એસેમ્બલ થયું છે એટલે #Jobwork કેહવાય.

Innovation કર્યું નથી.

93

Jobwork of @HPhobiaWatch to show Opposition Children

Have you shown any children background of Govt Minister?

@HPhobiaWatch Mera Earning pe Laat Q Maaru.

Bootlicking n Gaddari isko bolte hai India ke against

390

Jun 5

Jobwork in industry for those who may want to know: A big company engaged in manufacturing a large assembly needs various parts. It doesn’t make all the parts. In many cases, it purchases raw material, say steel rod, and gives to a small company that has say a CNC machine to turn the steel rod into a specified part. The small company doesn’t bill the part. It bills the price for turning rod into the part.

In case the small company gets the order for the entire part, where the scope for purchasing the steel is theirs, then they buy the steel, turn it into the specified part and bill for the part as a whole which will be pre-agreed.

So obviously, the revenue in the former is lot lesser than the latter.

Jun 5

That’s the point. One just can’t overstate just the revenue. If they have legit purchase and movement of gold, refined and sold again to various customers, that’s legit biz. Like oil refiners do.

If they do “jobwork” for a particular customer, then revenue is just the jobwork.

12

1,270

Jun 5

That’s the point. One just can’t overstate just the revenue. If they have legit purchase and movement of gold, refined and sold again to various customers, that’s legit biz. Like oil refiners do.

If they do “jobwork” for a particular customer, then revenue is just the jobwork.

If this is true, then raw material consumed must show gold purchases or stock movement (dore/bullion). Otherwise COGS won’t match revenue. If that’s missing, profits would look abnormally high and would clearly get flagged in audit and bank stock reconciliation.

1

4

2,323

May 31

🌀OTHER SME STOCKS H2FY26 FY26 RESULTS. 30th MAY 2025 - LIST1 (MACOBS, SAVY, MOTHER NUTRI, AMEENJI, MVK AGRO, KRISHCA, BABA FOODS, KENRIK, ARUNAYA etc)

Majority of companies have seen margin reduction in H2 affecting EPS growth and may cause potential consolidation of their stock price after results.

🍏MOTHER NUTRI FOODS: EXCELLENT NUMBERS. Rs.165 was at 24P/e. Now 18x.👍 Makes Peanutter Butter for Fast Food & Restaurant Chains. Did present Quality at time of IPO. Topline up from 90Cr to 124Cr in Fy26. PAT up from 6.6 to 11.6Cr. Improved margin at Op level.

🍏SAVY INFRA. EXCELLENT NUMBERS. Rs.160 was at 10.2P/e. Now 7.7x.👍 Company does pre construction site preparation works (earth work) at very large projects and Roads. Topline up from Rs.283Cr to Rs.644Cr in Fy26. Bottomline up from Rs.24Cr to Rs.43Cr. RE-RATE??

🫱KRISHCA STRAPPING: OVERALL FLAT even with big surge in topline due to severe 👎H2 margin reduction. Bottomline flat at 11.4Cr.

MVK AGRO – Company acquired related party companies (Sugar factories). After consolidation, Rs.505 is at 29P/E. Capex is ongoing. Since this is Sugar business, better be prepared for swings due to Govt control

🫱ARUNAYA ORGANICS - OVERALL FLAT. Rs.21 was at 9.5p/e Now 10.2x There is good topline growth from 83Cr to 105Cr. But due to margin trouble, Annual PAT is down to Rs.3.7Cr from 4.2Cr Makes textile Dyes and Pigments

👍MACOBS TECHNOLOGIES: JUST OKAY. Rs.220 was at 98 P/E. Now 75p/e Topline grew 78% from Rs.24Cr to Rs.43Cr. But due to operating margin 👎crash, Ebidta up by 18% only. At bottomline PAT is up from Rs.2.6 to 2.9Cr only at this chinese mens grooming product seller

👎AMEENJI RUBBER – OVERALL NEGATIVE. Topline grew from 94Cr to 124Cr in Fy26. But had a VERY POOR H2. Margin evaporated. Annual PAT down from Rs.7.7 to Rs.6.3Cr. Rs.158 was at 22P/e. Now 28x👎

🔴KENRIK INDUSTRIES –BAD. Has Slipped into Loss . Gold Jobwork. Raised ~9Cr in IPO in May 2025

🔴BABA FOODS – BAD. Has Slipped into LOSS after taking 33Cr from market out of which 24Cr was for expansion of Att Unit, company reports Rs.1.4Cr loss on 200Cr Sales. In Fy25 had reported 4.3Cr PAT on 100Cr sales. Topline stuck. Bottomline RED. Investor money processed into pocket through Atta!

May 30

🌀29 May 2026 OTHER SME RESULTS. LIST 2. FY26 ANNUAL RESULTS. H2FY26 RESULTS (Dev Labtech, Apollo Techno, ChatterBox, Asston)

👍DEV LABTECH – With company diluting equity with 1:1 bonus & then stock split, Rs.28.8 was at 119P/e. Now 14.3x. 👍

This is due to consolidation of UAE trading company’s finances, this year. On standalone basis, things were going down. UAE Subsidiary’s finances are not audited and hopefully there wont be any misrepresentation in future. (needs to be cautious)

🫱APOLLO TECHNO INDUSTRIES: OVERALL OKAY. New IPO. Need to give some time. Rs.97 was at 11.6 p/e. Now 12x. 🫱FY26 112Cr sales Vs 100Cr in Fy25. Annual PAT is slightly lower, with slight margin reduction over the last year. Market would expect big growth in Fy27, considering almost 50Cr IPO funding for WC and Loan repayment. (No capex) IPO was in Dec 2025 at Rs.130 at 15.5 p/e

🫱CHATTERBOX – Influencer Marketing. FLAT. 🫱 Rs.68.5 was at 9.9P/e. Now 10.7x. Annual Rev up from Rs.59 to Rs85Cr. Pat hardly moved from 8.85Cr to 9Cr. Lower margin this year compared to previous. Not able to take off. IPO was in OCT 2025 at Rs.115 at 18P/e.

🪳ASSTON PHARMA – NOT OKAY. Reported Operational loss and is on life support with other income . And this Small pharma marketing is getting 16P/e at Rs.73 (IPO was in July 2025 at Rs.123 at 21 P/e)

2

20

4,812

May 25

One of my uncle invested approx 6L each (total 30L) into strong fundamental companies which his friend recommended in 2014-15. My uncle was a normal guy doing EPC and Jobwork business, maybe earning 20LPA back then.

Today his business has gone to zero but his portfolio is upwards of 15cr. He has barely made any trades and holds companies for 4-5 years as long as his friend told him to. His friend's networth is now 150-200cr easily.

Looking back at some of the companies, debt free, 30-40% ROE and 30% growth were available for 8-10PE for multiple quarters.

1

4

76

13,311

My xtian Tamil boss who is residing in France and who hasn't paid me 10000 inr for my jobwork has spent nearly 1 lakh inr to come to India for Vijay's Cm ceremony. Imagine the missionary mafia behind this tharkuri.

5

81

233

4,129

Apr 30

Actually the company is in very narrow segment. Simply not possible to scale since there are so many EPC contractors who work with engineering consultants who in turn have their own favorite subsystem suppliers. Also it was actually doing jobwork fabrication by getting flow meters, valves and filters from EPC contractor to fabricate skids

It has to diversify into entire process piping ..full fledged like LAKSHYA did.

1

3

663

Bank Job Extreme Work Pressure..

He Quit 17 Lakh Bank Job ....

#Bank

#Job

#BankWork

#Jobwork

#BankIndia

5

2,223

Shalini's husband is in pharma business, she must be doing jobwork for them,

2

37

Feb 16

Jobwork for stitching.

Sizes will update within afternoon😁

1

2

104

Diamond industry surat use diff software due to jobwork tracking

Tiles industry morbi use diff software

ProfitNx

Medical stockist uses 1 type of software for easy entries

Yes it may happen local softwares are more popular bcz they built on specific requirement

1

2

76

Yes I still remember you did a twitter live with CDMO ko Jobwork bolne wale Chote Saab k saath when Laurus posted pathetic result and he was like Maine Bola tha.. Shouting anything about management and business profile and about Sajal sir. He is unseen now. Thanks to Sajal Sir🙏

2

7

241

8 Dec 2025

In Indian garment factories, a "job worker" specializes in specific tasks like stitching or embroidery, taking on outsourced work to help scale production without heavy investment. #GarmentIndustry #JobWork #IndiaApparel #TextileIndia #ProductionTips

1

3

91

27 Nov 2025

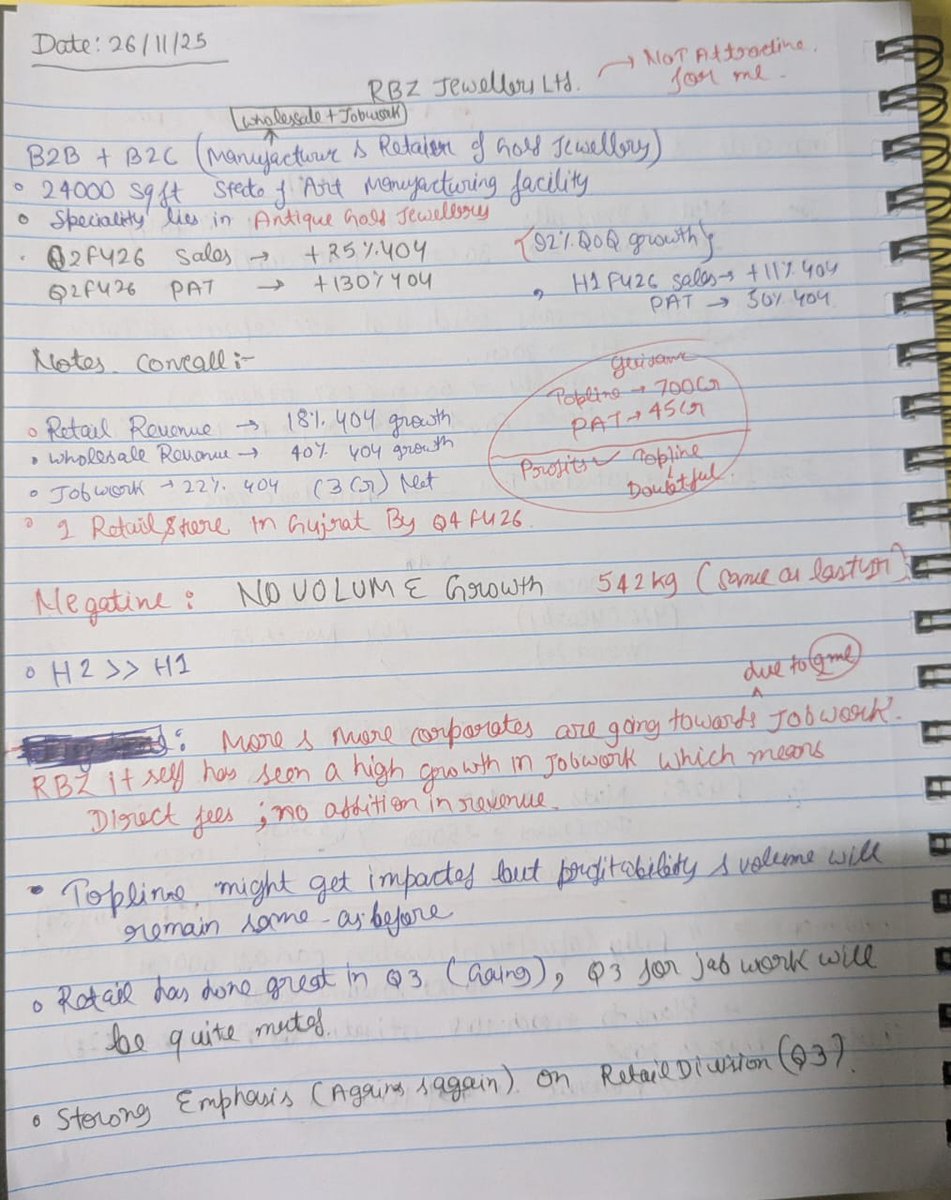

RBZ JEWELLERS Ltd. Q2FY26 REVIEW : STILL A BAD ONE FOR ME

RBZ is a B2B Jewelerry Manufacturer Retailer

Operates One store in Ahemdabad region. One more store to get operational in Q4. Planning to reac 4 stores count soon.

This business still remains an unattractive deal for me.

Sales grew b 25% YoY But There was NO VOLUME GROWTH.

Profitability improved due to increase in jobwork revenue.

Management is bullish for Retail segment revenue in Q3.

They might miss on topline guidance 700 CR But they are confident to achive pat guidance.

Still this deal stays a bad one for me due to better opportunity in peers group.

3

1

15

1,598

20 Nov 2025

Absolutely point taken. An forensic investigation will reveal how professionally the CA Audit firm did their jobwork, reportings.

The setting up of shell companies ain't feasible without an intellect CA Brain atleast to swindle millions.

Won't be surprised if CA firm is islamic..

1

25

15 Nov 2025

One of the biggest perils of the younger generation today apart from mindless scrolling is alcohol addiction. Received sad news of the death of an enterprising young entrepreneur who rose from the ranks of an operator. I had met the boy for the first time about 15 years ago. Had started his career at the age of 16 and had become a good cnc programmer by 21. Boy knew both cnc turning and cnc milling well and probably one of the few guys i have met who never saw the clock when at work. He would go home only when his target was finished.

Fittingly for his dedication, he grew rather well. Salary went from 18k a month to 80k a month in 15 years. Got married, had 2 daughters. To fuel his dreams, he took on debt from friends and even put up his own machine shop. Was doing well. I would give him occasional jobwork too.

But along the way fell into wrong company, bad movie influences and began drinking every evening. Some friends called him for drinks past 10 pm in the night when he was about to sleep. Man couldn’t resist and went drinking. Got too drunk, on the way home lost awareness of bike accelerator, jumped a hump and banged into a wall. Dead on spot. :(

a brilliant mind, committed hard worker and ethical man, gone in a flash! Only alcohol to blame. I hope movie makers and actors realise the influence they have on impressionable minds. Fans imitate their acts without realising its all just an act.

7

12

107

6,451

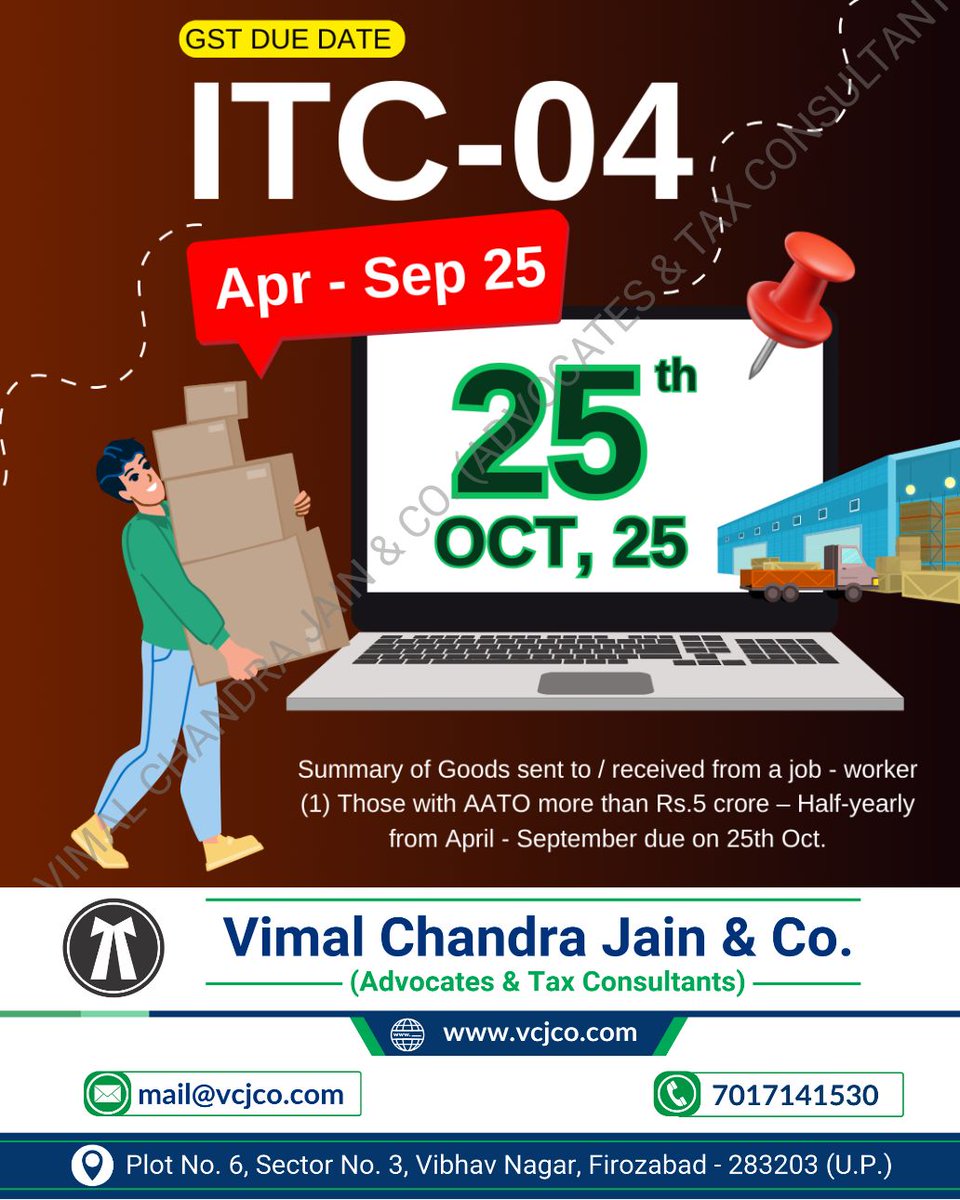

25 Oct 2025

ITC-04 Due Date Today !

#ITC04 #JobWork #goods #ITC #mathura #vrindavan #jalesar #kotla #dholpura #bharatpur #fariha #jasrana #sirsaganj #etah #auraiya #etawah #kanpur #tundla #vcjco #firozabad #agra #shikohabad #itr #incometaxreturn #refund #gst #gstr #gstregistration #tax #taxation

2

682

3 Oct 2025

❓ANY DARK HORSES AMONG THE SME CROWD OF SEPTEMBER 2025?

In the Sept 2025 SME rush, there were some good businesses, some that have flared up and couple of stocks that may do well in future.

💠GOOD BUSINESSES:

ANONDITA, CURRENT INFRA, GOEL CONSTRUCTION, KARBONSTEEL, TAURIAN, AIRFLOA, LT ELEVATOR, JD CABLES, PRIME CABLES, CHATTERBOX etc (KarbonSteel is going down currently)

💠 There were some which have flared up:

TECHD – Average potential being a service provider but presence of VK driving it

VASHISHTHA FASHION – Tiny eq of just 23,5L shares in total! The moment operators get out, there wont be any escape route👎

JAI AMBE – The IPO Valuation was high 25x. But stock has taken off. Most probably there in big potential in expanding supermarket business in Gujarat 👍

💠And feel these have DARK HORSE characteristics (These may get beaten down but in future may turn around. To only observe for change in price pattern, overtime)

AMEENJI RUBBER – Capex for New Product: Industrial Conveyor Belt (May be it will list and correct downwards initially)

SNEHAA ORGANICS – ONLY IF it succeeds in shifting from jobwork to direct manufacture and sale of solvents

💠There are few which can go either way!. BharatRohan, True Colors, Ecoline, Matrix Geo, JustO Real etc

There are many more to be listed in OCTOBER. Will do this exercise again in November First Week.

13

8

88

23,025