POWER FINANCE CORPORATION: CO THREE WHOLLY OWNED SUBSIDIARIES; DEOGHAR INFRA LIMITED, DEOGHAR MEGA POWER LIMITED AND JHARKHAND INFRAPOWER LIMITED; STRUCK OFF BY ROC EFFECTIVE JUNE 1

9

2

105

18,456

May 17

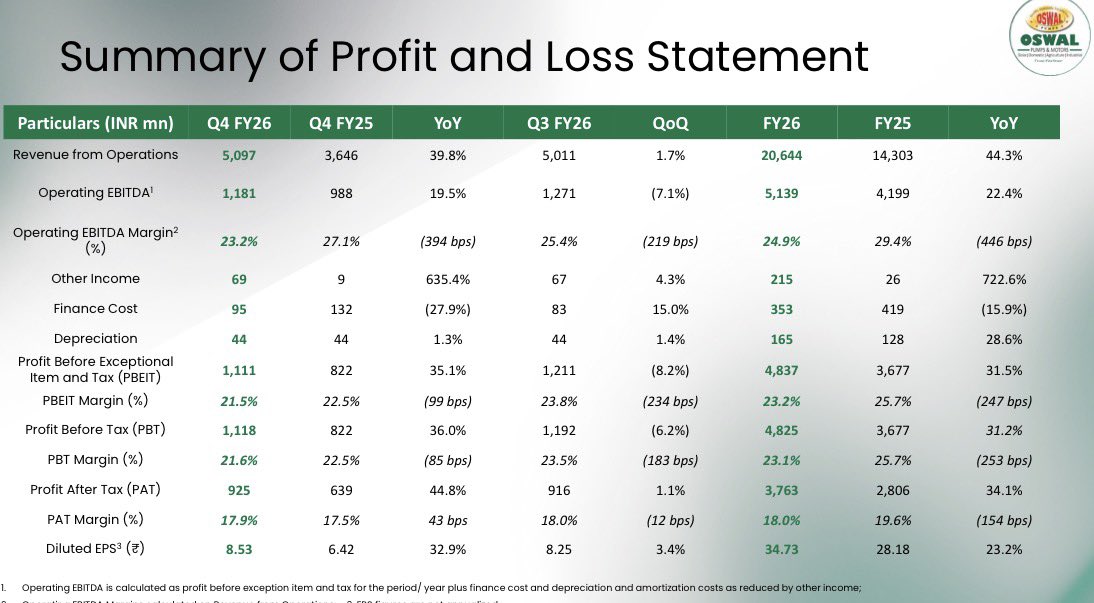

Oswal Pumps just dropped Q4 & FY26 results.

FY26 numbers are genuinely impressive on the surface:

Revenue grew 44% to ₹2,064 Cr.

PAT grew 34% to ₹376 Cr — highest ever.

EPS came in at ₹34.73.

And the company is now almost debt-free (D/E went from 0.99x to 0.08x thanks to the IPO).

EBITDA margin slipped from 29.4% to 24.9%.

Gross margin slipped from 44.1% to 39.3%.

That's 446 bps of operating margin gone in one year.

Management calls it "competitive tender pricing and input cost pressures from geopolitical uncertainties." Fair enough — it's true. But on a ₹2,000 Cr base, that compression is real money.

Receivable days also stretched from 111 to 155. State nodal agencies are paying late. Q4 cash flow did turn decisively positive at ₹170 Cr, and a ₹116 Cr collection on April 2nd flipped the full year to a hair above breakeven, but the full year reported CFO is still negative ₹77 Cr.

So the cash engine is repairing itself — just not yet repaired.

Now here's the part that nobody is talking about.

Direct PM KUSUM revenue actually DROPPED in FY26.

₹961 Cr in FY25 to ₹535 Cr in FY26. That's a 44% fall.

So where did the 44% topline growth come from?

One scheme. One state.

Magel Tyala. Maharashtra.

Revenue from this single state scheme went from ₹23 Cr to ₹964 Cr in a year. Roughly 42x.

Oswal supplied 42,119 pumps under Magel Tyala alone — that's nearly 40% of all pumps it has ever supplied to any government, anywhere.

This is concentration risk dressed up as diversification.

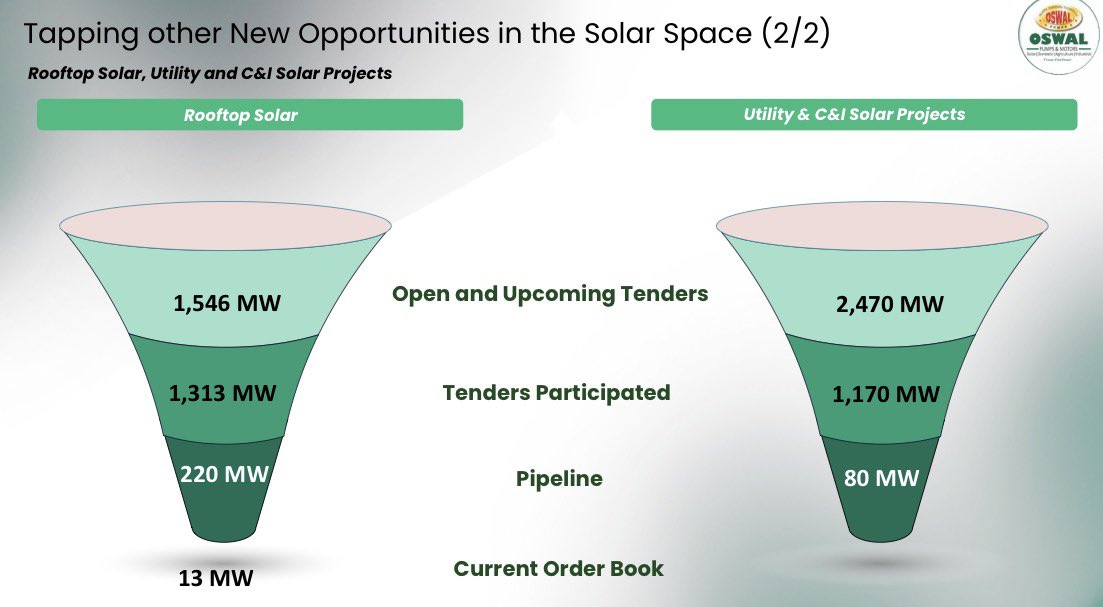

To be fair, management is trying to diversify — first PM Surya Ghar order is in, a 60% JV with Doon Infrapower has been set up for Rajasthan rooftop projects, and they're building a 300 MW pipeline across rooftop, utility, and C&I solar. But today, the engine is one state.

What's the forward look?

Order book: 19,912 pumps with letters of award.

Pipeline beyond that: 25,000 more.

PM KUSUM 2.0: expected to roll out in FY27. Management is positioning for it.

And on capital — ₹271 Cr of IPO money is still unutilized. Most of it earmarked for the new Karnal manufacturing units. Capacity expansion isn't done; it's loaded.

My take:

This was a "record on paper, pressure under the hood" kind of year.

The balance sheet is pristine now.

The order book is healthy.

But margins compressed sharply, working capital is stretched, and the FY26 growth came from one Maharashtra scheme that won't repeat at the same intensity.

FY27 will be decided by three things:

— When PM KUSUM 2.0 actually rolls out

— How fast state nodal agencies clear receivables

— Whether the 300 MW rooftop/utility pipeline converts to revenue

The stock is already ~57% below its 52-week high, so a fair bit of the worry is in the price. From here it's no longer a story stock. It's an execution stock.

I'll be watching Q1 and Q2 closely.

Not a recommendation. Just sharing what I read in the deck.

4

35

4,122

Technical Associates Infrapower reports consolidated net loss of Rs 8.85 crore in the December 2025 quarter theindiansubcontinent.com/53… #Insubcontinent #Technical #Associates #Infrapower #reports #consolidated #December #quarter INSWorld

6

6

21

Feb 11

Technical Associates Infrapower reports consolidated net loss of Rs 8.85 crore in the December 2025 quarter theindiansubcontinent.com/53… #Insubcontinent #Technical #Associates #Infrapower #reports #consolidated #December #quarter INSWorld

1

2

9

25 Dec 2025

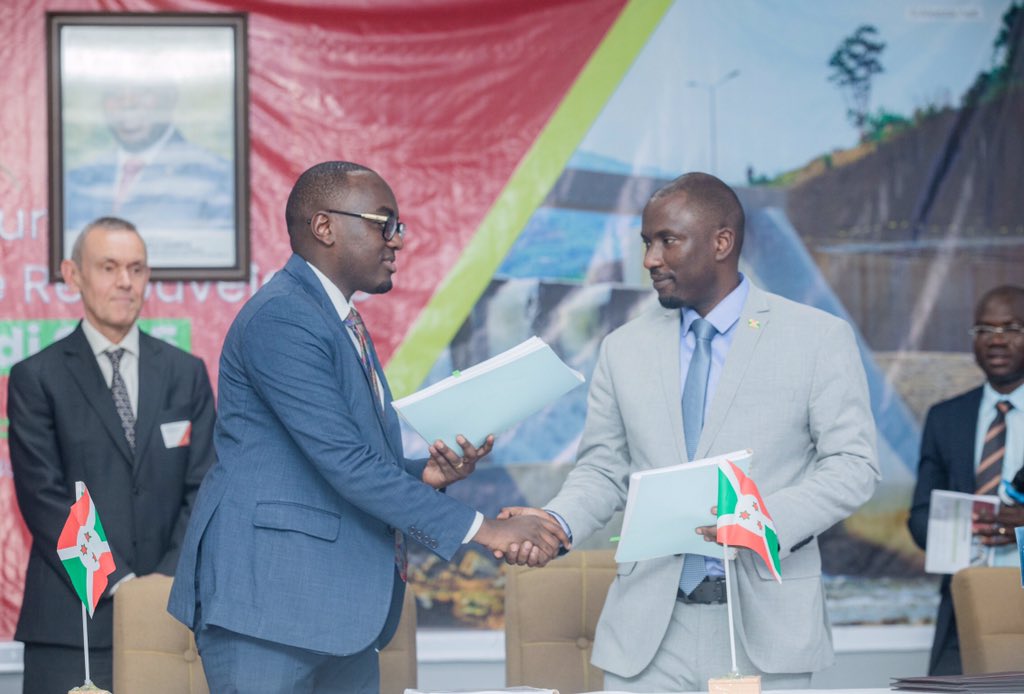

🔴⚡️ 𝗗𝗘 𝗟'𝗔𝗖𝗖𝗢𝗥𝗗 𝗔̀ 𝗟𝗔 𝗠𝗜𝗦𝗘 𝗘𝗡 Œ𝗨𝗩𝗥𝗘 : 𝗟𝗘 𝗕𝗨𝗥𝗨𝗡𝗗𝗜 𝗦𝗜𝗚𝗡𝗘 𝗨𝗡 𝗣𝗔𝗥𝗧𝗘𝗡𝗔𝗥𝗜𝗔𝗧 𝗣𝗨𝗕𝗟𝗜𝗖-𝗣𝗥𝗜𝗩𝗘́ (𝗣𝗣𝗣) 𝗘𝗧 𝗨𝗡 𝗖𝗢𝗡𝗧𝗥𝗔𝗧 𝗗'𝗔𝗖𝗛𝗔𝗧 𝗗'𝗘́𝗟𝗘𝗖𝗧𝗥𝗜𝗖𝗜𝗧𝗘́ (𝗣𝗣𝗔) 𝗣𝗢𝗨𝗥 𝗟𝗘 𝗣𝗥𝗢𝗝𝗘𝗧 𝗛𝗬𝗗𝗥𝗢𝗘̈𝗟𝗘𝗖𝗧𝗥𝗜𝗤𝗨𝗘 𝗗𝗘 𝗪𝗔𝗚𝗔 (𝟮 𝗠𝗪), 𝗘𝗡 𝗣𝗥𝗢𝗩𝗜𝗡𝗖𝗘 𝗗𝗘 𝗚𝗜𝗧𝗘𝗚𝗔.

=====================

🔹 Le 27 novembre 2025, le Gouvernement de la République du Burundi et Waga Hydropower Limited, la société de projet (SPV) mise en place par le consortium KAGE-Malthe Winje, ont signé le contrat de Partenariat Public-Privé (PPP) ainsi que le Contrat d'Achat d'Électricité (PPA) pour le développement de la centrale hydroélectrique de Waga d'une capacité de 2 MW, située en province de @Gitega.

✍️ La signature de ces accords constitue une étape majeure dans la réalisation des objectifs du Gouvernement visant à accroître l'accès à l'électricité et s'inscrit pleinement dans le Plan National de Développement.

🔹Cette avancée a été rendue possible grâce à l'implication coordonnée de plusieurs institutions nationales et partenaires techniques clés, notamment le @mrmeict, le Ministère des @FinancesBdi, ainsi que la @Regideso_bdi , aux côtés des partenaires du consortium, Malthe Winje Infrapower AS et KAGE Ltd.

📌 Waga Hydropower Limited est la société de projet créée par KAGE, développeur burundais spécialisé dans l'hydroélectricité, et Malthe Winje Infrapower AS, une entreprise norvégienne forte de plus de 100 ans d'expérience dans le développement et la construction d'infrastructures critiques et de centrales hydroélectriques de petite et moyenne taille en Afrique de l'Est et en Europe.

📍💬À cette occasion, le Directeur Général de KAGE Ltd, Monsieur Kaze Delphin, a déclaré : « Avec la signature des contrats PPP et PPA, le projet Waga passe de la vision à la mise en œuvre, nous rapprochant d'un Burundi où chaque communauté pourra accéder à une énergie propre, fiable et abordable. Cette étape démontre que notre pays est prêt à accueillir des projets d'énergie renouvelable structurés, transparents et attractifs pour les investisseurs »

📍💬 Et d’ajouter : « Chez KAGE, nous sommes fiers de construire cette dynamique aux côtés de Malthe Winje Infrapower, dont l'expérience centenaire et l'engagement ont été déterminants pour faire de Waga un projet bancable et à fort impact pour le Burundi. »

Pour plus d’info, contactez au :257 76 348 288 |️ 27 66 99 61 00

kazegreeneconomy.com mwip.no

info@kazegreeneconomy.com firmapost@mwg.no

#lesbeautesdecheznous #akezanet #energie #Burundi

9

25

8,736

17 Dec 2025

🇮🇳🫡 Indian Army convoy train crosses the world’s highest railway bridge the iconic Chenab Rail Bridge.

A powerful symbol of engineering excellence, strategic strength, and national pride.

#ChenabRailBridge #IndianArmy #NewIndia #InfraPower

1

3

154

5 Nov 2025

Dharan Infra Solar, a wholly owned subsidiary of EPC company Dharan Infra-EPC, has executed a supply agreement with Skymax Infrapower, an infrastructure company, for 75 MW of #solarpower projects spread across nine sites in Nanded, #Maharashtra.

mercomindia.com/dharan-infra…

2

4

567

1 Nov 2025

Dharan Infra-EPC signs Rs 215-cr supply agreement with Skymax Infrapower

economictimes.indiatimes.com…

1

4,404

7 Oct 2025

पाँच वर्षों की अथक मेहनत, हजारों किलोमीटर सड़कें 🔥

बिहार के विकास की धड़कन बना पथ निर्माण विभाग। :- @NitinNabin जी

#BiharDevelopment #InfraPower #NDA

9

9

67

6 Aug 2025

A $500B valuation for a private AI firm shows where the world’s real power is shifting.

This isn't just tech hype-it's centralization of intelligence, infrastructure, and global narrative control.

The AI capital era is here.

#AIValuation #OpenAI #AIGovernance #InfraPower

4

105

29 Jul 2025

🚪 Season 5 is knocking…

🟢 Nodes are running full throttle…

🤝 Partnerships are rolling in fast…

The game has changed and those who were early are about to reap the rewards!

@BeamableNetwork

@DrewBleam

@PlayPudgyParty

#Beamable #NodeSeason5 #InfraPower #CryptoGaming

1

6

57

28 Jul 2025

🧪 While Beamable is cooking something special behind the scenes…

❄️ The penguins don’t stop! They’re enjoying every second of Beamable’s powerful infrastructure.

@BeamableNetwork

@PlayPudgyParty

@DrewBleam

#Beamable #Solana #Web3Gaming #InfraPower #BuildersNeverSleep 🐧🔥

2

1

10

70

18 Jul 2025

The Unseen Infrastructure vs The Quiet Revolution

@Novastro_xyz

You won’t see Novastro on TikTok. But you’ll feel it — every time a real estate deal goes global in seconds or an invoice is traded like a token. That’s the silent power of infra done right.

@NetworkNoya

NOYA won’t yell. It listens. It learns. It evolves. It becomes better each day you use it. A revolution doesn’t need hype — it needs persistence. NOYA is patience made code.

#InfraPower #AIRevolution #Web3Quietly

6

6

104

14 Jul 2025

Infra is the new spotlight 🚨

No more silent backend — @OpenledgerHQ, @elympics_ai, @recallnet, @vooi_io, @JoinSapien, @tenprotocol — all rewriting the Web3 playbook.

Builders, this is our moment. Let’s rise 🚀

#Web3 #Crypto #Blockchain #InfraPower #nextgentech

4

1

15

163

14 Jul 2025

When the infra-core of Web3 starts humming in unison, it sounds like this:

🧠 @recallnet gives AI agents memory

⚙️ @vooi_io launches seamless cross-chain trading

🎮 @LumiterraGame expands GameFi to the world

🔐 @tenprotocol quietly scales past tech giants

🛰️ @theblessnetwork takes DePIN testnet live

💳 @Tabichain onboards users via TabiPay

🧠 @OpenledgerHQ launches $25M AI fund

Decentralized coordination is no longer a dream—

it's a stack.

And the stack is alive.

#KaitoAI #YapperLeaderboard #Web3Evolved #InfraPower #DePIN #GameFi #AIReputation #CrossChain

2

35

30 Jun 2025

You don’t need to buy expensive hardware to earn in Web3.

You just need a browser internet.

@theblessnetwork turns any device into a micro-data center.

Now that’s decentralization.

@kaitoAI supports it. @cookiedotfun logs it.

#EarnWithDevices #InfraPower

2

2

21

26 Jun 2025

🇳🇴🤝🇧🇮 Witnessing partnerships being created: Government of Burundi, Malthe Winje Infrapower & KAGE Ltd sign an MoU to boost Burundi’s energy production and launch the 3.7 MW Muhira hydro project. #EnergyTransition #Burundi #Norway

8

341

25 Jun 2025

Essel Group की एंटिटीज Konti Infrapower और Multiventures ने Kotak AMC के खिलाफ NCLT में मामला दर्ज कराया

#Essel_Group #NCLT

5

542

19 Jun 2025

From humble homes to towering infrastructures, one name stands behind it all - SG TMT.

Because real strength isn’t just seen, it’s felt in every foundation laid.

🔗 sgmart.co.in | 📞 91 9266157778

#Croatia #Khamenei #IranIsraelConflict #SGMart #Armenia #InfraPower

2

1,099

11 Jun 2025

📢 ये है विकसित भारत का अमृत काल! 🇮🇳

🚆 राजमार्ग हों या रेलवे,

🏗️ पुल हों या एक्सप्रेसवे,

🏙️ स्मार्ट सिटीज़ हों या वर्ल्ड क्लास एयरपोर्ट्स —

देश का हर कोना बन रहा है विकास का उदाहरण।

#11YearsOfInfraRevolution

क्योंकि देश में है मोदी सरकार। 💪

#ViksitBharat #InfraPower #ModiHaiToMumkinHai #TransformingIndia #NewIndia #AmritKaal #IndiaOnTheMove #InfraGrowth #PMModiLeadership #NeelRao #BJPNarmada

@narendramodi @AmitShah @JPNadda @CRPaatil @CMOGuj @Bhupendrapbjp @sanghaviharsh @BJP4Gujarat @BJP4India

1

25

30

147