May 11

Every day for the next long while, I'm going to tear down a new public software company and highlight the AI risks/opportunities around it- products launched to date, top startups, key quotes from earnings calls, etc.

Day 46: Guidewire $GWRE, which features one of the highest multiples in software

Peak share price: $260.71 (Sep 5, 2025)

Share price today: $132.95 (-49%)

EV today: $11.04bn

ARR today: $1.44bn ( 24% Y/y). Guidewire has an upfront to subscription transition under

NRR: Not disclosed, but does discuss 99% gross retention

EV/ARR: 7.7x

GAAP Operating Margin: 11%

EV/Run-rate GAAP EBIT: 72x

Headcount: 4,260 ( 12% Y/y)

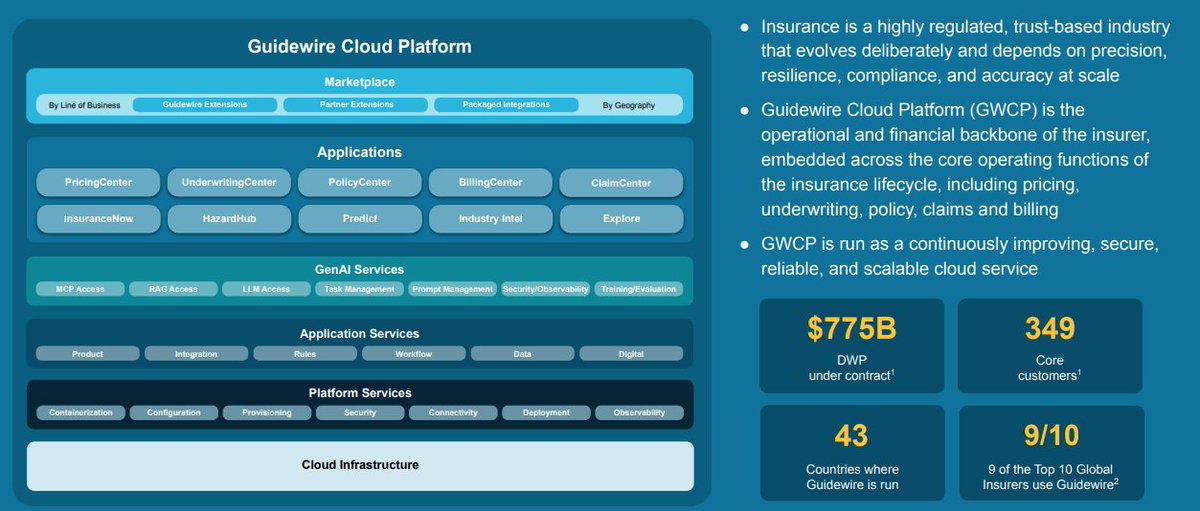

What Guidewire does:

Guidewire is the dominant core software platform for the property and casualty insurance industry. It sells software for each of the three pills- PolicyCenter (quoting, underwriting, issuing, etc.), ClaimCenter (claims management) and BillingCenter (straightforward, I hope!).

This is heavy, heavy, ERP-ish software that is often customized or heavily configured customer tby customer, and Guidewire has expanded the suite over time through acquisitions and organic product development.

AI bear case:

Guidewire is a vertical SaaS heavyweight and it shows up in the lack of punchy bear case.

Certainly if AI dramatically accelerates/speeds up software implementation, some of the famously high switching costs could go away, reducing the defensibility and pricing power of Guidewire's position.

Beyond that, a concern for Guidewire is that the software (like ERP, and very unlike Bentley/Autodesk), is heavily customized for customers- which raises the risk that they eventually opt to build it themselves as the cost of software falls.

Finally, some are concerned about secular risk to the auto insurance market (h/t @Anonymo09273651 from the comments). Auto is 35-40% of P&C volume in the US, so a sustained decline in auto insurance could be a meaningful headwind for Guidewire.

AI bull case:

Of all the things to vibecode, core transactional systems seem pretty far down the list and Guidewire is as core as it gets. Beyond that, the industry it sells into is famously conservative (see: still moving to the cloud)- and implementations require retraining thousands of humans (not yet clear how AI fully solves the pain of that!).

As such, it is easy to see Guidewire being an AI beneficiary over time- taking advantage of its entrenched market position to cross-sell value-added products and services into its customer base.

Finally (and importantly) AI seems to be encouraging customers to complete the on-prem to cloud transition (analogous to the dynamics Five9 has seen, without the existential risk), potentially accelerating a key strategic priority for Guidewire.

AI traction:

No specific metrics disclosed.

Adjacent AI-native startup summary:

Guidewire's most relevant competitor continues to be @DuckCreekTech (1,878 employees, -1% Y/y, Vista-owned).

Other relevant insuretech players are Socotra (192 employees, 14% Y/y), Britecore (99 employees, 9% Y/y) and Shift Technology (616 employees, 8% Y/y).

Management Quotes:

"There has obviously been a significant discussion across the market about the pace of generative AI advancement and its implications for the overall software category. What we are seeing in practice at Guidewire is increased demand for InsuranceSuite and InsuranceNow. The potential for generative AI in insurance is clear, and this is increasing the urgency for insurers to modernize legacy systems."

"Broadly speaking, AI for us is immensely beneficial and driving an acceleration in our business. It's helping create demand for core system modernization. It's helping us accelerate our development velocity. It's helping us accelerate our implementation velocity and will accelerate everything that customers and partners do with Guidewire."

"And I would definitely say that it would be quite a bold statement for us to say we're going to own AI in the insurance industry. What we're going to own in the insurance industry is core systems that I am very confident in. We see that momentum, and we see that insurance companies need to modernize. They need these core stacks to work effectively. There's plenty of insurance companies that need Guidewire to own the outcome with respect to AI capabilities. But running an open model where we see other companies that are going to use other components from other AI technologies in and with Guidewire, it's absolutely part of the medium-term outlook. And I think that this is really very, very important to understand."

"Our new embedded AI solution, ProNavigator, also got off to an incredible start with 9 deals in the second quarter. Notable deals included Aviva Canada and Gore Mutual who want to leverage this agentic assistant to deliver answers, suggestions and ultimately, actions embedded right in our core UI. ProNavigator leverages InsuranceSuite data and insurance standard operating procedures to increase employee efficiency and minimize claims leakage."

"And so the question about are we thinking about this from a -- are we thinking about generative AI from a software development perspective? Is it an efficiency play? Or is it a value play? Right now, I'm very much thinking about it as a value play. I think that we can take the developers that we have that know Guidewire, right? They know the technology stack and the cloud technology stack at Guidewire, and they know the insurance industry and they know what to do and we can accelerate. This is going to create more value for Guidewire, and it's going to help us continue the pace or maybe hopefully accelerate the pace that we've established with cloud."

Commentary:

Guidewire is another example that encourages caution when grouping public software companies together as a monolith. It has a genuine claim to an AI tailwind (although from accelerated modernization, not AI itself) and a credible path to monetizing AI as it becomes relevant for the insurance industry. Given the immense stickiness of its core solutions, anyone looking to penetrate/sell to the insurance industry will almost certainly seek to collaborate closely with Guidewire. Thus far, AI has not changed the competitive set or the unit economics of building a competitor. I'm not surprised that Guidewire trades at a heady (in today's world 7.7x EV/rev multiple.

3

11

5,277

🚨 Webinar: How insurers and MGAs are embedding AI directly into InsuranceNow with Claims Intel and Predict.

If you're looking for practical ways to protect loss ratios in a tough market, this webinar shows exactly what it looks like in production.

➡️ bit.ly/4sO2Bhc

1

3

88

3 Jun 2025

Key Takeaways from $GWRE's Earnings Call

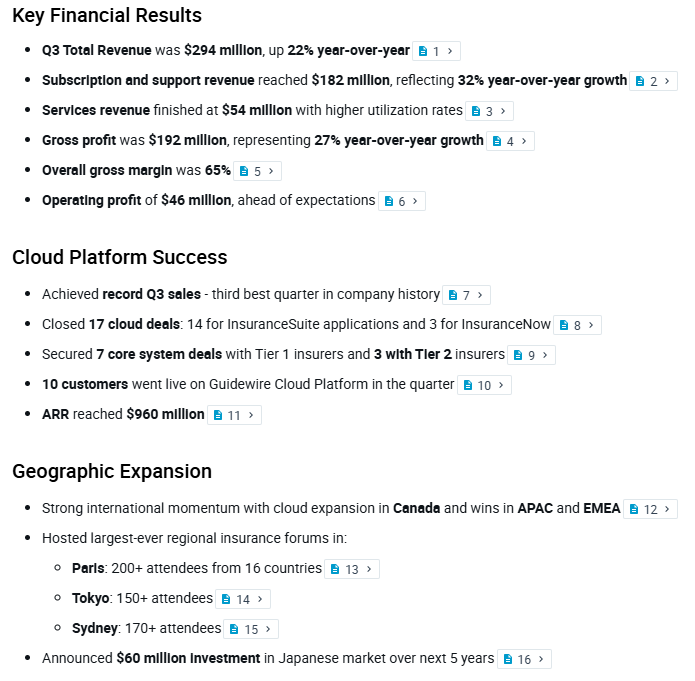

Key Financial Results:

- Q3 Total Revenue was $294 million, up 22% year-over-year

- Subscription and support revenue reached $182 million, reflecting 32% year-over-year growth

- Services revenue finished at $54 million with higher utilization rates

- Gross profit was $192 million, representing 27% year-over-year growth

Cloud Platform Success:

- Achieved record Q3 sales - third best quarter in company history

- Closed 17 cloud deals: 14 for InsuranceSuite applications and 3 for InsuranceNow

- Secured 7 core system deals with Tier 1 insurers and 3 with Tier 2 insurers

- 10 customers went live on Guidewire Cloud Platform in the quarter

- ARR reached $960 million

Financial Guidance and Outlook:

- Raised ARR outlook to $1.012 billion to $1.022 billion (17-18% year-over-year growth)

- Updated total revenue guidance to $1.178 billion to $1.186 billion

- Expect subscription revenue of approximately $660 million

- Projecting services revenue of approximately $215 million

- Anticipate subscription and support gross margin between 69% and 70% for the year

3

1

4

1,947

15 Jan 2025

Harnessing #InsuranceNow and #HazardHub, Innovated Holdings transformed its operations: faster quoting (70%), quicker #claims (25%), and a stronger #customerexperience ( 5 NPS). Find out how they’re driving #growth: bit.ly/4he2DJA

1

144

17 Oct 2024

Guidewire InsuranceNow has been recognized as a Challenger in the Gartner Magic Quadrant for SaaS P&C Core Platforms, North America! Read the press release bit.ly/4dVnTSe and check out the blog bit.ly/3Y2Z4xW.

2

2

138

20 Aug 2024

When is the best time to buy insurance?

Don't put your insurance cover off. It should be the first thought when you buy a high-value item, acquire property, start a business, and make big ventures in life. Keep yourself protected. #InsuranceNow #SmartChoices

1

2

31

1 Nov 2023

Velocity Risk established a clear objective, partnered with Guidewire and @Cognizant, and achieved a swift and on-budget InsuranceNow implementation. Check out their story here: bit.ly/3MMY3p5

3

185

28 Sep 2023

Transform Insurance Operations with Guidewire and One Inc’s New ClaimsPay app for InsuranceNow hubs.la/Q023zTLd0

2

30

11 Jan 2023

Enhancing the member experience is priority for @ArmedForcesIns. Check out how the insurer improved in many areas, including in pricing and claims management with InsuranceNow: guidewire.com/video/63148835…

#insurance #propertyandcasualtyinsurance #pandcinsurance #engage

1

2

231

3 Jun 2022

Eager to learn Elysian? Guidewire Education just launched 12 New Features courses for InsuranceSuite, Digital, Data, and InsuranceNow products. Check out the list of courses and start learning today! bit.ly/3NRvzbB #GuidewireElysian #education #learning

2

2

26 May 2022

Lititz Mutual Insurance Company recently selected #GuidewireInsuranceNow to increase #agent and #policyholder #digital engagement for #businessgrowth. Learn more about InsuranceNow here bit.ly/3PKoBa7 #insurance #innovation #underwriting

2

22 Apr 2022

Lititz Mutual Insurance Company recently selected #GuidewireInsuranceNow to increase #agent and #policyholder #digital engagement for #businessgrowth. To learn more about InsuranceNow, please visit bit.ly/3EG5vg4 #insurance #innovation

1

1

24 Mar 2022

We're pleased to welcome Lititz Mutual Insurance Company to the Guidewire customer family with its #GuidewireInsuranceNow selection to improve customer service and grow its business! bit.ly/3D9m6s6 #insurance #innovation #insurancenow

1

19 Mar 2022

Did you know that many of the newly created ecosystems have become hyper-scale #digitalplatforms that serve a multitude of customer #interactions?

bit.ly/3gGkQlE via @SabineVdL @AlchemyCrewLtd

#digital #ecosystem #insurtech #fintech #insurancenow

1

16 Mar 2022

U.S. insurers! Check out the blog post, "#GuidewireInsuranceNow: The Power of 'Small Guidewire'," where Darin Reffitt discusses his journey as the new InsuranceNow product marketer and why it's the best product for certain insurers. bit.ly/3u69rlw #insurance #innovation

2

3

7 Mar 2022

The pandemic forced our hands. We are seeing today is faster, consistent, and all-pervasive progress with strategic digital partnerships.

Find out why:

👇🏽

bit.ly/3gGkQlE via @SabineVdL @AlchemyCrewLtd

#digital #ecosystem #insurtech #fintech #insurancenow

1

2

3

28 Feb 2022

Qualitas Insurance Company recently selected #GuidewireInsuranceNow to improve customer service and grow its business. Learn more about InsuranceNow here: bit.ly/36R78uP #insurance #innovation #GuidewireLivePredict #coreoperations #predictiveanalytics

1

24 Jan 2022

We recently announced @CUREInsurance's successful #GuidewireInsuranceNow implementation to increase business agility and enable faster speed-to-market. To learn more about InsuranceNow, please visit bit.ly/30zTAAF #insurance #innovation #cloudcomputing

2

2