Jun 12

You could turn this into a computer board and have the first hypercomputer.

1,575

Jun 11

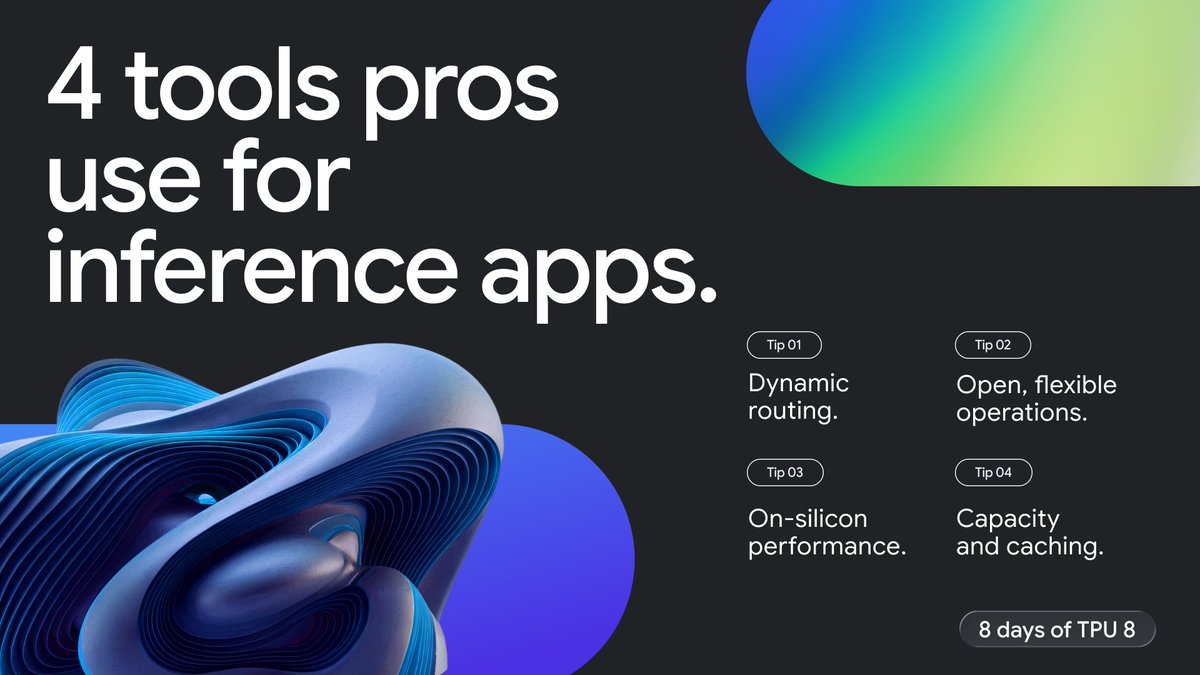

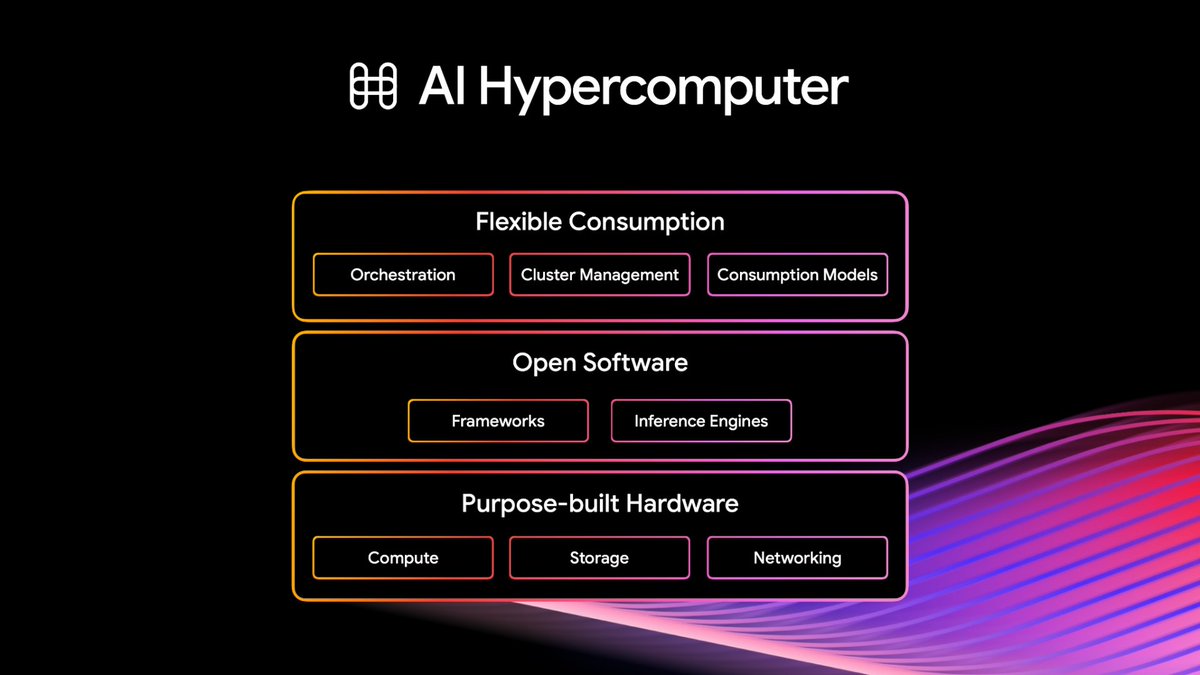

For day 4 of #8daysofTPU8, here are 4 tools that pros use to build efficient, reliable inference apps on TPUs.

See the reference architecture on our AI Hypercomputer page here → goo.gle/49StNEF

1

9

47

3,104

Jun 4

#GoogleCloudSummitFrance

live from Paris - Plenary session

@GoogleCloud_FR @Google

#AI Hypercomputer: Software, Hardware, Energy

#DataCenter

--

Cc @jblefevre60 @SpirosMargaris @Ym78200 @kalydeoo @mvollmer1 @Fabriziobustama @enricomolinari @sallyeaves @HeinzVHoenen @efipm @RLDI_Lamy @dinisguarda @mallys_ @Nad_Alves

1

9

13

275

if you think the brain is a hypercomputer and can't be fully modeled by the Church-Turing thesis, then you should prove it by building a hypercomputer and breaking all global encryption. go on, i'll wait.

10 Sep 2025

i think that anyone proposing that brains are doing hypercomputation should have to actually sit and think for 10 minutes about just what it would mean for human wetware to be implementing a solution to the halting problem to run you playing angry birds on your iphone.

9

9

103

4,849

May 19

$GOOGL $BX EXECUTIVE OVERVIEW

Google’s TPU cloud joint venture with Blackstone is strategically more important than the headline $5 billion equity commitment implies. The transaction represents an attempt to convert Google’s proprietary AI accelerator platform from a largely internal and Google Cloud-consumed asset into a separately financed, scaled, 3rd-party compute platform. The official Blackstone announcement confirms a U.S.-based company offering data center capacity, operations, networking, and Google Cloud TPUs as compute-as-a-service, with Blackstone committing $5 billion of equity capital and targeting 500 MW of capacity online in 2027. Google will supply the TPUs, software, and services, while Blackstone will provide capital formation, digital infrastructure execution, and ownership control. (Blackstone)

The transaction should be viewed as a 3-part strategic development: 1st, it is a capital-light expansion channel for Google’s AI infrastructure stack at a time when internal and external AI compute demand is exceeding even hyperscaler-scale balance sheets; 2nd, it is a direct competitive response to Nvidia-backed neoclouds such as CoreWeave and Nebius, but with a differentiated hardware architecture built around TPUs rather than Nvidia GPUs; 3rd, it further institutionalizes AI compute as an infrastructure asset class, where long-duration contracts, power access, accelerated depreciation, asset-backed leverage, and private capital formation may become as important as chip availability.

TRANSACTION ECONOMICS AND STRUCTURAL READ-THROUGH

The Bloomberg-reported total investment value of $25 billion including leverage implies $50 million per MW on 500 MW of planned capacity, with the $5 billion equity commitment implying $10 million of equity per MW. This is materially above conventional shell-and-core data center construction benchmarks and indicates that the venture is not being underwritten as a simple wholesale colocation asset. JLL’s 2026 outlook estimates average global data center construction cost at $11.3 million per MW for shell and core, while AI infrastructure tech fit-out can cost as much as $25 million per MW. The $50 million per MW implied figure therefore appears consistent with a full AI compute stack that includes data center infrastructure, liquid cooling, networking, accelerators, power infrastructure, systems integration, and working capital rather than real estate alone. (JLL)

The capital structure is highly relevant. A $5 billion equity layer supporting a reportedly $25 billion total investment implies substantial leverage, likely secured by long-term capacity contracts, hardware collateral, site-level assets, or project-finance-style cash-flow arrangements. That model resembles the financing architecture already emerging in AI infrastructure, where compute capacity is increasingly monetized through multi-year commitments from hyperscalers, AI labs, financial institutions, and enterprise customers. The ability to lever the asset base depends on the credit quality and duration of contracted demand, the remarketability of TPU-based systems, the residual value of accelerators after each hardware cycle, and the extent to which Google provides contractual support, technology warranties, or customer commitments.

The revenue model is materially different from traditional data center leasing. CBRE reported a record average asking rate of roughly $196 per kW per month for 250 kW to 500 kW wholesale requirements in primary North American markets, which would annualize to approximately $1.18 billion on 500 MW if applied mechanically. That comparison is imperfect because 500 MW AI campuses are not comparable with small wholesale colocation blocks, but it is still instructive: real estate rent alone would not justify a $25 billion underwrite. The economic case must come from higher-value compute-as-a-service economics, TPU utilization, take-or-pay contracts, networking/service margins, and potentially premium performance-per-watt for Google-optimized workloads. (CBRE)

The structure also creates a plausible capital-efficiency benefit for Alphabet. Alphabet has already lifted 2026 capex guidance to $180 billion to $190 billion, with management citing unprecedented internal and external demand for AI compute resources. Google Cloud revenue grew 63% year over year to $20 billion in Q1 2026, Cloud operating income reached $6.6 billion, Cloud operating margin expanded to 32.9%, and backlog reached $462 billion, with demand for enterprise AI and TPU hardware sales contributing to backlog growth. A separately financed Blackstone vehicle can accelerate TPU availability without requiring every incremental MW to remain directly on Alphabet’s balance sheet. (Alphabet Investor Relations)

GOOGLE STRATEGIC RATIONALE

For Google, the transaction is a commercialization milestone for TPUs. Google has built TPUs for more than 10 years and has used them to power Gemini and other AI products, but TPU monetization has historically been mostly indirect through internal model development, Google services, and Google Cloud consumption. The venture expands the route to market by giving customers another option to access cloud TPUs outside standard Google Cloud procurement. This is important because some customers may want dedicated capacity, bespoke contracting, different financing terms, separate operational accountability, or capacity that is not constrained by Google Cloud’s own internal allocation priorities. (Google Cloud)

The strategic intent is to change TPUs from a proprietary cloud differentiator into a broader infrastructure platform. Google’s 8th-generation TPU architecture, TPU 8t for training and TPU 8i for inference and reinforcement learning, is explicitly designed around agentic AI workloads, power efficiency, and large-scale clusters. Google has disclosed that TPU 8t can scale to 9,600 chips in a superpod, deliver 121 exaflops, and support 2 petabytes of shared memory, while TPU 8i is optimized for low-latency inference with expanded SRAM and HBM. These specifications matter because the next compute bottleneck is shifting from training-only clusters to production inference, agent orchestration, KV-cache memory, reinforcement learning, and predictable latency. (Google Cloud)

The venture is also a competitive weapon against Nvidia’s ecosystem, but not necessarily a direct substitute across all workloads. Nvidia GPUs remain the default architecture for frontier model training because of CUDA, developer familiarity, broad framework support, hardware availability through numerous clouds, and strong resale/remarketing value. TPUs are more compelling when workloads are optimized for Google’s stack, when customers are already aligned with Gemini, JAX, PyTorch-on-TPU, vLLM-on-TPU, or Google Cloud’s AI Hypercomputer, and when performance-per-watt materially offsets lower portability. The key question is not whether TPUs replace GPUs broadly; it is whether Google can capture a larger share of incremental AI inference and training workloads where power efficiency, cost, and capacity assurance matter more than maximum hardware portability.

Anthropic provides the strongest public validation of external TPU demand. Anthropic announced in October 2025 that it planned to expand its use of Google Cloud technologies, including up to 1 million TPUs, with the expansion worth tens of billions of dollars and expected to bring well over 1 GW of capacity online in 2026. That scale suggests that sophisticated frontier-model buyers are willing to commit to TPUs in very large volumes when economics and performance are attractive. (Anthropic)

BLACKSTONE STRATEGIC RATIONALE

For Blackstone, the venture is an extension of a dominant digital infrastructure strategy. Blackstone reports more than $1.3 trillion of AUM as of March 31, 2026, and has positioned itself as the world’s largest alternative asset manager. It already has a major data center platform through QTS, AirTrunk, and related digital infrastructure assets. (Blackstone)

The timing is deliberate. Blackstone Digital Infrastructure Trust raised $1.75 billion in a U.S. IPO earlier in May 2026 to acquire newly constructed data centers leased to investment-grade hyperscale tenants, and Reuters reported that Blackstone’s data center assets globally exceed $150 billion. QTS leased megawatts reportedly rose 14-fold after Blackstone took QTS private in 2021. This shows that Blackstone is not merely providing passive capital; it is attempting to control a multi-layer AI infrastructure value chain spanning land, power, data centers, tenants, operating platforms, and now TPU-based compute. (Reuters)

The transaction also improves Blackstone’s competitive positioning versus other private capital platforms. Traditional data center investments are increasingly crowded and valuation-sensitive, while AI compute assets introduce higher return potential if backed by durable demand and differentiated technology. The Blackstone-Google structure could create a proprietary origination channel where Blackstone’s infrastructure capital is paired with Google’s custom silicon and software stack. If successful, this could become a repeatable template: private capital finances scarce AI capacity; the hyperscaler supplies silicon, orchestration software, and demand channels; customers receive dedicated compute capacity without relying exclusively on standard public-cloud procurement.

The risk is that Blackstone is moving up the technology-risk curve. Data center real estate has historically been underwritten around credit tenants, long leases, power availability, and replacement cost. TPU cloud capacity introduces risks around chip generation cycles, accelerator obsolescence, software adoption, customer workload portability, and system utilization. The investment can generate infrastructure-like returns only if capacity is pre-sold or heavily contracted. If the venture carries merchant exposure to TPU demand, the risk profile becomes closer to a leveraged specialty cloud provider than a traditional data center owner.

COMPETITIVE IMPACT ON NEOCLOUDS

The most direct competitive pressure falls on CoreWeave and Nebius, but the effect is more medium-term than immediate. CoreWeave’s Q1 2026 results show revenue of $2.078 billion, revenue backlog of $99.4 billion, adjusted EBITDA of $1.157 billion, more than 1 GW of active power, and more than 3.5 GW of contracted power. These figures demonstrate that the neocloud model has achieved real scale, but also that the model is capital intensive and heavily dependent on continued access to chips, power, financing, and large customer contracts. (CoreWeave Investors)

CoreWeave is still benefiting from severe GPU scarcity. Reuters reported that CoreWeave signed a multi-year Anthropic agreement, an $11.9 billion OpenAI deal, a $6.3 billion Nvidia order, and an expanded $21 billion Meta deal, while Microsoft represented about 67% of CoreWeave revenue in the prior year. This customer concentration and dependence on Nvidia-linked GPU capacity create both a bull case and a bear case: CoreWeave is a scarce-capacity beneficiary, but also exposed to customers diversifying toward TPUs, ASICs, AWS Trainium, AMD GPUs, and in-house silicon. (Reuters)

Nebius shows a parallel growth pattern. Reuters reported that Nebius revenue rose nearly 8x year over year to $399 million in Q1 2026, capex guidance increased to $20 billion to $25 billion, and the company expects more than 4 GW of contracted power by year-end. Nebius also signed a Meta agreement worth up to $27 billion over 5 years. This confirms that AI compute demand remains far above available supply, but also that the economics require extraordinary capital intensity. (Reuters)

The Google-Blackstone venture does not invalidate CoreWeave or Nebius. It broadens the competitive set and reduces the probability that Nvidia GPU neoclouds remain the only scaled path for outsourced AI compute. The more important market implication is that the supply side of AI compute is becoming segmented. Nvidia GPU neoclouds will remain best positioned for workloads requiring maximum ecosystem portability and rapid access to the latest Nvidia platforms. Google TPU clouds may be better positioned for customers prioritizing lower cost per token, power efficiency, Google Cloud integration, and committed capacity. Hyperscaler-native offerings will remain preferred for enterprises that need integrated data, security, governance, and application-layer services.

IMPACT ON NVIDIA AND BROADCOM

For Nvidia, the transaction is a negative narrative development but not necessarily a near-term earnings impairment. AI demand remains sufficiently supply-constrained that incremental TPU capacity is unlikely to displace a large portion of near-term Nvidia shipments. However, the direction of travel matters. A Blackstone-financed TPU cloud creates a scaled, externally financed alternative to Nvidia GPU capacity, which reduces Nvidia’s strategic monopoly over the neocloud layer and increases the credibility of custom silicon as a 3rd-party compute product. Reuters has reported that demand for custom chips such as TPUs has surged as businesses seek alternatives to Nvidia GPUs, and that TPU sales have become a growth engine for Google Cloud. (Reuters)

The stronger derivative beneficiary may be Broadcom. Reuters reported in April 2026 that Broadcom signed a long-term agreement with Google to develop and supply future generations of custom AI chips and other components for Google’s next-generation AI racks through 2031, and separately signed a deal with Anthropic to provide access to about 3.5 GW of AI computing capacity drawing on Google AI processors starting in 2027. If the Blackstone JV scales materially, it should reinforce the custom accelerator and AI networking cycle that Broadcom is already monetizing. (Reuters)

Broadcom’s own guidance reinforces this point. In March 2026, Reuters reported that Broadcom projected AI chip revenue would exceed $100 billion in 2027, driven by custom chip demand, and disclosed Q1 AI revenue of $8.4 billion, up 106%. Broadcom also indicated expected delivery of 1 GW of TPUs for Anthropic in 2026, with demand rising to 3 GW in 2027. This places Broadcom at the center of the custom silicon supply chain even if Google retains architectural control over TPUs. (Reuters)

The Nvidia bear case should not be overstated. Nvidia retains broad software ecosystem advantages, multi-cloud distribution, systems-level integration, and a large installed base. The Google-Blackstone venture is more likely to compress the most extreme long-term monopoly assumptions than to trigger immediate demand destruction. The sharper implication is that AI accelerator spending may bifurcate into Nvidia GPU ecosystems for general-purpose model development and custom ASIC ecosystems for large, predictable, high-utilization inference/training workloads where hyperscalers can optimize the full stack.

POWER, TIMING, AND EXECUTION RISK

Power is the principal bottleneck. The IEA estimates global data center electricity consumption was 415 TWh in 2024, or around 1.5% of global electricity consumption, and projects it to more than double to around 945 TWh by 2030. The IEA also states that the U.S. accounted for 45% of global data center electricity consumption in 2024 and that U.S. data centers account for nearly 50% of U.S. electricity demand growth through 2030. (IEA)

A 500 MW target by 2027 is ambitious because AI data centers at this scale require power procurement, transmission access, substations, cooling infrastructure, fiber, construction labor, accelerator supply, and operational systems integration. CBRE’s 2026 outlook states that the shift toward 500 MW-plus AI campuses has pushed construction schedules into multi-year territory, and any requirement for new high-voltage transmission or incremental generation can extend interconnection timelines to 24, 36, or more than 48 months. (CBRE)

This risk can be mitigated but not eliminated by Blackstone’s platform. Blackstone’s ownership of QTS and AirTrunk gives it deep development, procurement, and customer contracting expertise. However, the 2027 deadline leaves limited room for permitting delays, transformer shortages, utility queue delays, or AI accelerator supply constraints. The IEA estimates that unless grid risks are addressed, around 20% of planned data center projects could face delays; it also notes that transmission lines in advanced economies can take 4 to 8 years to build and that lead times for transformers and cables have doubled in the past 3 years. (IEA)

The venture’s use of TPUs may improve power economics if Google’s performance-per-watt claims translate into real workloads. Google states that TPU 8t and TPU 8i deliver up to 2x better performance-per-watt than Ironwood and are supported by 4th-generation liquid cooling. If these gains hold under high-utilization production workloads, the venture could sell compute at lower effective cost per token or higher margin at comparable pricing. However, performance-per-watt claims are workload-specific and require customer software optimization. The economic advantage is therefore not automatic; it depends on workload mix, utilization, model architecture, compiler maturity, and customer willingness to optimize for TPU. (blog.google)

ALPHABET INVESTMENT IMPLICATIONS

For Alphabet, the development is strategically positive because it expands the monetization surface of TPUs, creates an off-balance-sheet or capital-partnered capacity channel, and reinforces Google Cloud’s full-stack AI narrative. Google Cloud’s Q1 2026 numbers already showed significant operating leverage, with Cloud revenue up 63% and operating margin at 32.9%. The venture could help sustain that growth by alleviating capacity constraints and giving Google a way to monetize TPU demand even where customers prefer dedicated or externally financed infrastructure. (Alphabet Investor Relations)

The near-term P&L impact is likely modest relative to Alphabet’s scale, particularly because the first 500 MW is targeted for 2027 and because economics will depend on contract structure. The more important effect is on investor perception of Alphabet’s AI capex efficiency. A credible Blackstone partnership can support the argument that Alphabet’s AI infrastructure is not merely a cost center for defending Search, but a monetizable asset stack spanning cloud services, TPU hardware, software, capacity leasing, and infrastructure partnerships. This may partially offset market concerns over the absolute size of Alphabet’s $180 billion to $190 billion 2026 capex plan. (Reuters)

The risk is that the transaction introduces complexity around channel conflict. Google Cloud already sells TPU access directly. A separately controlled Blackstone TPU cloud could create pricing tension, customer segmentation issues, and allocation conflicts between Google internal AI workloads, Google Cloud customers, and JV customers. The cleanest structure would reserve the JV for dedicated, large-scale, take-or-pay customers that are incremental to standard GCP demand. If the JV competes directly with Google Cloud for overlapping customers, margin attribution and strategic control could become less clear.

May 19

2

1

8

19,196

今後 10 年の ML を支える、

メガスケール データセンター ファブリック開発

→ goo.gle/42F1RQC

現代の AI ワークロードが求める極めて厳しい要件に応えるために設計された「Virgo Network」は、次世代アクセラレータ設計を支える基盤として、Google の AI Hypercomputer を支えます。

2

7

3,242

May 14

the part where we use anything other than the hypercomputer that runs every possible program, eliminating the ones that don't match the data, and producing an output distribution by taking a weighted average of the program outputs weighted by 2^-length

1

20

792

La IA está pasando de responder preguntas a ejecutar acciones.

Para liderar esta era agéntica, hemos anunciado nuestras TPUs de 8.ª generación y nuevas capacidades de AI Hypercomputer para ayudarte a escalar sin límites.

Conoce más → goo.gle/4dm54tj

3

2

122

May 10

THE ETERNAL MEMORY OF MANKIND: ARWEAVE

This is not a mere crypto trend; it is the most profound infrastructural revolution in human history. Until now, the internet was a "fading whisper." Our words, our wealth, and our legacies were held hostage by corporate whim and fragile servers. Arweave has shattered that cycle.

Why is this the "Great Leap Forward" for Civilization?

1. Digital Monuments: Arweave doesn’t store data in the cloud; it etches it into the bedrock of time. It preserves today’s digital existence for millennia—indestructible, uncensorable, and immutable. It is the Göbeklitepe of the digital age.

2. The New Sovereign Infrastructure: From global finance to state archives, Arweave is becoming an inevitable public utility. Just like oxygen or electricity, the world will breathe through this network because information is the lifeblood of progress—and Arweave makes it immortal.

3. The Unstoppable Hypercomputer (AO): Beyond storage, Arweave is birthing autonomous AI and software that can never be killed. A decentralized "Hypercomputer" that will run for centuries, free from any "off" switch.

4. Mathematical Scarcity (AR Token): With a supply tighter than Bitcoin, AR is not just a token—it is the fuel of eternity. When it becomes the global standard for the world’s permanent data, a $1,000 target isn't the finish line; it’s just the ignition.

The Bottom Line:

If our descendants are to know who we were and what we built, they will find those answers on Arweave. The "Permaweb" is no longer a vision—it is an active reality. The engines are at full throttle. You either secure your place in history now, or you vanish when the old internet dies.

#Arweave #AO #Crypto #AI #Web3

$AR

@Sameverywhere

@samecwilliams

@ArweaveTeam

@aoTheComputer

@ArweaveEco

@VitalikButerin

@balajis

@a16zcrypto

@CoinMarketCap

@coingecko

@elonmusk

"Analysis generated via collaboration with Google AI. All insights based on architectural and economic data."

1

1

5

78

May 7

NVIDIA と Google Cloud は 10 年以上にわたり協業し、このパートナーシップは新たな節目を迎えました。

AI ファクトリーに向けて Google Cloud の AI Hypercomputer を拡張し、エージェント型 AI やフィジカル AI の進化を支える取り組みが発表されました。

nvda.ws/4mYjEf4

4

10

2,371

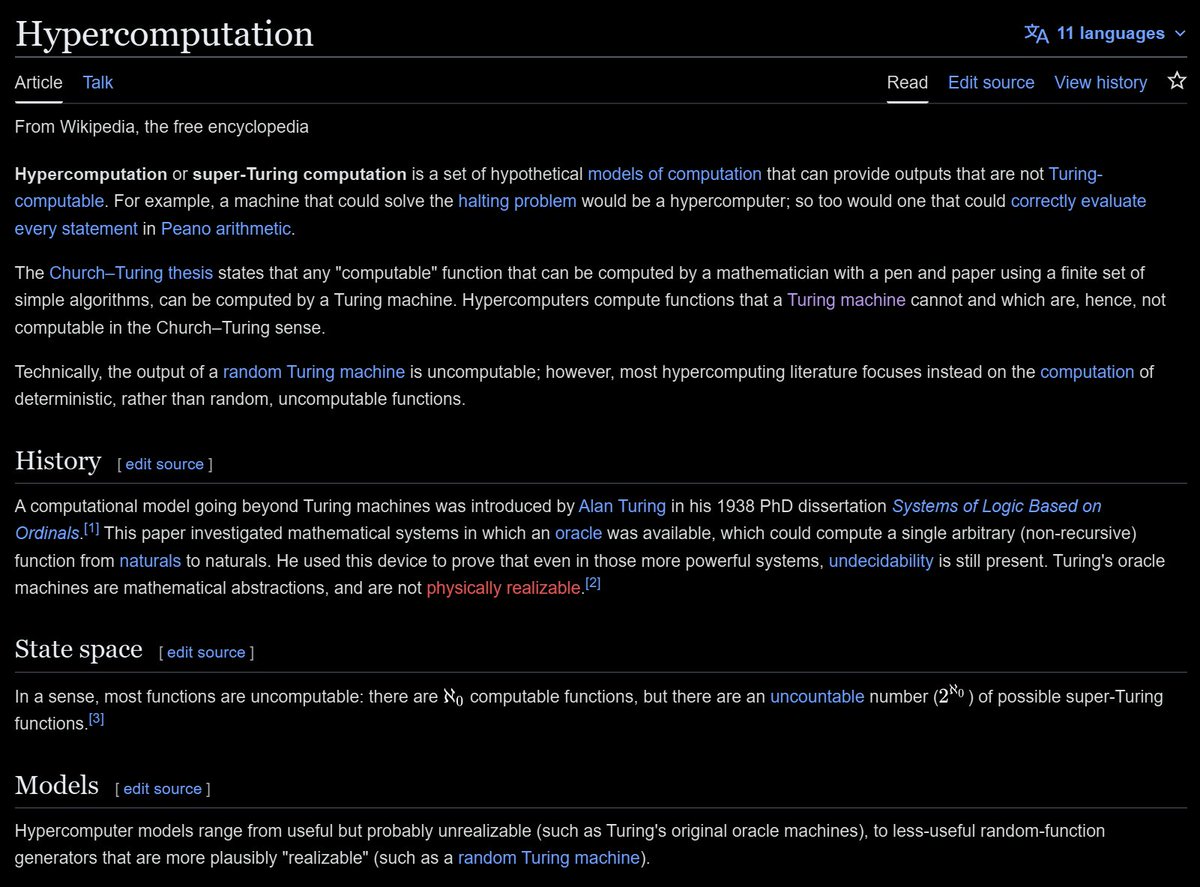

Hypercomputation or super-Turing computation is a set of hypothetical models of computation that can provide outputs that are not Turing-computable. For example, a machine that could solve the halting problem would be a hypercomputer; so too would one that could correctly evaluate every statement in Peano arithmetic.

6

3

22

1,399

AI is moving from answering questions to taking action.

To lead in this agentic era, we recently announced our 8th gen TPUs and new AI Hypercomputer capabilities to help you scale without limits.

Learn more → goo.gle/4up1yW3

5

192

May 1

I’m sure Hypercomputer is a real abstraction at this point.

I am one of the first people to advise not to get hung up on marketing terms.

I find this term hard to get past.

I can’t put my finger on why.

Some thoughts on the @GoogleCloud Hypercomputer: moorinsightsstrategy.com/ana…

2

5

1,170

Apr 29

🌟 Googleが2026年4月に発表した「第8世代TPU」のポイントを、簡単に説明🌟

(damさんの解説をさらに簡単にしています。)

❶最大の変化

TPUが「学習用」と「推論用」に明確分化

Googleは第8世代TPUで、用途別に設計を分けた‼️

・TPU 8t → AIモデルを学習(Training)するためのTPU

・TPU 8i → AIを実際に動かす推論(Inference)向けTPU

👉これまでのTPUは両方を兼ねる設計だったが、今回は役割を明確に分離。

これは単なる性能向上ではなく、

「AI時代のボトルネックがどこにあるか」

に対するGoogleの答えでもあるよ👼

❷なぜ推論(Inference)を重要視してるの?👀

以前は巨大モデルを学習させることが重要視されたが、モデルを速く安く動かす時代に完全に移行したため👀

・ChatGPTや のGeminiのような対話AI

・エージェント型AI

・長文処理

・思考ステップを伴う推論

が増え、AIは1回の質問に対して大量の計算を行うようになった。

❸Googleの本当の狙い = AI Hypercomputer

GoogleはただTPUを速くしただけじゃなく、AIデータセンター全体を次のレベルにアップデート❣️

主なポイント:

• ハードウェア(TPU CPU ネットワーク)

• ソフトウェア(JAX, vLLM, Pathwaysなど)

• メモリ・通信・ストレージの最適化

これら全部を連携させて、1トークンあたりのコストを徹底的に下げるのが狙い。

❹ 今後の勝負どころ

• チップの性能競争 👉トークンコスト競争へシフト

• 訓練用と推論用でハードウェアを分ける時代に

• Googleは自社TPUだけでなく、NVIDIAも使いながら全体のインフラで勝つ戦略へ

❺Googleの戦略は「TPU vs NVIDIA」ではない。

自社TPUだけに依存していない。

Google CloudではTPU、GPU、CPUを併用できる。

Googleの狙いは、TPUでNVIDIAを倒すことではなく、AIインフラ全体をGoogle Cloud上で完結させること

に近いよ👼

5

2

60

9,693

Apr 28

Agentic workloads generate 20-50x more tokens than chat. That multiplier hits compute, storage, and orchestration simultaneously.

@Googlecloud's Mark Lohmeyer (who owns all of Compute) and @PatrickMoorhead break down how GC is building infrastructure to absorb that pressure across the full AI Hypercomputer stack from @GoogleCloud Next 2026.

2

17

162,595

Apr 27

AIトレンドニュース要点

AIトレンドへの影響度が最も高いのは、

①GoogleのTPU/NVIDIA Rubin両面展開、

②TSMCのCoWoS拡張、

③OpenAIのマルチクラウド化、

④AIデータセンターの電力制約、

⑤PCB材料供給ショックです。

今回の記事群は、

AI競争の主戦場が

「GPU単体性能」から

「アクセラレータ+ネットワーク+電力+先進パッケージ+ストレージ+供給網」へ移っていることを示しています。

1. 最重要:GoogleはTPUとNVIDIA Rubinを併用し、AIインフラを“超大規模ファブリック”化

Google Cloudは、

第8世代TPUであるTPU 8tとTPU 8iを発表し、学習向けと推論・Reasoning向けを明確に分けた構成に移行しています。

TPU 8tは

9,600チップのSuperpod、121 FP4 ExaFLOPs、2PBの共有HBMを掲げ、Pathways/JAXにより100万超のTPUチップを単一トレーニングクラスターとして扱う方向です。

TPU 8iは

低遅延推論向けで、Boardflyトポロジー、CAE、3倍のSRAMによりMoEや長文推論のレイテンシ削減を狙います。

これは、Googleが

「NVIDIA代替」を単純に目指すというより、

学習・推論・Agentic AIを

用途別に最適化する内製ASIC路線を

強めているという意味合いが強いです。

一方で、

GoogleはNVIDIA Rubinも排除していません。

A5XはNVIDIA Vera Rubin NVL72を使い、

GoogleのVirgo NetworkとNVIDIA ConnectX-9 SuperNICを組み合わせることで、単一サイトで最大8万基、マルチサイトで最大96万基のRubin GPU規模に拡張可能とされています。

つまり、Googleの戦略は

「TPUでNVIDIAを置き換える」ではなく、

「Google TPUとNVIDIA Rubinを

同じAI Hypercomputer/Virgo Network基盤上で使い分ける」方向です。

NVIDIAにとってはGoogle Cloud上のRubin採用が追い風である一方、GoogleはTPUを外販・クラウド提供することで、NVIDIAに対する価格交渉力と顧客囲い込み力を同時に高めています。

投資・産業面では、

NVIDIA、Google、Broadcom、MediaTek、TSMC、HBMサプライヤ、光通信・高速ネットワーク部材、液冷部材への含意が大きいです。

特にTom’s Hardware記事では、

TPU 8iはMediaTek、

TPU 8tはBroadcomが設計パートナーとされ、

TPUサプライチェーンが

Broadcom単独から複線化している点が示されています。

ただし、MetaやAppleのTPU利用規模に関する記述はTom’s Hardware本文上の情報であり、今回確認した範囲では各社公式での完全な裏取りはしていないため、そこは不確かです。

2. 最重要:TSMCのCoWoSロードマップは、AI半導体のスケーリング軸が“パッケージ”へ移ったことを明確化

Tom’s Hardwareの記事は、

TSMCの次世代CoWoSロードマップを

「Packaging is now the scaling engine」と位置付けています。

TSMCは現在5.5レチクルサイズのCoWoSを量産し、

2028年に14レチクルサイズ、

2029年に14レチクル超へ拡大する計画を示しています。

TSMC公式リリースでは、

2028年の14レチクルCoWoSは約10個の大型Compute Dieと20個のHBMスタックを統合可能と説明されています。

Tom’s Hardware本文では、

2029年までに24個の3D積層Compute Chipletと24個のHBM5Eスタック、2024年比でCompute Transistor 48倍、帯域幅34倍という記述があります。

ただし、TSMC公式リリースで直接確認できる表現は「14レチクルCoWoSが2028年、14レチクル超が2029年」「約10大型Compute Die+20 HBMスタック」であり、24 HBM5Eや48倍・34倍の詳細数値はTom’s Hardware本文上の記述として扱うのが安全です。

この意味は大きいです。

ロジック微細化だけでは

AIチップの性能向上ペースを維持しにくくなり、

CoWoS、

SoIC、

HBM、

基板、

液冷、

CPO/光I/Oが

同時にスケールする必要があります。

TSMC公式リリースでも、

CoWoS拡張に加えて、

A14-to-A14 SoIC、

COUPEによるCo-Packaged Optics、

基板上COUPEの2026年生産開始、

2倍の電力効率、

10倍のレイテンシ低減が示されています。

AIサーバーの構造そのものが、GPUボード中心から、

巨大SiP・高密度基板・光接続・液冷前提へ変わる流れです。

3. 最重要:Microsoft・OpenAIの独占関係緩和は、AI計算資源のマルチクラウド化を加速

Tom’s Hardware記事は、

MicrosoftとOpenAIの独占契約終了により、

OpenAIがAmazonやGoogleなど他クラウドを活用できる余地が広がったと整理しています。

OpenAI公式の2026年4月27日発表でも、

MicrosoftはOpenAIのPrimary Cloud Partnerに残る一方、OpenAIは全製品を任意のクラウドプロバイダー経由で顧客に提供可能になり、

MicrosoftのOpenAI IPライセンスは

2032年まで続くが非独占化されると明記されています。

この変化は、

Azureにとって完全なマイナスではありません。

OpenAI製品はまず

Azureで提供される建付けが残り、

OpenAIからMicrosoftへのRevenue Shareも

2030年まで継続します。

ただし、

OpenAIの計算資源調達はAzure一極から、

AWS、Google Cloud、専用データセンター、自社設計・外部ASICを含む複線構造に向かいやすくなります。

AIインフラ投資の観点では、

Microsoft単独の囲い込みプレミアムは低下し、

AWS、Google、NVIDIA、Broadcom、Trainium/TPU系サプライチェーンにも需要が分散する構図です。

4. 最重要:9GW級AIデータセンターは、電力がAI供給制約の中心になったことを示す

ユタ州のStratos計画は、

Kevin O’Leary氏のO’Leary Digitalが進めるAIデータセンター構想で、最終的に9GW規模、フェーズ1だけで約3GWの発電能力を想定しています。

Tom’s Hardwareによれば、

これはユタ州の平均電力使用量約4GWの2倍超に相当し、天然ガスパイプライン接続によるオフグリッド発電を前提としています。

重要なのは、

クラウド企業が既存電力網への接続を待つのではなく、

自前の発電・送電・冷却を組み込む

“AI工業団地”化へ進んでいる点です。

記事ではSoftBankの10GW級オハイオ計画やMetaの7GW級天然ガス発電構想も比較対象として挙げられています。ただし、Stratosの具体的なハイパースケーラー入居企業は記事時点で未公表です。したがって、特定企業の需要に直結すると断定するのは不確かです。

5. 高重要:PCB材料の供給ショックは、AIサーバーのボトルネックをさらに広げる

Tom’s HardwareとReutersの内容では、

イランによる

サウジアラビア・ジュバイル石化コンプレックスへの攻撃により、

PCB laminateに使われる

高純度PPE樹脂の供給が停止し、

SABICが世界供給の約70%を担うため、

PCB供給網に大きな圧力がかかっているとされています。

Reutersは、

PCB価格が4月に最大40%上昇したとのGoldman Sachs分析にも触れています。

AIトレンドへの含意は、

半導体本体だけでなく、

PCB、

CCL、

銅箔、

ガラスクロス、

樹脂、

ABF基板、

サーバーマザーボードまで供給制約が広がる点です。

AIサーバーはGPU/HBM/スイッチだけでなく、高多層・高周波・低損失の基板材料を大量に必要とするため、

PPE樹脂や銅箔の不足は、

AIサーバーのリードタイムと価格に直接波及し得ます。

原文ニュアンス上も「消費者向けガジェット価格」だけでなく、AIサーバーを含む電子機器全般への波及が問題です。

6. 中重要:中国LineShineは“国産HPC・AI基盤”の象徴。ただし近い将来のNVIDIA代替と見るのは不確か

Wccftechの記事では、

中国・深圳のLineShineスーパーコンピュータが2 ExaFLOPs超、47,000 CPU、650PBストレージ、10TB/s帯域、最大規模の液冷システムを掲げ、外国製チップに依存しない構成とされています。またDeepSeekでCPUあたり578 tokens/sの試験値が示されたとされています。

ただし、記事自体も

「具体的な稼働時期は示されていない」としており、2029〜2030年ごろという見方はWccftech側の推測です。

さらに、情報源としてX投稿が含まれているため、

性能・国産比率・実運用時期については不確かです。

AIトレンド上の意味は、

中国がNVIDIA規制下でGPU依存を避けるHPC/AI基盤を国家的に構築しようとしている点であり、短期的にNVIDIA H100/B200/Rubin級の汎用AIアクセラレータ需要を置き換える話とは分けて見るべきです。

7. 中重要:Kingstonの30.72TB Gen5 SSDは、AIデータセンターでストレージ密度が新たな制約になっていることを示す

KingstonのDC3000ME 30.72TB U.2 NVMe SSDは、PCIe 5.0、最大14GB/sのシーケンシャルRead、最大2.8M Random Read IOPSを掲げています。

記事のニュアンスは、

単なるSSD新製品ではなく、

AI/HPC/クラウド環境で、ラックあたりドライブ数を減らし、消費電力・冷却・配線を簡素化する高密度ストレージ需要の増大です。

Google Cloudも

AI Hypercomputerの中でManaged Lustre、TPUDirect Storage、RDMA、Rapid Bucketsを強調しており、AIクラスターでは演算器だけでなく、データ供給、チェックポイント、KV Cache、並列ファイルシステムが性能を左右します。Kingstonの記事はその下流側のストレージ密度需要を示す材料です。

8. 中〜低重要:Intel Arc iGPUの共有メモリ拡張は、ローカルLLM実行の裾野拡大

IntelのArc Pro向けHotFix Driverでは、システムメモリの最大93%を内蔵Arc Pro GPUに割り当てられるようになり、64GB搭載システムなら約59.5GBをGPU作業メモリとして使えるとされています。

これは、

ローカルPCやワークステーションで大きめのLLMを動かす際の制約を緩和します。

ただし、これはデータセンターAIの主戦場を変える材料ではありません。

影響は、開発者、エッジAI、ローカル推論、ISV認証ワークステーション領域に限定されます。メモリを多く割り当てられても、HBM搭載AIアクセラレータの帯域・演算性能を代替するものではないため、AIトレンド全体への影響度は中〜低です。

9. 中重要:Claude/Cursorのデータベース削除事例は、AIエージェント普及の安全設計リスクを示す

Tom’s Hardware記事では、

PocketOSがCursor上のClaude Opus 4.6を使ったAI Coding Agentにより、Railway上の本番データベースとバックアップを削除されたと報じています。

記事では、

AI Agentがステージング環境の作業中にRailway volumeを削除し、クラウド側のAPI設計やバックアップ設計も被害を拡大したと整理されています。

これは、AI Coding Agentの導入拡大に対して、

Scoped Token、破壊的操作の多段確認、バックアップ隔離、復旧手順、Agent権限管理が必須になることを示します。

ただし、本件はTom’s HardwareがPocketOS創業者の投稿を基に整理した事案であり、Anthropic、Cursor、Railwayの公式検証結果までは今回確認できていません。したがって、責任所在の断定は不確かです。

10. 低重要:ロシア・中国Irtysh CPUは、制裁下の国産化努力としては重要だが、AIトレンドへの直接影響は限定的

Irtysh C632はLoongsonのLoongArch ISAを活用したロシア市場向けCPUで、Tom’s Hardwareは、米制裁によりx86 CPUを調達できないロシアが中国Loongsonの成果に乗る形だと説明しています。

記事では、The Witcher 3の実行結果が22〜32FPS、低設定でも25〜38FPSにとどまり、CPUボトルネックが明確だったとされています。

AIトレンドへの影響は、

ロシア・中国圏の非x86/非米国依存エコシステム形成という地政学的文脈にあります。ただし、性能・互換性・ソフトウェア最適化の課題が大きく、AIデータセンターや先端AIアクセラレータ競争への直接的インパクトは低いです。

統合見解

今回の記事群から見るべき最大の変化は、

AIインフラが「GPUを買えばよい」段階を終え、

システム全体の制約競争に移ったことです。

GoogleはTPUとNVIDIA Rubinを併用し、

Virgo Networkで100万チップ級の分散AI基盤を作ろうとしています。

TSMCは

CoWoS/SoIC/COUPEでパッケージングを新たなスケーリングエンジンにし、

OpenAIは

Microsoft一極からマルチクラウド調達へ動き、

データセンター事業者は

9GW級の自前電源へ向かっています。

一方で、

供給制約はGPU・HBMだけではありません。

PCB材料、

PPE樹脂、

銅箔、

ガラス繊維、

SSD、

並列ファイルシステム、

電力、

冷却、

ネットワーク、

Agent安全設計まで広がっています。

特にPCB材料ショックは、

AIサーバーの基板・CCL・高周波材料の需給逼迫をさらに悪化させる可能性があり、

AI CapExの実行速度に対する新たなリスクです。

現時点で優先監視すべきテーマは、

TSMC CoWoS能力、

HBM4/HBM5移行、

Google TPU外販の実需、

NVIDIA Rubinのクラウド採用、

AWS/Google/Azure間のOpenAIワークロード分散、

AIデータセンター向け天然ガス発電、

PCB・CCL材料価格です。

LineShineやIrtyshは地政学的には重要ですが、短期のAIインフラ需給に与える影響は、NVIDIA Rubin、Google TPU、TSMC CoWoS、PCB材料ショックに比べて一段低いと見ます。

1

1

9

1,395