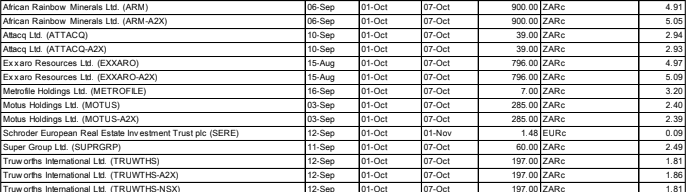

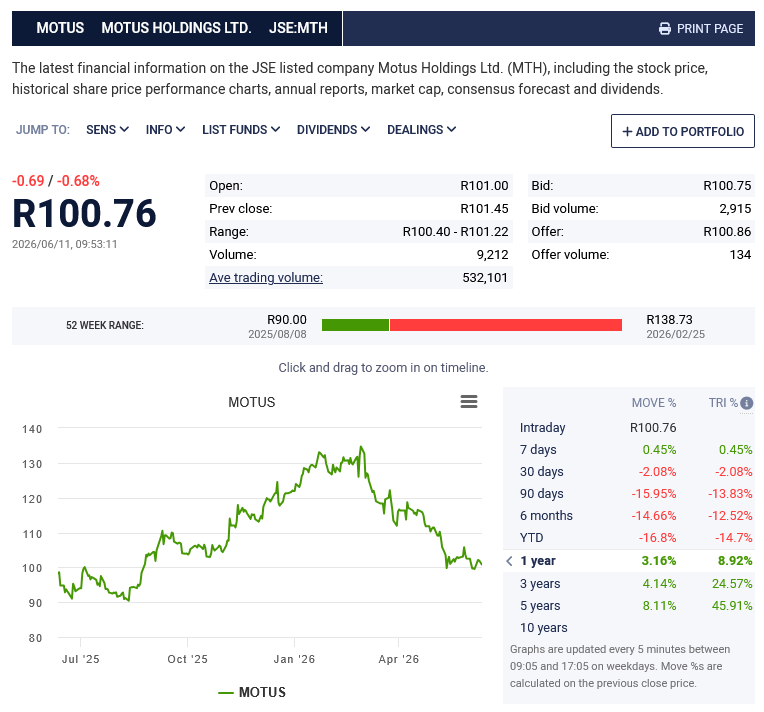

JSE Value Guy retweeted

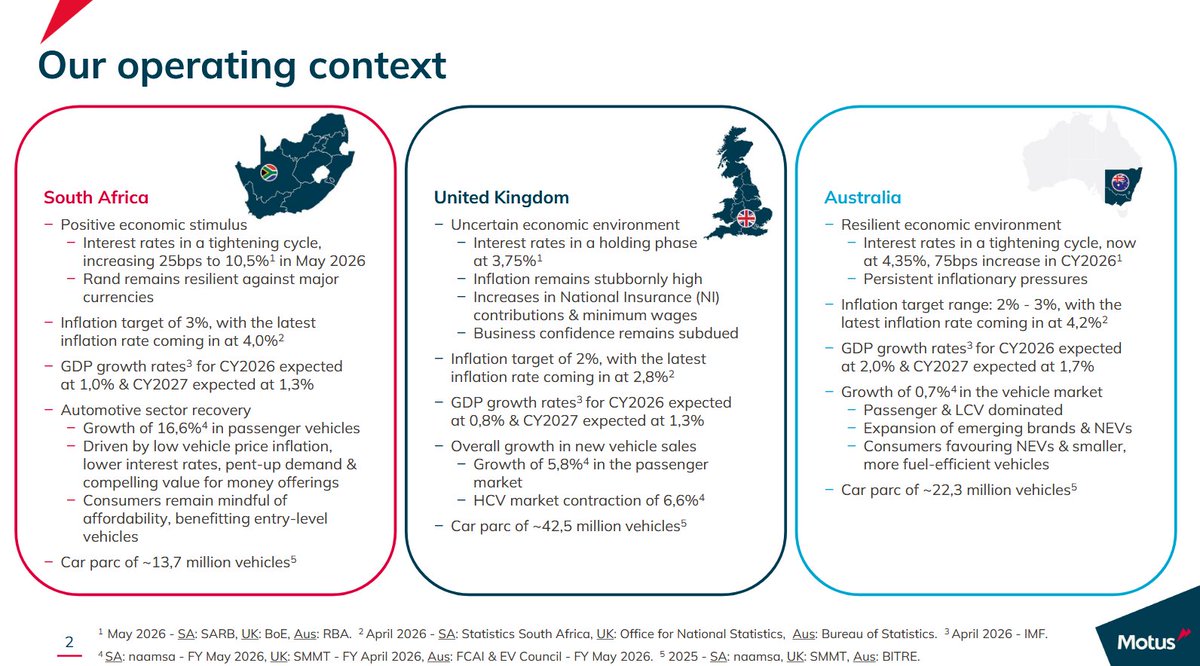

Just off the $JSEMTH Motus pre-close call for year end results to June 2026. The tonality reflected the challenges in some market segments (UK, Australia, used cars) but also indicated that #MTH was holding its own and even gaining in some areas

#MTH started the year well with the stock running hard to a peak of R132.50 then from March slumped -24% to the current price of R100.76 as the rampant charge of the Chinese and Indian vehicles rampaged through the sales landscape

#MTH indicated it had fared reasonably well in the past six months and highlighted that it expected profits growth in high teens and a -20% reduction in finance costs (past results have been driven by reduction in debt and the associated finance income saving)

On a current PE of 6.5x with a better reporting period ahead I'd wager that #MTH has probably reached its bottom with support around R100.00

Any movement from here will be sentiment directed on expectations on new vehicle sales given the recent rise in interest rates and the soaring price of fuel. This may temper investor interest in #MTH until guidance on results are seen in September

Here is a link to this morning's presentation

motus.co.za/wp-content/uploa…

1

5

1,174

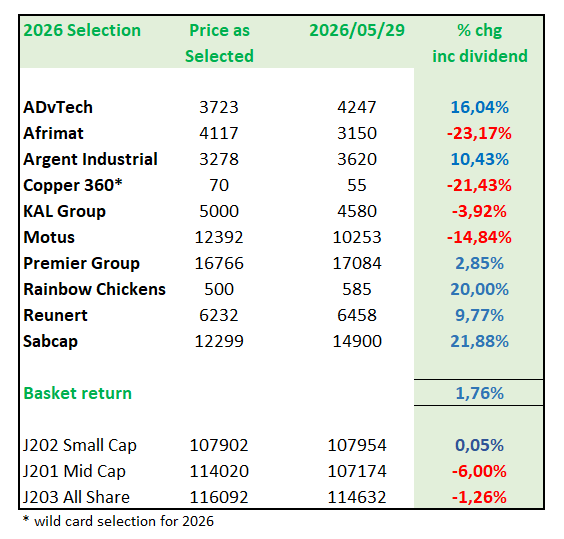

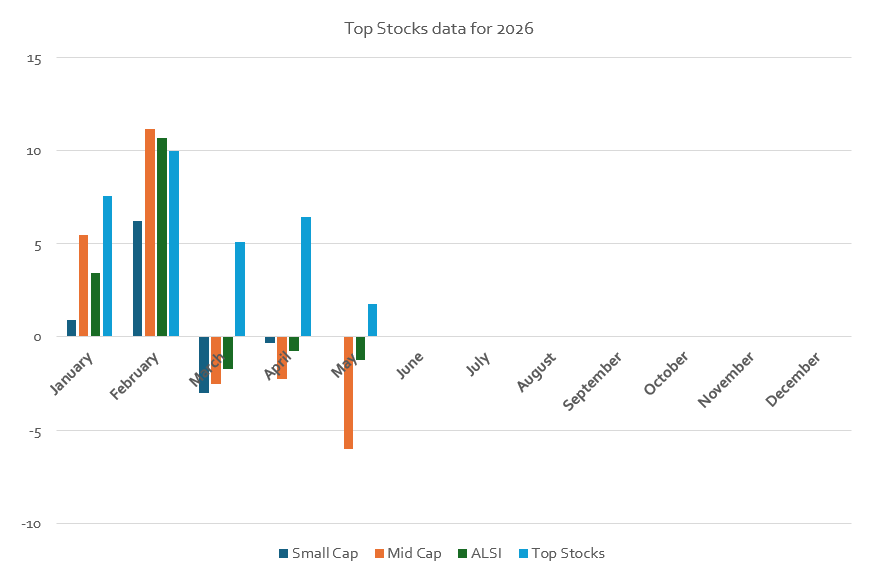

Month 5 (May) of my @smalltalkdaily Top Stocks of 2026 updated and I remain ahead of my benchmark indices but May was a brutal month for markets

Top Stocks 1.76% (versus 6.43% in April)

Small Cap Index 0.05%

Mid Cap Index -6.0%

Difficult month for the 10 stocks selected

(Only) Best performers change month-on-month

$JSEADH AdvTech 0.2%

$JSEART Argent Industrial 0.6%

Worst performers change month-on-month

$JSECPR Copper 360 -12.7%

$JSEMTH Motus -8.0%

$JSERLO Reunert -7.4%

$JSEPMR Premier Group -6.2%

7 months to go yet but markets do look very wobbly and indifferent so maybe the "sell in May and go away" mantra would have been the best scenario ... but I can't as the list is cast in stone for a year

1

5

1,480

The National Association of Automotive Manufacturers of South Africa (NAAMSA) have released their March sales data

In going through the data on passenger vehicles month-on month I find the following

New passenger car sales month-on-month 39,370 (4.8%)

What pushed the total industry sales stats in the March month was a SURGE in demand for commercial vehicles (CV)

Light CV 17.7%

Medium CV 14.3%

Heavy CV 6.6%

Extra heavy CV 27.9%

Buses -17.9%

Overall new vehicle sales 58,060 ( 8.6%)

What was really interesting was a changes in the vehicle manufacturers OEM market share & vehicle sales

The big losers month on month were the OEM represented by $JSECMH Combined Motor Holdings (Suzuki) and $JSEMTH Motus Holdings (Hyundai, Kia & Renault) both saw sales declines

The Chinese brands (big 4 GWM, Chery, Jetour, Jaecoo/Omoda) saw month-on-month growth to 8,368 units ( 6.0%)

The BIG OEM gainers were VW, Isuzu, Mahindra and BMW

Month-on-month changes in new vehicle sales ranked in sales order

Toyota 1,051 units or 8.6% to 13,323

VW 679 units or 13.9% to 5,574

Suzuki -1,515 units or -23.1% to 5,047

Isuzu 1,142 units or 48.2% to 3,513

Hyundai 122 units or 3.9% to 3,258

Ford -3.4%

GMW 6.2%

Chery 3.4%

Mahindra 14.2% to 2,280

Jetour 5.7%

Kia -5.7%

BMW 351 units or 28.4% to 1,588

Nissan 283 units or 23.5% to 1,487

Omoda/Jaecoo 10.5%

Renault -1.4%

4

1,378

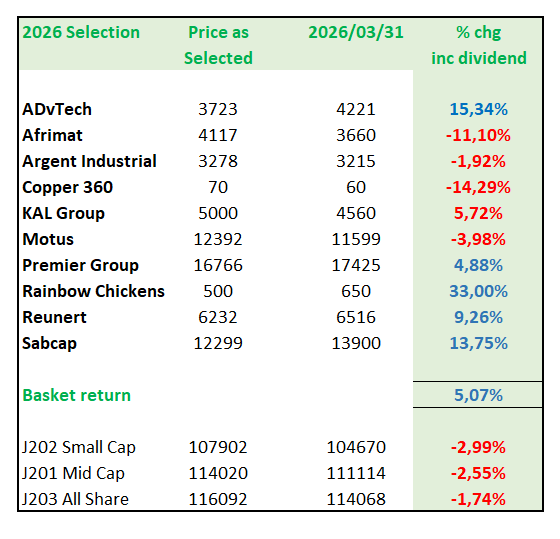

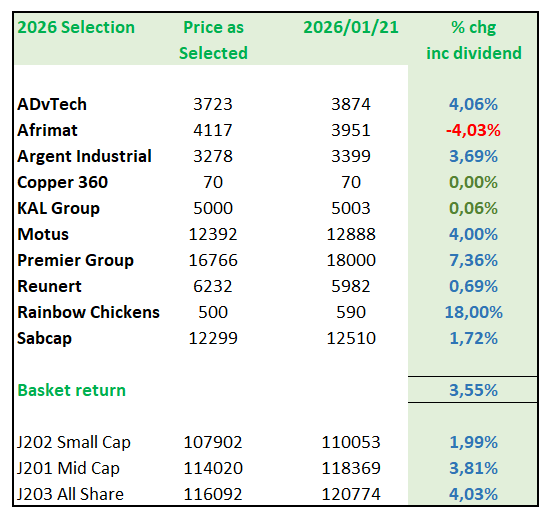

End of month 3 (Q1) of @smalltalkdaily Top Stocks of 2026 and as it has done from week 1, its continuing to outperform my J201 and J202 JSE Small and Mid Cap benchmark Indices. But I have 9 months to go yet

To date, from point of selection Top Stocks 5.07%

ALSI -1.74%

Mid Cap Index -2.55%

Small Cap Index -2.99%

March was a BRUTAL month for the market due to #TrumpWar #IranWar with my portfolio growth declining from February's 9.97% to 5.07%

However, on the month the ALSI was -11.2%, The Mid Cap Index -12.3% and the Small Cap Index -8.7% from the February month end close

In the Top Stocks, the only good performer in the March was $JSEADH ADvTech 2.9% and the worst performing stocks were $JSECPR Copper 360 -24.0%, $JSEMTH Motus -13.9% and $JSERBO Rainbow Chickens -10.3%

Still happy to own all the stock until the end of 2026, not that I can change the selection anyway given my self-imposed competition rules

1

2

10

1,244

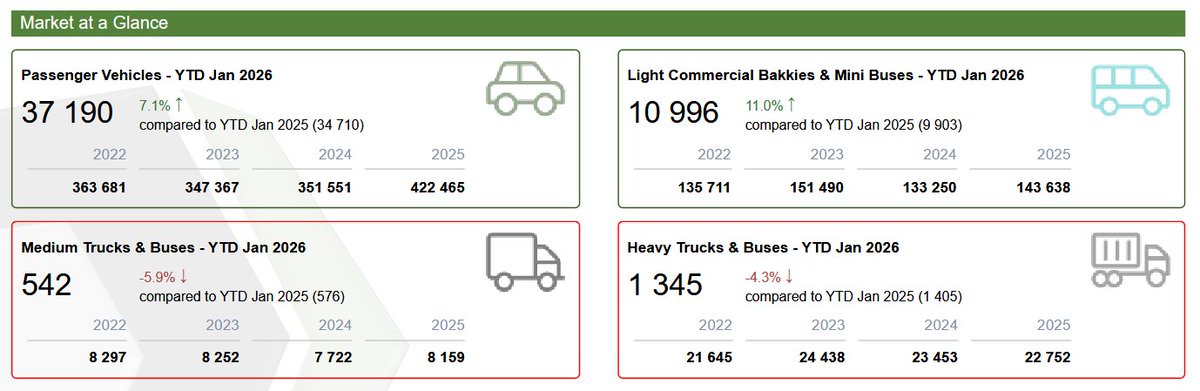

The January vehicle sales stats were released for January 2026 by The Nationals Association of Automotive Manufacturers South Africa

I break down the data points

In January NEW passenger car sales rose 7.1% to 37,190 units

Car rental sales to the sector were 13.3% of all new passenger vehicle sales c.4,497 units

Sales of bakkies and light commercial vehicles 11.0% in the month to 10,996 units

@Suzuki_ZA regained its N0.2 sales spot in January 2026 as it had been a consistent No.2, but in December 2025, @VW regained its N0.2 but slipped again into January 2026

Suzuki sales December 2025 to January 2026 rose 29% to 6,410 units (I'd wager many went into car rental as $JSECMH has the rights to the Suzuki OEM and many of it First Car Rental fleet is Suzuki)

VW fell -4.8% month-on-month to 4,774 units

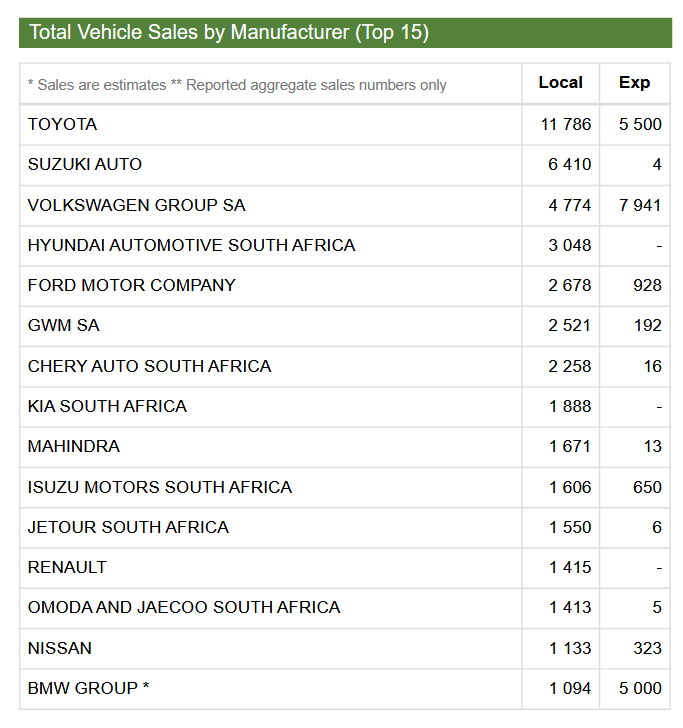

Looking on the Top 15 OEM brands change in sales from December 2025 data to January 2026 sales data

The Chinese & Indian imports in January 2026 continue to sell well

Toyota -8.9%

Suzuki 29.2% $JSECMH main importer

VW -4.8%

Hyundai -0.6% $JSEMTH main importer

Ford -10.3%

GWM 2.8%

Chery 0.4%

Kia 25.2% $JSEMTH main importer

Mahindra 35.4%

Isuzu -15.7%

Jetour 13.1%

Renault 8.5% $JSEMTH main importer

Omoda & Jaecoo 7.3%

Nissan 12.1%

BMW 29.8%

4

2

6

2,024

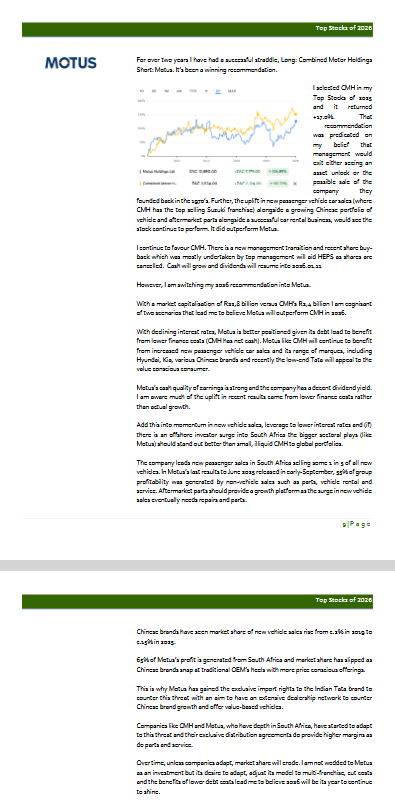

New 52-week high for $JSEMTH Motus at R132.99 but intra-day has been higher AND a record ever share price having smashed through the ceiling

I selected #MTH in my Top Stocks of 2026 and since selection its 7.32%

I anticipated there was greater upside and leverage benefit from motor retail sector trends and lower interest rate (benefits to #MTH but lower interest earned for $JSCMH) and I flipped by 2 year straddle LONG: #CMH SHORT: #MTH

That switch recommendation has been the correct call year-to-date with #MTH outperforming #CMH

My #MTH initial target price from selection is R155.00

1

11

1,488

Having discussed this since its selection, I provide a link to the entire report as well as a snap review of Top Stocks of 2025 performance

@smalltalkdaily Top Stocks of 2026

drive.google.com/file/d/1XVh…

If you want to listen to the entire narrative then listen into the webinar I undertook for @RandSwiss last week

youtube.com/watch?v=aNwNQP2B…

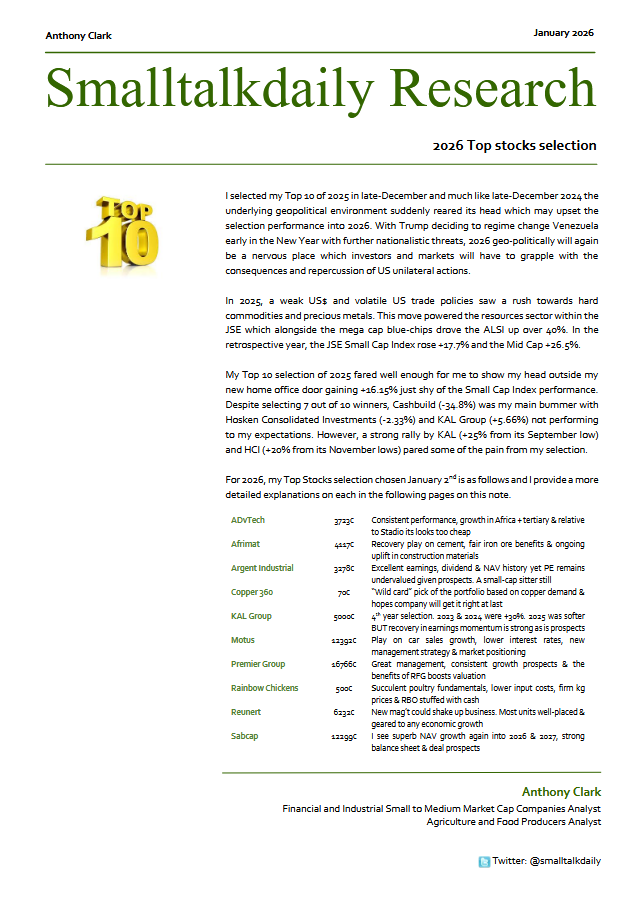

In the first few weeks of the selection its doing ok with $JSERBO Rainbow Chickens, $JSEADH AdvTech and $JSEMTH Motus faring best with $JSEAFT Afrimat the laggard (my premise on #AFT was a 2026 recovery play and still is)...

My total, balls to the wall, casino "wild card" is $JSECPR Copper 360

Still happy to own all 10 stocks for all of 2026

4

10

48

4,227

Recorded the second part of my Top Stocks of 2026 narrative with an interview with Classic Business @MichaelJAvery Michael Avery for @FineMusicRadio 101.3

It will air around 6.30pm tonight Monday 19th January

$JSEKAL KAL Group

$JSEMTH Motus

$JSEPMR Premier Group

$JSERBO Rainbow Chickens

$JSERLO Reunert

$JSESBP Sabvest Capital

3

4

19

2,250

4 Nov 2025

$JSEMTH - Finally cleared the seller around R106,5. Now likely to move up - time to add IMO.

2

1,378

30 Sep 2025

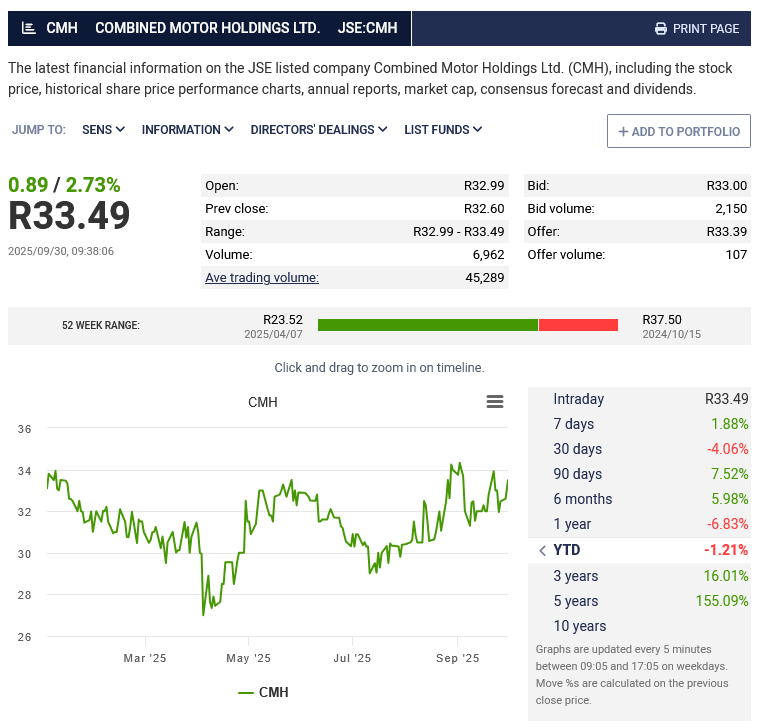

Solid H1 2025 trading update from motor retailer and car rental business $JSECMH Combined Motor Holdings

HEPS expected to increase by 20% to 25% to a range of 215.2 cents per share to 224.2 cents per share

Their affordable brands of Suzuki and Foton have gained solid market share in new vehicle sales

H2 should see he First Car Rental side kick-in to results

I also believe their cash hoard - R954 million - has also grown in the six months. Could this (perhaps) see a special dividend as no small-cap company needs R1bn cash on its balance sheet

Cash - at last results was worth R12.75 a share

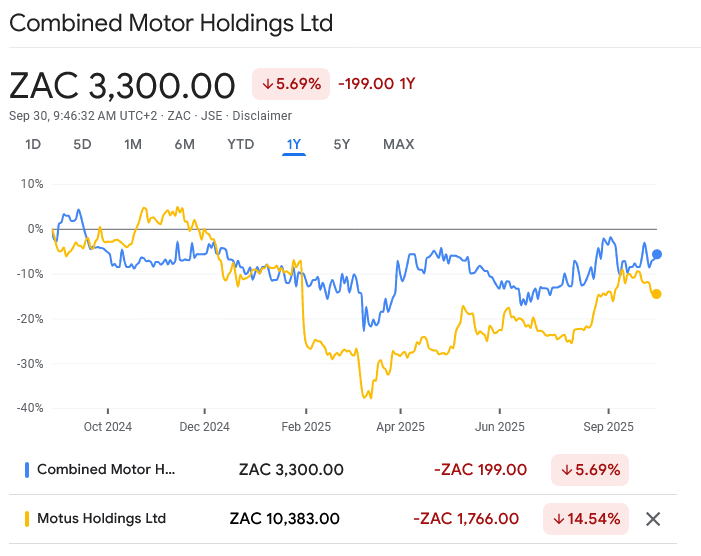

#CMH is trading at R33.49 year-to-date-1.21% but has still outperformed rival $JSEMTH Motus

I've has a long #CMH short #MTH as a straddle for the past 2 years and its been the right call

CMH Trading statement for the six months ended 31 August 2025 bit.ly/3IKHfQt

2

3

10

2,803

24 Apr 2025

Motus $JSEMTH raised to Overweight at ABSA Securities; target price R103 (implied upside of 24%).

Share price has fallen >30% from its peak in December. Market uncertainty is there but sell-side seems unphased.

Any one have this one in the portfolio or on the watchlist?

4

11

972

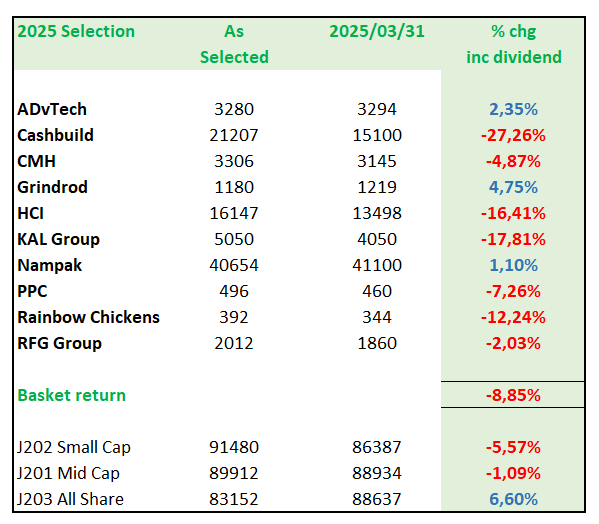

31 Mar 2025

Update on Month 3 of the @smalltalkdaily Top Stocks of 2024 as quarter one comes to a brutal close for what was an ugly March month

The selection was -8.85% year-to-date versus -1.09% for the JSE Mid Cap and -6.60% for the Small Cap Index. All the action again is in the gold sector and the ALSI where it was ahead 6.60% from point of portfolio selection

I said in my early-January report narrative, give the economy and Trump unertainty, it would be an ugly period and far more difficult to make money

Hindslight is a wonderful thing. I had $JSEBLU Blue Label Telecoms and $JSESBP Sabcap on the initial selection list but left them off. Ce la vie

The month's laggards

In the March month, there was a hefty sell-off in $JSECSB Cashbuild (-16.6%) which was the worst stock in the list

$JSERBO Rainbow Chickens slid -10.4% having recovered from much lower levels. Despite solid H1 results & prospects for H2, there was a slam in the stock on rumours of some corporate activity

$JSEKAL KAL Group fell -9.0% and continues to be weak since the February 6th AGM amid market concerns over growth plans

The month's winners

$JSEPPC PPC Group sharply recovered after a period of excessive weakness. The #PPC Capital Markets Day Riebeek site visit saw the stock surge 18.0%

$JSEADH AdvTech has solid YE2024 results with a positive outlook for ongoing growth in schools and tertiary with a big growth focus on Africa. @ADH was 3.7% in March

$JSECMH Combined Motor Holdings was a modest 1.5% and my straddle of LONG #CMH and SHORT $JSEMTH Motus continues to work as it has for two years. As a February year end and results and the usual fat dividend, I remain confident on its prospects

As always this is a 12-month cast in stone, I can't change anything selection and despite some horror shows in performance #CSB, #KAL, #HCI all the underlying reasons I chose the stocks remains in force

1

9

1,504

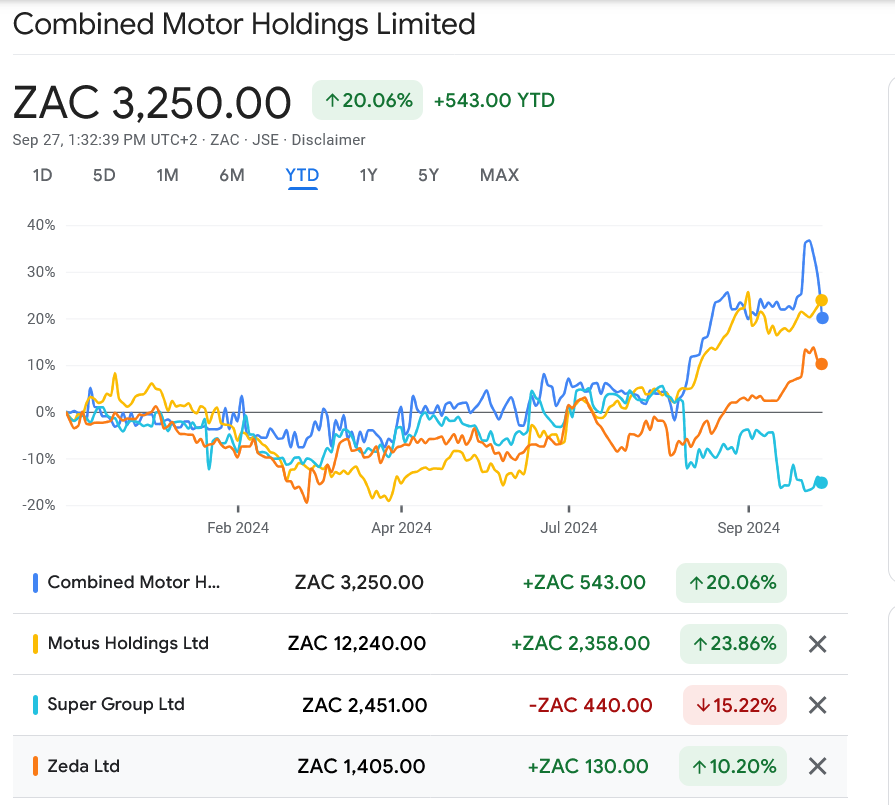

19 Dec 2024

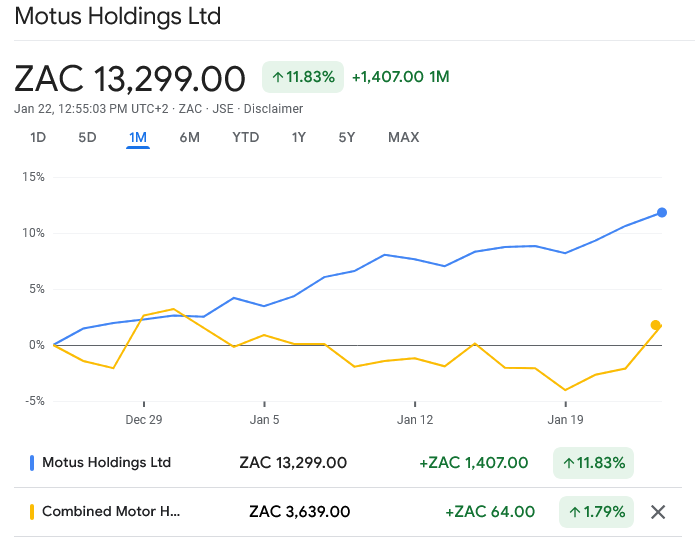

I've had a favoured sector recommendation on $JSECMH Combined Motor Holdings since March 2021 versus its largest sector comparative $JSEMTH Motus. It's been a pretty good call

Since October, #MTH has outperformed #CMH and with both stocks having results ahead December H1 (#MTH) and FebruaryYE25 (#CMH) a better look through should ensue

#MTH has a June reporting year end and #CMH February so timing is often something I consider

#MTH has a high debt load. #CMH carries fat net cash Thus ##MTH is a better beneficiary in a declining interest rate environment as South Africa is currently in

Both have marques in popular areas. #MTH Hyundai as example as master agents and #CMH has Suzuki. Affordable vehicles are doing well currently as as the Chinese brands

Both have car rental with #MTH having Europcar (c. 10% of its profit) and #CMH has First Car Rental which is c.50% of profit. In the current inbound tourism season - a bumper one is anticipated - #CMH should gain more skin

As & when new vehicle sales improve & bank lending loosens and consumers feel more confident both will be beneficiaries though I'm watching the Rand volatility, it is now the vehicle importers friend

Further, #MTH as a R22.1bn Mcap business versus #CMH R2.4bn, #MTH has greater liquidity which should draw in investors especially the big insto's and offshore funds

#CMH remains this desk's favoured play despite #MTH making a new 52-week intra-day high today

I like the businesses conservatism, owner-managers with big skin in the game & the net cash position which gives #CMH nimbleness

Currently #CMH is behind #MTH in the past two months, I anticipate it will play catch-up into Q1 2025

6

1,286

20 Nov 2024

$JSEMTH - Motus Holdings - Bullish breakout from symmetrical triangle targets 130 & 135.

2

1,042

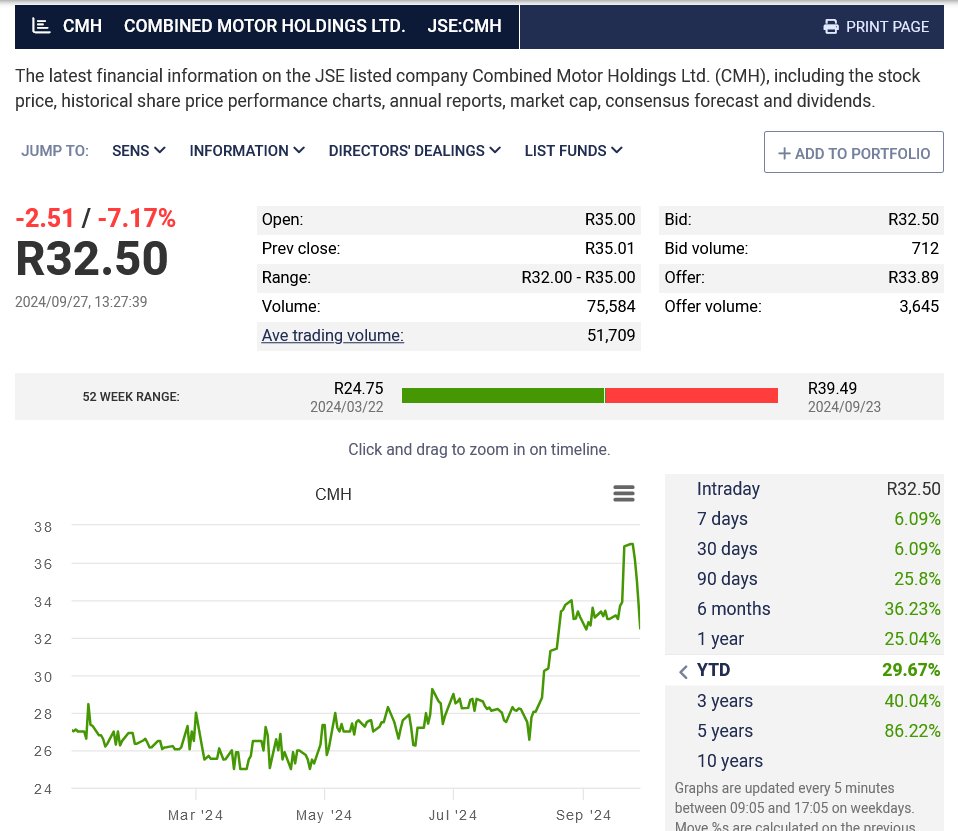

27 Sep 2024

Market reacting (or) as I believe over-reacting to the H1 2024 trading update from $JSECMH Combined Motor Holdings

#CMH -7.17% to 3250 cents in above average daily trade - not that daily trade is every huge @R1,7m per day

Company in a brief statement states its H1 guidance is for HEPS to be 25% t0 35% lower to range of 171 cents to 197.3 cents per share

#CMH much like $JSEMTH Motus & $JSESPG Super Group also issued weak updates on poor new vehicle sales data. How is market shocked at #CMH update?

Both #MTH & #SPGs hit on their trading updates but recovered as market woke up to prospects in changing market environment

#CMH, unlike #MTH & #SPG is stuffed with cash, the latter are filled with debt

#CMH, unlike #MTH & #SPG generated 50% of its group FY2024 profit from First Car Rental

First Car Rental is H2 biased for the summer tourist season, thus this current H1 period presumable saw softer demand due to the awful wet & cold Cape winter & tourist draw of Olympics?

With interest rates on the turn & #CMH having a range of affordable vehicle brands ... with Suzuki perennially a top 3 sales brand in South Africa alongside its Chinese brands, H2 for #CMH, like #MTH & #SPR should see improved demand

I doubt there is any institutional selling of #CMH on this trading update, as if they sell they will not be able to buy it back

I have owned #CMH for years, conservative business model, cash-stuffed balance sheet & majority owner-managers who have 50 years experience in the sector. I'm hanging in

1

8

1,947