10h

Citizens reiterated $CRNX Market Outperform; $95 and assigned atumelnant a 70% POS in CAH and 50% in Cushing's, w/ combined peak sales pot'l of $1.5B after CRNX's presentations at ENDO2026.

$BBIO NBIX $NVS RICFY PFE IPSEY AZN

Citizens said: CRNX took center stage at ENDO, with updates providing further support of Palsonify during its early launch phase in acromegaly, as well as updates for atumelnant in both CAH and Cushing's.

Palsonify continues to reinforce its best in class efficacy profile with durable-two-year OLE data validating it as a compelling alternative to long-acting injectable SSAs

Early launch dynamics remain highly encouraging, with ~$10M in 1Q sales (doubling Q/Q) and a steadily expanding prescriber base, supporting our view that the once-daily oral will continue to capture market share from legacy injectables.

We model 2026 sales of ~$65M (vs. $70M consensus).

Meanwhile, full Phase 1/2 data further strengthen the case for atumelnant, supporting the potential of its selective MC2R antagonist mechanism to deliver improved efficacy in both CAH and Cushing's with new model-informed analysis predicting robust, dose-dependent reductions in key androgen biomarkers in the ongoing Phase 3 trials. We assign atumelnant a 70% POS in CAH and 50% in Cushing's, with combined peak sales potential of ~$1.5B.

Jun 11

Citizens reiterated $CRNX Market Outperform: $95~says $CAMRF update an incremental VE for Crinetics—nonetheless it views Oclaiz as a non-threat to Palsonify.

$NVS RICFY PFE IPSEY AZN

Citizens said: Camurus' CRL is primarily related to manufacturing so we expect it can be resolved over time, but FDA may need to reinspect its third-party manufacturer and scheduling may result in an even further delay.

We view the update as an incremental positive for CRNX; however, we did and do not view Oclaiz as a major competitive threat to Palsonify.

Oclaiz is still a monthly injectable SSA and has advantage of self-administration over approved injectables but is still an injection, and we still anticipate a waning of effect toward the end of a treatment cycle.

Palsonify's daily oral convenience and super efficacy and safety profile should make it a preferred option for most acromegaly patients.

Palsonify's early launch metrics have looked strong with >430 start forms as of 1Q26, ~70% of patients on paid drug already, and $10M in 1Q26 sales.

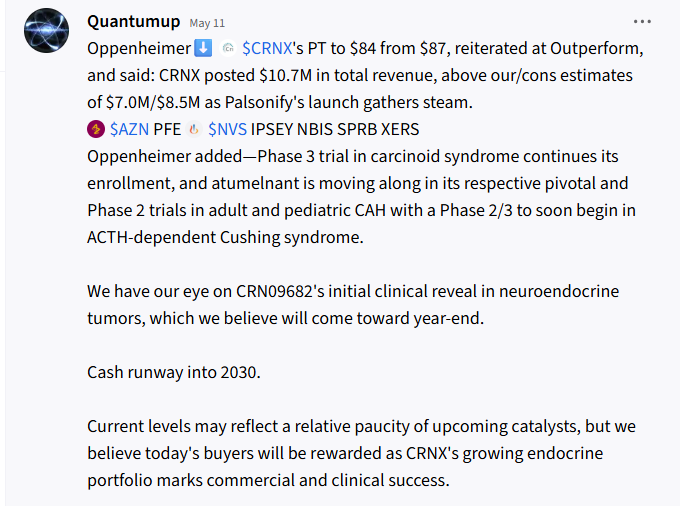

Oppenheimer from May 11, in image:

1

4

1,114

Jun 12

$IPSEY $CMPX $STTK

Ipsen ImChecks into pivotal development

- The gammadelta T-cell activator IPN60340 will start a phase 2/3 trial this year apexonco.com/ipsen-imchecks-…

164

Jun 12

$IPSEY

Ipsen R&D chief on pipeline discipline, partnerships and 2026 milestones

- Ipsen’s approach to partnering is described as being an “accelerator” that helps move promising science from academic labs and biotech partners toward patients. fiercebiotech.com/biotech/ip…

88

Jun 11

Stifel on $ORIC said: We resume coverage of ORIC Pharmaceuticals with a Buy Rating and a $14 target price.

$PFE $JNJ IPSEY DSNKY

Stifel added—ORIC's lead asset, rinzimetostat, is a PRC2 complex inhibitor being developed in combination with darolutamide in metastatic castration resistant prostate cancer (mCRPC) — a Ph3 clinical trial (Himalayas-1) is expected to initiate in June/July 2026 in mCRPC patients previously treated with abiraterone.

Logic for the combination is PRC2 inhibition blocks/reverts epigenetic reprogramming, resensitizing prostate cancer cells to androgen receptor pathway inhibitors (ARPIs) like darolutamide.

ORIC has cash runway out to 2H28, getting them through Himalayas-1 top-line data expected in early 2028.

May 15

Goldman Sachs➡️ $ORIC from Early-Stage Biotech to a Buy rating and a $15 PT.

$PFE IPSEY VIR CADL BAYRY NVS $JNJ

Goldman Sachs said in its note:

We move ORIC to a Buy rating (from Early Stage Biotech) following clinical data which demonstrated a potentially differentiated profile for rinzimetostat in prostate cancer (GSe: $2.6B peak sales), and ahead of key de-risking Ph3 data for the class in MEVPRO-1 (expected in 2026).

We view the key debate for the stock as whether rinzimetostat can realize multi-blockbuster revenue potential in prostate cancer, with outstanding questions on both the class (PRC2 inhibition) and profile of rinzi to be further elucidated this year.

ORIC recently presented Ph1b dose optimization data for rinzimetostat at the registrational dose, delivering competitive efficacy vs. benchmarks and a differentiated safety profile; if this profile is sustained (with updated results anticipated in 2H26), we anticipate meaningful share capture in the ~$7B addressable market of post-abiraterone mCRPC, consistent with precedent for second-to-market entrants.

We view PFE's MEVPRO-1 read-out as the key clinical catalyst for the class near-term, and therefore conducted a proprietary statistical analysis stressing the study's probability of success under a range of treatment and control arm assumptions; we view a relatively high PoS under most likely bull and base case assumptions, noting 30-40% upside to our current valuation of ORIC based on positive results.

Separately, ORIC continues to advance its EGFR inhibitor, enozertinib, across EGFR mutant lung cancer, with a clinical and program update anticipated mid-year (GSe: $700M).

1

1,332

Jun 11

Citizens reiterated $CRNX Market Outperform: $95~says $CAMRF update an incremental VE for Crinetics—nonetheless it views Oclaiz as a non-threat to Palsonify.

$NVS RICFY PFE IPSEY AZN

Citizens said: Camurus' CRL is primarily related to manufacturing so we expect it can be resolved over time, but FDA may need to reinspect its third-party manufacturer and scheduling may result in an even further delay.

We view the update as an incremental positive for CRNX; however, we did and do not view Oclaiz as a major competitive threat to Palsonify.

Oclaiz is still a monthly injectable SSA and has advantage of self-administration over approved injectables but is still an injection, and we still anticipate a waning of effect toward the end of a treatment cycle.

Palsonify's daily oral convenience and super efficacy and safety profile should make it a preferred option for most acromegaly patients.

Palsonify's early launch metrics have looked strong with >430 start forms as of 1Q26, ~70% of patients on paid drug already, and $10M in 1Q26 sales.

Oppenheimer from May 11, in image:

May 8

Citizens⬇️ $CRNX's PT to $95 (was $97) and reiterated at a Market Outperform rating.

$NVS $PFE IPSEY NBIX

Citizens said in its note:

Palsonify is off to a strong launch, consistent with our recent physician survey, with continued expansion of the prescriber base and early signs of improving reimbursement (see our 2Q survey here).

When we take a look at the early metrics, CRNX has received >430 start forms as of 1Q26, and 70% of patients are on paid drug.

If all of those patients stayed on drug for the rest of the year (without assuming any GTN/compliance discounts), that group would represent ~$66M in revenue.

This makes us comfortable with our $64M revenue estimate for 2026 (vs. consensus of $62M).

CRNX is now proving it can commercialize its drugs, and by mid-year the company will have four pivotal trials ongoing in carcinoid syndrome, pediatric and adult CAH, and Cushing's syndrome, which will provide multiple late-stage readouts, likely starting in 2027.

With a strong balance sheet providing runway beyond all of those readouts and a deep preclinical pipeline, CRNX remains one of our favorite names in the smid-cap space.

1

2,530

May 28

📈 Biotech Stock News 5/28 @ Open

$SPRC 183% Conditional Regulatory Approval Received

$AKTX 56% Breakthrough Potential of AKTX-101

$INKT 13% First Patient Dosed in Trial

$LNAI 11% Parkinson's and Rare Epilepsy AI Collab

$IMUX 9% Ph2 CALLIPER Trial Data

$INO 4% Participate in Scientific and Investor Conf.

$ALT 3% Pemvidutide shows metabolic improvements

$ZBIO 3% Submission of BLA for Obexelimab

$BCDA 3% Regulatory Submission for CardiAMP Tx

$COGT 3% Bezuclastinib & Sunitinib FDA Acceptance

$PMN 3% Participate in Upcoming Conferences

$BTAI 2% New data from SERENITY Ph3

$ARGX 2% Host Myositis R&D Webinar

$ENTX 2% EB613 data selected for presentation

$IONS 2% Bepirovirsen achieves functional cure rates

$NTRA 2% First Patients Enrolled in SIGNAL-ER 101

$ABBV 1% FDA Approves DECNUPAZTM

$IMMP 1% Eftilagimod alfa increases overall survival

$CPIX 1% Launch of VIBATIV® in China

$IPSEY 0% New data on IQIRVO® in PBC

$KALV 0% New data on injectable treatment burden

$JAZZ -1% Survival Benefit with Ziihera Combinations

$NRXP -2% EMOCARE Thermometer Clinical Validation

$ONC -3% Ph3 HERIZON-GEA Data Published

$JAGX -3% Advances Crofelemer for Rare Disorders

See the image and comments for more details!

May 28

$COGT FDA Acceptance of New Drug Application (NDA) with Priority Review for Bezuclastinib in Combination with Sunitinib for Patients with GIST. $DCPH $BPMC $SNY investors.cogentbio.com/news…

1

10

4,903

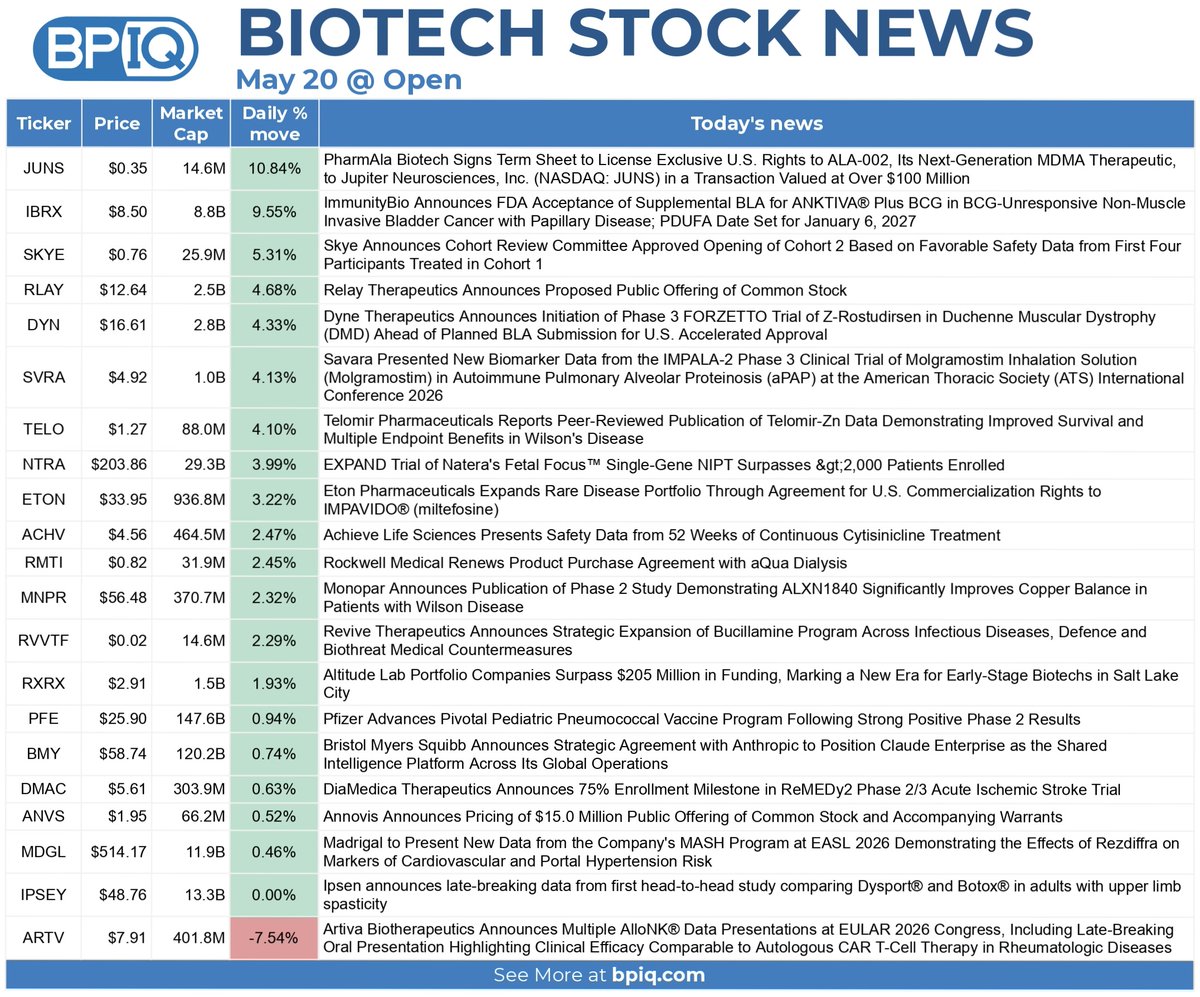

May 20

📢 Biotech Stock News 5/20 @ Open

$JUNS 11% License Exclusive U.S. Rights to ALA-002

$IBRX 10% FDA Acceptance of ANKTIVA® BLA

$SKYE 5% Comm. Approves Opening of Cohort 2

$RLAY 5% Proposed Public Offering of Stock

$DYN 4% Initiation of Ph3 FORZETTO Trial

$SVRA 4% New Biomarker Data for Molgramostim

$TELO 4% Telomir-Zn data shows improved survival

$NTRA 4% Fetal Focus NIPT Trial Surpasses 2,000

$ETON 3% IMPAVIDO Rare Disease Portfolio Expansion

$ACHV 2% Safety data from Cytisinicline treatment

$RMTI 2% Renews Product Purchase Agreement

$MNPR 2% Ph2 Study on ALXN1840

$RVVTF 2% Expansion of Bucillamine Program

$RXRX 2% New Era for Early-Stage Biotechs

$PFE 1% Advances Pediatric Pneumo Vaccine Program

$BMY 1% Strategic Agreement for Shared Intelligence

$DMAC 1% 75% Enrollment Milestone in ReMEDy2 Trial

$ANVS 1% Pricing of $15M Offering

$MDGL 0% New data on Rezdiffra effects

$IPSEY 0% Head-to-head study: Dysport vs Botox

$ARTV -8% AlloNK® Data Presentations at EULAR

See the image and comments for more details!

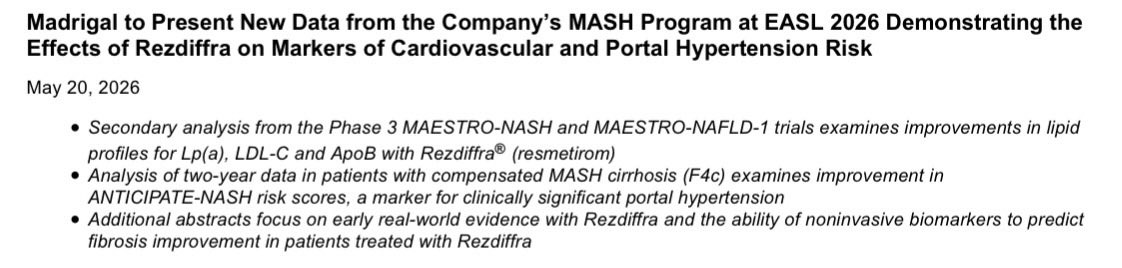

May 20

$MDGL Madrigal to Present New F4 Data from the Company’s MASH Program at EASL 2026 Demonstrating the Effects of Rezdiffra on Markers of Cardiovascular and Portal Hypertension Risk

1

1

5

6,297

May 18

📣 Biotech Stock News 05/18 @ Open (1️⃣ of 2)

$BIVI 4% Completion Phase 2 SUNRISE-PD Trial

$NTRA 4% Signatera™ CDx Approved for MIBC

$RNTX 3% Closing of $57.5 Million Offering

$AZN 1% BAXFENDY approved for hypertension; Enhertu Approved for New Indications

$IBRX 1% U.S. Patents for ANKTIVA and BCG; Exclusive U.S. Agreement for BCG

$MRK 0% TroFuse-005 Trial Met Primary Endpoints

$TCRT 0% Preclinical ALN1003 data on obesity

$NBIX 0% Completes Acquisition of Soleno Therapeutics

$VTRS 0% FDA Accepts New Drug Application

$QNCX 0% Improvements in Phase 2 Study; Acquisition and Private Placement Announcement

$IPSEY 0% Phase II corabotase data presented

See image below for details. 👇

May 18

📢 𝐉𝐔𝐒𝐓 𝐈𝐍: $IBRX ImmunityBio Secures U.S. Patents for 𝐀𝐍𝐊𝐓𝐈𝐕𝐀 𝐁𝐂𝐆 Through 𝟐𝟎𝟑𝟓

👉 𝐊𝐞𝐲 𝐇𝐢𝐠𝐡𝐥𝐢𝐠𝐡𝐭𝐬:

➤ ImmunityBio receives 𝟓 issued U.S. patents covering 𝐀𝐍𝐊𝐓𝐈𝐕𝐀 𝐁𝐂𝐆 therapies.

➤ Patent protection extends through at least 𝟐𝟎𝟑𝟓.

➤ Claims cover 𝐍𝐌𝐈𝐁𝐂 treatment methods, dosing regimens, and commercial kits.

➤ Portfolio protects approved 𝐀𝐍𝐊𝐓𝐈𝐕𝐀 plus BCG intravesical therapy platform.

➤ Supports ongoing 𝐐𝐔𝐈𝐋𝐓-𝟐.𝟎𝟎𝟓 registrational trial in bladder cancer.

➤ Patents align with exclusive U.S. 𝐓𝐨𝐤𝐲𝐨-𝟏𝟕𝟐 𝐁𝐂𝐆 supply agreement.

➤ ImmunityBio says portfolio strengthens long-term 𝐛𝐥𝐚𝐝𝐝𝐞𝐫 𝐜𝐚𝐧𝐜𝐞𝐫 franchise positioning.

3

1

11

8,179

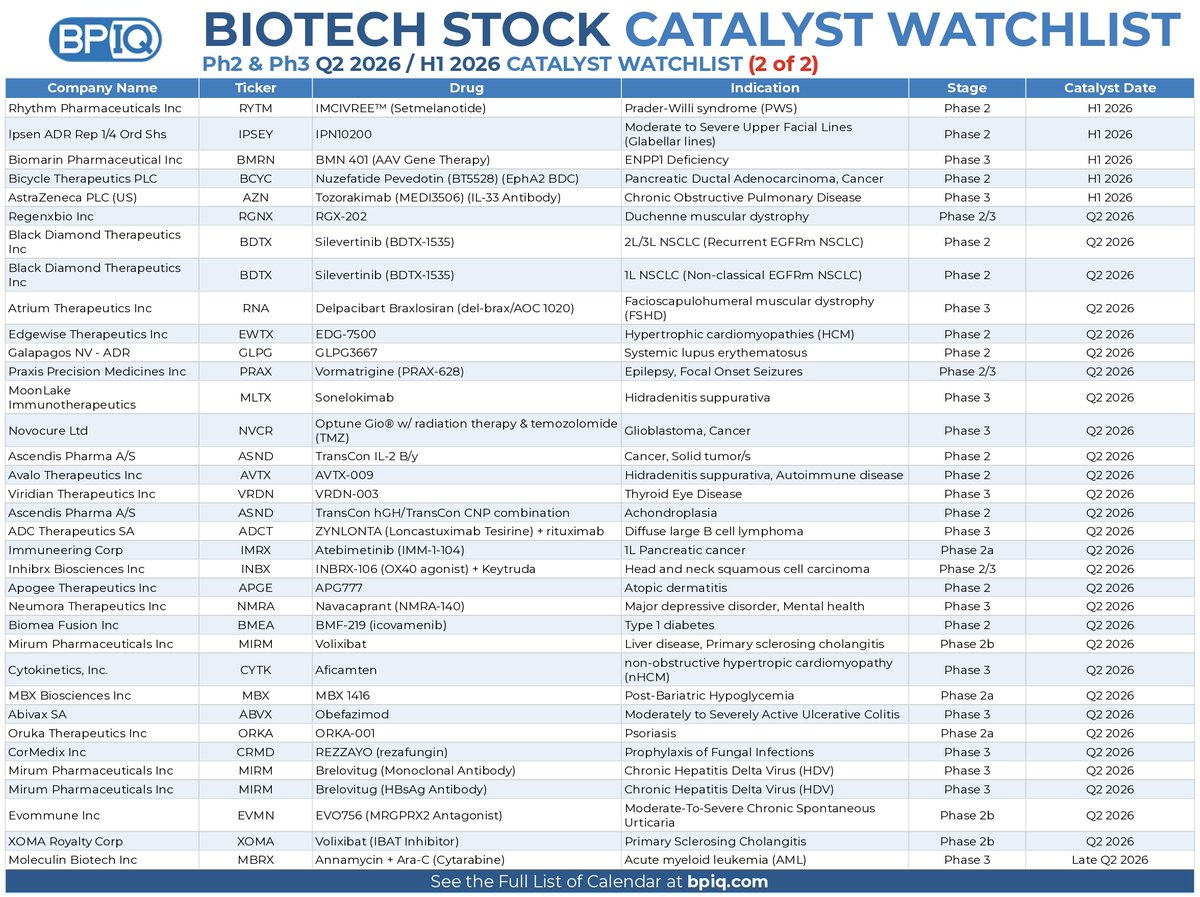

May 17

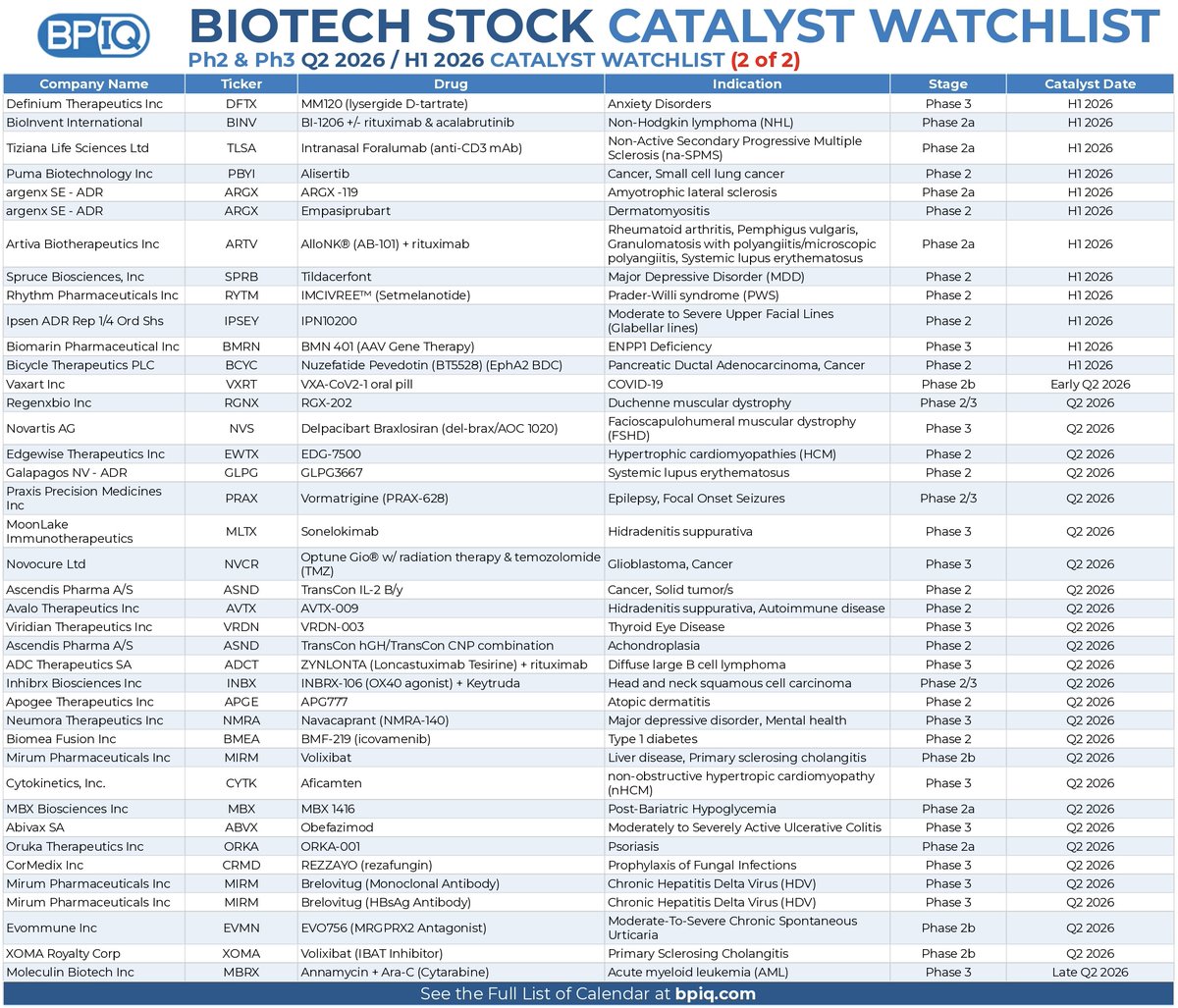

Biotech Stock Catalyst Watchlist

Ph2 & Ph3 readouts in Q2 2026 / H1 2026 (2️⃣/2)...

$CGON Phase 3

$IONS Phase 3

$GNPX Phase 2a

$BMRN Phase 3

$BINV Phase 2a

$ZNTL Phase 2

$PBYI Phase 2

$ELTX Phase 2

$TYRA Phase 2

$AGIO Phase 2b

$BINV Phase 2a

$TLSA Phase 2a

$PBYI Phase 2

$ARGX Phase 2a

$ARGX Phase 2

$SPRB Phase 2

$RYTM Phase 2

$IPSEY Phase 2

$BMRN Phase 3

$BCYC Phase 2

$NVS Phase 3

$EWTX Phase 2

$PRAX Phase 2/3

$MLTX Phase 3

$VTGN Phase 3

$NVCR Phase 3

$ASND Phase 2

$ASND Phase 2

$ADCT Phase 3

$VXRT Phase 2b

$APGE Phase 2

$NMRA Phase 3

$ABVX Phase 3

$XOMA Phase 2b

$DFTX Phase 3

$MBRX Phase 3

Check out the image for more details!

2

2

5

8,087

May 16

$IPSEY #Ipsen presents first-in-class late-breaking Phase II corabotase data in glabellar lines showing sustained duration of effect reinforced by consistently high patient satisfaction globenewswire.com/news-relea…

7

1,190

May 15

Goldman Sachs➡️ $ORIC from Early-Stage Biotech to a Buy rating and a $15 PT.

$PFE IPSEY VIR CADL BAYRY NVS $JNJ

Goldman Sachs said in its note:

We move ORIC to a Buy rating (from Early Stage Biotech) following clinical data which demonstrated a potentially differentiated profile for rinzimetostat in prostate cancer (GSe: $2.6B peak sales), and ahead of key de-risking Ph3 data for the class in MEVPRO-1 (expected in 2026).

We view the key debate for the stock as whether rinzimetostat can realize multi-blockbuster revenue potential in prostate cancer, with outstanding questions on both the class (PRC2 inhibition) and profile of rinzi to be further elucidated this year.

ORIC recently presented Ph1b dose optimization data for rinzimetostat at the registrational dose, delivering competitive efficacy vs. benchmarks and a differentiated safety profile; if this profile is sustained (with updated results anticipated in 2H26), we anticipate meaningful share capture in the ~$7B addressable market of post-abiraterone mCRPC, consistent with precedent for second-to-market entrants.

We view PFE's MEVPRO-1 read-out as the key clinical catalyst for the class near-term, and therefore conducted a proprietary statistical analysis stressing the study's probability of success under a range of treatment and control arm assumptions; we view a relatively high PoS under most likely bull and base case assumptions, noting 30-40% upside to our current valuation of ORIC based on positive results.

Separately, ORIC continues to advance its EGFR inhibitor, enozertinib, across EGFR mutant lung cancer, with a clinical and program update anticipated mid-year (GSe: $700M).

Feb 24

Oppenheimer reiterated $ORIC Outperform/$15, and said, ORIC reported fourth quarter and full year 2025 results that support what increasingly feels like a two-shots-on-goal story.

$PFE $JNJ TAK AZN NVS AVBP BDTX

Rinzimetostat continues to look competitive in mCRPC with 55% PSA50, 20% PSA90, and 59% ctDNA clearance, and has now moved into dose optimization ahead of a planned 1H26 Phase 3 start. While Pfizer's upcoming MEVPRO-1 readout will be a pivotal moment for the PRC2 class, we believe rinzi can differentiate on safety and PK.

In parallel, enozertinib's exon 20 and PACC data has demonstrated systemic activity and compelling CNS control, with the Phase 3 monotherapy dose selected and combo with subcutaneous amivantamab progressing.

We will be hosting ORIC management for a fireside chat during our Healthcare Conference on Wednesday, February 25th at 12:00 PM EST. Reiterate Outperform.

2

2,549

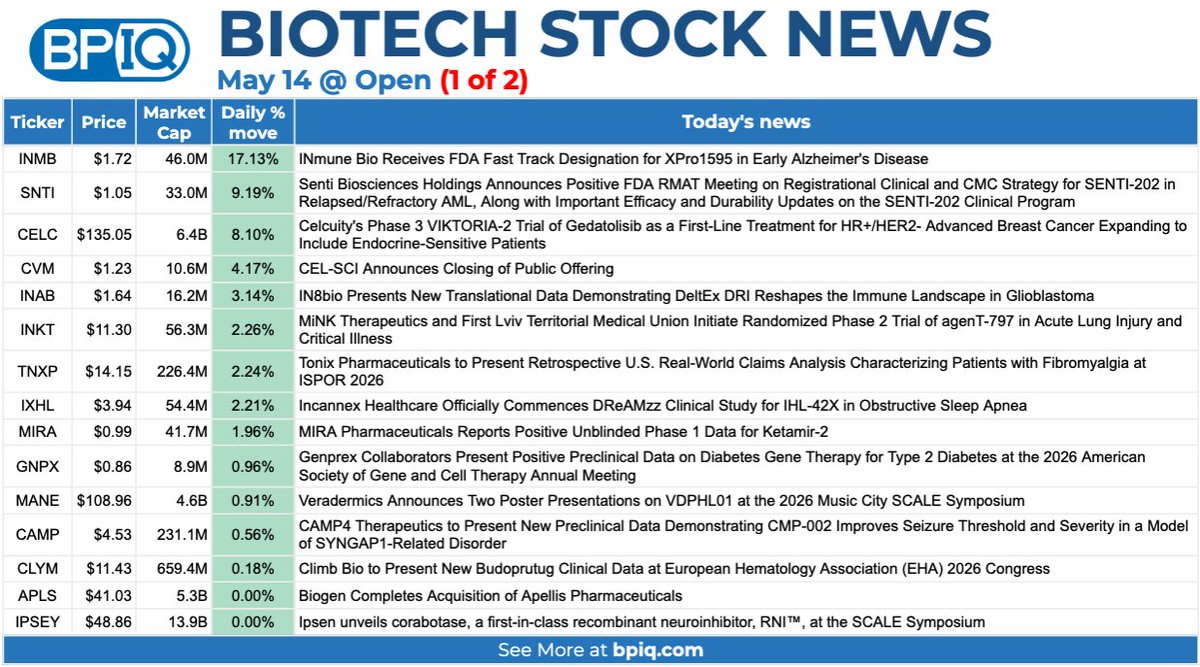

May 14

📣 Biotech Stock News 05/14 @ Open (1️⃣ of 2)

$INMB 17% FDA Fast Track for XPro1595

$SNTI 9% Positive FDA RMAT Meeting for SENTI-202

$CELC 8% VIKTORIA-2 Trial of Gedatolisib Expands

$CVM 4% Closing of Public Offering

$INAB 3% New Data on DeltEx DRI

$INKT 2% Phase 2 Trial of agenT-797

$TNXP 2% Retrospective Analysis of Fibromyalgia Patients

$IXHL 2% Commences DReAMzz Study for IHL-42X

$MIRA 2% Positive Phase 1 Data for Ketamir-2

$GNPX 1% Positive Preclinical Data on Diabetes Therapy

$MANE 1% Poster Presentations on VDPHL01

$CAMP 1% Preclinical data for CMP-002

$CLYM 0% New Budoprutug Clinical Data Presentation

$APLS 0% Completes Acquisition of Apellis

$IPSEY 0% Unveils corabotase at SCALE Symposium

See image below for details. 👇

May 14

$INMB Receives FDA Fast Track Designation for XPro1595 in Early Alzheimer's Disease

1

1

4

7,995

May 8

Citizens⬇️ $CRNX's PT to $95 (was $97) and reiterated at a Market Outperform rating.

$NVS $PFE IPSEY NBIX

Citizens said in its note:

Palsonify is off to a strong launch, consistent with our recent physician survey, with continued expansion of the prescriber base and early signs of improving reimbursement (see our 2Q survey here).

When we take a look at the early metrics, CRNX has received >430 start forms as of 1Q26, and 70% of patients are on paid drug.

If all of those patients stayed on drug for the rest of the year (without assuming any GTN/compliance discounts), that group would represent ~$66M in revenue.

This makes us comfortable with our $64M revenue estimate for 2026 (vs. consensus of $62M).

CRNX is now proving it can commercialize its drugs, and by mid-year the company will have four pivotal trials ongoing in carcinoid syndrome, pediatric and adult CAH, and Cushing's syndrome, which will provide multiple late-stage readouts, likely starting in 2027.

With a strong balance sheet providing runway beyond all of those readouts and a deep preclinical pipeline, CRNX remains one of our favorite names in the smid-cap space.

Mar 2

Citizens⬇️ $CRNX to $96 from $105 and reiterated at Market Outperform

$AZN $IPSEY NBIX NVS PFE

Citizens said in its note:

Early launch metrics reinforce our confidence in Palsonify's differentiated oral profile and long-term

acromegaly opportunity, with physicians in our recent survey expecting 20-30% adoption—implying a $670M-$1B U.S. market versus our ~$560M peak sales estimate.

CRNX also announced it received a positive opinion from the EMA's CHMP for paltusotine, recommending marketing authorization in the EU and positioning the program for EU approval.

In the pipeline, CRNX has three ongoing pivotal trials in carcinoid syndrome, pediatric and adult CAH and a pivotal Phase 2/3 for Cushing's syndrome kicking off this half.

Management is especially excited about CRN09682, a non-peptide drug conjugate, which is in Phaser 1 for neuroendocrine tumors which could unlock a new class of drugs.

While management did not provide Palsonify guidance, we model $63M in 2026 sales vs. consensus of $63M.

As the top line grows, investors will turn focus to the multiple pivotal readouts that will drive medium- and long-term growth.

1

4

5,143

May 3

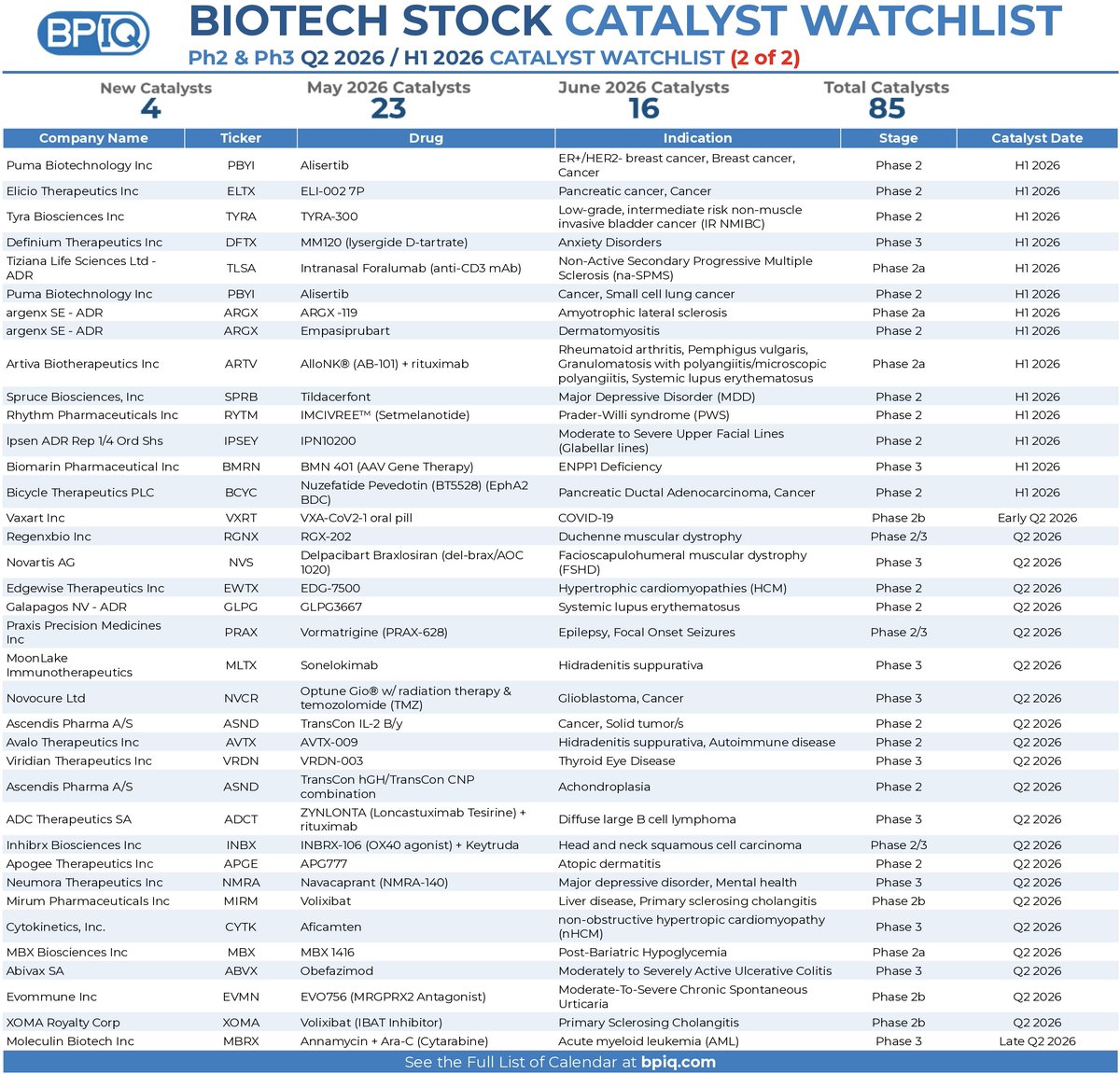

Biotech Stock Catalyst Watchlist

Ph2 & Ph3 readouts in Q2 2026 / H1 2026 (2️⃣/2)...

$PBYI Phase 2

$ELTX Phase 2

$TYRA Phase 2

$DFTX Phase 3

$TLSA Phase 2a

$PBYI Phase 2

$ARGX Phase 2a

$ARGX Phase 2

$ARTV Phase 2a

$SPRB Phase 2

$RYTM Phase 2

$IPSEY Phase 2

$BMRN Phase 3

$BCYC Phase 2

$VXRT Phase 2b

$RGNX Phase 2/3

$NVS Phase 3

$EWTX Phase 2

$GLPG Phase 2

$PRAX Phase 2/3

$MLTX Phase 3

$NVCR Phase 3

$ASND Phase 2

$AVTX Phase 2

$VRDN Phase 3

$ASND Phase 2

$ADCT Phase 3

$INBX Phase 2/3

$APGE Phase 2

$NMRA Phase 3

$MIRM Phase 2b

$CYTK Phase 3

$MBX Phase 2a

$ABVX Phase 3

$EVMN Phase 2b

$XOMA Phase 2b

$MBRX Phase 3

Check out the image for more details!

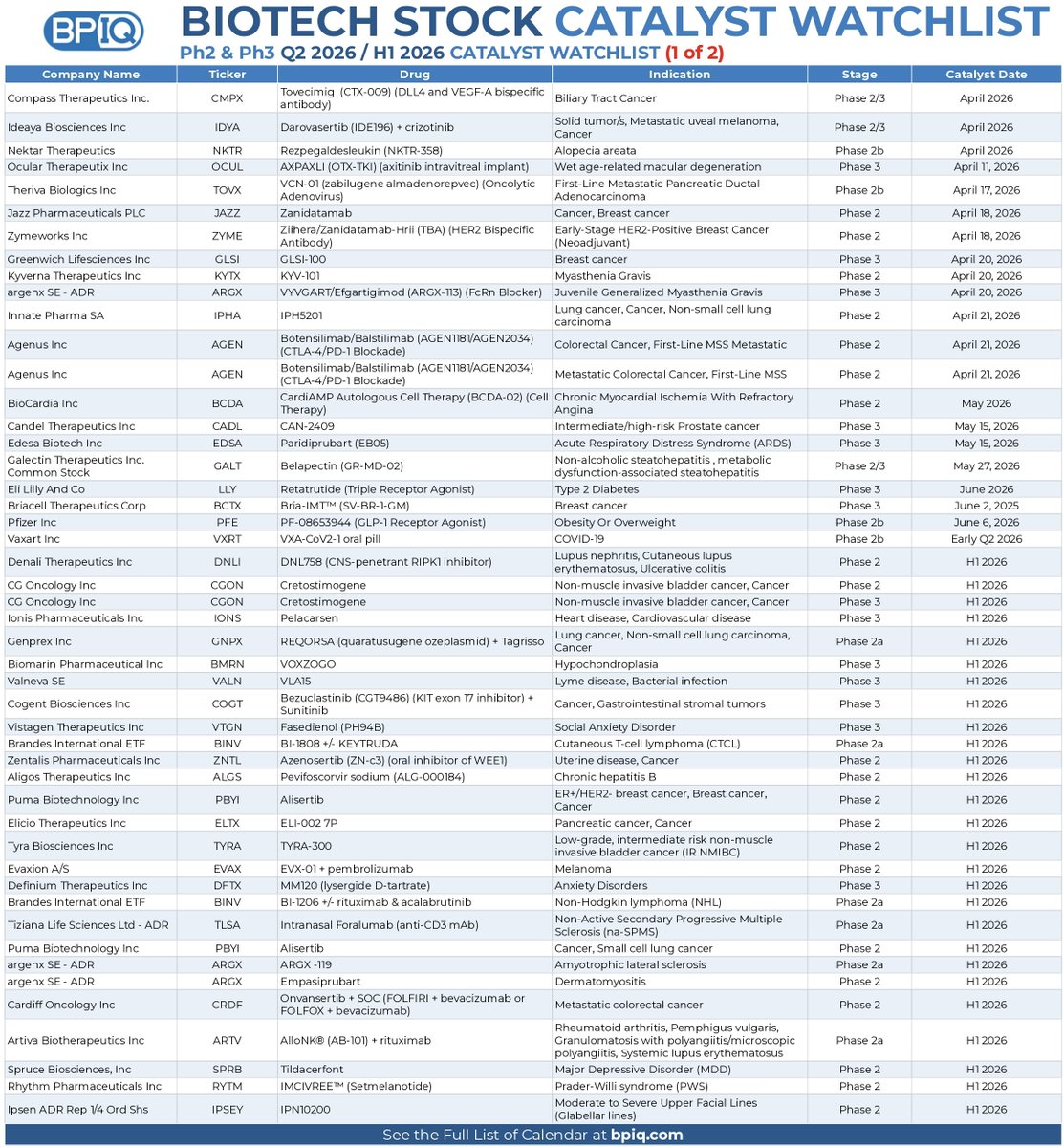

May 3

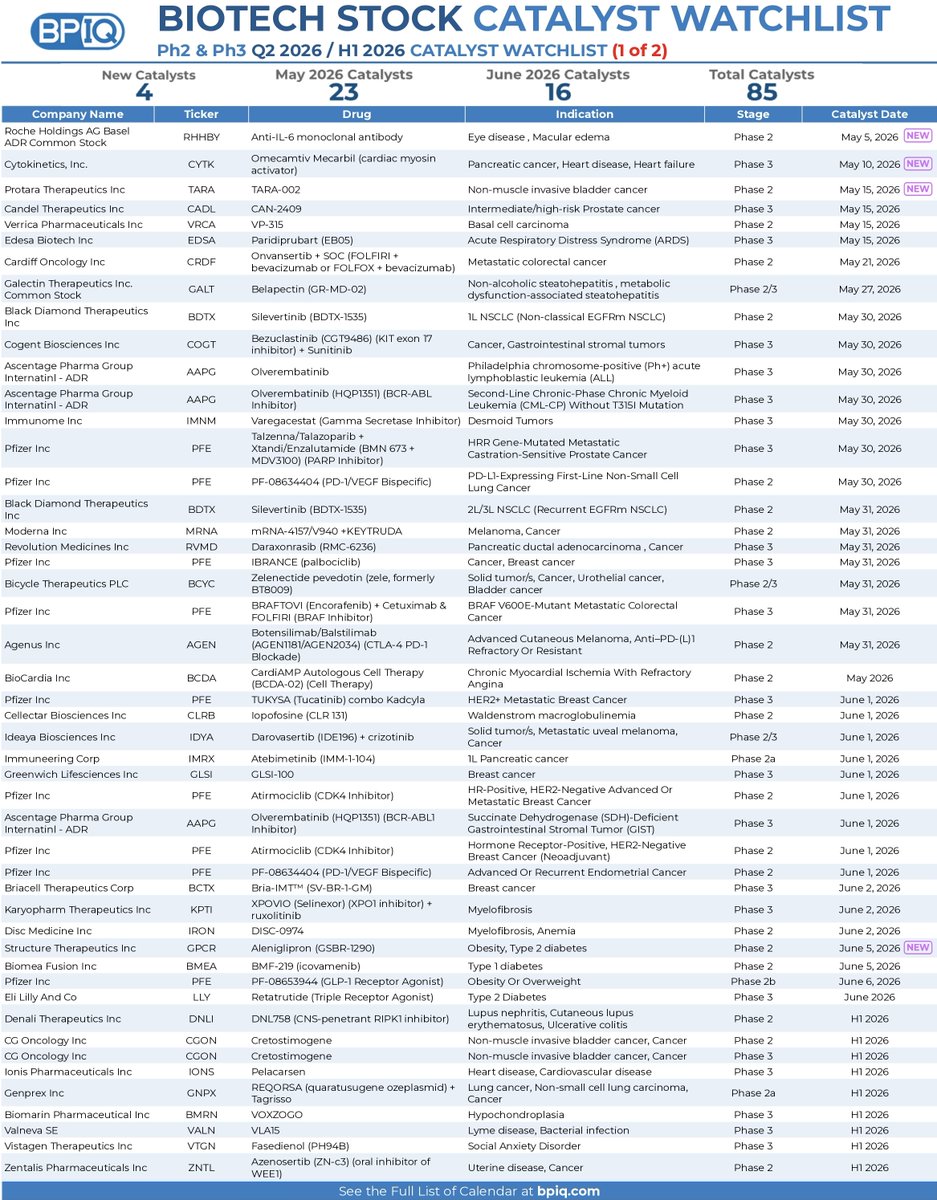

Biotech Stock Catalyst Watchlist

Ph2 & Ph3 readouts in Q2 2026 / H1 2026 (1️⃣/2)...

$RHHBY Phase 2

$CYTK Phase 3

$TARA Phase 2

$CADL Phase 3

$VRCA Phase 2

$EDSA Phase 3

$CRDF Phase 2

$GALT Phase 2/3

$BDTX Phase 2

$COGT Phase 3

$AAPG Phase 3

$AAPG Phase 3

$IMNM Phase 3

$PFE Phase 3

$PFE Phase 2

$BDTX Phase 2

$MRNA Phase 2

$RVMD Phase 3

$PFE Phase 3

$BCYC Phase 2/3

$PFE Phase 3

$AGEN Phase 2

$BCDA Phase 2

$PFE Phase 3

$CLRB Phase 2

$IDYA Phase 2/3

$IMRX Phase 2a

$GLSI Phase 3

$PFE Phase 2

$AAPG Phase 3

$PFE Phase 2

$PFE Phase 2

$BCTX Phase 3

$KPTI Phase 3

$IRON Phase 2

$GPCR Phase 2

$BMEA Phase 2

$PFE Phase 2b

$LLY Phase 3

$DNLI Phase 2

$CGON Phase 2

$CGON Phase 3

$IONS Phase 3

$GNPX Phase 2a

$BMRN Phase 3

$VALN Phase 3

$VTGN Phase 3

$ZNTL Phase 2

Check out the image for more details!

2

3

13

4,093

Apr 28

Stifel⬆️ $MIRM's PT to $130 from $125, reiterated at Buy, and said: We conducted a deep dive into each of MIRM's upcoming pivotal pipeline readouts: PSC (May -- ahead of EASL), HDV (2H26), EXPAND (4Q26), and PBC (1H27).

$IPSEY $CMMB

GILD VIR

GSK CALT

Stifel added—In short, we're bullish on each.

PSC is most important for the stock near-term where we see potential upside/downside of 20-25%/(25-30%), even as we'd argue the "floor" is higher.

Ultimately though, we expect the trial to work (70% POS) and think conservative assumptions (including potentially re:price) support a blockbuster opportunity for volixibat broadly (across PSC/PBC).

Big picture: MIRM continues to stand out as a unique rare disease company with a large—and growing—base business, strong management/execution, and a compelling catalyst path with four (in our view, de-risked) pivotals over the next ~12-18-months.

Shares have done well-but we're increasingly comfortable MIRM's $4B peak portfolio revenue potential may be conservative. And in that context, we still see room for meaningful upside as these catalysts play out.

Apr 10

Cantor reiterated $MIRM Overweight; $140

$VIR $GILD ASMB ALGS

Cantor said—2026 projected revenue across MIRM's products is $630-650M with meaningful growth still ahead, especially if Livmarli succeeds in the EXPAND study - which we expect it will and will push peak sales towards $1B/yr.

MIRM is already approaching profitability with its existing portfolio; volixibat and brelovitug synergize nicely and should see meaningful bottom-line contribution. While it's premature to pinpoint the ultimate PSC/PBC split for volixibat (in part because we lack insight into pricing, and in part because PBC is bigger but has more competitor dynamics) - we still believe this asset can easily surpass $1b in peak sales and potentially approach $2B - especially if we factor ex-U.S. sales (MIRM plans to launch in selective territories).

Brelovitug for HDV appears to be meaningfully derisked, and we expect positive data this year - the HDV market is a little hazier, but on a global basis, we're comfortable assuming peak sales in the $300-500M range.

So with a line of sight to peak sales in the $3B range (or higher) and our model forecast for nearly $8/share in EPS in 2030 growing to ~$13/share in 2032, we still see considerable upside from the current -$100/share stock price and ~ $6B mkt cap.

1

4

5,545

Apr 26

Biotech Stock Catalyst Watchlist

Ph2 & Ph3 readouts in Q2 2026 / H1 2026 (2️⃣/2)...

$DFTX Phase 3

$BINV Phase 2a

$TLSA Phase 2a

$PBYI Phase 2

$ARGX Phase 2a

$ARGX Phase 2

$ARTV Phase 2a

$SPRB Phase 2

$RYTM Phase 2

$IPSEY Phase 2

$BMRN Phase 3

$BCYC Phase 2

$VXRT Phase 2b

$RGNX Phase 2/3

$NVS Phase 3

$EWTX Phase 2

$GLPG Phase 2

$PRAX Phase 2/3

$MLTX Phase 3

$NVCR Phase 3

$ASND Phase 2

$AVTX Phase 2

$VRDN Phase 3

$ASND Phase 2

$ADCT Phase 3

$INBX Phase 2/3

$APGE Phase 2

$NMRA Phase 3

$BMEA Phase 2

$MIRM Phase 2b

$CYTK Phase 3

$MBX Phase 2a

$ABVX Phase 3

$ORKA Phase 2a

$CRMD Phase 3

$MIRM Phase 3

$MIRM Phase 3

$EVMN Phase 2b

$XOMA Phase 2b

$MBRX Phase 3

Check out the image for more details!

1

4

933

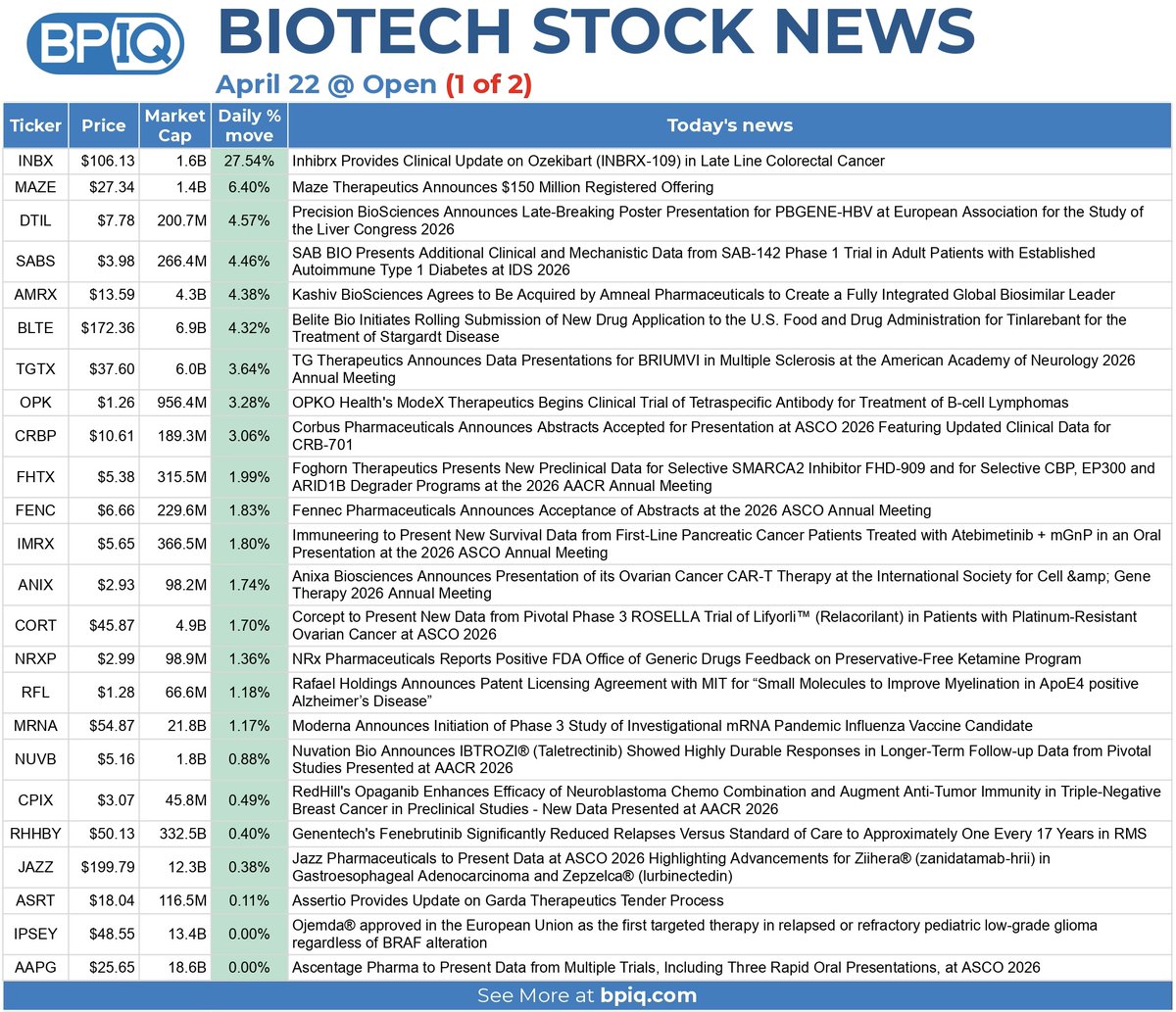

Apr 22

Biotech Stock News 4/22 @ Open (1️⃣ of 2)

$INBX 28% Clinical Update on Ozekibart

$MAZE 6% $150M Registered Offering

$DTIL 5% PBGENE-HBV Presentation

$SABS 4% Clinical data from SAB-142 trial

$AMRX 4% To Acquire Kashiv BioScience

$BLTE 4% Rolling Submission for Tinlarebant

$TGTX 4% Data Presentations for BRIUMVI

$OPK 3% Clinical Trial of Tetraspecific Antibody

$CRBP 3% Abstracts Accepted for CRB-701

$FHTX 2% New Preclinical Data for FHD-909

$FENC 2% Acceptance of Abstracts at ASCO Mtg

$IMRX 2% New survival data for Atebimetinib

$ANIX 2% Ovarian Cancer CAR-T Tx Presentation

$CORT 2% New data from ROSELLA Trial

$NRXP 1% Positive FDA feedback on Ketamine

$RFL 1% Patent Licensing Agreement w/ MIT

$MRNA 1% Ph3 Study of mRNA Vaccine

$NUVB 1% IBTROZI® Shows Durable Responses

$CPIX 0% Opaganib enhances chemo efficacy

$RHHBY 0% Fenebrutinib Reduces Relapses in RMS

$JAZZ 0% Data on Ziihera and Zepzelca

$ASRT 0% Update on Garda Therapeutics Tender

$IPSEY 0% Ojemda® approved for pediatric glioma

$AAPG 0% Present data from multiple trials

See the image and comments for more details!

$xbi

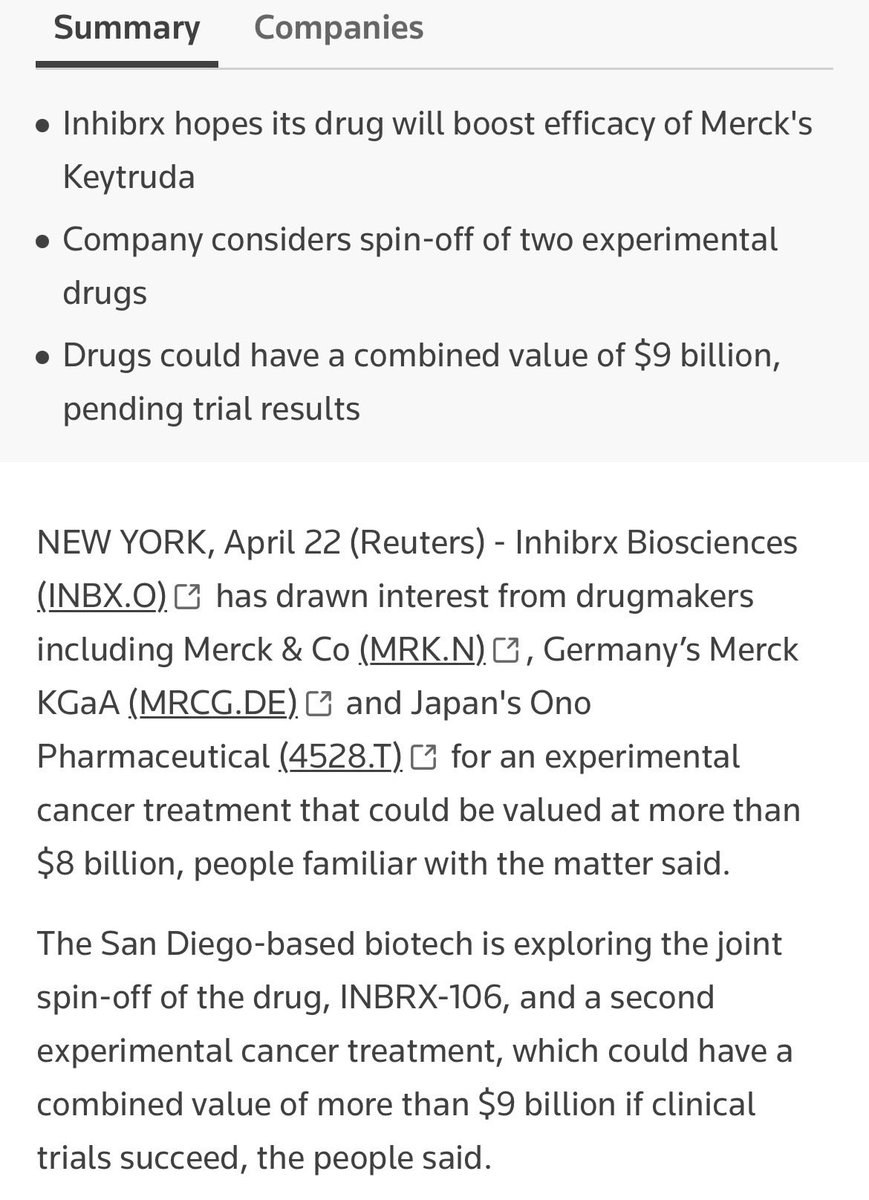

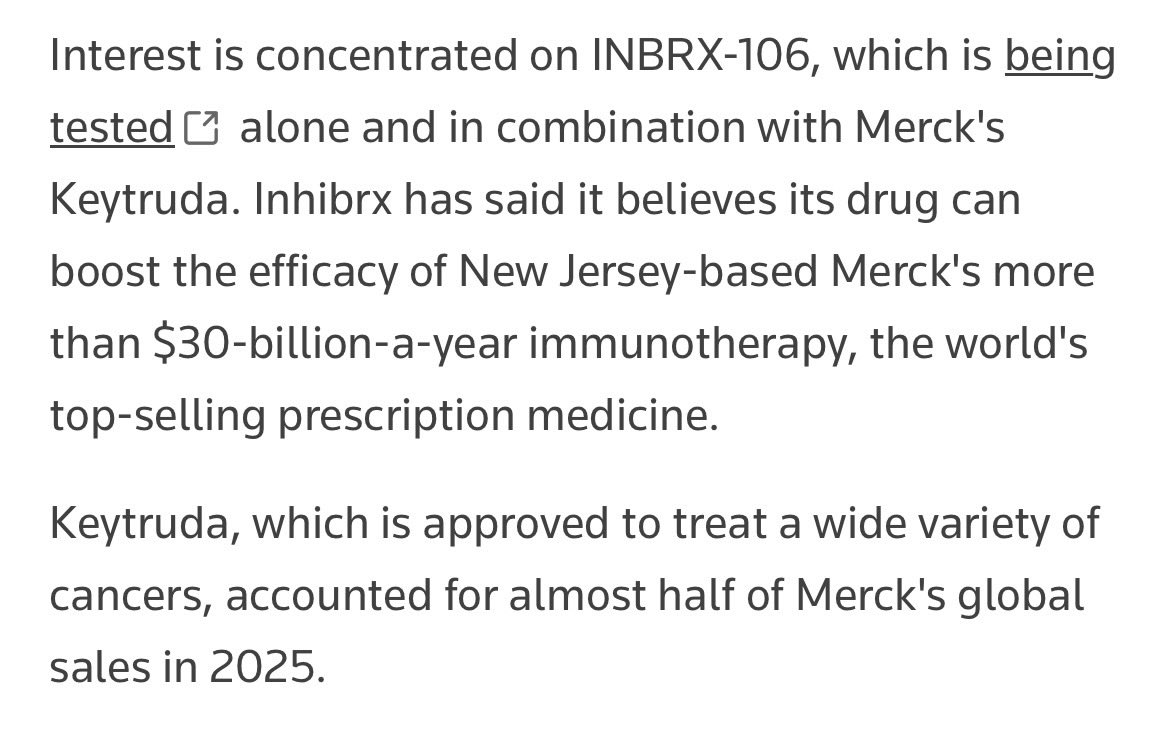

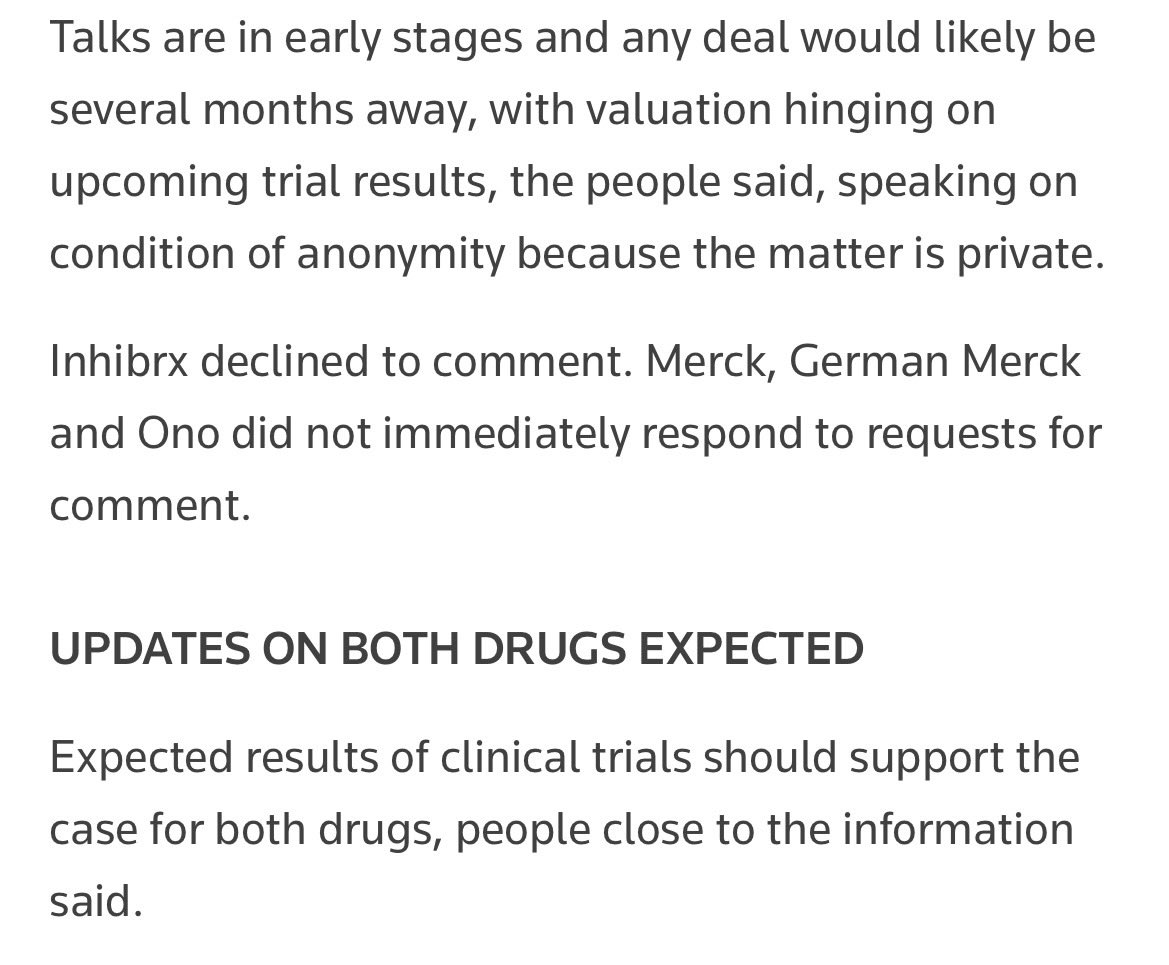

Exclusive: $MRK, rivals eye deal for $INBX experimental cancer drug, okizekibart, tied to Keytruda, sources say.

🎩 @Reuters

1

1

6

5,274

Apr 19

Biotech Stock Catalyst Watchlist

Ph2 & Ph3 readouts in Q2 2026 / H1 2026 (2️⃣/2)...

$RYTM Phase 2

$IPSEY Phase 2

$BMRN Phase 3

$BCYC Phase 2

$AZN Phase 3

$RGNX Phase 2/3

$BDTX Phase 2

$BDTX Phase 2

$RNA Phase 3

$EWTX Phase 2

$GLPG Phase 2

$PRAX Phase 2/3

$MLTX Phase 3

$NVCR Phase 3

$ASND Phase 2

$AVTX Phase 2

$VRDN Phase 3

$ASND Phase 2

$ADCT Phase 3

$IMRX Phase 2a

$INBX Phase 2/3

$APGE Phase 2

$NMRA Phase 3

$BMEA Phase 2

$MIRM Phase 2b

$CYTK Phase 3

$MBX Phase 2a

$ABVX Phase 3

$ORKA Phase 2a

$CRMD Phase 3

$MIRM Phase 3

$MIRM Phase 3

$EVMN Phase 2b

$XOMA Phase 2b

$MBRX Phase 3

Check out the image for more details!

1

1

6

1,102

Apr 5

Biotech Stock Catalyst Watchlist

Ph2 & Ph3 readouts in Q2 2026 / H1 2026 (1️⃣/2)...

$CMPX Phase 2/3

$IDYA Phase 2/3

$NKTR Phase 2b

$OCUL Phase 3

$TOVX Phase 2b

$JAZZ Phase 2

$ZYME Phase 2

$GLSI Phase 3

$KYTX Phase 2

$ARGX Phase 3

$IPHA Phase 2

$AGEN Phase 2

$AGEN Phase 2

$BCDA Phase 2

$CADL Phase 3

$EDSA Phase 3

$GALT Phase 2/3

$LLY Phase 3

$BCTX Phase 3

$PFE Phase 2b

$VXRT Phase 2b

$DNLI Phase 2

$CGON Phase 2

$CGON Phase 3

$IONS Phase 3

$GNPX Phase 2a

$BMRN Phase 3

$VALN Phase 3

$COGT Phase 3

$VTGN Phase 3

$BINV Phase 2a

$ZNTL Phase 2

$ALGS Phase 2

$PBYI Phase 2

$ELTX Phase 2

$TYRA Phase 2

$EVAX Phase 2

$DFTX Phase 3

$BINV Phase 2a

$TLSA Phase 2a

$PBYI Phase 2

$ARGX Phase 2a

$ARGX Phase 2

$CRDF Phase 2

$ARTV Phase 2a

$SPRB Phase 2

$RYTM Phase 2

$IPSEY Phase 2

Check out the image for more details!

5

17

90

921,458

Mar 29

Biotech Stock Catalyst Watchlist

Ph2 & Ph3 readouts in Q2 2026/H1 2026 (1️⃣/2)...

$LPCN Phase 3

$TOVX Phase 2b

$JAZZ Phase 2

$ZYME Phase 2

$GLSI Phase 3

$KYTX Phase 2

$ARGX Phase 3

$IPHA Phase 2

$AGEN Phase 2

$AGEN Phase 2

$CMPX Phase 2/3

$IDYA Phase 2/3

$BCDA Phase 2

$CADL Phase 3

$EDSA Phase 3

$BCTX Phase 3

$PFE Phase 2b

$LLY Phase 3

$DNLI Phase 2

$CGON Phase 2

$CGON Phase 3

$IONS Phase 3

$GNPX Phase 2a

$BMRN Phase 3

$VALN Phase 3

$VTGN Phase 3

$BINV Phase 2a

$ZNTL Phase 2

$ALGS Phase 2

$PBYI Phase 2

$ELTX Phase 2

$TYRA Phase 2

$EVAX Phase 2

$DFTX Phase 3

$UTHR Phase 3

$BINV Phase 2a

$TLSA Phase 2a

$IMVT Phase 3

$PBYI Phase 2

$ARGX Phase 2a

$ARGX Phase 2

$CRDF Phase 2

$ARTV Phase 2a

$SPRB Phase 2

$RYTM Phase 2

$IPSEY Phase 2

$BMRN Phase 3

$BCYC Phase 2

Check out the image for more details!

1

2

11

2,962