20. RateGain partners with ZentrumHub for simplified hotel distribution and global travel connectivity. #RateGain #ZentrumHub #TravelTech

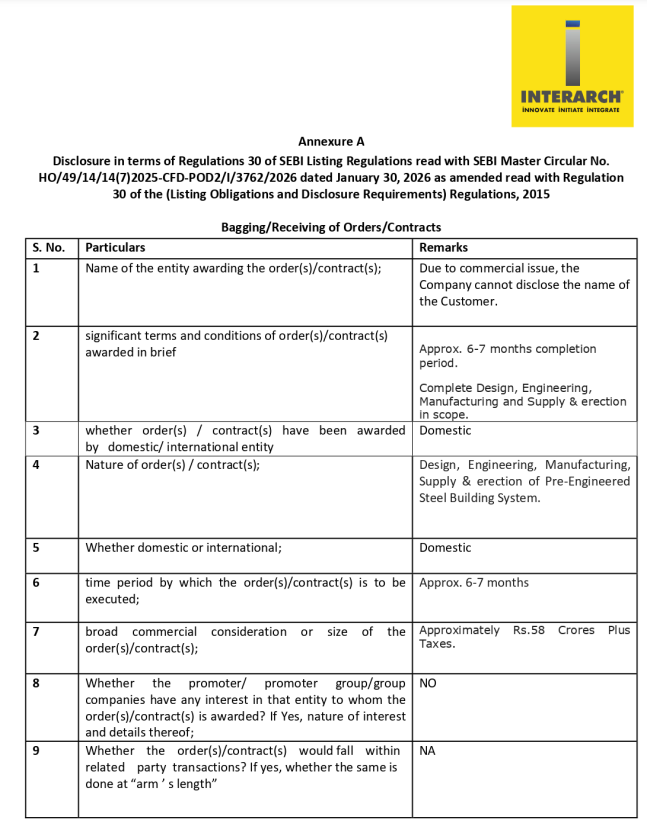

21. Interarch Building Solutions wins Rs 58 cr Pre-Engineered Steel Building order. #InterarchBuilding

135

Interarch Building Solutions has secured Rs.58 Cr (Excl. Taxes) Domestic order from a customer for Design, Engineering, Manufacturing, Supply & erection of Pre-Engineered Steel Building System.

Time Period : Approx. 6-7 months

#InterarchBuilding #Interarch #PEB

76

May 15

Interarch Building Solutions Ltd Concall Summary for Q4FY26

🔹 MANAGEMENT COMMENTARY

• Company positioned as capital goods partner

• Focus shifting toward new-age sectors

• FY26 revenue exceeded internal guidance

• Heavy steel structures gaining priority

• Export expansion focus intensified

🔹 FUTURE OUTLOOK

• FY27 revenue guided ₹2,150–2,200 crore

• FY28 revenue target ₹2,500 crore

• EBITDA margins guided 9.3–10%

• HSS production target 40,000 tons

• Gujarat plant commissioning by July

🔹 INDUSTRY TRENDS

• PEB saves nearly 50% construction time

• Semiconductor sector demand accelerating

• Renewable energy demand remained strong

• Steel prices remain highly cyclical

• Data center demand growing rapidly

🔹 COMPETITIVE POSITIONING

• Integrated design-to-erection model differentiated

• Preferred partner for new-age industries

• High-rise structural capabilities expanding

• Complex projects improving value-chain position

• Non-industrial opportunities expanding rapidly

🔹 RISKS & CONCERNS

• Skilled labor shortages remain major concern

• FY26 operating cash flow remained negative

• Inventory levels increased significantly

• Election-related labor migration impacted execution

• Larger projects increasing working capital

🔹 GROWTH DRIVERS

• Andhra HSS plant scaling aggressively

• North America export JV signed

• Robotics and welding automation explored

• QIP fundraising under evaluation

• HSS vertical targeting data centers

🔹 PRODUCT & BUSINESS TRENDS

• Industrial segment dominates current orderbook

• Non-industrial contribution expected rising

• Premium structural projects increasing steadily

• Heavy-duty steel demand accelerating

• Data center opportunities expanding rapidly

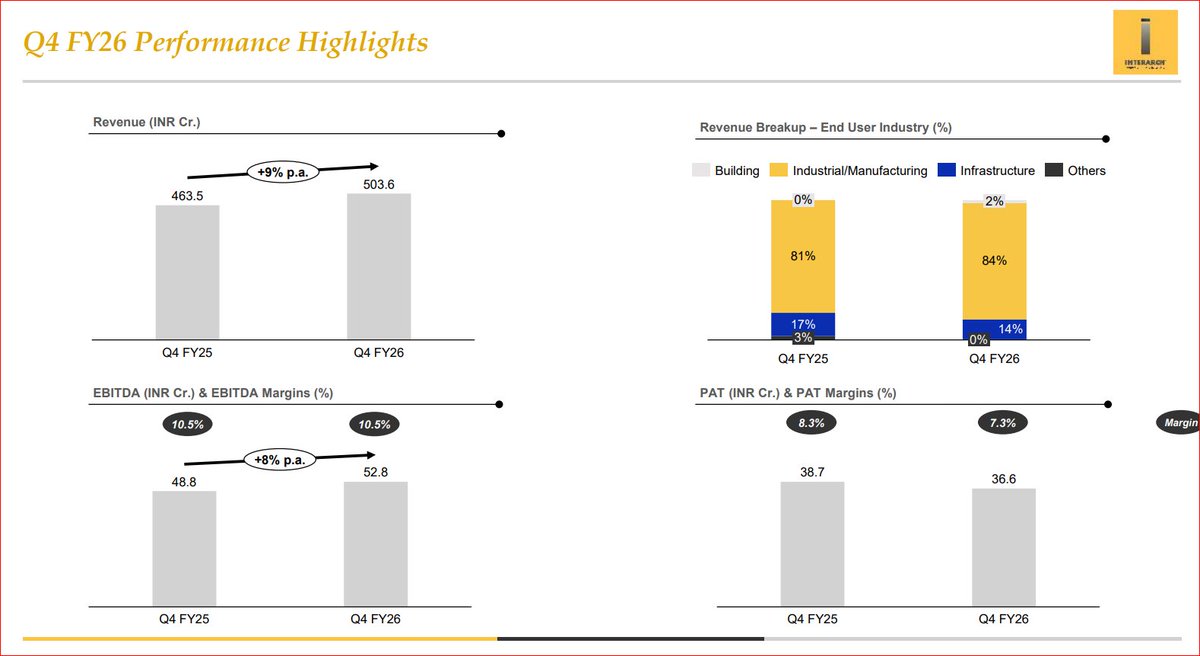

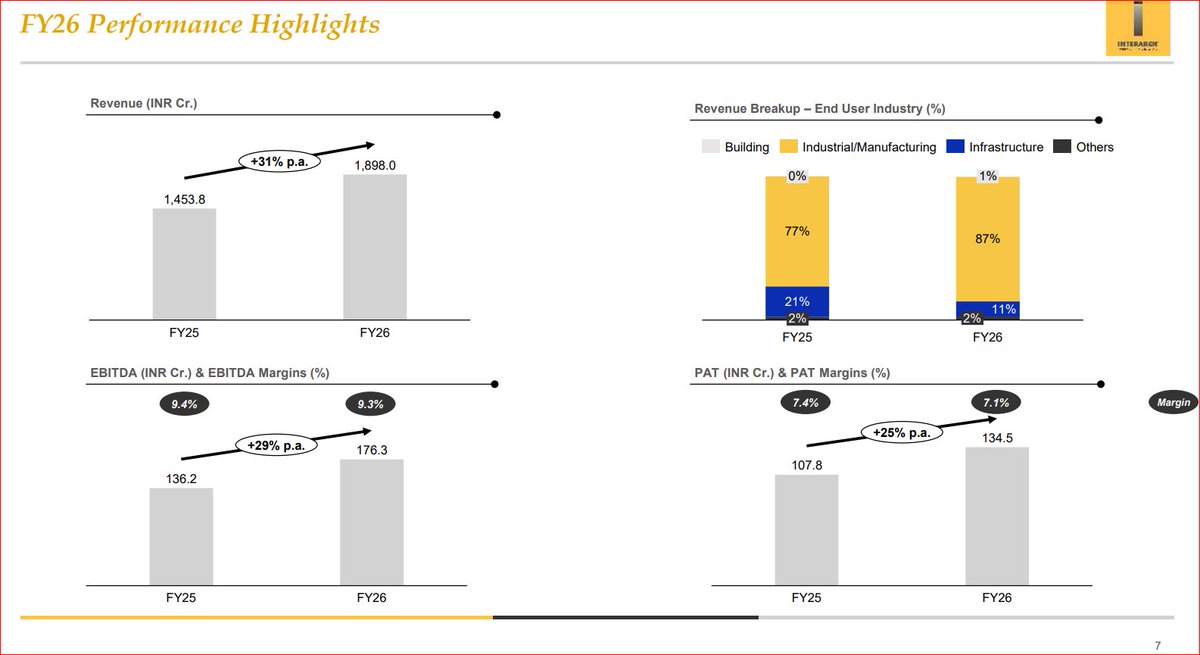

🔹 FINANCIAL HIGHLIGHTS

• FY26 revenue reached ₹1,898 crore

• Revenue grew 30.6% YoY

• EBITDA stood at ₹176 crore

• EBITDA margin remained 9.3%

• PAT increased to ₹135 crore

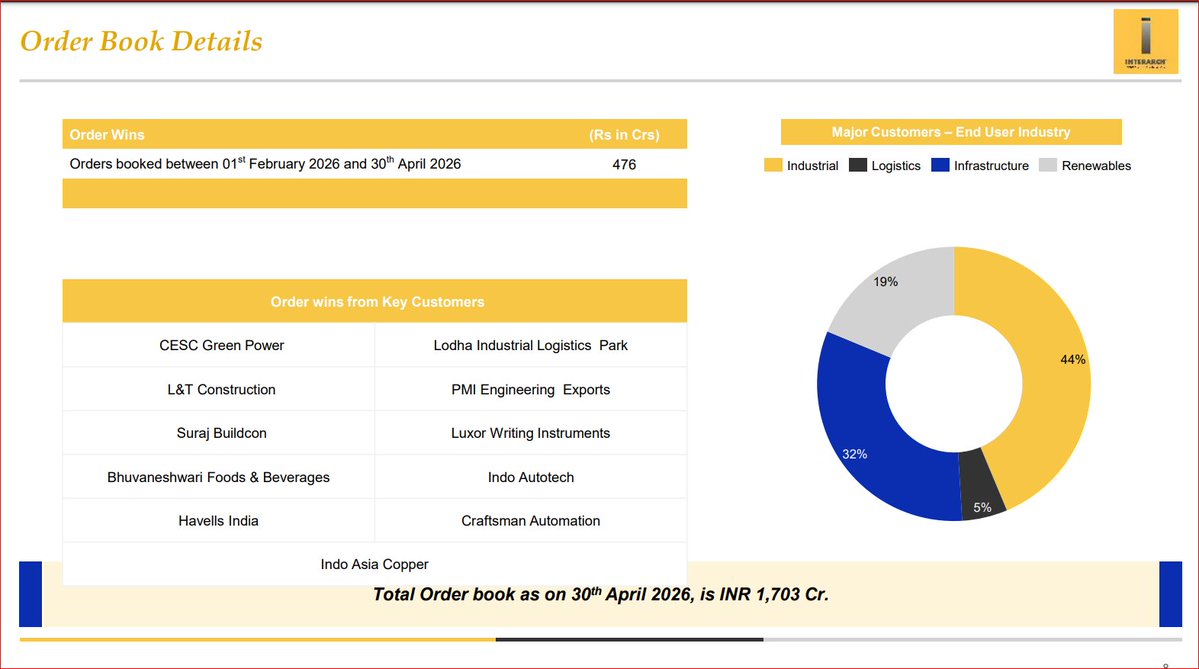

• Orderbook stood at ₹1,700 crore

🔹 SENTIMENT ANALYSIS

• Overall tone remained highly positive

• Confidence around demand remained strong

• Capacity expansion accelerating aggressively

• Global expansion strategy clearly emphasized

• Management outlook remained highly optimistic

🔹 KEY TAKEAWAYS

• Interarch entering major expansion phase

• HSS becoming critical growth driver

• Export opportunities improving materially

• Strong orderbook ensuring revenue visibility

• Automation focus improving scalability

#Interarchbuilding #Q4FY26 #stockmarket

2

1

4

575

May 14

#InterarchBuilding Solutions shares plunge 17%, most on record, after Q4 profit falls

@VivekIyer72 @ShlokaBadkar

cnbctv18.com/market/interarc…

1

6

3,555

Feb 3

#StocksOnTheMove | #Stocks Swings To Earnings

- #VarunBeverages

- #AtherEnergy

- #InterarchBuilding

- #CityUnionBank

- #UtkarshSmallFinanceBank

@VivekIyer72 with the #earnings fineprint. #CNBCTV18Market

1

4

1,583

Jan 14

#MarketsWithBS | Interarch Building share price rises 3.5% on securing ₹130-crore order

#Stocks #markets #stockmarket #sharemarket #InterarchBuilding

mybs.in/2g366io

479

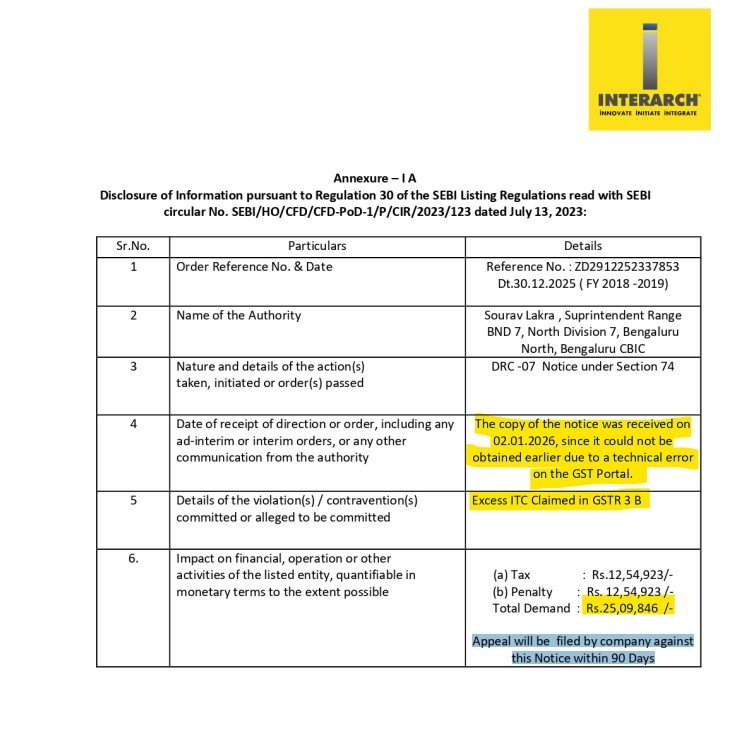

Interarch Building Solutions | Reason Behind Today’s Breakdown

The recent price breakdown in Interarch Building Solutions Ltd appears to be driven by a negative regulatory disclosure reported to exchanges on 02 January 2026.

What happened?

The company informed NSE & BSE about receiving a GST DRC-07 demand notice from the GST department related to FY 2018–19.

Nature of the issue:

• Allegation of excess Input Tax Credit (ITC) claimed in GSTR-3B

• Notice issued under Section 74 of the GST Act

Financial impact disclosed:

• Tax demand: ₹12.54 lakh

• Penalty: ₹12.54 lakh

• Total demand: ₹25.09 lakh

Additional clarity:

• Notice received on 02 Jan 2026 due to earlier technical error on GST portal

• Company has stated it will file an appeal within 90 days, so the matter is under dispute

Market reaction:

Despite the amount being relatively small and related to an old financial year, markets often react sharply to regulatory and compliance-related news, especially when sentiment is weak — leading to today’s price breakdown.

Key takeaway:

This is a regulatory overhang, not an operational update. Price action reflects sentiment-driven selling, not business performance deterioration.

#InterarchBuilding #GSTNotice

3

651

Nature warns before it reacts. With #InterarchLife–#LGFS, we build with the terrain—minimising excavation, preserving slopes, in harmony

#InterarchBuilding #BuildingWithNature #LGFS #InterarchLife #ESGInAction #HillConstruction #MinimalExcavation #SustainableInfrastructure

2

55

19 Dec 2025

20 STOCKS WHICH REPORTED STRONG RESULTS AND STRONG FUTURE GUIDANCE 💪

BOOKMARK THIS POST ✅️

1. #V2Retail

2. #MCX

3. #SMLMahindra

4. #EicherMotors

5. #MahindraAndMahindra

6. #BSE

7. #OSELDevices

8. #CUPID

9. #KRNHeat

10. #MuthootFinance

11. #YatharthHospital

12. #PNGadgil

13. #InterarchBuilding

14. #JeenaSikho

15. #BlackBuck

16. #DataPatterns

17. #YatraOnline

18. #FrontierSprings

19. #ThomasScott

20. #Cupid

No buy/sell reco.

I am not an advisor!

2

372

20 STOCKS WHICH REPORTED STRONG RESULTS AND STRONG FUTURE GUIDANCE 💪

BOOKMARK THIS POST ✅️

1. #V2Retail

2. #MCX

3. #SMLMahindra

4. #EicherMotors

5. #MahindraAndMahindra

6. #BSE

7. #OSELDevices

8. #CUPID

9. #KRNHeat

10. #MuthootFinance

11. #YatharthHospital

12. #PNGadgil

13. #InterarchBuilding

14. #JeenaSikho

15. #BlackBuck

16. #DataPatterns

17. #YatraOnline

18. #FrontierSprings

19. #ThomasScott

20. #Cupid

No buy/sell reco.

I am not an advisor!

3

12

99

7,508

30 STOCKS WHICH REPORTED STRONG RESULTS AND STRONG FUTURE GUIDANCE 💪

BOOKMARK THIS POST ✅️

1. #V2Retail

2. #MCX

3. #SMLMahindra

4. #EicherMotors

5. #MahindraAndMahindra

6. #BSE

7. #OSELDevices

8. #CUPID

9. #KRNHeat

10. #MuthootFinance

11. #YatharthHospital

12. #PNGadgil

13. #InterarchBuilding

14. #JeenaSikho

15. #BlackBuck

16. #DataPatterns

17. #YatraOnline

18. #FrontierSprings

19. #ThomasScott

20. #InfibeamAvenues

21. #AetherIndustries

22. #RenaissanceGlobal

23. #AdvancedEnzyme

24. #Cupid

25. #QualityPower

26. #NisusFinance

27. #TransrailLighting

28. #VishalMegamart

29. #TemboGlobal

30. #ZagglePrepaid

No buy/sell reco.

I am not an advisor!

#StockMarketIndia #stockmarketsindia #Nifty #niftycrash #NiftyBank #NIFTYIT #NIFTYMETAL

3

1

4

837

12 Dec 2025

#StockInNews | Interarch Building gets LoI for an order worth ₹84 cr from Shyam Sel and Power

#InterarchBuilding #StockMarket

1

2

1,094

9 Dec 2025

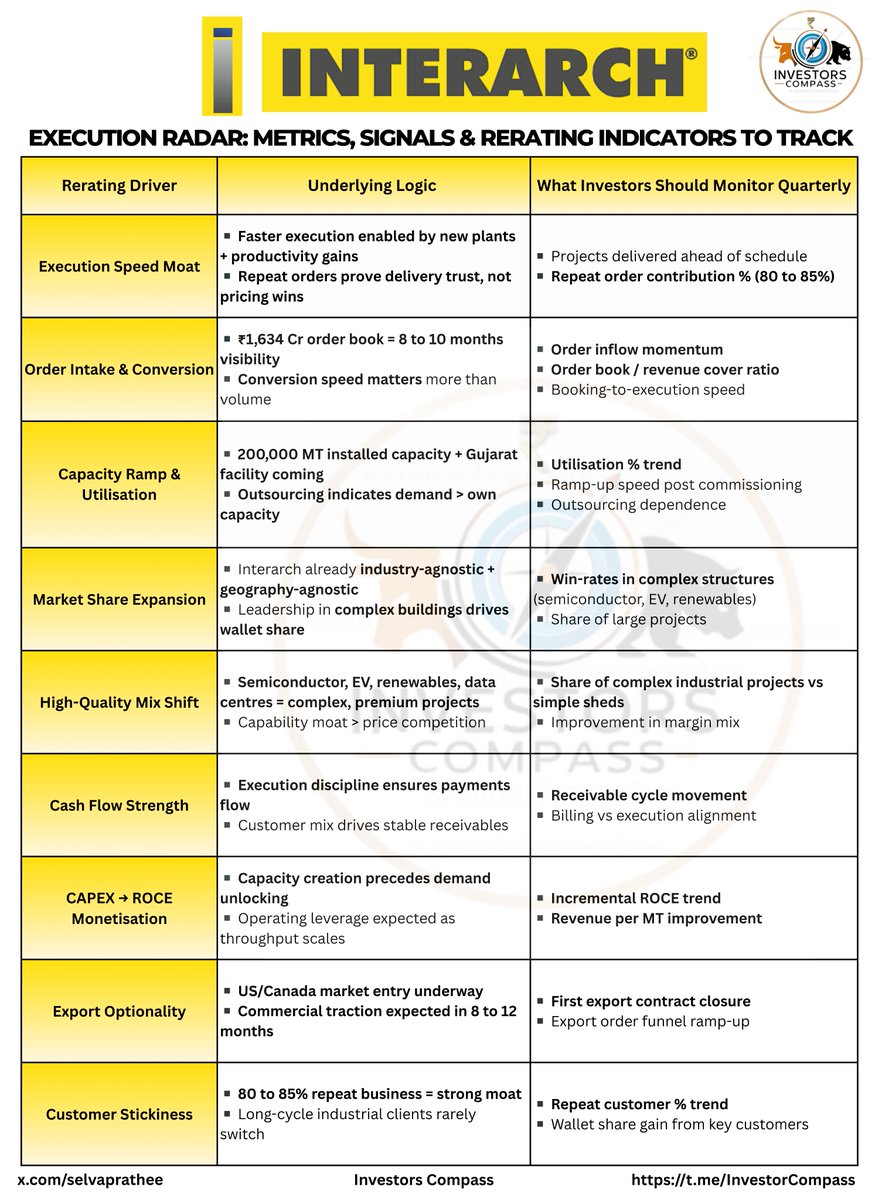

Interarch Building – Execution Radar | Metrics, Signals & Rerating Indicators

- A thread for investors who track delivery > narratives

1️⃣ Execution Speed Moat

▪️ Interarch’s biggest edge is execution velocity, not pricing.

▪️ New plants productivity gains have shortened delivery cycles.

▪️ Proof point: 80 to 85% repeat orders, customers come back only when timelines are met.

➡️ Speed becomes a cultural moat, not easily replicable.

2️⃣ Order Intake & Conversion

▪️ Current order book at ₹1,634 Cr = ~8 to 10 months revenue visibility.

▪️ Management prioritises conversion speed over order hoarding.

▪️ Quality of orders > quantity of orders.

➡️ This protects margins and working capital during scale-up.

3️⃣ Capacity Ramp Is Ahead of the Cycle

▪️ 200,000 MT installed capacity already live.

▪️ Gujarat plant adds the next leg of growth.

▪️ Outsourcing is used tactically, a signal that demand > in-house capacity.

➡️ Capacity readiness sets up operating leverage.

4️⃣ Market Share Expansion (Quiet, Not Loud)

▪️ Interarch is industry-agnostic geography-agnostic.

▪️ Complex buildings restrict competition to only a few credible players.

▪️ Large industrial clients prefer proven execution over lowest bid.

➡️ Market share grows via capability, not aggression.

5️⃣ High-Quality Mix Shift

▪️ Focus areas: semiconductors, EVs, renewables, data centres.

▪️ These projects are complex, timeline-sensitive, and premium priced.

▪️ Capability > commodity pricing.

➡️ Mix improvement is the real margin lever.

6️⃣ Cash Flow Strength

▪️ Execution discipline ensures billing stays aligned with progress.

▪️ Repeat customers reduce receivable volatility.

▪️ No reckless order chasing = better cash predictability.

➡️ This supports self-funded growth, not balance sheet stress.

7️⃣ CAPEX → ROCE Monetisation

▪️ Capacity built before demand peaks.

▪️ As utilisation improves, fixed costs get absorbed faster.

▪️ Revenue per MT becomes the key efficiency metric.

➡️ ROCE expansion is the real rerating trigger.

8️⃣ Export Optionality (Early but Real)

▪️ US & Canada market entry underway.

▪️ Commercial traction expected in 8 to 12 months.

▪️ Exports not in current numbers, optional upside.

➡️ Optionality isn’t priced in yet.

9️⃣ Customer Stickiness = Structural Moat

▪️ 80 to 85% repeat business = strong validation.

▪️ Industrial customers rarely switch once execution trust is built.

▪️ Wallet share expands quietly over time.

➡️ This is how industrial compounders are built.

🔟 Management Execution Culture

▪️ Clear bias towards planning discipline > aggressive growth.

▪️ Capability built across engineering, project management, tech (SAP/AI).

▪️ Long-term view on exports & heavy structures.

➡️ This is execution maturity, not startup expansion.

🧭 Investor Compass Takeaway

- Interarch is entering Phase 2 of its rerating cycle, where delivery, not storytelling, drives valuation.

▪️ Execution velocity > order wins

▪️ Utilisation mix > headline growth

▪️ Repeat customers > one time contracts

▪️ Capacity ahead of cycle = operating leverage setup

No Buy/Sell Recommendation

#StocksInFocus #StocksToWatch #Interarch #interarchbuilding #PEB

17 Feb 2025

🏗️Interarch Building Products - A Detailed Analysis

Interarch is a market leader in Pre-Engineered Buildings (PEB) in India. With strong financials, strategic partnerships, and aggressive capacity expansion, it is well-positioned to double revenue (2X) in the next 3-4 years!

📌 Current Price: ₹1,453

📊 52-Week High / Low: ₹1,925 / ₹1,110

💰 Market Cap: ₹2,417 Cr

🧵

#Interarch #StockMarketIndia #StocksToWatch #StocksToFocus

3

6

36

34,605

8 Nov 2025

INTERARCH BUILDING

#INTERARCHBUILDING

DAILY

#BREAKOUTSTOCKS

CMP: 2520

BREAKING OUT to DEMAND zone on DAILIES 🥳

Whatsapp: chat.whatsapp.com/ECBrLVSmcp…

Telegram: t.me/TradeCymatics

#StocksInFocus #StockMarket #stocks #Nifty #GIFTNIFTY #stockmarkets

487

7 Nov 2025

#BuzzingStocks At 3 pm

#LTFinance

#InterarchBuilding

#Pricol

#NESCO

#BSE

#CDSL

#AngelOne

#AmberEnt

#Venkys

#LumaxIndustries

@hormaz_fatakia #CNBCTV18Market

3

3

1,751

7 Nov 2025

#InterarchBuilding 13% Up today 🔥

Added at 1590 & 1940 for the long term

Next line up:

#Pennar - Earnings tomorrow ✅

#MBEL - Earnings on 11th Nov ✅

PEB sector is doing extremely well 👏

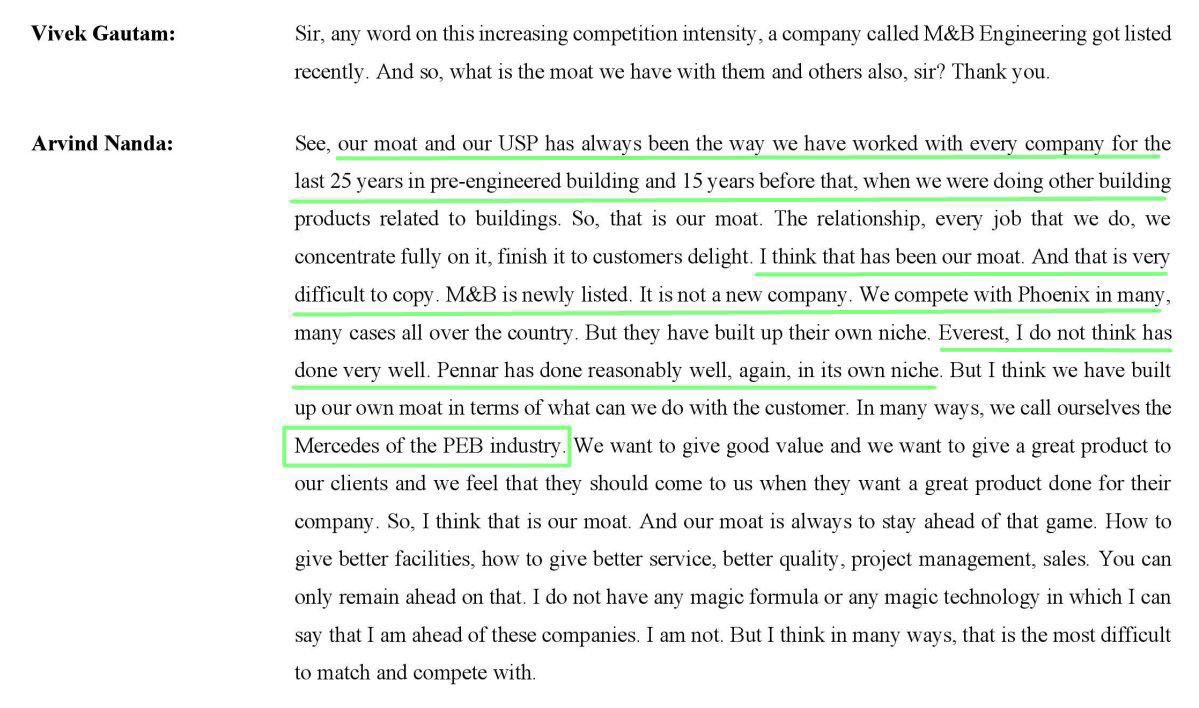

6 Nov 2025

#InterarchBuilding Q2 👏👏

Q1: “We’re the Mercedes of the PEB industry.”

Q2: Performance matched the word — smooth, powerful, and top-class! 🔥

The Mercedes of PEB is racing ahead!

3

62

24,466

6 Nov 2025

#InterarchBuilding Q2 👏👏

Q1: “We’re the Mercedes of the PEB industry.”

Q2: Performance matched the word — smooth, powerful, and top-class! 🔥

The Mercedes of PEB is racing ahead!

5

13

200

22,025

6 Nov 2025

#InterarchBuilding Q2 Result

Revenue Up 26% (QoQ), Up 51% (YoY)

PBT Up 15% (QoQ), Up 59% (YoY)

Net Profit Up 14% (QoQ), Up 56% (YoY)

Blockbuster Numbers 🔥🔥

20 Oct 2025

▶️▶️

Diwali Picks 2025 🌟

➖➖➖➖➖➖➖➖➖➖➖

01) P N Gadgil Jewellers

🌈 CMP - 680

02) Enviro Infra (EIEL)

🌈 CMP - 240

03) Transrail Lightning

🌈 CMP - 735

04) KPI Green Energy

🌈 CMP - 495

5) Interarch Building

🌈 CMP - 2000

Wishing you all a Happy & Prosperous Diwali! May these festive picks shine bright in your portfolio just like the lights of Diwali 🪔💫

#Samvat2082 #DiwaliPicks2025 #investing

1

1

27

4,634

12 Oct 2025

#InterarchBuilding bets on Gujarat expansion to boost FY28 revenues

@hormaz_fatakia @Reematendulkar

cnbctv18.com/business/compan…

1

16

7,871

8 Oct 2025

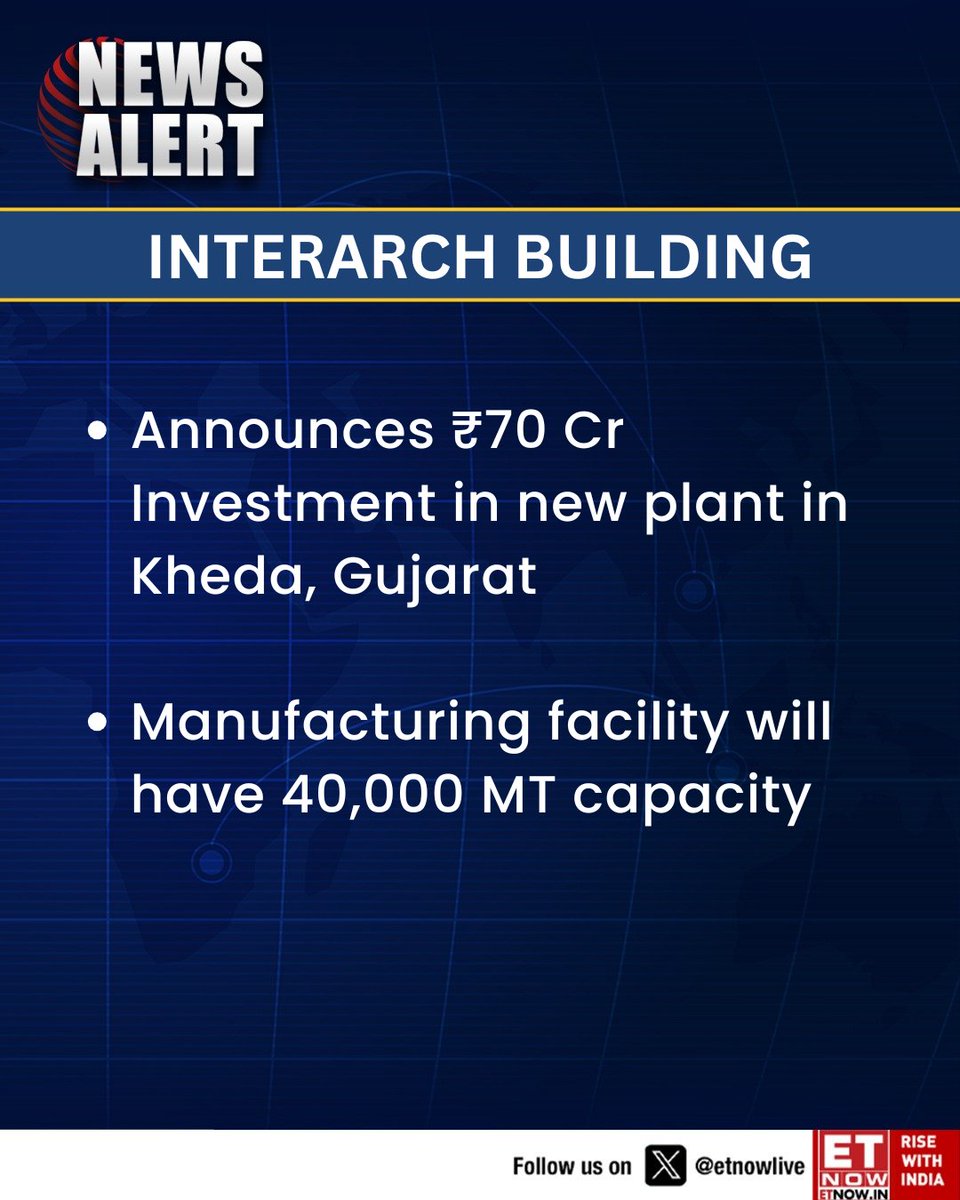

#NewsAlert | Interach Building: Announces ₹70 Cr Investment in new plant in Kheda, Gujarat

#InterarchBuilding #CapacityExpansion #ManufacturingUpdate #IndustrialGrowth

1

6

1,529