companies To Study, Research & Track

▪️ Msafe Equipments

▪️ Prime Cables

▪️ Systematic Industries

▪️ Aimtron Electronics

▪️ L. T. Elevator

▪️ KRM Ayurveda

▪️ OBSC Perfection

▪️ CFF Fluid

▪️ ABS Marine

▪️ Indo SMC

▪️ Suba Hotels

▪️ JD Cables

▪️ Patil Automation

▪️ Prizor Viztech

▪️ Freshara Agro Exports

▪️ Viviana Power

▪️ Yash Highvoltage

▪️ Oriana Power

▪️ Alpex Solar

▪️ Danish Power

▪️ Rajesh Power

▪️ Airfloa Rail

Disc: No Recommendation. Shared for educational purpose only. DYODD.

2

4

21

4,495

Jun 4

JD Cables Q4 FY26 concall insights - Capacity Expansion Meets EPC Execution

📈 Growth remained strong

• FY26 revenue grew 46% YoY while PAT increased 44% YoY

• H2 growth accelerated with revenue and PAT rising ~70% YoY

🏭 Next phase starts now

• New conductor facility starts this month and cable division follows shortly

• Capacity set to double initially with room for further expansion

🔌 Moving up the value chain

• Expanding into HT cables, HTLS conductors and other higher-value products

• New products expected to carry better margins than existing portfolio

🏗️ EPC is becoming meaningful

• EPC contributed ₹30 Cr revenue in FY26

• Management targets ₹200 Cr EPC revenue in FY27

• Current EPC project execution is only around 10%

📦 Visibility remains healthy

• Order book stands at ₹515 Cr

• Company has bid for ₹1,000 Cr worth of new projects

🎯 Growth guidance stays ambitious

• Management guides for 50-60% revenue growth in FY27

• Order book target of ₹700-800 Cr by FY27 end

⚠️ Execution will be key

• Margins moderated to ~12-13% in H2

• Working capital needs and debt are likely to increase with EPC scale-up

#JDCables #Q4FY26 #Concall

1

6

867

Jun 4

#SME #JDCABLES #JayDee

JD Cables Limited H2 FY26 Concall Highlights

👉 FY27 & Future Outlook

▫️Targeting 50-60% YoY growth in FY27, driven by new product lines, capacity ramp-up, and EPC execution.

💠 Core cables & conductors business alone expected to grow 30-40%; EPC segment to contribute significantly higher (from ₹30 Cr in FY26 to minimum ₹200 Cr in FY27 on conservative basis).

💠 Overall revenue potential from new Dankuni facility: 2x–4x within 2 years through higher-capacity machines and expanded product mix.

▫️Margins to remain stable – EBITDA margins expected to stay in the 12-13% range (similar to FY26 levels).

💠Newer products (MVCC, AL-59, HTLS, HT cables) expected to deliver incrementally higher margins than existing portfolio.

💠 EPC margins currently ~8%; overall blended margins to remain in double digits

▫️Capacity expansion on track – New 1.18 lakh sq. ft. facility at Dankuni: electricity connection expected this month (June 2026); conductor division to start immediately, cable division within next 2 months.

💠 FY27 utilization: 70-80% overall; full capacity utilization targeted in FY28.

💠 Additional CAPEX planned at ₹20-30 Cr (machinery adjacent land advance already paid) to support further scaling.

👉 Current Order Book / Projects and Future Pipeline

▫️Order Book – ₹515 Cr as of 31st March 2026 (execution visibility of 1–1.5 years).

💠 Provides revenue visibility for FY27 and beyond.

▫️EPC Project Update

💠National Highway development project (NHDP Phase V – Bihar–Jharkhand border): ~10% completed in FY26; good percentage expected by end of FY27.

💠 Synergistic with core cable supply – majority electrical works backed by in-house cables & conductors.

▫️ Tender Pipeline – Actively bidding in >₹1,000 Cr worth of tenders (both EPC and cables/conductors).

💠 Conversion ratio difficult to predict as company is scaling participation in larger transmission & distribution tenders.

💠 Order book target by 31st March 2027: ₹700–800 Cr (conservative); internal stretch target ₹1,000 Cr.

👉 Other Notable Points

▫️FY26 Operational Highlights

💠 Installed capacity: ~28,000 km p.a. (Unit I: 6,000 km @ 82.4% utilisation; Unit II: 22,000 km @ 84.56% utilisation).

💠 10 years experience, 15 states presence, ISO 9001:2015, 5 BIS certificates, in-house testing labs.

💠 Approved vendor to multiple State Electricity Boards (Assam, Odisha, Jharkhand, Bihar, etc.).

▫️Working Capital & Funding

💠 Cash flow from operations was negative (~₹70–74 Cr) primarily due to aggressive growth, higher inventory, and EPC execution (funds blocked in project milestones).

💠 Management comfortable – sufficient bank balances banks ready to extend debt funding as required. No immediate equity dilution planned.

▫️Strategic Focus

💠 Product portfolio expansion (MVCC, AL-59, HTLS, HT cables) capacity addition EPC diversification.

💠 Healthy balance sheet and execution capabilities position the company well for sustained long-term value creation

Mar 26

👉Mainboard stocks often get all the attention but some of the most compelling businesses are hiding in plain sight — on the SME Platform.

👉Smaller. Less covered, though noisy at times. Yet occasionally, genuinely exceptional.

———

👉Introducing SME Gems — a new independent series on Hidden Champions of the SME Platform :

💠 OBSC Perfection

💠 Aimtron Electronics

💠 Yash Highvoltage

💠 CFF Fluid Control

💠 DSM Fresh Foods

💠 L.T. Elevator

💠 Monolithisch India

💠 GSM Foils

👉Across Different Sectors. One common place.

🔗 smeresearch.github.io/SMEGem…

👉Stay tuned for more insights

———

⚠️ For educational purposes only. Not investment advice. Please DYODD.

#SMEGems #SMEPlatform #HiddenChampions #SME

2

4

40

5,730

Jun 4

𝗝𝗗 𝗖𝗮𝗯𝗹𝗲𝘀 𝗟𝘁𝗱. 𝗽𝗿𝗲𝘀𝗲𝗻𝘁𝗲𝗱 𝗶𝘁𝘀 𝗶𝗻𝘃𝗲𝘀𝘁𝗼𝗿 𝗽𝗿𝗲𝘀𝗲𝗻𝘁𝗮𝘁𝗶𝗼𝗻 𝗳𝗼𝗿 𝗛2 𝗙𝗬26, showcasing robust financial growth and strategic expansion initiatives. The company reported a significant 70% 𝗬𝗼𝗬 𝗿𝗲𝘃𝗲𝗻𝘂𝗲 𝗴𝗿𝗼𝘄𝘁𝗵 𝗳𝗼𝗿 𝗛2 𝗙𝗬26 and 46% 𝗳𝗼𝗿 𝘁𝗵𝗲 𝗳𝘂𝗹𝗹 𝗙𝗬26, driven by strong customer relationships and execution capabilities. 📈

𝗞𝗲𝘆 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗛𝗶𝗴𝗵𝗹𝗶𝗴𝗵𝘁𝘀 & 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲:

- 𝗧𝗼𝘁𝗮𝗹 𝗜𝗻𝗰𝗼𝗺𝗲: Increased to ₹24,375.47 Lakhs in H2 FY26 from ₹14,318.31 Lakhs in H2 FY25.

- 𝗘𝗕𝗜𝗧𝗗𝗔: Grew to ₹2,886.61 Lakhs in H2 FY26 from ₹1,895.33 Lakhs in H2 FY25, with the EBITDA margin at 11.84%.

- 𝗣𝗔𝗧: Rose to ₹1,979.86 Lakhs in H2 FY26 from ₹1,171.26 Lakhs in H2 FY25, with a PAT margin of 8.12%.

- 𝗙𝗬26 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲: Total Income ₹36,519.36 Lakhs, EBITDA ₹4,811.01 Lakhs, PAT ₹3,172.46 Lakhs.

- 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗥𝗮𝘁𝗶𝗼𝘀: ROE at 21.70% & ROCE at 23.11% for FY26.

𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗚𝗿𝗼𝘄𝘁𝗵 & 𝗘𝘅𝗽𝗮𝗻𝘀𝗶𝗼𝗻:

- 𝗜𝗻𝗳𝗿𝗮𝘀𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗲 𝗣𝗿𝗼𝗷𝗲𝗰𝘁𝘀: Expanded into infrastructure, currently involved in a key National Highway development project (NHDP Phase V). 🛣️

- 𝗣𝗿𝗼𝗱𝘂𝗰𝘁 𝗣𝗼𝗿𝘁𝗳𝗼𝗹𝗶𝗼: Adding new product lines like MVCC, AL-59, HTLS, and HT cables.

- 𝗖𝗮𝗽𝗮𝗰𝗶𝘁𝘆 𝗘𝘅𝗽𝗮𝗻𝘀𝗶𝗼𝗻: Acquired a new ~1.18 lakh sq. ft. industrial facility at Dankuni.

- 𝗢𝗿𝗱𝗲𝗿 𝗕𝗼𝗼𝗸: Maintained a strong order book of approximately ₹515 crore as of March 2026, ensuring revenue visibility. 💰

𝗕𝘂𝘀𝗶𝗻𝗲𝘀𝘀 𝗢𝘃𝗲𝗿𝘃𝗶𝗲𝘄:

- JD Cables manufactures Power Cables, Control Cables, Aerial Bunched Cables, Service Wires, and Conductors (AAC, AAAC, ACSR).

- Products are used in electricity transmission & distribution.

- Approved vendor for various State Electricity Boards across 15 States.

- 𝗜𝗻𝘀𝘁𝗮𝗹𝗹𝗲𝗱 𝗖𝗮𝗽𝗮𝗰𝗶𝘁𝘆: Unit I (6,000 Kms), Unit II (22,000 Kms), Unit III upcoming (28,000 Kms).

- 𝗖𝗮𝗽𝗮𝗰𝗶𝘁𝘆 𝗨𝘁𝗶𝗹𝗶𝘇𝗮𝘁𝗶𝗼𝗻: Unit I at 82.43%, Unit II at 84.56% (FY26).

𝗠𝗮𝗿𝗸𝗲𝘁 𝗢𝘂𝘁𝗹𝗼𝗼𝗸:

- The Indian Wires & Cables Market is valued at USD 9.32 Billion (2024) and projected to reach USD 17.08 Billion by 2032 (CAGR of 7.94%).

- Key growth drivers include power infrastructure expansion, renewable energy projects, construction boom, and urbanization. 🏙️

The company expressed confidence in sustaining its growth momentum and creating long-term value for stakeholders, citing a healthy balance sheet, improved financial ratios, and growing market opportunities. The presentation also detailed the management team, operational strategies, SWOT analysis, and stock data.

📊 JD CABLES LTD | 🏷️ Investor Presentation

🌐 Details: wegro.app/26aWp6

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/go

2

2

182

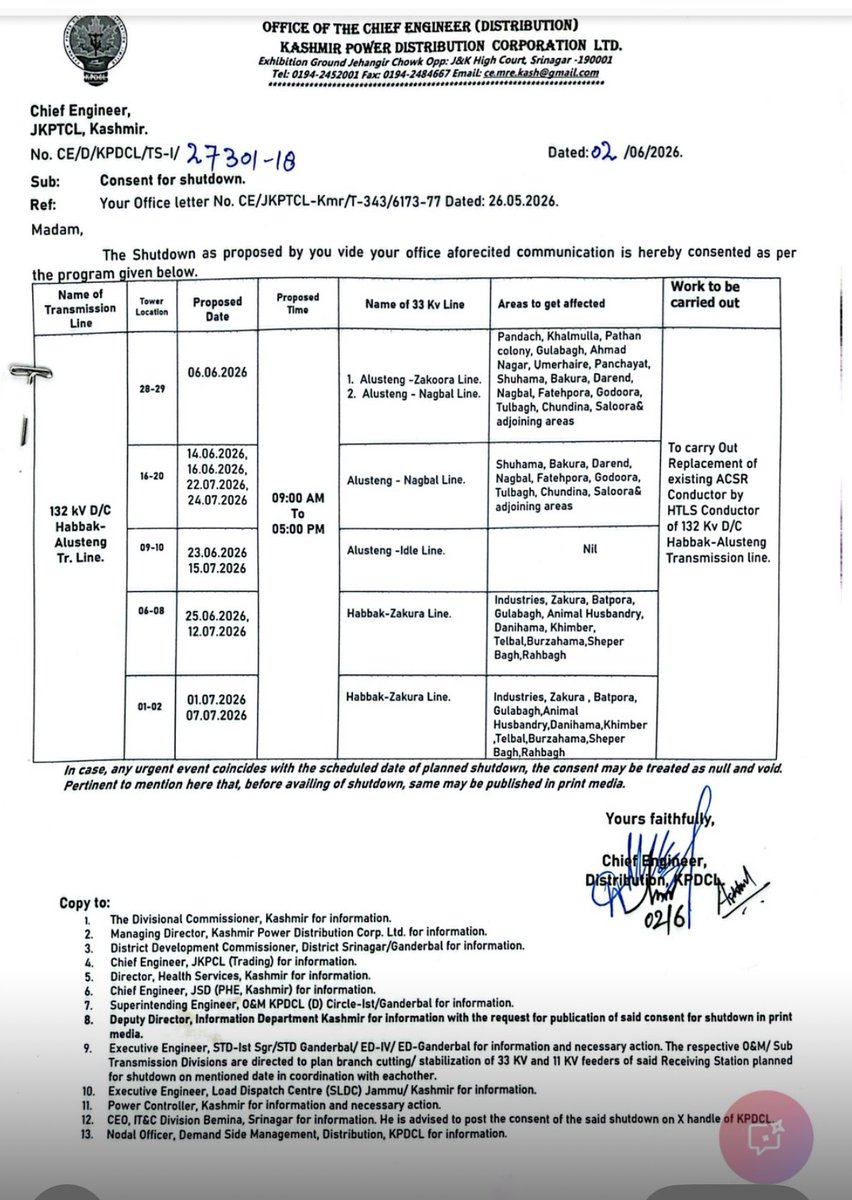

Public Notice | Power Shutdown

In order to facilitate the replacement of the existing ACSR conductor with HTLS conductor on the 132 kV D/C Habbak–Alusteng Transmission Line, a scheduled shutdown has been approved by the competent authority.

#PowerShutdown #InfrastructureUpgrade

2

1

107

May 28

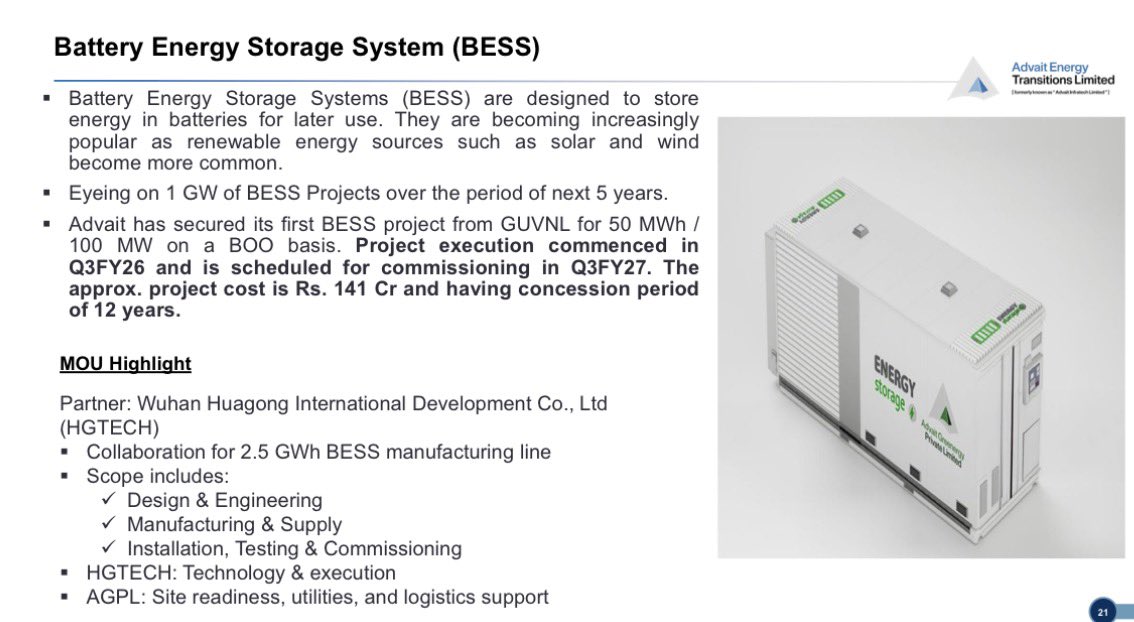

𝗔𝗗𝗩𝗔𝗜𝗧 𝗘𝗡𝗘𝗥𝗚𝗬 𝗧𝗥𝗔𝗡𝗦𝗜𝗧𝗜𝗢𝗡𝗦 𝗟𝗧𝗗

𝗤𝟰𝗙𝗬𝟮𝟲 & 𝗙𝗬𝟮𝟲 | 𝗙𝘂𝗻𝗱𝗮𝗺𝗲𝗻𝘁𝗮𝗹 𝗗𝗲𝗰𝗼𝗱𝗲

The rebrand from "Advait Infratech" to "Advait Energy Transitions" is not cosmetic. The numbers explain the pivot.

𝗙𝗬𝟮𝟲 𝗖𝗢𝗡𝗦𝗢𝗟𝗜𝗗𝗔𝗧𝗘𝗗

Revenue: ₹715 Cr ( 𝟴𝟬% 𝗬𝗼𝗬)

EBITDA: ₹84 Cr ( 64%) | Margin 11.73% (vs 12.87%)

PAT: ₹58 Cr ( 𝟳𝟱%) | Margin 7.71%

RoCE 30% | RoE 23%

𝗤𝟰𝗙𝗬𝟮𝟲 𝗖𝗢𝗡𝗦𝗢𝗟𝗜𝗗𝗔𝗧𝗘𝗗

Revenue: ₹228 Cr ( 18% YoY)

EBITDA: ₹29 Cr ( 49%) | Margin 12.61% (vs 9.97%)

PAT: ₹20 Cr ( 55%)

𝗢𝗥𝗗𝗘𝗥 𝗕𝗢𝗢𝗞 — 𝗧𝗛𝗘 𝗥𝗘𝗔𝗟 𝗦𝗧𝗢𝗥𝗬

₹1,304 Cr | 𝟭𝟱𝟵% 𝗬𝗼𝗬 | 107% 4-Yr CAGR

Mix: PTS 64% | NRE 36%

~1.8x cover on FY26 consolidated revenue, strong FY27 visibility

𝗜𝗡𝗦𝗜𝗗𝗘 𝗧𝗛𝗘 𝗥𝗘𝗩𝗘𝗡𝗨𝗘 𝗠𝗜𝗫

𝗣𝗧𝗦 (𝗹𝗲𝗴𝗮𝗰𝘆 𝗰𝗼𝗿𝗲)

Power DISCOM EPC: ₹223 Cr, 50% of standalone, 145% YoY (the engine)

Stringing Tools: ₹74 Cr ( 54%)

ACS-OPGW: ₹26 Cr ( 43%)

OPGW Liveline: -38% YoY

𝗡𝗥𝗘 (𝘁𝗵𝗲 𝘁𝗿𝗮𝗻𝘀𝗶𝘁𝗶𝗼𝗻 𝗯𝗲𝘁)

AGPL Solar EPC: ₹212 Cr ( 121%)

BESS EPC: ₹49 Cr ( 100%)

First BESS asset: 50 MWh / 100 MW GUVNL BOO, ₹141 Cr, 12-yr concession

𝗖𝗔𝗣𝗘𝗫 𝗖𝗬𝗖𝗟𝗘 𝗜𝗦 𝗟𝗜𝗩𝗘

CWIP: ₹1.78 Cr to ₹53 Cr

Gangad / Dholera facility (HTLS conductors, tools, ERS) commissioning by Q4FY27

30 MW electrolyser line FAT completed, scalable to 300 MW

2.5 GWh BESS line MoU with HGTECH (Wuhan)

𝗢𝗣𝗧𝗜𝗢𝗡𝗔𝗟𝗜𝗧𝗬 𝗦𝗧𝗔𝗖𝗞 — 𝗜𝗘𝗪 𝟮𝟬𝟮𝟲 𝗠𝗼𝗨𝘀

Power to Hydrogen (AEM electrolysers)

VJ Industries (hydrogen storage)

CENMAT (PEM / AEM systems)

Carbon credits / I-RECs: 1,200 MW pipeline, 5 Mn credits under issuance (₹35 Cr lifetime revenue)

𝗪𝗔𝗧𝗖𝗛𝗣𝗢𝗜𝗡𝗧𝗦

𝟭. 𝗠𝗮𝗿𝗴𝗶𝗻 𝗱𝗶𝗹𝘂𝘁𝗶𝗼𝗻 — Consol EBITDA margin slipped 12.87% to 11.73% as low-margin AGPL Solar EPC (~5%) scales; standalone still holds 15.78%

𝟮. 𝗪𝗼𝗿𝗸𝗶𝗻𝗴 𝗰𝗮𝗽𝗶𝘁𝗮𝗹 𝘀𝘁𝗿𝗲𝘁𝗰𝗵 — Receivables ₹78 Cr to ₹131 Cr; Payables ₹61 Cr to ₹131 Cr

𝟯. 𝗗𝗲𝗯𝘁 𝘂𝗽 — ₹46 Cr to ₹121 Cr (D/E 0.46x), but still 𝗻𝗲𝘁 𝗰𝗮𝘀𝗵 (-₹4.4 Cr)

𝟰. 𝗖𝗼𝗻𝗰𝗲𝗻𝘁𝗿𝗮𝘁𝗶𝗼𝗻 — 50% of standalone revenue from DISCOM projects

𝟱. 𝗦𝘄𝗶𝗻𝗴 𝗳𝗮𝗰𝘁𝗼𝗿 — BESS commissioning (Q3FY27) and electrolyser order conversion decide whether margins rebuild

𝗖𝗢𝗡𝗧𝗘𝗫𝗧

Market cap ₹1,825 Cr (31 Mar 2026) | Migrated to NSE in Q4FY26

𝗧𝗛𝗘 𝗧𝗛𝗘𝗦𝗜𝗦

Advait is morphing from a PTS niche player into an integrated power and energy-transition platform. Order book and capex confirm intent. The next four quarters — margin trajectory and BESS / electrolyser execution — decide the re-rating.

Dis : Educational decode, not a recommendation.

10

25

3,140

Most people still think Diamond Power (DIACABS) is an old bankrupt cable company.

That may be the opportunity.

FY26:

• Revenue 71%

• EBITDA 243%

• PAT 355%

But the real story?

The company is operating at just ~25–30% utilisation while claiming installed revenue potential of ₹14,000 Cr.

This is no longer a commodity cable business.

DIACABS is positioning itself around:

⚡ EHV cables

⚡ HTLS conductors

⚡ Renewable infra

⚡ Data centres

⚡ Grid modernisation

⚡ Premium transmission products

And the numbers are starting to reflect it:

• EBITDA margin: 6.1% → 12.1%

• Gross margin: 15.7% → 19.9%

What’s interesting:

→ 400kV EHV capability

→ 700kV NABL lab

→ Rod-to-cable integration

→ TS Conductor partnership

→ Exposure to India’s power capex supercycle

But this is NOT a “sleep peacefully” stock.

Risks remain:

• Rising finance costs

• Working capital intensity

• Execution risk

• NCLT baggage

• Balance sheet monitoring

This is the kind of stock that can either:

→ become a serious infra manufacturing platform

OR

→ disappoint badly if scaling breaks.

The next 8 quarters will decide everything.

One of the most fascinating industrial turnaround stories in India right now.

1

5

37

4,912

May 24

$ETH continues to show major weakness and cannot hold any meaningful level.

Compared to the broader market and even $BTC it keeps underperforming which only makes the situation look worse.

Lower prices still look very likely from here with the first major target being the HTLs.

May 24

$ETH is struggling right now.

I expect us to head lower from here.

Don’t underestimate how brutal a bear market can be.

1

1

4

340