28 Jan 2025

II. Latest Developments IXS

1. Strategic Partnerships

-Institutions: UBS, State Street, PwC tokenizing Variable Capital Companies (e-VCC).

-LINE Integration: 200M users access RWA investments.

- $CPOOL Partnership: $25M liquidity for decentralized RWA lending. Developing the RWA DEFI toolset.

2. Selection of RWA product launches demonstrating $IXS pioneering role in RWA & security offerings:

- Demon Hunters: Tokenized film investments targeting entertainment markets. (one of many pioneering recent RWA offerings)

- CKGP (@Coachkcrypto GameFi Portfolio) offering exposure to a diversified basket of high-potential GameFi and DeFi projects. Investors gain access to a mix of established and emerging gaming tokens with a minimum entry of 1 USDT.

- Sangamithra Epic: Tokenized film financing and intellectual property (IP) rights management, partnering with 1AssetExchange. This initiative allows investors to participate in revenue streams from film production and distribution

- $TRSR-DRC-1: Represents fractional ownership in a rare wine collection, including Domaine de la Romanee-Conti bottles. Investors benefit from potential returns tied to the luxury wine market’s appreciation and sales.

- Socialerus ($SCR-1): Enables investment in monetizable YouTube channels. Funds raised target high-potential channels identified via proprietary data analytics, offering exposure to the digital content creation boom.

- $SSOL1 (Solar-Collateralized Token): Funds sustainable energy projects, including a waste tire recycling initiative. Combines financial returns with ESG impact.

- Howey Tez BAYC (IXAPE): Fractional ownership of Bored Ape Yacht Club #2371, a blue-chip NFT. Token holders gain economic interest in the NFT’s profits, compliant under Singapore’s securities laws.

- TAU Digital: Security token offering (STO) tied to shares in TauRx Pharmaceuticals Ltd. Provides fractional ownership of biotech equity, democratizing access to private healthcare investments.

- Onchain Tokenized Portfolios (OTPs): ETF-like structures for DeFi assets, such as CKGP, providing instant diversification and liquidity.

3. Usecase Example: Tokenize high tech startups with IXswap

-KYC investors can gain exposure to e.g. high-growth startups with a $1 minimum entry, bypassing traditional 8 to 15-year exit timelines.

-Liquidity for Founders: Startups can tokenize equity, allowing early investors to trade shares on secondary markets via IX Swap’s AMM-DEX, reducing illiquidity risks.

-Think digital Employee Stock Ownership Plans enabling instant liquidity for corporate equity before IPO

4. Global Expansion

-Multi-chain growth: Interoperability with BNB Chain, Base, KAIA and XDC etc. 5 protocol integrations in development

-Regulatory reach: MAS and SCB licenses for compliance. Capital Markets Services (CMS) and Recognized Market Operator (RMO) licenses for trading RWA globally. US market as soon as regulatory risks reduce.

1

6

229

5 Jan 2025

Day 3 of 360 🧵

KPMG - Asset Tokenization - A C-Suite Perspective

•Introduction and Overview

Asset Tokenization Defined

The report defines asset tokenization as the process of converting assets into a digital format and recording ownership on a distributed ledger (typically a blockchain).

This process enables detailed documentation of asset attributes, status, and transaction history.

Digital tokens are created to represent various assets, including financial instruments and real assets. This allows for fractionalization, enabling ownership of portions of assets.

•Market Significance

Asset tokenization is presented as a significant development in the financial landscape, attracting considerable interest from institutional investors.

The report highlights a survey where 88% of institutional investors are actively advancing their digital asset plans and 91% are interested in tokenized products.

"According to a recent survey of 271 institutional investors, there is significant enthusiasm for digital asset investments, with 88% actively advancing their plans and 91% expressing interest in investing in tokenized products."

•Transformative Potential

Asset tokenization is anticipated to reshape both financial and non-financial markets within the next 5-15 years, with the potential to democratize access to investments and revolutionize the management of diverse asset classes.

•Report Purpose

This report aims to provide an extensive exploration of asset tokenization, its drivers, and the journey involved, including deal structuring, digitization, distribution, and management. It also addresses legal implications and provides a C-suite decision framework.

•Key Themes and Concepts

KPMG Digital Asset Taxonomy

The report introduces a taxonomy that uses the term "Off-Chain Assets" (OCAs) to represent all tokenized assets that are not digital currencies or cryptocurrencies.

This is favored over the term "Real-World Assets" (RWA) to avoid confusion with the traditional financial term "Risk Weighted Assets."

The taxonomy categorizes assets into Real Assets, Financial Assets, and Other Assets.

Examples of Tokenized Assets

The report provides examples of different tokenized assets, including bonds, repo securities, corporate bonds, MMMF shares, real estate, gold, wine, and carbon credits.

Market Opportunity

The potential to tokenize global illiquid assets (real estate, private equity, bonds, commodities, financial assets) is a multi-trillion-dollar opportunity, with forecasted market growth of 28x to 80x between 2023 and 2030.

Emerging Hubs

Singapore, Hong Kong, China, and Switzerland are identified as fast-emerging competitive hubs for asset tokenization, supported by government initiatives and developing regulatory frameworks.

"Singapore, Hong Kong (SAR), China, and Switzerland are fast emerging as competitive hubs for asset tokenization. This evaluation is based on several key factors, namely Government Sponsorship, Legal Framework, Regulatory Environment, and Market Infrastructure."

•Benefits of Tokenization

Increased Efficiency and Reduced Costs

Smart contracts enable automation, reducing administrative burdens and manual processes.

Increased Transparency and Better Risk Management

Blockchain enhances transparency and traceability, reducing counterparty risks and deterring fraudulent activities.

Increased Market Liquidity

Tokenization lowers investment barriers, removes geographical constraints, and enables fractionalization, which increases participation and overall market liquidity.

Increased Accessibility

Fractional ownership, enabled by tokenization, allows a wider range of investors to participate in high-value asset markets.

•Asset Tokenization Process

The report outlines a 5-stage process for asset tokenization:

Deal Structuring:

Defining the asset to be tokenized and its legal structure, determining if the asset is a security, commodity, or something else.

Digitization:

Immobilizing the physical asset by transferring it to a custodian and creating a digital representation of the asset (a token) on the blockchain.

A digital register of members (ROM) detailing current investors is created.

Primary Market:

Tokens are offered to investors in exchange for capital. This can be through traditional financial institutions or newer digital asset exchanges. Investors must establish a digital wallet to receive their tokens.

Corporate Actions:

Consistent servicing of the digital asset, including regulatory reports, NAV determination, dividend distribution, and shareholder voting.

These actions can be automated via smart contracts.

Secondary Market Trading:

Token holders can exchange tokens directly or through secondary trading platforms.

•Case Studies

Real Estate (CitaDAO)

CitaDAO tokenized industrial units in Singapore, enabling fractional ownership and increased liquidity. Users could trade tokens on decentralized exchanges. The platform attracted considerable liquidity to a traditionally illiquid asset.

"The main benefit to issuers is liquidity, with the approach successfully attracting about US $400,000 liquidity (~67% of the asset value) for the tokenized 20 Sin Ming Lane real estate."

Art & Collectibles (InvestaX)

InvestaX tokenized an NFT from the Bored Ape Yacht Club, creating security tokens (IXAPE) allowing for fractional ownership. This expanded access to the high-value NFT.

Wine-Based Securities (Alta Exchange)

Alta collaborated with PhillipCapital to offer tokens representing future bottles of select Bordeaux wines, listed on the exchange for trading.

•C-Suite Decision Framework

6-Point Checklist

KPMG provides a checklist for C-suite executives to assess the viability of tokenization projects, covering:

•Desirability (Market Demand)

•Viability (Strategic Alignment, Asset Suitability, Legal & Regulatory Outlook)

•Feasibility (Technology Infrastructure, Interoperability)

•Resilience (Risk Management, Data Security & Privacy)

•Professional Support

•Internal Expertise

Company Decision Matrix

The checklist is underpinned by a company decision matrix centered around four themes and nine specific considerations:

Desirability: Market demand, Partnerships and ecosystem.

Viability: Strategic alignment, Asset suitability & valuation, Legal & Regulatory outlook.

Feasibility: Technology infrastructure, Interoperability.

Resilience: Risk Management, Data security & Privacy.

•Adoption Challenges

Regulatory Complexity:

Navigating different regulations across various jurisdictions (KYC, AML, investor protections).

Uncertain Legal Claims:

Challenges in enforcing tokenized off-chain assets due to reliance on social norms and legal systems.

Technical Challenges:

Interoperability issues arising from varying technical standards across blockchain ecosystems.

Trust Deficit:

Lack of trust in verification of participants and transactions, and a lack of streamlined digital KYC processes.

•Future Outlook

Increasing Regulatory Clarity:

Regulatory authorities are providing clearer guidelines for digital assets.

Addressing Legal Claims:

New legal guidance and precedents are emerging worldwide.

Convergence of Technical Standards:

Technical standards are converging, with organizations issuing recommendations for digital asset issuance.

Decentralized Identity Adoption:

Governments are developing frameworks for decentralized identity to enhance user control over data.

•Expert Perspectives (HSBC and SMBC)

HSBC (Rajeev Tummala)

Tokenization will shift how institutions participate in the asset space.

Assets will become easier to own, with broader accessibility.

New roles will emerge (curators, specialist custodians), as will network types (enterprise-only, private, public).

Challenges:

Varying maturity levels of participants, value proposition differences in post-trade operations, and regulatory support.

SMBC (Thaddaeus Lee)

Tokenization can support SMEs and private debt/liquidity markets.

Promotes sustainability through fractional ownership, enhanced liquidity, and transparency.

Challenges:

Unfamiliarity with blockchain tech, immaturity of security infrastructure, and interoperability.

Signals of Adoption:

Funding requires a solid economic foundation, buzzwords will fade as the tech becomes more integrated, and AI proliferation will drive adoption of Web 3.0 applications for data control.

•Conclusion

Asset tokenization is more than a technological innovation; it's a paradigmatic shift in asset management and ownership.

The report provides a roadmap through the process, challenges, and key considerations for C-Suite executives. Despite the challenges, the future for asset tokenization is considered promising, with increasing activity from market participants and regulators.

4 Jan 2025

Day 2 of 360 🧵

Briefing Document:

DTCC - Transforming Collateral Management with Digital Assets

Introduction

The study focuses on the potential of digital assets and distributed ledger technology (DLT) to revolutionize collateral management within capital markets, highlighting a proof of concept (PoC) developed on the DTCC Digital Launchpad.

Key Themes and Ideas

Transformative Potential of Digital Assets

The report emphasizes the transformative impact digital asset technology can have on financial markets. It is not just an incremental improvement, but a potential "revolution" reshaping the entire value chain, from issuance to post-trade activities.

"Digital asset technology is set to have a transformational effect on financial markets, bringing new efficiencies, business models, and liquidity opportunities to the ecosystem."

Specifically, tokenization of real-world assets is seen as having a massive impact on capital markets, comparable to the effect of the Internet on information exchange.

"Institutional demand for tokenization of real-world financial assets is growing, and its impact on capital markets could be similar to the impact the Internet had on information exchange."

Need for a Harmonized Digital Asset Ecosystem

The current digital asset landscape is fragmented, with initiatives often isolated and using diverse networks and protocols.

This creates a need for industry-wide collaboration to harmonize standards, controls, and operations, aiming for a unified infrastructure similar to the centralized nature of U.S. post-trade services.

"The strength of US markets is that we have one post-trade provider; we’re aiming to do the same for digital markets."

The challenge is not just about system interoperability but aligning on frameworks that bridge traditional and DLT-based systems.

DTCC Digital Launchpad as a Catalyst for Innovation

DTCC's Digital Launchpad is positioned as a critical tool to address the challenges mentioned above. It is described as an "open ecosystem" designed for experimentation and collaboration, not just a sandbox.

"DTCC Digital Launchpad is more than just a milestone – it is a game-changer in our journey to build an open and interoperable digital asset ecosystem."

The Launchpad offers a robust technology stack with flexible connectivity to various blockchain networks, foundational tools, and digital asset products.

It is intended to accelerate the development of production-ready solutions and standards.

-Industry Launchpad: Broad collaboration on shared pain points.

-Client Launchpad: Dedicated client-specific projects.

JSCC Collateral Management PoC on the Launchpad

The collaboration between DTCC and JSCC serves as a prime example of how the Launchpad can be used for practical solutions.

They focused on the tokenization of assets (cash, stocks, bonds) to improve the efficiency, transparency, and speed of collateral management for CCPs (Central Counterparties).

"By leveraging digital assets for collateral processing, CCPs can potentially enhance market stability, improve digital asset quality, and increase the efficiency and liquidity of collateral."

This PoC goes beyond basic deposit and return, exploring:

•Seamless integration of margin calls.

•Automated movement of collateral through smart contracts.

•Intraday swapping of various digital assets.

Key Benefits Demonstrated by the PoC

•Increased Speed and Efficiency:

Digital assets enhance the speed, transparency, and efficiency of collateral processes.

•Seamless Integration of Margin Calls and Deposits/Withdrawals:

The PoC demonstrated how smart contracts and tokenized collateral create a unified process between CCPs, clearing members, and buy-side clients, reducing manual processing.

"Connecting margin calls and deposits through smart contracts and tokenized collateral created a seamless process among CCPs, clearing members, and buy-side clients, greatly enhancing efficiency and reducing manual processing."

•Automation of Business Processes:

Smart contracts were shown to automate workflows, significantly reducing operational risks and inefficiencies.

"Smart contracts to automate business workflows and enable movement of digital assets can not only increase STP/automation in the end-to-end process but also increase optionality for institutions involved."

•Standardized Smart Contracts:

Shared applications (smart contracts and UI) across CCPs, clearing members, and buy-side clients enable standardization.

"Digital assets offer financial markets a chance to rethink the ecosystem design to standardize and automate processes and applications."

•Improved Collateral Swap:

DLT atomic transactions enable seamless and secure substitution of various digital assets as collateral.

"JSCC verified the technical viability of CCPs enabling seamless collateral substitutions (Delivery-vs-Delivery) using the atomic transactions feature of DLT."

•On-Chain Shared Data for Optimization:

An Oracle node provided real-time market data and asset information, enabling participants to simulate, optimize, and manage risks.

"By using the Oracle node as a ‘golden source’ of data coupled with shared smart contracts, sell-side and buy-side entities on the network were able to simulate and optimize their collateral positions under different market scenarios, in near real-time."

Challenges and Future Directions

Managing User Account Hierarchies (Omnibus Accounts): The challenge of maintaining privacy and user account hierarchies in complex structures.

Interoperability: Future experiments will explore international CCP interoperability to improve cross-border transactions.

Lifecycle Management: Further development of digital asset lifecycle events for bonds and equities as collateral.

Smart Contract Refinement: Enhancements to meet diverse market needs and ensure auditability.

Conclusion

The DTCC and JSCC collaboration demonstrates the significant potential of digital assets and DLT to transform collateral management.

By leveraging the DTCC Digital Launchpad, JSCC developed a PoC that improved efficiency, reduced operational risks, and increased transparency.

While challenges remain, the study underscores the importance of collaboration and common standards. DTCC's Digital Launchpad will be pivotal in building a new digital asset industry ecosystem.

The report highlights the value of collaborative experimentation in driving industry-wide adoption of digital asset technology, positioning the Launchpad as a foundation for future innovations in capital markets.

1

2

7

2,032

10 May 2024

1/4 January

🔹RWA Panel Series Launch: We started the year by launching the first of our Real-World Assets (RWA) Panel Series, shedding light on the burgeoning RWA market.

x.com/IxSwap/status/17511991…

🔹Strategic Partnership with Vault Tech Hub: To further our commitment to innovation, we partnered with Vault Tech Hub, enhancing access to technologies and resources in the DeFi ecosystem.

x.com/IxSwap/status/17515630…

🔹Introduction of IXAPE Token Use Case: We unveiled the IXAPE token's use case, clarifying its utility and value proposition within the IX Swap ecosystem

ixswap.io/news/ixape-token-u…

27 Jan 2024

Don't miss out on this exclusive opportunity to gain valuable perspectives and stay ahead in the rapidly evolving world of RWAs. Mark your calendars and join us for an enlightening discussion!

📍x.com/i/spaces/1lPKqblzNZdGb

1

6

607

4 Mar 2024

Unlocking wealth shouldn't be an uphill battle!

With private investing often out of reach, @IxSwap flips the script.

Fractionalization crowdfunding = accessibility for all, starting from just $1.

More about $IXS 👇

------------------------------------------------------------

1️⃣ Overview of IX Swap

@IxSwap lets you invest in real-world assets using blockchain tech.

Their platform, powered by AMM, helps startups innovate crowdfunding and gives businesses global market access.

$IXS offers liquidity solutions through security tokens (ST) with licensed brokers and custodians.

Their ecosystem includes:

- A security token exchange

- Liquidity solutions for security tokens

- Compliant crowdfunding solutions via security tokens

@IxSwap revolutionises real-world asset tokenization by fractionalizing ownership with digital tokens on a blockchain.

Benefits include transparency and liquidity, allowing immediate buying, selling, and trading.

Fractionalization enables wider investor participation.

IXApe tokens exemplify this concept by democratizing NFT ownership, creating liquidity and profit-sharing opportunities for retail users.

2️⃣ Other features

Liquidity Pools: How do they work?

STOs require licenses and infrastructure for trading securities. Without them, investors risk legal ownership issues.

Mishandling regulated assets can harm business operations.

Do you think these problems have gone unnoticed? - Nope

IX Swap addresses these challenges by adopting a Uniswap-like model.

Liquidity providers can stake assets to generate wrapped tokens, ensuring secure trading within a pool

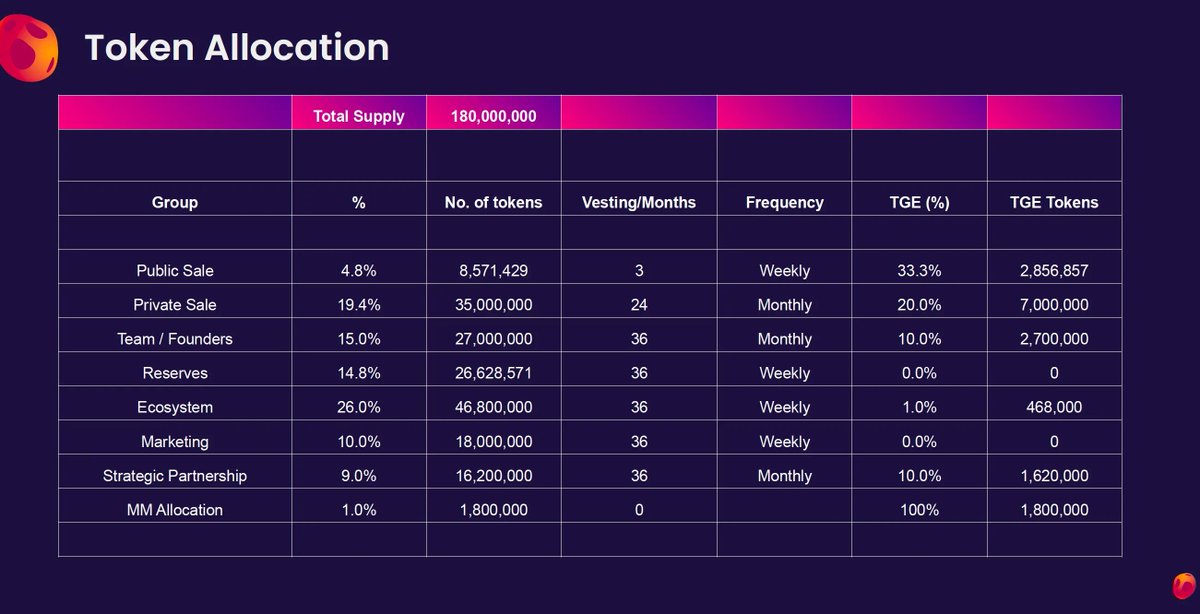

3️⃣ Tokenomics

IXS Tokenomics and Deflationary Mechanics ↓

IXS token's deflationary economics function benefits token holders by creating value as the platform is used.

Unlike central banks, IXS is deflationary like BTC, increasing in value with demand.

The fees collected will fund the Moon and Solar Vaults.

Moon Vault buys back tokens, while Solar Vault burns them to reduce supply permanently 🔥

Token distribution and vesting schedule can be seen here👇

Most of the token categories has a fairly long vesting schedule.

This will control the supply and reduce selling pressure from non-aligned users.

4️⃣ Team

IXSwap has a team of experts covering blockchain engineering, capital markets, tech and legal.

🔸 Julian Kwan, Co-Founder/CEO: serial entrepreneur, founded 6 businesses including blockchain/DLT areas

🔸 Aaron Ong, Co-Founder/President: >8 years of capital market experience in investment and local banks

🔸 Alice Chen, General Counsel: boasts >17 years of legal expertise

🔸 Alexander Cucer, CTO: >10 years of experience in tech development

5️⃣ Partnerships

❇️ Collaborating with @plumenetwork to build a robust RWA ecosystem aimed at enhancing liquidity for private investments.

twitter.com/IxSwap/status/17…

❇️ Industry leader @flowdesk_co brings cutting-edge market-making tech to improve user experiences.

This exciting collaboration enhances $IXS liquidity on exchanges.

twitter.com/IxSwap/status/17…

❇️ There is also a partnership between @Landshareio and @IxSwap!

This collaboration enhances accessibility to the $LSRWA token and enables cross-chain integration for #RWA's and security tokens.

twitter.com/Landshareio/stat…

I have only listed the recent partnerships and there are MANY more!

------------------------------------------------------------

What do you think of @IxSwap ?

Meaningful partnerships give confidence to users that things are going on, with thoughtful leadership helming it 💯

It's deflationary tokenomics is also a positive as it could boost demand for the tokens.

At <60MC, imo this poses a good opportunity to ride the RWA narrative.

$IXS team ↓

@julian2kwan

@aaronongsy

@shialicechen

$IXS supporters ↓

@TheEuroSniper

@gem_insider

@CryptoShadowOff

@0xRockefeller

@RWAsOverCrypto

@DaanCrypto

@Cryp__toad

@Coinballers

@wacy_time1

@M4Cero

Big chads ↓

@blocmates

@monosarin

@DeFiMinty

@andrewmoh

@CryptoShiro_

@CryptoGideon_

@Only1temmy

@andyyy

@NNovaDefi

@Louround_

@poopmandefi

@0xjeff

@splinter0n

@CryptoNikyous

@0xGoldenDegen

@0xShinChannn

@dontbuytops

@Cryptoalpharian

@thesaint_

@TweetByGerald

@matrixthesun

@Karamata2_2

@defi_antcrypto

@MoneyCrptBunny

@FomoCatchers

@Launchpad_Daddy

@blazing420s

11 Feb 2024

🤝 We’re pleased to announce our partnership with @IxSwap, a uniswap for real-world assets (#RWA's) & security tokens.

That’s a solid milestone in Landshare's trajectory toward seamless cross-chain integration and the $LSRWA token's accessibility to a wider audience.

In anticipation of this collaboration, we are excited to organize a joint Twitter Space and other co-marketing activities to delve into the intricacies of our platforms.

Stay updated on this exciting development by following us on social media - @Landshareio 🔔

10

5

33

3,107

17 Jan 2024

🟡 IXAPE Token Usecase

Dive into the intricacies of the IXAPE token and unravel its groundbreaking usecase. Learn more about the innovative process and cutting-edge technology that powers IXAPE.

Click here to learn more: ixswap.io/blog/ixape-token-u…

4

5

36

4,223

22 Nov 2023

Don't miss out on more rewards! Generate your own referral link here: app.ixswap.io/#/kyc

Plus, a heads up: $IXAPE Snapshot happens on Dec 2, and Zealy November Sprint ends on Nov 30.

IXAPE Airdrop: ixswap.io/blog/ixape-airdrop

Zealy: zealy.io/c/ixswap/questboard

1

2

5

1,383

22 Nov 2023

For our PH community, this guide simplifies the process to qualify for IXAPE airdrop and Zealy campaign rewards as it is done in Tagalog. Big thanks to @ALrOck14 for this!

1

5

1,384

22 Nov 2023

🚀 Community Partner Update! Our partner, @BRGYTamago, has crafted a helpful review and guide for our ongoing $IXAPE airdrop and @zealy_io campaign.

🔗 youtu.be/GJfu6H95LUw

4

4

18

1,688

15 Nov 2023

My 1st IXAPE token, ill acquire more soon. You can buy yours too, as it was limited date for the airdrop.

Thank you, @IxSwap 🤍

1

86

2 Nov 2023

1

2

43

17 Sep 2023

My top security token holdings ranked by $ invested

$Liti - @LitiCapital 🫶

$TAU - @IxSwap 🫶

$STM - @STOmarket 🫶

$IXApe - @IxSwap 🫶

And some others not worth mentioning rn

Starting to build a portfolio lol 🙏 lets gooo

#tokenization #securitytokens #rwas #realworldassets

1

5

366

31 Oct 2022

Hey everyone! To avoid the spinny ball page, make sure to sign in to your Metamask wallet to sign in on the app!

You also still have time to join our #Halloween Scavenger Hunt for a chance to win 3 $IXAPE for FREE! 😉

Hurry - sign up and join now! Good luck! 🚀

1

31 Oct 2022

🎃LAST DAY🔥

Today’s your last chance to hunt for the 5

hidden Howey Tez scattered all over IXS Academy for a chance to win 3 $IXAPE!

Get #haunting 👻 now!

👉🏻 academy.ixswap.io

#FREE #giveaway #Halloween #blockchain #crypto

27 Oct 2022

This year, we're celebrating #Halloween with a #HoweyTez twist. Ready to go #haunting? 👻🎃

1️⃣ Follow, RT & tag 3 friends

2️⃣ Go to academy.ixswap.io/

3️⃣ Find the 5 hidden Howey Tez in 5 random articles

4️⃣ Screenshot all 5 & comment below

🏆 3 $IXAPE = $30 🤑

👉🏻 Ends 10.31

2

5

13

30 Oct 2022

free money 👌

great product 👌

great platform 👌

i luh dis ❤️

#giveaway #NFTCommunity #NFTGiveaways #exchange #dex #Cryptocurency #ixswap $ixape

30 Oct 2022

Happy Sunday, #IXSwap fam! Did you know that you can bag #FREE $IXAPE that's worth around $30 💰 when you join our #Halloween Scavenger Hunt ?👻🎃

🏆 5 winners | 3 $IXAPE each 🤑

It ends tomorrow so hurry and JOIN NOW! Details below 👇🏻👇🏻

#HoweyTez #BAYC #blockchain #giveaway

2

1

2

30 Oct 2022

Happy Sunday, #IXSwap fam! Did you know that you can bag #FREE $IXAPE that's worth around $30 💰 when you join our #Halloween Scavenger Hunt ?👻🎃

🏆 5 winners | 3 $IXAPE each 🤑

It ends tomorrow so hurry and JOIN NOW! Details below 👇🏻👇🏻

#HoweyTez #BAYC #blockchain #giveaway

27 Oct 2022

This year, we're celebrating #Halloween with a #HoweyTez twist. Ready to go #haunting? 👻🎃

1️⃣ Follow, RT & tag 3 friends

2️⃣ Go to academy.ixswap.io/

3️⃣ Find the 5 hidden Howey Tez in 5 random articles

4️⃣ Screenshot all 5 & comment below

🏆 3 $IXAPE = $30 🤑

👉🏻 Ends 10.31

1

13

28 Oct 2022

From pitching #IXSwap to a global stage at @GITEX_GLOBAL to listing #IXAPE, #October was one awesome month!🚀

Tune in next week for our community #AMA where co-founders @julian2kwan and @AaronOngsy will talk about what was up and what's new at #IXSwap.💯

discord.com/invite/XXHzsJGYk…

1

8

19

28 Oct 2022

When black cats 🐈⬛ prowl and pumpkins 🎃 gleam, may luck be yours on #Halloween. 👻

1️⃣ Follow, RT, tag 3 friends

2️⃣ Go to academy.ixswap.io

3️⃣ Find 5 #HoweyTez hidden in 5 articles

4️⃣ Screenshot all 5 & comment on the pinned post

🏆 3 $IXAPE = $30

👉🏻 Ends 10.31

#giveaway

27 Oct 2022

This year, we're celebrating #Halloween with a #HoweyTez twist. Ready to go #haunting? 👻🎃

1️⃣ Follow, RT & tag 3 friends

2️⃣ Go to academy.ixswap.io/

3️⃣ Find the 5 hidden Howey Tez in 5 random articles

4️⃣ Screenshot all 5 & comment below

🏆 3 $IXAPE = $30 🤑

👉🏻 Ends 10.31

1

2

9