That’s a wrap on #ACVIM2026.

Thank you to everyone who stopped by the HawkCell booth in Seattle.

You can now test our HawkAI deep learning algorithm directly on your own DICOM MRI images.

👉🏻 Try it and upload your own scans: demo.hawkcell.com/

2

3

5

Stop imagining what your MRI could look like. See it, on your own scans, in minutes.

HawkAI turns noisy scans sharper, in your inbox, nothing to install. Your scan, your proof.

→ Sharper images

→ 2x faster scans

→ Less anesthesia

👉🏻Try it now: demo.hawkcell.com

2

3

5

May 27

A SaaS-led platform generating 2–3 lakh alerts daily, with most resolved in real time. Rajiv Kaul shares how HAWKAI™ is helping curb yank-and-go robberies through AI and on-ground execution.

Watch the full CORE podcast here: bit.ly/4uPstuq

#CMSInfoSystems

2

66

📣 #ACVIM2026

#HawkAI brings animal anatomy into veterinary MRI performance.

June 11–12 in Seattle, meet HawkCell at Booth 1319 and see how non-diagnostic, anatomy-aware AI supports sharper images, faster scans, and real clinical workflows.

👉🏻 Book now: meetings-eu1.hubspot.com/sbu…

2

3

34

May 15

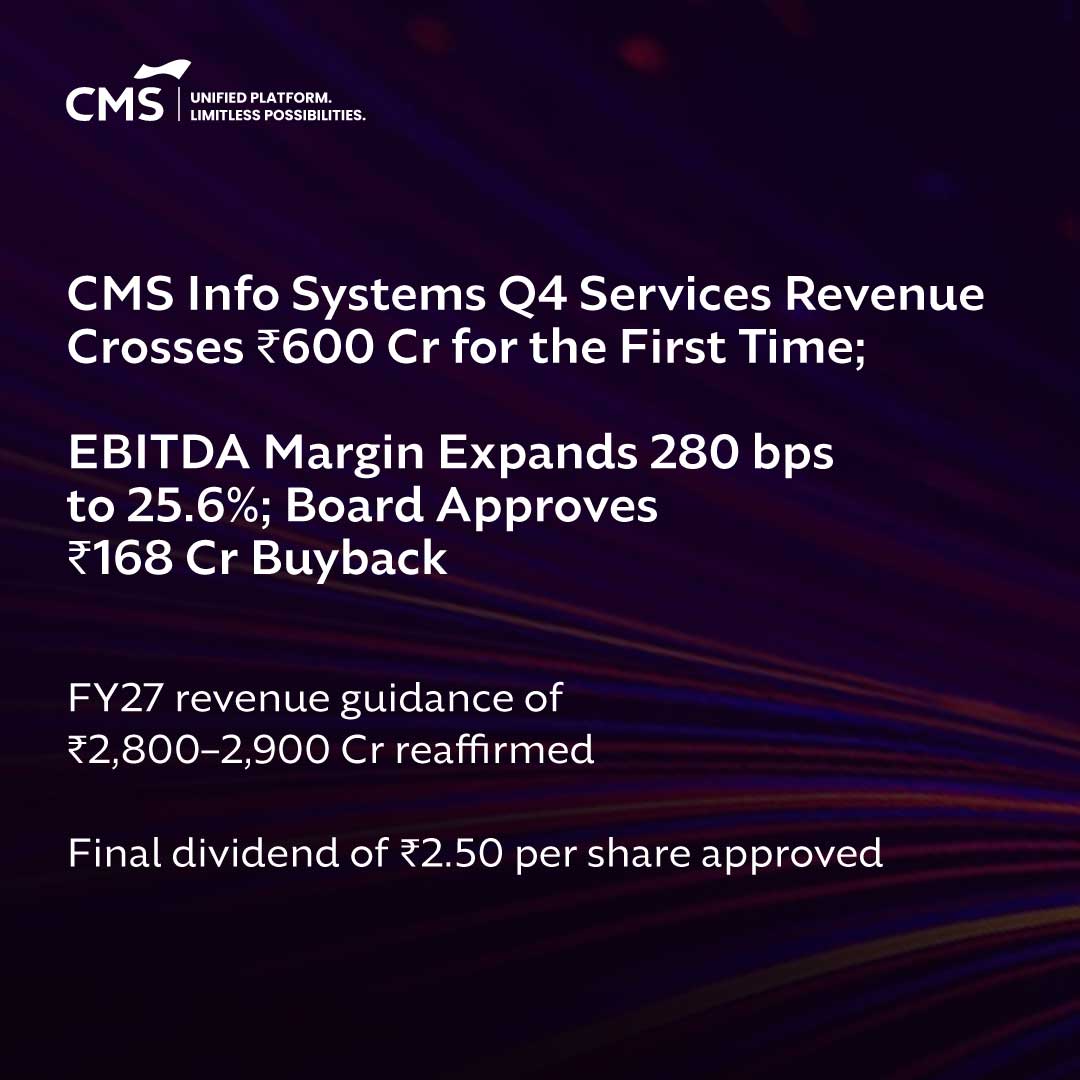

Q4 FY26 marked a strong turnaround with services revenue crossing ₹600 Cr, EBITDA margins expanding to 25.6%, and PAT surging 38% QoQ. Backed by acquisitions & HAWKAI™ scaling at 50,000 sites, FY27 guidance remains strong.

Read more: bit.ly/4fi8mjO

2

152

CMS Info Systems – Q4 FY26 Summary

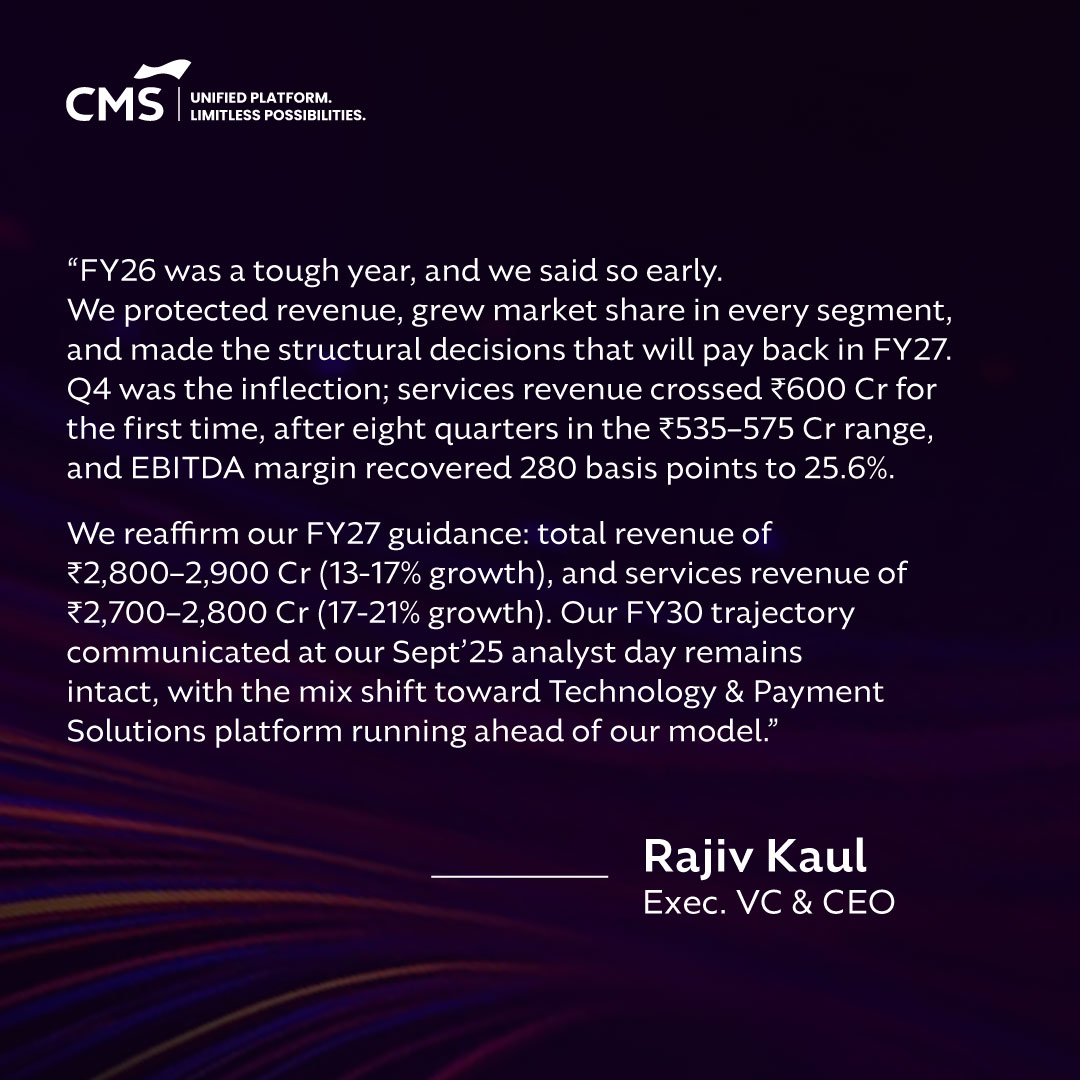

CMS Info Systems showed a good recovery in Q4 FY26 after a difficult year. Management said the business had “bottomed out” in Q3 and improved sharply in Q4 due to better execution, large contract rollouts, and improved efficiency.

Key Q4 FY26 Highlights

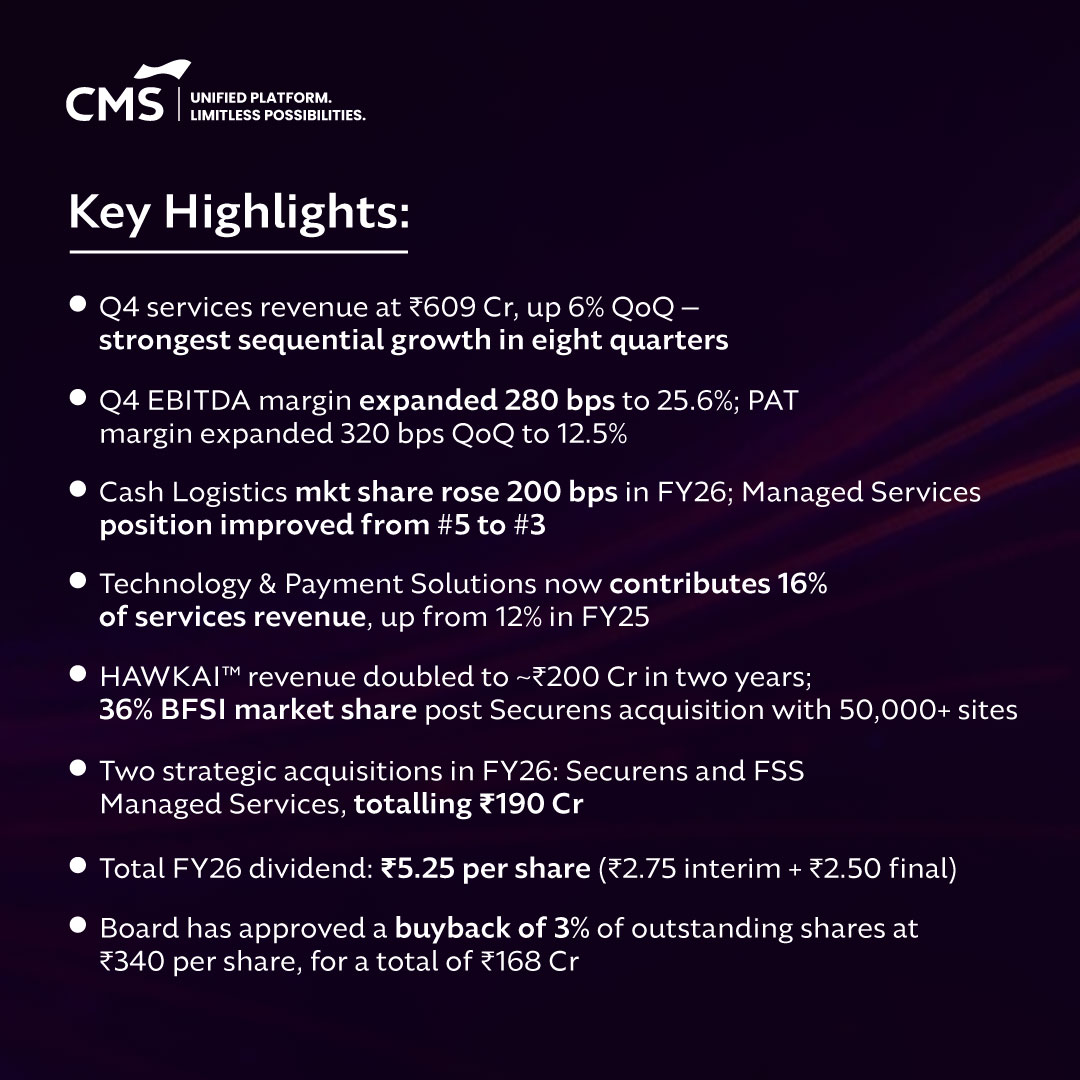

Services revenue reached ₹609 crore, up 6% quarter-on-quarter, crossing ₹600 crore for the first time.

EBITDA increased to ₹162 crore, growing 15% QoQ.

EBITDA margin improved significantly to 25.6%, up 280 basis points from Q3.

Profit after tax (PAT) rose to ₹79 crore, a strong 38% sequential increase.

What Drove the Recovery?

Full execution of the large ₹1,000 crore SBI contract, including ₹500 crore incremental business.

Strong progress in the ₹400 crore ICICI Bank contract, now 90% operational.

Better operational efficiency and recovery in services demand.

Business Segment Updates

ATM & Cash Management

ATM management business has doubled over the last five years.

Retail cash management market share increased to 38%.

The company’s gig delivery model now has 2,500 partners and handles 20% of retail touchpoints, improving flexibility and efficiency.

Technology & Payment Solutions (T&PS)

T&PS business continued strong growth with 25% CAGR and reached ₹370 crore revenue in FY26.

HAWKAI now monitors 50,000 sites and has an annual revenue run rate of around ₹200 crore.

ALGO MVS manages 68,000 machines and has around 40% market share in the SBI network.

FY26 Overall Performance

Even though Q4 improved strongly, the full year remained challenging due to slower consumption, delays in the SBI contract, and disruptions from competitor exits.

FY26 services revenue: ₹2,312 crore ( 6% YoY)

EBITDA: ₹600 crore (down 5% YoY)

EBITDA margin: 24.1%

The company also reduced dependence on SBI. Now, 52% of revenue comes from private banks, other PSU banks, and retail customers.

Acquisitions & Shareholder Returns

CMS used its debt-free balance sheet to strengthen its market position:

Acquired Securens for ₹75 crore to expand its Vision AI leadership.

Acquired FSS Managed Services for ₹115 crore to deepen banking relationships.

Announced a ₹168 crore buyback at ₹340/share.

Total dividends since IPO now stand at ₹438 crore.

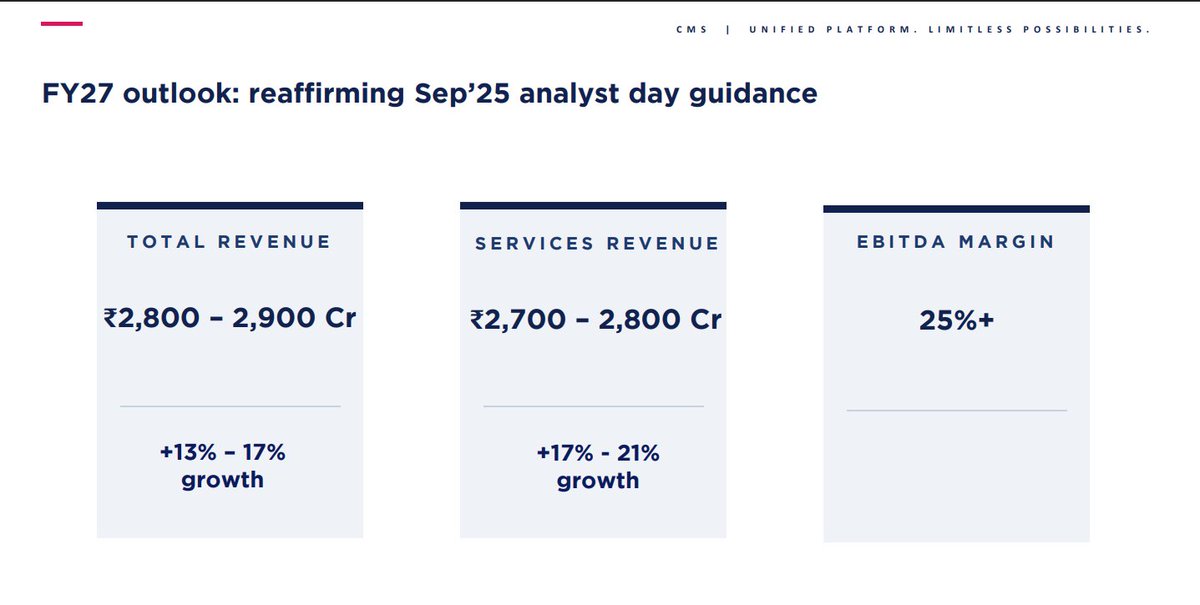

FY27 Outlook

Management remains optimistic for FY27 because of a strong order book of over ₹2,000 crore.

Guidance for FY27:

Total revenue target: ₹2,800–2,900 crore

Services revenue growth: 17%–21%

EBITDA margins expected to return above 25%

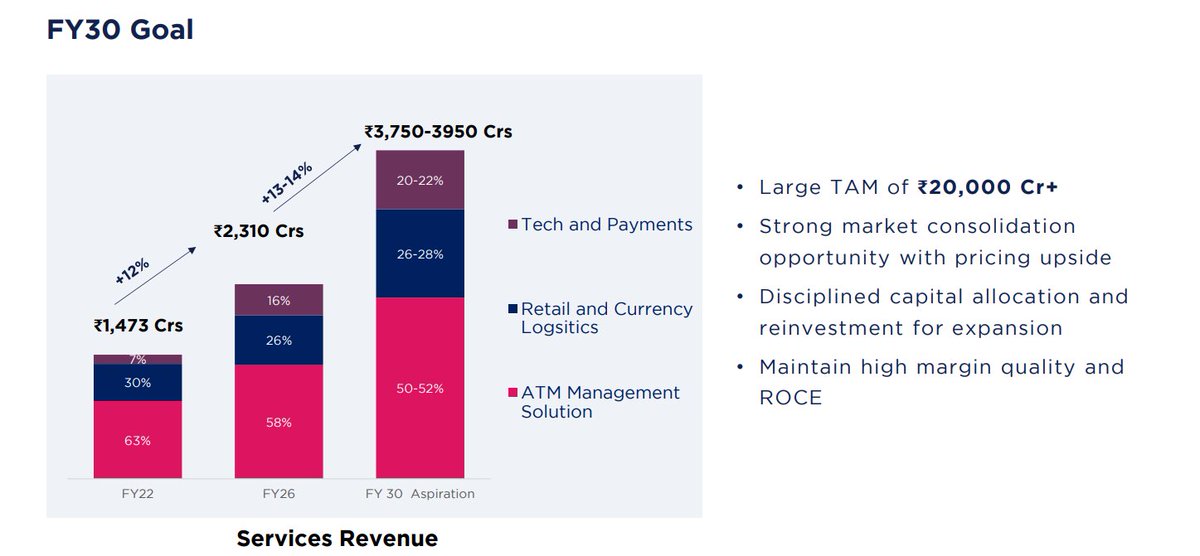

Long-Term FY30 Goal

By FY30, CMS aims to achieve:

Services revenue of ₹3,750–3,950 crore

Technology & Payment Solutions contributing 20%–22% of total services revenue.

#CMSinfosysytems #Q4FY26earnings #Cashlogistics

1

14

961

May 14

📈 CMS Info Systems: Key Business Updates & Forward Guidance | MCap 4,902.1 Cr

• Secured SBI contract worth ₹500 crore and ICICI Bank contract worth ₹400 crore

• Pipeline of over ₹2,000 crore in ATM Management Solutions

• HAWKAI Vision AI platform expanded to 50,000 sites

• Gig delivery model scaled to 2,500 partners

• FY27 total revenue guidance: ₹2,800–2,900 crore

• FY27 services revenue guidance: ₹2,700–2,800 crore

• EBITDA margin trending above 25%

• Long-term services revenue CAGR target: 13–14%

• FY30 revenue target: ₹3,750–3,950 crore

• FY26 services revenue: ₹2,312 crore (6% growth)

• Q4FY26 services revenue exceeded ₹600 crore

• T&PS revenue reached ₹370 crore (16% of services revenue)

• HAWKAI Vision AI revenue doubled in two years to ~₹200 crore

• FY26 EBITDA margin: 24.1% (down from 26.1% in FY25)

• Q4FY26 EBITDA margin improved 280 basis points to 25.6%

Disc: Information provided in this tweet can be inaccurate, verify through the source in reply before making any investment decision.

Preview 👇 (First 4 out of 30 pages)

2

2

253

May 11

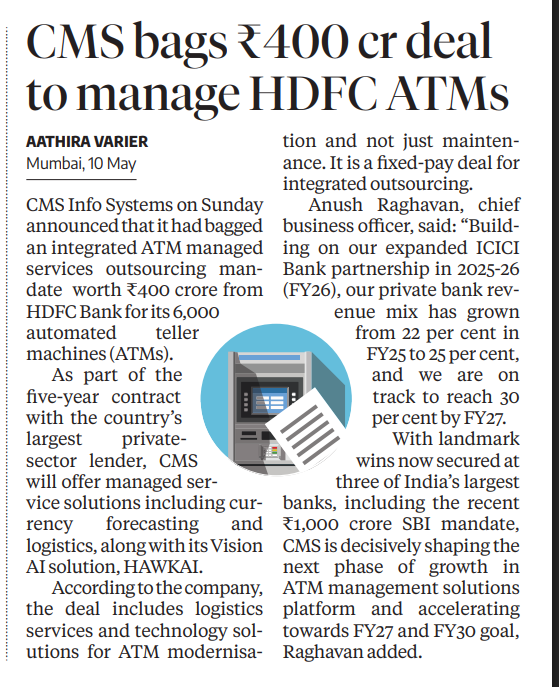

CMS Wins ₹400 Cr HDFC Bank ATM Outsourcing Deal

CMS Info Systems bags a ₹400 crore integrated ATM management contract from HDFC Bank

Deal covers 6,000 ATMs under a five-year agreement

Services include currency forecasting, cash logistics, ATM modernization, and AI-based monitoring (HAWKAI)

Contract strengthens CMS’s presence in the private banking segment

Private bank revenue mix expected to rise from 22% in FY25 to 30% by FY27

CMS now manages mandates from three major banks, including recent SBI and HDFC deals

Move positions the company for accelerated growth in ATM outsourcing and managed banking services

7

1,318

CMS Info Systems wins ₹400 Cr ATM Managed Services mandate from HDFC Bank

CMS Info Systems has secured a 5-year integrated ATM Managed Services outsourcing mandate from HDFC Bank, India’s largest private sector bank. The order is valued at approximately ₹400 crore and covers the management of 6,000 ATMs across the country.

Under the mandate, CMS will provide end-to-end managed service solutions including currency forecasting, cash logistics, and deployment of its Vision AI-powered platform, HAWKAI™.

Commenting on the development, Anush Raghavan, Chief Business Officer, said:

"This HDFC mandate is a powerful endorsement of the CMS platform — our technology, pan-India scale, and consistent execution on uptime and compliance. Building on our expanded ICICI Bank partnership in FY26, our private bank revenue mix has grown from 22% in FY25 to 25%, and we are on track to reach 30% by FY27. With landmark wins now secured at three of India’s largest banks, including our recent ₹1,000 Cr SBI mandate, CMS is decisively shaping the next phase of growth in ATM Management Solutions and accelerating towards its FY27 and FY30 goals."

The deal further strengthens CMS Info Systems’ position in India’s ATM managed services space and adds momentum to its long-term growth strategy focused on technology-led banking infrastructure solutions.

PPFAS raising stake in CMS Info Systems from ~3.65% (Dec’25) to ~8% (Mar’26).

Are they positioning for consolidation after AGS Transact Technologies collapse, the same way they played Bharti Airtel post Reliance Jio disruption?

@PPFAS @RajeevThakkar @EquityValueIn

What AGS fall means for the industry, business model, moats & key touchpoints 👇

theloggicalinvestor.substack…

2

15

2,067

May 10

CMS Info Systems has announced a major new win: a 5-year integrated ATM managed services outsourcing mandate from HDFC Bank.

What will CMS do?

- Currency forecasting

- Cash logistics

- AI monitoring with HAWKAI

Why is this huge?

Because banks only scale with partners that can deliver reliably.

CMS is strengthening its ATM management business and pushing hard toward FY27 and FY30 expansion goals.

CMS is becoming a serious backbone for India’s banking operations.

Source: company press release

5

11

50

6,668

May 10

CMS Info Systems Limited has secured a significant 5-year integrated ATM managed services outsourcing mandate from HDFC Bank. 🤝

This contract, valued at ₹400 Cr, covers the management of 6,000 ATMs and includes services such as currency forecasting, logistics, and the deployment of their Vision AI solution, HAWKAI™.

Key Highlights:

- 𝗖𝗼𝗻𝘁𝗿𝗮𝗰𝘁 𝗩𝗮𝗹𝘂𝗲 & 𝗗𝘂𝗿𝗮𝘁𝗶𝗼𝗻: ₹400 Cr over 5 years. 💰

- 𝗦𝗰𝗼𝗽𝗲: Managed services for 6,000 ATMs, including currency management & AI solutions.

- 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗜𝗺𝗽𝗮𝗰𝘁: This win is a strong endorsement of CMS's platform, technology, and operational capabilities. It follows recent large mandates, including one with SBI, further solidifying CMS's leadership in ATM management.

- 𝗥𝗲𝘃𝗲𝗻𝘂𝗲 𝗚𝗿𝗼𝘄𝘁𝗵: The company expects this mandate to contribute to its target of increasing the private bank revenue mix from 25% in FY25 to 30% by FY27. 📈

- 𝗠𝗮𝗿𝗸𝗲𝘁 𝗣𝗼𝘀𝗶𝘁𝗶𝗼𝗻: CMS is a leading integrated business services company in India, serving banks, financial institutions, and retail sectors with a pan-India network & advanced technology solutions. 🇮🇳

📊 CMS INFO SYSTEMS LTD | 🏷️ Press Release / Media Release

🌐 Details: wegro.app/RO2R6g

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/go

1

2

287

The CMS opportunity is about execution and structural optionality, not just multiple expansion.

Bear scenario: small upside (~6–10%) if recovery disappoints.

Base scenario: solid recovery (~70%) with normalization of revenue and margins.

Bull scenario: strong execution could more than double the stock, reflecting faster ATM ramp and HAWKAI growth.

FY28 upside: full optionality could push returns to ~2.5X-3X current market cap, showing how structural tailwinds compound over time.

Note : Good returns can be generated by earnings growth and Multiple expansion. If market continues to value CMS as their legacy business the return expectations from stock can be significantly dropped from 25-30 % CAGR ( earnings Multiple expansion) to 15-18% ( only earnings growth) over next few years. Optionality from AI and tech related business improving to larger mix can drive this shift , But when it will happen — is the real question ?

2

502

Valuation Analysis of CMS Infosystem Ltd — EV/EBITDA Method

Part 2 is now live. 👇theloggicalinvestor.substack…

CMS is a blended business — part cash logistics, part managed services, and a growing tech layer through HAWKAI.

So the valuation multiple should reflect this mix.

You cannot apply a high tech multiple to the entire company just because one segment is growing fast.

If you look at history, the range is quite clear.

After IPO, the stock traded at around 13X–15X EV/EBITDA due to High market share and premium positioning.

During a strong earnings cycle in FY24, it stayed in the 12X–14X range as growth and margins were both strong. In a normal, stable period, the stock has typically traded at 10X–12X.

Right now, in FY26, it is in a trough at around 6X-7X because of margin pressure, delayed RFPs, and AGS-related disruption.

Why the multiple cannot go beyond ~14x-16x ?

The core of CMS is still cash logistics, which contributes roughly 50–55% of revenue.

This is not a high-growth business. It grows at around 8–10%, is capital-intensive, and operationally heavy. Even if HAWKAI grows at 30% CAGR, it will still be only around 12–15% of total revenue by FY27. So the company will continue to be valued as a blended business.

A pure-play HAWKAI-type business might deserve 25x–30x, but CMS is not that. The market will not value the entire company based on its best segment. For a higher multiple to sustain, HAWKAI needs to become a much larger part of the business, closer to 25–30% of revenue, with clear margin contribution.

Till then, ~14x-16x is a reasonable upper limit even in a strong bull case.

6

761

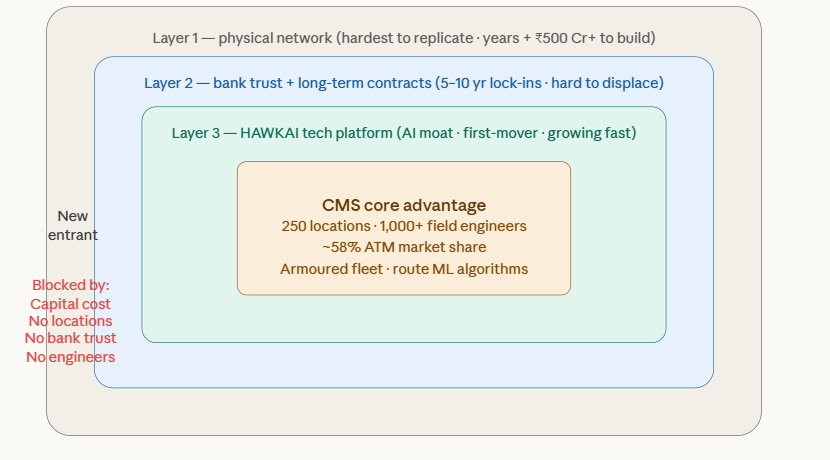

If CMS is making solid money, why isn’t everyone doing the same thing ?

This is the most important question for any investor. If CMS is making good money, why can’t someone else just copy the same model?

The simple answer is that the barriers here are physical, not digital. You can build software from a small room. But you cannot build a nationwide ATM network like this from scratch so easily.

The moat works in three layers.

1. The first layer is physical infrastructure. CMS has around 250 branches across India, thousands of armoured vehicles, trained staff, and more than 1,000 field engineers. They can reach and service ATMs almost anywhere in the country. Building this kind of network takes years and a lot of money. It’s not something a new company can set up quickly.

2. The second layer is trust and contracts. Banks don’t just hand over ATM operations to a new player. This is a highly sensitive business involving large amounts of cash every day. CMS has been working with major banks for over 20 years. It already has long-term contracts in place. Switching to a new vendor is not easy and comes with risk and cost.

3. The third layer is technology. CMS has built its own platform called HAWKAI. It is used to monitor operations across thousands of locations. Over time, it keeps collecting data on how systems normally behave. This creates an advantage because the system keeps improving with more data, and new players won’t have that history.

( Read the CMS infosystems deep dive

theloggicalinvestor.substack… )

So overall, the advantage is not just one thing. It is a combination of physical network, long-term relationships, and built-up data over time. That’s what makes it hard to replicate.

6

1

9

1,903

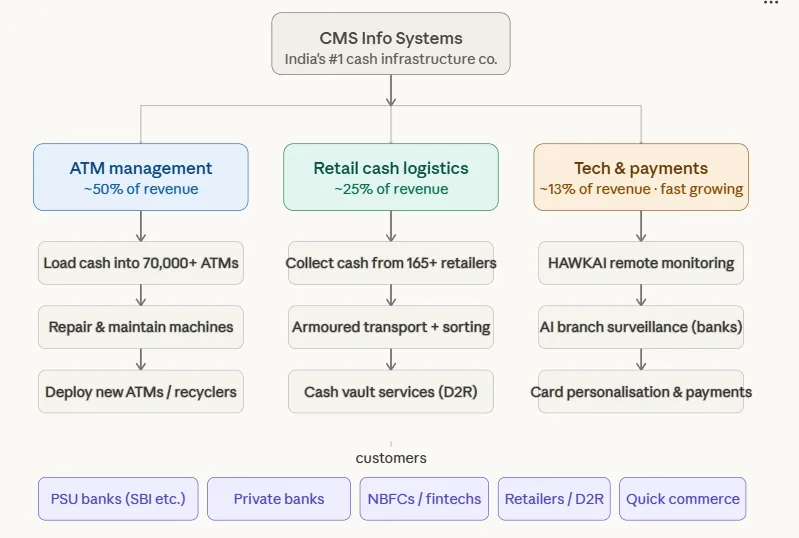

What does CMS Info systems actually do?

Imagine India has about 260,000 ATMs. Every single one of those machines needs cash loaded into it regularly. Someone has to drive to it in an armoured vehicle, count the cash, load it in, fix it if it breaks, and make sure it’s running 24/7.

Banks don’t want to do this themselves — it’s expensive, operationally complex, and not their core business. So they outsource it. CMS Info Systems is the largest company in India that does this outsourcing.

But that’s only the beginning of what they do. More details in below snapshot

Platform 1 : ATM Management

Think of this like a maintenance and fuelling contract for a fleet of machines. A bank owns 10,000 ATMs spread across India. They don’t want to hire 2,000 people to drive around loading cash and fixing broken machines.

So they call CMS and say: “Here’s our ATM network. You run it. We’ll pay you a fixed monthly fee per machine.”

CMS then deploys its fleet of armoured vehicles, its 1,000 field engineers, and its route-optimisation software to keep every single machine running at 95–98% uptime.

Platform 2 : Retail Cash Logistics

When a supermarket, jewellery store, or petrol pump collects cash from customers all day, that cash is sitting in a drawer doing nothing. It’s also a security risk.

CMS comes to the store, counts the cash, picks it up in an armoured vehicle, and either deposits it in the bank or stores it securely.

Think of it like a courier service — but for cash, with armoured vans. This segment is newer (CMS only had zero retail clients 2.5 years ago, now it has 165 clients ) and is the fastest expanding on the logistics side.

Platform 3: HAWKAI — The tech bet

This is the youngest and most exciting part of the business. HAWKAI is CMS’s AI-powered remote monitoring platform. A bank with 2,000 branches can’t station a guard at every entrance 24/7 — it’s too expensive.

Instead, CMS installs cameras, sensors, and software that watches everything in real time using AI. If something looks suspicious, an alert fires. The bank pays CMS a monthly subscription.

1

28

4,552

Apr 12

Stock to Study : CMS Info Systems Ltd (CMSINFO)

Company Snapshot

CMS Info Systems Ltd is India's leading cash management and business services company, specializing in cash logistics (ATM cash replenishment, retail cash pick-up), managed services, and technology solutions (including AI-driven platforms like HAWKAI). It serves banks, financial institutions, organized retail, and e-commerce, with dominance in ATM cash management and growing tech/payments segment. Strong moat from integrated network, long-term contracts, and scale.

Guidance & Outlook from Q3 FY26 Concall (Feb 2026)

Management commentary resilient and confident despite volatile FY26; Q3 viewed as bottom with strong recovery expected:

- FY27 Revenue Guidance: ₹2,800–2,900 Cr (focus on services revenue ~₹2,700–2,800 Cr).

- EBITDA Margin Target: 25–26% (recovery via operating leverage, network optimization, cost controls).

- Order Book: ~₹4,400 Cr (significant growth; includes ₹1,000 Cr SBI win over 10 years → incremental ₹500 Cr revenue; ICICI & India Post deals ~75% live; ₹750 Cr from two key customers).

- Key Drivers: Large long-duration wins (SBI/ICICI ₹1,500 Cr ), tech investments for productivity (dynamic routing, gig model), ATM yield improvement (5% by Mar'26), route reduction (10%).

- Q4 FY26: Strong QoQ gains expected from execution ramp and quality revenue improvement.

- Medium-term: Bottomed out in Q3; confident in profitable growth trajectory; one-time wage code impact absorbed; business transfer/acquisition (₹100–125 Cr) in managed services; cash-flow strong, low debt.

Valuation Analysis & Projections

FY26 Estimates (conservative, based on 9M Q4 momentum):

- Revenue: ~₹2,450–2,500 Cr (modest growth amid challenges).

- EBITDA: ~₹600 Cr (margin ~24–25%).

- PAT: ~₹220–240 Cr (implied EPS ~₹13–14).

Implied Multiples at ~₹284 (as of 20 Mar 2026):

- TTM P/E: ~14–15x (PAT impacted by one-offs/margins).

- EV/EBITDA: ~10–11x.

- EV/Sales: ~2x.

FY27 (at ₹2,800–2,900 Cr rev): Lower multiples with margin recovery; order-book-to-MCap ratio ~0.9–1x (strong visibility from long-term contracts). Compared to cash management/logistics peers (often 18–25x P/E on lower growth), CMS trades at discount despite annuity-like revenues and moat. Analyst models (DCF/peer) point to ₹360–416 range (consensus ~₹389).

Key Positives

- Market leadership in cash logistics growing tech/managed services.

- Massive long-duration order wins (SBI ₹1,000 Cr, ICICI) execution ramp.

- Margin recovery path (25–26% FY27) via optimization and leverage.

- Attractive dividend (₹2.75 interim declared); low debt, strong cash flows.

Key Risks (mitigated but monitor)

- Wage inflation, industry pressures, macro volatility impacting short-term margins/growth.

- Dependency on banking sector outsourcing cycles.

- Execution risks in large contracts and network changes.

- One-time costs (wage code, investments) in transition phase.

Longer-term: Large wins tech edge ATM/managed services outsourcing trend will drive sustainable 12–15% CAGR in revenue and higher earnings growth post-FY26. Position size accordingly; suitable for value growth portfolios. Monitor Q4 FY26 results, order execution, and margin trajectory closely.

Stock Valuation and Projected Price Target :

At current valuations (~₹272), CMS offers compelling risk-reward for a defensive, high-moat cash management leader. The combination of strong order book visibility, FY27 guidance reaffirmation, margin recovery to 25–26%, and annuity-like long-term contracts justifies a re-rating toward 18–22x forward P/E (target price ₹360–420 over 12–18 months, 27–48% upside; analyst consensus ~₹389 implies ~37% potential).

1

2

17

2,011

#HawkAI is redefining veterinary imaging performance.

Trained exclusively on animal data, it enables faster acquisitions, lower anesthesia time, higher SNR, better workflow control and optimized ROI.

👉🏻 Try it on your own images and see the difference: lnkd.in/dPNfkZYq

2

3

20

Apr 5

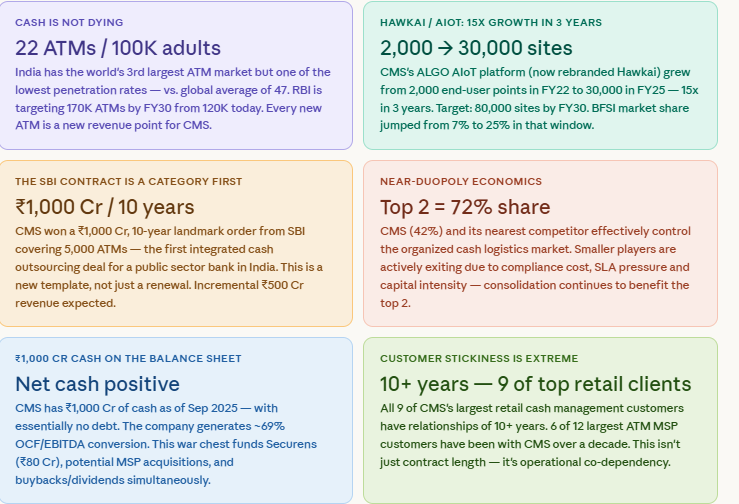

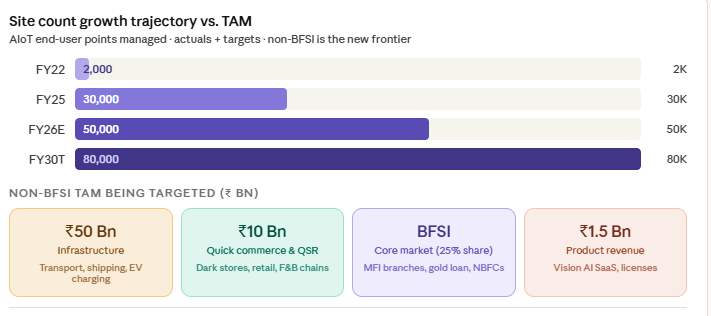

CMS info , some interesting data points and understanding the optionality with HAWKAI, very interesting what they are doing here for incremental optionality

4

36

2,749

Mar 29

CMS Info acquires FSS ATM business for ₹115 Cr! 🚀💳

• Adds 8,000 ATMs, total managed services → 39,000 units

• New private sector bank relationships onboarded

• Aligns with 2030 consolidation strategy (Analyst Day '25)

• HAWKAI monitoring ALGO software cross-sell potential

🟢 Positive: ATM platform scale-up synergies

#CMSInfo #ATMInfra #CashLogistics #FSSAcquisition

1

1

290