IFGL Refractories Ltd is seeking member approval via postal ballot for the appointment of Mr. Mukesh Harshadrai Rawal as a Non-Executive Non-Independent Director. The e-voting period will run from June 18, 2026, to July 17, 2026. Results are expected by July 21, 2026. Shareholders can vote electronically through NSDL's platform. The cut-off date for voting eligibility is June 12, 2026.

📊 IFGL REFRACTORIES LTD | 🏷️ Postal Ballot

🌐 Details: wegro.app/bjR4G8

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/go

108

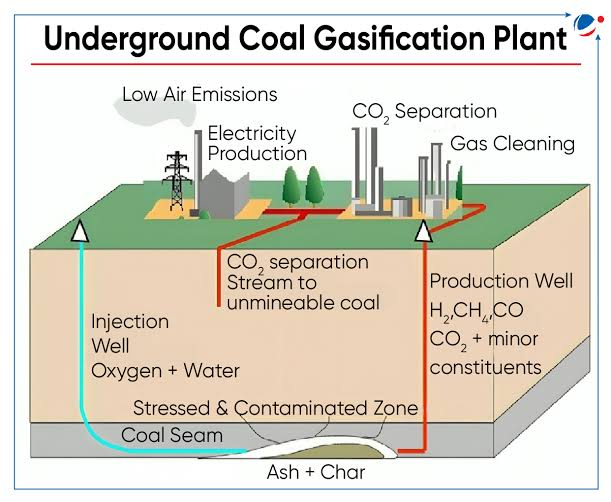

The only large-scale coal gasifier actually running in India today is not BHEL. Not Talcher. Not any PSU.

It is Jindal Steel at Angul, live since 2014.

Everyone is now chasing the ₹37,500 crore gasification scheme Anurag Thakur just flagged as India's hedge against the West Asia crisis. Almost nobody is asking the harder question: who can actually build one.

Coal gasification = coal or lignite to syngas to methanol, ammonia, urea and chemicals. India imports 80 to 90% of its methanol, around 20% of its urea and over half its LNG. Replace that with domestic coal and you save lakhs of crore in forex. Big pitch, slow build.

Here is the full value chain, sorted by where the money actually flows.

Proven and running today

🔹 Jindal Steel: world's first coal gasification plant for steelmaking, 225,000 Nm3 per hour syngas feeding the world's largest syngas based DRI plant at 2 MTPA. The only large-scale high ash gasifier operating in India. Second one planned at Raigarh.

Tech and flagship project, still pending

🔹 BHEL: indigenous fluidized bed gasifier for high ash coal, coal to methanol pilot at 99% purity, leading the BCGCL coal to ammonium nitrate JV at Jharsuguda with Coal India. Not scaled commercially yet.

🔹 NTPC: potential coal to syngas, hydrogen and chemicals operator. High conviction, long horizon.

🔹 Talcher Fertilizers (GAIL, RCF, Coal India, FCIL): ₹13,277 crore plant for 12.7 lakh tonnes urea a year, India's first gasification urea unit, around 71% built and slipping.

Feedstock layer

🔹 GMDC: one of the strongest lignite plays if Gujarat lignite gasification scales.

🔹 NLC India: lignite focused, actively evaluating gasification.

🔹 NMDC: mining giant, low direct gasification exposure today.

🔹 South West Pinnacle Exploration: coal drilling and resource development, Jharkhand block in 2027.

🔹 Asian Energy Services and Deep Industries: exploration and gas handling services, indirect.

🔹 Prabha Energy: small potential EPC and service role, limited direct exposure.

🔹 MSTC: coal auction platform, negligible direct earnings linkage.

Industrial syngas consumers

🔹 Sarda Energy and Godawari Power & Ispat: steel and ferro alloy users if domestic syngas turns cheaper.

🔹 Jindal Stainless: syngas and hydrogen user for decarbonisation, downstream beneficiary.

Picks and shovels, paid first when projects move

🔹 Engineers India: design, FEED and project management for gasification complexes.

🔹 L&T: EPC powerhouse, likely builder of the large complexes.

🔹 Power Mech Projects and SEPC: erection, commissioning and balance of plant.

🔹 Thermax: boilers, utilities, waste heat and environmental systems.

🔹 JNK India: process heaters and thermal equipment.

🔹 Kirloskar Pneumatic: compressors and gas handling equipment.

🔹 Elecon Engineering: coal handling and conveying systems.

The hidden one is oxygen

🔹 Linde India and INOX Air Products: gasifiers need giant air separation units. Every plant is a captive oxygen order.

Refractories

🔹 IFGL Refractories and Vesuvius India: line the high temperature reactors.

The downstream margin, a 2028 and beyond story

🔹 Deepak Fertilisers: ammonia, nitric acid, ammonium nitrate. Among the best chemical fits.

🔹 RCF: ammonia and fertilizer beneficiary if coal derived ammonia scales.

🔹 Balaji Amines and Alkyl Amines: coal to syngas to methanol to amines, the highest value add if India localises methanol.

🔹 Refex Industries, Sustainable Energy Infra Trust and Hi-Green Carbon: adjacent energy and circular economy names with limited direct gasification linkage.

The honest part. Indian coal ash runs 30 to 45%, high and variable, which is what makes gasification costly and hard to run stably here. Talcher is years late. BHEL's route is still pilot scale. So, the near-term order flow sits in engineering, oxygen and equipment. The chemical margin is the long game. Anyone pricing these as immediate methanol plays is early by years.

Watching the build layer, not the output layer, for now.

📌Disclaimer: Educational purposes only, not a buy/sell recommendation

2

7

33

5,799

🧵 India's Coal Gasification Value Chain – Listed Stocks Ranked from Feedstock to Chemicals

1. Coal gasification = Coal/Lignite → Syngas → Methanol/Ammonia/H₂ → Chemicals/Fertilizers/Industrial Products.

The biggest winners may not be miners, but companies controlling engineering, conversion & downstream chemicals.

2. NMDC

Primarily a mining giant. No direct coal gasification role today, but could participate in future mineral and industrial ecosystem expansion. Low direct exposure.

3. GMDC

One of the strongest lignite-linked plays. If lignite gasification scales in Gujarat, GMDC becomes a key feedstock supplier.

4. NLC India

Among the most direct beneficiaries. Focused on lignite resources and actively evaluating lignite gasification opportunities.

5. NTPC

Potential future coal-to-syngas, coal-to-hydrogen and coal-to-chemicals operator. One of the highest-conviction long-term plays.

6. Sarda Energy & Minerals

Could become a syngas/hydrogen consumer in steel and ferro-alloy operations. Indirect beneficiary.

7. Godawari Power & Ispat

Industrial consumer angle. Benefits if domestic syngas, hydrogen or ammonia-based inputs become cheaper.

8. Jindal Stainless

Future user of hydrogen/syngas solutions for decarbonization and energy efficiency. Downstream beneficiary.

9. South West Pinnacle Exploration

Coal drilling, exploration and resource development. Benefits if new coal blocks and underground gasification projects expand. Jharkhand coal block allotment in 2027.

10. Asian Energy Services

Field services, exploration and energy infrastructure support. Indirect beneficiary through higher resource development activity.

11. Deep Industries

Gas handling and energy services. Possible supporting role but not a core gasification beneficiary.

12. Prabha Energy

Potential EPC/service participant. Limited direct coal gasification exposure currently.

13. Engineers India (EIL)

One of the most important names in the chain. Feasibility studies, engineering design, FEED and project management.

14. Larsen & Toubro (L&T)

Likely builder of large coal gasification complexes. EPC execution powerhouse.

15. Power Mech Projects

Construction, erection and commissioning opportunities from large gasification projects.

16. SEPC

Potential balance-of-plant construction participant. Smaller exposure versus L&T or Power Mech.

17. Thermax

Utilities, boilers, steam systems, waste heat recovery and environmental solutions. Strong supporting beneficiary.

18. BHEL

India's flagship gasifier and technology player. One of the most important coal gasification stocks overall.

19. JNK India

Process heaters and thermal equipment. Niche equipment supplier to chemical and gasification projects.

20/ Kirloskar Pneumatic

Compressors and gas-handling equipment. Essential supporting equipment supplier.

21/ Elecon Engineering

Coal handling, material movement and conveying systems. Infrastructure beneficiary.

22. IFGL Refractories

High-temperature refractory materials used in gasification and chemical plants.

23. Vesuvius India

Advanced refractory and thermal solutions for high-temperature industrial operations.

24. MSTC

Possible role in coal/resource auctions but negligible direct earnings linkage to gasification.

25. Refex Industries

Very limited direct connection. More of a peripheral energy/environment play.

26. Sustainable Energy Infra Trust

No major direct coal gasification linkage identified currently.

27. Hi-Green Carbon

Focused on recovered carbon black/pyrolysis. Adjacent circular economy theme, not coal gasification.

28. Rashtriya Chemicals & Fertilizers

Major ammonia and fertilizer beneficiary if coal-derived ammonia scales in India.

29. Deepak Fertilisers

Strong downstream ammonia, nitric acid and ammonium nitrate linkage. One of the best chemical beneficiaries.

30. Alkyl Amines and Balaji Amines(Chemical Winners)

Coal → Syngas → Methanol → Amines. Among the most attractive downstream value-add beneficiaries. Long-term winner if India becomes self-sufficient in methanol.

31. Linde India Limited and INOX Air Products

Gasification consumes huge amounts of oxygen. Many Chinese Big coal gasification plants have dedicated oxygen units.

🏆 My Coal Gasification Watchlist:

Balaji Amines | NTPC | NLC India | Engineers India | L&T | Thermax | Deepak Fertilisers | Alkyl Amines | GMDC | BHEL | RCF | South West Pinnacle Exploration Ltd

Indirect Beneficiaries

-Aegis Logistics Limited

-Linde India Limited

-GAIL (India) Limited

These benefit if volumes rise.

Fertilizers theme become beneficiaries if domestic coal-derived ammonia replaces imports

The biggest wealth creation historically happens in chemicals for future, not mining.

Coal → Syngas → Methanol/Ammonia → Specialty Chemicals is where margins compound.

Not a buy sell recommendation. Not Sebi registered advisor, DYOR before taking any investment decision.

10

45

270

18,931

Jun 13

🚨 The Biggest Winners Of India's Growth Story May Never Become Household Names

Most investors focus on:

📱 Consumer Brands

🤖 AI

🚗 EVs

But some companies quietly operate behind the scenes of industrial growth.

👀 Worth tracking:

⚙️ IFGL Refractories

⚙️ Technocraft Industries

⚙️ Everest Kanto Cylinder

⚙️ Roto Pumps

⚙️ Pennar Industries

⚙️ Wendt India

⚙️ Yuken India

These businesses may never dominate headlines.

But they serve industries that keep factories running, infrastructure expanding and exports growing.

Sometimes the market notices them much later.

📌 Save this list.

💥💥

1

2

2

469

Jun 13

🚨 Some Businesses Quietly Benefit No Matter Which Sector Wins

EVs.

Defence.

Chemicals.

Data Centers.

Infrastructure.

Different stories.

But many rely on the same industrial ecosystem.

👀 Worth tracking:

⚙️ IFGL Refractories

⚙️ Wendt India

⚙️ Roto Pumps

⚙️ Everest Kanto Cylinder

⚙️ Pennar Industries

⚙️ Technocraft Industries

The market often notices these businesses much later.

📌 Worth tracking.

8

1,026

Jun 13

IFGL Refractories FY26

The business is in capex mode—greenfield plants at Khurda (Odisha) and Bhachau (Gujarat) are under evaluation or awaiting Government of India approvals, funded in part by debt, as management bets on steel-driven India capex cycles through the next 3–5 years.

Read more - eduinvesting.in/ifgl-refract…

63

Jun 12

IFGL Refractories FY26: Growth Amid Margin Squeeze, India Bets, Goodwill Windfall Ahead - Eduinvesting eduinvesting.in/ifgl-refract…

2

181

Jun 11

Indvandring - har de noget af det? Ikke ifgl medierne, de tossehoveder.

64

Jun 10

Hvis staten havde taget en narkedsrentd havde den tjent væstntligt mindre. Den tjente ifgl Erhvervsministeriet 17 mia hvilket svarede til en rente på 10%. Men hvad er det du gerne vil afsløre?

1

44

Jun 9

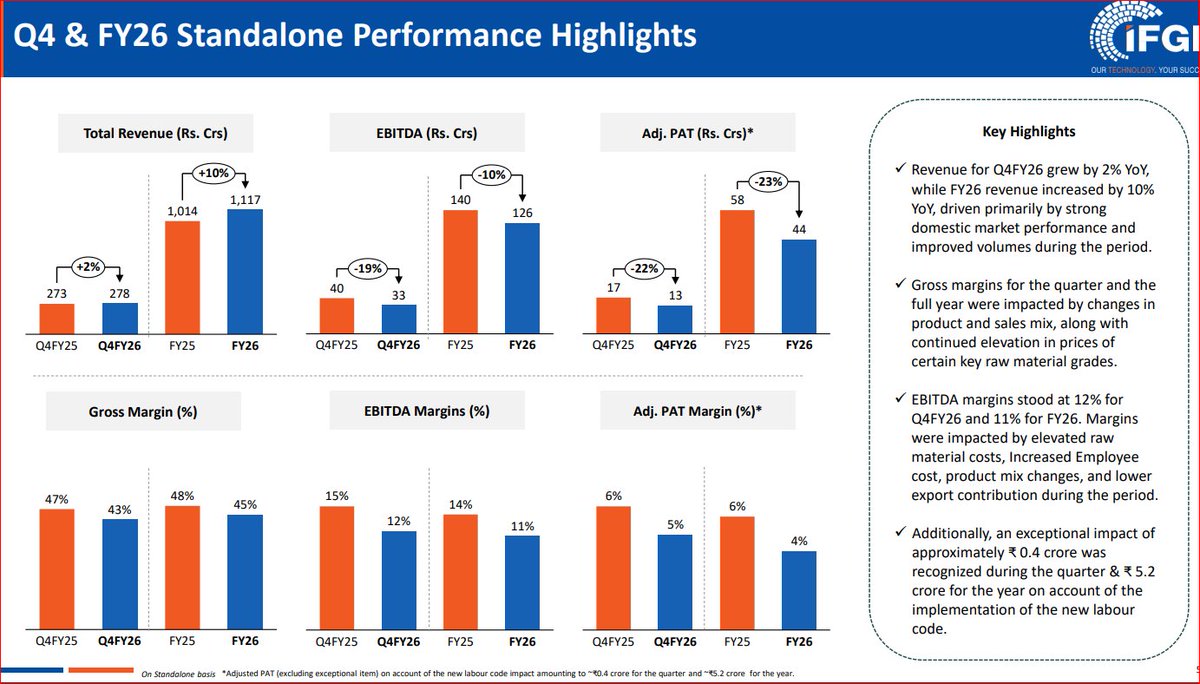

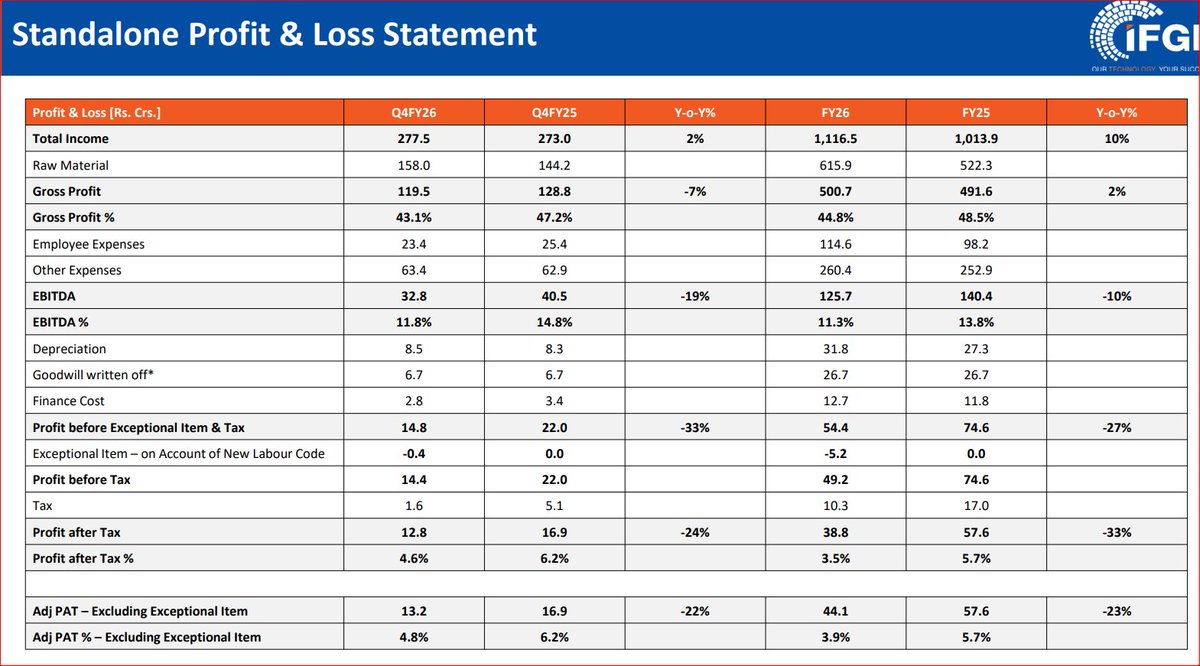

IFGL Refractories Ltd - Q4FY26 | Concall Insights

Financial Highlights

•Q4FY26 consolidated total income increased 7% YoY to INR486 crore

•FY26 consolidated total income grew 14% YoY to INR1,904 crore

•Q4FY26 standalone total income stood at INR278 crore with 2% YoY growth

•FY26 standalone total income increased 10% YoY to INR1,117 crore

•Adjusted FY26 consolidated PAT stood at INR40 crore excluding exceptional items

Revenue

•Domestic business revenue grew 20% YoY in FY26 to INR864 crore

•Domestic business delivered 7% YoY growth in Q4FY26 driven by market share gains

•Export revenue declined 11% in FY26 due to geopolitical uncertainties and weak overseas demand

•US market revenue grew 26% YoY in Q4FY26 and 25% YoY in FY26

•Management targeting double-digit domestic growth in FY27 supported by steel capacity expansion

Margins & Profitability

•Q4FY26 standalone EBITDA stood at INR32.8 crore with 11.8% margin

•FY26 standalone EBITDA stood at INR126 crore with 11.3% margin

•Q4FY26 consolidated EBITDA increased 13% YoY to INR42 crore

•US subsidiary margins improved to high-teen levels during FY26

•Margins impacted by elevated raw material costs, lower export contribution and product mix changes

Business Strategy

•Company strengthening leadership structure with dedicated India and International CEOs

•Focus shifting towards full-range refractory solution model and total refractory management services

•Growing preference among steel companies for integrated refractory solution providers benefiting IFGL

•Company targeting higher market share across steel, cement, foundry and non-ferrous segments

•Strategic focus remains on operational efficiency, innovation, customer engagement and profitable growth

Product Development

•Phase 1 of Sheffield Refractories technology transfer to India completed successfully

•Product recipe transfer, joint development and knowledge sharing activities completed

•Sheffield plastic ramming mass manufacturing introduced at Vizag facility

•Commercial trials for transferred technologies expected by end-FY27

•Company focusing on complementary product expansion across isostatic refractories and advanced solutions

Capacity Expansion

•Greenfield Khurda Odisha project work has picked up pace

•Board evaluating pace and structure of future investments prudently

•Vizag facility successfully completed first EOF campaign with indigenous lining system

•Company investing in R&D, Vizag and Rourkela facilities to capture future steel growth

•Bhachau project focused on cement and basic brick opportunities progressing gradually

International Business

•Americas business continues to witness strong growth and profitability improvement

•Mexico and Latin America emerging as attractive long-term growth opportunities

•Hofmann Ceramics losses reduced significantly with breakeven targeted during FY27

•Monocon targeting breakeven by Q4FY27 through new products and geographic expansion

•Europe and UK demand environment showing gradual recovery supported by manufacturing and defence investments

Other Updates

•Consolidated debt stood at INR195.6 crore as of March 2026

•Cash and cash equivalents stood at INR122 crore providing financial flexibility

•Working capital cycle improved with inventory levels declining sequentially

•Annual goodwill amortization charge of INR26.7 crore to cease from FY27 onwards

•Board recommended dividend of INR2.15 per share reflecting disciplined capital allocation

130

Jun 3

IFGL Refractories Ltd Concall Summary for Q4FY26

MANAGEMENT COMMENTARY

FY26 delivered strategic progress.

Revenue execution remained strong.

Leadership transition handled smoothly.

Domestic market gaining focus.

Technology transfer progressing well.

Repeated Focus:

India growth story

Technology transfer

Domestic market expansion

Operational continuity

GUIDANCE & OUTLOOK

Domestic volume growth double-digit.

International orders improving.

Profitability showing stabilization.

Monocon breakeven by Q4FY27.

Technology transfer entering trials.

Near-term Visibility:

Strong domestic demand.

Export orders improving.

Recovery signs emerging.

INDUSTRY & MACRO ENVIRONMENT

Global steel demand stabilizing.

India remains growth driver.

Infrastructure demand rising.

Manufacturing activity expanding.

Headwinds:

West Asia tensions.

LPG supply disruptions.

Freight inflation.

Shipping cost volatility.

Tailwinds:

India infrastructure growth.

Manufacturing expansion.

Domestic steel demand.

COMPETITIVE POSITIONING

Total refractory management model.

Integrated solution provider.

Strong technical capabilities.

Market share gains visible.

Strategic Advantages:

EOF technology success.

Wide product portfolio.

Application expertise.

Global technology access.

RISKS & CONCERNS

Imported mineral dependence.

Freight cost volatility.

Logistics disruptions.

Geopolitical uncertainty.

Leadership transition concerns.

Repeated Concerns:

Shipping costs.

Raw material sourcing.

West Asia disruptions.

GROWTH DRIVERS & STRATEGIC INITIATIVES

UK technology transfer ongoing.

Domestic market expansion.

Non-ferrous diversification.

Odisha project progressing.

Product localization increasing.

Strategic Initiatives:

Sheffield technology transfer.

Cement segment expansion.

Glass segment entry.

Aluminium segment focus.

PRODUCT MIX & PORTFOLIO

Domestic business grew 20%.

US business grew 25%.

Export revenue declined 11%.

Europe remains weak.

Non-ferrous portfolio expanding.

Higher value solutions growing.

FINANCIAL SNAPSHOT

Revenue: ₹1,904 Cr ( 14%)

EBITDA: ₹146 Cr

EBITDA Margin: 7.7%

Debt: ₹195 Cr

Cash: ₹122 Cr

Working Capital: Improved

Inventory: Elevated levels

Notable Shift:

Domestic market prioritized.

Export dependence reducing.

India-led growth strategy.

CONCLUSION

FY26 marked strategic transition.

India business gaining momentum.

Technology transfer progressing well.

US operations improving strongly.

Export challenges persist.

Logistics remain key risk.

Domestic growth outlook strong.

#stockmarket #Q4FY26 #Q4Results #IFGLRefractories #IFGL

2

5

316

Jun 3

Time to accumulate :

Birlasoft around 328

Newgen around 500-515 range

Dynamic cables around 310

IFGl around 195

1

3

36

3,317

IFGL Refractories (#IFGLEXPOR) has recommended a final dividend of ₹2.15 per share for FY26.

Record Date - July 29

Share Price - ₹176

Dividend Yield - 1.3%

Basic EPS - ₹5.4

Payout Ratio - ₹40%

Payment Date - TBA

Dividend History

FY26 - ₹2.15

1:1 Bonus

FY25 - ₹7

#Dividend

5

515

Jun 1

Some more good numbers were declared over the weekend.

Good Numbers

Hardwyn India

NMDC

Olectra Greentech

Rubicon Research

Fiem Industries

IFGL Refractories

Fantastic Numbers

NIBE

Gufic BioSciences

#Q4results

May 29

Some fantastic Q4 results were declared yesterday:

Bajel Projects Ltd

Marine Electricals (India) Ltd

Supriya Lifescience Ltd

As the Q4 earnings season comes to an end, several companies continue to show strong growth.

As retail investors, our job is not to chase every result, but to identify the best among the lot - companies where earnings visibility is strong and growth can sustain in the coming quarters.

Sustainable growth creates wealth.

#StockMarket #EarningsSeason

1

42

5,197

⚖️ MIXED / NEUTRAL

• UFLEX

• Kiri Industries

• Apex Frozen Foods

• Suraj Estate Developers

• Panacea Biotec

• IFGL Refractories

• MSP Steel & Power

• Gujarat Gas

• Deepak Builders & Engineers India

Key Observation:

Many companies reported numbers that were neither strong enough to drive re-rating nor weak enough to damage the long-term thesis.

The next few quarters will matter more than this quarter. Markets eventually follow the direction of earnings.

Educational purpose only. Not investment advice. Please do your own research before investing.

5

736

May 31

Companies which posted Strong #Q4FY26 Results on Saturday (30-5-2026)

Amic Forging

Blue Cloud Softech

Confidence Petroleum

Fiem Industries

IFGL Refractories

Jeena Sikho Lifecare

MSP Steel & Power

PTC Industries

Signpost India

Sunrakshakk Industries

Tenneco Clean Air

Titan Biotech

Uflex

Valiant Communicatios

Veranda Learning Solutions

Vishnu Chemicals

*I mostly cover Companies having >1,000 Cr M.Cap

This Marks the End of Q4FY26 Earnings Season, A Good One.

#ResultSeason

3

1

51

6,160

May 31

#Q4FY26 Mainboard #results on 30th May -

Solid Set –

Sunrakshakk (#Sunrakshak )

Signpost (#Signpost )

MSP Steel (#MSPL )

PTC inds (#PTCIL )

CWD (#CWD )

SMT Engg (#SMTEL )

Good/Decent Set –

Fiem (#FiemInd )

DC Infotech (#DCI )

Bharat Gears (#BharatGear )

Vishnu Chemicals (#Vishnu )

Jeena Sikho (#JSLL )

IFGL Refractories (#IFGLExpor )

Valiant Comm (#Valiant )

Star Delta Trans (#StarDelta )

Shree Vasu Logistics (#SVLL )

Vipul Organics (#VipulOrg )

Thomas Scott (#Thomascott )

Titan Bio (#TitanBio )

Veranda (#Veranda )

DHP India (#DHPInd )

Uflex (#Uflex )

Fluidomat (#Fluidom )

Competent Auto (#CompeAu )

Coral Labs (#Coralab )

PIGL (#PIGL )

Tenneco Clean Air (#TennInd )

Coastal Corp (#CoastCorp )

Confidence Petro (#ConfiPetro )

Blue cloud Softtech (#BlueClouds )

One Global (#OneGlobal )

Turnaround –

Aarey Drugs (#AareyDrugs )

1

16

1,478