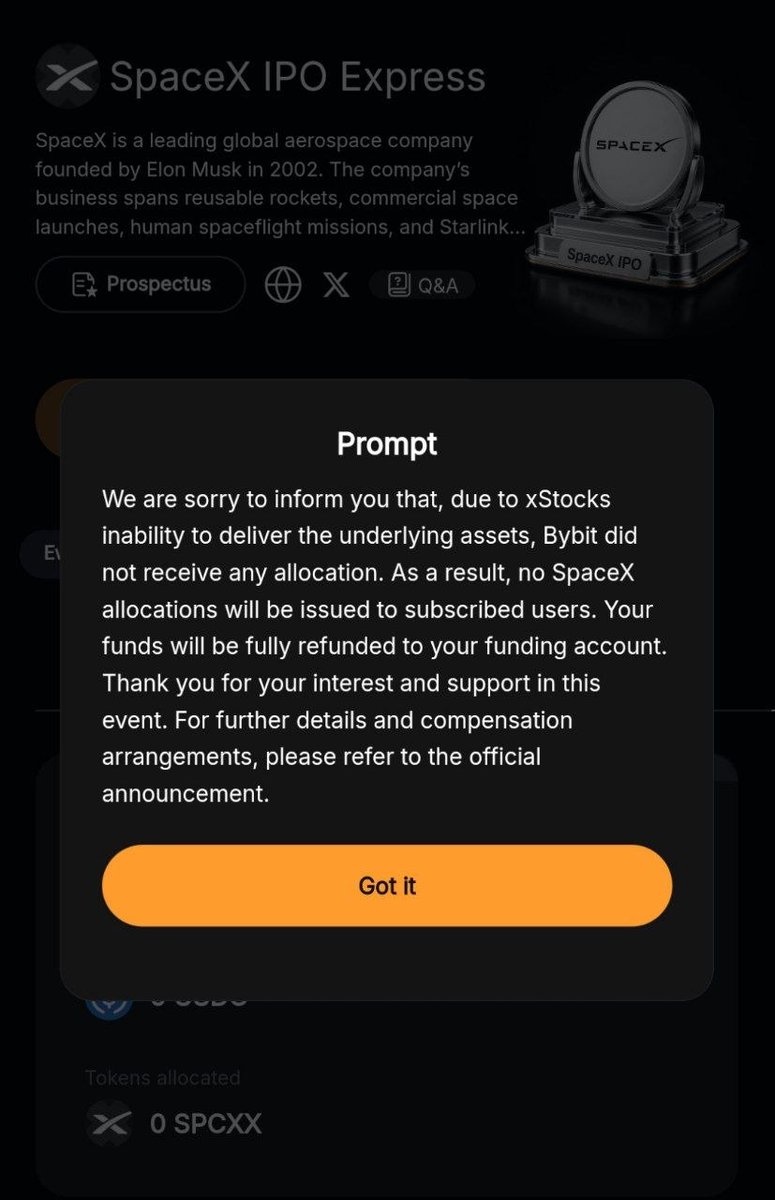

Jun 13

Locked $107 in @Bybit_Official IPO Express and got only $0.11 allocation. That's not an investment opportunity it's a joke. Retail users deserve transparency about realistic allocations before locking funds. This level of reward destroys trust #Bybit #IPOExpress

1

1

18

🚀 SpaceX IPO Lands Today – Historic Milestone!

SpaceX (ticker: SPCX) completed the largest IPO in history on June 12, 2026, raising $75 billion at $135 per share. Shares jumped strongly in debut trading (opened around $150), pushing market cap past $2 trillion.

Key Takeaways:

• SpaceX: “Turn impossible things into possible” — dual-listed on Nasdaq and Nasdaq Texas.

• Elon Musk: Celebrating in Texas as visionary leadership continues to shape the era — on track to become the world’s first trillionaire.

• Gwynne Shotwell: President & COO powerhouse ringing the bell at Nasdaq in New York — steady operational excellence behind the scenes, helping steer the company forward.

• Goldman Sachs, Morgan Stanley, Bank of America, Citigroup & JPMorgan Chase: Lead underwriters who flawlessly executed this record-breaking deal.

• My Fellow Investors: Congratulations on our positioning in the space/tech ecosystem — a significant milestone achieved. The future looks bright!

2026 is destined to be a banner year for IPOs — Cheers!

Video sources: SpaceX, Nasdaq, Goldman Sachs, Morgan Stanley, IPOEXPRESS

#SpaceX #SPCX #IPO #ElonMusk #Starlink

2

78

SpaceX IPO: The Numbers Are In 🚀

After working through the full prospectus, my verdict: SpaceX is worth ~$97.83/share (~$1.3T equity) — but it’s pricing at $135 (~$1.8T). Overvalued by 38%.

What the prospectus revealed:

•2025 revenue hit $18.7B ( 33% YoY). xAI came in 32× higher than I estimated — $3.2B vs. ~$100M.

•Capital structure: $22.9B debt, but offset by $24.7B cash → net debt slightly negative.

The three businesses, three different stories:

•🛰️ Connectivity (Starlink) — the crown jewel. 50% revenue growth, operating margin jumped from 17% → 39%. Best risk/reward of the trio.

•🚀 Space — strongest unit economics (67% gross margin), reusability driving improvement. R&D-heavy but should level off.

•🤖 AI (xAI) — the swing factor. Massive TAM optionality but worst margins and most capital-intensive. This is where the bull/bear case lives or dies.

The DCF math(via my Professor Aswath Damodaran framework): $400B revenue target by 2036, 8.25% terminal cost of capital → $1.3T equity value, $97.83/share.

Bottom line: The market is paying for an aspirational outcome. Intrinsic value supports ~$98, not $135.

•Investors: Pass at the rumored price. A pass at IPO ≠ never own — let price come to value(We invested earlier and participated IPO round also. Will hold long-term definitely).

•Traders: A pop at $1.8T is entirely plausible. Don’t short — mood beats math short-term.

This is a leveraged bet on futuristic tech and on Musk personally. For some that’s disqualifying; for others, his Tesla track record tilts the odds. Both views are legitimate — price them into your position.

My number: $97.83. The market may say $1.8–2T. Both can be defended — but only one belongs in a long-term portfolio at the offer.

— Jackson | IPOEXPRESS

1

125

Jun 9

❗️The Bybit cryptocurrency exchange has announced the launch of the Bybit IPO Express platform, which allows retail investors to purchase tokenized shares of companies at their initial public offering price.

#Bybit #IPOExpress #SpaceX #xStocks

32

#Bybit launched #IPOExpress, the second crypto exchange to offer tokenized IPO access after #Kraken. Inaugural offering: #SpaceX's $75B IPO at $1.75T valuation. Registration June 7-11, trading starts June 12. Powered by xStocks. Backed 1:1 by actual equity. #tokenization

1

21

Jun 8

我朋友上个月跟一个圈内大佬好上了

朋友圈晒LV下午茶 晒头等舱 晒维多利亚港夜景

配文”遇见对的人 才知道之前都是浪费时间”

我作为多年观察家 当时就觉得不对劲

果然 上周她半夜给我打电话哭“姐 我说有没有什么赚钱的可以带带我的 可他说要带我打新 SpaceX 让我先转 50 万过去帮我操作 我也想小额试水 但是他说小额根本没办法操作……”

我说停 你别说了

不管这个人有没有问题 转这么大数额都不太靠谱 你没必要让他帮你操作

第一没必要让他操作 第二是因为打新 SpaceX 这种事 没必要非50万

今天 100 USDC 就能做🫡

Bybit 刚正式上线了链上美股 IPO 打新产品

Bybit IPO Express

首发标的 就是全网最炸的 SpaceX

而且他不是币圈那种 SPV 模式的”Pre-IPO 代币”

那种东西本质是离岸空壳公司 一纸对赌协议

SpaceX、OpenAI 历史上都明确拒认过类似份额

2026 年 5 月 OpenAI 拒认 SPV 后 相关代币直接暴跌 40%

Bybit IPO Express 走的是完全不一样的路线

1. 1:1 真实股票打新

2. 和 Robinhood、Alpaca、xStocks 三方合作

3. 流程、定价、分配逻辑 跟传统券商打新一模一样

4. xStocks 还是 Bybit 合作的首家中心化交易所

而 xStocks 本身就是和 Alpaca 深度合作的合规发行方

正规军路线 不是空气对赌🫡

机制设计也很干净——

1. 100 USDC 起步 全球潜力 IPO 入场门槛打到地板

2. USDC 直接打新 不用开海外券商户 不用走 SWIFT

3. 按比例 Pro-rata 分配 公平 透明

4. 未中签自动退款 0 手续费 0 摩擦

5. 认购完成后 直接在 Bybit 现货市场无缝交易

为什么这事重要

过去打新 SpaceX 这种顶级一级资产

是只有美国机构 LP、华尔街内部圈层才能玩的游戏

普通人根本拿不到门票

而现在 100 U 就能上桌

最后回到我闺蜜

我让她打开 Bybit 自己注册

然后把那个”大佬”删了

姐妹们记住

真正能让你打新 SpaceX 的不是某个男人

是 Bybit IPO Express🫡

@Bybit_ZH @benbybit

#Bybit #IPOExpress #SpaceX

170

69

21,713

🚀 Bybit Launches Tokenized IPO Platform Debuting with SpaceX

Bybit introduced IPO Express, a platform that allows crypto exchange users to gain tokenized exposure to companies before they go public. The debut listing is SpaceX, one of the most closely watched private companies globally.

The platform gives access to assets traditionally reserved for institutional investors, offering synthetic or tokenized exposure rather than direct equity ownership. This involves different risk profiles, including custody and counterparty considerations, compared to standard brokerage accounts.

Selecting SpaceX for the launch emphasizes the product’s seriousness and its role in the growing tokenized real-world asset space. IPO Express also puts competitive pressure on other centralized exchanges and reflects the trend of integrating traditional financial products into crypto platforms.

🎓 At Cryptemic Academy, we explore how tokenized real-world assets and IPO-stage products can open institutional-grade opportunities to retail investors in the crypto space.

Full text is available on our news portal cryptemic.com

#cryptemic #cryptemicacademy #crypto #IPOExpress #Bybit #SpaceX

1

1

436

Jun 8

最近试了 Bybit 刚上线的 IPO Express,说实话有点惊喜。整个参与流程在Bybit里就能完成,不需要额外开任何券商账户,直接用账户里的 USDC 去认购。门槛也比我想象的低,最低 100 USDC 就能参与,普通用户完全够得上。

分配机制是按比例(Pro-rata)来的,意思是你的认购金额占总需求的比例决定你能分到多少,不是先到先得,也不是抽签碰运气,相对公平。如果超额认购导致你没有完全中签,多余的资金会自动退回账户,不会被平台占用,这点我觉得做得挺到位的。

认购结束之后,也不用等什么转仓、解锁之类的操作,直接就能在 Bybit 现货市场交易,整个链路非常顺滑。

有一点我觉得很重要,必须单独说——这不是那种市面上随处可见的 Pre-IPO 对赌产品。那类产品本质是 SPV 结构,你买的是一个合同权益,底层资产不透明,风险极高。Bybit IPO Express 背后走的是 xStocks 的合规路线,1:1 真实股票托管在受监管机构,符合欧盟 MiFID II 标准,安全性和你在传统券商打新是同一个级别,这才是我愿意真金白银参与的原因。

现在市场上全球 IPO 的机会越来越多,SpaceX、各种科技独角兽都在排队,Web3 人不应该因为渠道问题就一直缺席。Bybit IPO Express 算是真正给加密用户补上了这块拼图。

👇 点击链接参与 Bybit IPO Express:bybit.com/en/trade/spot/ipo

@benbybit @Bybit_ZH #Bybit #IPOExpress #xStocks #打新 #Web3投资

104

5

10,094

🚀 SpaceX 要 IPO 了,你打算怎么上车?

过去打美股 IPO,你要:

❌ 传统券商繁琐开户

❌ 资金出入金受限

❌ 错过最佳认购窗口期

现在 Bybit IPO Express 改变了这一切——

✅ 最低 100 USDC 即可参与全球 IPO 认购

✅ 无需开设任何传统券商账户

✅ 认购结束即可直接在 Bybit 现货市场交易

✅ 按比例公平分配(Pro-rata),未中签资金自动退还

🔒 而且这不是什么空气盘。

Bybit xStocks 背后是 1:1 真实股票托管于合规机构,由受监管发行方(Backed Finance)发行,符合 MiFID II 欧盟监管标准。跟你在传统券商买到的股票,是同一个逻辑——只是门槛更低、效率更高、24/7 随时可交易。

👇 点击链接参与 Bybit IPO Express:bybit.com/en/trade/spot/ipo

#Bybit #IPOExpress #xStocks #SpaceX @benbybit @Bybit_ZH

53

3

8,322

🚀 Trải Nghiệm Đặc Quyền VIP Cùng Bybit

Nếu anh em đang giao dịch khối lượng lớn hoặc đã là VIP trên các sàn khác, đây là thời điểm rất đáng để trải nghiệm hệ sinh thái VIP của Bybit.

✨ Những quyền lợi nổi bật dành cho khách hàng VIP:

💳 Hoàn tiền lên đến 10% với Bybit VIP Card

Nhận cashback cho các giao dịch và chi tiêu đủ điều kiện.

🚀 Ưu tiên tham gia IPO Express

Cơ hội tiếp cận các đợt IPO Express hấp dẫn đang được thị trường quan tâm, nổi bật là SpaceX.

👤 Quản lý tài khoản VIP riêng

Hỗ trợ 1-1 từ đội ngũ VIP Manager.

Hỗ trợ nhanh chóng các vấn đề liên quan đến giao dịch, nạp rút và sản phẩm.

🎁 Đặc quyền sự kiện và phần thưởng VIP

Ưu tiên tham gia các chiến dịch thưởng độc quyền.

Nhận quà tặng giới hạn và các đặc quyền dành riêng cho khách hàng VIP.

⭐ VIP 2 Status Match

Đang là VIP hoặc các sàn khác?

Bybit hỗ trợ nâng hạng lên đến VIP 2 để anh em tận hưởng quyền lợi tương đương ngay từ ngày đầu tiên.

👉 Trở thành VIP nhận ưu đãi 2 cấp VIP và được mua nhiều IPO hơn: forms.gle/vUwj7w1G5XLF8cbw8

Trong thời gian gần đây, Bybit liên tục mở rộng các sản phẩm dành cho nhà đầu tư chuyên nghiệp như IPO Express, RWA, xStocks và các chương trình ưu đãi riêng cho khách hàng VIP.

Anh em quan tâm có thể để lại comment hoặc inbox để được hỗ trợ kiểm tra điều kiện nâng cấp VIP và nhận các ưu đãi mới nhất từ Bybit. 🔥

#Bybit #BybitVIP #VIP99 #SpaceXIPO #IPOExpress #Crypto #Trading #RWA #xStocks #BybitCard

320

Jun 8

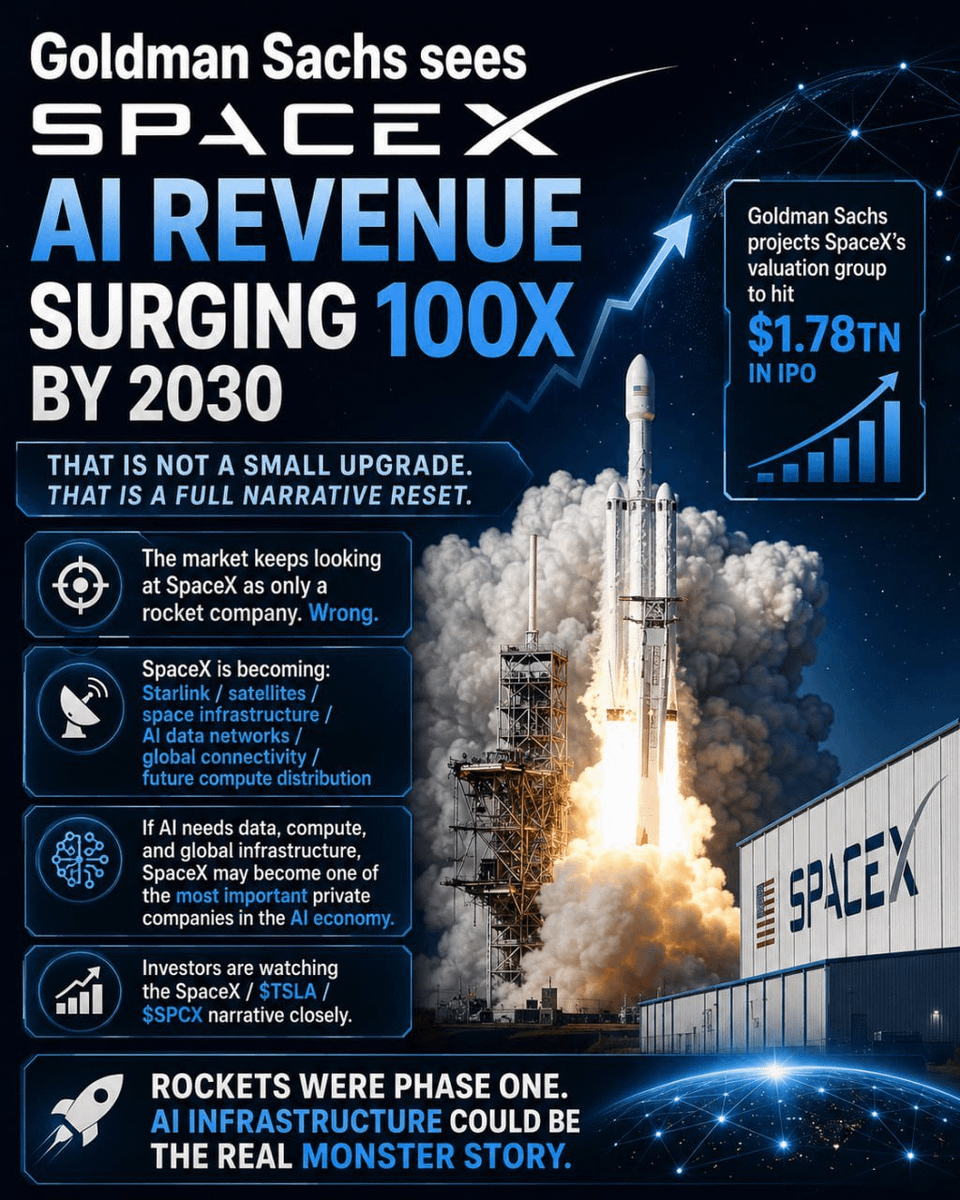

SpaceX打新,建议人人都要参与!🧐

高盛最近给SpaceX做了一个夸张的定调,他们预测,SpaceX的AI收入会从25年的32亿美金,暴涨到2030年的3220亿美金,将会成为一家市值30万亿美金的公司。我的天啊,4年时间,收入翻100倍,股价翻超15倍(如图2)!

这种机会,讲真的,一辈子可能就那么一次!

更劲爆的是,#Bybit 上,现在直接可以参与SpaceX的打新了!这可不是什么币圈Pre-IPO那套割韭菜的玩法,是正儿八经的美股IPO打新渠道。我讲讲其中的区别!👇

📊 这个代币化IPO到底是啥?

很多人一听"代币化IPO",脑子里就想到币圈那些乱七八糟的Pre-IPO,什么SPV结构、私募折价、锁仓18个月、项目方自己随便定价……您先把这些忘了,完全不是一回事。

Bybit这次跑通的路径是这样的:

• Robinhood 作为零售端已经拿到了SpaceX IPO的分配资格

• Alpaca 提供底层券商通道

• xStocks 做代币化中间层

• Bybit 是第一家接入xStocks的CEX

咱们通俗点说,分配逻辑、定价逻辑,跟您在美国用Robinhood打新走的是同一条供应链。这不是什么币圈的野路子,是正规的传统金融管道。

💡 门槛降了,机会来了

以前咱们想打美股新股,门槛高得吓人:

• 得开美国券商账户,SSN或者一堆繁琐KYC

• 账户得有足够的交易历史或者资产门槛

• 热门IPO散户基本没啥分配权,都被机构吃了

现在路径变了:

• 完成Bybit KYC,成为VIP或PRO

• 用USDC直接认购

• 按比例分配,没中的资金自动退回

• 认购完直接在Bybit现货市场交易,不用等着转仓

这对咱们华语用户来说,讲真的,实在太友好了,也算是第一次能以接近机构级别的进货渠道参与美股打新,而且是实打实的传统金融资产。

🚀 SpaceX只是开始

SpaceX是第一个,但绝对不是最后一个。xStocks的逻辑打通之后,后面能接入的IPO标的理论上可以持续扩展。

未来但凡有重量级IPO,OpenAI、Stripe、Anthropic……有Bybit VIP账户的小伙伴,都能参与其中,想想都让人兴奋,赶紧搞起来!

📌 参与条件:

• KYC 完成

• 主账户成为VIP或PRO用户

• 用USDC认购

入口:bybit.com/trade/spot/ipo

总结来说,这次Bybit算是开了个头,把Web3的基础设施和传统金融的IPO打通了。这个窗口,我觉得值得认真对待。这次机会,我个人觉得挺香的。DYOR🙏

@Bybit_ZH #Bybit #IPOExpress

25

10

46

208,811

Jun 8

CRYPTO BREAKING NEWS: Only the latest. No repeats 💙

• Bybit Launches IPO Express With Tokenized Access to SpaceX.

• Bitcoin Pushes Above $63,000, Trimming Losses From A Savage Selloff.

• The Altcoin Rocket May Have Already Launched Why These 4 Altcoins Are Emerging as Top Picks for Explosive Gains.

• EUR/JPY Rebounds from Triangle Support: Technical Outlook Near 185.00.

• Goldman Sachs Sees Fed Holding Rates Steady Through 2026.

• US Dollar Index Holds Near 100.00 as Middle East Tensions and Fed Rate Hike Bets Collide.

• Silver Price Drops Near $67.50 as Oil Weakness and Fed Rate Worries Weigh.

• Israeli Air Force Strikes Military Targets in Western and Central Iran After Missile Attacks.

• Peter Schiff Pushes Back on Jamie Dimon’s Crypto Capital Rule Call.

• Syscoin Suspends Bridge Operations After Unauthorized Minting of 5 Billion SYS Tokens.

• Bitcoin Set for Short-Term Rebound After Spot-Driven Sell-Off, 10X Research Says.

• Bitcoin Enters ‘Extremely Undervalued’ Zone, On-Chain Analyst Says: A Window for Long-Term Accumulation.

• Canadian Dollar Slips to Late-March Low Against US Dollar Despite Rising Oil Prices.

• New Zealand Dollar Rebounds Toward 0.5800 as Risk Appetite Improves.

Powered by neome.com

#BTC #SYS #ALTCOINS #CRYPTO #DEFI #IPOEXPRESS #SPACEX #TOKEN

1

140

Jun 7

🚀 Bybit's first-ever IPO Express is now LIVE with SpaceX!

In collaboration with @xStocksFi and @krakenfx, Bybit brings one of the most compliant and secure ways to gain exposure to a SpaceX pre-IPO opportunity.

✅ 1:1 stock-backed

✅ Compliant structure

✅ Secure access

✅ Available directly on Bybit

Join now:

bybit.com/en/trade/spot/ipo/…

#Bybit #SpaceX #IPOExpress #xStocks

64

62

4,588

Jun 7

Game changer! Bybit just opened tokenized SpaceX IPO access via IPO Express. Retail investors can now subscribe to one of the biggest IPOs ever at offering price — no Wall Street needed. The future of finance is here. " #Bybit #SpaceX #SPCX #TokenizedIPO #Crypto #IPOExpress

1

45

Jun 7

最近 SpaceX 打新熱度很高。很多平台上的 Pre-IPO 產品,底層可能是 SPV、合成敞口,甚至只是平台自己做的一層映射。這類產品最大的問題是:用戶以為自己買到的是未上市股票機會,實際上拿到的可能只是平台承諾。

所以這次 Bybit 推出的 IPO Express,我覺得值得看看。

這次首發項目是 SpaceX,參與方式很簡單:

用 USDC 認購

最低門檻 100 USDC

認購後按照最終配額分配

6 月 12 日上線後,可在 Bybit 現貨市場交易 xStocks

這個模式更接近傳統美股券商的 IPO 認購邏輯,對 Web3 用戶來說,最大的改變就是門檻降低了。

以前想參與美股打新,通常需要券商帳戶、資格審核、資金出入金流程,很多人連入口都摸不到。現在透過 Bybit IPO Express,用加密資產帳戶和 USDC 就能參與,流程會簡單很多。

時間也比較緊:

6 月 7 日 - 6 月 11 日:開放認購

6 月 12 日:SpaceX xStock 現貨上線

當然,這類產品依然要看配額、分配規則和上市後市場波動,不能直接當成穩賺機會。

但如果你本來就關注 SpaceX、美股 IPO、代幣化股票,那 Bybit IPO Express 這次確實可以研究一下。

🔗 參與入口:

bybit.com/zh-MY/trade/spot/i…

#Bybit #IPOExpress #xStocks #SpaceX #美股打新

7

7

10,321

Jun 7

Bybit just opened tokenized IPO access to the masses 🤯

SpaceX is first — IPOs are coming on-chain 🔗

Curious? Check it out: kanalcoin.com/p/bybit-launch…

#Bybit #IPOExpress #CryptoNews

409

Jun 7

Разрыв шаблона: Bybit запускает токенизированное IPO SpaceX» 🚀💳

Срочная и супер-хайповая новость дня, которая идеально дополняет твой фокус на космические технологии и деривативы.

RU: Крипта окончательно стирает границы с реальным бизнесом. Сегодня Bybit официально запустил платформу IPO Express, и первым доступным активом стали... токены акций SpaceX Илона Маска! 🚀

С сегодняшнего дня по 11 июня открыто окно подписки, где можно подать заявку на покупку долей SpaceX по официальной цене предложения до её выхода на Nasdaq.

Помните, мы обсуждали Pre-IPO фьючерсы на Binance? Тренд на «акции внутри крипты» официально стал главным драйвером июня 2026 года. Традиционный рынок и блокчейн сливаются в одно целое. Те, кто считает крипту просто «фантиками», пропускают исторический момент. 🛡️💻✨

EN: Crypto is merging with traditional finance faster than you think. Today, Bybit launched IPO Express, offering tokenized access to Elon Musk’s SpaceX shares at the official offering price before the Nasdaq debut!

The subscription window is open until June 11. The tokenized equity trend we discussed with Binance Pre-IPO perps is officially taking over June 2026. Don't blink. 🛡️💻✨

#SpaceX #Bybit #IPOExpress #PreIPO #TokenizedEquity #ElonMusk #CryptoNews2026

2

78

Jun 7

最近关于 SpaceX IPO 的讨论越来越多。说实话,以前散户想摸到这种顶级资产的入场券,门槛高得像堵墙:开海外券商、跨境入金、等审核,折腾半天往往连资格都拿不到。

去了解了一下 @Bybit_ZH 新推的 IPO Express,思路很直接,直接把传统券商那套繁琐流程变成了我们最熟悉的链上玩法:

⚡ 极低门槛:无需传统券商账户,KYC1 的 VIP 或 PRO 用户最低 100 USDC 就能参与。

🛡️ 真实底层:不是虚的 SPV 结构,而是由真实股票份额支持。按比例分配,未中签资金自动退回。

🔄 闭环交易:认购完直接在 Bybit 现货市场开盘交易,从打新到变现一条龙打通。

以前是我们费劲去适应复杂的金融系统,现在是顶级资产直接变成了用 USDC 就能参与的轻量游戏。从最初只能站在场外围观科技巨头的盛宴,到今天能用最熟悉的方式提前锁定全球上市红利,这种打破圈层边界的真实体感,确实挺让人期待接下来的明星项目。

🔗 入口:bybit.com/en/trade/spot/ipo/

🔗注册点这里: partner.bybit.com/b/132706

#SpaceX #IPO #Bybit #IPOExpress

57

8

53

7,191

Jun 7

🚨 史上最大 IPO,这次散户能跟机构同价上车

SpaceX。6 月 12 号。纳斯达克。代码 SPCX。 发行价 135 美元,估值约 1.77 万亿——人类历史上最大的一次 IPO,没有之一。

以前这种盛宴轮得到散户吗?券商开户、跨境入金、地区限制……等你全搞定,股价早飞了。

这次真不一样。Bybit @Bybit_Official IPO Express:账户里的 USDC,直接按 IPO 发行价认购,跟机构同一个价进场。SpaceX 就是开门第一单。

最要命的是——认购登记窗口只有 6/7–6/11,就这几天,过了只能去二级市场追高。

而且千万别拿它跟那些 pre-IPO 空气币混为一谈。5 月那波还记得吧?OpenAI、Anthropic 一句"未经批准的 SPV 份额无效",几个相关代币一周蒸发近 40%,高位接盘的全套牢。IPO Express 完全是另一回事:上市当天 1:1 对应受监管托管里的真实股票,你拿的是真资产,不是等归零的对赌敞口。

门槛还低到离谱: 💰 最低 100 USDC 就能进 ⚖️ 按比例分配,没中签自动原路退回 🆓 零额外认购费(可能有点网络费)

波动肯定有,别上头梭哈、按自己仓位来——但这种名额,过了这村真没这店。 我已经把名额登记上了,想上车的抓紧 👇

🥇 Bybit(我最常用,有财VIP最高返佣 35%) 🔗 partner.bybit.com/b/yc888邀请码:YC888

#SpaceX #Bybit #IPOExpress #xStocks #打新

18

3

11

2,448