May 5

$IDXX Q1 2026 earnings: Stellar Execution Defies Veterinary Visit Headwinds

IDEXX delivered a powerful first quarter, accelerating revenue growth to 14% YoY despite persistent declines in U. S. clinical foot traffic. The company is successfully leveraging pricing power and new product innovations (like IDEXX inVue Dx) to drive diagnostic utilization per visit, completely overwhelming sector-level macro pressures. EPS grew 17% to $3.47, prompting management to confidently raise FY26 guidance across the board. While the top-line story is bulletproof, an aggressive 17% ramp in operating expenses—partially due to R&D and commercial investments—kept reported operating margin expansion to a meager 10 basis points.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐔𝐧𝐬𝐭𝐨𝐩𝐩𝐚𝐛𝐥𝐞 𝐂𝐨𝐧𝐬𝐮𝐦𝐚𝐛𝐥𝐞𝐬 𝐄𝐧𝐠𝐢𝐧𝐞 — IDEXX VetLab consumables grew an explosive 20% reported (15% organic). The premium instrument installed base grew 12%, fueled by 1,100 new IDEXX inVue Dx placements, locking in future high-margin recurring revenue.

• 𝐈𝐧𝐭𝐞𝐫𝐧𝐚𝐭𝐢𝐨𝐧𝐚𝐥 𝐌𝐨𝐦𝐞𝐧𝐭𝐮𝐦 𝐀𝐜𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 — International CAG Diagnostics recurring revenue surged 21% reported (12% organic), proving the commercial footprint expansion strategy is unlocking highly underpenetrated overseas markets.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐌𝐚𝐜𝐫𝐨 𝐕𝐢𝐬𝐢𝐭 𝐏𝐫𝐞𝐬𝐬𝐮𝐫𝐞𝐬 — Underlying U. S. clinical visit volumes remain negative. The company is extracting more revenue from fewer visits, a strategy that relies heavily on pricing power and innovation to sustain growth.

• 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐄𝐱𝐩𝐞𝐧𝐬𝐞 𝐂𝐫𝐞𝐞𝐩 — Operating expenses jumped 17% as reported, severely muting operating margin expansion (only 10 bps). Management is investing heavily in commercial and R&D capabilities, which must generate sufficient top-line return to defend historical margin expansion rates.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🟢

Bullish. IDEXX continues to demonstrate absolute pricing power and innovation dominance. Upgraded FY26 guidance indicates management sees no imminent threat from the broader slowdown in veterinary foot traffic.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢🟢 𝐈𝐃𝐄𝐗𝐗 𝐢𝐧𝐕𝐮𝐞 𝐃𝐱 𝐚𝐧𝐝 𝐂𝐚𝐭𝐚𝐥𝐲𝐬𝐭 𝐃𝐫𝐢𝐯𝐢𝐧𝐠 𝐂𝐨𝐧𝐬𝐮𝐦𝐚𝐛𝐥𝐞𝐬

Accelerating. IDEXX VetLab consumables generated 20% reported revenue growth. The global premium instrument installed base grew 12%, fueled heavily by 1,100 IDEXX inVue Dx placements in Q1 alone. The Catalyst platform continues to capture more test menu share, embedding IDEXX deeper into clinic workflows and ensuring recurring revenue stickiness.

🟢 𝐈𝐧𝐭𝐞𝐫𝐧𝐚𝐭𝐢𝐨𝐧𝐚𝐥 𝐂𝐨𝐦𝐦𝐞𝐫𝐜𝐢𝐚𝐥 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧 𝐏𝐚𝐲𝐬 𝐎𝐟𝐟

Accelerating. The targeted expansion of commercial density in international markets is generating outsized returns. International CAG Diagnostics recurring revenue jumped 21% reported (12% organic), outpacing the U. S. organic growth rate of 11%. This validates management's thesis that lower overseas diagnostic penetration offers a steeper, longer growth runway.

⚪ 𝐔.𝐒. 𝐂𝐥𝐢𝐧𝐢𝐜𝐚𝐥 𝐕𝐢𝐬𝐢𝐭 𝐇𝐞𝐚𝐝𝐰𝐢𝐧𝐝𝐬 𝐏𝐞𝐫𝐬𝐢𝐬𝐭

Stable. The macro backdrop remains a headwind, with management previously noting ongoing pressures in U. S. clinical visits. IDEXX is bypassing this volume drag through sheer force of innovation—increasing diagnostic frequency and utilization per visit. However, if foot traffic declines steeply, reliance on pricing and 'more tests per dog' could hit a ceiling.

🔴 𝐑𝐚𝐩𝐢𝐝 𝐀𝐬𝐬𝐚𝐲 𝐂𝐚𝐧𝐧𝐢𝐛𝐚𝐥𝐢𝐳𝐚𝐭𝐢𝐨𝐧

Stalling. Rapid assay revenues were flat on an organic basis ( 1% reported). Management explicitly attributes this sluggishness to the growing adoption of the Catalyst Pancreatic Lipase Test, which is actively shifting testing volume from standalone rapid assays onto the chemistry modality. While net-positive for the ecosystem, it caps growth in the legacy rapid assay segment.

🔴 𝐇𝐞𝐚𝐯𝐲 𝐈𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭𝐬 𝐌𝐮𝐭𝐞 𝐌𝐚𝐫𝐠𝐢𝐧 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧

Decelerating margin growth. Gross margins were outstanding (up 90 bps to 63.4%), but reported operating margin expanded by only 10 bps to 31.8%. The culprit: a 17% spike in operating expenses, driven by higher R&D spend, software investments, and commercial build-outs. IDEXX is prioritizing long-term market capture over short-term margin maximization.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐑𝐞𝐟𝐞𝐫𝐞𝐧𝐜𝐞 𝐋𝐚𝐛𝐨𝐫𝐚𝐭𝐨𝐫𝐲 𝐃𝐢𝐚𝐠𝐧𝐨𝐬𝐭𝐢𝐜 𝐚𝐧𝐝 𝐂𝐨𝐧𝐬𝐮𝐥𝐭𝐢𝐧𝐠 𝐒𝐞𝐫𝐯𝐢𝐜𝐞𝐬: $386.2 million

Accelerating. Up 12% reported and 10% organically in Q1 2026. This segment continues to benefit from net new customer gains and higher testing volumes, supported by the rising profile of specialty diagnostics like the IDEXX Cancer Dx platform.

𝐕𝐞𝐭𝐞𝐫𝐢𝐧𝐚𝐫𝐲 𝐒𝐨𝐟𝐭𝐰𝐚𝐫𝐞, 𝐒𝐞𝐫𝐯𝐢𝐜𝐞𝐬 & 𝐃𝐢𝐚𝐠𝐧𝐨𝐬𝐭𝐢𝐜 𝐈𝐦𝐚𝐠𝐢𝐧𝐠: $91.3 million

Stable. Grew 12% reported (11% organic), led entirely by cloud-native software and record diagnostic imaging system installations. This software ecosystem is a critical moat, driving higher clinic efficiency and deeper integration with IDEXX diagnostic hardware.

𝐅𝐢𝐫𝐬𝐭 𝐐𝐮𝐚𝐫𝐭𝐞𝐫 𝐅𝐫𝐞𝐞 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰: $234.3 million

Highly stable cash generation. Operating cash flow of $266.2M minus $32.0M in Capex yielded strong FCF. This fueled aggressive shareholder returns, with IDEXX repurchasing $361M in stock on the open market during the quarter.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐅𝐘𝟐𝟔 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $4.675 - $4.760 billion

Accelerating slightly vs prior guidance. Management raised the midpoint by $42M, implying 8.6% - 10.6% reported growth (7.7% - 9.7% organic). Driven directly by stronger-than-expected CAG Diagnostics recurring revenue utilization.

𝐅𝐘𝟐𝟔 𝐄𝐏𝐒: $14.45 - $14.90

Accelerating. Raised by $0.13 at the midpoint vs prior guidance. Represents 11% - 14% reported growth. Outperformance is supported by top-line strength, comparable margin expansion, and a 1-2% reduction in share count.

𝐅𝐘𝟐𝟔 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐌𝐚𝐫𝐠𝐢𝐧: 32.1% - 32.5%

Accelerating. Raised the reported outlook to capture 50-90 basis points of expansion. Despite the heavy Q1 OpEx jump, management clearly expects gross margin strength and operational productivity to pull through significantly in the back half of the year.

𝐅𝐘𝟐𝟔 𝐂𝐀𝐆 𝐃𝐢𝐚𝐠𝐧𝐨𝐬𝐭𝐢𝐜𝐬 𝐑𝐞𝐜𝐮𝐫𝐫𝐢𝐧𝐠 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐆𝐫𝐨𝐰𝐭𝐡: 9.6% - 11.6% (Reported)

Accelerating vs previous 8.6% - 10.6% guide. Upgraded explicitly due to easing clinical visit pressures in the U. S. and continued robust testing utilization gains globally.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐋𝐢𝐦𝐢𝐭𝐬 𝐨𝐟 𝐔𝐭𝐢𝐥𝐢𝐳𝐚𝐭𝐢𝐨𝐧 𝐯𝐬 𝐕𝐢𝐬𝐢𝐭 𝐃𝐞𝐜𝐥𝐢𝐧𝐞𝐬

You continue to post double-digit growth despite a sluggish clinical visit environment in the U. S. Mathematically, how far can increased diagnostic frequency per visit stretch if macro conditions force visits to decline further?

𝐌𝐚𝐫𝐠𝐢𝐧 𝐈𝐦𝐩𝐚𝐜𝐭 𝐨𝐟 𝐑𝐚𝐩𝐢𝐝 𝐀𝐬𝐬𝐚𝐲 𝐂𝐚𝐧𝐧𝐢𝐛𝐚𝐥𝐢𝐳𝐚𝐭𝐢𝐨𝐧

With Rapid Assays stalling organically due to cannibalization from Catalyst tests, what is the net margin impact of shifting this specific volume from standalone tests to chemistry analyzers?

𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐄𝐱𝐩𝐞𝐧𝐬𝐞 𝐂𝐚𝐝𝐞𝐧𝐜𝐞

OpEx grew 17% in Q1 compared to 14% top-line growth. With full-year operating margin guidance raised to 32.1-32.5%, should we expect a sharp deceleration in commercial and R&D investment spend in H2 2026?

1

1

391

Mar 12

I quite literally installed one of these yesterday. Was supposed to do two, but one of my stores lost the damn Invue key and you can't unlock the clamp without it.

2

34

If the “show” at the front of the room isn’t engaging… it’s time for a podium upgrade. 🎤📺✨

That’s exactly why we built the InVue Lectern! 🎉🙌

Ready to bring halftime-show energy to your podium?💥🚀

spectrumfurniture.com/produc…

#LearningSpaces #PresentationTech #Lecterns #EdTech

1

2

87

$IDXX Q4 ’25 earnings had two underappreciated drivers:

1) Hardware supercycle kicking off with 1,900 placements in Q4 alone for inVue Dx. That’s strong momentum going into FY ‘26.

2) International diversification. International CAG recurring revenue grew 12% organic vs. 9% in the U.S.

Owning $IDXX is a leveraged play on long-term pet healthcare spending.

7

832

Feb 2

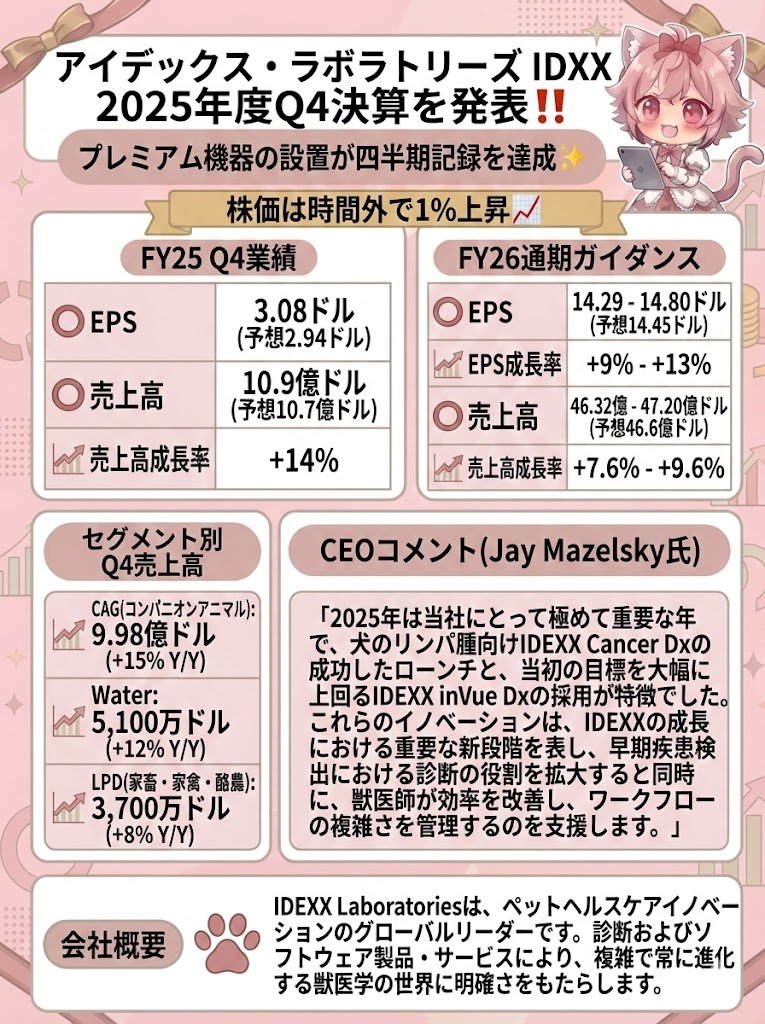

アイデックス・ラボラトリーズ $IDXX

2025年度Q4決算を発表‼️

プレミアム機器の設置が四半期記録を達成✨

🔸FY25 Q4業績

⭕️EPS: 3.08ドル(予想2.94ドル)

⭕️売上高: 10.9億ドル(予想10.7億ドル)

📈売上高成長率: 14%

🔸FY26通期ガイダンス

⭕️EPS: 14.29 - 14.80ドル(予想14.45ドル)

📈EPS成長率: 9% - 13%

⭕️売上高: 46.32億 - 47.20億ドル(予想46.6億ドル)

📈売上高成長率: 7.6% - 9.6%

✔️営業マージン: 32.0 - 32.5%

📈営業マージン拡大: 40 - 90 bps

🔸セグメント別Q4売上高

📈CAG(コンパニオンアニマル): 9.98億ドル ( 15% Y/Y)

📈Water: 5,100万ドル ( 12% Y/Y)

📈LPD(家畜・家禽・酪農): 3,700万ドル ( 8% Y/Y)

🔸CAG Diagnostics Recurring Revenue

📈Q4売上高: 8.50億ドル ( 12% Y/Y)

📈FY26ガイダンス成長率: 8.6% - 10.6% Y/Y

🔸CAG Diagnostics内訳(Q4)

📈IDEXX VetLab消耗品: 3.89億ドル ( 17% Y/Y)

📉迅速検査製品: 7,600万ドル (-2% Y/Y)

📈リファレンスラボ診断・コンサルティング: 3.49億ドル ( 11% Y/Y)

📈診断サービス・アクセサリー: 3,500万ドル ( 10% Y/Y)

📈診断機器(キャピタル): 5,800万ドル ( 76% Y/Y)

🔸獣医ソフトウェア・サービス・画像診断システム

📈Q4売上高: 9,100万ドル ( 13% Y/Y)

✔️リカーリング収益: 7,100万ドル ( 12% Y/Y)

✔️システム・ハードウェア: 2,000万ドル ( 17% Y/Y)

🔸Q4プレミアム機器設置数

✔️合計: 6,567台 (米国: 2,667台, 国際: 3,900台)

📈Catalyst: 1,776台 (新規・競合置換: 1,369台, セカンド: 407台)

📈Premium Hematology: 1,860台 (新規・競合置換: 1,450台)

📈SediVue Dx: 991台

📈IDEXX inVue Dx: 1,940台(四半期記録達成)

🔸プレミアム機器設置ベース(千台単位)

📈Catalyst: 77.9千台 ( 5% Y/Y)

📈Premium Hematology: 55.9千台 ( 8% Y/Y)

📈SediVue: 24.3千台 ( 14% Y/Y)

📈inVue Dx: 6.4千台 (2024年Q4: 0.3千台から大幅増)

🔸米国コンパニオンアニマルセクター動向(2025年Q4)

✔️診療所収益成長率: 2.4% (前年同期比)

✔️総来院数: -2.8% (前年同期比)

✔️臨床来院数: -1.7% (前年同期比)

✔️非ウェルネス来院数: -0.5% (前年同期比)

✔️ウェルネス来院数: -3.6% (前年同期比)

✔️診断利用の増加が高齢ペット人口の影響を受けて米国成長を支援

🔸CEOコメント(Jay Mazelsky氏)

「IDEXXは2025年を力強く終え、世界中のIDEXXチームによる一貫した高水準の実行に支えられました。」

「2025年は当社にとって極めて重要な年で、犬のリンパ腫向けIDEXX Cancer Dxの成功したローンチと、当初の目標を大幅に上回るIDEXX inVue Dxの採用が特徴でした。これらのイノベーションは、IDEXXの成長における重要な新段階を表し、早期疾患検出における診断の役割を拡大すると同時に、獣医師が効率を改善し、ワークフローの複雑さを管理するのを支援します。」

🔸会社概要

IDEXX Laboratoriesは、ペットヘルスケアイノベーションのグローバルリーダーです。

診断およびソフトウェア製品・サービスにより、複雑で常に進化する獣医学の世界に明確さをもたらします。

世界中の獣医コミュニティが自信を持って意思決定を行い、医療ケアを向上させ、効率を改善し、繁栄する診療所を構築できるよう、洞察とソリューションを提供することで、ペットのより長く充実した生活を支援しています。

2

4

39

11,068

Feb 2

🚨 BOOM DE RESULTADOS: La economía de las mascotas es A PRUEBA DE BALAS. 🐶📈

$IDXX (IDEXX) acaba de presentar su Q4 y los números son una locura. Si pensabas que el consumo estaba frenado, mirá esto:

📊 Q4 2025 HIGHLIGHTS: ✅ Ingresos: $1,091M ( 14% reportado) ✅ EPS (Beneficio por acción): $3.08 ( 18% !!!) ✅ Márgenes Operativos: 150 puntos básicos. ✅ Crecimiento Orgánico: 12%.

💡 ¿El secreto?No solo venden tests, venden el ecosistema. RÉCORD de colocación de instrumentos: 1,900 unidades del nuevo inVue Dx en un solo trimestre.

🚀 GUIDANCE 2026 (Lo que viene): Esperan un EPS de $14.29 - $14.80. Eso es un crecimiento de doble dígito otra vez ( 10-14%).

🧠 Mi opinión de Contador: Cuando ves una expansión de márgenes de 150 bps en este entorno y un crecimiento de ingresos recurrentes del 12%, estás ante una empresa con un "MOAT" (foso defensivo) gigante. La gente deja de comer afuera antes de dejar de cuidar a su perro.

👇 Debate:¿Pagarías el "premium" de valoración de $IDXX por esta calidad o preferís buscar gangas? Los leo.

3

183

Feb 2

$IDXX Q4 2025 earnings: Innovation Supercycle Drives Accelerated Growth

IDEXX closed FY25 with a definitive acceleration, delivering 12% organic revenue growth in Q4 compared to just ~5% in Q1. The catalyst is the massive adoption of the inVue Dx platform, which drove a 69% surge in instrument revenue. While the macro environment for veterinary visits remains tepid, IDEXX is successfully decoupling its growth through price realization, mix shift to higher-margin consumables, and international expansion. FY26 guidance suggests a stabilization of this high-growth tier, projecting 7-9% organic growth and continued margin expansion.

Full article finsee.ai/earnings/idxx/2025…

3

530

Feb 2

$IDXX Earnings:

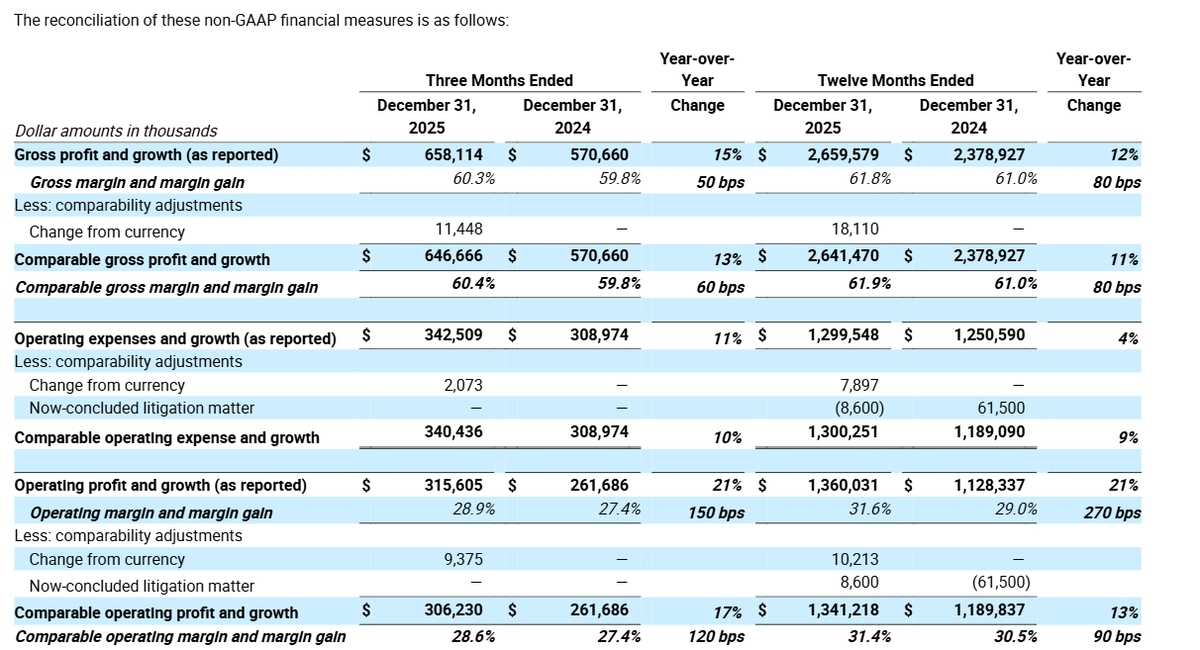

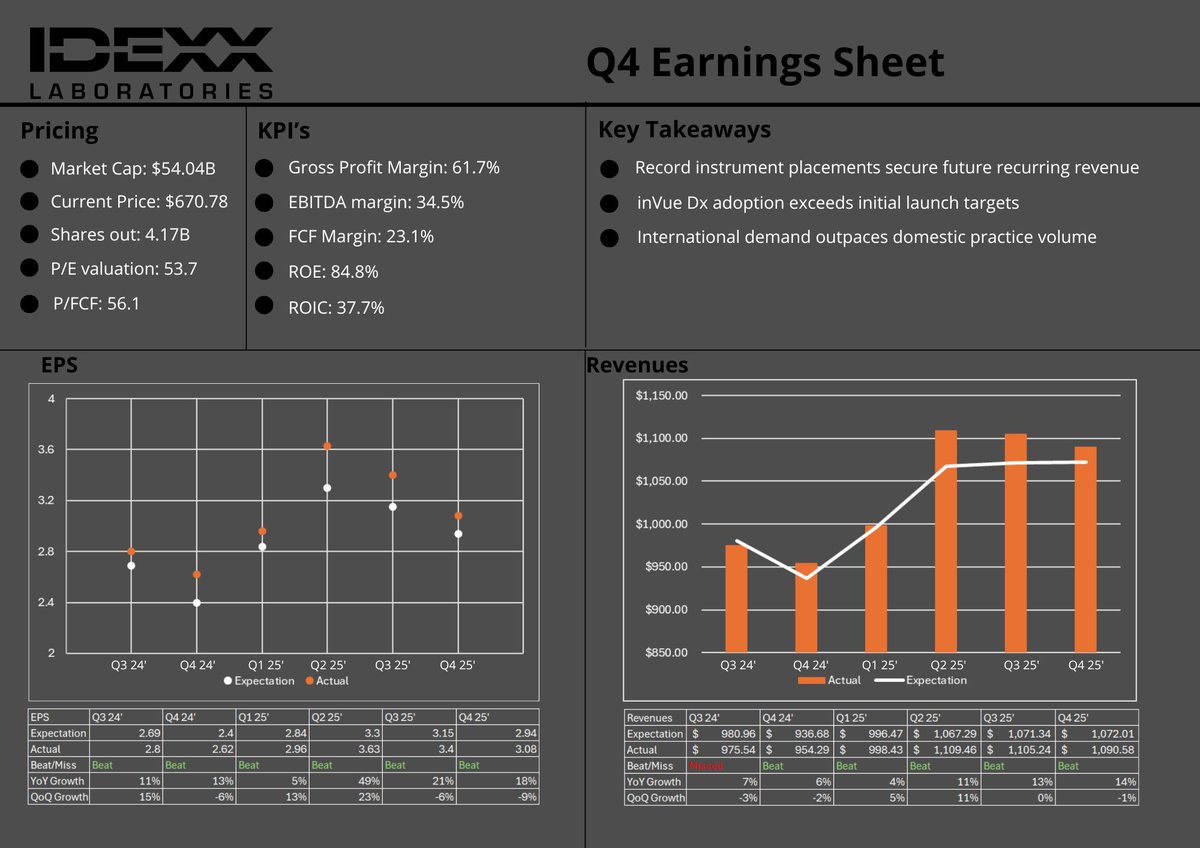

- Revenues of $1,091 million for the fourth quarter of 2025, an increase of 14% compared to the prior year period as reported and 12% on an organic basis, driven by Companion Animal Group ("CAG") growth of 15% as reported and 13% organic and Water revenue growth of 12% as reported and 10% organic.

- EPS of $3.08, an increase of 18% as reported and 17% on a comparable basis, supported by operating margin expansion of 150 basis points as reported and 120 basis points on a comparable basis.

- Provides initial outlook for 2026 revenue guidance range of $4,632 million - $4,720 million, reflecting growth of 7.6% - 9.6% reported and 7.0% - 9.0% organic, led by CAG Diagnostics recurring revenue growth of 8.6% - 10.6% as reported and 8.0% - 10.0% on an organic basis.

- Projects 2026 EPS of $14.29 - $14.80, an increase of 9% - 13% as reported and 10% - 14% on a comparable basis.

“IDEXX delivered a strong finish to 2025, supported by consistently high levels of execution by IDEXX teams around the world,” said Jay Mazelsky, President and Chief Executive Officer. “2025 was a pivotal year for the Company, marked by the successful launch of IDEXX Cancer Dx™ for canine lymphoma and meaningful adoption of IDEXX inVue Dx well ahead of our initial goals. These innovations represent an important new phase of IDEXX’s growth, expanding the role of diagnostics in earlier disease detection while helping veterinarians improve efficiency and manage workflow complexity. We enter 2026 with an exciting innovation pipeline, expanding instrument and software installed bases, and strong momentum across our global business.”

research.alpha-sense.com?doc…

1

3

1,300

Feb 2

IDEXX Laboratories $IDXX 🐶

Q4 2025

🔸Achieves fourth quarter revenue growth of 14% as reported and 12% organic, reflecting strong CAG Diagnostics recurring revenue, growing 12% reported and 10% organic.

🔸Strong organic growth benefits from IDEXX execution and commercial performance, including over 1,900 IDEXX inVue Dx™ placements, delivering a quarterly record of instrument placements and 12% year-over-year expansion of IDEXX's global premium instrument installed base.

🔸Delivers fourth quarter EPS of $3.08, an increase of 18% as reported and 17% on a comparable basis, supported by operating margin expansion of 150 basis points as reported and 120 basis points on a comparable basis.

Provides initial outlook for 2026 revenue guidance range of $4,632 million - $4,720 million, reflecting growth of 7.6% - 9.6% reported and 7.0% - 9.0% organic, led by CAG Diagnostics recurring revenue growth of 8.6% - 10.6% as reported and 8.0% - 10.0% on an organic basis.

🔸Projects 2026 EPS of $14.29 - $14.80, an increase of 9% - 13% as reported and 10% - 14% on a comparable basis.

1

2

496

$IDXX just reported a Q4 double beat. The stock stays flat after these earnings.

IDEXX delivered a stellar finish to 2025, proving its razor-and-blade model is stronger than ever. The company achieved double-digit organic growth, powered by record-breaking placements of its new inVue Dx analyzer. This is a big win because every new machine installed locks in years of future sales for testing supplies.

While domestic vet visits have been slightly soft, $IDXX is successfully offsetting this through higher-value innovations like its new cancer diagnostics and strong international demand.

Looking ahead to 2026, management is signaling confidence with a robust forecast for both revenue and profit. By combining cutting-edge medical tech with cloud-based software, IDEXX is making itself indispensable to vet clinics worldwide.

3

1

6

773

CleverQ Taps MagTek in Authentication Boost, While MagTek Notes Several Similar Moves - Digital Transactions

Click to read: buff.ly/SYQyI88

#payments #MagTek #cardreaders #POSequipment #cleverQ #GrabScanGo #Vault #InVue #pointofsale #security #Magensa @magtek

3

203

$IDXX being my best performer YTD with 85% return is crazy, especially considering weak vet visits. InVue and Cancer DX inovations have been exceptional, and are leading to big increase in consumables revenue. Business is doing great, but valuation is stretched again.

2

323

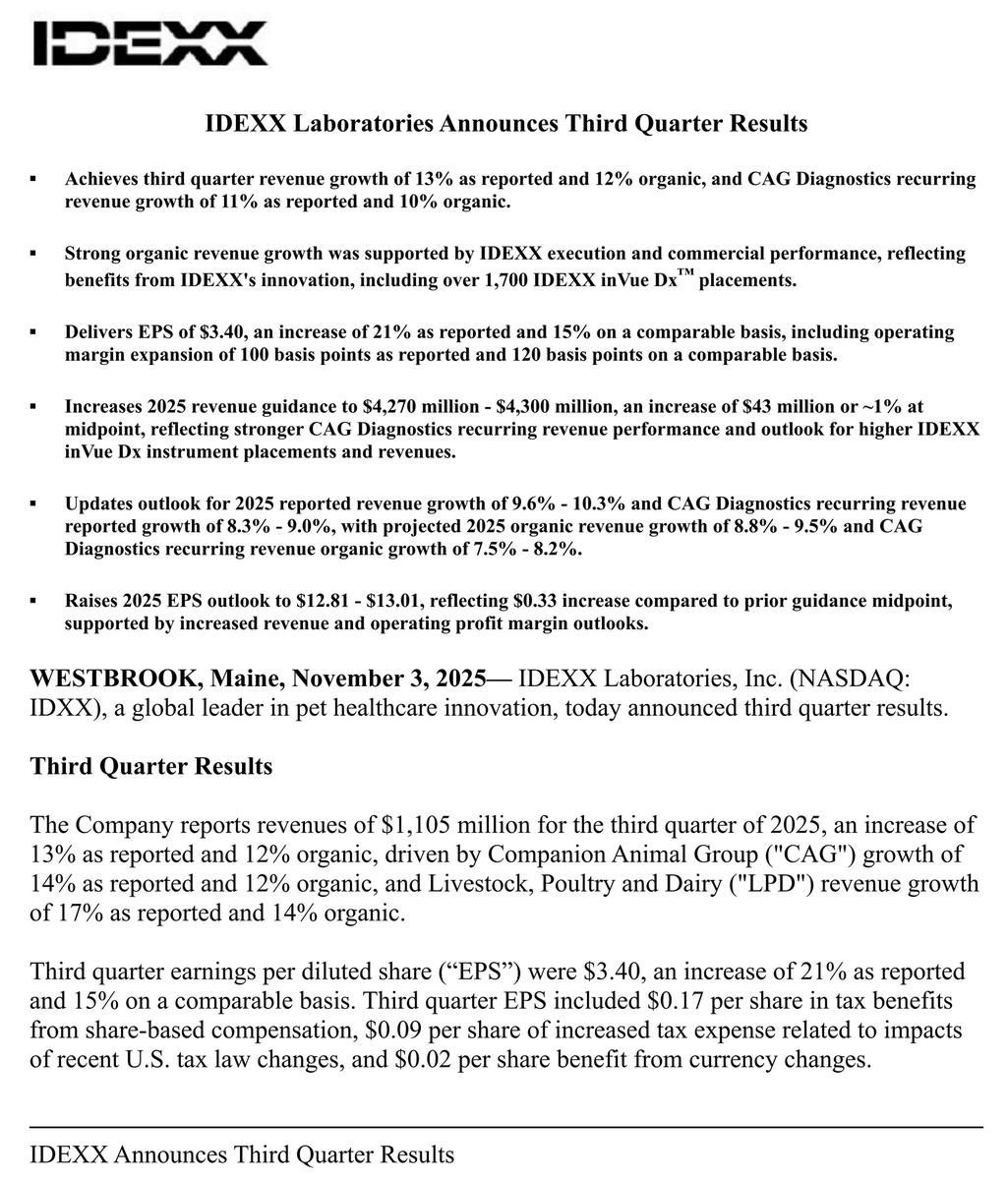

3 Nov 2025

アイデックス・ラボラトリーズ $IDXX 🐾

2025年度Q3決算を発表‼️

イノベーション主導の成長戦略が奏功し、

予想を上回る業績を達成✨

株価は時間外取引で6.5%上昇🚀

🔸2025年Q3業績

⭕️EPS: 3.40ドル(予想3.14ドル)

⭕️売上高: 11.05億ドル(予想10.7億ドル)

📈売上高成長率: 13% Y/Y、オーガニック 12%

🔸2025年通期ガイダンス(上方修正)

⭕️EPS: 12.81~13.01ドル(予想12.63ドル、従来12.40~12.76ドル)

⭕️売上高: 42.7億~43.0億ドル(予想42.3億ドル、従来42.05億~42.8億ドル)

📈売上高成長率: 9.6%~10.3%、オーガニック 8.8%~9.5%

📈CAG診断リカーリング収益成長率: 8.3%~9.0%、オーガニック 7.5%~8.2%

📈営業利益率: 31.6%~31.8%( 260~280bps)

🔸セグメント別売上高(Q3)

📈CAG(コンパニオンアニマル): 10.13億ドル( 14% Y/Y、オーガニック 12%)

📈Water(水質検査): 5,430万ドル( 8% Y/Y、オーガニック 7%)

📈LPD(家畜・家禽・酪農): 3,390万ドル( 17% Y/Y、オーガニック 14%)

🔸CAG診断リカーリング収益

📈8.73億ドル( 11% Y/Y、オーガニック 10%)

📈IDEXX VetLab消耗品: 3.88億ドル( 18%、オーガニック 16%)

📈リファレンスラボ診断サービス: 3.63億ドル( 10%、オーガニック 9%)

❌迅速検査製品: 8,860万ドル(-4%、オーガニック-5%)

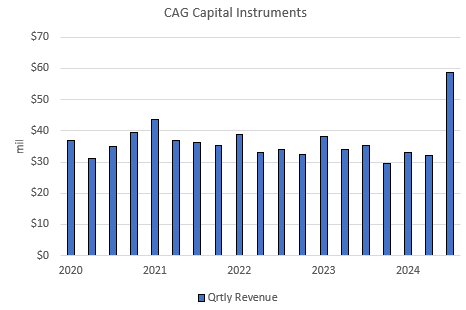

🔸CAG診断機器(キャピタル)

📈5,150万ドル( 74%報告ベース、オーガニック 71%)

📈IDEXX inVue Dx設置台数: 1,700台超

🔸収益性指標

📈粗利益率: 61.8%(前年同期61.1%、 70bps)

📈営業利益率: 32.1%(前年同期31.2%、 100bps報告ベース、 120bps比較可能ベース)

🔸その他の財務指標

📈営業キャッシュフロー: 純利益の105%~115%

📈フリーキャッシュフロー: 純利益の95%~100%

📈設備投資: 約1.4億ドル

📈自社株買い: 発行済株式数2.5%~3%減少見込み

🔸事業ハイライト

✔️IDEXX inVue Dxの設置が急速に進展(Q3で1,700台超)

✔️プレミアム機器設置ベースが10%成長

✔️米国のコンパニオンアニマル診療所の訪問数が改善傾向

✔️診断頻度の向上とIDEXXイノベーションの採用拡大

✔️国際市場でのCAG診断リカーリング収益が強力に成長( 18%、オーガニック 14%)

🔸CEOコメント(Jay Mazelsky氏)

「IDEXXはイノベーション主導の成長戦略において顕著な進展を遂げ、強力な実行力とグローバルな顧客採用を実現しました。IDEXX Cancer Dx、膵リパーゼとコルチゾール用の新しいCatalyst専門検査の成功的なローンチ、そしてIDEXX inVue Dxの革新的な影響を基に、強力な新しい診断機能を提供しています。これらのソリューションは臨床的洞察を高め、ワークフローを合理化し、獣医療チームに有意義な価値を創出します。強力な成長プロファイルに反映される熱狂的な反応は、顧客がIDEXXに寄せる信頼を際立たせています。」

🔸会社概要

IDEXX Laboratoriesは、ペットヘルスケアイノベーションのグローバルリーダーです。

診断製品とソフトウェアにより、複雑で絶え間なく進化する獣医学の世界に明確さを提供しています。

175以上の国と地域で約11,000人の従業員を擁し、S&P 500指数の構成銘柄です。

3

4

53

9,717

3 Nov 2025

$IDXX Q3 2025 earnings: Innovation Drives Strong Beat and Raise as US Headwinds Ease.

IDEXX delivered an excellent quarter, surpassing prior guidance and raising its full-year outlook across the board. Growth accelerated, driven by strong adoption of new products, particularly the inVue Dx platform, and continued momentum in international markets. Crucially, the company noted that pressure from declining U.S. vet clinic visits is now easing, addressing a key concern from the previous quarter. The results demonstrate strong execution on their innovation-focused strategy.

🐂 𝗕𝘂𝗹𝗹 𝗰𝗮𝘀𝗲

* Strong beat and a significant raise to full-year guidance for revenue, organic growth, operating margin, and EPS.

* Organic revenue growth accelerated to 12% from 9% last quarter.

* A key prior concern is improving, with management citing an "easing of clinical visit pressures" in the U.S.

* Innovation is paying off: 1,700 inVue Dx placements and 16% organic growth in high-margin VetLab consumables.

* International CAG recurring revenue growth accelerated to 14% organic.

* Excellent financial discipline, with comparable operating margin expanding 120 basis points and a huge raise to the free cash flow outlook.

🐻 𝗕𝗲𝗮𝗿 𝗰𝗮𝘀𝗲

* While strong, inVue Dx placements of 1,700 units represent a sequential slowdown from 2,388 in Q2.

* The small Rapid Assay product line declined 5% organically, though this was attributed to a product mix shift rather than competitive loss.

* Share repurchases slowed to $242M from $329M in the prior quarter.

⚖️ 𝗩𝗲𝗿𝗱𝗶𝗰𝘁

The bull case is significantly more compelling. This was a high-quality beat-and-raise quarter. The company is executing extremely well, the innovation pipeline is driving growth, and a major external headwind (U.S. visit trends) is showing signs of improvement. The bear points are minor and do not detract from the overwhelmingly positive results and outlook.

***

𝟮. 𝗧𝗵𝗲𝗺𝗲𝘀, 𝗱𝗿𝗶𝘃𝗲𝗿𝘀, 𝗮𝗻𝗱 𝗰𝗼𝗻𝗰𝗲𝗿𝗻𝘀

🟢 𝗜𝗻𝗻𝗼𝘃𝗮𝘁𝗶𝗼𝗻 𝗮𝘀 𝗣𝗿𝗶𝗺𝗮𝗿𝘆 𝗚𝗿𝗼𝘄𝘁𝗵 𝗘𝗻𝗴𝗶𝗻𝗲 (𝗜𝗺𝗽𝗿𝗼𝘃𝗶𝗻𝗴)

This theme strengthened considerably. The company placed another 1,700 inVue Dx units and raised the full-year outlook for placements. VetLab consumables grew an impressive 16% organically, supported by new test adoption. This confirms the core of the growth story is intact and performing ahead of plan.

🟢 𝗦𝘁𝗿𝗼𝗻𝗴 𝗜𝗻𝘁𝗲𝗿𝗻𝗮𝘁𝗶𝗼𝗻𝗮𝗹 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲 (𝗜𝗺𝗽𝗿𝗼𝘃𝗶𝗻𝗴)

International growth remains a standout, accelerating this quarter. CAG Diagnostics recurring revenue in international markets grew 14% organically, up from 11% in Q2. This continues to be a powerful, long-term growth driver.

🟢🟡 𝗣𝗲𝗿𝘀𝗶𝘀𝘁𝗲𝗻𝘁 𝗗𝗲𝗰𝗹𝗶𝗻𝗲 𝗶𝗻 𝗨.𝗦. 𝗖𝗹𝗶𝗻𝗶𝗰𝗮𝗹 𝗩𝗶𝘀𝗶𝘁𝘀 (𝗜𝗺𝗽𝗿𝗼𝘃𝗶𝗻𝗴)

This was the primary concern last quarter. The tone has shifted positively, with the company now citing an "easing of clinical visit pressures." While the headwind hasn't vanished, this improvement is a significant positive development and de-risks the story.

🟡 𝗶𝗻𝗩𝘂𝗲 𝗣𝗹𝗮𝗰𝗲𝗺𝗲𝗻𝘁 𝗖𝗮𝗱𝗲𝗻𝗰𝗲 (𝗠𝗮𝘁𝗲𝗿𝗶𝗮𝗹𝗶𝘇𝗲𝗱 𝗖𝗼𝗻𝗰𝗲𝗿𝗻)

As questioned by an analyst last quarter, the record pace of inVue placements in Q2 was not sustained. The 1,700 placements in Q3, while still very strong, represent a sequential slowdown from 2,388. While the full-year guide was raised, the pace of adoption has moderated from its initial peak.

🔴 𝗥𝗮𝗽𝗶𝗱 𝗔𝘀𝘀𝗮𝘆 𝗗𝗲𝗰𝗹𝗶𝗻𝗲 (𝗡𝗲𝘄 𝗖𝗼𝗻𝗰𝗲𝗿𝗻)

A new, minor negative is the 5% organic decline in rapid assay revenues. Management attributes this to customers shifting to the newer, more advanced Catalyst Pancreatic Lipase test, which is a positive product mix shift. However, it is a segment decline worth monitoring.

***

𝟯. 𝗠𝗮𝗶𝗻 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹𝘀

* 𝗧𝗼𝘁𝗮𝗹 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: $1,105M, up 𝟭𝟮% 𝗼𝗿𝗴𝗮𝗻𝗶𝗰𝗮𝗹𝗹𝘆. This is a clear acceleration from 9% organic growth in Q2.

* 𝗖𝗔𝗚 𝗗𝗶𝗮𝗴𝗻𝗼𝘀𝘁𝗶𝗰𝘀 𝗥𝗲𝗰𝘂𝗿𝗿𝗶𝗻𝗴 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: Up 𝟭𝟬% 𝗼𝗿𝗴𝗮𝗻𝗶𝗰𝗮𝗹𝗹𝘆, a strong acceleration from 7.5% in Q2.

* 𝗨.𝗦. grew 𝟴% 𝗼𝗿𝗴𝗮𝗻𝗶𝗰𝗮𝗹𝗹𝘆.

* 𝗜𝗻𝘁𝗲𝗿𝗻𝗮𝘁𝗶𝗼𝗻𝗮𝗹 grew 𝟭𝟰% 𝗼𝗿𝗴𝗮𝗻𝗶𝗰𝗮𝗹𝗹𝘆.

* 𝗖𝗔𝗚 𝗜𝗻𝘀𝘁𝗿𝘂𝗺𝗲𝗻𝘁 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: Grew an exceptional 𝟳𝟭% 𝗼𝗿𝗴𝗮𝗻𝗶𝗰𝗮𝗹𝗹𝘆, driven by strong inVue Dx placements.

* 𝗘𝗣𝗦: $3.40. On a comparable basis, EPS grew 𝟭𝟱%.

* 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗻𝗴 𝗠𝗮𝗿𝗴𝗶𝗻: Comparable operating margin expanded by 𝟭𝟮𝟬 𝗯𝗮𝘀𝗶𝘀 𝗽𝗼𝗶𝗻𝘁𝘀 (1.20%), showing strong profitability and cost control even with increased investments.

* 𝗦𝗵𝗮𝗿𝗲 𝗥𝗲𝗽𝘂𝗿𝗰𝗵𝗮𝘀𝗲𝘀: The company repurchased $241.6M of its stock during the quarter.

***

𝟰. 𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲

Management provided a significant raise to the full-year 2025 outlook, signaling strong confidence in Q4 and beyond.

🟢 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: Raised to $𝟰,𝟮𝟳𝟬𝗠 - $𝟰,𝟯𝟬𝟬𝗠 from a prior $4,205M - $4,280M.

🟢 𝗢𝗿𝗴𝗮𝗻𝗶𝗰 𝗥𝗲𝘃𝗲𝗻𝘂𝗲 𝗚𝗿𝗼𝘄𝘁𝗵: Raised to 𝟴.𝟴% - 𝟵.𝟱% from a prior 7.0% - 9.0%. This implies continued acceleration.

🟢 𝗖𝗔𝗚 𝗗𝗶𝗮𝗴𝗻𝗼𝘀𝘁𝗶𝗰𝘀 𝗥𝗲𝗰𝘂𝗿𝗿𝗶𝗻𝗴 𝗥𝗲𝘃𝗲𝗻𝘂𝗲 𝗢𝗿𝗴𝗮𝗻𝗶𝗰 𝗚𝗿𝗼𝘄𝘁𝗵: Raised to 𝟳.𝟱% - 𝟴.𝟮% from a prior 5.8% - 8.0%.

🟢 𝗘𝗣𝗦: Raised to $𝟭𝟮.𝟴𝟭 - $𝟭𝟯.𝟬𝟭 from a prior $12.40 - $12.76. A large $0.33 raise at the midpoint.

🟢 𝗖𝗼𝗺𝗽𝗮𝗿𝗮𝗯𝗹𝗲 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗻𝗴 𝗠𝗮𝗿𝗴𝗶𝗻 𝗘𝘅𝗽𝗮𝗻𝘀𝗶𝗼𝗻: Raised to 𝟴𝟬 - 𝟭𝟬𝟬 𝗯𝗽𝘀 from a prior 50 - 80 bps.

🟢 𝗙𝗿𝗲𝗲 𝗖𝗮𝘀𝗵 𝗙𝗹𝗼𝘄 𝗖𝗼𝗻𝘃𝗲𝗿𝘀𝗶𝗼𝗻: Raised significantly to 𝟵𝟱% - 𝟭𝟬𝟬% of Net Income from a prior 80% - 85%.

***

𝟱. 𝗠𝗮𝗶𝗻 𝗾𝘂𝗲𝘀𝘁𝗶𝗼𝗻𝘀 𝗳𝗼𝗿 𝘁𝗵𝗲 𝗲𝗮𝗿𝗻𝗶𝗻𝗴𝘀 𝗰𝗮𝗹𝗹

1. Could you please quantify the "easing of clinical visit pressures" in the U.S. during Q3, and what specific trend is now assumed in your updated full-year guidance?

2. You raised the outlook for inVue Dx placements but the Q3 number of 1,700 was down from 2,388 in Q2. Can you provide the new full-year target and discuss if Q3 represents a more normalized quarterly run-rate?

3. VetLab consumables had exceptional 16% organic growth. How should we think about the contribution from new innovations versus underlying price and testing frequency?

4. The free cash flow conversion guidance saw a very large increase. What were the primary drivers behind this significant improvement in the outlook?

2

598

3 Nov 2025

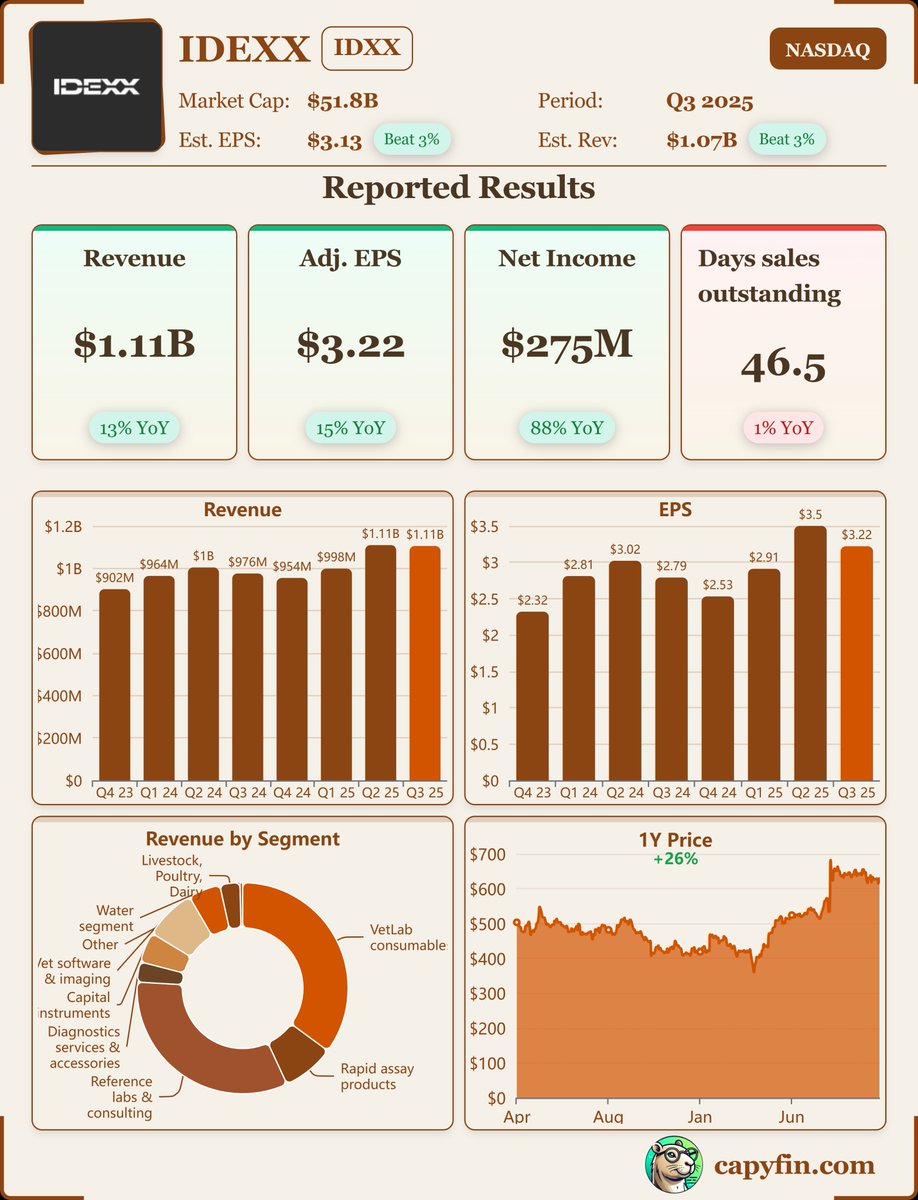

IDEXX Laboratories, $IDXX, Q3-25. Results:

📊 Adj. EPS: $3.22 🟢

💰 Revenue: $1.11B 🟢

📈 Net Income: $275M

🔎 Surge in IDEXX inVue Dx™ placements and strong CAG Diagnostics recurring revenue drove double-digit growth across core segments.

1

4

23

9,563

3 Nov 2025

$IDXX Q3 '25:

Revenue $1,105m, up 13% (12% organic)

EPS $3.40, up 21% (15% comparable)

CAG Diagnostics 11% recurring revenue

1,700 inVue Dx placements

'25 guidance raised: $4,270-$4,300m revenue, $12.81-$13.01 EPS

PR: urlu.xyz/9eba55ce

1

2

315

15 Aug 2025

🐾 $IDXX 2025 Investor Day Takeaways

IDEXX Laboratories held its Investor Day yesterday. Here are a few notes from the presentation:

TAM: $45B global vet diagnostics (~⅔ intl)

Share Gains: Outpacing sector growth (9% vs. 7.5–8.5%)

Innovation: Cancer Dx → 50% of canine cancers detectable by 2028

Point-of-Care: inVue Dx & MultiCue Dx → ref-lab quality in clinic

Growth: 10% organic, 97% retention, high ROIC

Runway: Premium instruments could 3x globally

My take: strong innovation pipeline, durable recurring growth, clear market share gains — but big bets on cancer screening will need strong execution to deliver.

1

7

824

5 Aug 2025

"a record quarter of premium instrument placements, including nearly 2,400 Idexx inVue Dx instruments..." $IDXX 👀

1

4

419

5 Aug 2025

$IDXX - Idexx raises 2025 revenue outlook to $4.28B as inVue Dx placements surge and innovation momentum builds. seekingalpha.com/news/447775… #stocks #economy #finance

2

2

2,254